winning through disruption in the transport...

TRANSCRIPT

1 | © 2017 Infinera

Winning Through Disruption In The Transport Market

Investor Overview

November 2017

2 | © 2017 Infinera

This presentation contains "forward-looking" statements that involve risks, uncertainties and assumptions. If the risks or uncertainties ever materialize or the assumptions prove incorrect, our results may differ materially from those expressed or implied by such forward-looking statements. All statements other than statements of historical fact could be deemed forward-looking, including, but not limited to, any statements about future market and financial performance and similar statements; statement regarding future products or technology as well as the timing to market of any such products or technology; any statements about historical results that may suggest trends for our business; any statements of the plans, strategies, and objectives of management for future operations; any statements of expectation or belief regarding future events, potential markets or market size, technology and product developments, or enforceability of our intellectual property rights; statements regarding our second quarter outlook; and any statements of assumptions underlying any of the items mentioned.

These statements are based on estimates and information available to us at the time of this presentation and are not guarantees of future performance. These risks and uncertainties include, but are not limited to, delays in the release of new products or updates to existing products and market acceptance of these products; customer consolidation; fluctuations in customer demand, changes in industry trends, and changes in the macroeconomic market; the risks of competitive responses and shifts in the market; the effect that changes in product pricing or mix, and/or increases in component costs could have on our gross margin; our ability to respond to rapid technological changes; aggressive business tactics by our competitors; our ability to adequately respond to demand as a result of our restructuring plan announced in November 2017; our reliance on single and limited source suppliers; our ability to protect our intellectual property; claims by others that we infringe their intellectual property; war, terrorism, public health issues, natural disasters and other circumstances that could disrupt the supply, delivery or demand of Infinera’s products; and other risks and uncertainties detailed in our SEC filings from time to time. More information on potential factors that may impact our business are set forth in Infinera’s Quarterly Report on Form 10-Q for the fiscal quarter ended on September 30, 2017 as filed with the SEC on November 8, 2017, as well as subsequent reports filed with or furnished to the SEC from time to time. Our SEC filings are available on our website at www.infinera.com and the SEC’s website at www.sec.gov. Forward-looking statements are subject to change, and we may not inform you when changes occur. We assume no obligation to, and do not currently intend to, update any such forward-looking statements.

Safe Harbor

3 | © 2017 Infinera

The most vertically integrated optical transport systems company• Unique technology innovation with PIC

• Vertical integration drives superb reliability and

differentiated cost structure

• Best-in-class systems with automation,

convergence and scalability

Industry-leading global service and support

Right tools for right job

Focused on customer success

Infinera: A Differentiated Optical Systems Company

Enabling An Infinite Pool of Intelligent Bandwidth

Cloud XpressDTN-X

XTC Series

Photonic Integrated Circuit (PIC)

XT-500

XTM/XTG Series

Cloud Xpress 2

FlexCoherent® Electronics

XT-3600

XT-3300

4 | © 2017 Infinera

Global Customer Base

Over 600 customers

spanning six continents

Three of thetop four

internet content providers

Majority of largecable operators

in North America and Europe

Leading North America and

pan-European wholesale operators

19 Tier 1 operators globally

5 | © 2017 Infinera

Technology LeadershipInfinera Uniquely Delivers Massive Scale

The Infinera ApproachConventional Approach

Electronics/ASICs

Intelligentsoftware

Photonic integrated circuitsCoherent optical engine

VerticallyIntegrated

Vertically Integrated

Moore’s Law-like for Optical

Industry’s only large-scale photonic integrated circuit

Significant Barriers to Entry• Hundreds of millions of

dollars spent over the years to build indium phosphide PIC factory

• 15+ years of experience

• More than 450 patents covering IP

6 | © 2017 Infinera

An End-to-End Portfolio to Serve an Expanding Market

7 | © 2017 Infinera

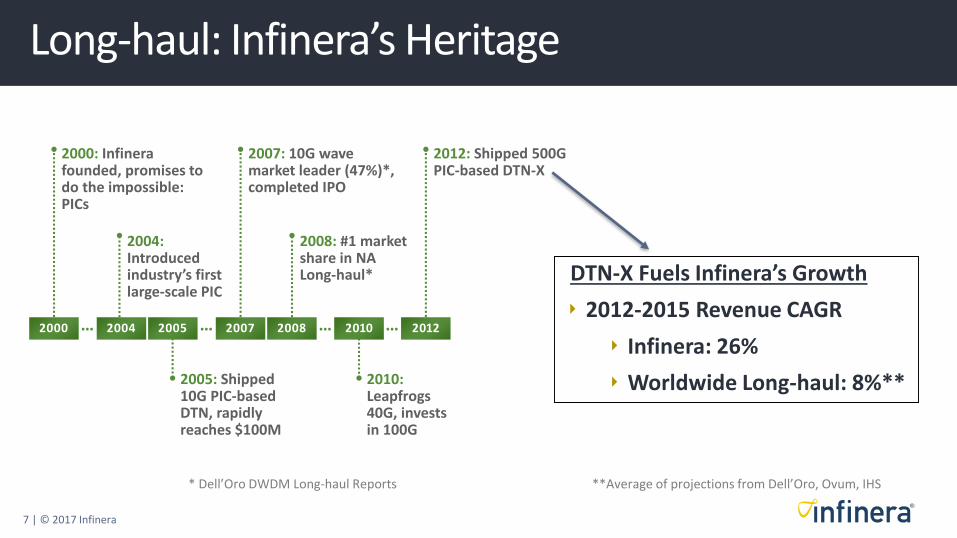

Long-haul: Infinera’s Heritage

* Dell’Oro DWDM Long-haul Reports

2005: Shipped 10G PIC-based DTN, rapidly reaches $100M

2007: 10G wave market leader (47%)*, completed IPO

2000: Infinera founded, promises to do the impossible: PICs

2004: Introduced industry’s first large-scale PIC

2008: #1 market share in NA Long-haul*

2010: Leapfrogs 40G, invests in 100G

2012: Shipped 500G PIC-based DTN-X

…2000 2004 2005 2007 2008 2010 2012…… …

DTN-X Fuels Infinera’s Growth

2012-2015 Revenue CAGR

Infinera: 26%

Worldwide Long-haul: 8%**

**Average of projections from Dell’Oro, Ovum, IHS

8 | © 2017 Infinera

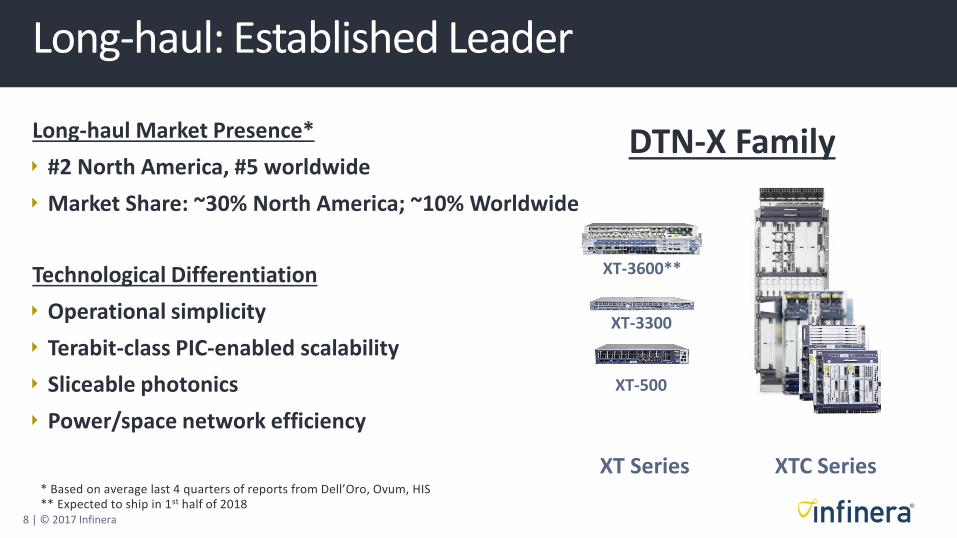

Long-haul: Established Leader

* Based on average last 4 quarters of reports from Dell’Oro, Ovum, HIS** Expected to ship in 1st half of 2018

Long-haul Market Presence*

#2 North America, #5 worldwide

Market Share: ~30% North America; ~10% Worldwide

XTC Series

XT-500

XT-3600**

XT-3300

Technological Differentiation

Operational simplicity

Terabit-class PIC-enabled scalability

Sliceable photonics

Power/space network efficiency

XT Series

DTN-X Family

9 | © 2017 Infinera

DCI: Cloud Architecture Drives Network Demands

sources: google.com, facebook.com

Search Query

930x Network Traffic

Cloud Data Center Network

1500 Miles

HTTP request

10 | © 2017 Infinera

Cloud Xpress Cloud Xpress 2

DCI: Infinera Cloud Xpress Family

500 Gb/s super-channel line10/40/100 GbE clients

Hyperscale Density Simple OperationLow Power Automation Built-in SecurityInstant Bandwidth

1.2 Tb/s super-channel line in 1RU100 GbE clients16QAM

11 | © 2017 Infinera

1G to 100G packet-optical

100G at Layer 1 and Layer 2 P-OTS

16QAM applications with XTM-2, XT-3300 and XT-3600

Multi-service, access to core

Low power and latency, high-density design

Metro: Solutions From Core To Access

Cloud Xpress Family

XTC-2/2E

Building a differentiated portfolio from core to access

XTM/XTG Series

XT-3600*

XT-3300

* Expected to ship in 1st half of 2018

12 | © 2017 Infinera

Metro: A Significant Growth Opportunity

• Strong customer base and reputation in metro edge/access• Power-efficient and purpose-built products

• Early technology leadership in applications like Remote PHYDifferentiated Approach

• High-capacity solutions for metro core upgrades to 100G• Over time, lowers cost structure and enhances tech

differentiationVertical Integration

• Long-haul customer base upgrading to 100G metro• Strong presence in metro-heavy cable vertical

Customer Base

Infinera Current Metro Market Share: 3% Worldwide*

Significant opportunities to grow! *Average of latest projections from Ovum, IHS, Dell’Oro and ACG

13 | © 2017 Infinera

Instant Network: The Next Generation of Software Defined Capacity (SDC) for Cloud Scale Networks

Instant Network - Leading the Way to Cognitive Networking

▪ Reduce OpEx• Fewer truck rolls, automate LSO

▪ Accelerate Service Delivery• Respond quickly to new service demands

▪ Increase Service Reliability• Reduce human touchpoints

▪ Reduce Idle CapEx

• As much as 50% of capacity idle

• Lower initial CapEx by activating SDC when revenue-generating services demand it

• Reduce business risk by shrinking time between paying for capacity and activating services

Instant Network Benefits

Cognitive NetworkingInstant NetworkInstant Bandwidth

▪ Infinera DNA Software and Xceed Software Suite ▪ Microservices Architecture▪ Open Software and SDN APIs

Software Foundation:

▪ Industry-leading Photonics - 500G PIC, 2.4T Infinite Capacity Engine▪ Integrated and Disaggregated Architecture▪ Massive Pre-deployed Capacity, Sliceable

Hardware Foundation:Soft

wa

re D

efin

ed C

ap

aci

ty

14 | © 2017 Infinera

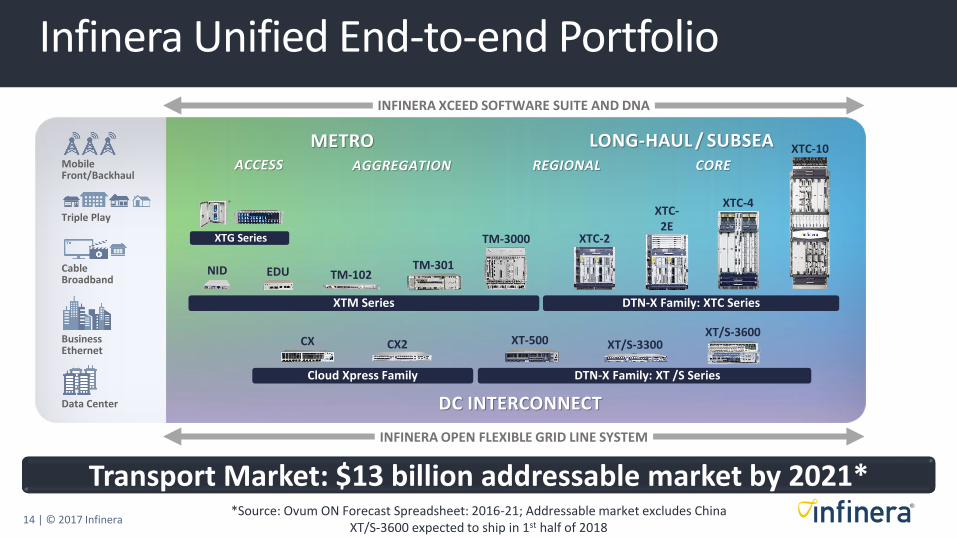

Infinera Unified End-to-end Portfolio

XTM Series DTN-X Family: XTC Series

Cloud Xpress Family DTN-X Family: XT /S Series

XTG Series

XTC-10

XTC-4XTC-2E

XTC-2TM-3000

TM-301TM-102EDUNID

CX CX2 XT-500 XT/S-3300XT/S-3600

DC INTERCONNECT

LONG-HAUL / SUBSEAMETROACCESS AGGREGATION REGIONAL CORE

INFINERA XCEED SOFTWARE SUITE AND DNA

MobileFront/Backhaul

Triple Play

Cable Broadband

Business Ethernet

Data Center

INFINERA OPEN FLEXIBLE GRID LINE SYSTEM

Transport Market: $13 billion addressable market by 2021**Source: Ovum ON Forecast Spreadsheet: 2016-21; Addressable market excludes China

XT/S-3600 expected to ship in 1st half of 2018

15 | © 2017 Infinera

Market Expansion

Bandwidth Explosion and Evolving Network Architectures Create Opportunities

16 | © 2017 Infinera

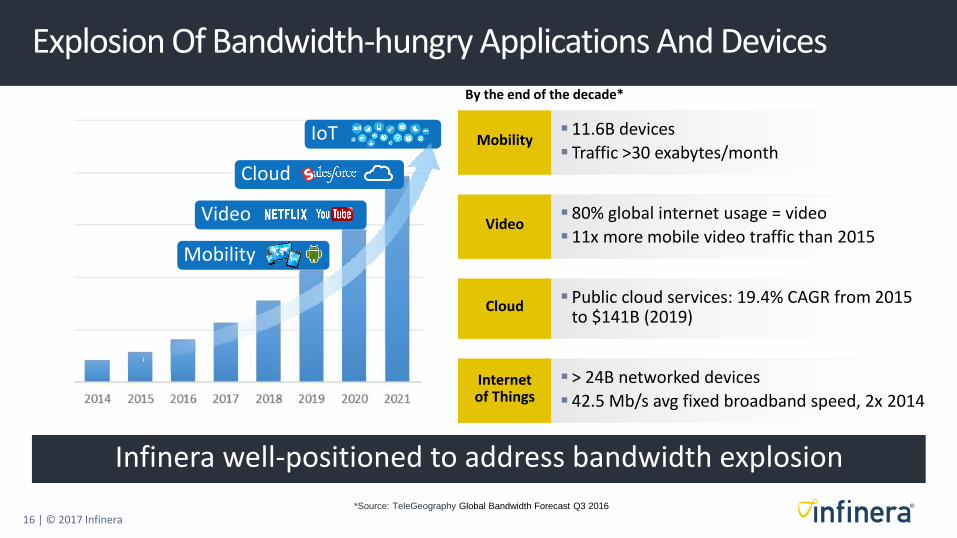

Explosion Of Bandwidth-hungry Applications And Devices

Infinera well-positioned to address bandwidth explosion

*Source: TeleGeography Global Bandwidth Forecast Q3 2016

Video

Cloud

Mobility

IoT

By the end of the decade*

Mobility▪ 11.6B devices

▪ Traffic >30 exabytes/month

Video▪ 80% global internet usage = video

▪ 11x more mobile video traffic than 2015

Cloud▪ Public cloud services: 19.4% CAGR from 2015

to $141B (2019)

Internet of Things

▪ > 24B networked devices

▪ 42.5 Mb/s avg fixed broadband speed, 2x 2014

17 | © 2017 Infinera

The Dismantling of Status Quo Networks is Underway

Transport Becomes More Capable with More Intelligence

Intelligent Transport shifting $$ away from Routing

Pressure to break Proprietary OS, Slow

Innovation

Routing (L3)

Transport(L0-L2)

Routers need transport systems to connect

XX

XX

X

NFV/Software pressuring traditional router infrastructure

Intelligent Transport increasingly capable of substituting for many router functions

“LAYER T”

18 | © 2017 Infinera

Network Transformation: The New Layers T and C

Open packetoptical, move bitsDC-DC, DC-user

Every possiblenetwork function runs in cloud

Layer T: IntelligentTransport

New Model

NFV Apps

SDN Control

Layer C:Cloud Services

Firewall

SBC

B-RAS

CPE

Packet

OTN

WDM

L0 – L3

L3 – L7

Old Model

Open APIs

Appliance per Function,Rigid, $$$, Closed

Shared Infrastructure, Agile, Open, $

LAYER C

LAYER T

Layer T powers hyperscale cloud networks – positive for Infinera

19 | © 2017 Infinera

0

50

100

150

200

250

300

350

2012 2013 2014 2015 2016 2017 2018 2019 2020

Tb/s

DCI and Long-haul: Layer T Traffic Patterns Changing

Private: 70% CAGRMostly DC to DC

Internet: 21% CAGRMostly user to content

Trans-Atlantic Bandwidth MixSource: Telegeography

100G Services are SurgingSource: Ovum

100G: 75% CAGR

10G: 16% CAGR

20 | © 2017 Infinera

Packet-Optical Requirements

Ethernet ServicesLow LatencySuperior SyncLow Space and PowerHardened Systems

Metro: Layer T Architectural Shift, Fiber Deeper Into Metro

100G Mobile Backhaul

MobileFronthaul BBUFiber to the tower

Fiber-deep Opportunity

Fiber to the business

CPE

CPE

Metro Biz Services

100GBackhaul

Deepfiber

accessB’cast

CCAPFiber to the node

21 | © 2017 Infinera

Market Expansion

How Infinera Wins

22 | © 2017 Infinera

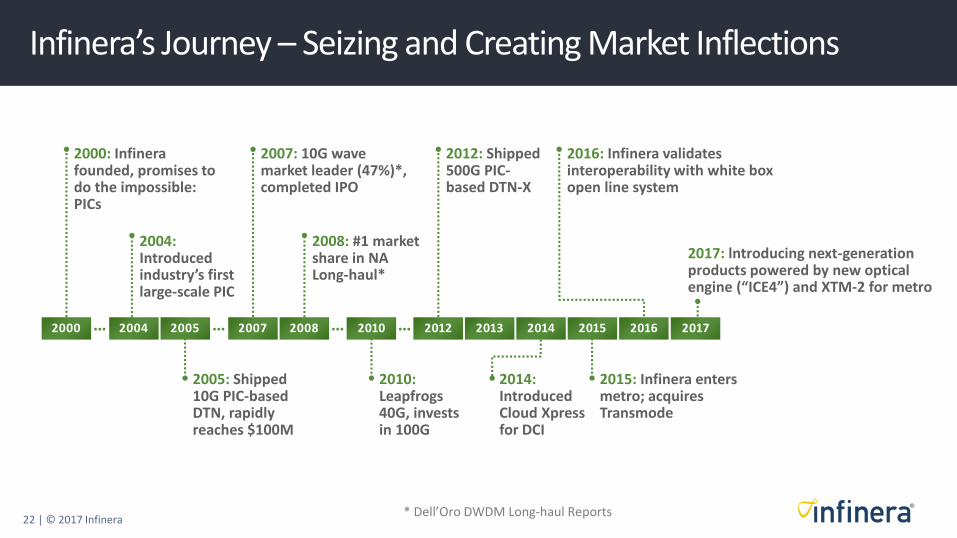

Infinera’s Journey – Seizing and Creating Market Inflections

* Dell’Oro DWDM Long-haul Reports

2005: Shipped 10G PIC-based DTN, rapidly reaches $100M

2007: 10G wave market leader (47%)*, completed IPO

2000: Infinera founded, promises to do the impossible: PICs

2004: Introduced industry’s first large-scale PIC

2014: Introduced Cloud Xpress for DCI

2015: Infinera enters metro; acquires Transmode

2016: Infinera validates interoperability with white box open line system

2008: #1 market share in NA Long-haul*

2017: lntroducing next-generation products powered by new optical engine (“ICE4”) and XTM-2 for metro

2010: Leapfrogs 40G, invests in 100G

2012: Shipped 500G PIC-based DTN-X

…2000 2004 2005 2007 2008 2010 2012 2013 2014 2015 2016 2017…… …

23 | © 2017 Infinera

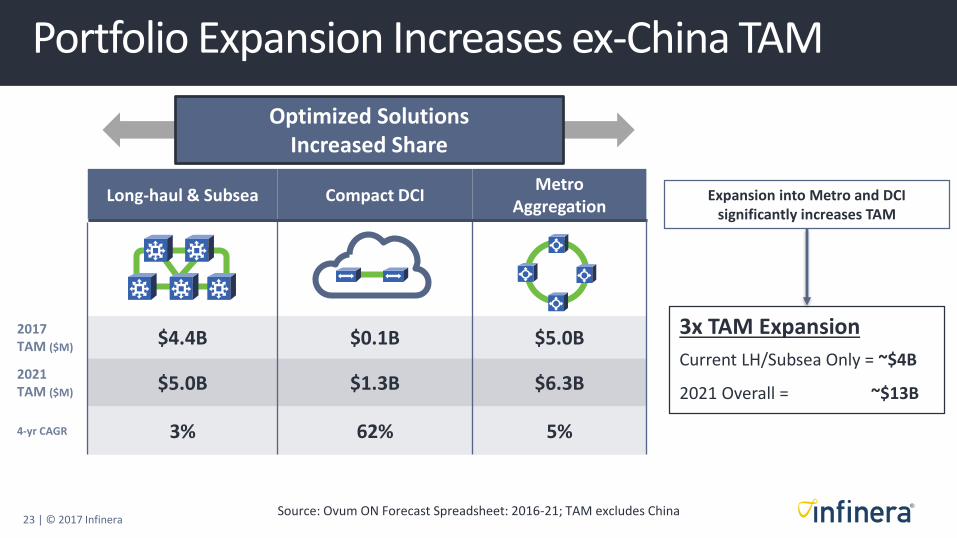

Portfolio Expansion Increases ex-China TAM

Long-haul & Subsea Compact DCIMetro

Aggregation

2017 TAM ($M)

$4.4B $0.1B $5.0B

2021TAM ($M)

$5.0B $1.3B $6.3B

4-yr CAGR 3% 62% 5%

Source: Ovum ON Forecast Spreadsheet: 2016-21; TAM excludes China

Optimized SolutionsIncreased Share

3x TAM Expansion

Current LH/Subsea Only = ~$4B

2021 Overall = ~$13B

Expansion into Metro and DCI significantly increases TAM

24 | © 2017 Infinera

Optical Engines At Cloud Cadence

ICE4Up to 2.4T

Up to 200G/λUp to 33 Gbaud

Infinite Capacity Engine Family

2017 2018

ICE6Up to: 6.4T

Up to 800G/λUp to 100 Gbaud

Time

ICE5Up to 4.8T

Up to 600G/λUp to 66 Gbaud

ICE NGIn Planning

Targets:1T/λ

128Gbaud

20202019

Ca

pa

city

per

mo

du

le p

air

2021

25 | © 2017 Infinera

Building Blocks

Markets

Our Strategy: How Infinera Wins

DeliverNext-Gen Platforms

Increase Cadence of Optical Engine

Lead in Open:Open APIs,

Open Line Systems

Disaggregated and Integrated Solutions

Optimized per Customer

Balanced Portfolio –LH/SS/Metro/DCI

(End-to-end)

Grow Faster thanthe Overall

Optical Market

Help Customers Transition to “Layer T”and Win in Their Markets

26 | © 2017 Infinera

Differentiated Financial Opportunity

27 | © 2017 Infinera

GrossMargin

Operating Expenses

A Structure to Deliver Differentiated Financials

Structured long-term financial model

High scale integrationUnique pricing

structures

InstantNetwork

Long-haul

DCI

Metro

Fixed cost leverage

R&D = long-term target 20% of revenue

Success basedS&M investment

G&A grows slowerthan revenue

Financial discipline

28 | © 2017 Infinera

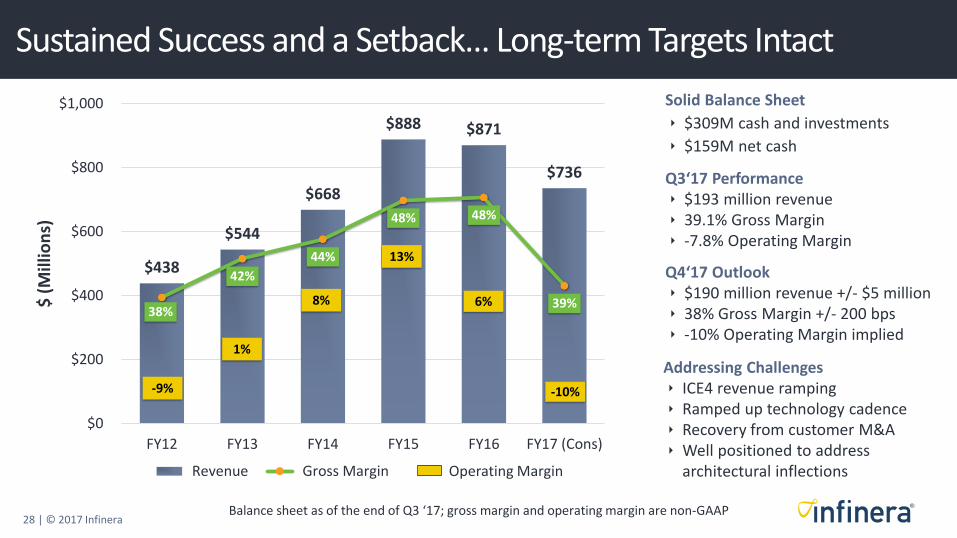

$438

$544

$668

$888 $871

$736

38%

42%

44%

48% 48%

39%

25%

30%

35%

40%

45%

50%

55%

$0

$200

$400

$600

$800

$1,000

FY12 FY13 FY14 FY15 FY16 FY17 (Cons)

$ (

Mill

ion

s)

Revenue Gross Margin Operating Margin

-9%

1%

8%

13%

6%

Balance sheet as of the end of Q3 ‘17; gross margin and operating margin are non-GAAP

Sustained Success and a Setback… Long-term Targets Intact

Q3‘17 Performance $193 million revenue 39.1% Gross Margin -7.8% Operating Margin

Solid Balance Sheet

$309M cash and investments

$159M net cash

Q4‘17 Outlook $190 million revenue +/- $5 million 38% Gross Margin +/- 200 bps -10% Operating Margin implied

-10%

Addressing Challenges ICE4 revenue ramping Ramped up technology cadence Recovery from customer M&A Well positioned to address

architectural inflections

29 | © 2017 Infinera

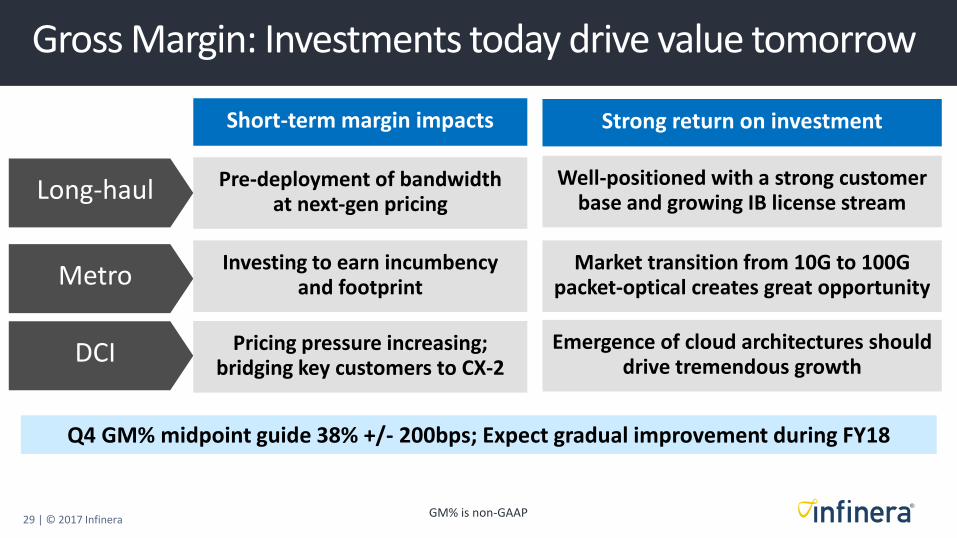

Gross Margin: Investments today drive value tomorrow

Q4 GM% midpoint guide 38% +/- 200bps; Expect gradual improvement during FY18

GM% is non-GAAP

Long-haul Pre-deployment of bandwidthat next-gen pricing

Well-positioned with a strong customer base and growing IB license stream

MetroInvesting to earn incumbency

and footprint Market transition from 10G to 100G

packet-optical creates great opportunity

DCI Pricing pressure increasing; bridging key customers to CX-2

Emergence of cloud architectures should drive tremendous growth

Short-term margin impacts Strong return on investment

30 | © 2017 Infinera

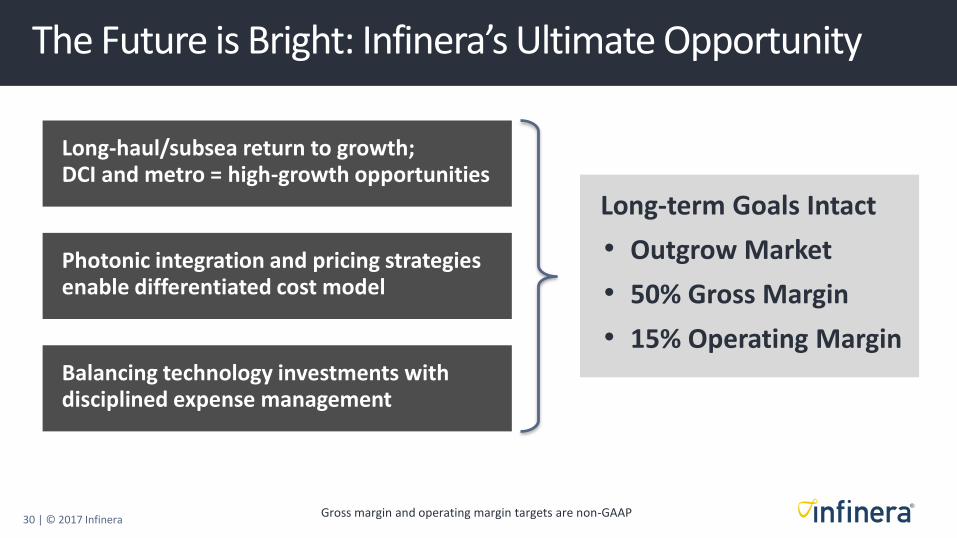

The Future is Bright: Infinera’s Ultimate Opportunity

Long-haul/subsea return to growth; DCI and metro = high-growth opportunities

Photonic integration and pricing strategies enable differentiated cost model

Balancing technology investments with disciplined expense management

Long-term Goals Intact

• Outgrow Market

• 50% Gross Margin

• 15% Operating Margin

Gross margin and operating margin targets are non-GAAP

32 | © 2017 Infinera

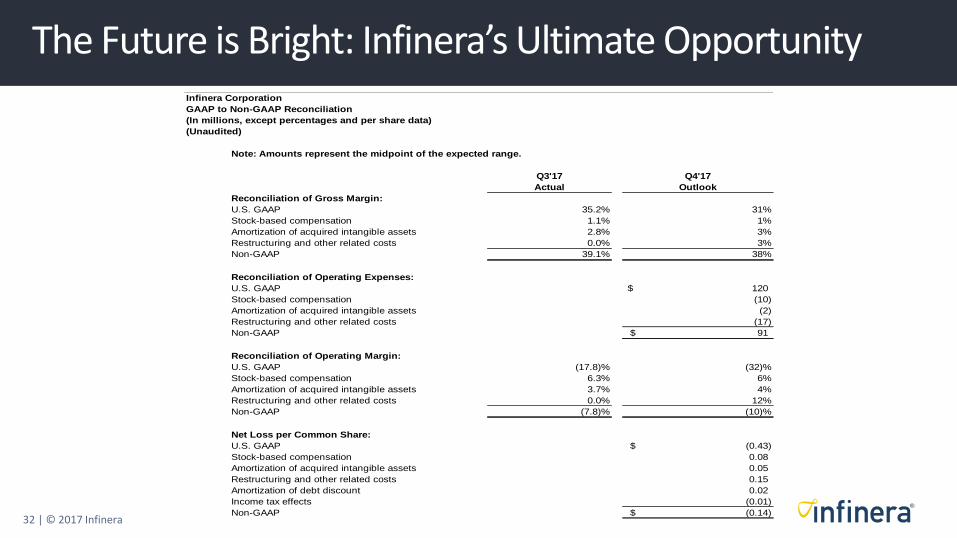

The Future is Bright: Infinera’s Ultimate OpportunityInfinera Corporation

GAAP to Non-GAAP Reconciliation

(In millions, except percentages and per share data)

(Unaudited)

Note: Amounts represent the midpoint of the expected range.

Q3'17 Q4'17

Actual Outlook

Reconciliation of Gross Margin:

U.S. GAAP 35.2% 31%

Stock-based compensation 1.1% 1%

Amortization of acquired intangible assets 2.8% 3%

Restructuring and other related costs 0.0% 3%

Non-GAAP 39.1% 38%

Reconciliation of Operating Expenses:

U.S. GAAP 120$

Stock-based compensation (10)

Amortization of acquired intangible assets (2)

Restructuring and other related costs (17)

Non-GAAP 91$

Reconciliation of Operating Margin:

U.S. GAAP (17.8)% (32)%

Stock-based compensation 6.3% 6%

Amortization of acquired intangible assets 3.7% 4%

Restructuring and other related costs 0.0% 12%

Non-GAAP (7.8)% (10)%

Net Loss per Common Share:

U.S. GAAP (0.43)$

Stock-based compensation 0.08

Amortization of acquired intangible assets 0.05

Restructuring and other related costs 0.15

Amortization of debt discount 0.02

Income tax effects (0.01)

Non-GAAP (0.14)$