09 july 2021 1qfy22 results preview autos & transportation

TRANSCRIPT

09 July 2021 1QFY22 Results Preview

Autos & Transportation

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

Mixed recovery trends While auto demand will benefit from the expected pick-up in economic growth,

the pent-up demand has been low in the current unlock phase vis-à-vis last year

due to higher fuel prices (+40% YoY) and price hikes taken by OEMs. 2W

demand has been tepid while that of PVs is more resilient, given the relatively

better income profiles of car customers. We see limited room for EPS upgrades,

going ahead, due to (1) elevated growth expectations and (2) margin headwinds

on the back of firm commodity prices. Consequently, the auto index is expected

to perform in line with the broader market. We reiterate our preference for

stocks that have a diversified geographic presence - Bajaj Auto, Tata Motors

and Bharat Forge. We also have a BUY on Maruti amongst the domestic-centric

OEMs due to its product portfolio comprising alternate fuel variants (CNG and

upcoming hybrid models).

Pent-up demand is low in the current unlock phase: In the current unlock

phase, the pent-up demand is lukewarm (unlike last year) as customer

sentiment has been partially impacted by (1) higher fuel prices - petrol prices

are more than INR 100 (+40% YoY) in several states, which has resulted in

high running costs and (2) price hikes taken by the OEMs to offset rising

commodity prices. Further, demand in the rural segment has not been as

resilient as that in the previous year, with 2W OEMs reporting flattish sales in

Jun-21. However, demand for PVs is holding up (as the higher income

consumers have been relatively less impacted by COVID). The progress of the

south-west monsoon will be a key variable to determine the extent of

recovery.

Margin headwinds in 1QFY22: Commodity prices have remained firm, with

OEMs raising prices to partially offset the above. Further, the sudden outburst

of the COVID wave in Apr-May 2021 had resulted in temporary production

shutdowns, which will impact profitability this quarter.

Sector returns are converging with the broader market: The NIFTY Auto

index has performed in line with the broader market in 1QFY22 (+7% QoQ)

due to commodity cost inflation and moderating growth trends across 2Ws.

The sector returns have been normalising over the past six months due to

inflationary cost pressures/elevated valuations. We foresee limited scope for

EPS upgrades as growth rates are adequately factoring in the expected

recovery.

Key recommendations: We are downgrading Endurance Technologies to an

ADD. While the company will continue to outperform the industry due to its

increasing content per vehicle, the overall recovery in the 2W industry has

been tepid. We believe the current valuations of 30x forward PE are

adequately factoring in future growth prospects. We prefer stocks that have a

diverse business mix across geographies and reiterate our BUY rating on Bajaj

Auto, Tata Motors, and Bharat Forge. We also have a BUY on Maruti due to

its product portfolio comprising alternate fuels (CNG and upcoming hybrid

models). We prefer Subros amongst the domestic auto ancillaries.

Logistic/aviation: As the trial runs have started on the 650km stretch between

Palanpur (Gujarat) and Haryana, we believe that Gateway (BUY) and

CONCOR (ADD) will benefit from the shift towards the rail. We have a

REDUCE on Indigo as we believe its margins will be impacted by firming

crude prices.

RECO

CMP

(INR)

*

TP

(INR)

Ashok

Leyland REDUCE 124 115

Bajaj Auto BUY 4,048 4,860

Eicher REDUCE 2,715 2,500

Escorts ADD 1,204 1,325

Hero Moto ADD 2,914 3,320

Mahindra ADD 777 900

Maruti BUY 7,451 8,680

Tata Motors BUY 317 380

Amara Raja ADD 739 840

Bharat Forge BUY 807 940

Endurance ADD 1,633 1,660

Gulf Oil BUY 687 850

Subros BUY 322 410

Sundram

Fasteners ADD 793 810

IndiGo REDUCE 1,809 1,725

CONCOR ADD 693 740

Gateway

Distriparks BUY 290 360

*CMP as of 7th Jul-21

NIFTY Auto index

Source: Bloomberg, HSIE Research;

indexes rebased to 100

Aditya Makharia

+91-22-6171-7316

Mansi Lall

+91-22-6171-7357

80

100

120

140

160

180

Ap

r-20

May

-20

Jun

-20

Jul-

20A

ug

-20

Sep

-20

Oct

-20

No

v-2

0D

ec-2

0Ja

n-2

1F

eb-2

1M

ar-2

1A

pr-

21M

ay-2

1Ju

n-2

1Ju

l-21

NIFTY NIFTY AUTO

Page | 2

Autos & Transportation: 1QFY22E Results Preview

1QFY22E earnings preview

Volume (in units '000) NET SALES (INR bn) EBITDA margin (%) APAT (INR bn) Adj. EPS (INR)

1Q

FY22E

QoQ

(%)

YoY

(%)

1Q

FY22E

QoQ

(%)

YoY

(%)

1Q

FY22E

QoQ

(bps)

YoY

(bps)

1Q

FY22E

QoQ

(%)

YoY

(%)

1Q

FY22E

4Q

FY21

1Q

FY21

AUTOS

Ashok

Leyland 18 (59) 372 30.0 (57) 361 6.3 (133) NA (0.1) NA NA (0.0) 0.7 (1.3)

Bajaj Auto 1,006 (14) 127 75.4 (12) 145 17.4 (33) 413 11.9 (10) 126 41.3 46.0 18.2

Eicher 124 (40) 116 17.4 (41) 113 20.5 (108) 2,004 2.8 (46) NA 10.4 19.3 (2.0)

Escorts 26 (20) 43 17.4 (21) 64 15.2 (39) 393 2.1 (24) 124 20.5 26.9 9.1

Hero Moto 1,024 (35) 82 55.3 (36) 86 13.5 (44) 986 5.6 (35) 820 28.2 43.3 3.1

Mahindra 187 (8) 96 119.5 (10) 114 14.0 (70) 375 8.7 (13) 2,146 7.3 8.4 0.3

Maruti 354 (28) 362 173.3 (28) 322 9.0 71 NA 13.9 19 (658) 46.1 38.6 (8.3)

Tata Motors 115 (40) 358 131.8 (34) 390 6.9 (179) NA (5.7) NA NA (1.6) 0.9 (5.9)

Aggregate 2,853 (27) 122 620.1 (29) 196 11.3 (14) 1,459 39.4 (31) (288)

Source: Company, HSIE Research

NET SALES (INR mn) EBITDA margin (%) APAT (INR mn) Adj. EPS (INR)

1QF

Y22E QoQ (%) YoY (%)

1QF

Y22E

QoQ

(bps)

YoY

(bps)

1Q

FY22E QoQ (%) YoY (%)

1Q

FY22E

4Q

FY21

1Q

FY21

AUTO ANCS

Amara Raja 17,266 (18) 50 14.5 (55) 126 1,713 (10) 173 10.0 11.1 3.7

Bharat Forge 8,354 (36) 96 26.5 (97) NA 1,110 (46) NA 2.4 4.4 (1.2)

Endurance 12,062 (43) 100 15.7 15 864 685 (63) NA 4.9 13.3 (1.8)

Gulf Oil 4,222 (18) 75 14.7 (39) 416 492 (18) 186 9.9 12.0 3.5

Subros 5,076 (23) 588 9.5 (18) NA 164 (36) NA 2.5 3.9 (3.7)

Sundram Fasteners 5,971 (53) 60 18.0 (60) 1,394 615 (56) NA 2.9 6.7 (1.3)

Source: Company, HSIE Research

NET SALES (INR mn) EBITDA margin (%) APAT (INR mn) Adj. EPS (INR)

1QFY22E QoQ (%) YoY (%) 1QFY22E QoQ

(bps)

YoY

(bps) 1QFY22E QoQ (%) YoY (%) 1QFY22E 4QFY21 1QFY21

TRANSPORTATION

CONCOR 17,520 (10) 47 18.0 825 463 1,428 83 132 2.3 1.3 1.0

Gateway Distriparks 3,356 (4) 33 26.5 (70) (114) 343 (26) 208 3.2 4.2 1.0

Interglobe Aviation 47,152 (20) 525 14.0 350 NA (7,890) NA NA (20.5) (22.7) (74.2)

Source: Company, HSIE Research

Page | 3

Autos & Transportation: 1QFY22E Results Preview

Change in estimates and target price

Coverage

companies

Old

Rating

New

Rating

Old

TP

(INR)

New

TP ^

(INR)

Old target

multiple

New target

multiple

Old EPS (INR) New EPS (INR) % change

FY

22E

FY

23E

FY

24E

FY

22E

FY

23E

FY

24E

FY

22E

FY

23E

FY

24E

Ashok

Leyland REDUCE REDUCE 115 115

11x

EV/EBITDA

11x

EV/EBITDA 3.0 5.6 7.2 3.0 5.6 7.2 - - -

Bajaj Auto BUY BUY 4,360 4,860 20x 20x 186.9 217.6 - 188.2 232.6 274.0 0.7 6.9 -

Eicher REDUCE REDUCE 2,400 2,500

23x core

business

16x VECV

23x core

business

16x VECV

82.3 109.5 - 82.3 109.5 125.9 - - -

Escorts ADD ADD 1,300 1,325 14x 14x 84.2 93.0 - 84.2 93.0 99.4 - - -

Hero

Motocorp ADD ADD 3,240 3,320 17.5x 17.5x 171.2 185.3 - 171.2 185.3 202.7 - - -

Mahindra ADD ADD 890 900 15x core

business

15x core

business 40.1 48.5 - 39.9 48.3 53.7 -0.5 -0.5 -

Maruti

Suzuki BUY BUY 7,750 8,680 27x 27x 219.5 287.4 - 220.9 299.7 386.2 0.6 4.3 -

Tata Motors BUY BUY 380 380

11x

EV/EBITDA

on core

business

11x

EV/EBITDA

on core

business

10.2 18.8 - 1.2 16.1 25.3 NA -14.2 -

Amara Raja ADD ADD 910 840 19x 19x 40.4 47.8 - 38.6 42.8 47.6 -4.4 -10.5 -

Bharat Forge BUY BUY 860 940 34.5x 35x 16.4 24.8 - 16.5 25.3 31.3 1.1 2.0 -

Endurance BUY ADD 1,600 1,660 30x 30x 45.7 53.4 - 45.7 53.4 61.5 - - -

Gulf Oil BUY BUY 840 850 19x 19x 40.8 44.0 - 40.8 44.0 47.4 - - -

Subros BUY BUY 410 410 22x 22x 12.7 17.4 22.8 12.7 17.4 22.8 - - -

Sundram

Fasteners ADD ADD 750 810 27.5x 28x 21.2 27.0 - 21.2 27.5 33.6 - 1.9 -

CONCOR ADD ADD 690 740 28x 28x 16.8 24.5 - 16.6 24.5 32.4 -1.1 0.1 -

Gateway

Distriparks BUY BUY 235 360

10x

EV/EBITDA

Rail business

14x

EV/EBITDA

Rail business

9.2 12.8 - 9.3 12.9 17.7 1.4 1.2 -

IndiGo REDUCE REDUCE 1,580 1,725 7x

EV/EBITDA

7x

EV/EBITDA -52.2 68.6 - -52.2 63.5 103.8 - -7.5 -

Source: Company, HSIE Research, ^Jun-23E TP

Page | 4

Autos & Transportation: 1QFY22E Results Preview

Peerset comparison

Mcap

(Rs bn)

CMP*

(Rs/sh) Reco

TP

(Rs)

Adj EPS (Rs/sh) P/E (x) RoE (%) EV/EBITDA (x)

FY

22E

FY

23E

FY

24E

FY

22E

FY

23E

FY

24E

FY

22E

FY

23E

FY

24E

FY

22E

FY

23E

FY

24E

AUTOS

Ashok Leyland 363 124 REDUCE 115 3.0 5.6 7.2 40.6 22.2 17.2 12.7 20.9 23.7 20.5 12.7 10.1

Bajaj Auto 1,171 4,048 BUY 4,860 188.2 232.6 274.0 21.5 17.4 14.8 21.4 25.6 28.9 16.7 13.7 11.5

Eicher 74 2,715 REDUCE 2,500 82.3 109.5 125.9 33.0 24.8 21.6 19.4 22.1 21.6 24.9 18.7 15.6

Escorts Ltd. 162 1,204 ADD 1,325 84.2 93.0 99.4 14.3 12.9 12.1 14.7 14.1 13.2 7.8 6.5 5.4

Hero Moto 582 2,914 ADD 3,320 171.2 185.3 202.7 17.0 15.7 14.4 21.9 21.9 22.1 11.1 9.8 8.7

Mahindra 926 777 ADD 900 39.9 48.3 53.7 19.5 16.1 14.5 13.1 14.2 14.0 11.4 9.5 8.0

Maruti 2,250 7,451 BUY 8,680 220.9 299.7 386.2 33.7 24.9 19.3 12.4 15.3 17.6 21.6 15.7 11.6

Tata Motors 1,141 317 BUY 380 1.2 16.1 25.3 NA 19.6 12.5 0.8 10.6 14.7 5.7 4.3 3.5

AUTO ANCS

Amara Raja 126 739 ADD 840 38.6 42.8 47.6 19.1 17.3 15.5 14.9 14.6 14.5 9.8 8.3 7.0

Bharat Forge 376 807 BUY 940 16.5 25.3 31.3 48.8 31.9 25.8 13.1 17.7 18.6 30.1 21.8 18.5

Endurance 230 1,633 ADD 1,660 45.7 53.4 61.5 35.7 30.6 26.5 17.4 17.5 17.3 18.2 15.4 13.1

Gulf Oil 34 687 BUY 850 40.8 44.0 47.4 16.9 15.6 14.5 22.2 21.4 20.7 10.1 8.7 7.4

Subros 21 322 BUY 410 12.7 17.4 22.8 25.4 18.5 14.1 10.0 12.4 14.4 9.6 7.4 5.7

Sundram

Fasteners 167 793 ADD 810 21.2 27.5 33.6 37.5 28.9 23.6 18.6 20.8 21.1 22.8 18.6 15.5

TRANSPORTA

TION

CONCOR 422 693 ADD 740 16.6 24.5 32.4 41.6 28.3 21.4 9.7 13.5 16.6 24.1 18.4 14.3

Gateway

Distriparks 32 290 BUY 360 9.3 12.9 17.7 31.1 22.5 16.3 7.9 10.6 13.8 12.2 10.3 8.2

Interglobe 696 1,809 REDUCE 1,725 (52.2) 63.5 103.8 NA 28.5 17.4 NA NA NA 20.1 8.1 5.7

Source: Company, HSIE Research, *CMP as of 7th Jul-21

Page | 5

Autos & Transportation: 1QFY22E Results Preview

1QFY22 Volume Summary

Volumes in units 1QFY21 4QFY21 1QFY22 % QoQ % YoY

Ashok Leyland 3,814 44,060 17,987 (59) 372

- MHCV 1,021 26,277 9,050 (66) 786

- LCV 2,793 17,783 8,937 (50) 220

Bajaj Auto 443,103 1,169,664 1,006,014 (14) 127

- 2W 399,929 1,047,632 899,305 (14) 125

- CV 43,174 122,032 106,709 (13) 147

Eicher 59,398 222,771 129,446 (42) 118

- 2W 57,269 204,604 123,640 (40) 116

- CV 2,129 18,167 5,806 (68) 173

Escorts 18,150 32,588 25,935 (20) 43

Hero Motocorp 563,268 1,568,242 1,024,489 (35) 82

Maruti 76,599 492,235 353,614 (28) 362

M&M 95,308 202,223 186,777 (8) 96

- Auto 29,651 108,329 86,848 (20) 193

- Tractors 65,657 93,894 99,929 6 52

Tata Motors* 23,805 182,824 107,786 (41) 353

- PV 14,571 83,857 64,386 (23) 342

- CV 9,234 98,967 43,400 (56) 370

TVS 266,903 927,579 657,758 (29) 146

- 2W 255,398 886,614 618,701 (30) 142

- 3W 11,505 40,965 39,057 (5) 239

Source: SIAM, Company, HSIE Research; *only domestic sales

Volume estimates

Company FY18 FY19 FY20 FY21 FY22E FY23E FY24E

Ashok Leyland Total volumes 174,851 197,366 125,250 100,728 125,459 149,737 171,439

% YoY 21 13 (37) (20) 25 19 14

Bajaj Auto Total volumes 4,006,788 5,018,712 4,615,212 3,972,914 4,363,141 4,801,954 5,320,276

% YoY 9 25 (8) (14) 10 10 11

Eicher RE Total volumes 820,493 823,828 696,052 612,060 757,468 885,442 997,075

% YoY 23 0 (16) (12) 24 17 13

Escorts Total volumes 80,405 96,412 86,017 106,741 109,267 116,558 122,682

% YoY 26 20 (11) 24 2 7 5

Hero Motocorp Total volumes 7,587,193 7,820,831 6,409,719 5,786,374 6,203,155 6,718,753 7,281,563

% YoY 14 3 (18) (10) 7 8 8

M&M Total volumes 868,132 938,546 779,809 706,771 780,696 865,464 951,865

% YoY 13 8 (17) (9) 10 11 10

Maruti Suzuki Total volumes 1,779,574 1,862,449 1,563,297 1,457,861 1,735,816 1,993,766 2,272,893

% YoY 13 5 (16) (7) 19 15 14

Tata Motors Total volumes 641,133 732,739 473,502 485,361 591,975 697,135 796,493

% YoY 17 14 (35) 3 22 18 14

Source: SIAM, Company, HSIE Research

Page | 6

Autos & Transportation: 1QFY22E Results Preview

Monthly volumes (in units)

Ashok Leyland: MHCV volumes to recover from

2HFY22 onwards

Bajaj Auto: Volume momentum sustaining due to

exports

Source: SIAM, Company, HSIE Research Source: SIAM, Company, HSIE Research

Royal Enfield: Volumes have moderated from the

earlier 65k+ levels

Hero Motocorp: Volume growth has moderated over the

past few months

Source: SIAM, Company, HSIE Research Source: SIAM, Company, HSIE Research

Escorts: Tractor sales have risen in anticipation of

normal monsoons

Maruti Suzuki: PV demand is holding up

Source: SIAM, Company, HSIE Research Source: SIAM, Company, HSIE Research

-

3,000

6,000

9,000

12,000

15,000

18,000

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun

-21

-

50,000

100,000

150,000

200,000

250,000

300,000

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun

-21

-

20,000

40,000

60,000

80,000

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun

-21

-

150,000

300,000

450,000

600,000

750,000

900,000

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun

-21

-

3,000

6,000

9,000

12,000

15,000

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun

-21

-

50,000

100,000

150,000

200,000

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun

-21

Page | 7

Autos & Transportation: 1QFY22E Results Preview

Commodity prices are at elevated levels

Brent crude Lead

Source: Bloomberg, HSIE Research Source: Bloomberg, HSIE Research

Copper Aluminium

Source: Bloomberg, HSIE Research Source: Bloomberg, HSIE Research

Steel prices

Source: Steelmint, HSIE Research

10

30

50

70

90

Jun

-16

Jun

-17

Jun

-18

Jun

-19

Jun

-20

Jun

-21

Brent price ($/bbl)

1,600

1,800

2,000

2,200

2,400

2,600

Jun

-16

Jun

-17

Jun

-18

Jun

-19

Jun

-20

Jun

-21

Lead Price ($)

4,000

6,000

8,000

10,000

Jun

-16

Jun

-17

Jun

-18

Jun

-19

Jun

-20

Jun

-21

Copper Price ($)

1,200

1,600

2,000

2,400

2,800Ju

n-1

6

Jun

-17

Jun

-18

Jun

-19

Jun

-20

Jun

-21

Aluminium Price ($)

Page | 8

Autos & Transportation: 1QFY22E Results Preview

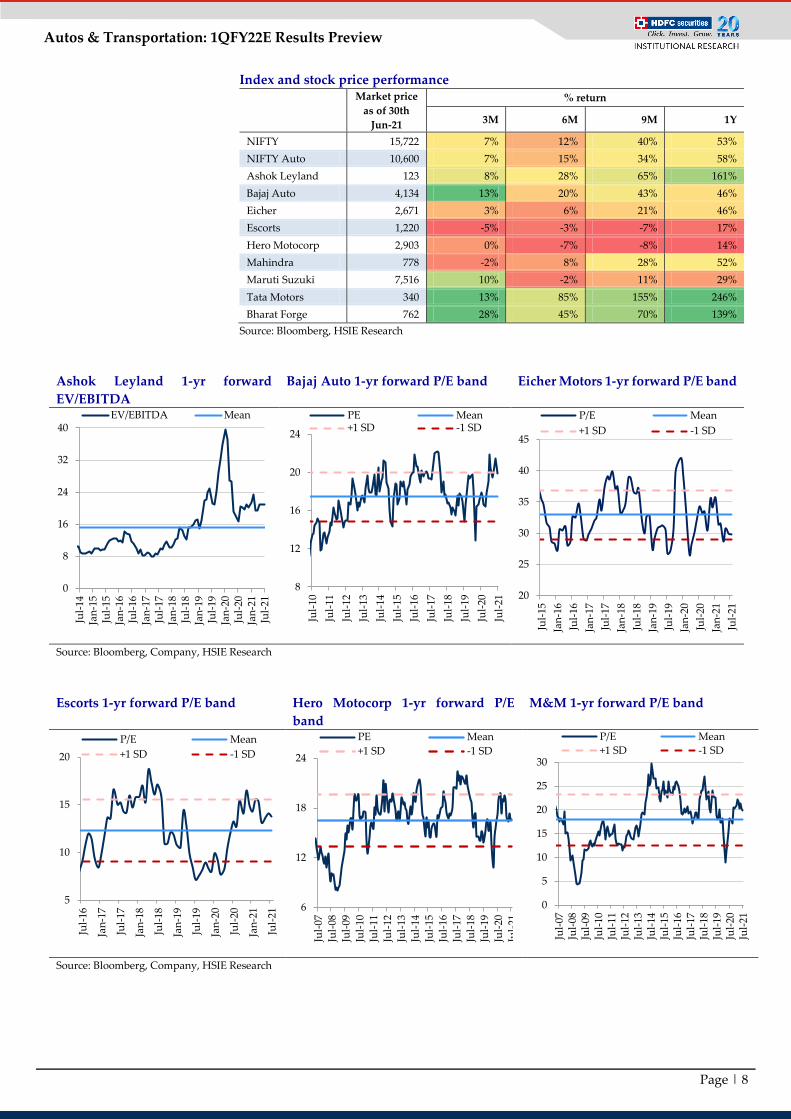

Index and stock price performance

Market price

as of 30th

Jun-21

% return

3M 6M 9M 1Y

NIFTY 15,722 7% 12% 40% 53%

NIFTY Auto 10,600 7% 15% 34% 58%

Ashok Leyland 123 8% 28% 65% 161%

Bajaj Auto 4,134 13% 20% 43% 46%

Eicher 2,671 3% 6% 21% 46%

Escorts 1,220 -5% -3% -7% 17%

Hero Motocorp 2,903 0% -7% -8% 14%

Mahindra 778 -2% 8% 28% 52%

Maruti Suzuki 7,516 10% -2% 11% 29%

Tata Motors 340 13% 85% 155% 246%

Bharat Forge 762 28% 45% 70% 139%

Source: Bloomberg, HSIE Research

Ashok Leyland 1-yr forward

EV/EBITDA

Bajaj Auto 1-yr forward P/E band Eicher Motors 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

Escorts 1-yr forward P/E band Hero Motocorp 1-yr forward P/E

band

M&M 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

0

8

16

24

32

40

Jul-

14Ja

n-1

5Ju

l-15

Jan

-16

Jul-

16Ja

n-1

7Ju

l-17

Jan

-18

Jul-

18Ja

n-1

9Ju

l-19

Jan

-20

Jul-

20Ja

n-2

1Ju

l-21

EV/EBITDA Mean

8

12

16

20

24

Jul-

10

Jul-

11

Jul-

12

Jul-

13

Jul-

14

Jul-

15

Jul-

16

Jul-

17

Jul-

18

Jul-

19

Jul-

20

Jul-

21

PE Mean+1 SD -1 SD

5

10

15

20

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Jul-

19

Jan

-20

Jul-

20

Jan

-21

Jul-

21

P/E Mean

+1 SD -1 SD

6

12

18

24

Jul-

07

Jul-

08

Jul-

09

Jul-

10

Jul-

11

Jul-

12

Jul-

13

Jul-

14

Jul-

15

Jul-

16

Jul-

17

Jul-

18

Jul-

19

Jul-

20

Jul-

21

PE Mean

+1 SD -1 SD

0

5

10

15

20

25

30

Jul-

07Ju

l-08

Jul-

09Ju

l-10

Jul-

11Ju

l-12

Jul-

13Ju

l-14

Jul-

15Ju

l-16

Jul-

17Ju

l-18

Jul-

19Ju

l-20

Jul-

21P/E Mean

+1 SD -1 SD

20

25

30

35

40

45

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Jul-

19

Jan

-20

Jul-

20

Jan

-21

Jul-

21

P/E Mean

+1 SD -1 SD

Page | 9

Autos & Transportation: 1QFY22E Results Preview

Maruti Suzuki 1-yr forward P/E band Amara Raja 1-yr forward P/E band Bharat Forge 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

Endurance 1-yr forward P/E band Gulf Oil 1-yr forward P/E band Subros 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

Sundram Fasteners 1-yr forward P/E

band

CONCOR 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

5

15

25

35

45

Jul-

07

Jul-

08

Jul-

09

Jul-

10

Jul-

11

Jul-

12

Jul-

13

Jul-

14

Jul-

15

Jul-

16

Jul-

17

Jul-

18

Jul-

19

Jul-

20

Jul-

21

P/E Mean

+1 SD -1 SD

0

10

20

30

40

Jul-

09

Jul-

10

Jul-

11

Jul-

12

Jul-

13

Jul-

14

Jul-

15

Jul-

16

Jul-

17

Jul-

18

Jul-

19

Jul-

20

Jul-

21

P/E Mean

+1 SD -1 SD

0

10

20

30

40

50

60

70

Jul-

11

Jul-

12

Jul-

13

Jul-

14

Jul-

15

Jul-

16

Jul-

17

Jul-

18

Jul-

19

Jul-

20

Jul-

21

P/E Mean+1 SD -1 SD

10

15

20

25

30

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Jul-

19

Jan

-20

Jul-

20

Jan

-21

Jul-

21

PE Mean

+1 SD -1 SD

0

10

20

30

40

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Jul-

19

Jan

-20

Jul-

20

Jan

-21

Jul-

21

P/E Mean+1 SD -1 SD

15

25

35

45

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Jul-

19

Jan

-20

Jul-

20

Jan

-21

Jul-

21

P/E Mean

+1 SD -1 SD

5

15

25

35

Jul-

13

Jul-

14

Jul-

15

Jul-

16

Jul-

17

Jul-

18

Jul-

19

Jul-

20

Jul-

21

P/E Mean+1 SD -1 SD

5

15

25

35

45

55

Jul-

12

Jul-

13

Jul-

14

Jul-

15

Jul-

16

Jul-

17

Jul-

18

Jul-

19

Jul-

20

Jul-

21

P/E Mean

+1 SD -1 SD

Page | 10

Autos & Transportation: 1QFY22E Results Preview

HDFC securities

Institutional Equities

Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park,

Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Board: +91-22-6171-7330 www.hdfcsec.com

Disclosure:

We, Aditya Makharia, CA & Mansi Lall, MBA, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report

accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also

certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC

Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication

of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest.

Any holding in stock –YES

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is solely for information of the recipient only. The report must not be used as a singular basis of any investment

decision. The views herein are of a general nature and do not consider the risk appetite or the particular circumstances of an individual investor; readers are requested to

take professional advice before investing. Nothing in this document should be construed as investment advice. Each recipient of this document should make such

investigations as they deem necessary to arrive at an independent evaluation of an investment in securities of the companies referred to in this document (including merits

and risks) and should consult their own advisors to determine merits and risks of such investment. The information and opinions contained herein have been compiled or

arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty,

representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without

notice. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete. HSL is not obliged to update this report for such

changes. HSL has the right to make changes and modifications at any time.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident

or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation

or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to the attention

of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or indirectly, for any purposes or in any manner.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the

income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It

should not be considered to be taken as an offer to sell or a solicitation to buy any security.

This document is not, and should not, be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report should not

be construed as an invitation or solicitation to do business with HSL. HSL may from time to time solicit from, or perform broking, or other services for, any company

mentioned in this mail and/or its attachments.

HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the

company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in

the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of

interests with respect to any recommendation and other related information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any

action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs,

reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report,

or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for

any other assignment in the past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this

report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory

service in a merger or specific transaction in the normal course of business.

HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the

research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research

Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with

and reach different conclusion from the information presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject

company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai

400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066 Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600 HDFC Securities

Limited, SEBI Reg. No.: NSE, BSE, MSEI, MCX: INZ000186937; AMFI Reg. No. ARN: 13549; PFRDA Reg. No. POP: 11092018; IRDA Corporate Agent License No.:

CA0062; SEBI Research Analyst Reg. No.: INH000002475; SEBI Investment Adviser Reg. No.: INA000011538; CIN - U67120MH2000PLC152193

Rating Criteria

BUY: >+15% return potential

ADD: +5% to +15% return potential

REDUCE: -10% to +5% return potential

SELL: > 10% Downside return potential