what’s old is new: white-labeling trends in the dc...

TRANSCRIPT

1

ModeratorWinfield Evens, CFA®

Director of HRO Investment Solutions & StrategiesAon Hewitt

What’s Old is New: White-Labeling Trends in the DC Marketplace

SpeakersJeffrey S. Coons, Ph.D., CFA ®

President, Co-Director of ResearchManning & Napier

Kendall FrederickSenior Manager, Finance IntegrationHanesbrands, Inc.

David HeinyDC Practice LeaderArtisan Partners

Erik LinvogManager Benefit InvestmentsDaimler Trucks North America

2

Poll of the Audience• What is your DC plan’s approach to White Labeling?

1.) We do it today2.) We have considered it, and may do it in the future still3.) We have considered it, and have rejected the approach4.) We have not formally considered the approach yet5.) I am not sure what you mean by White Labeling

Special thanks to our diamond sponsor: 2

3

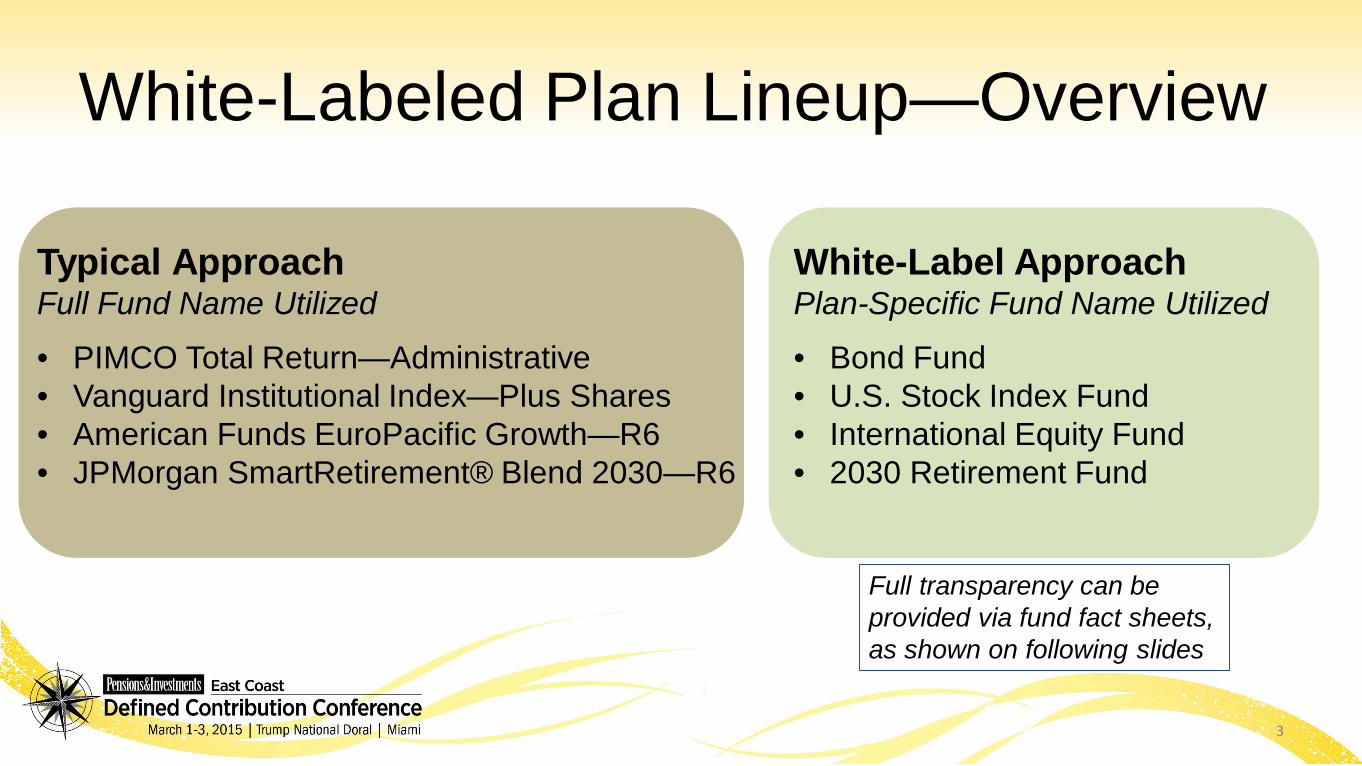

White-Labeled Plan Lineup—Overview

Typical Approach Full Fund Name Utilized

• PIMCO Total Return—Administrative• Vanguard Institutional Index—Plus Shares• American Funds EuroPacific Growth—R6• JPMorgan SmartRetirement® Blend 2030—R6

White-Label Approach Plan-Specific Fund Name Utilized

• Bond Fund• U.S. Stock Index Fund• International Equity Fund• 2030 Retirement Fund

Full transparency can be provided via fund fact sheets, as shown on following slides

3

4

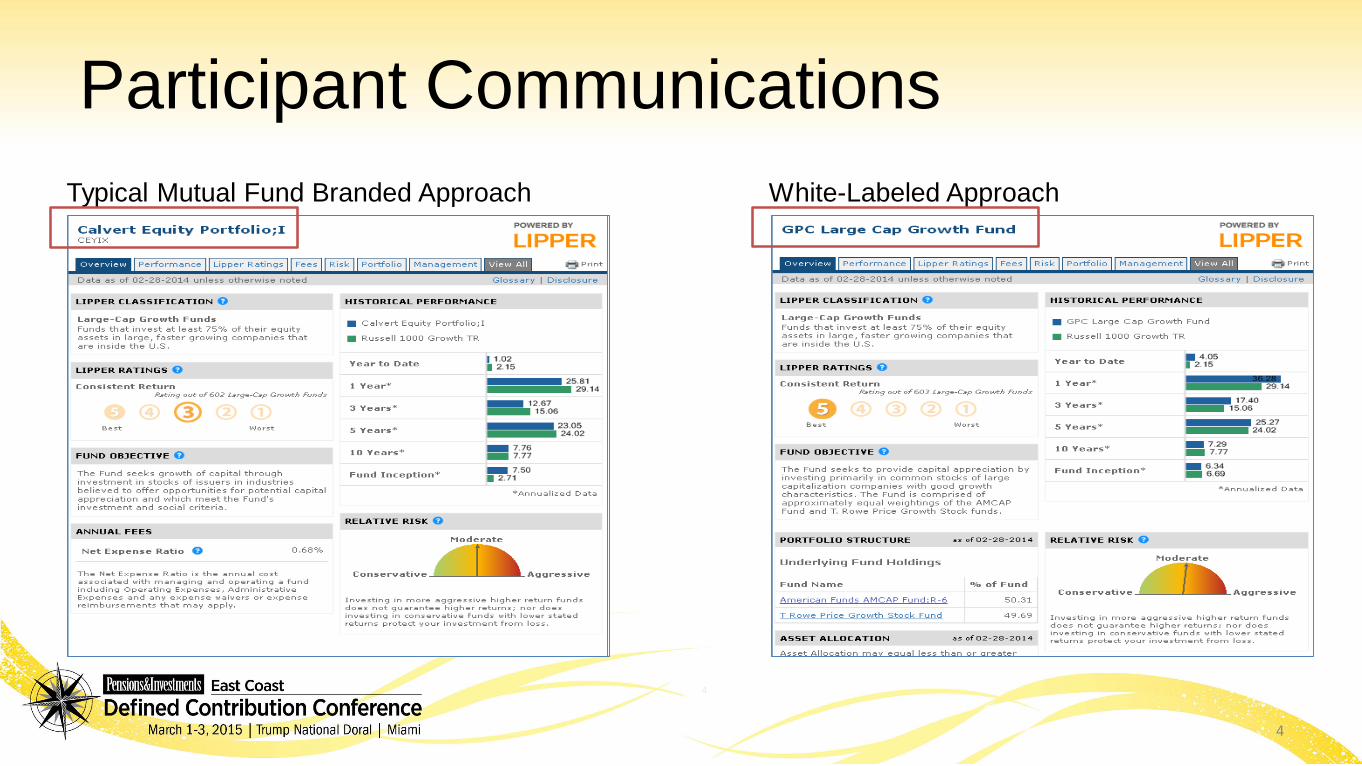

Participant CommunicationsTypical Mutual Fund Branded Approach White-Labeled Approach

4

5

Participant CommunicationsWhite-Labeled Examples

5

6

Large Cap

Equity

Large Cap

Value

Large Cap

Blend Large Cap

Growth

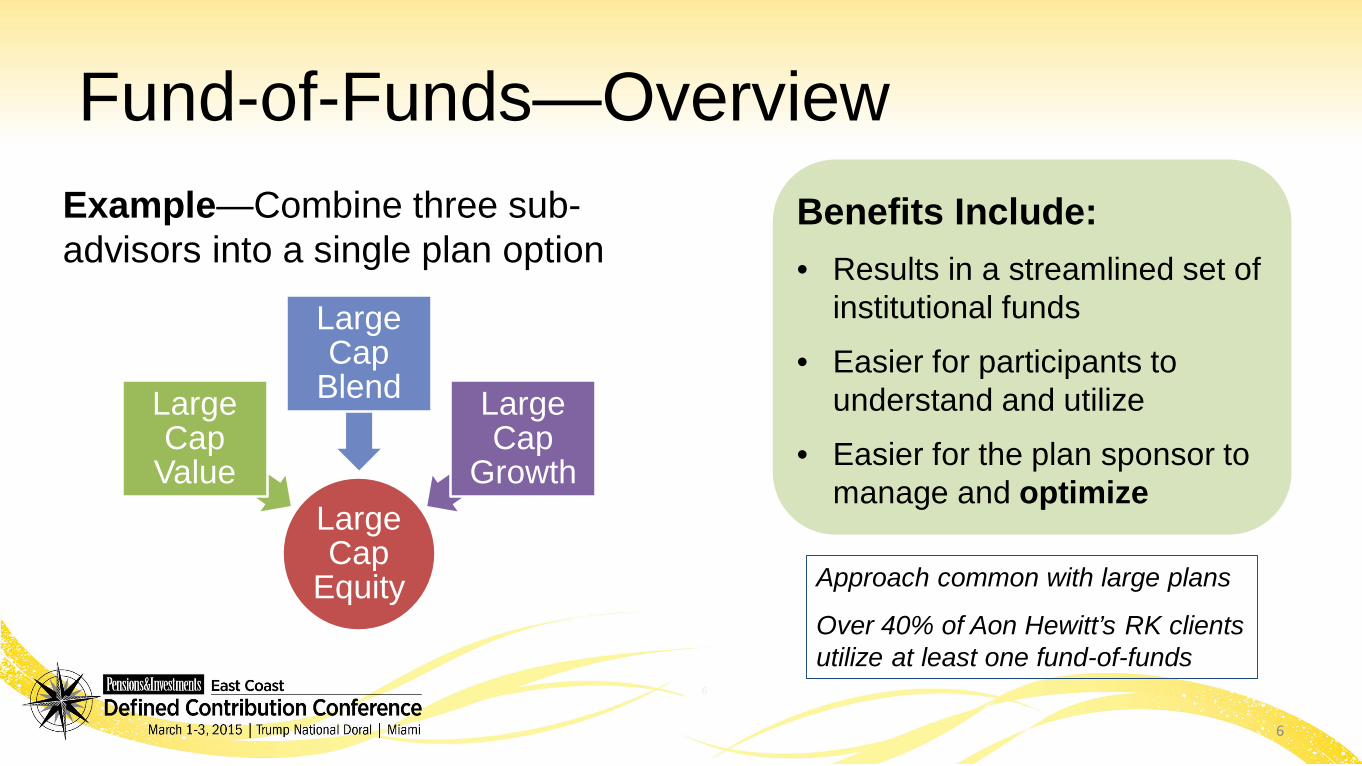

Example—Combine three sub-advisors into a single plan option

Fund-of-Funds—Overview Benefits Include: • Results in a streamlined set of

institutional funds

• Easier for participants to understand and utilize

• Easier for the plan sponsor to manage and optimize

Approach common with large plans

Over 40% of Aon Hewitt’s RK clients utilize at least one fund-of-funds

6

7

Plan Structure—Illustrative SpectrumTypical Brand Name Approach

Vanguard Prime Money Market

Galliard Stable Value

Lord Abbett Short Duration Income

PIMCO Total Return—Admin.

BlackRock US Debt Index

Goldman Sachs Strategic Income

Templeton Global Bond

Vanguard Inflation-Protected Sec.

BlackRock Strategic Completion

Dodge & Cox Stock

Vanguard Institutional Index—Plus

Fidelity Growth Company

NWQ Small-Mid Cap Value

SSgA Small-Cap Index

Wells Fargo Advantage Discovery

Artisan Global Opportunities—Inv.

American Fds. EuroPacific Growth

DFA Emerging Markets—II

WL—Asset ClassApproach

CapitalPreservation

Non-U.S. Equity

U.S. Core Plus Bond

Inflation Protection

Non-U.S. Bond

U.S. Large-Cap Equity

U.S. Small & Mid-Cap Equity

WL—Objectives-Based Strategies

Capital Preservation

Income

InflationProtection

Growth

WL—Asset Style Approach

Money Market

Stable Value

Short-Term Bond

Core Bond--Active

Core Bond--Index

Enhanced Bond

International Bond

TIPS

Real Assets

Large-Cap Value

Large-Cap Index

Large-Cap Growth

Small/Mid-Cap Value

Small/Mid-Cap Index

Small/Mid-Cap Growth

World Equity

International Equity

Emerging Markets Equity

7

8

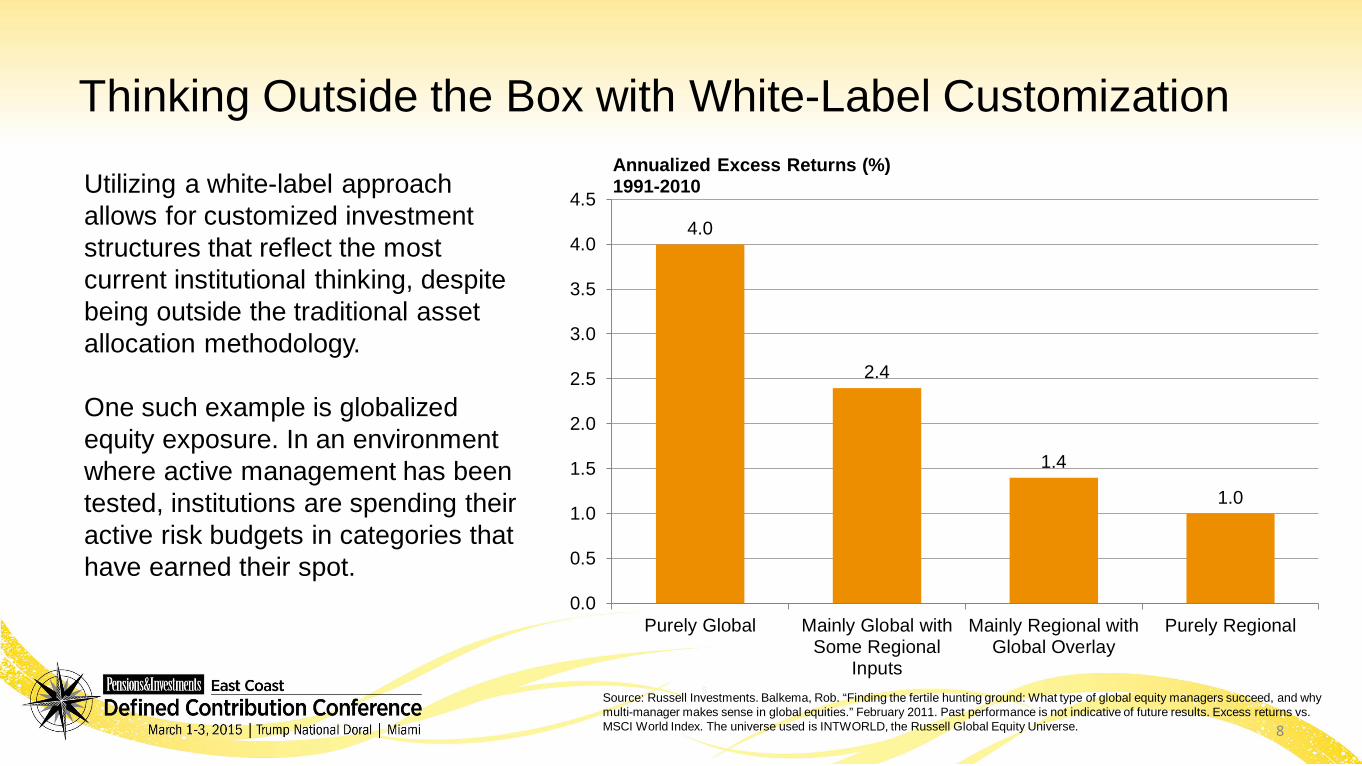

Thinking Outside the Box with White-Label Customization

Utilizing a white-label approach allows for customized investment structures that reflect the most current institutional thinking, despite being outside the traditional asset allocation methodology.

One such example is globalized equity exposure. In an environment where active management has been tested, institutions are spending their active risk budgets in categories that have earned their spot.

4.0

2.4

1.4

1.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Purely Global Mainly Global withSome Regional

Inputs

Mainly Regional withGlobal Overlay

Purely Regional

Annualized Excess Returns (%)1991-2010

Source: Russell Investments. Balkema, Rob. “Finding the fertile hunting ground: What type of global equity managers succeed, and why multi-manager makes sense in global equities.” February 2011. Past performance is not indicative of future results. Excess returns vs. MSCI World Index. The universe used is INTWORLD, the Russell Global Equity Universe. 8

9

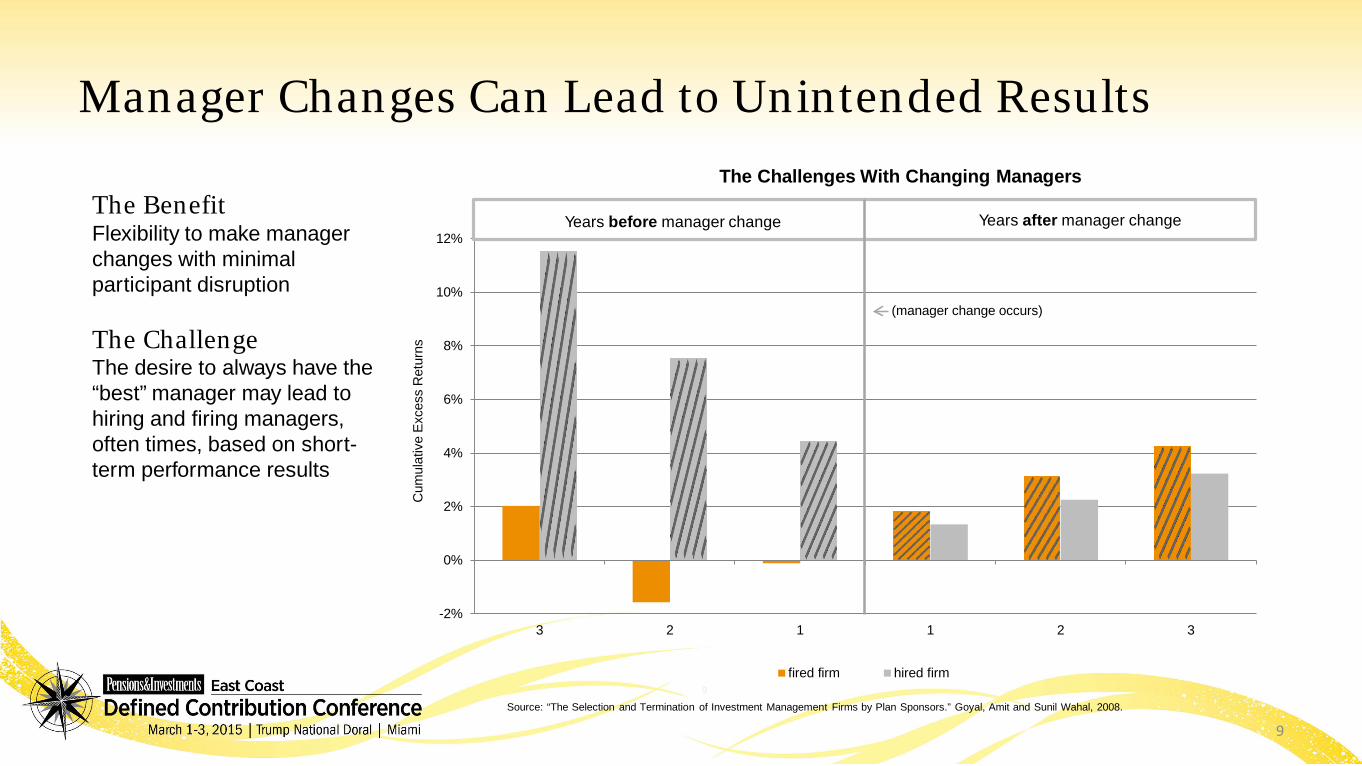

Manager Changes Can Lead to Unintended Results

The BenefitFlexibility to make manager changes with minimal participant disruption

The ChallengeThe desire to always have the “best” manager may lead to hiring and firing managers, often times, based on short-term performance results

The Challenges With Changing Managers

-2%

0%

2%

4%

6%

8%

10%

12%

3 2 1 1 2 3

fired firm hired firm

Years after manager change

Cum

ulat

ive

Exc

ess

Ret

urns

Years before manager change

Source: “The Selection and Termination of Investment Management Firms by Plan Sponsors.” Goyal, Amit and Sunil Wahal, 2008.

(manager change occurs)

9

10

Multi-Manager Portfolio ConstructionHypothetical example

The BenefitDiversify the category with institutional investment managers

The ChallengeCombining managers ina complementary way to avoid the potential for over diversification and index-like returns

0%

10%

20%

30%

40%

50%

60%

70%

80%

Large Cap Fund #1 Large Cap Fund #2 Large Cap Fund #3 Multi-ManagerLarge Cap Fund

Act

ive

Shar

e %

Individual Funds Aggregate Portfolio

Active Share: Effective Tool for Evaluating Managers and Structuring Portfolios

+ + =

66.4% 64.0%67.0%

53.5%

Data shown is for illustrative purposes only. Active share can range from 0% to 100%. A high active share indicates that a portfolio’s investments significantly differ from the benchmark, while the investments of a portfolio with a low active share largely mirror the benchmark. Please note that diversification does not assure a profit or protect against loss in a declining market.

10

11

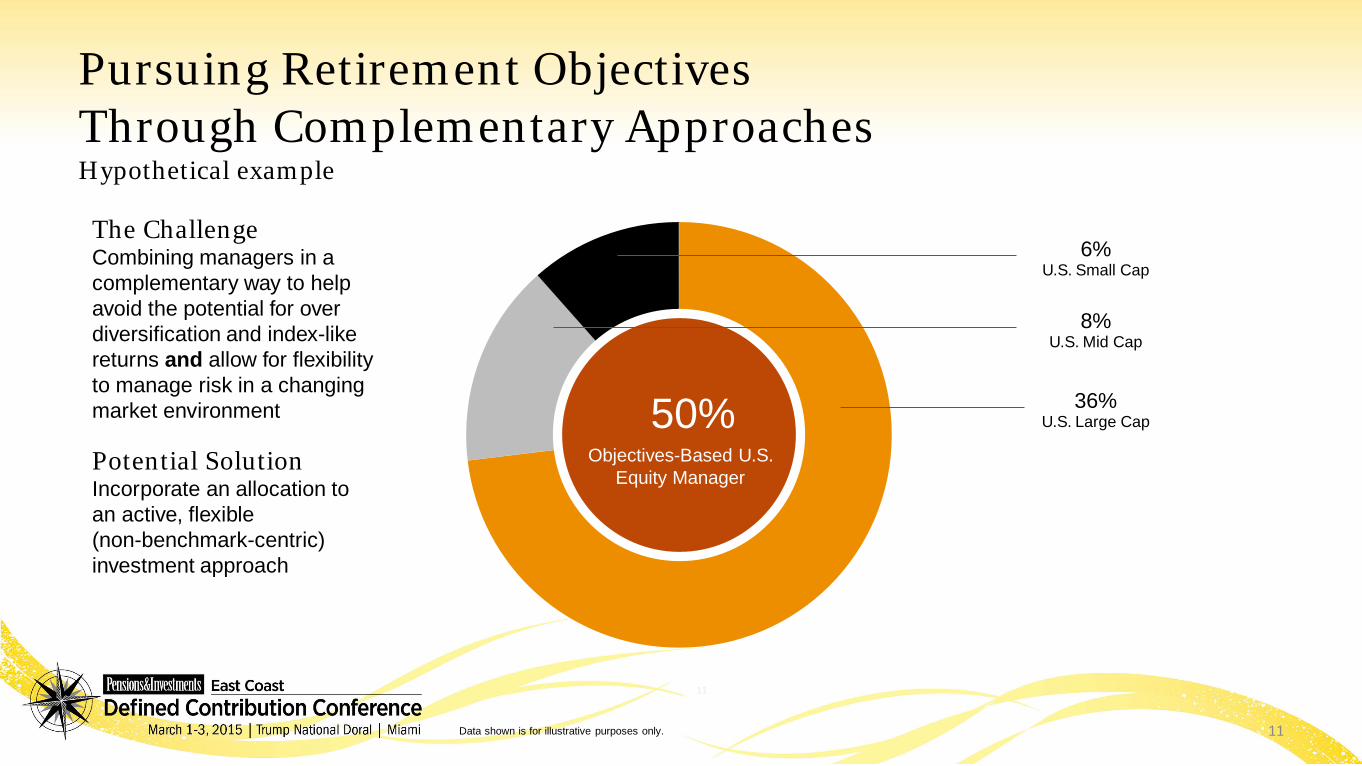

Pursuing Retirement Objectives Through Complementary Approaches Hypothetical example

The ChallengeCombining managers in a complementary way to help avoid the potential for over diversification and index-like returns and allow for flexibility to manage risk in a changing market environment

Objectives-Based U.S. Equity Manager

Potential SolutionIncorporate an allocation to an active, flexible (non-benchmark-centric) investment approach

50% U.S. Large Cap36%

U.S. Mid Cap8%

U.S. Small Cap6%

Data shown is for illustrative purposes only. 11

12

Objectives-Based Manager Mandate: To meet the portfolio objective through active investment in the broad, U.S. Equity market. This manager will be enabled to seek results in line with the portfolio objective by adjusting the portfolio in accordance with the risks and opportunities presented by the prevailing market environment in a benchmark-agnostic manner.

Benchmark-Centric Manager Mandate:To deliver market (passive) or above-market (traditional active) returns based on the opportunity set presented in the stated market benchmark, over a full market cycle. These managers attempt to minimize risk relative to the benchmark by maintaining similar profiles as their stated benchmarks, and can include a style, capitalization, sector, and security constraint perspective.

Portfolio Objective: To seek long-term capital appreciation while mitigating downside risk through investments in the U.S. Equity market

Pursuing Retirement Objectives Through Complementary Approaches

Approved SMA-SEM044 (2/15)

12

13

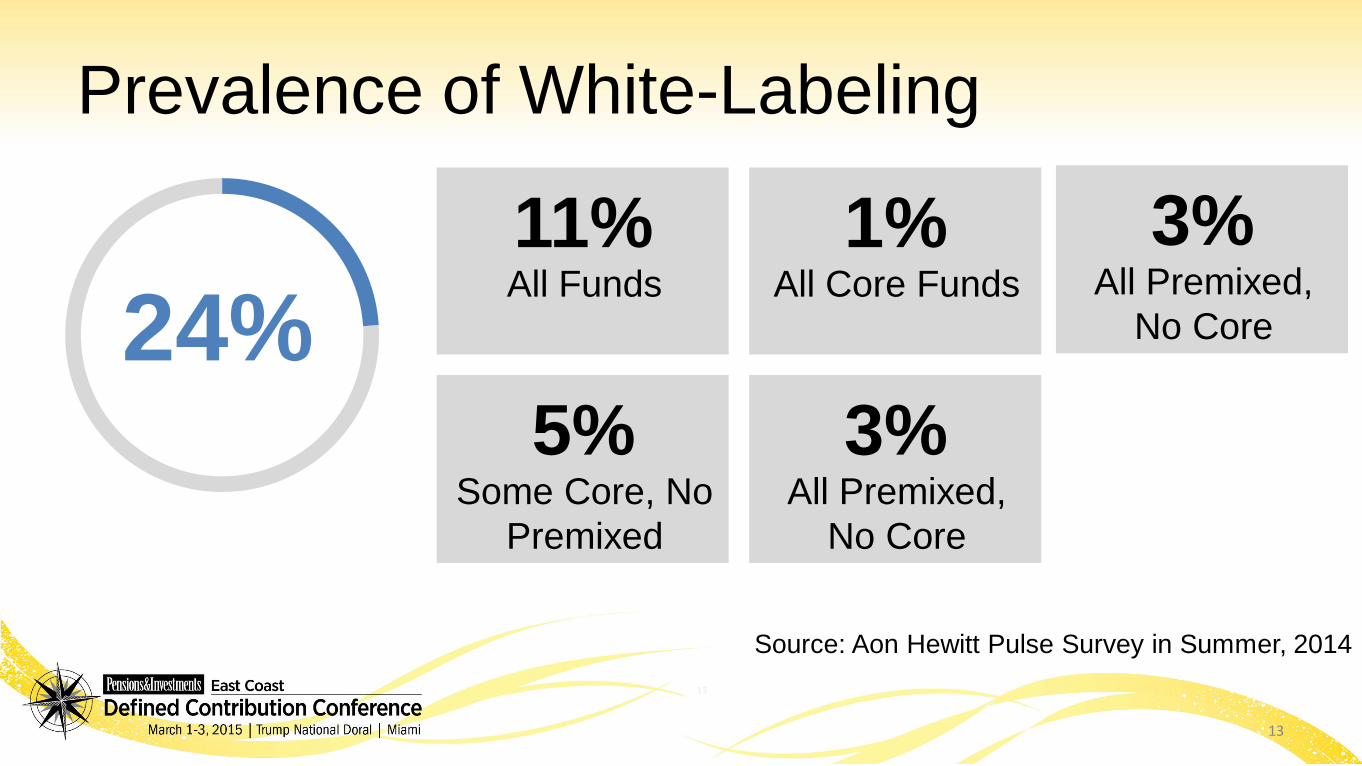

Prevalence of White-Labeling

24%

Source: Aon Hewitt Pulse Survey in Summer, 2014

11%All Funds

5%Some Core, No

Premixed

1%All Core Funds

3%All Premixed,

No Core

3%All Premixed,

No Core

13

14

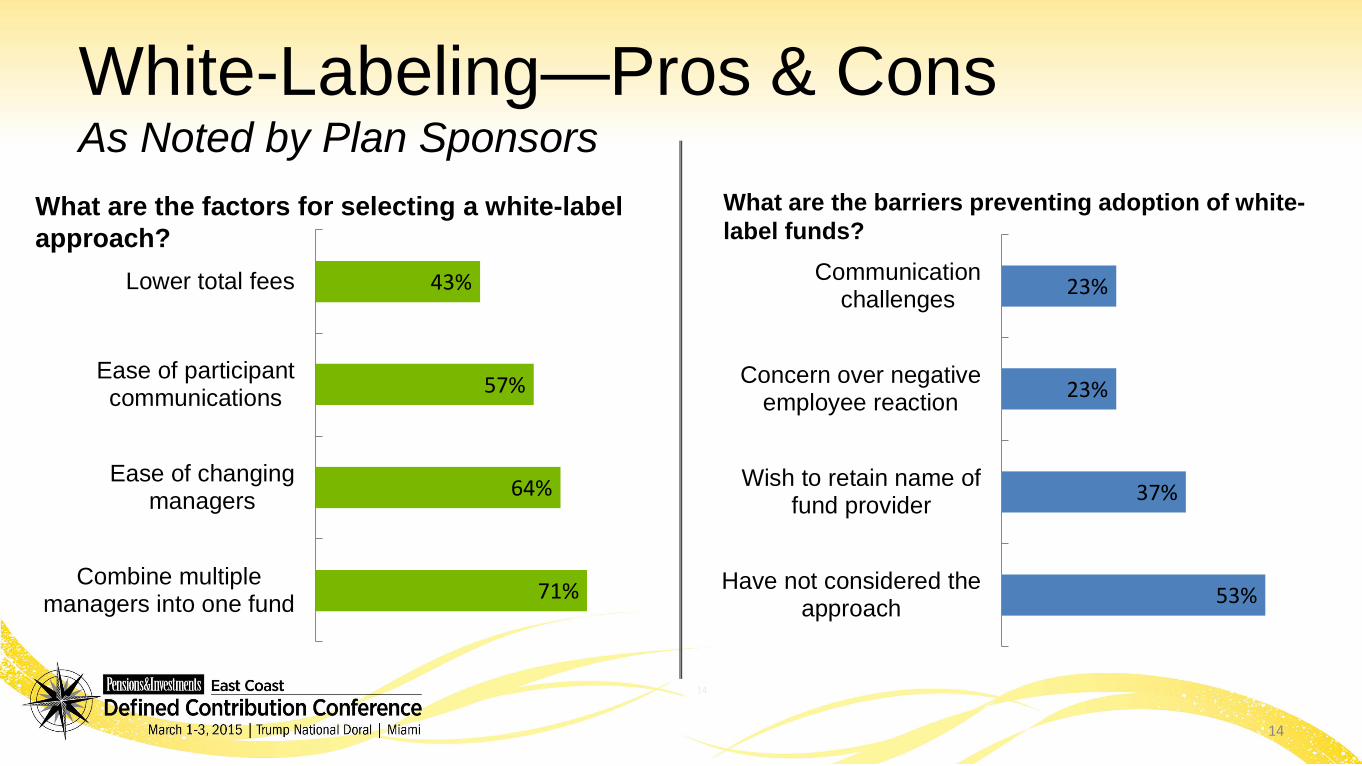

White-Labeling—Pros & Cons As Noted by Plan Sponsors

What are the factors for selecting a white-label approach?

What are the barriers preventing adoption of white-label funds?

53%

37%

23%

23%

Have not considered theapproach

Wish to retain name offund provider

Concern over negativeemployee reaction

Communicationchallenges

71%

64%

57%

43%

Combine multiplemanagers into one fund

Ease of changingmanagers

Ease of participantcommunications

Lower total fees

14

15

Final Thoughts• Implementation requires thoughtful coordination between the:

– Plan sponsor– Investment consultant– Plan administrator– Trustee

• The white-label approach provides plans with a variety of benefits, including:– Simplified decision framework for participants– Better diversification– Improved active management– Opportunities for cost reductions

15