why next generation networks? market drivers and ... · market trends: new providers’ revenue...

TRANSCRIPT

1

Why Next Generation Networks? Market Drivers and Quantitative Models for Convergence

Mark Bass

Director, Bell Labs Business Modeling

Lucent Technologies – Proprietary - Use pursuant to company instruction

2

New Types of Users - Why are they important?

They are the children of the baby boomer generation of the 1950s and 1960sThey have grown up with the internetThey like instant responseThey love brands like Apple, Virgin, Nike...They create their own web sites and make CDs and DVDsThey like to personalise and customise the way they interact

3

What do they like to do?Activities revolve around computers, games console, TV, Mobile Phone, Music player.Learning - forget text books and libraries. Want to know something?Just ‘Google’ it…Don’t completely understand the technology – but they know how to use it effectivelyTo define their own

experiences, when they are reachable, and by whom

4

Market Trends:New Providers’ Revenue Model – Other People’s Money

Service Providers

AttractingEyeballsModel

TelecomModel

“87% from Ads 13% from Premium Service”

“0% from Ads 95% from Tranx, 5% VoIP”

-Limited From Ads, (Directory Services ?)-Nearly 100% from Telephony”

“98% from Ads, 2% from Software*”Google

Yahoo!

AOL

MSN

Skype/eBay

“58% From Ads, 42% from Internet Access”

“19% From Ads, 81% from Internet Access”

Riding On-Line Advertising Growth, & to a Lesser Extent Premium Services**

*Google Software: Enterprise Search Appliance, Google Earth, etc; **Yahoo Preimum Services: Music, Game, Telco, SMB

5

Future Competitive LandscapeThree Main Business Models for Providers

Sessions, Content, Advertising

Emerging Service Providers (Google, etc)

Expand on Core Competency: eg content, Capture New Subscribers

Rapid Service Delivery: First to Market

Further Segment User Preferences: Increase Advertising Revenue

Parasite on Networks: Low costs

Build Strength in Mobility: Increase Knowledge of User Preferences

Traditional Providers

Content & Advertising: Increase Revenue

Personalization: IncreaseKnowledge of User Preferences

Enterprise Strength: Limited Competition

Speed to Deploy: First to Market

6

Key Questions From Service ProvidersHow do I characterize my customers?

What services will they buy and how much will they pay for them?

Does the business case prove in

Does a Platform approach (IMS) give me an advantage against Point Solution competitors ?

If so, when should I move to IMS?

1. The answers depend on the Network Operator’s specific situation.2. Modeling is essential to facilitate Decision-making & help Manage

Risk- Multiple Parameters- Rapid Iteration- Business Quantification

7

Service Bundling vs. Service BlendingService bundling offers unified ordering and billing for otherwise separate services.Service Blending enables different services to control one another, providing a unified service experience.

Service Blending (with Unified Control via IMS)

Voice Subscriber

ControlVoice

Data

Video

Voice Network Control

Video Subscriber

Control

Video Network Control

Data Subscriber

Control

Data Network Control

For Voice Connections

For MobileVoice Connections

Third party

Wireline

Wireless

For Data Connections

For VideoVoice Connections

Voice

Data

Video

Unified Control

Wireline

Wireless

Mobile TV

Alerts

Gaming on Demand

Caller ID on TV

Family Finder

Web on TV

Service Bundling

8

Consumer Findings

Willingness to Switch for Blended Services

2006 Lucent Technologies –Western Europe Blended Services Primary Market Research

5% 3% 4%7%

22%

16%19%

14%

3%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1 Definitelywould not

2 3 4 5 6 7 8 9 10Definitely

Would

59%41%

Consumers are generally willing to switch service providers to gain access to blended lifestyle services.

9

Willingness to Pay for Blended Services

Consumer Findings2006 Lucent Technologies –Western Europe Blended Services Primary Market Research

0%

5%

10%

15%

20%

25%

30%

Single Providerw/o Blending

Single Providerw/Blending

While lower price expectations prevail when moving to a single provider, blended services increase the number of potential customers who expect to pay more.

% o

f aud

ienc

e w

ho

expe

ct to

pay

mor

e

10

Consumer Segment Demographics

Consumer Findings2006 Lucent Technologies –Western Europe Blended Services Primary Market Research

HHI $50,000+

HHI under $50,000

Children in household

Male

Married

45-65

25-44

Age 18-24

Female

Median current monthly spending

6.05.78.08.17.3Mean interest in blended services

22%24%21%18%15%Segment size (% of population)

SkepticsOlder Low Income

HHs

Premium Adopters

Fun Techies

Secure & Connected

HHI $50,000+

HHI under $50,000

Children in household

Male

Married

45-65

25-44

Age 18-24

Female

€129Median current monthly spending

6.05.78.08.17.3Mean interest in blended services

22%24%21%18%15%

SkepticsOlder Low Income

HHs

Premium Adopters

Fun Techies

Secure & Connected

Low Average HighLow Average High

€131 €156 €108 €146

11

Revenue Forecast Methodology

RelativeBundle

Adoption

Bundle AdoptionConstraints in year T

AddressableMarket

CurrentSubscriber

Base

ExpectedGrowth/

De-growth

ExpectedBundle

Adoption in year T

Number ofSubscribers per

Year

Expected Demand & Revenue in

year T

BundleSelection

ApplicationCoverage

HighPreference

MaximumService

Adoption

Coeff. OfInnovation

Coeff. OfImitation

Individual service adoption

in year T

Price Constrained Preference

Preference for

Bundle

OptimalPrice

PurchaseLikelihood

A forecast model to estimate the subscriber and revenue potential of Blended Services solutions Based on primary research results, conjoint pricing model, and Bass Diffusion model

12

Estimation of Service Diffusion Coefficients for Next Generation Services

Maximum adoption rates (m) can be derived from primary research data

All consumer features of consumer blended package are categorized into 3 groups to use the the p and q values of the 3 representative services

Example: Bass Diffusion Coefficients p and q

13

Market Simulation of Custom Service Bundles

Communications Portal offers the blended features to compete with 8 other existing blended packages in the market

14

Simulation Results by Segment – Optimal Market Pricing

To maximize the total market revenue potential, the market simulation results indicate that the optimal price for Comm. Portal would be US$30 (~ €23.6) along with other existing blended service offers

Market divided into 2 segments – current operator subscribers have higher preference and purchase likelihood than other subscribersThe optimal price is inclusive of the usage charge per feature in addition to the platform/enabler charge

15

Blended Lifestyle ServicesPlatform (IMS) vs. Point Solution

ENDPOINTS

SESSION

APPLICATION

IM VoIP

… …

Video Conf.

IMS• Common Session control • Privacy and personalization• Single sign-on • Sharing of common data

across applications

IMS• Common Session control • Privacy and personalization• Single sign-on • Sharing of common data

across applications

Master Brand• Single Subscriber Identity• Seamless• Common user experience

Master Brand• Single Subscriber Identity• Seamless• Common user experience

Common Resources• Sharing of common data• Single user profile• Single Sign on• Integrated Web portal experience

Common ResourcesCommon Resources• Sharing of common data• Single user profile• Single Sign on• Integrated Web portal experience

Simplified Converged Apps• Common apps across Networks• Independent applications• Integrated voice/data services

Simplified Converged Apps• Common apps across Networks• Independent applications• Integrated voice/data services

IMS enables service providers to build and launchservices faster, efficiently adapting to market changes

16

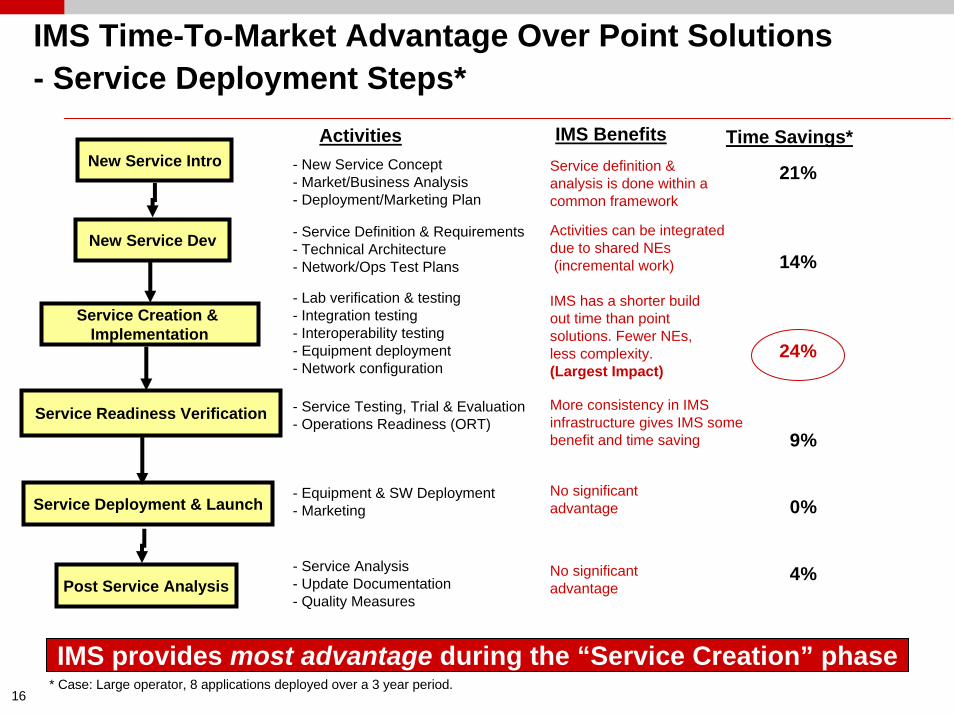

IMS Time-To-Market Advantage Over Point Solutions - Service Deployment Steps*

IMS Benefits Time Savings*- New Service Concept- Market/Business Analysis- Deployment/Marketing Plan

Activities

- Service Definition & Requirements- Technical Architecture- Network/Ops Test Plans

- Lab verification & testing- Integration testing- Interoperability testing- Equipment deployment- Network configuration

- Service Analysis- Update Documentation- Quality Measures

New Service Intro

Service Readiness Verification

Service Creation & Implementation

New Service Dev

Service Deployment & Launch

Post Service Analysis

Activities can be integrated due to shared NEs(incremental work)

Service definition & analysis is done within a common framework

IMS has a shorter build out time than point solutions. Fewer NEs, less complexity.(Largest Impact)

More consistency in IMS infrastructure gives IMS some benefit and time saving

No significant advantage

No significantadvantage

21%

14%

24%

9%

0%

4%

- Equipment & SW Deployment- Marketing

- Service Testing, Trial & Evaluation- Operations Readiness (ORT)

IMS provides most advantage during the “Service Creation” phase* Case: Large operator, 8 applications deployed over a 3 year period.

17

Optimal Deployment Strategy

Transition Cost

IMS time-to-market advantage results in

• significant incremental revenue, with

• slight increase in investment and expense

Early transition to IMS will • reduce transition cost, and• improve profitability by as

much as 24%

Optimal Strategy

18

IMS Reduces Risks of Introducing New Services

• IMS reduces risk and provides a platform for “experimentation”• Opportunity to level the playing field with Internet companies

IMS services are financially viable at lower adoption levels than point solutions

Opportunity to profitably provide services to niche markets

Service adoptionService adoption

100%

80%

60%

40%

20%

0Mobile voice

SMS Service A

Service B

Service C

Service D

Service E

Unattractive services to a non IMS operator

ILLUSTRATIVE

100%

80%

60%

40%

20%

0Mobile voice

SMS Service A

Service B

Service C

Service D

Service E

Unattractive services to a non IMS operator

ILLUSTRATIVE

Both IMS and point solutions viable

Only IMS solutions viable

No solutions viable

***Based on Lucent research and are not indicative or representative of actual results or experience. Actual results could differ significantly from what is shown.

19

Simulation of Market DynamicsSimulation Model – “Optimal Control” formulation of market dynamics

where operator and consumer rational behaviour is explicitly modelledService providers compete for customer shares trying to optimize NPV of their cash

flows, e.g., revenue, operational cost of adding new customers, investment in additional infrastructure

Customers optimize their “value” by selecting freely between offers and their combinations.

Operators adjust offer plans for next

period

Financial resultsand customer

shares analysed by operators

Customer Segments

select from service offers

New transition probabilities

based on plans and utilities

)( 12 bb UUgker −=

Given choice of bundles customer switches to another bundle at the rate ofCurrent

Mkt StateStrategicAction A Strategic

Action BStrategicAction C

Mkt StateII

StrategicAction A Strategic

Action BStrategicAction C

Mkt StateIII

StrategicAction A Strategic

Action BStrategicAction C

Mkt StateIV

20

Overall Projected Share for Voice, Convergence and Data Offers

DMS offer is the only service with steady growthCable-data offer remains flat mainly due to being included in more bundles, including the converged offers

The two converged offers that include data, wireline, and wireless voice are the front-runnersPlain WiFi roaming offers (BYOBB), only gain moderate market sharesDMS has an advantage over the closest rival mainly due to sticky, value-added services

Share Dynamics by Offer

02468

101214161820

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20quarters

Nor

mal

ized

Mkt

Sha

re, M

P OT S D ata - D SL D ata - C B L Wireless D M S

Market Share Dynamics - Converged Voice

0123456789

10

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Quarters

Nor

mal

ized

Mkt

. Sha

re, M

SP1/SP2 SP3 SP5/CBL SP4 SP6

Anywhere blended minutes,B’band, &VAS

Bundled minutes&B’band

BYOBB

21

Simulation Results for Dual-Mode ServiceMarket Share Simulation Scope:

– Specific Region: 7 operators, 7 offer types, 40 service bundles, 6 market segmentsImpact of Dual- Mode Service on DSL Churn

1.50%

1.90%

2.30%

2.70%

3.10%

3.50%

2007 2008 2009 2010 2011

Mon

thly

Chu

rn in

DSL

More than 30% drop in 5 years

No Dual-Mode

With Dual-Mode

Market Share Dynamics - Converged Voice

25%

35%

45%

55%

65%

75%

85%

2007 2008 2009 2010 2011

Mkt

. Sha

re, %

More than 3 to 1 advantage in 5 years

Converged Operator

Mobile Operator

Converged operators increase market share:

− Converged platforms enable coordination of Family Number, Personal Number, etc

− Integration of Mobile and Wireline voice features with data services

Introduction of Dual-Mode Service can reduce churn on DSL

− Service integration increases Dual-Mode offer stickiness

− Dual-Mode Service includes DSL service, and as Dual-Mode Service adoption increases, overall DSL churn reduces

Operators Offering Converged Voice and Data Services Can - Build Significant Market Share Advantage, and - Reduce Churn on Their Existing Voice and Data Services

22

Summary: Why Next Generation Networks? Market Drivers and Quantitative Models for Convergence

Operators need to seek new revenue generating services and deploy them efficiently as a way to counter voice erosion and threats from non-traditional players.

– There is pent-up demand for new applications and blended services

IMS provides an efficient deployment platform for launching next generation services

– As the number of services increase, the added efficiency builds up quickly– Services are deployed faster, translating into higher revenue potential– In a competitive environment, the impact on profitability will be significant– Positive cross-elastic impact on existing broadband services– Platform efficiencies also translate into operational savings

As competition increases, growing commitment to Converged Services is a key strategy

– Converged, blended services will be key to customer acquisition and retention

Operators need to explore new business models to exploit the convergence of all media