autos malaysia

DESCRIPTION

Autos MalaysiaTRANSCRIPT

June 26, 2012

IMPORTANT DISCLOSURES. INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. Designed by Eight, Powered by EFA

AUTOS More vrooom to grow

AUTOS June 26, 2012

2

TABLE OF CONTENTS

1. BACKGROUND .................................................................................................................................. 6

2. OVERVIEW OF MALAYSIAN AUTOS ............................................................................................... 6

3. MALAYSIA’S AUTO SECTOR VIS-À-VIS THAILAND AND INDONESIA ....................................... 9

4. OPPORTUNITIES FOR THE MALAYSIAN AUTO PLAYERS ......................................................... 17

5. CHALLENGES AHEAD FOR THE MALAYSIAN AUTO PLAYERS ................................................ 23

6. VALUATION AND RECOMMENDATION ...................................................................................... 30

June 26, 2012

3

REGIONAL

MALAYSIA

SINGAPORE

INDONESIA

THAILAND

PHILIPPINES

CHINA, HONG KONG

AUTOS SHORT TERM (3 MTH) LONG TERM

Conviction

More vrooom to grow Despite Malaysia’s high vehicle penetration relative to Indonesia and Thailand, vehicle demand should continue to see support from the country’s favourable demographics, rising disposable incomes, new model launches and pent-up demand this year, among others.

Figure 1: Malaysia’s vehicle sales

0

100000

200000

300000

400000

500000

600000

700000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

F

units

SOURCES: CIMB, MAA

Further out, there are pockets of export opportunities under AFTA and the upcoming ASEAN Economic Community (AEC) 2015, which local auto players can capitalise on. We maintain our Overweight call on the sector with DRB-HICOM as our preferred pick.

Demand fundamentals are intact Malaysia has a sizeable car-buying population that presents huge opportunities. An estimated 46% of the population fall into the 20-49 age bracket. This age bracket tends to be the key driver of vehicle demand. Also, the government is seeking to transform the country into a high-income nation by 2020, which would require the annual income to rise to the equivalent of US$15,000 p.a. from US$9,700 currently. As income levels rise, so will the propensity to spend on big-ticket items like cars.

One of the lowest cost of vehicle ownership Interestingly, while Malaysia’s car prices are among the top three highest in the region, the cost of vehicle ownership is relatively low, largely due to the country’s subsidised fuel. As long as affordability levels stay low, we believe that domestic demand for cars should remain firm.

Pockets of export opportunities are present Although Malaysia lags behind Thailand and Indonesia in terms of total vehicle exports, there are pockets of export opportunities which auto players can capitalise on. We like auto players such as DRB-HICOM, which is well-poised to ride Volkswagen AG’s pursuit of the ASEAN auto market. Tan Chong also has a foothold in the Indochina auto market.

Notes from the Field

Loke Wei Wern

T (60) 3 20849946 E [email protected]

“When the market opens, there will definitely be more players that want to come in. One of the positive things about our country is the disposable income, especially with the middle class, compared with neighbouring countries”.

─ Datuk Aminar Rashid

Salleh, Managing Director

of Perodua

Highlighted Companies

DRB-HICOM With the recent acquisition of Proton, DRB’s brands now straddle the premium and mid-market segments. As Volkswagen AG’s (VW) local partner, DRB will play an integral part in VW’s expansion plans in the ASEAN region.

UMW Holdings UMW controls close to 50% of Malaysia’s total vehicle sales via Toyota and Perodua, both of which are market leaders in the non-national and national segments, respectively. UMW boasts the highest dividend yield in the sector.

Tan Chong Motor Tan Chong’s strategic expansion of its product mix is intact. By year-end, it will have a presence in the B-segment through Nissan Almera. Its presence in the small but growing Indochina market will provide additional growth opportunities.

AUTOS June 26, 2012

4

KEY CHARTS

Malaysia’s position in ASEAN Malaysia ranks third in terms of total vehicle sales in the region after Indonesia and Thailand. It is the second-largest passenger car market in ASEAN and the fourth-largest in terms of commercial vehicles.

-100,000200,000

300,000400,000500,000600,000700,000

800,000900,000

1,000,000

Brun

ei

Indo

nesi

a

Mal

aysi

a

Philip

pine

Sing

apor

e

Thai

land

Viet

nam

High vehicle penetration rate The vehicle penetration rate for Malaysia, as measured by the number of vehicles owned per capita, is relatively high. The vehicle penetration rate is estimated to be around 40%, i.e. 4 out of 10 Malaysians own some form of vehicle.

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Annual domestic vehicle sales (LHS) Motorcar/capita (RHS)

Sizeable car-buying population Malaysia has a sizeable car-buying population that auto players can tap. An estimated 46% of the current population falls into the 20-49 age bracket. This age bracket tends to be the key driver of vehicle demand.

43% 43% 43% 42% 42% 42% 41% 37% 37% 37% 37%

43% 43% 43% 43% 43% 43% 43% 46% 46% 46% 46%

13% 14% 14% 14% 15% 15% 15% 16% 16% 16% 16%

0%

20%

40%

60%

80%

100%

120%

2002 2003 2004 2005 2006 2007 2008 2009 2010F 2011F 2012F

0 to 19 years ('m) 20 to 49 years ('m) 50 and above ('m)

Private vehicles will stay as the dominant choice of transport, for now The utilisation of public transport (measured as a percentage of journeys during peak periods) in Malaysia is relatively low. As such, we applaud the government’s efforts to improve the country’s public transportation network in order to increase usage. But we note that these efforts will take time to bear fruit. Also, much of the improvements in the public transport network are focused on the Greater KL/Klang Valley area, which means that other populous states, like Johor and Perak, still offer good potential for auto players. - 10 20 30 40 50 60 70 80 90 100

Klang Valley

Penang

Johor Bahru

Singapore

Hong Kong

London

Toronto

SOURCE: CIMB, 10MP, PRESS REPORT

AUTOS June 26, 2012

5

Figure 2: Sector Comparisons Price Target Price

(local curr) (local curr) CY2012 CY2013 CY2012 CY2013 CY2012 CY2013 CY2014 CY2012 CY2013 CY2012 CY2013Brilliance China Automotive 1114 HK Outperform 7.07 11.70 4,579 9.7 7.0 38.2% 2.90 2.05 35.3% 34.3% 28.6% 70.0 54.9 0.0% 0.0%Dongfeng Motor Group 489 HK Neutral 12.26 15.80 13,612 8.3 7.6 6.4% 1.61 1.36 21.3% 19.4% 17.6% 3.2 2.3 1.8% 1.9%Guangzhou Auto - H 2238 HK Trading Buy 6.53 7.50 6,883 7.8 6.7 9.4% 1.02 0.92 13.7% 14.5% 14.6% 10.2 7.6 3.8% 4.5%Geely Automobile Holdings 175 HK Neutral 2.70 3.30 2,601 8.9 7.0 19.2% 1.49 1.25 18.2% 19.5% 17.8% 6.6 5.0 1.3% 1.7%Great Wall Motor 2333 HK Outperform 15.00 19.30 7,170 8.6 7.4 18.0% 1.85 1.56 23.6% 22.7% 21.0% 4.3 3.6 3.1% 3.6%Minth Group 425 HK Neutral 8.50 7.70 1,180 8.9 7.9 10.9% 1.15 1.04 13.5% 13.9% 13.9% 3.9 3.1 3.9% 4.4%Qingling Motors Company-H 1122 HK Outperform 1.81 3.50 579 9.1 7.8 16.7% 0.51 0.50 5.6% 6.4% 7.4% -3.6 -3.5 9.0% 10.5%Weichai Power Co Ltd-H 2338 HK Neutral 31.55 34.40 7,609 9.2 8.9 -2.6% 1.57 1.34 18.6% 16.3% 14.6% 3.8 3.5 0.3% 0.3%China/Hong Kong average 8.6 7.5 10.4% 1.52 1.30 19.1% 18.7% 17.4% 4.5 3.5 1.9% 2.2%Astra International ASII IJ Outperform 6,700 7,700 28,525 14.8 12.0 12.8% 3.83 3.18 27.9% 29.1% 27.3% 11.0 8.6 2.5% 2.6%Indomobil Sukses Int'l IMAS IJ Outperform 6,850 9,200 1,992 15.2 10.6 35.2% 3.27 2.56 23.7% 27.1% 24.5% 20.3 15.1 0.6% 1.0%Indonesia average 14.9 11.9 14.0% 3.79 3.13 27.6% 28.9% 27.1% 11.4 8.9 2.4% 2.5%Tan Chong Motor Holdings TCM MK Underperform 4.50 4.20 946 14.6 9.4 15.4% 1.53 1.35 11.0% 15.3% 15.4% 9.0 6.9 2.2% 2.3%UMW Holdings UMWH MK Outperform 9.02 9.55 3,298 12.5 11.9 11.0% 2.26 2.10 18.8% 18.3% 18.1% 6.6 6.3 4.8% 5.0%DRB-Hicom DRB MK Outperform 2.55 4.10 1,543 8.5 6.1 37.8% 0.49 0.44 6.4% 7.5% 7.9% -5.3 -4.5 1.9% 2.2%Malaysia average 14.6 9.4 15.4% 1.53 1.35 11.0% 15.3% 15.4% 9.0 6.9 2.2% 2.3%Average (all) 10.6 9.0 11.6% 2.07 1.76 21.2% 21.2% 19.8% 6.9 5.6 2.1% 2.3%

EV/EBITDA (x) Dividend Yield (%)Core P/E (x) 3-year EPS CAGR (%)

P/BV (x) Recurring ROE (%)Company Bloomberg Ticker

Recom. Market Cap (US$ m)

SOURCES: CIMB, COMPANY REPORTS

Calculations are performed using EFA™ Monthly Interpolated Annualisation and Aggregation algorithms to December year ends

AUTOS June 26, 2012

6

Malaysian autos 1. BACKGROUND 1.1 Where does Malaysia stand? Among the ten member nations of ASEAN (Malaysia, Thailand, Indonesia, the Philippines, Brunei, Singapore, Vietnam, Cambodia, Myanmar and Laos), only three countries, namely Thailand, Indonesia and Malaysia, are major demand centres for motorcars (excluding motorcycles and scooters). Accommodative government policies, an expanding middle-income group and rising disposable income are among the common factors helping to propel their auto industries forward. While all three countries have gained significant mileage in the auto sector and lead the other seven member nations, by perhaps leaps and bounds, in terms of annual vehicle sales and the development of the local automotive industry, future growth prospects among the three member nations differ.

In this report, we will 1) provide a brief overview of Malaysia’s auto industry, 2) study Malaysia’s auto sector vis-à-vis the other two major demand centres, i.e. Indonesia and Thailand, and 3) examine the opportunities and threats facing auto assemblers in the country.

2. OVERVIEW OF MALAYSIAN AUTOS 2.1 Brief background on Malaysia’s auto sector Malaysia’s automobile industry dates back to the 1960s when the government developed a policy to promote an integrated automotive industry to strengthen its industrial base and reduce its dependency on the agricultural sector. The country’s automobile industry comprises the following parties: 1) national car manufacturers, 2) local assemblers of foreign brands, and 3) parallel importers. Further down the supply chain are the used car dealers, whose role is to provide an avenue for vehicles to be resold, and the automotive components/parts manufacturers, who supply car parts to vehicle manufacturers and assemblers. In total, there are four vehicle manufacturers and 10 vehicle assemblers with over 15 manufacturing and assembly plants in Malaysia. There are numerous auto components and parts players.

Table of Contents 1. BACKGROUND p.4

2. OVERVIEW OF MALAYSIAN AUTOS p.4

3. MSIA VIS-À-VIS THAILAND AND INDO p.7

4. OPPORTUNITIES p.15

5. THREATS p.21

5. VALUATION AND RECOMMENDATION p.28

Notes from the Field

“There are about one billion people living in this region (Asia, outside China), so the potential to grow the business is huge”

– Jean Yves Dossal, sales director of PSA Peugeot Citroen Asian operations

AUTOS June 26, 2012

7

Figure 3: Manufacturing and assembly plants in Malaysia Assembly and manufacturing plants Vehicle makeHicom Automotive Manufacturers (Malaysia) Sdn Bhd (Plant I) Suzuki (PV)

Volkswagen (PV)Hicom Automotive Manufacturers (Malaysia) Sdn Bhd (Plant II) Mitsubishi Fuso (CV)

Mercedes Benz (PV and CV)Assembly Services Sdn Bhd Toyota (PV and CV)

Hino (CV)Honda Malaysia Sdn Bhd Honda (PV)Inokom Corporation Sdn Bhd BMW (PV)

HD5000 (CV)Hyundai-Inokom (PV and CV)Landrover (CV)Mazda (PV)

Isuzu-Hicom Malaysia Isuzu (CV)Isuzu D'Max (CV)Hicom Perkasa (CV)

Oriental Assemblers Sdn Bhd Chery (PV)Changan (PV)Dong Feng (CV)Hyundai (PV)Joy Long (PV)Tuah (CV)ZX Auto (CV)

Swedish Motor Assemblies Sdn Bhd Volvo (PV and CV)Kinglong (CV)Renault (CV)

Tan Chong Motor Assemblies (Plant I) Nissan (PV and CV)Renault (CV)Foton (CV)

Tan Chong Motor Assemblies (Plant II) Nissan (PV)Perodua Manufacturing Sdn Bhd Perodua (PV)Perusahaan Otomobil Nasional Bhd (Proton) Proton (PV and CV)Proton Tanjung Malim Sdn Bhd Proton (PV)

Kia (PV)Naza (PV)

Naza Automotive Manufacturing Sdn Bhd Peugeot (PV)Scania (Malaysia) Sdn Bhd Scania (CV)

SOURCES: CIMB, MAA

The four national car manufacturers in the country are Proton, Perodua, Inokom Corporation and Malaysian Truck & Bus. Proton and Perodua are the biggest players in the domestic market as both players control close to 56% market share combined in terms of total vehicle sales. The other 10 car assemblers assemble non-national brands. Non-national vehicle sales in Malaysia are skewed towards the Japanese brands although their market positions have been somewhat weakened by last year’s back-to-back natural disasters in Japan and Thailand and the gradual rise of the Korean brands. Assembly Services (Toyota), Tan Chong Motor (Nissan) and Honda Malaysia (Honda) are the three biggest assemblers after Proton and Perodua. They collectively control 25% of the total vehicle market.

The European brands’ presence in Malaysia is still somewhat restricted to the luxury and premium segments. The punitive tax structure on non-ASEAN imports has inflated European car prices, making their cars generally uncompetitive from a pricing point of view compared to the national car brands and other locally-assembled Japanese brands. But this is gradually changing as European car companies, such as Mercedes Benz, Volvo, Peugeot and Volkswagen AG (VW), have set up CKD operations in the country. The European brands in Malaysia control only c.6% of the country’s total vehicle sales.

AUTOS June 26, 2012

8

Figure 4: Auto players in Malaysia National players Brands assembled ShareholdersPerusahaan Otomobil Nasional Sdn Bhd ProtonPerodua Manufacturing Sdn Bhd Perodua Daihatsu & Mitsui (51%), Perodua Sdn Bhd (49%)Inokom Corporation Inokom 53%-owned by Sime DarbyMalaysian Truck & Bus Sdn Bhd HICOM and Isuzu commercial trucks DRB, Isuzu Motor, Itochu Corp, Hicom Holdings

Other car assemblersHICOM Automotive Manufacturers Malaysia Mercedes, Suzuki, Isuzu, Mitsubishi Fuso, Daewoo, Iveco, LDV, VW DRB-Hicom (93%)Assembly Services Sdn Bhd Toyota UMW (51%), Toyota Motor (49%)Honda Malaysia Sdn Bhd Honda DRB (34%), Oriental Holdings (15%), Honda (51%)Kinabalu Motor Assembly Sdn Bhd Isuzu MBM Resources (70%)Naza Automotive Manufacturing Sdn Bhd Peugeot, Kia, Naza Naza GroupOriental Assemblers Sdn Bhd Hyundai, Chery, Joy Long, LMG Oriental Holdings (97%)Swedish Motor Assemblers Sdn Bhd Ford, Mazda, Volvo Volvo Car Corporation (100%)Tan Chong Motor Assemblers Sdn Bhd Nissan, UD Tan Chong Motor (70%)Asia Automobile Industries Sdn Bhd Sinotruk Mikani HoldingsScania (Malaysia) Sdn Bhd Scania Scania CV AB (100%)

SOURCES: CIMB, MAA

Figure 5: Total vehicles sales in Malaysia in 2011 (passenger and commercial) Makes Passenger Commercial Total Market sharePerodua 179,989 - 179,989 30.0%Proton 158,601 56 158,657 26.4%Toyota 63,493 23,458 86,951 14.5%Honda 32,480 - 32,480 5.4%Nissan 25,504 6,772 32,276 5.4%Mitsubishi 3,754 8,299 12,053 2.0%Naza 9,347 - 9,347 1.6%Isuzu - 9,299 9,299 1.6%Volkswagen 7,350 - 7,350 1.2%Suzuki 7,308 - 7,308 1.2%Others (30 players) 47286 16881 64167 10.7%Total 535,112 64,765 599,877 100.0%

SOURCES: CIMB, MAA

2.2 Second-largest passenger car market in ASEAN Malaysia ranks third (600,123 units in 2011) in terms of total vehicle sales in the region after Indonesia (894,164) and Thailand (794,081). It is the second-largest passenger car market in ASEAN (sold 535,113 units in 2011), having lost the coveted first place to Indonesia (601,945) in 2010. It ranks fourth in terms of commercial vehicle sales (sold 65,010 units in 2011), after Thailand (433,640), Indonesia (292,219) and the Philippines (96,754).

Figure 6: Motor vehicle sales in ASEAN in 2011 Country Passenger vehicles Commercial vehicles 2011 2010Brunei 13,472 1,083 14,555 13,589 Indonesia 601,945 292,219 894,164 764,710 Malaysia 535,113 65,010 600,123 605,156 Philippine 44,862 96,754 141,616 168,490 Singapore 33,493 6,077 39,570 51,891 Thailand 360,441 433,640 794,081 800,357 Vietnam 64,505 45,155 109,660 111,737

SOURCES: CIMB, ASEAN AUTOMOTIVE FEDERATION

AUTOS June 26, 2012

9

Figure 7: Passenger vehicle sales in 2011 Figure 8: Commercial vehicle sales in 2011

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Brun

ei

Indo

nesi

a

Mal

aysi

a

Philip

pine

Sing

apor

e

Thai

land

Viet

nam

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Brun

ei

Indo

nesi

a

Mal

aysi

a

Philip

pine

Sing

apor

e

Thai

land

Viet

nam

SOURCES: CIMB, ASEAN AUTOMOTIVE FEDERATION SOURCES: CIMB, ASEAN AUTOMOTIVE FEDERATION

3. MALAYSIA’S AUTO SECTOR VIS-À-VIS THAILAND AND INDONESIA 3.1 Vehicle penetration rate is often used as a yardstick for

growth Barring years where sales were affected by the unexpected financial crises, supply shocks from natural disasters and uncertainties surrounding the National Automotive Policy (NAP), Malaysia’s vehicle sales have consistently trended up. The country’s population has achieved a CAGR of 2% over the past ten years while vehicle sales (excluding motorcycles) have outpaced it with a CAGR of 4%. From 97,262 in 1980, total vehicle sales have risen to 599,877 units in 2011.

Malaysia’s solid economic growth and high GDP per capita relative to the other member ASEAN nations (except Brunei and Singapore) were among the key factors underpinning this sales uptrend over the past three decades.

Figure 9: GDP per capita, current prices

0

2,000

4,000

6,000

8,000

10,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

US$

Cambodia Indonesia Lao People's Democratic Republic

Malaysia Myanmar Philippines

Thailand Vietnam

SOURCES: CIMB, IMG

AUTOS June 26, 2012

10

As a result, the vehicle penetration rate, measured by the number of vehicles owned per capita, is relatively high in Malaysia. It is estimated that a total of 21.4m motor vehicles run on our roads today, out of which 11.4m or 53% are motorcars. This translates into an estimated vehicle penetration rate of 40% (i.e. 4 out of 10 Malaysians own some form of vehicle), considerably higher than Indonesia (7%) and Thailand (21%). Since the vehicle penetration rate is often used as a yardstick for vehicle sales growth, low levels in Indonesia and Thailand suggest that there is a lot of potential for expansion in the two countries’ auto industries.

Figure 10: Estimated vehicle penetration among ASEAN’s major vehicle demand centres

2010 2011Malaysia 38.7% 39.7%Indonesia 6.3% 6.6%Thailand 19.7% 20.8%Philippines 3.5% 3.6%

SOURCES: CIMB

Figure 11: Malaysia - motorisation rate Figure 12: Thailand - motorisation rate

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Annual domestic vehicle sales (LHS) Motorcar/capita (RHS)

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0%

5%

10%

15%

20%

25%

Annual domestic vehicle sales (LHS) Motorcar/capita (RHS)

SOURCES: CIMB, IMF, MAA SOURCES: CIMB, IMF, AAF, JAMA

Figure 13: Indonesia - motorisation rate Figure 14: Philippines - motorisation rate

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0%

1%

2%

3%

4%

5%

6%

7%

Annual domestic vehicle sales (LHS) Motorcar/capita (RHS)

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0%

1%

1%

2%

2%

3%

3%

4%

4%

Annual domestic vehicle sales (LHS) Motorcar/capita (RHS)

SOURCES: CIMB, IMF, AAF, JAMA SOURCES: CIMB, IMF, AAF, JAMA

AUTOS June 26, 2012

11

3.2 Debunking the expensive car myth The tax structure for Malaysia’s auto sector is designed to encourage the development of the local automotive sector. There are three different types of levies on vehicles: 1) import duties, 2) excise duties, and 3) sales tax. Prior to the ASEAN Free Trade Agreement (AFTA), Malaysia’s duty structure was punitive to protect the interests of the two national auto players. While the Malaysian government has gradually relaxed its protective grip on the sector, the duty structure still favours the national brands.

Figure 15: Types of taxes on motor vehicles Apart from the normal corporation tax, the government levies three other types of taxes on motor vehicles sold in Malaysia. These three types of taxes can be summarised as follows:1) Import duties - Levied on the CIF (carriage, insurance and freight) price of the vehicle. The rate depends on:a) type of vehicleb) CBU or CKDc) engine size2) Excise duties - Levied on the CIF price + local parts + local assembly costs3) Sales tax - 10% of the OMV plus excise duties and import duties

SOURCES: CIMB

Import duties of vehicles from within ASEAN have been gradually reduced to o% over the years. But vehicles in the country are still relatively more expensive compared to its peers in the region. The key culprit is the exorbitant excise duties, which the government imposed to make up for the revenue lost from the scrapping of import duties under AFTA in 2004. These excise duties range from 60% to 105%, depending on engine capacity and vehicle type. On top of this, all vehicles are slapped with a 10% sales tax. To put things into perspective, Indonesia imposes luxury tax of 0-75% on its vehicles, along with a 10% VAT, while Thailand imposes excise duties of 3-35%, in addition to a 7% VAT.

Figure 16: ASEAN car duty structure (as at Jan 10) Tax description

CKD CBU CKD CBU CKD CBU CKD CBU CKD CBUImport duty MFN rate 5%-45% 83% 10% 30% 0%-30% 80% 10% 40% 10% 30%

CEPT rate 5% 83% 0% 0% 0% 0% 0% 0% 0% 0%Excise/special consumption/luxury sales tax 45%-60% 45%-60% 60%-105% 60%-105% 17%-40% 17%-40% 30%-75% 30%-75% 2%-60% 2%-60%VAT/sales tax 10% 10% 10% 10% 7% 7% 10% 10% 12% 12%Interior tax - - - - 10% 10% - - - -

PhilippinesVietnam Malaysia Thailand Indonesia

SOURCES: CIMB, COMPANY

A comparison of the absolute prices of Honda Accord and Toyota Vios sold in selected countries in this region revealed that car prices in Singapore and Vietnam are among the highest. On fears that uncontrolled growth in the number of vehicles running on the road will cause massive traffic jams on the small island, the Singapore government has taken several measures to manage car ownership. These measures include the hefty ad valorem tax, registration fee, certificate of entitlement (COE), vehicle quota systems (VQS), road taxes and electronic road pricing (ERP), among others. Vietnam is second due to its punitive tax structure. Unlike the ASEAN-6 countries, import duties for vehicles in Vietnam have yet to be fully removed. Malaysia ranks third.

AUTOS June 26, 2012

12

Figure 17: Price comparison of similar models in ASEAN Honda Accord Local currency US$ VariantSingapore 179,900 142,332 2.4 (new facelift)Vietnam 1,435,000,000 68,858 2.4Malaysia 168,144 54,565 2.4 Vti-LIndonesia 483,500,000 51,944 2.4 Vti-LThailand 1,547,000 49,377 2.4 ELPhilippines 1,700,000 36,263 2.4 SToyota Vios Local currency US$ VariantSingapore 114,188 90,343 1.5G (with non-guaranteed COE)Vietnam 602,000,000 28,914 1.5GMalaysia 87,952 28,335 1.5GIndonesia 241,850,000 26,063 1.5GThailand 690,000 21,936 1.5GPhilippines 820,000 19,126 1.5G

SOURCES: CIMB

Interestingly, while Malaysia’s car prices are among the top three highest in the region, the cost of vehicle ownership (CVO) is said to be one of the lowest. The CVO is based on the purchase price of the car and its running costs, including fuel prices, road tax, insurance premium and vehicle registration fees. Critical to Malaysia’s low CVO is the subsidised fuel, which is the lowest compared to Thailand, Singapore, Indonesia, Vietnam and the Philippines. As such, while Malaysia’s absolute car prices are inflated by the excise duties, low running costs help to bring down the overall cost of owning a vehicle in the country. As long as affordability levels stay low, domestic demand for cars should remain intact, in our opinion.

3.3 Passenger car segment is Malaysia’s mainstay; Thailand and Indonesia focus on trucks and MPV

Due to the establishment of the national car programme, Malaysia’s auto sector is largely geared towards the production of passenger vehicles. The segment accounted for 80-90% of total vehicle sales in the country over the last 10 years. Specifically within the passenger vehicle segment in Malaysia, Perodua and Proton are the strongest players with 34% and 30% market share, respectively, followed by the three Japanese players Toyota (12%), Honda (6%) and Nissan (5%).

Figure 18: Malaysia's vehicle sales by type (passenger vs. commercial)

81% 80%

91% 91% 91% 90% 89%

19% 20%

9% 9% 9% 10% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011

Passenger cars Commercial cars

SOURCES: CIMB, MAA

AUTOS June 26, 2012

13

Figure 19: Total passenger vehicle sales in 2011 Makes Total PV Market sharePerodua 179,989 33.6%Proton 158,601 29.6%Toyota 63,493 11.9%Honda 32,480 6.1%Nissan 25,504 4.8%Naza 9,347 1.7%Volkswagen 7,350 1.4%Suzuki 7,308 1.4%Hyundai 6,469 1.2%Mazda 5,716 1.1%Mercedes Benz 5,439 1.0%Peugeot 5,345 1.0%Others (17 players) 28,071 5.2%Total 535,112 100%

SOURCES: CIMB, MAA

In the commercial vehicle segment, which the national auto players are absent in, Toyota is by far the strongest player with a 36% market share. Isuzu plays second fiddle with a 14% market share, followed closely by Mitsubishi with a 13% market share.

Figure 20: Total commercial vehicle sales in 2011 Makes Total Market shareToyota 23,458 36.2%Isuzu 9,299 14.4%Mitsubishi 8,299 12.8%Nissan 6,772 10.5%Hino 5,584 8.6%Ford 2,349 3.6%Daihatsu 2,118 3.3%Mitsubishi Fuso 1,756 2.7%Hyundai-Inokom 1,519 2.3%Hicom Perkasa 1,518 2.3%Others (13 players) 2,093 3.2%Total 64,765 100.0%

SOURCES: CIMB, MAA

Within the passenger vehicle segment, there are four sub-categories, namely, 1) passenger cars (sedans, hatchbacks), the largest sub-category in terms of vehicle sales, 2) multi-purpose vehicles (MPV), 3) four-wheel drives/sports utility vehicles (4WD/SUV), and 4) window vans.

The passenger cars sub-category, which is traditionally the national auto players’ stronghold, has always dominated the passenger vehicle segment. But the market share of passenger cars has been on a downtrend over the years as more affordable people-movers muscle their way up. Two notable launches that turned the tide were Proton Exora (launched in Apr 09) and Perodua Alza (launched in Nov 09). These two were Proton’s and Perodua’s maiden MPV models and have proven to be the bullets which helped the carmakers conquer the two top spots within the MPV segment with a combined market share of 62% in 2011. In 2010, the year which captured the first full-year contribution of both the Exora and Alza, sales of the MPV segment jumped 70% yoy. In the non-national segment, Toyota and Nissan are by far the largest players in the segment with a collective market share of 29%.

AUTOS June 26, 2012

14

Figure 21: Malaysia's passenger vehicle sales by sub-category

78% 78% 76%

69% 70%

9% 10% 12%18% 16%

3%3%2%2%3%1%1%1%1%1%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2007 2008 2009 2010 2011

Passenger cars 4WD/SUV Window Van MPV

SOURCES: CIMB, MAA

Figure 22: PV: Passenger car sub-category Makes Passenger cars Market sharePerodua 142,587 34.1%Proton 137,535 32.9%Toyota 45,470 10.9%Honda 27,203 6.5%Nissan 10,006 2.4%Suzuki 6,940 1.7%Naza 6,933 1.7%Volkswagen 6,815 1.6%Mercedes Benz 5,377 1.3%Mazda 4,623 1.1%Ford 4,548 1.1%BMW 4,315 1.0%Peugeot 4,089 1.0%Hyundai 3,489 0.8%Hyundai/Inokom 2,866 0.7%Lexus 1,711 0.4%Chevrolet 871 0.2%Mitsubishi 787 0.2%Audi 582 0.1%Volvo 475 0.1%Mini 301 0.1%Porsche 136 0.0%Renault 71 0.0%Chery 61 0.0%Kia 26 0.0%Subaru 8 0.0%Land Rover - 0.0%Mahindra - 0.0%Ssangyong - 0.0%Total 417,825 100.0%

SOURCES: CIMB, MAA

AUTOS June 26, 2012

15

Figure 23: PV: MPV sub-category Makes MPV Market sharePerodua 37,402 40%Proton 21,064 23%Toyota 14,229 15%Nissan 12,557 13%Chery 2,662 3%Naza 2,324 2%Honda 1,170 1%Mazda 788 1%Peugeot 477 1%Mitsubishi 456 0%Volkswagen 205 0%Ssangyong 186 0%Ford 58 0%Renault 10 0%Total 93,588 100%

SOURCES: CIMB, MAA

The 4WD/SUV sub-category is entirely dominated by non-national brands. Honda is the biggest contender in this category with a market share of 22%, followed by Mitsubishi (14%) and Hyundai (11%). Market share for this sub-category has been inching up over the past five years, in line with the general trend in emerging markets.

Figure 24: PV: 4WD/SUV sub-category Makes 4WD/SUV Market shareHonda 4,107 22.3%Mitsubishi 2,511 13.6%Hyundai 2,004 10.9%Toyota 1,763 9.6%Kia 1,384 7.5%Nissan 1,088 5.9%Hyundai/Inokom 952 5.2%Peugeot 779 4.2%BMW 685 3.7%Chevrolet 401 2.2%Suzuki 368 2.0%Audi 345 1.9%Volkswagen 330 1.8%Volvo 326 1.8%Mazda 305 1.7%Porsche 279 1.5%Ford 233 1.3%Chery 187 1.0%Land Rover 133 0.7%Naza 90 0.5%Ssangyong 58 0.3%Mercedes Benz 53 0.3%Mahindra 10 0.1%Renault 10 0.1%Subaru 9 0.0%Lexus - 0.0%Mini - 0.0%Perodua - 0.0%Proton - 0.0%Total 18,410 100.0%

SOURCES: CIMB, MAA

Although the market share of the passenger car sub-category has been floundering over the past three years, a slew of new launches in this segment could tip the scales in its favour this year. The 1% pt increase in market share from 69% in 2010 to 70% in 2011 was partly due to new models, such as the all-new Myvi (launched in Jun 11) and the Proton Saga facelift (launched in Dec 2010). This year, there is a host of major launches in the passenger cars sub-category, such as Proton Preve, Honda City facelift, all-new Toyota Camry,

AUTOS June 26, 2012

16

all-new Hyundai Elantra, Toyota Prius C and the Toyota Prius facelift. These models could draw interest back to the passenger car sub-category.

Both Thailand and Indonesia do not have their own national car programmes. Largely through incentives and low tax rates, Thailand has established itself as a hub for pick-up trucks in the region, where sales are supported by the country’s agricultural activities. Thailand is also the world’s number two market for pick-up trucks after the US. Sales of this segment account for a good 41% of Thailand’s total vehicle sales. Meanwhile, Indonesia focuses on the MPV segment, where sales account for slightly over 40% of the country’s total vehicle sales.

3.4 Thailand and Indonesia are major production bases; Malaysia is largely domestic-centric

Based on the table below, Thailand’s vehicle production has historically exceeded its domestic sales. This is because many global auto players have made Thailand their production base for the region. Major auto players, such as Toyota, Nissan, Honda, Isuzu, Suzuki, Mitsubishi, General Motors and Ford, have already set up manufacturing plants in the country. Thailand’s seamless supply chain is partly the reason behind its success as a production hub for global auto players in this region. According to an industry expert, Thailand has the largest number of Japanese automotive parts suppliers investing in the country, i.e. 500 vs. Indonesia’s 160.

But Indonesia is catching up. For example, Nissan has pledged to further strengthen its presence in Indonesia to support its programme to make the country a production hub for ASEAN. Indonesian Industry Minister MS Hidayat was quoted as saying that the company planned to invest US$400m to expand the production capacity of its existing plant in the country from the current 100,000 units to 250,000 units in 2014. Indonesia’s demography, i.e. huge population base and expanding middle-income class, is one of the country’s key attractions. That said, the country’s supply chain is not as developed as Thailand’s while infrastructure such as roads is still inadequate.

On the other hand, vehicles produced in Malaysia are largely to feed domestic demand. In the past, protectionist measures prevented global auto players from penetrating the country’s automotive sector. But the landscape is slowly changing. Peugeot and more recently Volkswagen AG (VW) have expressed interest to make Malaysia their production hub for the region. Both Peugeot and VW do not currently have a manufacturing presence in the region.

Figure 25: Vehicle sales vs. vehicle production Vehicle sales

2006 2007 2008 2009 2010 2011Brunei 12,522 14,220 14,680 12,365 13,589 14,555 Indonesia 318,904 433,341 603,774 483,550 764,710 894,164 Malaysia 490,768 487,716 548,115 536,905 605,156 600,123 Philippines 99,541 117,903 124,449 132,444 168,490 141,616 Singapore 137,564 122,254 110,574 79,503 51,891 39,570 Thailand 682,161 631,251 615,270 548,871 800,357 794,081 Vietnam 40,897 80,392 110,186 119,460 111,737 109,660

Vehicle production2006 2007 2008 2009 2010 2011

Brunei - - - - - - Indonesia 296,008 411,638 600,844 464,816 702,508 837,948 Malaysia 503,048 441,678 530,810 489,269 567,715 533,515 Philippines - - 63,621 62,523 80,477 64,906 Singapore - - - - - - Thailand 1,188,044 1,287,346 1,394,029 999,378 1,645,304 1,457,795 Vietnam 35,087 75,249 115,038 107,760 106,166 100,465

SOURCES: CIMB, AAF

AUTOS June 26, 2012

17

3.5 Exposure to green technology; Thailand is ahead while Indonesia plays catch-up

The global auto market is increasingly gravitating towards green technology with Asia leading in terms of the sales of electric and hybrid vehicles. According to J.D. Power and Associates, Asia controls 56% of the hybrid/electric vehicle market, followed by North America (32%) and Europe (13%). Within Asia, Japan is the biggest market, followed by China. The hybrid/electric vehicle market in ASEAN is relatively small, although this is gradually changing. Thailand is the first ASEAN country to build hybrid vehicles with the Camry hybrid the first model it rolled out. Unfavourable tax structures have previously kept the cars expensive and beyond the reach of the masses.

To encourage the development of the green car industry and to reduce the reliance on pick-up trucks, Thailand has introduced the eco-car programme, which provides incentives to auto players that build small and fuel-efficient cars meeting Euro 4 emissions standards and consume less than 5 litres per 100km. Companies investing in the manufacturing of small eco-cars are provided up to eight years of corporate tax breaks and duty-free imports of related machinery and equipment. So far, five auto players, i.e. Nissan, Honda, Suzuki, Mitsubishi and Toyota, have signed on for the eco programme and invested. The total eco-car production capacity of these five companies is 585,000 vehicles per year.

Malaysia does not have a comprehensive green vehicle programme like Thailand. But there was no shortage of initiatives and incentives rolled out during the 2009 National Automotive Policy (NAP) and budget to encourage the manufacturing of green vehicles in the country. We also expect eco-friendly measures to feature in the upcoming revised NAP. In Malaysia, Toyota is the first mover in introducing green vehicles with the rollout of Toyota Prius. Although sales of green vehicles were still relatively negligible at less than 5%, acceptance of these vehicles is definitely improving.

Indonesia is relatively far behind in terms of green vehicle sales as the government imposes high taxes on imported cars. A 10-75% tax is slapped on vehicles which are deemed as luxury items, a category that the hybrid and electric vehicles fall under. This is on top of the 40% tax imposed on imported vehicles. But this is set to change. Indonesia’s President Susilo Bambang Yudhoyono has said that the government plans to offer various incentives to auto players to make hybrid cars more affordable, including cancelling luxury sales taxes on these green vehicles in exchange for a lower excise tax. An eco-car project is expected to hit the road this year to propel the country towards becoming a full-scale production base for hybrid vehicles by 2020.

4. OPPORTUNITIES FOR THE MALAYSIAN AUTO PLAYERS Based on the vehicle penetration rate, which is one of the yardsticks for growth for the auto sector, Malaysia’s vehicle sales growth potential could be more subdued compared to Indonesia and Thailand. The potential for exports also seem rather limited given that most of the global auto players have made either Thailand or Indonesia their production base. That said, while growth prospects seem relatively less exciting, there are trends and opportunities in Malaysia that the domestic auto players can take advantage of, such as 1) the country’s favourable demographics in the form of a large working population and rising middle-income group, 2) improved export opportunities under AFTA and the ASEAN Economic Community (AEC) in 2015, and 3) a sizeable replacement market.

AUTOS June 26, 2012

18

4.1 Favourable demographics; large working population and rising middle-income group

Malaysia has a sizeable car-buying population that auto players can tap. Over the past 10 years, Malaysia’s population has expanded at a steady clip of about 2% p.a. from 23.8m in 2001 to 28.7m in 2011. An estimated 46% (or est. 13.7m) of the current population falls into the 20-49 age bracket. This age bracket tends to be the key driver of vehicle demand as it comprises the young working population through to the more established working adults who are generally more affluent.

Figure 26: Population breakdown by age group 0 to 19 years 20 to 49 years 50 and above

('m) ('m) ('m)2002 10.6 10.6 3.32003 10.8 10.9 3.42004 10.9 11.1 3.62005 11.1 11.3 3.82006 11.2 11.5 3.92007 11.3 11.8 4.12008 11.5 12.0 4.32009 10.4 12.9 4.6

2010F 10.6 13.2 4.72011F 10.7 13.4 4.82012F 10.9 13.7 4.9

SOURCES: CIMB, CEIC

Figure 27: Population breakdown by age group (%)

43% 43% 43% 42% 42% 42% 41% 37% 37% 37% 37%

43% 43% 43% 43% 43% 43% 43% 46% 46% 46% 46%

13% 14% 14% 14% 15% 15% 15% 16% 16% 16% 16%

0%

20%

40%

60%

80%

100%

120%

2002 2003 2004 2005 2006 2007 2008 2009 2010F 2011F 2012F

0 to 19 years ('m) 20 to 49 years ('m) 50 and above ('m)

SOURCES: CIMB, CEIC

Out of the 13.7m, 20% (or 2.7m) are aged 20-24 years old. This group of people is generally either approaching the end of their tertiary education or has just joined the workforce. Given the state of Malaysia’s public transportation system, a car might be deemed essential for travelling to and from work. Therefore, we think this age group should be a good representation of first-time car buyers.

Meanwhile, youths aged 15-19 make up an estimated 9% (or est. 2.8m) of the country’s population. Since the legal driving age in Malaysia is 18, this age group represents another potential source of demand for cars. We think these two groups make good target markets for entry-level vehicles.

Less than 15% (or 3.4m) of Malaysia’s population are 55 years old and above. While the older age group, such as retirees, will still buy cars, the loss of earnings could mean more cautious spending, especially on big-ticket items.

AUTOS June 26, 2012

19

Figure 28: Breakdown of 20-49 age group (%)

21% 21% 21% 21% 21% 21% 21% 20% 20% 20% 20%

19% 18% 19% 19% 19% 19% 19% 18% 18% 18% 18%

18% 17% 17% 17% 17% 17% 17% 17% 17% 17% 18%

16% 16% 16% 16% 16% 16% 16% 16% 16% 16% 16%

14% 15% 15% 15% 15% 15% 15% 15% 15% 15% 15%

12% 12% 13% 13% 13% 13% 13% 13% 13% 13% 13%

0%

20%

40%

60%

80%

100%

120%

2002 2003 2004 2005 2006 2007 2008 2009 2010F 2011F 2012F

20 to 24 Years ('m) 25 to 29 Years ('m) 30 to 34 Years ('m) 35 to 39 Years ('m)

40 to 44 Years ('m) 45 to 49 Years ('m)

SOURCES: CIMB, CEIC

Vehicle sales are also, to a large extent, driven by income levels since income determines the purchasing capacity of households and the relative affordability of cars. Apart from Vietnam and Singapore where vehicle sales are affected by sharp changes in excise duties, taxes and COE premiums, vehicle sales in Malaysia, Thailand, Indonesia and the Philippines have largely tracked the GDP per capita.

As such, we see it as good news that the government plans to transform the country into a high-income nation by 2020, which would require the annual income to rise to the equivalent of US$15,000 p.a. from US$9,700 currently. As income levels increase, a bigger proportion of the population will be able to afford cars. This presents an opportunity for new players. National car players with entry-level cars, like Proton and Perodua, will be able to take advantage of new car buyers who were previously unable to afford the big-ticket purchase while non-national car players can take advantage of existing car owners who wish to upgrade to non-national cars.

AUTOS June 26, 2012

20

Figure 29: Malaysia - vehicle sales vs. GDP per capita (US$) Figure 30: Thailand - vehicle sales vs. GDP per capita (US$)

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

2,000

4,000

6,000

8,000

10,000

12,000

Annual vehicle sales Gross domestic product per capita, current prices

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

1,000

2,000

3,000

4,000

5,000

6,000

Annual vehicle sales Gross domestic product per capita, current prices

SOURCES: CIMB, IMF, AAF, VARIOUS AUTO BODIES SOURCES: CIMB, IMF, AAF, VARIOUS AUTO BODIES

Figure 31: Indonesia - vehicle sales vs. GDP per capita (US$) Figure 32: Philippines - vehicle sales vs. GDP per capita (US$)

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Annual vehicle sales Gross domestic product per capita, current prices

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

500

1,000

1,500

2,000

2,500

Annual vehicle sales Gross domestic product per capita, current prices

SOURCES: CIMB, IMF, AAF, VARIOUS AUTO BODIES SOURCES: CIMB, IMF, AAF, VARIOUS AUTO BODIES

Figure 33: Vietnam - vehicle sales vs. GDP per capita (US$) Figure 34: Singapore - vehicle sales vs. GDP per capita (US$)

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2006

2007

2008

2009

2010

2011

0

200

400

600

800

1,000

1,200

1,400

1,600

Annual vehicle sales Gross domestic product per capita, current prices

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Annual vehicle sales Gross domestic product per capita, current prices

SOURCES: CIMB, IMF, AAF, VARIOUS AUTO BODIES SOURCES: CIMB, IMF, AAF, VARIOUS AUTO BODIES

AUTOS June 26, 2012

21

4.2 Opportunities under AFTA and the ASEAN Economic Community (AEC) in 2015

To seek further growth opportunities, auto players are eyeing the overseas markets, especially within the region. The ASEAN Free Trade Agreement (AFTA), where its main objective is to create an integrated market within ASEAN in order to increase the region’s competitive edge compared to the rest of the world, has made this possible. AFTA’s main mechanism is the Common Effective Preferential Treatment (CEPT). Member countries had decided to reduce tariffs within a period of 15 years beginning 1 Jan 93 where final effective tariffs were agreed to be within the range of 0-5%. Under the CEPT, motor vehicles are eligible for concessional tariffs if it has 40% ASEAN content.

Figure 35: Import and excise duties on CKD motor vehicles for Malaysia (%)

Type/Engine capacity 2003 2004 2005 2006 2003 2004 2005 2006 2003 2004 2005 2006 2003 2004 2005 2006Passenger cars< 1800 42 25 0 0 55 60 90 75 42 35 10 10 55 60 90 751800 - 1999 42 25 0 0 55 70 120 80 42 35 10 10 55 70 120 802000 - 2499 60 25 0 0 55 80 150 90 60 35 10 10 55 80 150 902500 - 2999 70 25 0 0 55 90 200 105 70 35 10 10 55 90 200 105Above 3000 80 25 0 0 55 100 250 125 80 35 10 10 55 100 250 125MPV/Van< 1500 5 0 0 0 30 30 40 60 5 5 5 0 30 30 40 601500 - 1799 10 10 0 0 30 30 40 65 10 20 10 10 30 30 40 651799 - 1999 20 10 0 0 30 40 60 75 20 20 10 10 30 40 60 751999 - 2499 30 10 0 0 30 70 120 90 30 20 10 10 30 70 120 902499 - 2999 40 10 0 0 30 80 150 105 40 20 10 10 30 80 150 105Above 3000 40 10 0 0 30 90 170 125 40 20 10 10 30 90 170 1254WD< 1800 10 10 0 0 45 50 60 65 10 20 10 10 45 50 60 651800 - 1999 20 10 0 0 45 60 90 75 20 20 10 10 45 60 90 752000 - 2499 30 10 0 0 45 70 120 90 30 20 10 10 45 70 120 902500 - 2999 40 10 0 0 45 80 150 105 40 20 10 10 45 80 150 105Above 3000 40 10 0 0 45 90 170 125 40 20 10 10 45 90 170 125

ASEAN (CEPT) NON-ASEAN (MFN)Import Duty (ID) Excise duty (ED) Import duty Excise duty

SOURCES: CIMB, VARIOUS

Figure 36: Import and excise duties on CBU motor vehicles for Malaysia (%)

Type/Engine capacity 2003 2004 2005 2006 2006 2010 2003 2004 2005 2006 2003 2004 2005 2006 2003 2004 2005 2006Passenger cars< 1800 140 70 20 15 5 0 0 60 90 75 140 80 50 30 0 60 90 751800 - 1999 170 90 20 15 5 0 0 70 120 80 170 100 50 30 0 70 120 802000 - 2499 200 110 20 15 5 0 0 80 150 90 200 120 50 30 0 80 150 902500 - 2999 250 150 20 15 5 0 0 90 200 105 250 160 50 30 0 90 200 105Above 3000 300 190 20 15 5 0 0 100 250 125 300 200 50 30 0 100 250 125MPV/Van< 1500 60 40 20 15 5 0 0 30 40 60 60 60 50 30 0 30 40 601500 - 1799 60 40 20 15 5 0 0 30 40 65 60 60 50 30 0 30 40 651799 - 1999 80 50 20 15 5 0 0 40 60 75 80 70 50 30 0 40 60 751999 - 2499 150 90 20 15 5 0 0 70 120 90 150 100 50 30 0 70 120 902499 - 2999 180 110 20 15 5 0 0 80 150 105 180 120 50 30 0 80 150 105Above 3000 200 120 20 15 5 0 0 90 170 125 200 130 50 30 0 0 170 1254WD< 1800 60 40 20 15 5 0 0 50 60 65 60 60 50 30 0 50 60 651800 - 1999 80 50 20 15 5 0 0 60 90 75 80 70 50 30 0 60 90 752000 - 2499 150 80 20 15 5 0 0 70 120 90 150 100 50 30 0 70 120 902500 - 2999 180 100 20 15 5 0 0 80 150 105 180 120 50 30 0 80 150 105Above 3000 200 110 20 15 5 0 0 90 170 125 200 130 50 30 0 90 170 125

ASEAN (CEPT) NON-ASEAN (MFN)Import Duty (ID) Excise duty (ED) Import duty Excise duty

SOURCES: CIMB, VARIOUS

Liberalisation under AFTA-CEPT has opened up opportunities for the Malaysian auto sector. The low duties applied across all ASEAN countries provide auto players a much more sizeable market to tap. Higher production volume leads to economies of scale, which will have positive implications on the

AUTOS June 26, 2012

22

cost base. Not only that, AFTA has made it possible for foreign players to set up production bases in the region. Malaysia has been chosen as the main production hub for Peugeot right-hand-drive vehicles in ASEAN. The key beneficiary of this is Naza Group, which has been appointed its contract assembler. More recently, DRB-HICOM has been appointed the contract manufacturer for Volkswagen (VW). The VW cars will first be assembled for Malaysia, then ASEAN.

But the liberalisation of the sector, as with any other sectors, is not without its challenges. There will be a more level playing field and auto players (whether national or non-national brands) will no longer be able to enjoy favourable treatment at home. Cost structures have to be streamlined. Auto players that are able to gain mileage in export markets and increase production volumes in domestic assembly and manufacturing facilities should generally be able to achieve the economies of scale needed to lower unit production costs. Ultimately, we think auto players with the clout, scale and lower production cost base will be the ones that will be able to withstand the competition under AFTA.

Proton and Perodua are already working on growing their export markets. Other beneficiaries of increased economic cooperation under AFTA are DRB-HICOM, UMW and Tan Chong. DRB-HICOM is VW’s partner of choice for the latter’s expansion initiatives in the region. Tan Chong also has plans in place for its expansion in the Indochina region. For UMW, we think that expansion into markets like Thailand and Indonesia will be limited given Toyota Motor’s direct presence in these countries. But we think UMW will stand to benefit if Malaysia is made the hub for the production of selected models for onward export to other countries in the region.

Currently, only the ASEAN-6 (Malaysia, Thailand, Indonesia, the Philippines, Singapore and Brunei) has reduced import duties for vehicles with minimum 40% local content to 0%. The other ASEAN-4 countries (Cambodia, Myanmar, Vietnam and Laos) have not fully complied with the 0-5% duty structure under the AFTA-CEPT. The ASEAN Economic Community is expected to be enforced in 2015 where a single market and production base is to be established by the 10 ASEAN members. By implication, all 10 ASEAN members should, by then, have 0-5% import duties on ASEAN cars. The removal of duties should help facilitate cross-border sales and open up new markets for auto players.

4.3 Sizeable replacement demand The replacement market in Malaysia is sizeable. Malaysia has the second-largest passenger car market in ASEAN, which provides a good platform for auto players. Given the combination of economic uncertainty and good quality cars, the lifespan of a car before it is replaced could be creeping up. While we are unable to accurately ascertain the average lifespan of a car before it is replaced, if we assume a typical 5-year replacement cycle, an estimated 487,176 vehicles are due for replacement this year. In our analysis, we assume that 20% of owners will replace their vehicles after five years, 30% after six years and 40% after seven years. Based on these assumptions, sales from replacement demand will total about 465,592 units in 2012 alone. On top of that, we estimate that 6% of the 2.7m population within the age group of 20-24 years will purchase vehicles for the first time as this group generally consists of people who are either approaching the tail end of their tertiary education or have just joined the workforce and will need a car to commute to/from work. Based on these factors, the total vehicle sales from replacement and first-time owners will total about 625,639 units, which is marginally below our 2012 sales projection of 628,022.

If we extend our analysis to 2017 based on the same assumptions, we arrive at a vehicle sales CAGR of 4%. But again, we think this is a rough estimation of the long-term sustainable growth rate. Year-on-year growth in vehicle sales could vary depending on economic conditions, new model launches, government policies and the like.

AUTOS June 26, 2012

23

Figure 37: Estimates of sustainable vehicle demand 2012F 2013F 2014F 2015F 2016F 2017F

% of people who replace cars after five (5) years 20% 20% 20% 20% 20% 20%% of people who replace cars after six (6) years 30% 30% 30% 30% 30% 30%% of people who replace cars after seven (7) years 40% 40% 40% 40% 40% 40%Replacement demand

Replacement after five years 97,435 109,623 107,381 121,031 119,975 125,604 Replacement after six years 147,230 146,153 164,435 161,072 181,547 179,963 Replacement after seven years 220,926 196,307 194,870 219,246 214,762 242,062

Total replacement demand 465,592 452,083 466,686 501,349 516,284 547,630 New vehicle demand 160,047 186,722 213,397 213,397 213,397 213,397 % of first time buyers from the age group of 20-24 years (i.e. 2.7m) 6% 7% 8% 8% 8% 8%Implied vehicle demand (units) 625,639 638,805 680,083 714,745 729,681 761,027

SOURCES: CIMB, MAA, CEIC

5. CHALLENGES AHEAD FOR THE MALAYSIAN AUTO PLAYERS 5.1 Current public transport system makes car ownership

almost a necessity for some The country’s inadequate public transportation system has been one of the country’s vehicle demand growth drivers. This is particularly true when compared to more developed countries, like Singapore and Hong Kong. Despite improvements in the public transportation system over the years, this mode of transport has been falling out of favour. The market share of land public transport (LPT) in the morning peak hour has fallen from 34% in the 1980s to 10-12% in 2008. This share is relatively low compared to other international cities, such as Hong Kong (90% of LPT), Singapore (63% of LPT) and London (55% of LPT).

While the increase in vehicle penetration rate has resulted in a rise in congestion, door-to-door travel times for private vehicles remain competitive against the use of public transport, according to the Land Public Transport Commission (SPAD). Travel times are typically much higher by public transport. MRT Corp said that the choice of private vehicles over public transport by residents in the Greater KL and Klang Valley area is showing an uptrend. We believe these trends reflect not only the affordability of cars, rising income levels and changes in household characteristics but also the state of the country’s public transport and increase in highway network supply.

Figure 38: Summary of existing issues

Rail passengers key issuesBus passengers key issues Taxi passengers key issues

Service availability Punctuality Service availabilityService capacity Waiting and travel time Users safetyPoor integration with bus feeder services Accessibility Drivers attitudeQuality of existing track and signaling Bus condition Call serviceTicketing integration Interchange Taxi condition

Bus driver attitude Willingness to go to destinationInformation Charging according to the meterBus service

SOURCES: CIMB, SPAD

AUTOS June 26, 2012

24

Figure 39: Population density (persons per sq km)

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Klang Valley

Penang

Johor Bahru

Singapore

Hong Kong

London

Toronto

SOURCES: CIMB, 10MP, PRESS REPORTS

Figure 40: Regional comparison (% of public transport usage)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Kuala Lumpur

Seoul

Singapore

Manila

Tokyo

Bangladesh

SOURCES: EDGE WEEKLY

Figure 41: Public transport (% of journeys in peak periods)

- 10 20 30 40 50 60 70 80 90 100

Klang Valley

Penang

Singapore

Hong Kong

London

Toronto

SOURCES: CIMB, 10MP, PRESS REPORTS

AUTOS June 26, 2012

25

Figure 42: Vehicle density (vehicles per km per road)

- 100 200 300 400 500 600 700 800 900 1,000

Klang Valley

Penang

Johor Bahru

Singapore

Hong Kong

London

Toronto

SOURCES: CIMB, 10MP, PRESS REPORTS

Unless there is a significant overhaul in the connectivity and efficiency of the public transportation system, we think that private cars will still be the preferred mode of transport. But now that the government is stepping up its initiatives to improve the country’s public transport, what will be the implications on the future demand for cars?

Recall that improving urban public transport is one of the six National Key Result Areas (NKRAs). RM2.8bn has been allocated to this NKRA initiative, which is to be completed in the first two years of the 10th Malaysian Plan (10MP). The mass rapid transit (MRT) system, which is the biggest infrastructure project in Malaysia, is one of the key entry point projects for the NKRA. Designed to significantly improve the coverage of rail-based public transport in the Klang Valley, it will enable 50% of all trips in the Klang Valley to be done on public transport by 2020, from the current 17%. Phase 1 of the project is expected to be completed in 2017. The LPT mode share is projected to increase from the current 12% to 25% when all the three MRT lines are completed, and to 40% by 2020.

Apart from this, the existing Ampang and Kelana Jaya light railway transit (LRT) lines will also be extended. The Ampang line extension starts from the Seri Petaling station and passes through Kinrara and Puchong before ending at Putra Heights. The extension is 17.7km long with 12 new stations. Meanwhile, the Kelana Jaya line will begin from the Kelana Jaya station and pass through 13 new stations, including Subang Jaya and USJ, before ending at Putra Heights. The extension covers a distance of 17km. Both projects are expected to be completed in 2014.

AUTOS June 26, 2012

26

Figure 43: LRT extension alignment (Ampang and Kelana Jaya line)

SOURCES: CIMB, WWW.LRTEXTENSION.COM

Other plans include:

• Completion of the integrated transport terminal (ITT) in Bandar Tasik Selatan and construction of ITT in Gombak by 2012.

• Increasing transport capacity. Full delivery of 35 sets of new four-car trains will increase the capacity of the Kelang Jaya LRT line from 24k to 98k passengers/hour.

• Potential extension of the monorail system to improve connectivity between existing KTM Komuter, LRT and monorail systems.

• Implementation of 49km bus rapid transit (BRT) system in Kuala Lumpur and potential expansion to Iskandar in Johor.

• The estimated RM16.5bn high speed railway (HSR) linking Kuala Lumpur with Singapore to improve connectivity between the two cities.

As public transportation gradually improves, people should drive less. This should reduce the need for new private passenger vehicles. This can be deduced from the relatively low car penetration rate in more advanced countries, where the public transportation system is more comprehensive and developed. It is also evident in the lower vehicle density per km of road in cities such as Singapore, Hong Kong and London.

We applaud the government’s efforts to improve the country’s public transportation network. But we note that these efforts will take time to bear fruit. For example, the MRT will only be operational in 2017 while the LRT extension lines will only be completed in 2014, which is still a long wait. Also, much of the improvements in the public transport network are focused on the Greater KL/Klang Valley area, which means that other populous states, like Johor and Perak, still offer good potential for auto players. For now, we think that private cars will remain the dominant means of transport in Malaysia, although this trend looks set to shift.

AUTOS June 26, 2012

27

5.2 Improvements in highway network supply We think another reason behind the rising vehicle penetration rate is the improving highway infrastructure in the country, which helps strengthen connectivity and shorten the time to commute between two places. The 10MP has outlined seven new highways to be built over the next 4-5 years. The total value of the seven highways is estimated to be RM19bn. Our checks indicate that three urban highways are already at the planning stages. They are the Sg. Besi Ulu Kelang Expressway (Suke), Damansara-Shah Alam Highway (Dash) and Kinrara-Damansara Expressway (Kidex).

Suke Suke is a 31.8km, three-lane, dual-carriageway expressway that will start at Sri Petaling and pass through Sungai Besi, Alam Damai, Cheras-Kajang, Taman Bukit Permai, Taman Putra, Taman Permai Jaya, Taman Dagang Permai, Taman Kosas, Ampang dan Taman Hillview before ending at Ulu Kelang.

Figure 44: Details of Suke Designation : Sungai Besi-Ulu Kelang Elevated Expressway (SUKE) Length : 31.8km, 3 lane, dual carriageway (fully elevated)Total cost : UnknownTotal cost/km : UnknownTotal toll stops : 3 toll plazas,11 interchangesTotal land to be acquired : UnknownConstruction period : 4-5 yearsConcession period : UnknownConcession owner : Projek Lintasan Kota Holdings Sdn Bhd (Prolintas) - 100%-owned by PNBCoverage area : Alternative route for MRRII, linking major highways in Eastern Klang Valley

SOURCES: CIMB, COMPANY REPORTS

Dash Dash is a 20.1km, three-lane, dual-carriageway expressway that will commence at the Puncak Perdana U10 Shah Alam intersection and serve as a link for Puncak Perdana, Alam Suria, Denai Alam, Kampung Melayu Subang, Jalan Sungai Buloh, the Rubber Research Institute of Malaysia, Kota Damansara, Damansara Perdana and Mutiara Damansara. The expressway ends at the Penchala interchange.

Figure 45: Details of Dash Designation : Damansara-Shah Alam Highway (DASH)Length : 20.1km, 3 lane, dual carriageway (fully elevated)Total cost : UnknownTotal cost/km : UnknownTotal toll stops : 3 toll plazas,12 interchangesTotal land to be acquired : UnknownConstruction period : 4-5 yearsConcession period : UnknownConcession owner : Projek Lintasan Kota Holdings Sdn Bhd (Prolintas) - 100%-owned by PNBCoverage area : Link between east and west of Klang Valley: Shah Alam to Damansara Perdana

SOURCES: CIMB, COMPANY REPORTS

Kidex The Kinrara-Damansara Expressway (Kidex) will link Kinrara in Puchong and Pusat Bandar Damansara. The main purpose of this fully-elevated, 50km highway is to divert the heavy traffic on the Lebuhraya Damansara Puchong (LDP).

AUTOS June 26, 2012

28

Figure 46: Details of Kidex Designation : Kinrara-Damansara Expressway (KIDEX)Length : 50km, 3 lane, dual carriageway (fully elevated)Total cost : RM2.2bnTotal cost/km : RM44mTotal toll stops : 3 toll plazas,11 interchangesTotal land to be acquired : UnknownConstruction period : 4-5 yearsConcession period : UnknownConcession owner : UnknownCoverage area : Kinrara-Damansara

SOURCES: CIMB, COMPANY REPORTS

5.3 Risk of fuel price hike A hike in fuel prices will increase the running cost of a car and reduce affordability. In Malaysia, RON95, which is pumped by most motorists, retails at RM1.90 per litre (after a subsidy of RM1.09 per litre by the government). Our analysis below shows the impact on the cost of a full tank for vehicles of different engine capacities from a 1) 5 cents increase in RON95 from RM1.85 per litre to the current RM1.90, and 2) 10 cents increase in RON97 from RM2.80 per litre to the current RM2.90. The average impact is a 2.7% to 3.6% increase in cost. The government might not be able to fully absorb future fuel price increases, which means that there is the risk of higher fuel costs for consumers.

Figure 47: Impact of fuel price increase (5 sen for RON95, 10 sen for RON97) Before After Before AfterRON95 RON95 Change Change RON97 RON97 Change Change

CC Fuel tank capacity (L) Full tank Full tank (RM) % Full tank Full tank (RM) %659-989 RM RM RM RMPerodua Kancil 32 59.2 60.8 1.60 2.7% 89.6 92.8 3.20 3.6%Perodua Viva 36 66.6 68.4 1.80 2.7% 100.8 104.4 3.60 3.6%Perodua Myvi 40 74.0 76.0 2.00 2.7% 112.0 116.0 4.00 3.6%

1075-1597Proton Savvy 40 74.0 76.0 2.00 2.7% 112.0 116.0 4.00 3.6%Perodua Myvi 40 74.0 76.0 2.00 2.7% 112.0 116.0 4.00 3.6%Toyota Avanza 45 83.3 85.5 2.25 2.7% 126.0 130.5 4.50 3.6%

1308-1498Proton Gen 2 50 92.5 95.0 2.50 2.7% 140.0 145.0 5.00 3.6%Proton Saga 40 74.0 76.0 2.00 2.7% 112.0 116.0 4.00 3.6%Honda Civic 50 92.5 95.0 2.50 2.7% 140.0 145.0 5.00 3.6%Toyota Vios 42 77.7 79.8 2.10 2.7% 117.6 121.8 4.20 3.6%Honda City 42 77.7 79.8 2.10 2.7% 117.6 121.8 4.20 3.6%Perodua Alza 42 77.7 79.8 2.10 2.7% 117.6 121.8 4.20 3.6%Toyota Avanza 45 83.3 85.5 2.25 2.7% 126.0 130.5 4.50 3.6%Toyota Rush 50 92.5 95.0 2.50 2.7% 140.0 145.0 5.00 3.6%

1584-1799Proton Waja 60 111 114.0 3.00 2.7% 168.0 174.0 6.00 3.6%Proton Saga 40 74 76.0 2.00 2.7% 112.0 116.0 4.00 3.6%Nissan Latio 52 96.2 98.8 2.60 2.7% 145.6 150.8 5.20 3.6%Honda Civic 50 92.5 95.0 2.50 2.7% 140.0 145.0 5.00 3.6%Proton Exora 55 101.75 104.5 2.75 2.7% 154.0 159.5 5.50 3.6%Nissan Grand Livina 52 96.2 98.8 2.60 2.7% 145.6 150.8 5.20 3.6%

SOURCES: CIMB

5.4 Risk of increase in hire purchase (HP) rates A hike in HP rate is generally negative as it increases the loan servicing burden for buyers. HP rates usually track the trend in Bank Negara Malaysia’s (BNM) overnight policy rate (OPR). BNM’s OPR now stands at 3% and our economics team is not projecting a change in 2H12. We believe BNM will maintain its accommodative monetary policy for an extended period on the back of continued caution about the external environment. For next year, we are

AUTOS June 26, 2012

29

projecting OPR to hover around 3-3.5%. But we think that an increase, if any, is unlikely to throw buyers’ vehicle purchasing off track, as long as it is done gradually. Our analysis shows that a moderate interest rate hike increases car buyers’ monthly payments by just a small amount. But it could be a cause for concern if it is accompanied by rising fuel prices and heightened economic worries.

Figure 48: Hire purchase structure (rates offered by CIMB Bank) Margin of financing up to 90% of seller's invoiceFinancing tenure up to 9 years (108 months)

New car financing rates Fixed rate (p.a. flat)Types of vehiclesPassenger vehicles 2.60% to 2.70%Proton & Perodua 3.10% to 3.60%Unregistered reconditioned 2.65% to 2.80%

New commercial vehicles Fixed rate (p.a. flat)Types of vehiclesBTM up to 5,000 kg 3.25% to 3.60%BTM more than 5,000 kg 4.20% to 4.60%

SOURCES: CIMB

Figure 49: Impact of HP rate increase from 3.50% to 3.75% on yearly instalment Old scenario @ 3.50% p.a.

Year 1 2 3 4 5 Total Interest Tenure

3.50% 5 4,378 3,414 2,450 1,486 522 12,250

Principal 1 2 3 4 5 Total 70,000 12,072 13,036 14,000 14,964 15,928 70,000

Instalments 1 2 3 4 5 Total 1,371 16,450 16,450 16,450 16,450 16,450 82,250

New scenario @ 3.75% p.a.Year 1 2 3 4 5 Total

Interest Tenure 3.75% 5 4,691 3,658 2,625 1,592 559 13,125

Principal 1 2 3 4 5 Total 70,000 11,934 12,967 14,000 15,033 16,066 70,000

Instalments 1 2 3 4 5 Total 1,385 16,625 16,625 16,625 16,625 16,625 83,125

Increase /(Decrease) in yearly instalment (RM)Year 1 2 3 4 5 Total

175 175 175 175 175 875

SOURCES: CIMB

5.5 Consumer sentiment will affect decisions to buy cars The demand for vehicles is quite closely correlated with economic conditions via consumer sentiment. When times are bad, potential buyers are generally less willing to commit to big-ticket items. While the current state of the country’s public transport makes it almost a necessity to own cars for some, buyers may choose to defer purchases until the global economy recovers and job security improves. If conditions in the eurozone deteriorate more rapidly than expected, there could be sharp declines in the global asset markets and risk appetite. The spillover would dampen consumer sentiment and affect the willingness to buy cars.

AUTOS June 26, 2012

30

Figure 50: Correlation between auto industry index and vehicle sales

Figure 51: Correlation between consumer sentiment index and vehicle sales

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

0

20

40

60

80

100

120

140

160

180

Vehicle sales (LHS) MIER auto industry index (RHS)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

0

20

40

60

80

100

120

140

Vehicle sales (LHS) Consumer sentiment index (RHS)

SOURCES: CIMB, MIER SOURCES: CIMB, MIER

5.6 Lowering of trade and non-trade barriers welcome more competition

Since the birth of the national car project 25 years ago, the Malaysian auto industry has been highly protected. Compared to neighbouring countries, like Thailand, Malaysia’s auto industry is characterised by high trade and non-trade barriers that shield both the national and non-national auto players, which have invested substantially in car manufacturing and assembling operations in the country. Gradual liberalisation via the lowering of trade and non-trade barriers would mean intensifying competition for local car manufacturers and assemblers as the country becomes more open to investments from foreign car companies and imports of cars and car parts into the country.

6. VALUATION AND RECOMMENDATION 6.1 Maintain OVERWEIGHT on Malaysian autos Thailand, Indonesia and Malaysia are the major demand centres for motorcars, thanks to rapid economic growth, accommodative government policies, an expanding middle-income group and rising disposable income, among other factors. Although all three countries have gained significant mileage in the auto sector in terms of the development of the industry, Indonesia’s and Thailand’s growth prospects, based on the opportunities for exports and vehicle penetration rates, seem to trump Malaysia’s. Still, the demand drivers for the Malaysian auto sector are intact. Favourable demographics in the form of a large working population and rising middle-income group, still-firm economic outlook, relatively low cost of vehicle ownership, low interest rate environment, the country’s dismal public transportation system and new model launches are among factors that should continue to support domestic buying interest. Further out, full liberalisation under AFTA and AEC in 2015 should enhance auto players’ export opportunities.

This year, we are projecting total industry volume to scale a new high of 628,022 units. This implies a 4.7% growth from the 599,877 units recorded in the disaster-stricken 2010 and is 2.1% above the Malaysian Automotive Association’s (MAA) projection of 615,000 units. Jan-May sales totalled 244,579 units. Sales in the remaining seven months of the year have to grow by about 11% yoy to hit our sales projection. We think this is achievable as we expect 1) vehicle supply to recover to meet pent-up demand, 2) new model launches to spur buying interest, and 3) banks to adapt to the tighter credit guidelines over time.

AUTOS June 26, 2012

31

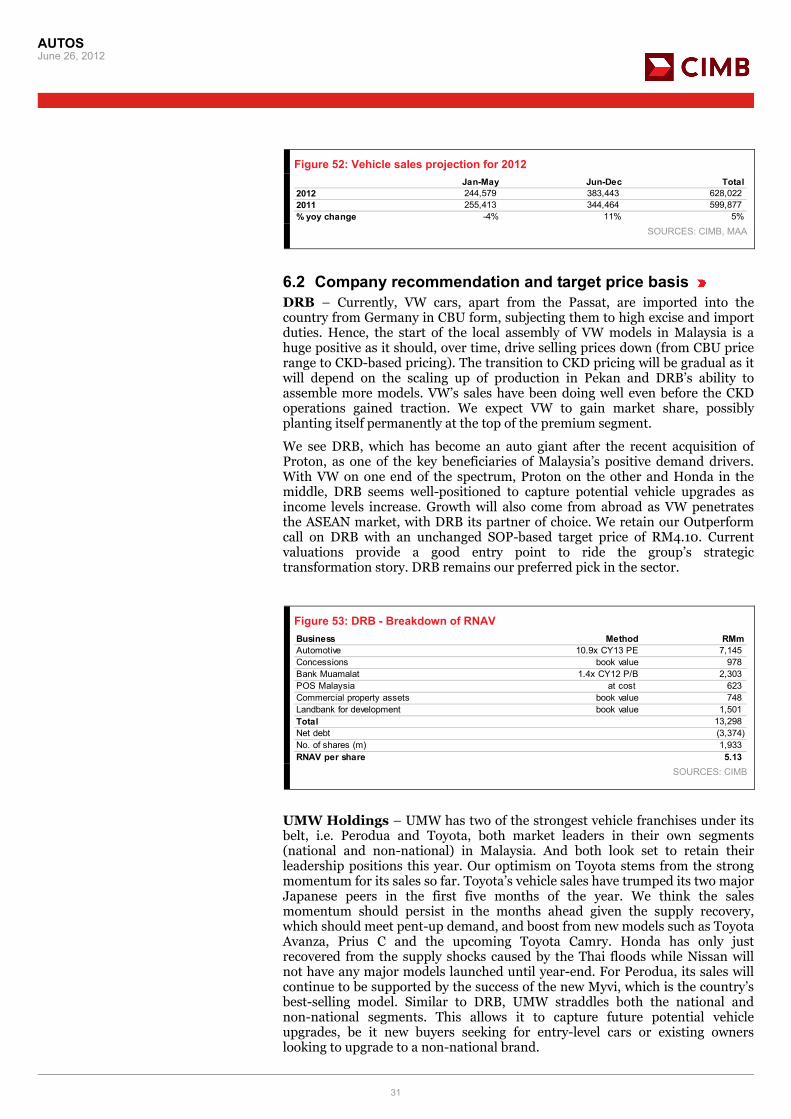

Figure 52: Vehicle sales projection for 2012 Jan-May Jun-Dec Total

2012 244,579 383,443 628,022 2011 255,413 344,464 599,877 % yoy change -4% 11% 5%

SOURCES: CIMB, MAA

6.2 Company recommendation and target price basis DRB – Currently, VW cars, apart from the Passat, are imported into the country from Germany in CBU form, subjecting them to high excise and import duties. Hence, the start of the local assembly of VW models in Malaysia is a huge positive as it should, over time, drive selling prices down (from CBU price range to CKD-based pricing). The transition to CKD pricing will be gradual as it will depend on the scaling up of production in Pekan and DRB’s ability to assemble more models. VW’s sales have been doing well even before the CKD operations gained traction. We expect VW to gain market share, possibly planting itself permanently at the top of the premium segment.

We see DRB, which has become an auto giant after the recent acquisition of Proton, as one of the key beneficiaries of Malaysia’s positive demand drivers. With VW on one end of the spectrum, Proton on the other and Honda in the middle, DRB seems well-positioned to capture potential vehicle upgrades as income levels increase. Growth will also come from abroad as VW penetrates the ASEAN market, with DRB its partner of choice. We retain our Outperform call on DRB with an unchanged SOP-based target price of RM4.10. Current valuations provide a good entry point to ride the group’s strategic transformation story. DRB remains our preferred pick in the sector.

Figure 53: DRB - Breakdown of RNAV Business Method RMmAutomotive 10.9x CY13 PE 7,145 Concessions book value 978 Bank Muamalat 1.4x CY12 P/B 2,303 POS Malaysia at cost 623 Commercial property assets book value 748 Landbank for development book value 1,501 Total 13,298 Net debt (3,374) No. of shares (m) 1,933 RNAV per share 5.13

SOURCES: CIMB

UMW Holdings – UMW has two of the strongest vehicle franchises under its belt, i.e. Perodua and Toyota, both market leaders in their own segments (national and non-national) in Malaysia. And both look set to retain their leadership positions this year. Our optimism on Toyota stems from the strong momentum for its sales so far. Toyota’s vehicle sales have trumped its two major Japanese peers in the first five months of the year. We think the sales momentum should persist in the months ahead given the supply recovery, which should meet pent-up demand, and boost from new models such as Toyota Avanza, Prius C and the upcoming Toyota Camry. Honda has only just recovered from the supply shocks caused by the Thai floods while Nissan will not have any major models launched until year-end. For Perodua, its sales will continue to be supported by the success of the new Myvi, which is the country’s best-selling model. Similar to DRB, UMW straddles both the national and non-national segments. This allows it to capture future potential vehicle upgrades, be it new buyers seeking for entry-level cars or existing owners looking to upgrade to a non-national brand.

AUTOS June 26, 2012

32

Export opportunities for UMW Toyota do not look as compelling as it does for DRB or Tan Chong. Unlike DRB, which will play a role in driving VW’s ASEAN aspirations, or Tan Chong, which is Nissan’s vehicle in the growing Indochina, UMW Toyota’s move abroad will be limited by its principal Toyota Motor Corp’s direct presence in the key automotive markets, such as Thailand and Indonesia. But we think UMW will stand to benefit if Malaysia is made the hub for the production of selected models for onward exports to other countries in the region.

We are positive on UMW Toyota’s launch of hybrid vehicles like the Prius C, Prius and the Lexus CT200h as they gave it a headstart in terms of the offering of eco-friendly vehicles in the country. As the Malaysian government steps up on the development of the green industry in the country, more incentives to promote green technology can be expected, which will ultimately benefit first-movers like UMW Toyota.

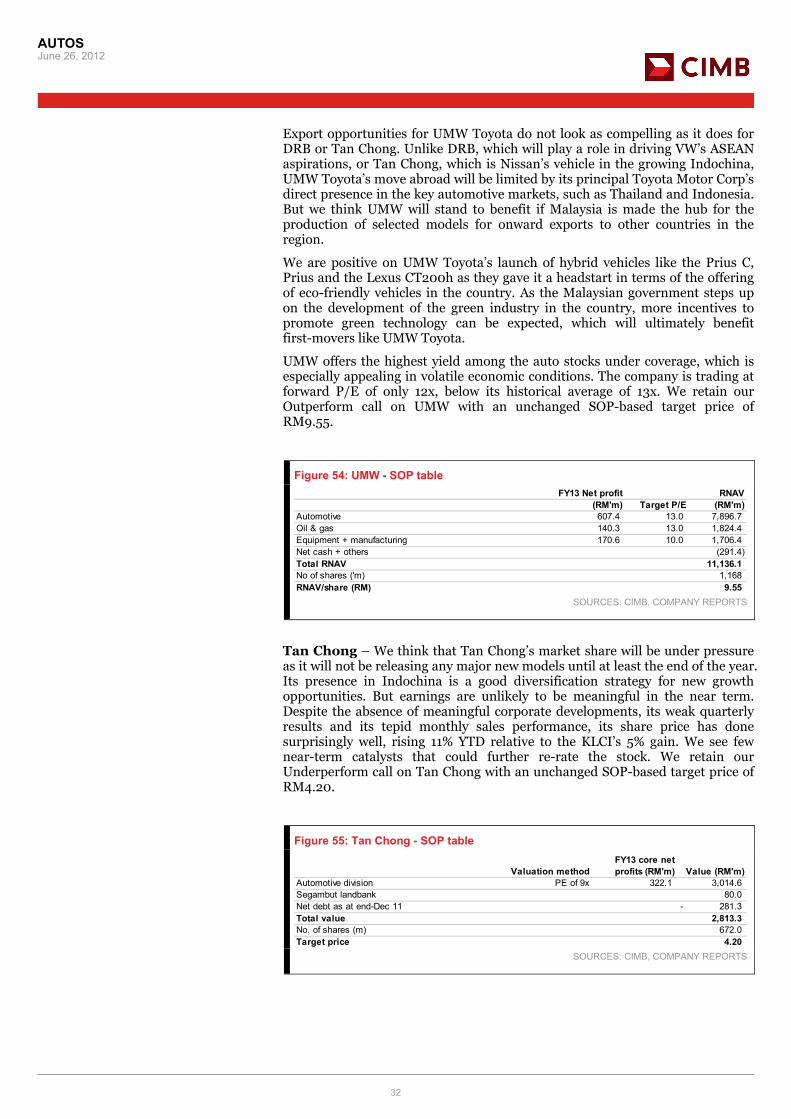

UMW offers the highest yield among the auto stocks under coverage, which is especially appealing in volatile economic conditions. The company is trading at forward P/E of only 12x, below its historical average of 13x. We retain our Outperform call on UMW with an unchanged SOP-based target price of RM9.55.

Figure 54: UMW - SOP table FY13 Net profit RNAV

(RM'm) Target P/E (RM'm)Automotive 607.4 13.0 7,896.7Oil & gas 140.3 13.0 1,824.4Equipment + manufacturing 170.6 10.0 1,706.4Net cash + others (291.4)Total RNAV 11,136.1No of shares ('m) 1,168RNAV/share (RM) 9.55

SOURCES: CIMB, COMPANY REPORTS