10 outstanding financial advisors provide valuable … outstanding financial advisors provide...

TRANSCRIPT

RETIREMENT PLANNING

Compiled and Edited by Sydney LeBlanc & Lyn Fisher

for the Savvy Investor

10 Outstanding Financial Advisors Provide Valuable Insight on ....

Specia

l Cha

pter E

xcerp

t by S

avan

t Cap

ital M

anag

emen

t, Inc

.

Savan

t’s To

p 10 List

for a

Happy a

nd Succes

sful R

etirem

ent

RETIREMENT PLANNING for the Savvy Investor

Compiled and Edited by:Sydney LeBlanc and Lyn Fisher

Foreword

The following pages are a single chapter excerpt from Retirement Planning for the Savvy Investor, by Sydney LeBlanc and Lyn Fisher. The book is a compilation of

chapters contributed by 10 professionals and wealth management teams in the financial services industry whom the authors chose, based on their combined 50+ years of journalistic experience, as the “best and brightest” on the topic of retirement planning.

Industry experts suggest there are three major areas retirees should focus on when entering the “golden years,” — financial planning, maintaining good health, and keeping a strong social network. It is important to have all three elements in place to be successful in aging. The purpose of the book is to expand on and educate investors on these topics, to ensure they enjoy a success-ful retirement.

We are pleased the authors chose to include information shared by Team Savant in this outstanding book. When compiling our chapter, each member of our team shared, what they considered to be, the most important things you should know about retirement planning.

We hope you enjoy reading, and can incorporate some of the ideas included in Savant’s Top 10 List: Strategies for a Happy and Suc-cessful Retirement.

SAGE Retirement Advice

Savant’s Top 10 List:Strategies for a Happy and

Successful Retirement

Before heading out on your next life’s adventure — retirement — you should have some basic requirements in place. First, you’ll need good physical and mental

health as well as healthy relationships with family and friends. Next, you certainly want to have enough money to pursue the retirement of your dreams, whatever it may be.

In order to make your retirement planning process enjoyable and our suggested strategies easy to review, we decided to create a Top 10 List. These ten strategies are based on a consensus of thoughts and ideas from our entire advisory team. It is also based on the collective experience we have gained from working with well over 2,000 clients during the last 25 years.

Before you review our strategies on the Top 10 List, here is a

1

1

Chapter

Retirement Planning for the Savvy Investor

2

statistic you might want to think about. It is rather sobering, but important to know:

The Employee Benefit Research Institute reports that nearly

half of boomers aged 56 to 62 are still at risk of not having

enough retirement income to pay for basic expenses and

uninsured health care costs.

Without a sizable nest egg, many retirees face the real possibility of outliving their retirement savings. Don’t be one of them.

If you are like many pre- or post-retirees, you are concerned — first and foremost — about the financial aspects of retire-ment planning. And, you should be. But what about retirement “living?” In other words, what would you like to do with the rest of your life? Financial issues aside, there’s a lot you can do to make retirement living a great time of life. We want to use the accumu-lated experience and wisdom that we have gained from working with successful retirees to explore all of these issues with you and be a part of helping you pursue the retirement of your dreams.

But first, let’s take a look at each of the points on the Top 10 List now, and following those we will elaborate on the most im-portant strategies as outlined and voted on by our entire Savant advisory team. (See page 3.)

Now that you’ve had the opportunity to review each point on our Top 10 List, here is more detail on the strategies we suggest for a “happy and successful retirement.”

Get a handle on your “financial means” as they ap-ply to your “needs.” Developing a sustainable budget and disciplined portfolio strategy will reduce stress and help assure lifelong financial independence.

1.

Chapter 1 — Savant’s Top 10 List

3

Savant’s Top 10 List for a Happy and Successful Retirement

Get a handle on your “financial means” as they apply to your “needs.” 1.

Developing a sustainable budget and disciplined portfolio strategy

will reduce stress and help assure lifelong financial independence.

Don’t take too much or too little risk. Too much risk may create excess 2.

worry and require you to reduce your lifestyle if markets go awry. Too little

risk means that inflation and taxes may cause you to run out of money.

Get your estate and house in order for your and your family’s peace 3.

of mind.

Ask and answer this question: What do I want to do in retirement? Con-4.

tinue to set and work toward new and exciting goals.

Don’t die with too much money. Often, it is better to spend your 5.

money now or to make gifts in a responsible manner while you are

still alive. Balance prudence and indulgence. When in doubt, just do

it. You are not getting any younger.

Spend your kids’ and grandkids’ inheritance — on them. Spoil your 6.

grandchildren. Pay for education. Take and fund great vacations

with your extended family members.

Be generous with your time, spirit, wisdom, and energy. This stage 7.

of life is not about coasting, but about giving back to your family, the

community and the next generation.

Take gratitude into account. Don’t forget to truly appreciate 8.

where you are in life. Slow down and recognize you are in a

great place and have much to be thankful for.

Focus on your most important relationships. Consider how retire-9.

ment will affect these relationships and balance your needs with the

needs of your family and friends.

Focus on developing a healthy lifestyle. Maintain your level of phys-10.

ical fitness. Exercise regularly. Finally, go to the gym.

Retirement Planning for the Savvy Investor

4

The reason this strategy is #1 on our list is simple: It encour-ages you to follow a disciplined plan and work with your wealth manager on achieving your retirement goals. But, without bogging you down with numerous calculations and figures, let’s just examine what we already know: A portion of your expenses in retirement will be met from Social Secu-rity and/or pensions. And your investment portfolio should provide the remainder of your income needs that will allow you to sustain your current lifestyle. The strategies your ad-visor uses will help create this stream of retirement income (think of it as your paycheck!). And, speaking of Social Se-curity, since these benefits will supplement your income, the age at which you claim your benefits is important.

Some other things you will want to consider are the terms and value of your life insurance coverage, any employee retirement benefits you may still have, methods to manage your taxes and to protect against inflation, and ways to get a handle on your expens-es, to name just a few. You will want to have the freedom to spend money on the things you enjoy (travel, family, etc.) when you want to; and, you may be able to spend extra money earlier on in retire-ment if you prepare a “retirement projection” with your advisor.

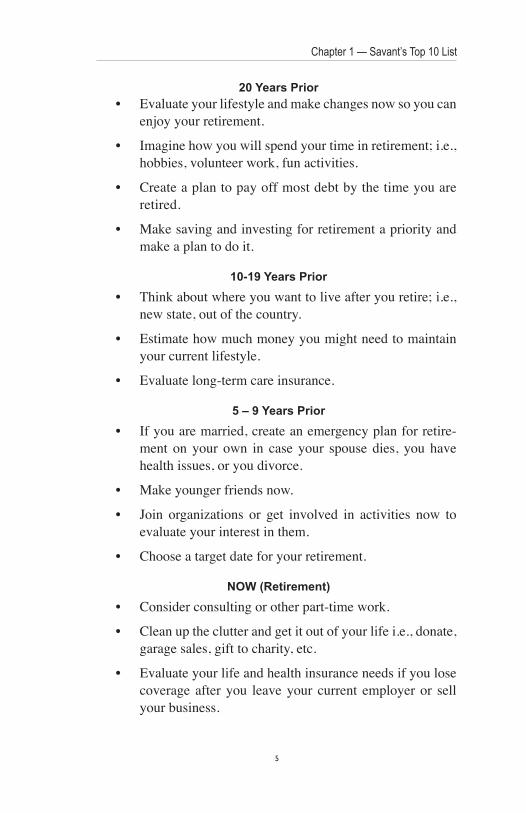

You can begin by asking your advisor for a checklist of things to consider at the various stages prior to retirement (depending upon your own time horizon, of course). This will motivate you and give you a comparison picture of your pre-retirement years versus your post-retirement years. Here are some good examples illustrating the kinds of things you may need on your retirement checklist. Get a notebook or journal and put these headings at the top — 20 Years Prior, 10-19 Years Prior, 5-9 Years Prior, NOW (Retirement). Start with the lists on the following page and add your own items.

Chapter 1 — Savant’s Top 10 List

5

20 Years PriorEvaluate your lifestyle and make changes now so you can • enjoy your retirement.

Imagine how you will spend your time in retirement; i.e., • hobbies, volunteer work, fun activities.

Create a plan to pay off most debt by the time you are • retired.

Make saving and investing for retirement a priority and • make a plan to do it.

10-19 Years Prior

Think about where you want to live after you retire; i.e., • new state, out of the country.

Estimate how much money you might need to maintain • your current lifestyle.

Evaluate long-term care insurance.•

5 – 9 Years Prior

If you are married, create an emergency plan for retire-• ment on your own in case your spouse dies, you have health issues, or you divorce.

Make younger friends now. •

Join organizations or get involved in activities now to • evaluate your interest in them.

Choose a target date for your retirement.•

NOW (Retirement)

Consider consulting or other part-time work. •

Clean up the clutter and get it out of your life i.e., donate, • garage sales, gift to charity, etc.

Evaluate your life and health insurance needs if you lose • coverage after you leave your current employer or sell your business.

Retirement Planning for the Savvy Investor

6

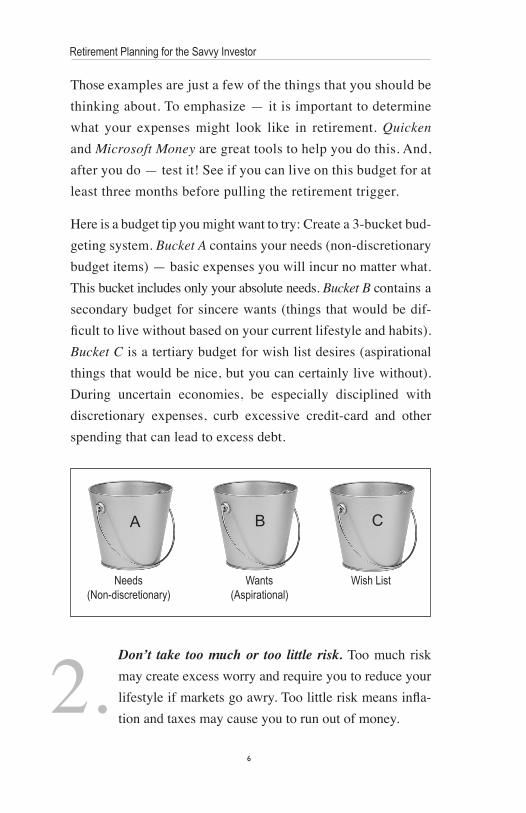

Those examples are just a few of the things that you should be thinking about. To emphasize — it is important to determine what your expenses might look like in retirement. Quicken and Microsoft Money are great tools to help you do this. And, after you do — test it! See if you can live on this budget for at least three months before pulling the retirement trigger.

Here is a budget tip you might want to try: Create a 3-bucket bud-geting system. Bucket A contains your needs (non-discretionary budget items) — basic expenses you will incur no matter what. This bucket includes only your absolute needs. Bucket B contains a secondary budget for sincere wants (things that would be dif-ficult to live without based on your current lifestyle and habits). Bucket C is a tertiary budget for wish list desires (aspirational things that would be nice, but you can certainly live without). During uncertain economies, be especially disciplined with discretionary expenses, curb excessive credit-card and other spending that can lead to excess debt.

Don’t take too much or too little risk. Too much risk may create excess worry and require you to reduce your lifestyle if markets go awry. Too little risk means infla-tion and taxes may cause you to run out of money.

A B C

Needs Wants Wish List (Non-discretionary) (Aspirational)

2.

Chapter 1 — Savant’s Top 10 List

7

We all know there is no reward without some risk. However, de-termining the level of risk you are comfortable with can be a balancing act. You and your advisor should review your portfo-lio allocation along with amount of risk you are willing to take, and this should be done well in advance of your retirement. Too much risk will keep you awake at night, create stress, and may adversely affect your lifestyle in retirement. If the stock market becomes volatile and an excessive portion of your portfolio is at risk, will it affect your lifestyle in retirement?

On the flip side, taking too little risk means that inflation may cause you to run out of money before you run out of steam. Be aware of the danger of being overconfident in your own invest-ing skill or discipline. Carefully choose your allocation, be dis-ciplined, and stick with it. Work with your advisor to assist you with these important strategies and invest with your risk toler-ance and return requirements in mind.

As an investor, you also need to understand the emotional dan-gers and the human nature factors of fear and greed. As the leg-endary investor Warren Buffett has said, “Be fearful when others are greedy, and be greedy when others are fearful.” Wise words for an investor to heed.

Get your estate and house in order for your and your fam-ily’s peace of mind. Peace of mind is one of the most vital aspects of having a “happy and successful retirement.”

Taking action now, before your retirement, and having a plan in place for handling your estate is mandatory. You may feel uneasy contemplating estate planning and the many details about death. But most pre- and post-retirees tell us quite candidly they want to die “right” — meaning the proper estate and gift planning strat-

3.

Retirement Planning for the Savvy Investor

8

gies are in order. This not only ensures a peaceful retirement, but also gives them comfort knowing they are leaving things “right” when they are gone. This includes ensuring your will is up-to-date and your desire to leave a legacy is in order. We discuss charitable giving and philanthropy in # 5 and # 7 of our Top 10 List in more detail, but this is also a meaningful element of your overall estate plan.

Everything needs to be in order, and that means “cleaning house.” Literally. Evaluate your housing arrangements. Get a dumpster. Clean out the garage. Clean out the basement. Ask yourself these important questions: Does the “family home” still make sense? Will moving cost me or save me money? Is buying a second home affordable or practical — will the kids actually use that Florida place when I/we are not there? Should I change my/our residency to a state with different income or estate tax rates? Your answers to these questions could mean major changes to your plan.

Ask and answer this question: What do I want to do in retirement? Continue to set and work toward new and exciting goals.

In the beginning of this chapter we asked what you would like to do with the rest of your life. We mentioned that — financial issues aside — there is a lot you can do to make retirement living the best time of your life. Here are three simple steps to a “happy and successful” retirement that you can post on your refrigerator door to help remind you and keep you motivated:

Have a plan for something to do (Activity) •

Have someone to do it with (Spouse or Friend)•

Have something to do it with (Money) •

4.

Chapter 1 — Savant’s Top 10 List

9

We know the question sounds simple: “What do I want to do in retirement?” You already know what you want to do: You want to TAKE IT EASY. That being said, after you have your “resting” period, you should be ready to do something in your retirement! Throughout our working lives, we dream of our retirement and all the things we want to do. Take an Alaskan cruise; spend a year in Paris; buy an RV and see the back roads of the U.S.; spend more time with children and grandchildren; do more volunteer work, or simply take up a new hobby. So when you ask yourself that question, you need to think of more than just what is the end destination (sitting at the pool every day and getting a great tan), but rather how are you going to stay active, remain productive, and continue to be engaged in the lives of those you love and in your community.

You will want to set new goals and work toward them, but feel free to adjust them. Goals and activities will keep your mind and body active and young. Keep learning and experiencing, i.e. take a class at your local community college. Research has shown that individuals who continue learning and creating new experiences are happier and healthier. After retiring, consider taking a couple of years before attempting any drastic steps or making major life-changing decisions.

You may feel like some retirees that often complain of being “tired,” and find yourself spending all your time in front of the TV as a couch potato, or on the internet writing on Facebook walls, and checking the market. While it may be entertaining, make sure to limit those activities to a few hours a day. On the other hand, you may be like some retirees who jump to doing something like updating their kitchen or bathroom with the hope that the feeling of being old and tired will go away. Instead, join

Retirement Planning for the Savvy Investor

10

a group with a focus on something you are passionate about. Attend a church group. Volunteer with your favorite charity. Or become a political activist, for example, and campaign for your local representatives to help change your community, city, or state for the betterment of all.

Don’t die with too much money. Often, it is better to spend your money now or to make gifts in a responsible manner while you are still alive. Balance prudence and indulgence. When in doubt, just do it. You are not getting any younger.

Don’t die with too much money. In other words, “die broke.” No, obviously we don’t mean you should live in poverty; but, in the words of author Stephen Pollan’s revolutionary 1997 best selling book “Die Broke,” he suggests in his 4-step process that we should, “Quit today, pay cash, don’t retire, and die broke.” Let us explain what he means by that. His process literally has become the ultimate blueprint for baby boomers (pre-retirees) who have already left the corporate world (quit today), rid them-selves of debt (pay cash), plan to remain active (don’t retire), and safely transfer their assets to their heirs while they are still around to enjoy the giving (die broke). This may be a good recipe that can help lead you to a “happy and successful retirement.” And it might also be a good plan that will lead to gift planning and other philanthropic activities — whether through financial gifting or volunteering your time.

Many times retirees leave too much to their children — especially when the children are too old to need it, appreciate it, or truly benefit from it. Instead, it is much better to make gifts in a responsible manner while you are still alive. That way you can enjoy seeing your children and grandchildren benefit from

5.

Chapter 1 — Savant’s Top 10 List

11

it. While gifting, you and your advisor can review tax strategies that will allow you to keep more for your family and favor-ite charities. Ask him or her about Donor-Advised Funds and Charitable Trusts for pre-funding your donations. You should also discuss ways to time gifting during higher tax years. Proper gift planning is so important for future taxation of your assets i.e., gifting highly appreciated securities to charitable funds. (Note: We could provide you with more sophisticated strat-egies here, but as we mentioned earlier, we don’t want to bog you down with too many specifics and details. We suggest you discuss them in-depth with your advisor.)

In our title of this particular Top 10 strategy we said, “You are not getting any younger.” Well, none of us like to be reminded of that fact. But, maybe it is time to really reflect on what that means. We suggest you “balance prudence and indulgence.” As we age, most of us become overly conservative. Worry less and enjoy life more. When in doubt, just do it! If you can do it now, you should. If there is something you have always wanted to do, do it now instead of waiting. If you wait, your health, family is-sues, lack of longevity, or other outside forces may prevent you from accomplishing what you have always wanted to do. Keep in mind that later on you may not have the health, energy, or ability to check off items from the “bucket list” (needs, wants, desires) in Point #1 of our Top 10 List. In fact, you might not even be alive. Just do it now!

Spend your kids’ and grandkids’ inheritance on them. Spoil your grandchildren. Pay for education. Take and fund great vacations with your extended family members.6.

Retirement Planning for the Savvy Investor

12

Is it time to consider spending your kids’ and grandkids’ inheri-tance on them now? According to news reports, the recent acro-nym for those who “Spend Kids’ Inheritance” on them is SKI-ers. Is this likely to happen more frequently? According to the Asso-ciated Press, more than 60% of baby boomers plan to give money to their children before they die — some by funding long-term family trips, paying for an advanced degree, helping them pur-chase a first home, or paying for their grandkids’ education (edu-cation is the gift that keeps on giving). In our experience, this is one of the best ways to spend your kids’ inheritance. Many want to have the pleasure of seeing their children or grandchildren en-joy their money while they are still around, consequently, leaving less to them when they are gone. Fewer than half the respondents in a recent inheritance survey conducted by the Federal Reserve believed it was “important to leave an estate to heirs.”

Spending their inheritance on them now seems to be an interest-ing trend. So, go ahead and spoil your grandchildren. Maybe, more than anything, this can bring joy to your life. But here is a caveat: First make sure your own retirement is fully funded. Don’t overdo gifts to kids or college funds for grandkids if such gifts are beyond your means. Take care of yourself first!

Be generous with your time, spirit, wisdom, and energy. This stage of life is not about coasting, but about giving back to your family, the community, and the next generation.

We touched on the strategy of “giving back” in Points #3 and #4 of this Top 10 List. We believe that now is the perfect time for you to give back to your immediate family, the community, and the next generation. Generously give your time, spirit, wisdom,

7.

Chapter 1 — Savant’s Top 10 List

13

and energy. Most times these efforts are more meaningful than giving money to charities. Effective philanthropy often means giving more money to fewer charities and getting personally involved to assure your contributions are well-stewarded. This is where your volunteerism steps in. Give your time to orga-nizations and causes for which you really have a passion, i.e., children’s organizations, the local food pantry, your local hos-pital or arts organization, a religious organization, political ad-vocacy, cures for disease, etc. You will find there are many op-portunities surfacing that can fill your day.

Just remember — this is not just about volunteering. This is about helping you decide what the best strategies are for a “happy and successful retirement.” Maybe you don’t want (or can’t afford) to retire right now. Instead of focusing on retiring, focus on becom-ing financially independent. And, while finishing your working career, explore creative opportunities to use your talents. Perhaps you could consult part-time, take on a lifestyle job, OR volunteer. For some individuals, the right answer is to keep working, but doing so in an area they enjoy and at a pace that allows them to enjoy life to its fullest. No one can really tell you what is best for you; it is a personal choice and one you can make once you have explored all of your options. At that point, you can make an informed, wise decision.

Take gratitude into account. Don’t forget to truly appre-ciate where you are in life. Slow down and recognize you are in a great place and have much to be thankful for.

Retirement is an ideal time to start a concentrated effort of showing an abundance of gratitude to others. The following is a list of areas in which to find reasons for gratitude in your life.

8.

Retirement Planning for the Savvy Investor

14

Family.• We become the individuals we are because of the influence of our families on our lives. Think for a moment and you will find something about your family — even if it meant you had been taught a difficult lesson — that inspired some measure of gratitude.

Friends.• Our friends bring us joy. Friends also challenge us to be the very best we can be. One of the most won-derful things about friendship is that our friends don’t have to be part of our lives; they choose to be part of our lives. Think about your friends and the richness they bring to your life. You are sure to find a few reasons to be grateful.

Opportunities.• Life brings us many opportunities. Most of us are quick to act on opportunities and make the most of them. But it is very easy to become so wrapped up, we forget to stop and be grateful for those oppor-tunities that, either, have come our way, or continue to come our way.

Challenges.• Life also brings each of us challenges. Whether we overcome challenges, cope with them, or find ourselves defeated by them, our lives and our per-sonalities are shaped by these challenges. Having grati-tude for the current challenges in life is extremely dif-ficult. It is easier, though, if we begin with challenges from our past. Think about the things you have learned and how you grew as a result. The dark cloud you are currently experiencing might have a silver lining if you just look for it.

Life.• Daily life can fill us with wonder and gratitude if we can learn to open ourselves to it. When we pay attention to the world around us and the people we en-counter, there are many things to be thankful for in each new day. Try living one day with your eyes and ears — and your heart — open to the world around you. By

Chapter 1 — Savant’s Top 10 List

15

cultivating gratitude for each day, you will get closer to reaching a “happy and successful retirement.”1

Remember: Try to truly appreciate where you are in life now. Slow down and recognize you are in a great place and have much to be thankful for. Say you are sorry and make sure you give the opportunity to others to do the same. Carrying grudges or leaving disputes unresolved hurts you more than anyone.

Focus on your most important relationships. Consider how retirement will affect these relationships and balance your needs with the needs of your family and friends.

First, consider how retirement will impact your relationship with your spouse. What will it feel like being home every day with your spouse? Next, consider how you will interact with (and the needs of) your family members after you retire — elderly par-ents, children, and grandchildren. Will it be enjoyable and are you looking forward to spending additional time with them? Or — will they be a financial and time-consuming drain? Now is the time to determine how you will balance your needs with those of your children or grandchildren.

In addition to interacting with your kids and grandkids, create new relationships with members of the younger generation. Teach a children’s class, offer to tend a neighbor’s child, volunteer at a local school or library. This keeps life interesting. Also, it assures you will still have friends throughout your life, even if you live to age 100! Mentor someone. You have gained a lifetime of experi-ence and wisdom; so, don’t let that merely fade away after you retire. Mentoring others is as much about you as it is about help-ing them learn from your experience. Share your wisdom.

1 Dr. Cynthia Barnett, author and retirement lifestyle expert

9.

Retirement Planning for the Savvy Investor

16

Focus on developing a healthy lifestyle. Maintain your level of physical fitness. Exercise regularly. Finally, go to the gym.

For those of you who are already retired — you can’t say you don’t have time to go to the gym now! If you are just beginning to plan your retirement, take heed. Start now to develop your healthy lifestyle, or improve upon a current program. Take a swim, or just walk around the block. Consider walking to the shopping center instead of taking the car, or simply choose to walk up or down the stairs instead of taking the escalator or elevator. Medical statistics have shown that it only takes 30 minutes of walking per day to lower the chances of heart disease by 30% to 50%.2 Do this and you will feel better all day long.

Exercise provides a greater benefit to older individuals than it does to the young. Studies undertaken by the University of Wash-ington found that the energy levels of people age 50+ increased by as much as 30% compared to only 2% in younger people when they participated in the same set of exercises.

By the way, do not feel guilty about taking naps during the day. You can afford to now, plus there is an added health benefit. A recent study by the Harvard School of Public Health in Boston found napping not only revs a person up for the rest of the day, improving brain function, but also helps protect the heart. In a study of nearly 24,000 people, it was found that those who regularly took afternoon naps were nearly 40% less likely to die from heart disease than non-nappers. Also, a previous Harvard study showed the brain is more active in people who nap than in those who do not. 2 American Heart AssociationRef: Credit Union National Association (PlanIt)

10.

Chapter 1 — Savant’s Top 10 List

17

Are You Ready to Start Planning?

According to current longevity statistics, you will likely live in retirement for a very long time. Your financial advisor, planner, or wealth manager can help you anticipate and plan for many retirement scenarios — some of which you might not have con-sidered. Issues such as those discussed in this chapter can be worked on, and solutions could be provided in order for you to live the retirement of your dreams. Not only can retirement in-come planning and asset protection strategies be employed, but financial management strategies also can be utilized to optimize your plan.

Now that you have had time to read our SAGERetirementAdvice chapter, we hope you enjoyed learning about each strat-egy on our Top 10 List, and that our team has given you sugges-tions for serious consideration. Hopefully, these strategies will help you close the gap to a “happy and successful retirement.” These are smart ways to start preparing for retirement and ac-tions you can take right now!

uuu

CONTRIBUTORSResearch Coordinator: Brian Conroy, CFP® Editors: Matthew D. Armstrong; Brent R. Brodeski, MBA, AIFA®, CPA, CFP®, CFA; Brian P. Conroy, CFP®; Thomas A. Muldowney, MSFS, CFP®, ChFC, CLU, CRC, CMP, AIF® Special Thanks: Savant Advisory Team for the development of “Savant’s Top 10 List: Strategies for a Happy and Successful Retirement.”

Retirement Planning for the Savvy Investor

18

Chapter 1 — Savant’s Top 10 List

19

ABOUT SAVANT CAPITAL MANAGEMENT

Savant Capital Management, Inc. is an independent, fee-only wealth management firm

headquartered in Rockford, Illinois. Since 1986, Savant has provided integrated invest-

ment management, financial planning, and family office services to financially established

individuals, trust funds, retirement plans, and non-profit organizations. Savant strives to

provide much-needed wisdom and focus in an era of information overload. We offer a

personalized, comprehensive, and integrated approach to clients’ financial needs and help

align your assets and decisions to work toward achieving your ideal future.

Savant’s goal is to provide insight, wisdom, and perspective to clients; to provide direction

and confidence regarding your financial decisions. Savant serves you in a manner that we

believe is fully transparent. This leads to greater peace of mind, simplicity, and clarity.

As a fee-only advisor, Savant does not receive benefits from brokerage services, com-

missions, or finder’s fees. In our opinion, this independence allows Savant to remain

impartial. Additionally, Savant does not sell products and thus offers objective fiduciary

advice and services that do not create conflicts of interest. We serve only you, our

client. To assure that Savant adheres to industry best practices, we became one of

the nation’s first investment advisors to attain CEFEX Fiduciary Certifications from the

Center for Fiduciary Excellence.

Savant is regularly recognized among the top wealth managers in the United States.

In March of 2008, Savant was named the top independent advisor in Chicagoland by

Chicago magazine. Recently, Savant was named by Barron’s magazine as one of the 100

best independent financial advisors in the United States. Inc. magazine named Savant

as the fastest growing Registered Investment Advisor in Illinois. Savant has also been

recognized as one of the nation’s top 100 financial advisors by Worth magazine each year

since 1997 (list discontinued in 2008). Since 2004, Savant has been selected by Medical

Economics magazine as one of the 150 best financial advisors for doctors in the nation. In

addition, Savant has regularly been included in other prestigious top advisor lists published

by Wealth Manager, Financial Advisor, Registered Representative, CPA Wealth Provider,

J. K. Lassers, and Family Wealth Alliance.

Savant Capital Management Inc is a Registered Investment Advisor. Please contact the Advisor to find out if they are qualified to provide investment advisory services in the state where you reside. There is no a guarantee that clients will experience a certain level of results if they engage the ad-visor’s services. Lists or rankings published by magazines and other sources are generally based exclusively on information prepared and submitted by the recognized advisor. Past performance is no guarantee of future results.

Retirement Planning for the Savvy Investor

20

Hope you enjoy and can use some of the ideas outlined in Savant’s Top 10 List for a Happy and Successful Retirement.

Savant Capital Management, Inc.866 489 0500

www.savantcapital.com