willis re lsg value proposition_121814

TRANSCRIPT

WILLIS RE LIFE SOLUTIONS GROUP VALUE PROPOSITION

Willis Group

Headquartered in London / NYC

Traded on NYSE (WSH)

CEO: Dominic Casserley

2013 commission and fees: $3.7B

Approximately 18,000 employees in

over 120 countries

2

Property, 49%

Casualty, 31%

Life, Accident & Health, 2%

Surety, 2%

3

Willis Re global outreach and experience

Made up of over 1,500 employees across 39 offices in Africa,

Australia, Asia, Europe, Middle East and North America

3rd largest and fastest growing global reinsurance broker with

2013 Revenue of $531M

Decades of combined experience in each office with specialists

in:

– Facultative and Treaty reinsurance

– Financial & Actuarial analytics

– Rating Agencies

– Alternative reinsurance solutions

Resources across the globe allow for business leverage

U.S. Life Executive Team

Michael Kaster, FSA, MAAA, MBA - Senior Vice President

– 30+ years of insurance/actuarial executive leadership experience,

both with direct writers and as a senior actuarial consultant.

– Deep industry knowledge and relationships, which facilitates client

development and solution implementation.

Amit Ayer, FSA, MAAA, FRM – Vice President

– Significant life insurance industry and consulting experience in

structuring, advising and managing life and annuity risks, domestic

and international.

– Leads our analytical approaches through use of technical tools and

industry leading modeling approaches.

4

Willis Re’s Life Solutions Group (LSG) brokerage business model mimics Willis Re’s Property & Casualty brokerage model

5

Dimension Traditional brokerage

model Willis Re LSG brokerage model

Willis Re LSG

brokerage

advantage

1 Broker

compensation Ceding company may pay

portion of broker fee Ceding company pays no fee

2 Products Diffuse understanding of

products

Exposures on balance sheet

Deep understanding and experience with life asset-

intensive and traditional life products, long term care,

SPIA, structured settlements and payout annuities

Exposures not taken on balance sheet

3 Analytical

solutions /

capabilities

Minimal investment in modeling

capabilities and infrastructure to

support brokerage process

Dedicated analytics team (AXIS and other platforms) to

model asset intensive life business

Analytics group led by experienced former consultant with

12+ years of advisory experience

4 Interaction

with ceding

company

Loosely affiliated relationship

Trusted advisor of ceding company (work hand in-hand)

Improve efficiency of transactions between markets and

ceding company through analytical rigor, alleviating conflict

management

5 Interaction

with market

markers

Minimal interaction with market

makers

Work hand-in-hand with reinsurers and other market makers

to ensure best price execution and optimal transactional

structure

6 Access to

markets Traditional reinsurance markets

Supplement to direct reinsurer relationship

Partner with non-traditional and alternative markets to

pursue specific market needs and solutions

Significant advantage for Willis LSG Model Significant advantage for traditional brokerage model

EXAMPLES OF WILLIS RE’S EXPERIENCE WITH LIFE PRODUCTS

7

Examples of LSG Engagements

Offering Description Examples

1 Capital

management

solutions

Strong analytics and sophisticated structures to

optimize capital efficiency

Portfolio analysis and capital restructuring to

support new business strategies

Obtaining embedded value in closed blocks

Disposition or acquisition of specific risks

Optimizing capital efficiency with intra-group

transactions

Capital financing via reinsurance solutions

2 Risk Solutions

Structures to release capital and finance future

company growth

Targeting specific risks to enhance the company’s

risk-based capital (RBC) position through product

diversification

Understanding of risk appetite of ALL Reinsurance

markets.

Improve ROE by structuring solution for

older legacy business with low returns and

volatile earnings

3 Capital

Deployment

Solutions

Partnering with business development and

alternative market distribution to pursue specific

market niches

Access to “best in class” alliances with distribution

groups and select insurers and reinsurers

Products include Life Insurance, Annuities (Fixed,

Indexed and Variable), and Long Term Care

Roadmap to deploy capital into new

ventures, through partnerships and/or

reinsurance solutions

Propose multiple solutions for LTC business,

including a bifurcated structure, splitting the

investment risk from the morbidity risk, via

different solution providers

Life insurance products are exposed to credit, interest rate, equity, and underwriting risks

Risks

Product Description Sub-products

GAAP

standard Credit

Interest

rate Equity

Under-

writing

Individual

annuities

Fixed

Immediate

Earn a fixed rate for the life of

the contracts

Single-premium

immediate annuity

Structured settlement

FAS 60

Fixed

Deferred

Earn a fixed rate for a period followed by

a floating rate set by the insurer

FAS 97

Variable Premiums are invested in separate

account funds earning a floating rate

Living benefit VA

Death benefit VA

FAS 133/

SOP 03-1

Individual

life

Term Life Provide a death benefit over a specified

benefit period with no cash value

FAS 60

Permanent

Life

Provide life insurance with cash value

accumulation, not contingent on

specified benefit period

Whole life

Universal life

FAS 60

Long-term

Care (LTC)

Provide benefits based on need for long-

term care

FAS 60

Group Group

Benefits

Provide life insurance for groups Group life insurance FAS 60

Retirement

Retirement

Benefits-

GICS

Guarantee institutional clients principal

repayment and a fixed/floating rate

Defined contribution

Defined benefit

FAS 97

Defined

contribution

Provide benefits based on contributions

by institutions/employees plus invest-

ment earnings

FAS 97

Defined

benefit

Provide fixed benefit for employees over

specified period

FAS 60

Significant risk exposure Some risk exposure

Surrender Charge

The standard cash flows involved in a variable annuity contract are depicted below

Variable Annuity –

key cash flow diagram

9

Variable Annuity – key cash flow descriptions

Cashflow Description

Initial

Commission

Paid by insurer to adviser at policy issue

Typically ~ 5% of deposit

Trailer

Commission

Paid by insurer to adviser in Years 2+ while business is

inforce

Typically 0.5% – 1%. May be a function of deposit or AV

Investment

Management

Fee

Fee charged for the management of the funds

in policy

Typically 150 – 200 bps of AV

Investment manager shares IMF with insurer

Insurance

charge

Sometimes called M&E

Typically 10 – 20 bps of AV

Rider charge Fee to support rider

Ranges between 50 – 100 bps of GV

Admin charge Fee for contract admin; usually $30

Surrender

charge

Paid by policyholder to insurer in the event of lapse (to

compensate for commissions paid)

Typically 7 – 8%; declining by 1% pa

Separate

Account

Policyholder

Investment manager

Advisor

General

Account

Deposit

Commission

(Initial +

Trailer)

IMF = Investment

Management Fee

IMF

Insurance charge

Administrative Charges

Rider charge

Expenses

(e.g.,

Marketing,

Maintenance)

Revenue

sharing

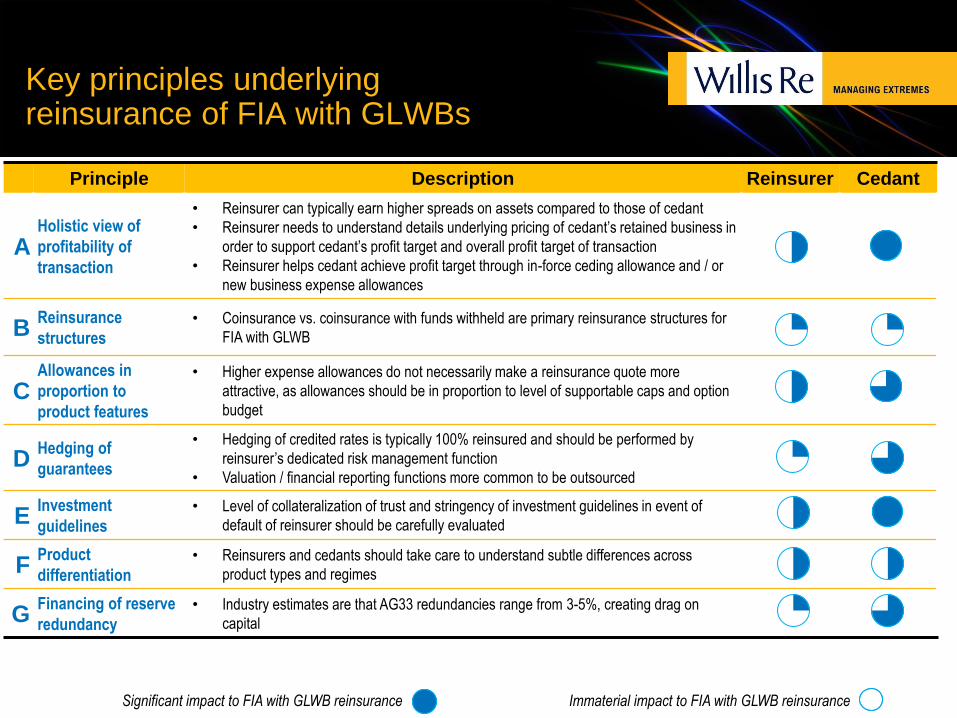

Key principles underlying reinsurance of FIA with GLWBs

Principle Description Reinsurer Cedant

A Holistic view of

profitability of

transaction

• Reinsurer can typically earn higher spreads on assets compared to those of cedant

• Reinsurer needs to understand details underlying pricing of cedant’s retained business in

order to support cedant’s profit target and overall profit target of transaction

• Reinsurer helps cedant achieve profit target through in-force ceding allowance and / or

new business expense allowances

B Reinsurance

structures

• Coinsurance vs. coinsurance with funds withheld are primary reinsurance structures for

FIA with GLWB

C Allowances in

proportion to

product features

• Higher expense allowances do not necessarily make a reinsurance quote more

attractive, as allowances should be in proportion to level of supportable caps and option

budget

D Hedging of

guarantees

• Hedging of credited rates is typically 100% reinsured and should be performed by

reinsurer’s dedicated risk management function

• Valuation / financial reporting functions more common to be outsourced

E Investment

guidelines

• Level of collateralization of trust and stringency of investment guidelines in event of

default of reinsurer should be carefully evaluated

F Product

differentiation

• Reinsurers and cedants should take care to understand subtle differences across

product types and regimes

G Financing of reserve

redundancy

• Industry estimates are that AG33 redundancies range from 3-5%, creating drag on

capital

Significant impact to FIA with GLWB reinsurance Immaterial impact to FIA with GLWB reinsurance

Profit targets for both reinsurer and cedant must be considered in FIA with GLWB reinsurance

11

Reinsurers can typically earn higher

spread on assets (10% in example) than

cedant can

However, given higher spreads on assets,

reinsurer cannot propose high option

budget (5% in example) and supportable

caps (10% in example) to cedant, as

cedant will be unable to support profit

margin at proposed option budget and

cap

Reinsurer ensures profit margins for

cedant is met through ceding allowances

(e.g., % of reserves)

Reinsurer must have detailed

understanding of the profit objective of the

cedant (e.g., non-ceded FIA with GLWB

business) in order to quantify ceding

allowance

Derivation of option budget for FIA with GLWB - reinsurer

3.0%

10.0%

1.0%

0.8%

0.7%

2.5%

3.0%

5.0%

0%

2%

4%

6%

8%

10%

12%

14%

Risk free rate Spread onAssets

Defaults Acquisitioncosts

Maintenancecosts

Minimumcrediting rate

Cost ofcapital /

profit

Optionbudget

5% option budget would

support approximately a

10% cap

10% spread based on

investments in riskier

assets (illustrative)

Observations

Translates into

profitability of FIA with

GLWB (e.g., 12% IRR)

Initial 1 2 3 4 5 6 7 8 9 10

Initial 1 2 3 4 5 6 7 8 9 10

Initial 1 2 3 4 5 6 7 8 9 10

Interest rate guarantees and surrender options

Fixed annuities are essentially tax-advantaged certificates of deposit (CDs), however

– Insurers set the crediting rate annually, often subject to a minimum guarantee

– Policyholders have access to their funds prior to maturity subject to a surrender charge schedule during the initial

contract years

Insurers choose asset maturities based on expected, but uncertain, policyholder cash flows

The surrender timing is driven by the interest rate environment

– Effective liability maturity extends when rates drop and shortens when rates rise

Rates stay steady at 3%

Customer lapses after 7 years

121 121

0

100

200

1 2 3 4 5 6 7 8 9 10

115 111

0

100

200

1 2 3 4 5 6 7 8 9 10

5% Rates rise to 5%

Customer lapses after 5

years

Rates drop to 1%

Customer lapses after 10

yrs

Assets maturity matches FA

maturity – no loss

Assets sold 2 yrs prior to

maturity at reduced asset

market value – loss of $4

Assets mature, but 3-year

reinvestment returns 2%

less than crediting rate –

loss of $6

Cash Flow Assets Liabilities

125 119

0

100

200

1 2 3 4 5 6 7 8 9 10

3%

1%

5%

3%

1%

5%

3%

1%

Example: Fixed Annuity

Longer-dated liabilities can have structural duration mismatches with assets

SPIA cash flows Cash flow dynamics

Accounting standards

Assets have a maturity shorter than liabilities

Regulations penalize use of derivatives to

address duration mismatch

Upon asset maturity, insurer is exposed to

reinvestment risk

Longer-dated protection products generally

follow FAS 60 accounting standards

Reserves are based on discount rate locked in

at issue (not marked-to-market to reflect

changing market conditions)

Cas

h f

low

Time

Assets Liabilities

Maximum available

asset maturity

Asset duration: 15 yrs

Liabilities duration: 20 yrs

Duration mismatch: 5 yrs

Illustrative example

Example: Single premium immediate annuity (SPIA)

Liquidity / solvency of life insurance liabilities

Highly Liquid Semi-liquid Highly illiquid

• Callable debt and

investment contracts

• Callable but with incentives to

hold securities

– Tax-deferred savings

– High surrender charges

– Guarantees

• Defined liability pay-outs that

cannot be modified

• Pay-outs triggered by

occurrence of insured event

(death, disability)

• GIC

• Senior debt

• Commercial paper

• Fixed deferred annuity

• Variable annuity

• Group annuity

• Defined contribution

• Universal life

• SPIA

• Term life

• Long-term care/disability

• Whole life

APPENDIX

Partial List of companies

We have a broker of record agreement with the following

companies:

16

CNO Financial

Universal Insurance

Vantis Life

Securian Financial

Arch Capital

Deutsche Bank

Humana

National Brokers

CUNA Mutual

Hartford Life

Amerilife

Baltimore Life

Investors Heritage Life

GBG Financial

Western & Southern

Michael Edwards Direct

Universal Life

17

Contact information

Mike Kaster, FSA, MAAA, MBA

Senior Vice President

Life Solutions Group

(E): [email protected]

(T): 212 915 8332

Amit Ayer, FSA, MAAA, FRM

Vice President – Senior Actuary

Life Solutions Group

(E): [email protected]

(T): 212 915 8310

Willis Re

Brookfield Place

200 Liberty Street

New York, NY 10281