you can't forget the patient— in patient safety

TRANSCRIPT

Inside Medical LiabilityA P I A A P U B L I C A T I O N F O R T H E M E D I C A L P R O F E S S I O N A L L I A B I L I T Y C O M M U N I T Y

2 0 1 4 T H I R D Q U A R T E R W W W . P I A A . U S

ERM for MPLA N D

You Can’t Forget the Patient—

in Patient Safety

Covers 3Q 2014 FINAL USE _Layout 1 8/8/14 11:43 AM Page 2

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:00 PM Page 1

PIAA polls its members on a regular basis, to keep up to date on

the issues that matter most to the community. In our most

recent survey, an old, but perennially important, topic was top

of mind for many PIAA members: patient safety.

Patient safety has long been a central concern for everyone who

is part of the Association. In fact, back in the 1970s, the founding

companies that joined together to launch PIAA broke new ground, in

many areas, when it came to developing a safer environ-

ment for healthcare. Innovative risk management and

loss prevention initiatives comprised the foundation of

these efforts, along with the analysis of MPL claims and

cause-of-loss data.

Today, in light of the ongoing transformation of the

healthcare system, and the intense focus on reducing the

cost of healthcare while at the same time increasing its

quality, patient welfare is arguably more central than

ever for those in healthcare and in the MPL arena. The interests of

healthcare professionals and their patients are squarely aligned when it

comes to safety. Nobody in the chain of care is more focused on a pos-

itive outcome than the healthcare professional. So, in this instance, the

interests of patients, healthcare professionals, and the MPL community

truly are in sync.

For this reason, in this issue of Inside Medical Liability, our cover

story examines the top ten patient safety concerns for healthcare

organizations. It then goes on to provide details about three of

these—care coordination, reporting test results, and drug shortages.

The article can help healthcare organizations in determining where

they can most usefully focus their patient safety efforts, and will assist

them in selecting priorities and devising corrective action plans that

can minimize adverse outcomes. You will also hear from two of your

peers—PIAA member companies that offer some illustrative stories

about what they’ve done to advance their progress in patient safety.

These are, of course, only two instances of the contributions that

PIAA members have made to a safer healthcare environment. We hope

that this discussion will serve as a springboard for a fruitful dialogue

and the sharing of new ideas on patient safety. We urge you to keep us

informed of your progress in this area.

It goes without saying that your feedback is the single most

important driver in all that we do at PIAA. In the latest

member survey, you told us about what you anticipate

will be your most daunting challenges over the next

three years: for example, the evolving healthcare land-

scape, the shifting MPL marketplace, operating and

defense costs, and state regulation and legislation.

You also told us what we are doing best at this

point: providing unique MPL data, leadership of the

MPL community, offering exceptional continuing educa-

tion for MPL professionals, and providing networking and relationship

building opportunities, among others.

In addition, and perhaps most important, you helped us under-

stand how we can assist you with your business, both now and in the

future: we should sustain our focus on patient safety, provide cutting-

edge information on loss prevention and risk management, expand

our data collection and research capabilities, favorably influence legis-

lators and public policy makers, and serve as a connecting point for

the larger MPL community, to name a few.

We will keep all of this clearly in mind, in the months ahead, as

we ensure that PIAA serves your needs to the best of our ability—and

provides even greater value for each PIAA member. As your trade

association, we endeavor to see for you, hear for you, and represent you

whenever a need arises. Nothing is more important to us than meet-

ing your needs.

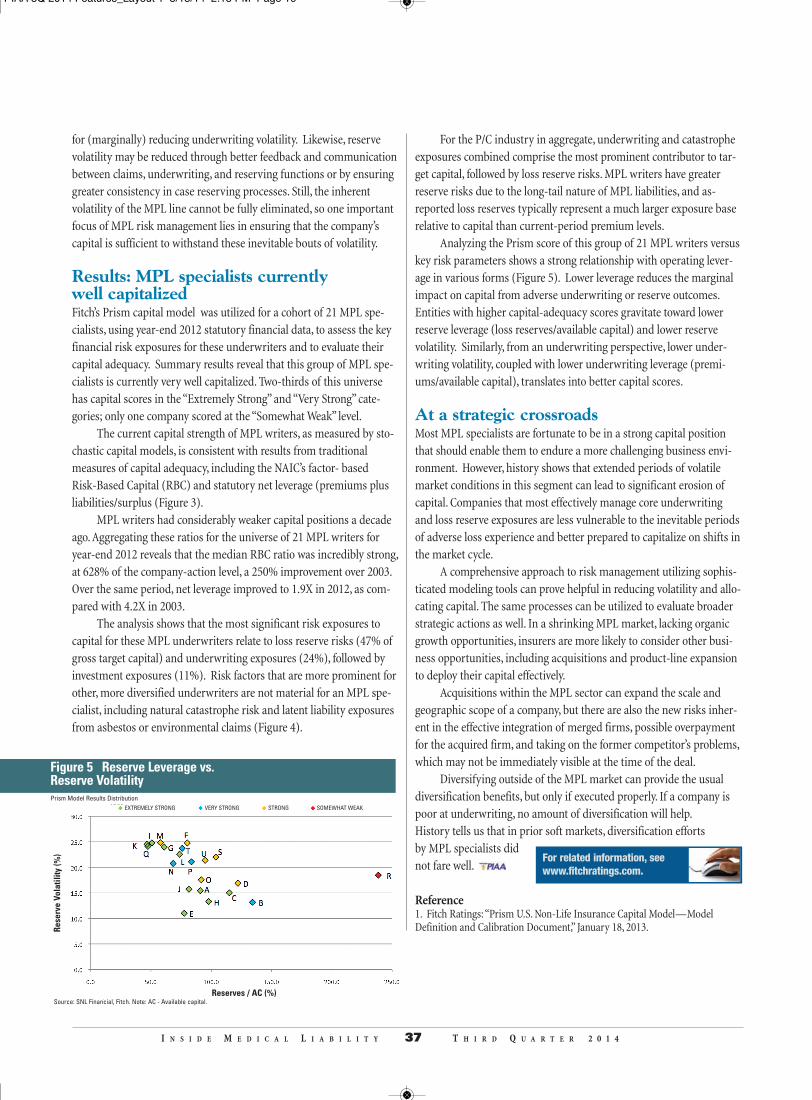

Patient safety has longbeen a central concern foreveryone who is part of theAssociation.

PATIENT SAFETY AND YOUR NEEDS—ALWAYS MOVING FORWARD

P R E S I D E N T , B R I A N A T C H I N S O N

P E R S P E C T I V E

I N S I D E M E D I C A L L I A B I L I T Y 1 T H I R D Q U A R T E R 2 0 1 4

“”

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:01 PM Page 2

F e a t u r e s22 Cover Story: Using PSO Data to Identify the Leading Patient

Safety Concerns—and Lessons LearnedBy Cynthia Wallace, CPHRM, and Karen P. Zimmer, MD, MPH, FAAP

28 Feature: The ‘Seven Deadly Sins’ of Large-Scale IT Project Management By Martin Lippiett

31 Feature: Transparency: Changing the World We Live In, for the BetterBy Kevin Bingham, Mark Bethke, Greg Chrin, and Josh Merck

34 Feature: Enterprise Risk Management for MPL SpecialistsBy Gerry Glombicki

S p e c i a l S e c t i o n

54 2014 PIAA Medical Liability Conference

D e p a r t m e n t s

10 On MarketingThe Measure of Your Brand By David Kinard

14 Legislative Update

16 Case and CommentThe Dental Professional Review and Evaluation Program: Lessons and Implications for Professional License Defense By Thomas Bright, Esq., and Vincent Dunn, Esq.

39 Alternatives for RisksQ&A with Nathan Reznicek, Assurance Partners

43 Insights on AccountingLoss Reserves: The IRS’ Kryptonite or Gold Mine?By Brandy Vannoy and Derek Freihaut

47 International PerspectiveApproaching Risk in the Information AgeBy Dr. Thom Petty

50 By the NumbersA Pause in TimeBy Richard B. Lord and Stephen J. Koca

60 Last Word

U p F r o n t1 Perspective

4 Events & Calendar

6 Observer

8 PIAA DSP Data SnapshotMost Prevalent and Expensive Outcomes

A PIAA PUBLICATION FOR THE MEDICAL PROFESSIONALLIABILITY COMMUNITY

2014 THIRD QUARTER

“By collecting data from many providers,PSOs can spot problems and trends thatan individual organization, with a limitedpool of data, may be unable to detect.”—Cover story

I N S I D E M E D I C A L L I A B I L I T Y 2 T H I R D Q U A R T E R 2 0 1 4

28

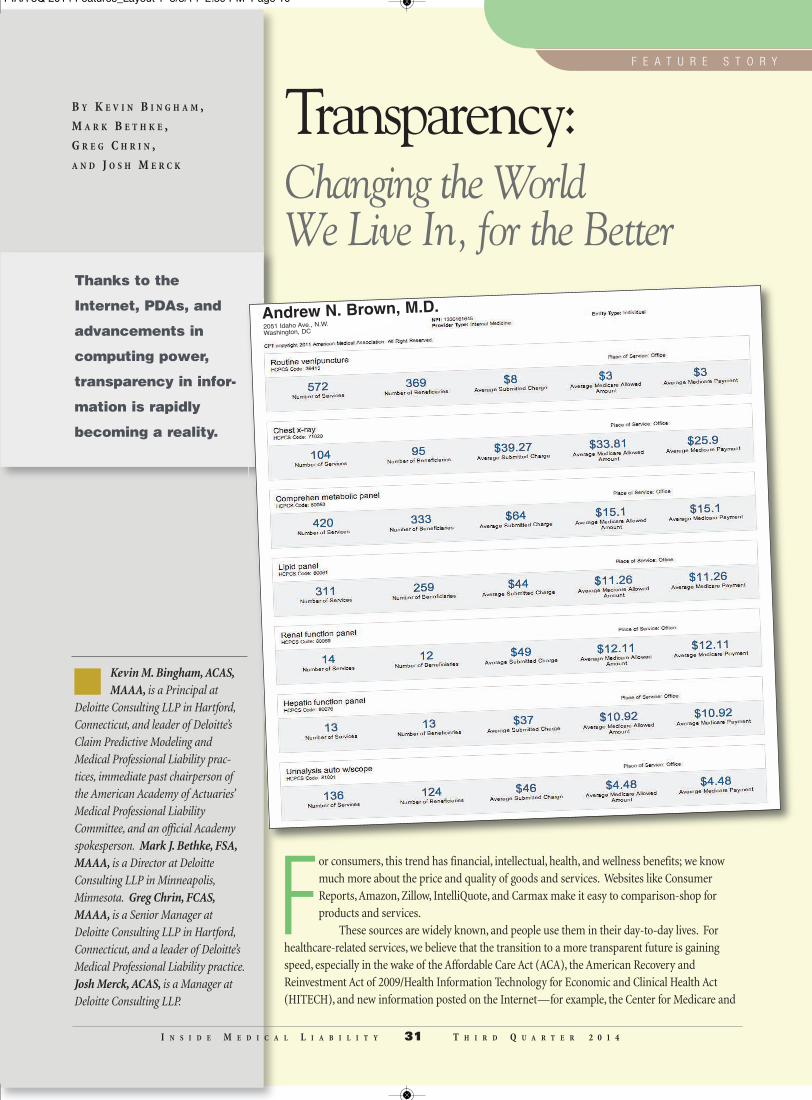

Andrew N. Brown, M.D.2051 Idaho Ave., N.W.Washington, DC

31

34

Inside Medical Liability

22

contents

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:02 PM Page 3

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:02 PM Page 4

■ 2014 Claims and Patient Safety/Risk Management WorkshopSessions on high-risk situations in the ER, and successful courtroomstrategies

“Common Complaints/Catastrophic Outcomes”This is an essential topic for managing risk inevery MPL enterprise: how to identify the com-mon patient complaints in the ER that may signala high-risk situation. Michael J. Gerardi, MD,FAAP, FACEP, President, American College ofEmergency Physicians, will discuss what can gowrong in responding to symptoms such as abdom-inal pain, back pain, vomiting, headache, rash,

syncope and more. He will then explain how risk management canlower, or even prevent, catastrophic outcomes in the ER.

“In the Courtroom, but Outside the Box”You can also learn about the occasions when a successful outcome in thecourtroom requires something novel—a nontraditional technique orstrategy. In this session two experts will tell you when to use these, andhow to deploy them to maximum effect, based on actual cases. TracieM. Dorfman, Esq., Associate, Hancock, Daniel, Johnson & Nagle, P.C.and Richard L. Nagle, Esq., Director, Hancock, Daniel, Johnson &Nagle, P.C., will help you become more innovative in finding newapproaches to persuading a jury.

■ 2014 Underwriting Workshop Sessions on advanced-practice nurses,and use of the da Vinci robot inhealthcare

“The Expanding Role of Advanced-Practice Nurses” More of the tasks that were once restricted tophysicians are now done by advanced-practicenurses. This raises important questions for MPLentities. Melissa Joy Roberts, JD, MSN, FNPBC,Associate Dean, UMKC School of Nursing andHealth Studies, will discuss the crucial issueswith advanced-practice nursing for MPL. Forexample, how will states modify their scope-of-practice restrictions in response to physician shortages? As standalonenurse practitioner practices proliferate, what impact will that have onMPL exposures and rates?

“The da Vinci Robot: The Rest of the Story”Physicians and patients are bombarded with advertisements promotingnew medical technology like the da Vinci “robot.” In light of the volumeof these procedures, it is time to examine their actual impact for MPL.Barry N. Gardiner, MD, will provide full coverage of this complex topic,including a roster of the surgical specialties that now use robotic surgery,rates of complications, and product defects. He will provide an insider’sview of the strategies that plaintiff ’s attorneys use in claims of allegedharm from robot-assisted surgical procedures.

EVENTS & CALENDAR

C O M I N G A T T R A C T I O N S

I N S I D E M E D I C A L L I A B I L I T Y 4 T H I R D Q U A R T E R 2 0 1 4

September 10–12, 2014THRF WorkshopFairmont Olympic HotelSeattle, WA

September 30–October 1, 2014Introduction to MPLIWorkshopOmni San Diego HotelSan Diego, CA

October 1–3, 2014Underwriting WorkshopOmni San Diego HotelSan Diego, CA

October 8–10, 2014International ConferenceRenaissance Hotel AmsterdamAmsterdam, the Netherlands

October 16–17, 2014Corporate CounselWorkshopFairmont Hotel VancouverVancouver, Canada

November 5–7, 2014Claims/Risk ManagementWorkshopBaltimore Marriott Waterfront HotelBaltimore, MD

March 11–14, 2015CEO/COO MeetingThe Westin Kierland Resort & SpaScottsdale, AZ

March 12–15, 2015Board GovernanceRoundtableThe Westin Kierland Resort & SpaScottsdale, AZ

April 8–10, 2015Marketing WorkshopThe Ritz CarltonCharlotte, NC

April 8–10, 2015Dental WorkshopThe Ritz CarltonCharlotte, NC

May 13, 2015Leadership CampCaesars PalaceLas Vegas, NV

May 13–15, 2015Medical Liability ConferenceCaesars PalaceLas Vegas, NV

MICHAEL J. GERARDI MELISSA JOY ROBERTS

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:03 PM Page 5

Join the many medical professional liability insurance carriers, captives, and risk retention groups who rely on ECRI Institute for unbiased advice and proven risk reduction strategies. Healthcare professionals across the continuum of care refer to ECRI Institute as the “gold standard” for risk management and patient safety resources. Partner with a trusted healthcare research agency whose sole mission is to improve patient care.

Let ECRI Institute be your source for:

Online guidance and tools

Evidence-based best practices

Patient Safety Organization reporting and federal protection

Risk assessment services

Online CME and webinars

Healthcare technology decision support

Access to our 450-person interdisciplinary staff

Make claims reduction more than wishful thinking.

Jump start your risk management and patient safety initiatives today.

Visit www.ecri.org/insurance, e-mail [email protected], or call (610) 825-6000, ext. 5145.

MS14062

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:03 PM Page 6

How can you not love this one? Robotsthat shoot ultraviolet light onto roomsurfaces proved sufficiently powerfulto drive down rates of the hospital-

acquired infections (HAIs) that are caused bymultidrug-resistant organisms or Clostridiumdifficile. The study confirming this happy factwas published in the venerable AmericanJournal of Infection Control.

Ultraviolet disinfection (UVD) technologyuses mercury bulb devices or pulsed-xenonbulbs. The pulsed-xenon devices were firstused in May 2011, at a 643-bed New York hos-pital. Teams from several departments—infec-tion prevention, environmental services, andperformance management—monitored theresults weekly.

More than 11,000 applications of UVDbetween July 2011 and April 2013 resulted ina 20% decrease in overall HAIs related to mul-tidrug-resistant organisms, despite the factthat the researchers had missed nearly a quar-ter of the possible opportunities to use thetechnology.

Adult inpatient rooms at the hospital areroutinely cleaned with sodium hypochlorite0.55% disinfectants, and pediatric rooms arecleaned with a quaternary ammonium com-pound. During the study period, UVD wasadded to the regimen.

Study lead author Janet P. Haas, PhD,RN, director of infection prevention and controlat Westchester Medical Center in Valhalla,New York, says that because UVD seems to

work everywhere else in the hospital, it couldplausibly do the same in operating rooms.However, she warns that the current clinicalevidence for using UVD in the operating roomis less compelling; more research is needed to fully assess how effective it might be in surgical-care areas.

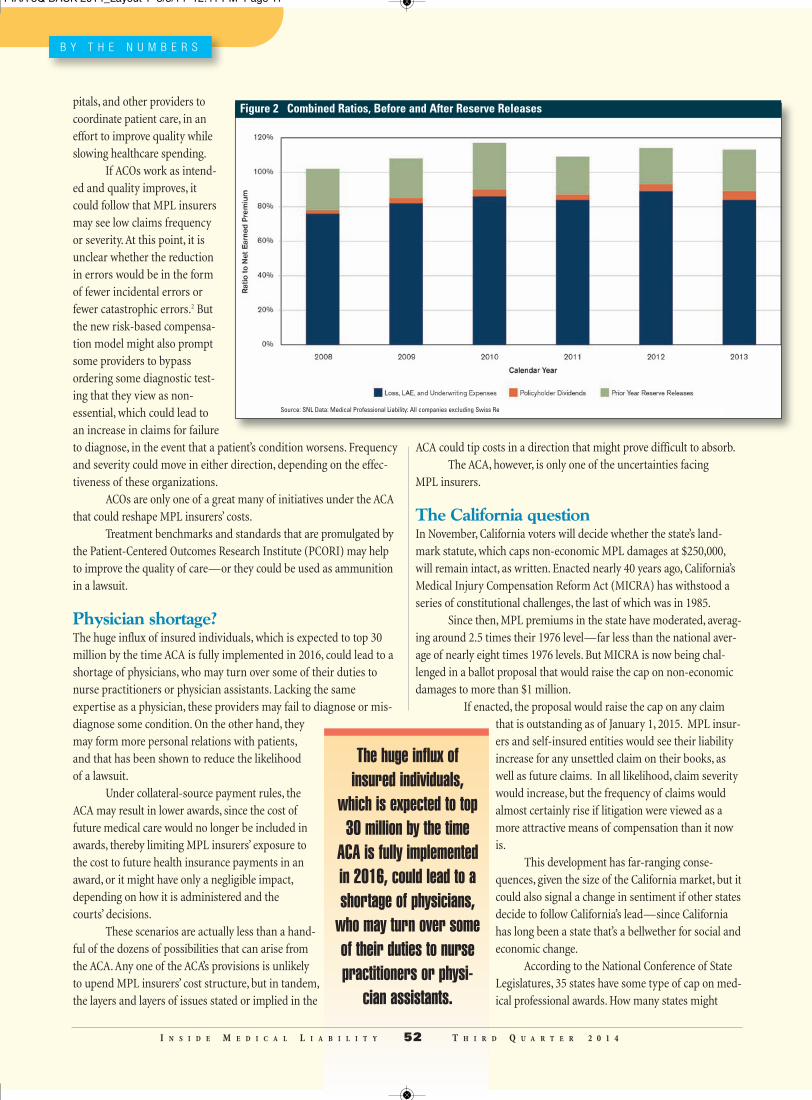

Despite their challenging financial circumstances, reinsurers havecontinued to report attractive results in recent quarters. Lowcatastrophe losses and positive reserve developments have helped.But can this be sustained? Not surprisingly, opinions differ.

The market, at any rate, has weighed in on the matter: reinsuranceshare prices have begun to slip as the abundant levels of traditional andalternative capital have exerted pressure on reinsurance rates.

Recently, presenters at a seminar sponsored by the CasualtyActuarial Society, in New York, offered their take on the relative extent ofdisruption in the reinsurance market resulting from the entry of newcapital. Two of the analysts, Alan Zimmerman, managing director of

Assured Research, and Matthew Mosher,SVP rating services at A.M. Best, suggestedthat the best option was to simply moveon—to explore new opportunities. Theynoted that both insurers and reinsurers needto work hard to remain relevant—even ifthat means abandoning segments of the

market to the new capital. There was a dissenting opinion from MeyerShields, of Keefe, Bruyette and Woods. He suggested less drastic action,advising that insurers and reinsurers investigate the possibility of prof-itable niches within the affected market segments.

But it was Zimmerman who came up with the most memorableimage for the market. He depicted the stark difference between the pre-Hurricane Andrew situation and today. Reinsurers in the prior era werelike “huge, impregnable castles,” he said, with a broad base and under-writing depth. Today, he suggested, they seem more like “mobile homes,”with a greater number than ever before, and more competition.

Reinsurance: From Impregnable Castles to Mobile Homes

Source: Artemis, June 24, 2013

N O T A B L E N E W S A N D T R E N D S

I N S I D E M E D I C A L L I A B I L I T Y 6 T H I R D Q U A R T E R 2 0 1 4

Source: American Journal of Infection Control,June 2014

OBSERVERUV Light Lowers Hospital-Acquired Infections

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:05 PM Page 7

Tacking against the headwinds of general consensus, University ofCincinnati College of Law professor Jim O’Reilly believes that theAffordable Care Act will actually transform MPL litigation into an uphillbattle for the plaintiff ’s attorney. When the huge influx of new patients is

fully in effect, O’Reilly says, we can expect to see a corresponding proliferation oftelemedicine, as well as grocery and convenience store clinics that are staffed bynurses, not doctors.

“There will be errors and there will be compensation,” O’Reilly notes, “but itwon’t be anything like what we’ve seen where patients win millions of dollars.”Speaking as a professor of future attorneys, he cautions, “For lawyers to better servetheir patients, they need to understand that the system has changed. If they don’tknow about it, their client loses.”

Overall, O’Reilly predicts, there will be fewer and fewer cases where a patientgoes to court directly against his family doctor.

The other big factor in the possible decline of MPLclaims, he says, is the rise of large hospital-basedaccountable care organizations (ACOs). The thoughtof taking on a mega-hospitals cadre of lawyers maywell be intimidating to a plaintiff ’s attorney contem-plating whether or not to take on a particular case.

The way out of this quandary? Well, this isAmerica, where the answers to so many problemsare revealed in a steady stream of brand-new pub-lications. O’Reilly offers his: The New MedicalMalpractice. Described by his employer, theUniversity of Cincinnati, as “groundbreaking,” thebook will supposedly help lawyers negotiate whatO’Reilly sees as a whole new healthcare scenario,with a “more diverse set of defendants and a muchmore complicated decision for compensation.”

Department of Upbeat Predictions: In-Store Clinics, Telemedicine—and the Death of Windfall MPL Judgments

Quiz Time! Students’ Concernsre MPL and Defensive Medicine

Compliance with hand hygiene is animportant goal in infection preven-tion. And yet the hand-to-handtransfer of infectious bacteria is

still a common public health hazard. Asdraconian as it sounds, some clinicians arepushing to prohibit the familiar greeting, thehandshake, between providers and patients.

According to a recent proposal published online in JAMA,hospitals, surgical centers, and office practices would be designated“handshake-free zones.” The authors, clinicians from the DavidGeffen School of Medicine in Los Angeles, propose some possiblesubstitutes: open-handed waves, bowed heads, hands over the heart,and yoga-style “Namaste” gestures.

There is actually some research toback up the proposal. Last year,researchers from the University of WestVirginia compared the infection-transferpotential of fist bumps vs. handshakes, andfound that the fist bumps were less likely to pass on infecting agents.

The UCLA clinicians are quite insistent about the impor-tance of the no-handshake policy. “Removing the handshake fromthe healthcare setting may ultimately become recognized as animportant way to protect the health of patients and caregivers,” they say, “rather than a personal insult to whoever [sic] refusedanother’s hand.”

Arecent report in the Western Journal of EmergencyMedicine (William F. Johnson et al., Hackensack UniversityMedical Center) noted the responses of third-year medicalstudents to a series of statements about defensive medi-

cine and their related medical liability concerns (MLC).The study employed a five-point Likert scale, and their

responses were tabulated as percentages, with a 95% confidenceinterval. Now it’s your turn. Match the statements in the first sec-tion with your guesses on the percentage of students who agreed,in the section below. The answers appear at the end of this article.The statements1. I rarely worry about being sued ____2. The faculty are concerned about MPL ____3. The faculty teach defensive medicine ____4. My satisfaction as a doctor will be decreased by MLC

and lawsuits ____5. My choice of medical specialty will be influenced by MLC ____6. My enjoyment of learning medicine is lessened by MLC ____7. I worry about practicing and learning procedures because

of MLC ____Percentage of students who agreed

I N S I D E M E D I C A L L I A B I L I T Y 7 T H I R D Q U A R T E R 2 0 1 4

Let’s Shake on It: Ban the Handshake

Source: Outpatient Surgery magazine, May 27, 2014

Source: Western Journal of Emergency Medicine, May 2014. Source: Medical Xpress, May 22, 2014

a. 51.0%b. 32.4%c. 21.6%d. 85.3%

e. 16.7%f. 55.9%g. 23.5%

Answers: 1, d; 2, f; 3, b; 4, a; 5, c; 6, g; 7, e.

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:05 PM Page 8

F O R E S I G H T

In conjunction with the cover story on page 22, Using PSO Data to Identify the Leading Patient

Safety Concerns—and Lessons Learned, ECRI Institute ranked “retained devices and unretrieved

fragments” as number seven on its 2014 Top 10 Patient Safety Concerns for Healthcare

Organizations. A review of closed claims in the PIAA Data Sharing Project from 2008–2012

revealed “foreign body, surgical, left in patient during a procedure” as the fourth most prevalent

patient outcome. This outcome is similar to “retained devices and unretrieved fragments” as iden-

tified in the previously named ECRI publication and also in ECRI’s 2014 Top 10 Health Technology

Hazards. Among these claims, 28% totaled more than $20 million in indemnity payments. The

claims had an average indemnity payment of $85,427.

I N S I D E M E D I C A L L I A B I L I T Y 8 S E C O N D Q U A R T E R 2 0 1 4

MPL DATA—MOSTPREVALENT AND EXPENSIVEOUTCOMES

P I A A D S P

When compared to the most expensive outcomes, “foreign body, surgical, left in patient during a procedure” was not among the top five and was

less than 1% of the total indemnity ($8.2 million) for all claims paid between 2008 and 2012; however, it’s critical to consider these claims as

they impact areas for improvement in patient safety.

The PIAA Data Sharing Project provides information on claim trends for the most recent ten-year period and other timeframes.

For more information, please visit the PIAA website at www.piaa.us.

MOST PREVALENT RESULTINGMEDICAL CONDITIONS

Closed Paid % Paid-to- Total AverageClaims Claims Closed Indemnity Indemnity

2,814 726 25.8 $252,065,722 $347,198

1,021 200 19.6 $54,810,736 $274,054

952 120 12.6 $14,286,539 $119,054

880 243 27.6 $20,758,861 $85,427

863 285 33.0 $132,015,648 $463,213

Cardiac/cardiorespiratory arrest

Postoperative infection

Emotional distress only

Foreign body, surgical, left in patient during a procedure

Breast cancer

MOST EXPENSIVE RESULTINGMEDICAL CONDITIONS

Closed Paid % Paid-to- Total AverageClaims Claims Closed Indemnity Indemnity

2,814 726 25.8 $252,065,722 $347,198

607 233 38.4 $172,109,686 $738.668

590 246 41.7 $132,480,940 $538,540

863 285 33.0 $132,015,648 $463,213

650 231 35.5 $96,639,029 $418,351

Cardiac/cardiorespiratory arrest

Brain damaged infant

Birth trauma

Breast cancer

Acute myocardial infarction

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:06 PM Page 9

Wells Fargo Advisors, LLC, Member SIPC, is a registered broker-dealer and a separate non-bank affiliate of Wells Fargo & Company. ©2013 Wells Fargo Advisors, LLC 0211-1214A 03/13

at the top of your game requires focus, foresight and the ability to act

your

Joe Montgomery, Judy Halstead, Christine Stiles, TC Wilson, Bryce Lee,

Robin Wilcox, Cathleen Duke, Kathryn Jenkins, Brian Moore, Loughan Campbell,

Karen Hawkridge, Evan Francks, Vicki Smith and Brad Stewart

428 McLaws Circle, Suite 100 Williamsburg, Virginia 23185757-220-1782 888-465-8422

of Wells Fargo Advisors

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:06 PM Page 10

In a nutshell, AAU looks at these:Awareness. The percentage of your targetaudience (customers or potential customers)who recognize your organization or its brand,either aided or unaided. It also measures howmuch knowledge the target audience hasabout your organization’s products and serv-ices. So, not only do you look to see if theyknow about you, you measure what theyknow about you.

Attitudes. This is a combination of what yourtarget audience believes and how strongly theybelieve it. Measurements cover the target audi-ence’s perceptions of quality, effectiveness, andvalue as they relate to your organization, andalso cover intention to make a purchase orbecome involved with your cause.

Usage. This is simply the target audience’s self-reported behavior, as it relates to yourorganization.

So, how do you get this type of informa-tion? Here are two ideas.

But first, a caveat: make sure you specificallyidentify the target audience you want to meas-ure. I can’t overemphasize the need for specifici-ty in this step. Saying you want to measureawareness among the physicians will not giveyou actionable data, because your organizationprobably doesn’t have the marketing budget forthat large a study. Think specifically about the

If you ask 25 marketing professionals whata brand is, you’ll likely get 25 differentanswers. The best definition of a brand I’veheard is this: “a promise held in the mind

of the consumer, of an expected, consistent,and personal experience from a product, per-son, or organization.” But, despite the vast vol-ume of words written about brands (Amazonhas more than 5,000 books on the subject), itseems that many marketers today find it chal-lenging to define their brand, let alone meas-ure its impact.

The first brands were literally justthat—names of companies burned intopacking barrels, so they could be identifiedduring the loading and unloading of ships inport. Some have said that the first brand totruly take root was that of the NationalBiscuit Company, which burned its abbreviat-ed name—NABISCO—into these barrels to sort theirs from the other cargo morequickly.

More recently, however, branding funda-mentally changed and became a marketingstaple in the early 1980s, when Jack Trout andAl Ries published their seminal book,Positioning: The Battle for Your Mind. Thatsimple paperback redefined the role of brand-ing and put the business-customer relation-ship front and center in the purview of the

marketing department, thereby sparking awhole new series of efforts meant to createspecific associations and evoke positive feel-ings for brands in consumers’ minds.

The challengeThe challenge facing insurance marketerstoday is how to refresh our brands in a waythat keeps them out of the general commodi-ty market and viewed instead by the buyerand consumer as essential to their success.But how do you, as a marketer, know whatthat promise is—the one that is in the mindof the consumer? How do you unlock thepower of your brand, if that power isn’t fun-damentally yours to begin with?

The best place to start assessing yourbrand’s capabilities is with a simple metricdesigned to tell you how many people areaware of your brand, find out their attitudesabout it, and reveal their behaviors in regardto your brand.

Typically referred to as AAU (“aware-ness,” “attitudes,” and “usage”), this metric ismost useful when results are set against someform of comparator—that is, data from aprior term (e.g., year-over-year), differentmarkets (e.g., geographic or demographic), orinformation from your competitor(s). AnAAU metric by itself is meaningless, until youhave a pivot point from which to demonstratemovement. In that light, several data sets areessential for identifying valid trends andmovement in AAU.

O N M A R K E T I N G

B Y D A V I D K I N A R D

David Kinard is Vice President of BusinessDevelopment at Physicians Insurance A MutualCompany, Seattle, Washington.

I N S I D E M E D I C A L L I A B I L I T Y 10 T H I R D Q U A R T E R 2 0 1 4

The Measure ofYour Brand

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:06 PM Page 11

CREATE A WIN WHEN YOU CHOOSE THE IMPERIAL PFS INSTALLMENT SOLUTIONS PROGRAM

To find out more about the advantages of the Imperial PFS Installment Solutions Program, call:

For information on all other Imperial PFS programs, visit: ipfs.com

JACK MERRIMAN312.205.4838

DICK CRNKOVICH253.466.3583

JASON SANDERS312.205.4821

1. INSTALLMENT PLAN FLEXIBILITY/OPTIONS

• When a consumer finances a purchase, the focus is on the amount down and the monthly payment.

• Offering more down payment and monthly installment options correlates to higher sales success for carriers.

• Add significant value to your product offerings by dramatically improving your billing options.

2. REDUCE BILLING & CUSTOMER SERVICE EXPENSES

• Collect premium payments UP FRONT.

• Eliminate the cost of billing and servicing deferred installments.

• Imperial PFS handles customer service calls.

3. FINANCIAL BENEFITS• Cash flow, liquidity and investment income all grow when

full premium is collected UP FRONT.

• No deferred installments means reduced operating expenses and credit risk.

HAPPIER CUSTOMERS.MORE PROFITS.

LESS RISK. THAT’S A WIN.

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:07 PM Page 12

finite group you want to study, for example,radiologists in Arizona.

You can use surveys conducted byresearch organizations that know how toreach your target audience. These might beonline, intercept, mail, or telephone surveysthat ask a series of questions. Use the sameset of questions over time, so you have datapoints to measure against.

Yes, you can administer a survey your-self if you’re measuring your internal con-stituents, but I’d still suggest that you employa true researcher to help with the set-up, col-lection, and analysis. They’re the experts atthis type of work—you’re likely not.

Or, you can scan discussion boards andsocial sites for first-hand comments andreviews. You can gather a wealth of knowledgejust by becoming a quiet participant in userforums and sites that are talking about you.Resist the urge to defend and comment. Justlisten and regularly monitor the tone of theposts, and the information shared.

Here are three kinds of data streams youmight get and what to do about them.

■ High awareness, high attitude, lowusage. In essence, these people are saying, “Iknow about you, but I do not think highly ofyou and will not engage with you.” How to respond. These people may notknow how to engage with your organization.Maybe your communications are unclearabout your educational opportunities. Maybeyour opportunities for learning are not whatthis audience wants. Go to them, find out howthey want to engage with you, and then createthe opportunities they’re looking for.

■ High awareness, low attitude, lowusage. These individuals may know aboutyou, but they don’t think highly of you andwill not engage with you. How to respond. These people should be leftalone; instead, you should focus your energieson higher-yield opportunities. Seriously, themore you try to engage this population, themore likely you are to annoy them and createnegative brand experiences.

■ Low awareness, low attitude, lowusage. Basically, these individuals don’t know

you exist, and therefore do not engage with you.How to respond. An awareness campaignmight move the members of this group intoanother, more fruitful category for your mar-keting efforts. But you’ll need to evaluate thecost of a program compelling enough to breakthrough the noise in the market space as youcompete for attention. Make sure you have aplan in place to engage with (or disengagefrom) these people once you do.

Bottom line For many insurers, the commonly acceptedidea is that if more people are aware of anorganization, there will be more prospectsand, ultimately, more buyers. These insurersequate awareness with moving the organiza-tion forward and enhancing success. Rather,the opportunity with branding is to createengagement, not awareness. Because if aware-ness were the name of the game, we’d all beshoveling pamphlets out of airplanes—from30,000 feet.

O N M A R K E T I N G

I N S I D E M E D I C A L L I A B I L I T Y 12 T H I R D Q U A R T E R 2 0 1 4

For related information, seewww.phyins.com.

CEN

EPL

Learn more about our actuarial services at www.oliverwyman.com/actuaries or email us at [email protected].

THE ACTUARIAL PRACTICE OFOLIVER WYMANOur more than 90 credentialed actuaries provide customized actuarial services and strategic insight, supporting healthcare clients as they strive to exceed their business objectives. Our exceptional client and employee retention exemplifies our commitment to relationships built on trust, responsiveness and clear communication.

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:07 PM Page 13

CENTER FOR QUALITY IMPROVEMENT IN RADIOLOGY INTERPRETATIONS

The Center for Quality Improvement

in Radiology Interpretations

offers two ways toimprove outcomes in

medical liability litigation

STRENGTHEN EXPERT TESTIMONYWe provide your expert with the litigation study hidden

among multiple control studies for interpretation

BLINDED CLAIMS ASSESSMENTHave your litigation study read and reported by 10 ABR certified radiologists in the course of their daily routine

■ ■ ■

Visit our website, www.VeritasReporting.comor contact us at [email protected]

ELIMINATE HINDSIGHT BIASPLAIN FILMS • CT • MRI • MAMMOGRAPHY • ULTRASOUND

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:07 PM Page 14

While regular readers of“Legislative Update” will recallprevious articles about PIAA’slobbying efforts in

Washington, D.C., that represents only a por-tion of what it takes to advance the PIAA agen-da and defend our companies from groups thatoppose your interests. To be truly effective,advocacy efforts must include three compo-nents—grassroots, lobbying, and politicalfundraising. Unless we engage all three, it isnearly impossible to achieve legislative successin the nation’s capital.

GrassrootsIn 2011, the Congressional ManagementFoundation (defined by them as an “organiza-tion founded to aid in management-relatedissues in Congress”) released a report on howwell various types of advocacy efforts are per-ceived on Capitol Hill. Congressional stafferswere nearly unanimous in saying that an in-per-son visit from a constituent had at least someinfluence over the Member of Congress.Compared with a meeting with a lobbyist (moreon that later), nearly six times as many stafferssaid the constituent visit had “a lot of positiveinfluence” on the legislator. Hill staffers also payattention when an individual represents the

views of multiple constituents. The same reportnoted that 96% of staffers said “contact from aconstituent who represents other constituents”has an influence on the Member’s views.

With this information in mind, onSeptember 15 and 16, PIAA will host a CapitolHill Advocacy Day. The event will feature anetworking dinner on the evening of the firstday, so attendees can connect with their med-ical professional liability (MPL) colleaguesfrom around the country. The next morning,participants will be briefed on the most press-ing MPL issues facing Congress, and then meetwith their elected legislators. Because the mid-term elections will be less than two monthsaway at that point, and many Congressmen willalready be thinking about which issues they’llneed to deal with first during the anticipatedpost-election lame duck session, PIAAAdvocacy Day will be perfectly timed to getMembers of Congress thinking about impor-

tant MPL issues.To find out more information about this

special event, or to learn how you can helpeven if you can’t come to Washington, D.C., see www.piaa.us.

LobbyingGrassroots advocacy is critical, but PIAAknows you have many important things to doin keeping your company prosperous. This iswhy PIAA has a full-time GovernmentRelations Department that connects withCongress and the Administration throughoutthe year. The lobbyist’s responsibility is torepresent you and your interests when youcannot be there to represent yourself. In prac-tical terms, this means meeting with Hillstaff, Members of Congress, and officials fromthe Administration, to help shape policy.

Lobbyists’ efforts span a broad array of tasks, for example, working with a

Understanding the Advocacy Process

L E G I S L A T I V E U P D A T E

B Y M I C H A E L C . S T I N S O N

Michael C. Stinsonis Director ofGovernmentRelations at PIAA.

I N S I D E M E D I C A L L I A B I L I T Y 14 T H I R D Q U A R T E R 2 0 1 4

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:07 PM Page 15

Congressional office to draft legislation, writing up talking points or questions for aCongressional hearing, developing strategy foradvancing a particular piece of legislation (orto stop its progress), and explaining the impactof proposed regulation.

It is probably most accurate, however, todescribe lobbyists as educators whose pri-mary function is to ensure that governmentofficials know as much about an issue as pos-sible before they take action on it.

To many people, the lobbying process issomehow tainted, but in fact it’s a vital ele-ment in governing. For starters, no Memberof Congress, Hill staffer, or regulator can knowall the ramifications of a piece of legislation orproposed rule. In the case of Congress, legis-lators and their staffs are asked to consider lit-erally thousands of bills over every two-yearcycle, and there is simply not enough man-power on Capitol Hill to permit every office tohave an expert on all possible issues. In addi-tion, as noted above, you, as PIAA members,can’t be expected to serve as the resource foryour Member of Congress on every issue ofimportance to you. You’ve got other things todo. Lobbyists ensure that your voice is heardand your issues are understood by the peoplewho are making important policy decisions.

CampaignsThe third element in advocacy is politicalfundraising. While nearly every lobbyist Iknow would rather focus on his role as aneducator, rather than spend time at campaignfundraising events, it is a sad truth thatmoney is very often necessary to get access.That does not mean that money will neces-sarily influence a given official, however(more often than not, money is used to sup-port a candidate who already holds a specificview, rather than in trying to convince thatindividual to change his mind). Instead, cam-paign contributions are used to pay for atten-dance at fundraising events, where you canfocus a candidate’s attention on a key policyissue. These discussions are usually quitebrief and superficial, but they can open thedoor for more in-depth conversations at somelater point—and this was the actual objectiveof the initial discussion in the first place.Admittedly, this is not the ideal approach togetting things done, but overly zealous ethics

“reforms” enacted several years ago bannedmany lobbying activities that were perfectlylegitimate, leaving advocates with few optionsother than paying what may be large sums toattend fundraisers.

In this regard, PIAA maintains a politicalaction committee (PIAAPAC) just for this pur-pose. Annual fundraising efforts from withinthe PIAA membership (federal law prohibitsPIAAPAC from accepting funds from non-members and even a substantial number ofindividuals directly affiliated with a PIAAmember company) provide the revenue neededto attend political fundraising events. To maxi-mize the effectiveness of our extremely limitedPAC dollars, PIAA focuses its attention on thosecandidates who sit on specific important com-mittees or otherwise hold positions that willallow them to influence their colleagues. Allfunds given to campaigns from PIAAPAC arefirst approved by the PAC Board of Directors,and are donated without regard to the political

affiliation of the candidate or their views onissues outside the scope of PIAA interests.

ConclusionWhile PIAA is small compared with manyother interest groups and associations, itstrives to make the most of its resources.Utilizing grassroots advocacy, lobbying, andpolitical contributions, PIAA has achievedremarkable success in recent years. Amongthese victories has been successfully defendingMPL insurers from efforts to limit or eliminatelimited antitrust exemptions for insurers andobtaining bipartisan support for efforts to pre-vent the misuse of federal guidelines/regula-tions in MPL lawsuits.

Advocacy is a key component of PIAA’sservices to its membership—and one thatPIAA takes very seriously. Only the strategicimplementation of all three elements of ouradvocacy program will enable us to sustain our current success.

I N S I D E M E D I C A L L I A B I L I T Y 15 T H I R D Q U A R T E R 2 0 1 4

PIAA thanks the following companiesfor participating in the PAC this year:

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:07 PM Page 16

The Dental Professional Review andEvaluation Program, or D-PREP, wasrecently developed by the AmericanAssociation of Dental Boards (AADB)

as a tool for evaluating the competency ofdental professionals. The program may begood idea in theory, but a recentMassachusetts case highlights the seriouslegal issues and difficulties that its applicationposes for dental professionals and insurersalike.

D-PREP presents unique challenges forprofessional licensing defense. The sanctionis so severe—and the results of it so unpre-dictable—that taking a matter to a hearingwill likely prove more desirable than agreeingto D-PREP as a settlement term. Generally,going through a full adjudicatory hearinggreatly increases the costs of defending anaction. The D-PREP program itself is very

expensive, however, and insurers and practi-tioners should be mindful of who will bestuck with the hefty fees associated with theprogram, should it be required.

This case note discusses the issuesraised by D-PREP and offers some insightsfrom our experience in successfully defendingagainst it recently in Massachusetts.

What is D-PREP?D-PREP was created by the AADB and mod-

The Dental Professional Review and Evaluation Program:

C A S E A N D C O M M E N T

B Y T H O M A S B R I G H T, E S Q . , A N D V I N C E N T D U N N , E S Q .

eled after the Physician Assessment andClinical Education (PACE) program designedfor physicians. D-PREP consists of the follow-ing six phases, with fees totaling nearly$20,0001 : 1. A dentist is referred by a licensing boardand applies to the program at one of threehost universities. 2. The dentist undergoes a full mental andphysical examination, the results of whichmust be provided to the AADB for their

Thomas Bright, Esq., and Vincent Dunn,Esq., are with Hamel Marcin Dunn Reardon & Shea, P.C.

Lessons and Implications for Professional License Defense

I N S I D E M E D I C A L L I A B I L I T Y 16 T H I R D Q U A R T E R 2 0 1 4

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:08 PM Page 17

review. 3. The AADB assembles all the informationavailable about the dentist. 4. The dentist travels to one of the host uni-versities, in Wisconsin, Louisiana, orMaryland. There, they undergo a full evalua-tion, including written and clinical testing,over the course of four to five days. 5. The reviewers write a comprehensiveanalysis of the dentist’s competency for thereferring dental board. The dentist will receiveone of three grades: a pass, a pass with rec-ommendations, or fail. A pass with recom-mendations will include suggested remedia-tion. A fail is a determination that he cannotpractice dentistry at a level of minimumpatient safety, and in all likelihood will func-tion as a complete revocation of the dentist’slicense. 6. The dentist completes the remediation rec-ommended in the D-PREP evaluation once ithas been approved by the board.

There is no appellate procedure oropportunity to obtain an appellate review atany stage of the program. The evaluation isfinal, and there is no mechanism for challeng-ing the D-PREP report.

D-PREP is still in its relative infancy. As of January 2014, only approximately tenindividuals had enrolled in D-PREP for serious issues that had cast doubt on theircompetency.

Legal implications of D-PREPGenerally, licensing boards are creatures ofstatute and must have a statutory grant ofauthority for any action they take. Dueprocess requires that when a board seeks torevoke a license, the licensee be given a hear-ing on the allegations against him. These fun-damental legal principles are called into ques-tion by the very nature of D-PREP.

First, while boards are frequently givenwide discretion in fashioning an appropriatesanction, such discretion is not unlimited. InMassachusetts, the action of at least one licens-ing board has been overturned by a reviewingcourt, when it attempted to require a licensee totake and pass an industry examination as a con-dition for maintaining licensure.2 InMassachusetts, there is nothing in the dentalboard’s enabling statute giving them authority

to order a dentist to undergo assessment by athird party. Compare this to the MassachusettsBoard of Registration in Medicine’s statute,which explicitly allows the board to utilize reme-diation programs like the Physician Assessmentand Clinical Education Program (PACE), buteven then, only on a voluntary basis.3

Second, the D-PREP report is used bythe board to determine whether a dentist willbe able to retain his license. The evaluation isnot limited to the issues that caused the caseto be referred to D-PREP in the first place.Thus, a dentist enrolled in the D-PREP pro-gram risks losing his license completely forissues on which a hearing was never held andfor which no appellate review was available.

This possibility flies directly in the faceof traditional notions of due process andessentially outsources the hearing process toan unaccountable third party.

A case studyOur client dealt with a difficult patient popu-lation. He had received a series of patientcomplaints that, we believe, were motivated bya desire for free care, as the patients’ insur-ance program had recently cut benefits sub-stantially. In response to the complaints, theboard conducted a thorough investigation,which included an unannounced complianceinspection of our client’s office. Ultimately,the board did not move forward on the quali-ty-of-care issues raised in the patient com-plaints, except for one allegation that involvedan overfilled root canal. Instead, the boardsought discipline for recordkeeping deficien-cies and other issues discovered during thecompliance inspection.

The board’s proposed sanction, from the

beginning, was to require that our clientenroll in D-PREP. We viewed this as highlydraconian; after all, our client was only beingaccused of a single clinical deficiency. D-PREP was designed for dentists with seri-ous competency problems, not bad recordkeepers. Furthermore, if our client were toenroll in D-PREP, he would need to pay nearly$20,000 and spend a week away from his fam-ily. He would lose any type of control over theprocess, and also risked losing his ability topractice entirely, should the D-PREP assess-ment come back negative.

Keeping in mind that board cases rarelybenefit from a full hearing, we sought toaddress the board’s concerns by proposingthat our client complete additional continuingeducation in the areas noted by the board. Wealso proposed to demonstrate that he had nophysical or mental impairments that mightimpact his ability to practice. The board con-tinued to insist on D-PREP, however, and, con-sequently, this became one of the rare caseswhere a hearing appeared the more attractivealternative to a negotiated resolution.

Our primary theory of the case was thatD-PREP was not warranted under the facts.Nearly all the violations of which our clientwas accused were minor or entirely defensi-ble. In particular, our expert was fully sup-portive of our client’s treatment of the singleoverfilled root canal, which is a known com-plication of root canal therapy.

We also vigorously disputed the board’sauthority to order D-PREP as a sanction.There was evidence, developed through discov-ery, that tended to show that the board was notactually familiar with what D-PREP entailed.We attacked the board’s position on both pro-cedural and substantive grounds. Because webelieved the board would go forward with itsintention to order D-PREP, we thoroughlydeveloped a number of issues for appeal.

In one final push, shortly before thehearing commenced, the case went back tothe board for reconsideration. Our messagewas clear: this was not a case that warrantedD-PREP, and we would challenge it. Shouldwe prevail on appeal, the board risked losingD-PREP as an option in the future in caseswhere a D-PREP assessment might be a farmore appropriate remedy. Ultimately, theBoard relented and accepted our initial coun-

I N S I D E M E D I C A L L I A B I L I T Y 17 T H I R D Q U A R T E R 2 0 1 4

Generally, licensing

boards are creatures

of statute and must

have a statutory grant

of authority for any

action they take.

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:09 PM Page 18

teroffer. This was only after substantial andintense efforts and expenditures needed toprepare the case and highlight the issues D-PREP raised, however.

Insights and lessonsLike outright revocation of a dental license,when D-PREP is proposed as a settlementterm, taking the case through a full adjudica-tory hearing may be the preferable option.The defense will be far more costly, but thisapproach does ensure some limitation in thescope of the issues considered, some level ofdue-process protection for the licensee, andappellate options not available with D-PREP.

If you are confronted with D-PREP as asettlement option, conduct a thorough evalu-ation and assessment of your client’s case.This is an extreme sanction, with whollyunpredictable, and possibly disastrous, conse-quences for your client. Your board’s enablingact may not authorize third-party assess-ments; your client may not be willing to sacri-fice his substantive and procedural dueprocess rights to the unknown individuals at

the D-PREP centers; and you may obtain amore predictable result for your clientthrough the established procedures of anadjudicatory hearing.

D-PREP may serve a suitable purposefor those whose clinical competency is inserious doubt, but it is likely not an appropri-ate option for practitioners facing more rou-tine allegations.

D-PREP can be a useful tool for theboards, and offers an attractive alternative torevocation when the facts warrant it. Theboards need to understand, however, that ifthey order it when it is not warranted and

subsequently lose on appeal, they may fore-close the possibility of ever ordering it.

ConclusionIt remains to be seen how D-PREP will be uti-lized by the boards as the program maturesand boards become more familiar with it. If,as in the Massachusetts case, the boards seekto require it for routine violations, it willimpede the ability to reach negotiated resolu-tion, and defense of professional licensuremay become far more costly. If, however, theboards use it sparingly, and only where seri-ous issues warrant it, the program could bean attractive alternative to the ultimate sanc-tion of revocation.

References1. See http://dentalasp.com/D-PREP.htm.2. George v. Board of Registration of HomeInspectors, 27 Mass. L. Rptr. 186, 2010 WL 3038729(Mass.Super. May 26, 2010). 3. See M.G.L. c. 112, § 5.

C A S E A N D C O M M E N T

I N S I D E M E D I C A L L I A B I L I T Y 18 T H I R D Q U A R T E R 2 0 1 4

For related information, seewww.hmdrslaw.com.

Due process requiresthat when a boardseeks to revoke alicense, the licenseebe given a hearing onthe allegationsagainst him.

AAA

Our handshake means more than an engagement. It means commitment.

MEDICAL PROFESSIONAL LIABILITYALTERNATIVE MARKETSENTERPRISE RISK MANAGEMENTLEGISLATIVE COSTINGLITIGATION SUPPORT LOSS RESERVING

Commitment Beyond Numbers

Commitment Beyond Numbers

Commitment Beyond Numbers

Empathetic Customer Service.elationships, not just transactions. Wr

consulting services in every aspect of medical prinsurance at the local, state and national levels.

e about our medical pro learn morTTovisit us at pinnacleactuaries.com.

Empathetic Customer Service. At Pinnacle, we believe in ovided actuarial e have prelationships, not just transactions. W

ofessional liability consulting services in every aspect of medical prinsurance at the local, state and national levels.

ofessional liability expertise, e about our medical prpinnacleactuaries.com.

MEDICAL PROFESSIONAL LIABILITYTERNALLT

ENTERPRISE RISK MANAGEMENTLEGISLA

TION SUPPORLITIGALOSS RESERVING

At Pinnacle, we believe in ovided actuarial

ofessional liability

ofessional liability expertise,

MEDICAL PROFESSIONAL LIABILITYTIVE MARKETSNAAT

ENTERPRISE RISK MANAGEMENTTIVE COSTINGLEGISLA

TTION SUPPORLOSS RESERVING

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:09 PM Page 19

StoneHill

Advancing Your Business. Ensuring Success.

Inquire. Collaborate. Execute.

www.stonehi l l re.com

ancAdvva

our BusinessYancing

Ensuring Successour Business

Ensuring Success

Ensuring Success

ancAdvva

StoneHill

our BusinessYancing

StoneHill

Ensuring Success.our Business

StoneHill

Ensuring Success

. Ensuring Success

CollaboraInquire.

www

te.Collaboraat

.come.stonehi l l rwww

Execute.

.com

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:10 PM Page 20

H E R C U L E SHIGH SOUTHERN SKYOH SGIH

REHH

RYKN SREHTUO

SELC U

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:10 PM Page 21

Bulk up.Gain capital and scale by becoming a mutual owner of Constellation.If you’re feeling a bit insignificant in the universe of physician-owned medical liability companies, you’re not alone. Many are finding it increasingly tough to compete against large stock companies.

That’s why we formed Constellation, a mutual holding company created for like-minded medical liability insurers and other types of health care organizations. As a joint owner of Constellation, you’ll enjoy significant benefits, such as increased scale, efficiencies, capital and support.

With this kind of strength, you’ll be protected from consolidation and more able to compete against commercial carriers. Most importantly, you’ll remain independent and maintain your customary

operations, allowing you to continue focusing on improving patient outcomes and serving the unique needs of your market.

Find out more about how your company can shine brighter as a part of Constellation. Contact us at 888.965.0503 or visit ConstellationMutual.com.

brighter together

l

klk

B

luB

klkk

puup

p.

p

p.

sniage atpemocna. Menolt aonenwo-niacisyhhypgnielee ffer’uof yI

tipan ciaG ap

.seinapmok ccotrge sat lsylgnisaercnt ig inidne firy annapmoy ctilibial lacided mene uhn tt inacfiinigsnt iig a b

ey be blacd snl aat y b

ruof ys odeenag pnivorpmil, asnoitarpeo

oh tguoy ter’uo, yseinfse orevvein

autug a mnimoec

goe

m

t.ekrar mgnivrd sens aemoctuut oneitaacoe ffounitnoo cu tog yniwooll

etsnof Cr oenwl oa

euqine uhg tng onisuc

.noitlale

uq

n

s eicneicffi, eelacso nigy sojnl el’uoy

. Ar snoitazinargosi rerusny itilibiallnapmog cnidloh

e fy ws whhy’taaTh

gp

nj

t.rpopud snl aatipa, csecns ih acu, sstfient benacfiinleltsnof Cr oenwt onios a jA

h tlaef hs opeyr tehtd ons ad ednime-kir lod ffoetaaery cnu, a mnoitaleltsnod Cemroffo

pg

3050.569.888s a pr aethhigrb

rot muud oniF

dseaerc,noitaal

eraclacidem

lautuu

sn

i

tuMnoitaleltsnot Cisir v3 otno. Cnoitaleltsnof Ct orapynapmor cuow yoot huboe ar

.moc.lauts aat uact

enihn say c

mtaai

npeednn iiamerral ciacremmoc

n aoitaadilosnocd nis kihh ttiWWi

ur cuon yiatniad mnt anedno, yyy,ltnatrpomt iso. Msreirrge atpemoo ce tlbe arod mn

etorl be pl’uo, yhtgnertf so

yramotsull’u

tsniagmord ffretc

olnd

rehttheogge ttorehttegghirb r ig

PIAA 3Q 2014 AFRONT _Layout 1 8/8/14 12:10 PM Page 22

Cynthia Wallace, CPHRM, and Karen P. Zimmer, MD, MPH, FAAP,are with ECRI Institute.

I N S I D E M E D I C A L L I A B I L I T Y 22 T H I R D Q U A R T E R 2 0 1 4

C O V E R S T O R Y

Using PSO Data toIdentify the LeadingPatient SafetyConcerns—and Lessons Learned

Patient safety is a top priority for every healthcare

organization, but knowing where to direct patient

safety initiatives can be daunting. To help organiza-

tions decide where to focus their patient safety

efforts, ECRI Institute has developed a list of the top

ten patient safety concerns confronting healthcare

organizations (Figure 1).

B Y C Y N T H I A WA L L A C E , C P H R M , A N D

K A R E N P. Z I M M E R , M D , M P H , FA A P

PIAA 3Q 2014 Features_Layout 1 8/8/14 2:52 PM Page 1

I N S I D E M E D I C A L L I A B I L I T Y 23 T H I R D Q U A R T E R 2 0 1 4

We’ve been collecting events since 2009, and with closeto 400,000 events, we’re at a point where it’s impor-tant to share where we’re seeing recurring themes,”says Karen P. Zimmer, MD, MPH, FAAP, medicaldirector of ECRI Institute’s patient safety, risk, and

quality group and of ECRI Institute PSO. The initiative underscores the intent of the Patient Safety and

Quality Improvement Act of 2005, which laid the groundwork forproviders to voluntarily report patient safety events and other informa-tion (e.g., root-cause analyses) to Patient Safety Organizations (PSOs)in a protected environment. The PSOs aggregate, analyze, and share

findings and lessons learned. By collecting data from many providers,PSOs can spot problems and trends that an individual organization,with a limited pool of data, may be unable to detect.

The list as a starting pointThe list, which highlights risks to patient safety that stem from issueswith processes and systems, is not intended to be comprehensive, andnot all of the patient safety concerns will be applicable at all healthcarefacilities. “We encourage facilities to use the list as a starting point forpatient safety discussions and for setting their patient safety priori-ties,” says Zimmer.

“

PIAA 3Q 2014 Features_Layout 1 8/8/14 2:53 PM Page 2

Although many of the organizations reporting to ECRI Institute PSOare hospitals, the list of patient safety concerns, such as drug shortages,mislabeled specimens, and care coordination, also applies to non-hospitalsettings, such as physician practices and long-term care settings.

This article highlights three of ECRI Institute’s 2014 Top 10: carecoordination, test result reporting, and drug shortages.

Where to find the full listThe complete 2014 ECRI Institute Top 10 Patient Safety Concerns list,which ECRI Institute plans to update annually, is available for freedownload at https://www.ecri.org/Products/PatientSafetyQuality

RiskManagement/Pages/Free-Reports-Advisories.aspx. It includesstrategies for mitigating each of the ten concerns and is accompaniedby a poster, PowerPoint presentation, and other tools.

Care coordinationCare coordination is a “shared responsibility” of all providers involvedin a patient’s care, says Lorraine Possanza, DPM, JD, MBE, patient safe-ty, risk, and quality analyst at ECRI Institute. However, events reportedto ECRI Institute PSO reveal gaps in communication—between hospi-tals and providers, among providers, and between long-term care set-tings and hospitals or other providers. For example, in one event, an

P A T I E N T S A F E T Y C O N C E R N S

I N S I D E M E D I C A L L I A B I L I T Y 24 T H I R D Q U A R T E R 2 0 1 4

On June 13, 2014, more than 200 patientsafety advocates from across the coun-

try gathered to participate in a day-longsymposium that was focused on how culturecan progressively impact patient safety inhealthcare organizations. Sponsored byCRICO, the goal was to gain a better under-standing of the ways by which culture canenhance or inhibit safety improvements, andhow organizations can affect their own envi-ronment by learning to “Walk This Way.”

In a unique opening segment, a skitcomprising a series of acts depicted the evo-lution of smoking behavior in the hospitalsetting. Many of you may recall a time in thenot so distant past when it was commonpractice for clinicians and patients to smokeon the wards, in the break room, and at nurs-ing stations. This practice evolved—slowly,but surely—to remote smoking rooms at theend of the hallway, outside designated smok-ing areas, and finally, to present-day smoke-free campuses around the country.

Looking back, it’s difficult to believe weever smoked on the ward, drove our childrenaround without car seats, or allowed them toride their bicycles helmet-free. However,through years of research, education, and per-sistence, all of these safety risks have indeedbeen recognized and changes introduced, andpeople have adapted. This premise segued toa robust program that captured an array ofperspectives and impactful lessons for creat-ing a stronger safety culture, including:

Paul McTague, Esq.: Culture as aContributing Factor to Legal Defense■ Three “Cs” for MDs: be Competent,Confident, and Caring—in court and in practice.■ Follow policies; it’s difficult to defend aclaim when they’re not followed.■ Document, as needed, to provide forgood medical care, not what you think willprotect you in court.

Asaf Bitton, MD: Envisioning YourFuture Work Environment■ If we want to make drastic changes, weneed to take drastic steps. ■ Imagine a patient-centered medicalhome that was designed for maximumteamwork and connected by robust IT systems. ■ Establish the goal of your culturethrough seven habits: co-location, huddles,warm handoffs, weekly meetings, staffingthat matches the culture, work force devel-opment, and committed leadership.

Tracy Granzyk: What’s Your Story?The Power of Narrative■ Storytelling can change attitudes andbeliefs, because it breaks down cognitiveresistance.■ Data helps us focus on “what” to fix;storytelling gives us the emotional connec-tion to “why” it matters.■ Honor patient and caregiver stories

through actions respectful of their lesson.

Jerry Hickson, MD: How to Recognize and Remove Obstacles■ Establish an infrastructure that promotes reliability and professionalaccountability.■ Fix your faulty systems and promoteprofessional behavior to set the right balance. ■ Respond to every incident of unprofes-sional behavior with a consistent construc-tive response.

At lunch, attendees were asked to envisionevolved cultural events five to ten years fromnow that may be as difficult to believe as the“smoking story.” The day wrapped up with asummary of the myriad submissions on thegeneral topic: It’s hard to believe there was atime when…■ We did not always wash our handsbefore seeing a patient.■ We did not do formal timeouts forevery surgery. ■ We were afraid to report adverse events.■ We did not have efficient systems fortracking/follow-up on abnormal test results.■ We did not consider patients part oftheir own care team.

Missy Padoll is Director, Strategic Analysisand Communication, CRICO.

By Missy Padoll

For related information, see www.rmf.harvard.edu.

“Walk This Way”: Impacting the Culture of Safety through Time and Example

PIAA 3Q 2014 Features_Layout 1 8/8/14 2:54 PM Page 3

infant’s discharge summary andfollow-up care information werenot provided to the patient’s pri-mary care physician:

An infant who died from sud-den infant death syndrome had pre-viously been seen in the hospital for alife-threatening event. Because ofabnormal findings on the patient’s CTscan, the patient’s discharge summaryindicated the patient should have anMRI exam. The discharge summarywas not sent to the patient’s primaryphysician. The patient did not under-go the MRI study.

While a best practice is forhospitals to send a patient’s dis-charge information to all thepatient’s providers, staff can beoverwhelmed trying to identifythose providers. “It’s not only the hospital’s responsibility,” saysPossanza, who previously had a podiatry practice and has experiencewith care coordination challenges. “It’s also on me as the patient’sprovider to communicate with the patient’s other providers,” she says,recalling that in addition to communicating with patients’ providers asneeded, she used to “touch base” with her patients’ other providers atleast once a year “so they know I’ve been involved in the patient’s care.”

One “simple and basic” strategy to improve care coordinationbetween hospitals and ambulatory settings is for practices to providecurrent contact information, such as phone and fax numbers, on theirwebsites. Possanza adds: “Identify the providers in your practice. If thehospital needs to contact you, the information is right there.”

Linda C. Wallace, BSN, MSN, CPHRM, a consultant in aging serv-ices risk management at ECRI Institute, notes some of the strategiesshe has seen put in place to improve care coordination between hospi-tals and post-acute care providers. They include:■ Preadmission nurses from the postacute care setting evaluate thepatient before discharge and prepare the post-acute care provider formeeting the patient’s needs.■ Hospital representatives visit the post-acute care organization toensure an understanding of the services available there and to mini-mize the risk of transferring patients whose condition cannot be man-aged at that post-acute care facility.■ There are closer affiliations between hospitals and post-acute careproviders, through accountable care organizations or other means.

As providers develop more arrangements to ensure care coordina-tion, Possanza reminds them, “You can’t forget the patient. The patientis overwhelmed by their disease process and by navigating the

system . . . someone needs to helpthat person, especially an elderlypatient, to remind them to makeappointments, to take medications,and to help them know what to askand expect at their next healthcarevisit.”

Reporting test resultsBreakdowns in reporting test resultscan occur for many reasons.Sometimes, the ordering providernever gets the results or receivesthem after a delay. Or, the reportingprovider may be unavailable, andorganizations may not have a backupplan for ensuring that results withimportant findings are communicat-ed to someone else who can act onthem. These breakdowns can con-tribute to “bigger issues of delays inpatient care, as well as delays in diag-

nosing an acute condition,” says Christine M. Callahan, RN, MBA, physi-cian practice management consultant for ECRI Institute.

Examples of test result reporting errors reported to ECRI InstitutePSO include:■ A baby’s treatment with antibiotics was delayed because the testresults confirming an infection were not reported promptly to theordering clinician.■ Prompt management of a patient with C. difficile infection washindered because of a delay in reporting test results confirming theinfection.■ A patient’s seizure due to a low sodium level could have been avoid-ed if blood chemistry results had been provided on a timely basis.

Callahan observes that breakdowns in test results reporting, par-ticularly in physician practices, typically have one or more of threecauses: ■ Technology limitations, such as an inadequate interface betweenan electronic health record (EHR) system and a laboratory system thatprovides the results electronically■ Provider-to-provider communication gaps, such as those thatoccur when no backup plan is in place to designate a provider toreview test results for another provider who is unavailable.■ Staffing and training failures, for example, requiring that a staffmember periodically check an EHR system for test results but notinforming him about the volume of test results he can expect to see.

As more healthcare organizations adopt EHR systems, Callahanwarns against being lulled into thinking the systems can prevent testreporting failures. “It’s another tool,” she says. “It won’t improve test

I N S I D E M E D I C A L L I A B I L I T Y 25 T H I R D Q U A R T E R 2 0 1 4

Figure 1 ECRI Institute’s Top 10Patient Safety Concerns for 2014

MS1

4036

PIAA 3Q 2014 Features_Layout 1 8/8/14 2:54 PM Page 4

I N S I D E M E D I C A L L I A B I L I T Y 26 T H I R D Q U A R T E R 2 0 1 4

results reporting if it’s not used correctly.”Whether test results are reported on paper, electronically, or in

some combination of both, organizations must have policies and pro-cedures to guide reporting of the results and must educate and trainstaff about the policies, says Debra Ann Maleski, MBA, senior associatewith ECRI Institute’s Applied Solutions Group, which provides cus-tomized consulting. The policy should address key questions:■ Who gets the results?■ What is the process for reporting abnormal findings?■ Is there a designated backup provider to review the results if theordering provider is unavailable or does not review the results within aspecified time frame?■ What is the expected time frame for providers to review results?■ How are findings communicated to the patient?■ What is the policy for ensuring that information gets to the

patient if that person is unavailable?

In addition, organizations must audit staff compliance, Maleskiadvises. “You may have a great policy, but if it’s not enacted or followed,the organization needs to be aware and implement corrective action.”

Drug shortagesThe potential implications of drug shortages for patient care werehighlighted when a hospital contacted ECRI Institute PSO about asevere shortage of emergency drugs. Unable to replenish its supply ofinjectable unit-dose medications stored on crash carts, the hospitalwanted to know whether its remaining supply of expired drugs couldbe used instead.

“In the intervening months, the topic remained on our radar andshowed an escalating level of interest from healthcare providers,” says

With a supporting pledge of $50 millionfrom MagMutual Insurance Company,

the MagMutual Patient Safety Institute wasestablished this past October, to facilitate in-depth study and analysis of patient safetyissues confronting MagMutual policyholders.The institute endeavors to create evidence-based resources and practical tools to pro-mote the adoption of best practices in orderto improve safety among its policyholdersand decrease their exposure to risk.

“We believe the best defense againstmedical error is to proactively assist physi-cians and other healthcare providers in thecreation of environments conducive to opti-mal care and outcomes,” said Dr. Joe WilsonJr., MagMutual’s chairman and chief execu-tive officer. “Patient safety is one of the mostpressing challenges in healthcare today. “

In addition to analyzing historicalclaims data, the institute facilitates riskassessments for the more than 19,000 physi-cians insured by MagMutual and its affiliate,Professional Security Insurance Company.This number includes solo practitioners aswell as physicians employed by larger prac-tices and hospitals. The data derived fromthese assessments serves as the basis for con-tinuing medical education (CME), as well asspecialty-specific and even practice-specific

tools and resources.Dr. Mary Gregg, senior vice president

and chief medical officer of MagMutual,serves as president of the institute. Dr. Greggpreviously served as medical director forquality and patient safety and vice presidentof medical affairs with Swedish HealthServices in Seattle, one of the largest nonprof-it health systems in the Pacific Northwest. Shewas also medical director for ClinicalOutcomes Assessment and Performance(COAP) at the Foundation for HealthcareQuality (FHCQ), and medical director of clin-ical quality at Swedish Heart and VascularInstitute.

“Physicians appreciate the power ofeducation and collaboration, and by tappinginto our network of policyholders, we are tak-ing our patient safety and quality efforts tonew levels,” said Gregg. “We help them under-stand their areas of greatest risk, and then wedesign tools to help address them.“

So what are some of the key patientsafety risks identified by the Institute so far?“Two of the most common of the many con-cerns we encounter are medication errorsand issues with electronic medical records[EMRs],” explained Gregg.

“Not only do physicians need to cross-check multiple lists of medications at every

step of the prescribing and dispensingprocess; they also need to be more aware ofdrug interactions and side effects.”

“With regard to EMR issues, caregiversneed to ensure that their system works forthem. Technology can greatly enhance thequality of patient care, but there are risks aswell. We encourage healthcare professionalswho are prescribing and treating to take anactive role in the formatting of order sets,progress notes, procedure notes, and careplans. Providers need to make the ‘right thing’the easiest thing to do.”

“At the end of the day, our goal is to helpour policyholders create a culture of safetycharacterized by transparency and trust, allgrounded in the creation of a database that isfocused on root causes,” added Gregg. “We arelearning as we go, but we aspire to be the go-to organization for new ideas, solutions, andmodels that promote patient safety and mitigate risk, and to attract partners who are willing to pilot new processes.”

Terrell McCollum is Director, MarketingCommunications, MagMutual InsuranceCompany.

By Terrell McCollum

MagMutual Patient Safety Institute Researches Safety Concerns

For related information, see MagMutual.com/patient-safety/resource-library.

P A T I E N T S A F E T Y C O N C E R N S

PIAA 3Q 2014 Features_Layout 1 8/8/14 2:54 PM Page 5

I N S I D E M E D I C A L L I A B I L I T Y 27 T H I R D Q U A R T E R 2 0 1 4

Patricia Neumann, RN, MS, patient safety analyst/consultant for ECRIInstitute PSO. An event reported to ECRI Institute PSO shows the needfor established policies that will guide pharmacists, nurses, and physi-cians on what to do when a drug is unavailable:

A patient in intensive care had a critical phosphate level. The physi-cian ordered an intravenous sodium phosphate for the patient. The phar-macist could not fill the order because the drug was unavailable and didnot tell the patient’s nurse or the ordering physician about the shortage. Thepatient had a seizure due to abnormally low phosphate levels in the blood.

Neumann advises healthcare organizations to develop a proac-tive plan for managing drug shortages. The plan should assign a taskforce to monitor impending shortages, she says. Two good resourcesfor identifying potential drug shortages are the U.S. Food and DrugAdministration’s (FDA) website on drug shortages, which provides alist of national shortages for which there are no substitutes, and theAmerican Society of Health-System Pharmacists’ (ASHP) drug short-ages website, which provides information on regional drug shortages.1

In addition to tracking shortages that can affect the organiza-tion’s supplies, the action plan should address these areas:■ Documenting drug shortages and approving alternatives todrugs that are unavailable or in short supply■ Monitoring adverse drug events to determine whether any mayhave been caused by shortages■ Keeping the quality improvement and pharmacy and therapeu-tics committees informed of any shortages■ Providing an annual report on shortages and their impact on the organization to its leaders.

Information about drugs in short supply or substitute drugsmust be communicated to clinical staff. All ordering providers mustknow what drugs are in short supply, when regular distribution ofthem will resume, what alternatives or substitutes are available, andbasic information on each alternative drug, including its current for-mulations, contraindications, and potential for error.

To keep clinical staff informed about any shortages and the orga-nization’s planned response, it should consider posting updates on anIntranet site available to clinical staff at all times, suggests Neumann.In addition, it should ensure that a pharmacist is available to clinicalstaff to answer any questions. Components of the organization’s healthIT system—EHR systems, electronic drug ordering, and electronicmedication administration records—must be kept up-to-date as drugavailabilities change. Although time-consuming, system updates arevital for preventingmedication errors,says Neumann.

Reference1. FDA’s website on drug shortages is athttp://www.fda.gov/Drugs/DrugSafety/DrugShortages/default.htm. ASHP’s website is at http://www.ashp.org/shortages.

For related information, see www.ecri.org.

PIAA 3Q 2014 Features_Layout 1 8/8/14 2:54 PM Page 6

I N S I D E M E D I C A L L I A B I L I T Y 28 T H I R D Q U A R T E R 2 0 1 4

Martin Lippiett is VicePresident of Business

Consulting, Delphi Technology, Inc.

The main news

item, a few months

ago, was the failure

of the Affordable

Care Act website to

perform as intend-

ed. There were

many reasons for

this, and each

failed project has

its own story. But

the following fac-

tors are almost

always in play, to

varying degrees,

when the implemen-

tation of an enter-

prise-level system

ends up in trouble.

The “Seven Deadly Sins” of Large-Scale IT Project Management

B Y M A R T I N L I P P I E T T

F E A T U R E S T O R Y

PIAA 3Q 2014 Features_Layout 1 8/8/14 2:54 PM Page 7

Poor governance

This is probably the number-one reason why projects fail. Theproject is begun without an adequate and achievable planwith respect to requirements, budget, and resources. Then, asthe work continues, control over changes in the plan is poorlymanaged, and mid-course corrections are made with politics,

face-saving, extreme optimism, and other undesirable considerationsassuming priority in decision-making.

The keys to effective project governance are these: ■ It’s critical to incorporate scenario modeling into the initial pre-project analysis, so that different options can be evaluated and the one

that is most realistic—and shows optimal benefits—is selected. Inother words, make sure the project you are planning in the first place isthe right one for the business.■ Project criteria, roles, processes, and outcomes must be estab-lished early and then actively monitored to enhance project success.Have an escalation strategy in mind; nothing goes exactly as planned.■ Governance must be accepted and supported by all levels of management.■ Warning signs should be recognized and effective action takenearly to avoid a snowballing failure.