alternatives - conferencesconferences.pionline.com/uploads/conference_admin/pi_030915_alts...eric...

TRANSCRIPT

Advertising Supplement

Alternativesin Defined Contribution Plans

15pi0090.pdf RunDate: 03/09/15 8 x 10.875 Color: 4/C

Investing for Retirement—An Alternative ApproachAQR is a custom retirement investment solutions provider. We focus on both nontraditional investment solutions and innovative long-only style-based investment capabilities to help mitigate retirement savings risks.Employing our unique skill at

portfolio risk environment, we strive to deliver both new and non-correlated sources of excess returns.

term and disciplined — seeks to limit portfolio drawdowns and downside capture.

Rob Caponep: +1.203.742.6736e: [email protected] Capital ManagementTwo Greenwich PlazaGreenwich, CT 06830w: aqr.com

© 2015 AQR Capital Management, LLC. All rights reserved. This information does not constitute an offer

and should not be construed as such nor serve as the basis of any investment decision.

If It Ain’t Broke, Now’s The Time To Fix It 4A Bull Run in Traditional Assets Should Not Make Sponsors Complacent

How Can You Not? 8Today’s Alternatives Offer Myriad Ways to Help Participants Improve Retirement Outcomes

Measuring Value In A Fee-Sensitive World 10Though fees are coming down for alternative strategies, plan sponsors still wrestle with the issue of cost vs. benefits

How Do You Get It Onto The Menu? 12For Most DC Plans, Managers Recommend Buying Rather Than Building an Alts Allocation

Alts in DC 3

SponsorsAQR Capital ManagementTwo Greenwich PlazaGreenwich, CT, 06830Robert CaponeManaging [email protected]

Goldman Sachs Asset Management200 West Street, FL 37New York, NY 10282John AxtellManaging [email protected]

InvescoTwo Peachtree Pointe1555 Peachtree Street, NEAtlanta, GA 30309Eric JohnsonHead of US Sales, Service and Consultant [email protected]

John Hancock Investments601 Congress StreetBoston, MA 02210Todd J. CasslerPresident of Institutional Distribution866.582.2777tcassler@jhancock.comwww.jhinvestments.comJohn Hancock Funds, LLC, member FINRA,SIPC

Neuberger Berman605 3rd AvenueNew York, NY 10158Michelle RappaManaging [email protected]

Contents

Advertising Supplement

“It seemed that after the financial crisis, many investors had a clearer view of the potential value of alternatives, which was

downside protection,” says Donna Wilson, Direc-tor of U.S. Portfolio Management for Invesco Quantitative Strategies. “Now that we have had nearly six years of bull markets in traditional as-sets, investors are eager to fully participate in the upside. It’s a natural behavioral phenomenon that our bias and expectations change as the environ-ment changes.”

In the absence of market extremes (e.g., prolonged periods of volatility or contraction), it can be harder to make the case for alternatives. But she cautions that it’s easy, and potentially dangerous, to overlook the benefits of alts just because the market has been moving direction-ally one way.

“Things can change very quickly,” says Wilson, “and we constantly need to remind ourselves that retirement investing requires a long-term perspective. Over the course of a lifetime, if you

want a smoother ride, that may mean taking some performance off the top, and, potentially, some off of the bottom. That’s how you get a more predictable return and wealth accumulation pattern.”

Her most incisive point is this: “Unfortu-nately, you cannot achieve that after the fact.” Thus, she argues that participant portfolios should be structured to weather a wide variety of economic and investing environments. “That could potentially mean that you don’t achieve the best returns in bull markets,” she says, “but it also should mean that you don’t participate in the worst part of down markets either. Unfortunately, you have to live through various cycles to actually achieve that objective and be confident that your portfolio is structured appropriately. So patience is required, because in many cases investors began implementing, or starting to implement, alternatives in a post-crisis environment.”

And she says that the background to all this needs to be a steely-eyed appraisal of risk.

All Environments(Average Over

Period)

Overheating(Growth Up +Inflation Up)

“Goldilocks”(Growth Up +

Period)

Stagflation(Growth Down +

Inflation Up)

Recession(Growth Down +Inflation Down)

-5%

0%

5%

10%

15%

Aver

age

Exce

ss o

f Cas

h Re

turn

s

Global 60/40 Simple Global Risk Parity

3.6%

7.1%

3.1%

7.5% 7.8%

9.6%

-3.4%

3.6%1.3%

6.5%

9.3%

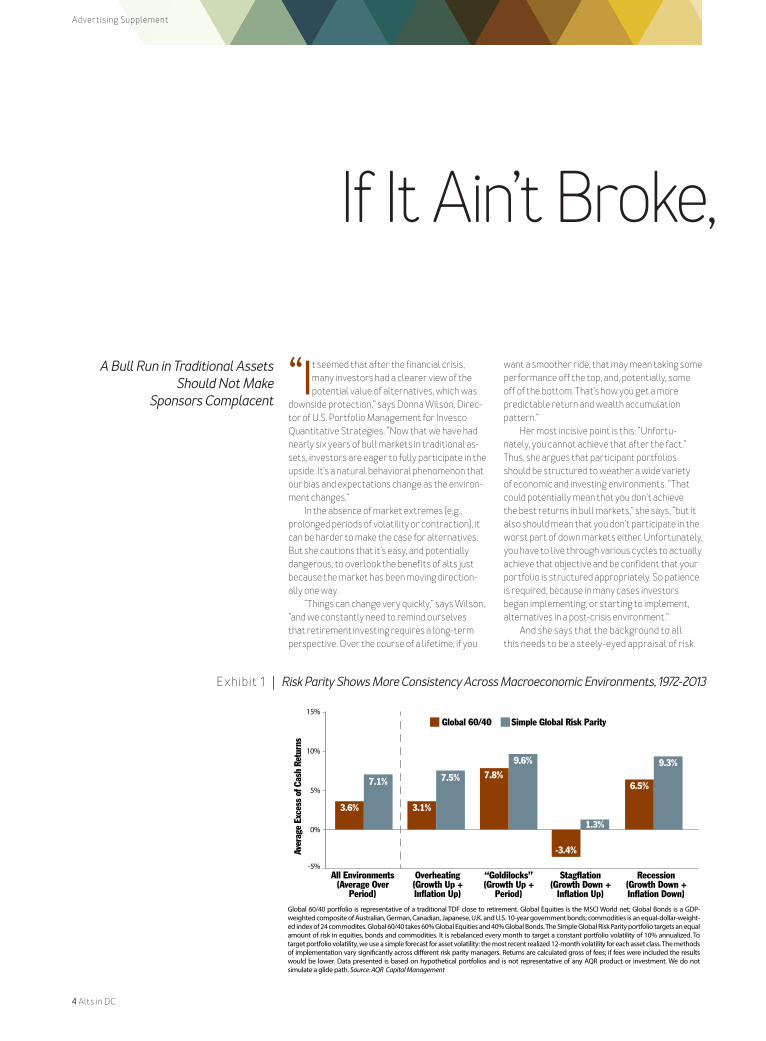

Global 60/40 portfolio is representative of a traditional TDF close to retirement. Global Equities is the MSCI World net; Global Bonds is a GDP- weighted composite of Australian, German, Canadian, Japanese, U.K. and U.S. 10-year government bonds; commodities is an equal-dollar-weight-ed index of 24 commodites. Global 60/40 takes 60% Global Equities and 40% Global Bonds. The Simple Global Risk Parity portfolio targets an equal amount of risk in equities, bonds and commodities. It is rebalanced every month to target a constant portfolio volatility of 10% annualized. To target portfolio volatility, we use a simple forecast for asset volatility: the most recent realized 12-month volatility for each asset class. The methods of implementation vary signi�cantly across di�erent risk parity managers. Returns are calculated gross of fees; if fees were included the results would be lower. Data presented is based on hypothetical portfolios and is not representative of any AQR product or investment. We do not simulate a glide path. Source: AQR Capital Management

Exhibit 1 | Risk Parity Shows More Consistency Across Macroeconomic Environments, 1972-2013

4 Alts in DC

A Bull Run in Traditional Assets Should Not Make

Sponsors Complacent

Advertising Supplement

If It Ain’t Broke,

Plan sponsors need to ask themselves how they are defining risk and managing it going forward. Wilson asks: “Have I properly thought about risk, and what that ultimately means to participants in terms of wealth accumulation and protection?”

Gary Chropuvka, Head of the Customized Beta Strategies business within Goldman Sachs Asset Management’s Quantitative Investment Strategies team, points out that portfolio diversification within defined contribution plans has reached a new frontier. It now extends beyond traditional asset classes (i.e., equities and bonds) and even satellite asset classes (i.e., emerg-ing markets and commodities). He says that to maximize the chances of generating strong risk-adjusted returns going forward, diversification into non-traditional asset classes and strategies, including liquid alternatives, is of paramount importance.

“DC plan participants only have one shot at

their retirement nest egg,” he says, “and the more diversified they are, the higher the probability of success in meeting their objectives. Currently, DC plans are generally over-allocated to equities.”

Chropuvka says that the diversification power of alternatives is compelling, in both equity bear markets and rising rate environments. In the four equity bear markets since 1990, alts outperformed the S&P 500 Index on average by 27%. The U.S. 10-Year Treasury has seen five rising-rate periods since 1990, and alts outper-formed the Barclays U.S. Aggregate Bond Index by an average of 16% in those five periods. He also says that investors face those kinds of headwinds much more often than they realize: in 53% of the months since 1990, investors have faced either a rising rate month or a bear market equity market month.

Robert Capone, Head of Defined Contribution and Sub Advisory at AQR Capital Management, points out that a simple risk parity strategy shows

much more consistent positive performance over different macroeconomic regimes, compared to a traditional long-only 60/40 portfolio. (See Exhibit 1)

“If you preserve capital on the way down, you obviously have more capital at work,” says Gold-man’s Chropuvka. “But that requires putting more investment dollars into diversifying strategies before the market starts moving against you. And most DC plan participants are not as diversified as they think they are.”

Chropuvka argues that helping participants reach their goals requires having different streams of return that can benefit from different cycles, and that given the outlook for traditional asset classes, DC plans should be moving faster to diversify their asset allocations. “Our concern is that we’d like to help mitigate the chances that investors relive the pain of 2008, or 2000, or even the rising rate environment of the 1970s,”

Alts in DC 5

continues on page 6

Advertising Supplement

Now’s The Time To Fix It

says Chropuvka. “That’s why we are so passionate about diversifying with alternatives.”

Were You Good, Or Just Lucky?“Sponsors may be asking, why do I need this fund in my lineup?” says David Kupperman, Ph.D., co-head of Neuberger Berman Alternative Invest-ment Management and Portfolio Manager to the Neuberger Berman multi-manager, alternative funds. “DC plans have grown over the years with the mass baby boomer demographic accumulat-ing assets for retirement. With simple dollar-cost averaging, they could keep putting money in and with a diversified, multi-strategy fund in their portfolio, be comfortable staying invested even through market blips.”

But in reality, there is an element of good tim-ing to that success — an era in which participant demographics coincided with generally rising markets. Now a majority of defined contribution plan participants are moving closer to retire-ment. The assets they have accumulated over the years are extremely vulnerable to the risks of equity volatility and inflation shocks. In the past, they could stay the course with traditional assets and were well served; now they need different options.

“Protecting participants from the full weights of market drawdowns and volatil-ity is critically important,” says Kupperman. “When they are working with a plan menu of 18 options, and the vast majority are equity funds, complemented by a few money market and core bond funds, that’s not allowing for the type of di-versification that is needed today. And if the menu is lacking robust diversification to help manage volatility, growth and income, then do they have the options for a successful retirement? Probably not.”

According to Kupperman, the risk of invest-ment loss raises an even larger threat. He says that the worst possible outcome after a large drawdown is a panicked rush to the exits. Low volatility, low beta strategies help inves-tors stomach the ride and stay invested. He is concerned that today’s defined contribution plan participants are facing a potentially catastrophic event in which they will fully participate in the next market downturn, then panic and entirely miss the upside — all at the worst possible time in the savings lifecycle. “That is the real power of alts,” says Kupperman, “improving the consis-tency of performance and encouraging them to remain invested.”

According to Robert Capone, Head of Defined Contribution and Sub Advisory at AQR Capital Management, plan sponsors should not get lulled into a false sense of security and believe that participants are diversified and allocated appropriately. He asks: “You may be allocated appropriately based upon the market conditions of today, but what happens if those market condi-tions change? What happens if we have another 2008 market event? The industry is not prepared for such an event because we are still so heavily over-allocated to equities from a risk perspective,

particularly a home bias toward U.S. equities.” He points out that target-date funds are

thought to be well diversified because their strategic asset allocation to equities fall from 85% in the beginning to 55% through the retire-ment years. In reality, he says that 90% or more of the risk in a target-date portfolio remains in that equity allocation, since equities are four times riskier than bonds. (Exhibit 2)

“There is work to do on the part of plan spon-sors to recognize that, as fiduciaries, we have a problem to deal with around DC investment plan design,” says Capone. “We are in a very low infla-tionary environment. Volatility remains muted, for the most part. Equity markets have been gen-erating high returns. Why worry? We get lulled into this belief that it’s all going well. Investors who have stayed the course with a high allocation to equities have recouped most, if not all, of their drawdown from the 2008 financial crisis. But near-retirement investors who bore the brunt of equity ‘tail risk’ were not so fortunate.”

Capone counsels that defined contribution plan investing is a long-term investment proposi-tion, and over a 40-year work lifecycle it requires

a range of allocations to suit a range of scenarios. That includes high inflation regimes, as well as equity bear markets. “Those conditions don’t necessarily exist today,” says Capone. “But we still want to maintain long-term strategic alloca-tions that hedge against those possible events, because they will happen at some point. We can’t predict when, so it’s essential that participants are meaningfully diversified into uncorrelated strategies.”

The Dangers of a Market Timing Mentality“One of the reasons why we haven’t seen a tre-mendous amount of flow into alts within DC plans is the spectacular run in the equities market,” says Nathan W. Thooft, CFA, Portfolio Manager for John Hancock Asset Management. “The market has lacked a catalyst to move people toward strategies designed to help provide downside

protection, or manage volatility. So we face an educational challenge around where are we in the market cycle, and where these strategies fit into a portfolio from a performance blueprint perspective.”

He says that the discussion should be less about whether or not to implement alternatives in a defined contribution plan and more about how to get the right balance of alts. Participants need alternatives for diversification, but also for risk reduction, income and return benefits. And in that discussion, it’s important to help partici-pants avoid a market timing mentality, which can impose risks on their investments.

“Today the demand is for alternatives that may be better suited as a fixed income substitute,” says Thooft. “But in our view, another concern is a potential hiccup in equity markets. Rates are likely to go up, but we don’t think they will go to 6% overnight in the 10-year Treasury. So we don’t believe that interest rate risk is as significant as most investors think. On the other hand, it is very probable that at some point, perhaps over the next few years, we could see a 20% drop in the equity market. It may not be prolonged. It could be a very quick correction, but it’s a risk that people are probably underestimating.”

In designing an alts solution, Thooft urges plan sponsors not to get caught up in short-term market dynamics. “The alts universe is pretty wide and inclusive, so one of the best ways for retirement participants to access alternatives is within an asset fund like a target-date portfolio,” he says. “Participants will potentially own a target-date fund for 40-plus years. We suggest they take the time to identify the ones that may add long-term value in terms of wealth accumula-tion, risk reduction and ultimately a better retire-ment outcome.”

Equities

Fixed Income

Other (Cash or Commodities)

Even at retirement TDFs may seem diversified…

…But in practice their risk is still driven by equities

How Dolllars Are Allocated

How Risk Is Allocated

Exhibit 2 | Risk Allocation versus Asset Allocation in Target-Date Funds

“PROTECTING PARTICIPANTS FROM THE

FULL WEIGHTS OF MARKET DRAWDOWNS AND

VOLATILITY IS CRITICALLY IMPORTANT.” David Kupperman, Ph.D.

6 Alts in DC

Sour

ce: A

QR

Capi

tal M

anag

emen

t

Advertising Supplement

15pi0085R.pdf RunDate: 03/09/15 8 x 10.875 Color: 4/C

EXPERTISE in defined contribution and defined benefit plan asset management

DEEP RESOURCES and THOUGHT LEADERSHIP in stable value, non-traditional and alternative asset classes, risk management and qualified default investment options (QDIA)

1 Pensions & Investments, GSAM; October 2013, Based on DCIO AUM. 2 As of December 31, 2014. Assets Under Supervision (AUS) includes assets under management and other client assets for which Goldman Sachs does not have full discretion. 3 As of September 30, 2014 . These materials are provided solely on the basis that they will not constitute investment advice and will not form a primary basis for any person’s or plan’s investment decisions, and Goldman Sachs is not a fiduciary with respect to any person or plan by reason of providing the material or content herein. Plan fiduciaries should consider their own circumstances in assessing any potential investment course of action. The material provided herein is for informational purposes only. It does not constitute an offer to sell or a solicitation of an offer to buy any securities relating to any of the products referenced herein, notwithstanding that any such securities may be currently being offered to others. Confidentiality: No part of this material may, without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient. © 2015 Goldman Sachs. All Rights Reserved. Date of first use: January 16, 2015. 150298.MF.OTU/1/2015

Partnering with Plan Sponsors, Every Day

At Goldman Sachs Asset Management (GSAM), we partner with institutions and consultants every day to deliver thoughtful, dependable solutions that are designed to help participants achieve financially secure retirements.

Goldman Sachs Asset Management Delivers...

Learn more about how GSAM can partner with you. Contact John Axtell at (917) 343-7480 or [email protected].

Established in 1988, Goldman Sachs Asset Management is one of the world’s leading asset managers:

Over $1 trillion in assets under supervision2

Ranked among the top 10 Defined Contribution Investment Only providers1

Over 2,000 professionals based in 33 locations worldwide3

EXPERIENCE that matters in managing alternative asset classes in complex markets

“The question plan sponsors need to ask is, how can they not offer alternatives?” says Michelle Rappa, Managing Direc-

tor and Head of Defined Contribution Marketing at Neuberger Berman. “As the industry has ma-tured, many of the hurdles that once stood in the way of alts implementation have been removed.”

She points to declining fees, which although they are high compared to traditional long-only funds, can be reasonable for what these strategies deliver, and significantly lower than traditional hedge funds. Many alts funds now have three-year track records, a common minimum for defined contribution plans, and more high-quality alterna-tive managers with proven track records are entering the defined contribution market. She says that a vast majority of alternative strategies work very well in liquid vehicles, and 40 Act regulations ensure a high degree of transparency and protec-tions. “Given all the advances in alternatives, I think only giving DC plan participants access to tradi-tional assets is questionable,” says Rappa. She also says that while the definition of “alternatives” can be quite broad, before getting into the weeds of what is, and is not, included in the universe of alts, one has to focus on their function in a portfolio.

“I am a big believer in thinking about the menu in terms of what is a fund designed to be used for,” she says. “Are they supposed to reduce the impact of drawdowns, or provide long-term growth by di-versifying and smoothing my equity returns? Are they supposed to provide uncorrelated sources of income, as opposed to help me manage volatility or protect against inflation?”

Rappa says that in addition to helping with those kinds of targeted objectives, alts share one other big benefit: potentially delivering a “smoother ride.” Alts often have low beta to tra-ditional assets and returns that are independent of market direction. (Exhibit 1) Thus, she says that alts can function as portfolio shock absorbers that help participants stay invested through changing market regimes — no matter where they are in their savings lifecycle. “Smoothing the ride can help participants stay invested and avoid big

mistakes,” she says. “And if alts can improve their outcomes, it’s tough as a fiduciary to justify not having alternatives as an option in a DC plan.”

Alts Can Abate Risk While Enhancing Return“We define alternative investment strategies as those that try to solve or mitigate issues, dilemmas or problems,” says Robert Capone, Head of Defined Contribution and Sub Advisory at AQR Capital Management. “In a defined benefit environment, the burden of risk is on the sponsor. The participant bears no investment risk. No longevity risk. But in a DC plan, a wide range of risks now shift to the participant — from volatility and drawdowns, to inflation, to longevity, to wealth accumulation.”

Capone says that in a defined contribution plan, alternatives can enhance the fiduciary role of the sponsor while abating the risk burden on participants. He says that is a very different way of thinking about asset allocation compared to a traditional approach like splitting your equity allocation among large-, mid- and small-cap Morningstar-style box strategies. “Yes, that’s easy to do, but what is it doing for you?” he says. “My message is much more about understanding the implications and ramifications of your invest-ing approach, in terms of mitigating problems and achieving outcomes.

He says that with better risk management tools, plan sponsors can help participants limit downside risk and drawdowns, which is extremely important to preserving wealth. Overall, the hoped-for benefit is a smoother, more stable return profile, compared to what participants can be subjected to with an overreliance on equities.

But to implement new solutions, sponsors have to get beyond a fear of the unknown. Capone says that while alternatives are different from traditional strategies, they are not so different that they are beyond the due diligence capabili-ties of the average plan sponsor.

“Take risk parity as an example,” says Capone. “It’s a risk-managed portfolio that puts more dollars in less risky assets, and fewer dollars into riskier assets. It’s a Finance 101 concept

Exhibit 1 | Potential Benefits of Liquid Alts

Traditional Mutual Fund Investing

Traditional Hedge Fund Investing

Return Objective

Relative returns

Absolute returns

Benchmark Benchmark constrained

Unconstrained by benchmark index

Investment Strategies

Limited strategies, long-only, no leverage

Flexible strategies (log & short posi-tions, leverage)

Market Beta

High beta to traditional asset classes

Generally low beta to traditional asset classes

Performance Dependent on market direction

Often independent to market direction

Management Fees

Asset-based fee only; no performance fees

Generally higher asset-based fee than mutual funds; performance fees

Liquidity Daily at NAV

Liquidity restric-tions & lock-ups

Investor Base

Publicly available

Qualified purchasers

Transparency High disclosure & transparency

Limited or no position-level transparency

BridgingBenefits

8 Alts in DC

How Can

You Not?Today’s Alternatives

Offer Myriad Ways to Help Participants Improve

Retirement Outcomes

Sour

ce: N

eube

rger

Ber

man

Advertising Supplement

of balancing your risk and smoothing out your return profile, which is a foundational need within retirement investing. Better controlling the risk within your portfolio can help you weather storms in a more stable way across a wide variety of market conditions.”

According to Donna Wilson, Director of U.S. Portfolio Management for Invesco Quantitative Strategies, current defined contribution plan menus and allocations — with their heavy reliance on equities — force participants to bear too much timing risk. They also limit the range of tools par-ticipants can use for risk reduction. She says that alts can smooth the ride for participants thanks to their dual role in retirement portfolios: as risk diversifiers and return enhancers.

“When you have both of those components present, you often have cycles when you get one or the other,” says Wilson. “Typically, what we have seen is that you get the risk diversification when it matters most, when risk is high. And a key long-term benefit of alternatives comes from their ability to potentially generate positive re-turns in down markets. So alternatives can have a multiplier effect of compounding the return benefit you get in those down markets.” (Exhibit 2)

She says that historically, in the defined con-tribution framework, participants could only rely on their bond allocation or stable value allocation to help manage risk. Now they have access to target-date funds as well as professionally man-aged portfolios that may include alternatives, which can help generate returns over and above traditional bond and equity allocations in certain cycles. “That’s how you get that smoother return pattern overall,” says Wilson. “In a good number of cases, these benefits come when you need them most, which is when equity risk is high and equity market returns are low.”

Wilson says that investors need to get out of the mindset that alternatives are high-risk, high-return strategies. “You can’t come in expecting double-digit returns,” she says, “and you shouldn’t see them as materially higher in risk. In most cases, they fall somewhere between equities and bonds. So it’s important to spend time getting to know alternatives across a wide risk spectrum, understanding how that risk is generated and un-derstanding the dual function of alts in a portfolio.”

Diversification, Correlation, Income and Return“Having asset classes with low correlations to one another in your portfolio is a good thing,” says Todd Cassler, President of Institutional Distribution at John Hancock Investments. “But just focusing on correlation and diversification does not answer the ultimate question that the client wants us to help solve, which is, how do I achieve a better retirement outcome?” Cassler says that alternatives can help mitigate a range of critical issues: lowering a portfolio’s correlation to the stock market, improv-ing performance potential in a rising rate regime, reducing manager concentration risk, or weather-ing some macro element or global political shock.

He points to retirement income as an objec-tive that is subject to many of these risks. “One of the big challenges for participants is meeting their income needs in retirement,” says Cassler. “As participants move into retirement, multi-as-set income products may better help participants achieve their retirement goals. Investors may not get enough income from traditional fixed income in the current interest rate environment.” He says that alternatives can play a fantastic role in those multi-asset income portfolios by delivering non-correlated return streams.

“The other benefit alternatives can offer is protection against major market drawdowns,” says Cassler. “In 2008, participants who were close to retirement suffered massive drawdowns in their portfolios. Liquid alternatives and non-traditional investments can help protect against such market stresses or events.”

Cassler believes that over the long haul, participants will be very well-served if they are offered portfolios that include both traditional and alternative asset classes. “We think DC plan participants are underallocated to alternative strategies and we want to help educate plan sponsors on the topic,” he says. “We think it’s even more important today, given the performance of the equity and fixed income markets over the last three years. Liquid alternatives will be a welcome solution for many plan sponsors and participants in the coming years.”

Nadia Papagiannis, Director of Alternative Investment Strategy for Global Third Party Distribution at Goldman Sachs Asset Manage-ment, says that diversification is generally lacking in defined contribution plans — even though diversification is one of the most important tenets of investing.

“Alternatives can be an important part of achieving that diversification,” she says. “Unfor-tunately, when you look at target-date options,

there appears to be a significant underutilization of alternatives. More recently, we have observed some DC plans incorporating what we would consider satellite asset classes — REITs, com-modities, high-yield bonds, anything that is not core equity and fixed income. While we believe those asset classes can be an important source of diversification, that’s not what we are talking about when we refer to alternatives.”

She says that additional diversification may be achieved by including a range of hedge fund-like investment strategies, such as equity long-short, event driven, relative value, tactical trading and multi-strategy. Defined contribution plan percent-age allocations to non-traditional asset classes are in the low single digits, according to Papagiannis, and allocations to liquid alternatives and hedge fund-like strategies are even lower.

“That’s extremely low compared to defined benefit plan allocations,” she says. “DC plans are headed in the right direction, but there’s still a fair distance to go before they are likely to realize the benefits of alternatives.” As an example, she says that a hypothetical portfolio with an 8% expected return and 16% expected standard deviation would be expected to deliver annualized returns ranging from negative 8% to positive 24% two-thirds of the time. Similarly, a portfolio with an expected return of 8% and expected standard deviation of 8% means that two-thirds of the time, returns will be between 0% and 16%.

“The key to building wealth over the long term is avoiding — and not compounding — negative returns,” says Papagiannis. “Alternatives can help portfolios achieve similar expected returns to portfolios with traditional asset classes only, but with significantly lower volatility, helping to mitigate losses. Diversification is absolutely key, and alternatives can provide that. But only with materially higher allocations than DC plans cur-rently allow.”

Equities Fixed Income Traditional 60/40 Portfolio Alternative Portfolio40

30

20

10

0

-10

-20

-30

-40Tech Bubble1/97–12/99

Com

poun

d An

nual

Ret

urn(

%)

Bursting ofTech Bubble1/00–12/02

Debt Run Up1/03–12/07

FinancialCrisis

1/08–12/08

Post CrisisBull Market1/09–6/14

Total Period1/97–6/14

Exhibit 2 | Major Market Indices During Significant Events (Jan. 1997 to June 2014)

Alternatives are represented by a portfolio comprising equal allocations to alternative assets: real assets (FTSE NAREIT All Equity REIT Index, Dow Jones UBS Commodity Index and Alerian MLP Index); relative value strategies (BarclayHedge Equity Market Neutral Index); global investing and trading strat-egies (BarclayHedge Global Macro Index, BarclayHedge Multi Strategy Index and BarclayHedge Currency Traders Index); alternative equity strategies (BarclayHedge Long/Short Index); and alternative fixed income strategies (Credit Suisse Leveraged Loan Index, HFN Fixed Income Arbitrage Index and BarclayHedge Fixed Income Arbitrage Index). The performance of individual alternative investments will differ from that of the index. Equities represented by the S&P 500 Index. Fixed Income represented by the Barclays U.S. Aggregate Bond Index. Traditional 60/40 Portfolio represented by 60% S&P 500 & 40% Barclays U.S. Aggregate Bond Index. An investment cannot be made directly in an index. Past performance is not a guarantee of future results. For Institutional Investor Use Only – Not for Use with the General Public. Source: Invesco Quantitative Strategies

Alts in DC 9

Advertising Supplement

“With scale, you are seeing fees declin-ing more and more over time,” says Robert Capone, Head of Defined

Contribution and Sub Advisory at AQR Capital Management. “But you also have to consider why you want to use these strategies — what are you trying to solve for? And then what are you going to pay for?”

He counsels plan sponsors that due diligence on fees needs to be done in the broad context of the plan’s objective: What are the underlying long-term investment goals of the plan? How do those goals align with the investment goals of the alternative investment strategy that’s being con-sidered? What’s the economic value of the invest-ment, given the added costs and complexities?

“It may be appropriate to pay a higher fee for the alternative investment services that investors are getting,” says Capone. “Alternative investments are trying to garner returns in a less volatile way by being uncorrelated to traditional assets. So, yes, in that regard, alternative invest-ment strategies are goal-oriented and designed to deliver something different, yet specific for the plan.”

Michelle Rappa, Managing Director and Head of Defined Contribution Marketing at Neuberger Berman, knows that fees are extremely impor-tant to plan sponsors. “This market is very sensi-tive to fees, and fiduciaries want to make sure they’re doing the right thing by their participants,” says Rappa. “However, just because a solution is a low-cost alternative doesn’t mean it’s necessarily a better option for the participant.”

Today, liquid alternatives offered through mutual funds give participants relatively low-cost access to hedge fund strategies that have only been available to institutional and high-net-worth investors. “Liquid alts strategies are not the lowest-cost strategies,” says Rappa, “but fiduciaries should think about the role of alts in the overall portfolio and review recent U.S. Department of Labor guidance as they consider plan investments. When evaluating a strategy that is more complex and more ex-pensive, what matters most is having the right process in place to understand the product and the potential value it provides. It’s important to affirm that the strategy makes sense from

an investment perspective, and then look at comparative fees.”

New Structures Drive Fees DownGreg Jenkins, Senior Director of Consultant Rela-tions, and Board Chair of Invesco’s DC Institute, knows that sponsors have spent a great deal of effort trying to get expenses as low as they can, and it can be difficult to add strategies with higher fees, even in smaller allocations.

“The good news is that for many liquid alternative strategies, the fees are coming down as assets grow,” says Jenkins. “We have definitely seen that with risk parity and real assets. I think we’ll continue to see that pattern with other types of strategies.” According to Jenkins, the costs may be lower than investors imagine, and the marketplace is evolving quickly. He says that the other good news is that some managers are now offering lower-cost collective fund versions of many liquid alternatives strategies, with institutional pricing.

“I would encourage plan sponsors not to get too sticker shocked by what they’ve seen in the retail marketplace,” says Jenkins. “Work with managers that have collective fund or institu-tional versions of these strategies that are priced more appropriately for DC plans. They should also seek help from a consultant if they don’t have the staff internally to do their own analysis.”

“Reducing fees removes one of the main hurdles to diversify-ing participant portfolios,” says Nadia Papagiannis, Director of Alternative Investment Strategy for Global Third Party Distribution at Goldman Sachs Asset Management. But she says that fund design is part of the equation, too.

According to Papagiannis, “completion” funds, which mix betas or long-only exposures with hedge fund-like strategies, can be a low-cost solution that adds alterna-tives to a portfolio at roughly half the cost of individual liquid hedge fund strategies.

She says that this approach can also reduce

“line item risk,” where participants may see large performance fluctuations for individual funds on their statements — which can lead them to chase over-priced assets during a run-up, or dump as-sets in a cyclical downturn. Completion portfolios often combine real estate, commodities and other inflation-sensitive assets with emerging equities, emerging credit and high-yield credit, and various types of liquid hedge fund strategies. “If you can capture the benefits of alternatives, and round out participant portfolios that may be invested only in core equities and bonds, diversification can help improve risk-adjusted returns,” she says.

Managers Face Fee Pressures TooTodd Cassler, President of Institutional Distribu-tion at John Hancock Investments, says bench-marking fees should be part of the due diligence process just like it would be when choosing a traditional strategy.

“Relative to traditional strategies, fees for liquid alts are still high,” says Cassler. And as a manager of managers, he understands the fee

10 Alts in DC

Measuring Value In A Fee-Sensitive World

Though fees are coming down for alternative strategies, plan sponsors still wrestle with the issue of cost vs. benefits

continues on page 14

Advertising Supplement

15pi0089.pdf RunDate: 03/09/15 8 x 10.875 Color: 4/C

Invesco has served DC plan sponsors for nearly 35 years. We are dedicated to helping you build better plans and fulfill your duty as a fiduciary. With expertise in alternative investments, we offer strategies to meet your growing needs.

Bank loans

Commodities Global macro

Long/short Market neutral

Real estate

Risk parity

Customize Your Target Date Portfolios With Alternatives

Your plan has unique needs. Shouldn’t your target date portfolios be tailored to meet them?

Customizing with alternative strategies gives your plan participants exposure to an asset class that may help them diversify their portfolios, reduce volatility, generate returns and uncover new sources of income. And partnering with Invesco as your alternatives provider gives you access to institutional-quality alternatives management in DC-suitable vehicles.

Explore Invesco’s alternatives capabilities, and learn more about the role alternatives can play in your plan participants’ portfolios. invesco.com/customize

Invesco Advisers, Inc. is an investment adviser; it provides investment advisory services to individual and institutional clients and does not sell securities. Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail mutual funds, exchange-traded funds and institutional money market funds. Both are wholly owned, indirect subsidiaries of Invesco Ltd.

Alternative products typically hold more nontraditional investments and use more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks. Like all investments, performance will fluctuate. You can lose money.

“We are still in the first inning when it comes to alternatives and defined contribution,” says Nadia

Papagiannis, Director of Alternative Investment Strategy for Global Third Party Distribution at Goldman Sachs Asset Management. “But if you are looking at suitability for a DC plan, from an investment perspective, we think alternatives may be appropriate for many investors.”

She says that a great many plan spon-sors understand the investment rationale for alternatives. Yet, implementation is slowed by common misperceptions about risk and the due diligence burden of liquid alternatives. Papagiannis says, “Sometimes unfamiliar-ity can be confused with riskiness. But liquid alternatives are generally lower in volatility than equities, and they follow the same rules as traditional 1940 Act mutual funds: rules on liquidity, leverage, disclosure, auditing, reporting and independent custody. Those are the exact same requirements as any other mutual fund. So whatever operational due diligence a sponsor may perform for traditional long-only funds, it’s likely similar to what you may want to do for liquid alternatives.”

She also says that it is now clear that “you can’t just look at your record-keeper’s target-date option and call it a day. So while most off-the-shelf target-date funds have little to no alternatives allocations, you should still consider all the options, including funds with

meaningful alternatives exposure.”Robert Capone, Head of Defined Contribution

and Sub Advisory at AQR Capital Management, says that considering where most defined contri-bution fund flows are going today, implementing alternatives within target-date funds makes the most sense. “It’s a lot easier from a participant education and communications standpoint to add alts as part of an asset allocation product, vs. try-ing to add it as a stand-alone menu option,” says Capone. “As a stand-alone option, you run the risk that uninformed participants may chase strate-gies they don’t fully understand — potentially making allocations without having a conceptual idea of what the purpose of the strategy is.”

Todd Cassler, President of Institutional Distribution at John Hancock Investments, believes that simple, easy-to-understand alts (e.g., absolute return) may have a place as stand-alone options. “But in general, there are risks to putting individual strategies on a DC plan menu, particularly if the plan doesn’t have an adviser or a model portfolio guiding participants’ asset allocation,” he says.

According to Cassler, the most popular choices for plan sponsors are packaged solutions that offer a combination of alternatives that com-plement each other, or hiring a target-date fund series that includes alternatives in their lineup. He says that currently, the favored solution is a pack-aged “single-ticker” fund. “A professional manager allocates across a range of individual alternative

strategies and delivers it in a single-ticker mutual fund, in a range of share classes,” says Cassler. “It gives participants access to new and diversifying asset classes while simplifying the due diligence and education requirements for sponsors.”

Alts Allocations Should Not Be Static Donna Wilson, Director of Portfolio Management for Invesco Quantitative Strategies, says that she is an advocate of using alts as a component of a larger strategy rather than as a stand-alone option. And with regard to selecting the right combination of alts, she says: “A lot of it has do with what the plan already has — looking at what they are currently providing participants and what exposures they could potentially be lacking.” For that reason, she keeps the definition of “alts” quite broad in order to be inclusive of a wide range of risk-return characteristics.

“When adding alts to a portfolio, it’s impor-tant to look at what is happening in aggregate and the intended outcome,” says Wilson. “We look at each component of the portfolio, what is its job, and what does the sponsor expect it to do. For example, we’ve seen sponsors take a portion of the equity bucket and allocate it to a risk parity strategy to take some of that equity volatility off the table. Towards the end of a glidepath, when you’re relying more on income-based invest-ments, private real estate, for example, can replace some of your fixed income allocation and may reduce interest rate risk.”

David Kupperman, Ph.D., co-head of Neuberg-er Berman Alternative Investment Management, emphasizes that one of the benefits of using a professionally packaged alts vehicle is that it can be actively managed. Unlike traditional asset classes, with liquid alts there is wide variation in performance between the top- and bottom-decile managers across strategies. Managers employing similar strategies can end up with very different portfolios and risk profiles. Implement-ing through a professionally managed fund — which invests in multiple strategies and selects differentiated managers to capitalize on current market conditions — may help avoid investing with ineffective managers.

“Additionally, in a multi-manager target-risk or target-date-type structure, you have flexibility to tailor to your participants,” says Kupperman. “For example, the further out you are on the

12 Alts in DC

continues on page 14

How Do You Get It Onto The Menu?

For Most DC Plans, Managers Recommend Buying Rather Than Building an Alts Allocation

Advertising Supplement

15pi0086.pdf RunDate: 03/09/15 8 x 10.875 Color: 4/C

R0192_HancockBrandPrint_Retirement_8x10_875_MG.indd

Client: John HancockAd ID #: NoneDescription: HANC_FUNDPublication: NoneScale: 1:1Print Scale: None

Live: 7” x 10”Frame: N/ATrim: 8” x 10.875”Bleed: 8.25” x 11.125”Gutter in Spread: N/A

Art Director: Kar-Kate LeungStudioDesigner: HullUsername: Kelsea AshworthProjectManager: MalenfantProduction: MajeauFile Status: LayoutArt Status: InProgress/Not ApprovedResolution: 300 dpi

Job Colors: N/A

Ink Name: Cyan Magenta Yellow Black

Font Family:Frutiger LT Std

R0192 1-23-2015 12:58 PM Page 1

JHI logo 295_4C.eps (images RO:Hh:Hancock Corporate:DAM:Brand Assets:1_Logos:JH Investments:EPS:JHI logo 295_4C.eps), Vector Smart Object 3.ai (images RO:Hh:Hancock Corporate:DAM:Brand Assets:2_Icons and Graphics:Vector Smart Object 3.ai), Vector Smart Object 2.ai (images RO:Hh:Hancock Corporate:DAM:Brand Assets:2_Icons and Graphics:Vector Smart Object 2.ai), Vector Smart Object 1.ai (images RO:Hh:Hancock Corporate:DAM:Brand Assets:2_Icons and Graphics:Vector Smart Object 1.ai)

SPECIAL INSTRUCTIONS:Pensions & Investments Supplement – Release Date: 1/23/15

The supplement will be featured in the February 23, 2015 issue of P&I

5 years3 years1 year0

50

100

Top 33% of peers

Top 9% of peers

Top 21% of peers

Pie chart for illustrative purposes only.

John Hancock Retirement Living through 2030 Portfolio’s Morningstar percentile ranking among target-date 2026-2030 funds. As of 12/31/14, rankings were 75 out of 228 funds over 1 year, 18 out of 193 funds over 3 years, and 35 out of 164 funds over 5 years. Rankings are based on total return, apply to Class R6 shares, and do not account for sales charges. Please note that Class R6 shares may not be available to all investors and that performance of other share classes will vary. Past performance does not guarantee future results.

The portfolio’s performance depends on the advisor’s skill in determining asset class allocations, the mix of underlying funds, and the performance of those underlying funds. The portfolio is subject to the same risks as the underlying funds and exchange-traded funds in which it invests: Stocks and bonds can decline due to adverse issuer, market, regulatory, or economic developments; foreign investing, especially in emerging markets, has additional risks, such as currency and market volatility and political and social instability; the securities of small companies are subject to higher volatility than those of larger, more established companies; and high-yield bonds are subject to additional risks, such as increased risk of default. Certain market conditions, including reduced trading volume, heightened volatility, and rising interest rates, may impair liquidity, the ability of the fund to sell securities, or close derivative positions at advantageous prices. Each portfolio’s name refers to the approximate retirement year of the investors for whom the portfolio’s asset allocation strategy is designed. The portfolios with dates farther off initially allocate more aggressively to stock funds. As a portfolio approaches and passes its target date, the allocation will gradually migrate to more conservative, xed-income funds. The principal value of each portfolio is not guaranteed, and you could lose money at any time, including at, or after, the target date. Hedging and other strategic transactions may increase volatility and result in losses if not successful. Please see the portfolio’s prospectus for additional risks.A fund’s investment objectives, risks, charges, and expenses should be considered carefully before investing. The prospectus contains this and other important information about the fund. To obtain a prospectus, contact your �nancial professional, call John Hancock Investments at 800-225-5291, or visit us at jhinvestments.com. Please read the prospectus carefully before you invest.NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE. NOT INSURED BY ANY GOVERNMENT AGENCY.John Hancock Funds, LLC, Member FINRA, SIPC. © 2015 John Hancock. All rights reserved.

20 SPECIALIZED INVESTMENT TEAMS INSIDE EVERY RETIREMENT PORTFOLIO.

WE THINK IT’S A BETTER WAY TO INVEST.

JOHN HANCOCK RETIREMENT LIVING PORTFOLIOS

Ten portfolios with target retirement dates spanning from 2010 to 2055, actively allocated across traditional and alternative asset classes by the team at John Hancock Asset Management—now with lower expenses.

Diversi�cation by security, asset class, strategy and manager

Including those managed by: John Hancock Retirement Living through 2030 Portfolio

• Baillie Gifford • Dimensional Fund Advisors • Epoch Investment Partners • First Quadrant • GMO• Jennison Associates • John Hancock Asset Management • Robeco Investment Management • Stone Harbor Investment Partners • Wellington Management • Wells Capital Management • Western Asset Management Company

A record of strong performance

Discover our different approach to investing.

73 proven portfolio teams at 28 elite rms worldwide.

Over 250 investment strategies

vetted annually.

165+ experts in manager research

and oversight.

retirement glidepath, the more flexibility you have to do much more illiquid investing.” He also reminds sponsors that the return objective for alts is just as important as the risk manage-ment objective. He says that when an inves-tor can withstand market risk (e.g., early in a target-date glidepath), he does not recommend weighing down return-seeking portfolios with low-volatility, low-return alts strategies. “If you are investing for a 20-year-old who has many, many years before retirement, putting them in low volatility alts is completely the opposite of what they should be doing,” says Kupperman. “A more appropriate approach would be to replace some of the portfolio’s equity allocation with a long-short equity strategy, which is higher volatil-ity but also slightly higher in return potential than the average hedge fund strategy.”

And he cautions that as participants age, they need more effective shock absorbers in the port-folio. “At that point, you need investment options that are biased toward low-volatility strategies, replacements for equities like risk parity and multi-strategy income-seeking strategies.”

According to Nathan W. Thooft, CFA, Portfo-lio Manager for John Hancock Asset Manage-ment, “Different alternatives pull different risk and return levers to varying degrees, and we believe there is value in having a professional buyer controlling the weights to those underlying strategies.”

Thooft says that during the equity bull market that followed the financial crisis, he passed on a lot of trend-following strategies (e.g., managed futures) because he felt there would be too many inflection points in the run-up that could whipsaw those types of strategies (e.g., the summer correction of 2011 or the taper event of 2013). Another example he offers is merger arbitrage, in which early on during the market recovery, M&A activity and spreads between acquirer and acquiree were low. However in recent years that has changed.

Professional Allocators Add Value “You have to remember that this industry is very slow to change,” says AQR’s Robert Capone. “Target-date funds themselves were around for years before they began to see strong adoption. Today, we are seeing the more progressive spon-sors not as satisfied with the off-the-shelf offer-ings, including closed-architecture target-date funds. Even though off-the-shelf target-dates are beginning to include some of the more familiar single-asset alternatives, like commodities and

real estate, they still are primarily wedded to traditional style box investing.”

By comparison, he says that open-archi-tecture, multi-manager target-date funds offer sleeves of true alternative investment strategies (e.g., style premia, risk-balanced commodities, risk parity, market neutral and equity long/short). “Alternative investment solutions are purpose built,” says Capone. “For reducing home bias and equity risk concentration, that’s a risk parity type solution. Hedging against inflation might require a multi-strategy real-asset solution. That’s how I believe these alternative strategies need to be thought about and implemented, to help partici-pants reach their accumulation and preservation objectives in an easier, smoother way.”

Nathan Thooft of John Hancock says, “We believe a better approach is creating an alts bas-ket or multi-strategy fund that has a risk-return profile somewhere between traditional fixed in-come and equities. So you can choose whether to source more from your equities or fixed income. Or if alts are built directly into a target-date suite, that active decision is left up to the portfolio management team.” He says that under different market conditions, the source of the alts alloca-tion can have a big impact on performance. Over the past 10 years, splitting the allocation source between equities and fixed income would likely have delivered slightly higher risk-adjusted return compared to taking the full allocation from either equities or fixed income alone. (Exhibit 1)

Gary Chropuvka, Head of the Customized

Beta Strategies business within Goldman Sachs Asset Management’s Quantitative Investment Strategies team, says that his firm provides alternatives strategies directly to managers of open-architecture target-date funds.

“We believe that is the most appropriate out-let for alternatives in a DC plan,” says Chropuvka. “Primarily, alternatives have been sourced out of equities, which is where we think it should come from over the long term. It is very difficult to battle back from a severe drawdown, and though we don’t know what the environment will be going forward, equities are statistically overdue for a large correction. And later in a glidepath, even when equities are reduced to 50% or 60% of the portfolio, that still represents more than 90% of portfolio risk.”

Greg Jenkins, Senior Director of Consul-tant Relations and Board Chair of Invesco’s DC Institute, believes that while alts implementation can feel daunting, the simplest place to start is by looking at the goals. “Rather than focusing on the specifics of how an alternatives strategy is put together, start with an outcome orientation,” he says. “Focusing too early on implementation can overshadow the ultimate goal of improving participant outcomes. I think things become clearer once you have an understanding of the role each component plays within the portfolio and why it’s being included. Often we see a phased implementation and there are plenty of partners — including consultants, custodians and record-keepers — to help with the mechanics.”

Exhibit 1 | Funding Source for Alts Allocation Can Significantly Impact Risk/Return

10-Years Ending 12/31/14

40 MSCI World /40 BCAG / 20Alts

48 MSCI World /32 BCAG / 20Alts

60 MSCI World /20 BCAG / 20Alts

60 MSCI World /40 BCAG

10-Year Annualized Standard Deviation %

10-Y

ear A

nnua

lized

Ret

urn

%7.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

7.50 8.00 8.50 9.00 9.50 10.00 10.50 11.00 11.50

14 Alts in DC

pressures that plan sponsors are under. “For our multi-manager, multi-strategy funds, we are reluctant to hire performance-fee managers,” says Cassler. “We negotiate very heavily to get break points with asset growth. We look at whether fees are competitive vs. the category

average and peers.”Cassler says that there are many alternative

strategies on the market that are probably too expensive for what investors get in return for their investment. But at the same time, he says that if investors do their due diligence well, they

can find good managers and products that are fairly priced relative to what they offer from an investment perspective. Above all, he says, “Many of these strategies are unique, and investors need to ask, What kind of performance blueprint am I getting for my cost of investment?”

Measuring Value In A Fee-Sensitive World , continued from page 10

Alternatives are respresented by an equal weighting of the HFRI Macro Index, the HFRI Merger Arbitrage Index, the HFRI Equity Market Neutral Index, the Morningstar Emerging Market Bond Category Average, the Morningstar Real Estate Category Average and the DJ UBS Commodity Index minus 85 bps annually to simulate a management fee. It is not possible to invest directly in an index. Past performance does not guarantee future results. Source: John Hancock Asset Management: Morningstar Direct: as of 12/31/13.

Advertising Supplement

15pi0087Resized.pdf RunDate: 03/09/15 8 x 10.875 Color: 4/C

Four Practical Considerations...When you’re considering liquid alts as options in your DC plan

2

4

1

3

Manager Selection Not all managers are created equal

Risk Management Portfolio oversight and systems

Operational Expertise Familiar does not mean ‘safe’ ... know what you’re investing in and why

Real Experience Market cycles are a great instructor

A Practical Alternative from Neuberger Berman

15pi0102.pdf RunDate: 03/09/15 8 x 10.875 Color: 4/C

For many years, DB pension plan managers have recognized that alternative investments can be sources of growth potential and can also help mitigate volatility and the impact of inflation. So now, as many DC plans begin to “DB-ify”, they are also willing to consider alternatives as a way to give portfolio diversification outside of the traditional stocks, bonds, cash or real estate.

REGISTER to hear top industry experts discuss this growing trend of incorpo-rating alternatives into DC plans and its potential for improving retirement outcomes. Our agenda includes the following timely sessions:

PANEL DISCUSSIONS• Assessing the Net-Return Performance Improvement of Alternatives over

Listed Assets

• How to Structure Your Plan Menu to Include Alternatives

• Developing a Roll-Out Plan for Incorporating Alternative Assets

WORKSHOPS• A New Word Order: The Language of Alternatives

• All Alternative Funds are Not Equal

• Meaningful Diversification Through Risk Parity

• Do Liquid Alternatives Work?

• Measurement and Oversight of Alternative Strategies

“Alternatives are very important and will grow in DC allocation - good conference!”

“Excellent conference, very topical.”

WHY ATTEND?Here’s what your peers had to say about last year’s event:

May 19 | New York

All registration requests are subject to verification. P&I reserves the right to refuse any registrations not meeting our qualifications. The agenda for the Alternatives in DC Conference is not created, written or produced by the editors of Pensions & Investments, and does not represent the views or opinions of the publication or its parent company, Crain Communications, Inc.

*Registration is only open to pension plan sponsors and a limited number of investment consultants.

Questions? For more details please contact Elayne Glick at (212) 210-0247 or [email protected]

sponsored by:

REGISTER NOW

Complimentary registration* at www.pionline.com/ALTS2015

“Overall it was a great experience. Thank you!”