what's coming, and are you ready for it?

TRANSCRIPT

Are you prepared for the deep socio-demographic, technological, economic, and political trends in the next 5-10 years? Charity Comms Brand Conference Keynote Presentation Luba Kassova, Richard Addy 24 October 2013

1

Sofia, Bulgaria in 1997 - where Luba lived

2

1000% Inflation

Bulgaria

1.7% Inflation

UK

Currency collapsed – lives were destroyed

16 years later, who would have predicted…

Bulgaria has the lowest EU inflation 3

Lowest EU Inflation

Bulgaria

Highest EU Inflation

UK

The Bulgarian currency collapse was a “Black Swan” event

1997 Bulgarian currency collapse

2001 Twin towers

attacks

2008 Collapse of

Lehman Brothers

2011 London Riots

4

Black Swans are unpredictable, large impact events - they change people’s lives overnight

5 years?

10 years?

3 years?

now

So, beware of forecasters who claim to be certain about future events

5

Sometimes the best we can do is understand the now… Nowcasting

6

Britain is going through an age of uncertainty which makes forecasting challenging

7

Respected institutions like the IMF, Treasury and OBR have consistently made errors

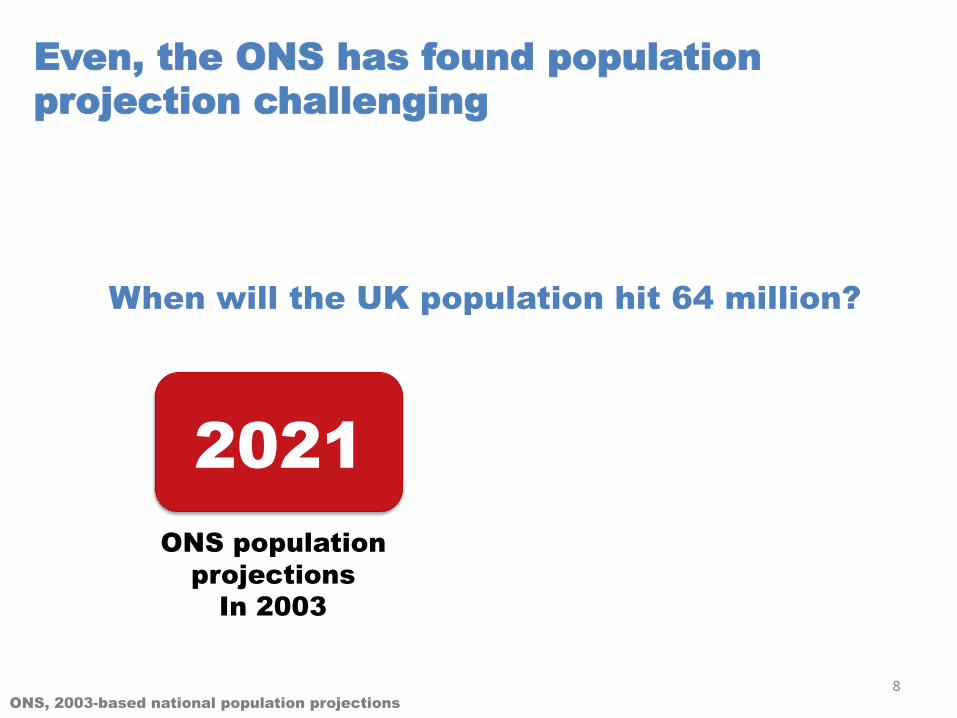

Even, the ONS has found population projection challenging

When will the UK population hit 64 million?

2021

8

ONS population projections

In 2003

ONS, 2003-based national population projections

ONS population projections

In 2003

Actuals

When will the UK population hit 64 million?

2021 2013

9

Even, the ONS has found population projection challenging

ONS, 2003-based & 2010-based national population projections

So you need to continuously, track

trends, forecasts, and predictions against what the latest data says and what you

observe! 10

Some of the sources for this presentation

We have only focused on trends which we believe

are of higher importance to you

12

Part 1: Socio-demographic trends and public attitudes

13

There is good news…

14

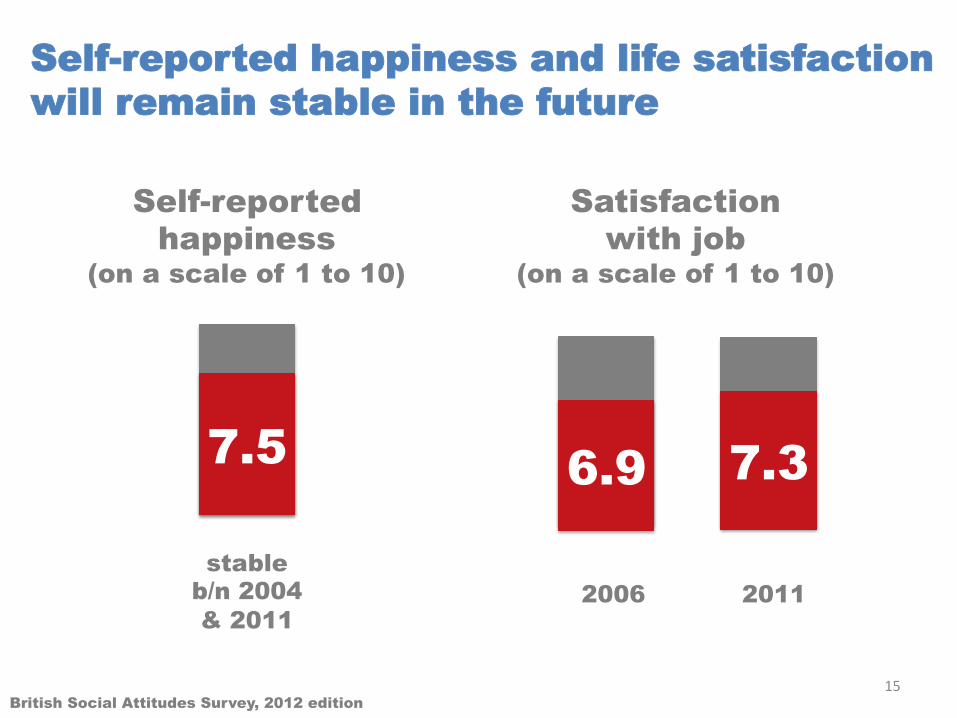

Self-reported happiness and life satisfaction will remain stable in the future

Self-reported happiness

(on a scale of 1 to 10)

Satisfaction with job

(on a scale of 1 to 10)

2006 2011

7.5 6.9

stable b/n 2004 & 2011

7.3

15 British Social Attitudes Survey, 2012 edition

New scientific revelations will revolutionise the thinking about people’s decision-making

16

Emotions will become a consumer/public measurement currency

95% unconscious

5%

17

rational

Decision Making

Gerald Zaltman, How Customers Think (2003)

The public will continue to trust charities

66% 51% 49%

Nov 03 Sep 06 Mar 13

How much trust do you have in charities? (quite a lot/a great deal)

nfpSynergy Charity Awareness Monitor survey, 2003 - 2013; c1000 Adults 16+ 18

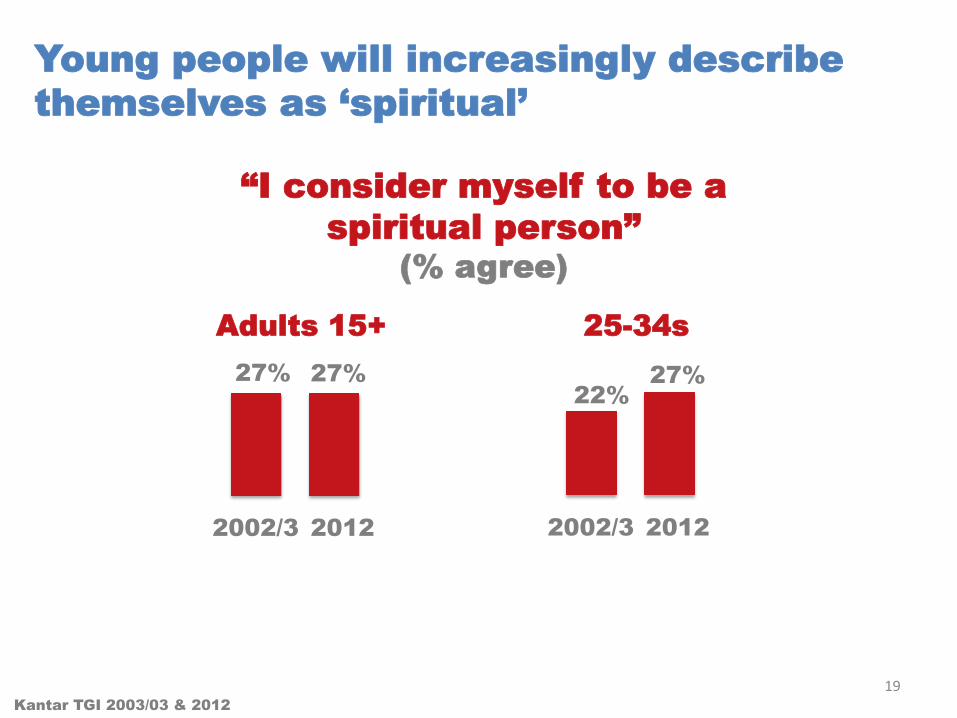

Young people will increasingly describe themselves as ‘spiritual’

“I consider myself to be a spiritual person”

(% agree)

2002/3 2012 2002/3 2012

Adults 15+ 25-34s

27% 27% 27% 22%

Kantar TGI 2003/03 & 2012 19

The NHS will continue to have a special place in public’s heart

2003 1983 1993 2012 Public ranking of health as a priority area for extra gov/t spend

Top Top Top Top

% of the public who chose health as a priority area for extra government spend

79% 70% 71% 63%

20 British Social Attitudes Survey, 2013 edition

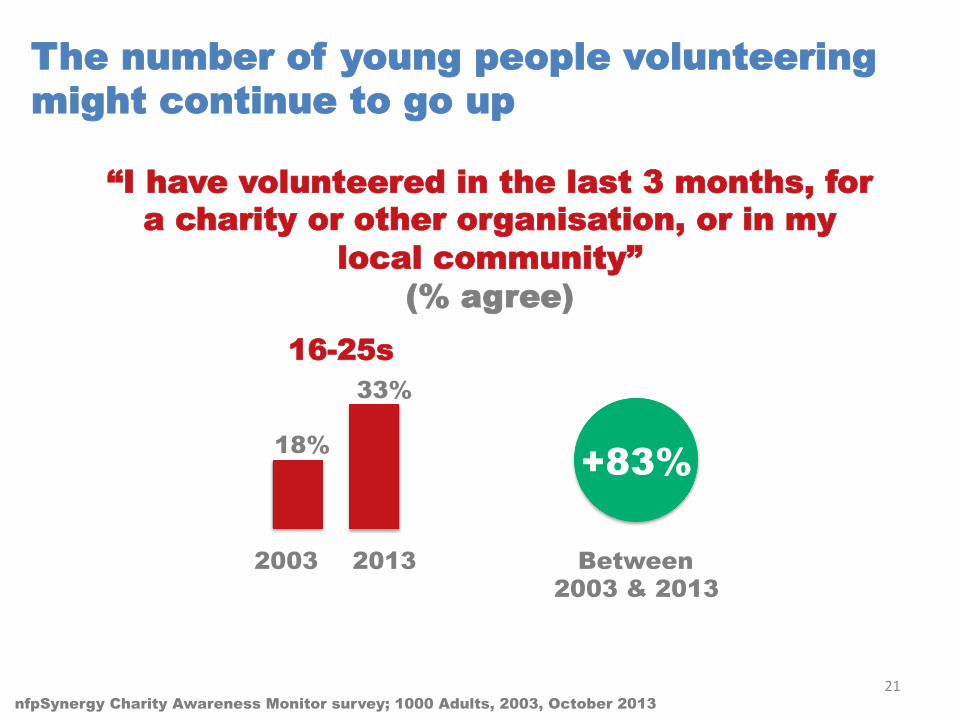

The number of young people volunteering might continue to go up

“I have volunteered in the last 3 months, for a charity or other organisation, or in my

local community” (% agree)

2003 2013

16-25s

18%

33%

nfpSynergy Charity Awareness Monitor survey; 1000 Adults, 2003, October 2013

+83%

Between 2003 & 2013

21

There are challenges…

22

Public views on welfare will harden

1991 2012

“Government should spend more on welfare benefits even if it

leads to higher taxes” (% agree)

58% 34%

23 British Social Attitudes Survey, 2013 edition

More people will believe that one needs to help oneself when the ‘going gets tough’

1991

2012

Government should

redistribute income

Would like to see more government spending on

benefits for disabled people, who cannot work

(% agree)

1996

2011

74%

53%

49%

41%

(% agree)

24 British Social Attitudes survey, 2012 & 2013 editions

Personalisation will be more important to some but not others

58%

44%

29%

26% 9%

4%

18 - 24

More Likely

No Difference

Less Likely

55+

Likelihood that website or email personalisation will lead to extra donations

25 YouGov Survey for Rocket Communication, Nov 2012; 1,441 UK adults online who donated money to charity last year

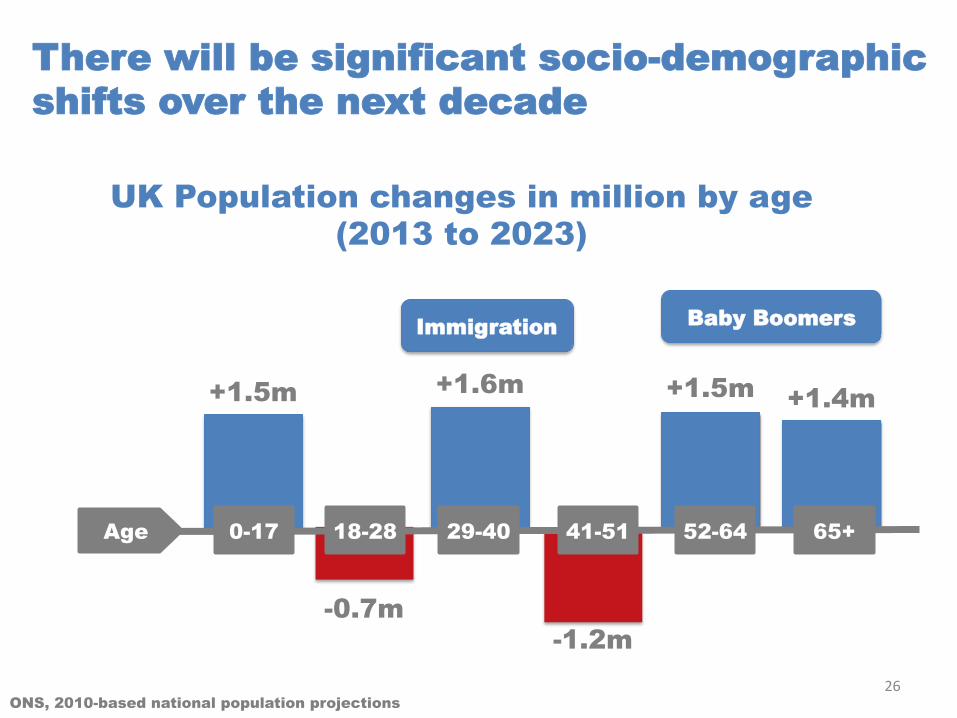

There will be significant socio-demographic shifts over the next decade

+1.5m

-0.7m -1.2m

+1.5m +1.6m +1.4m

UK Population changes in million by age (2013 to 2023)

26

0-17 18-28 Age 29-40 41-51 52-64 65+

Baby Boomers Immigration

ONS, 2010-based national population projections

Volunteering in the UK will remain lower than in other countries, but could improve

UK

Volunteering time in the last month

USA

2012 2007

44% 42%

29% 23%

27 CAF Giving Index 2012, Gallup 2007

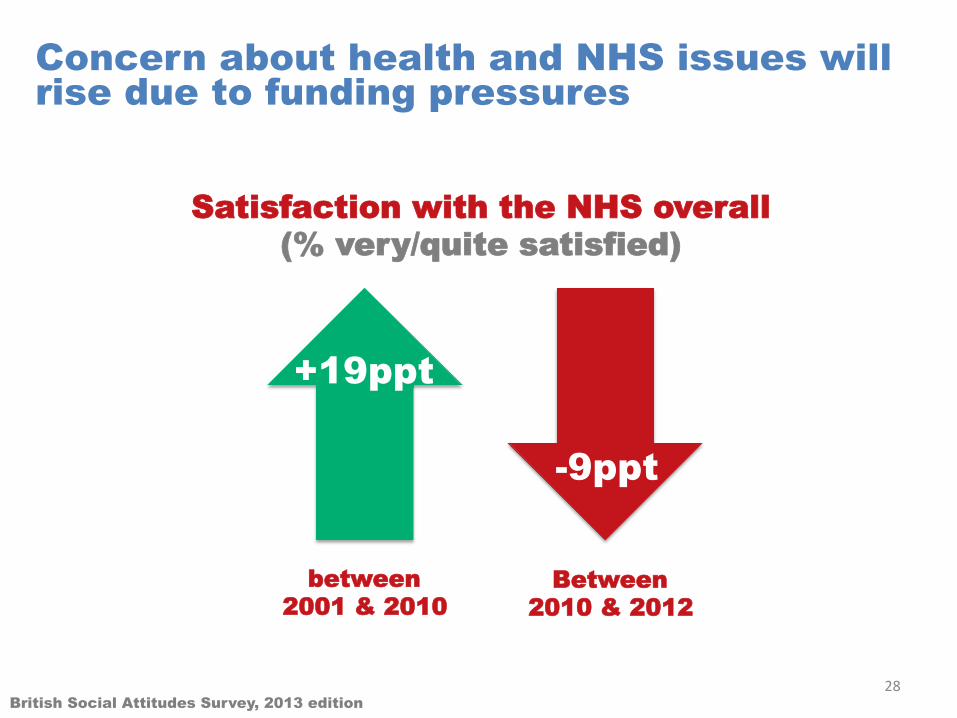

Concern about health and NHS issues will rise due to funding pressures

Satisfaction with the NHS overall (% very/quite satisfied)

between 2001 & 2010

Between 2010 & 2012

+19ppt

-9ppt

28 British Social Attitudes Survey, 2013 edition

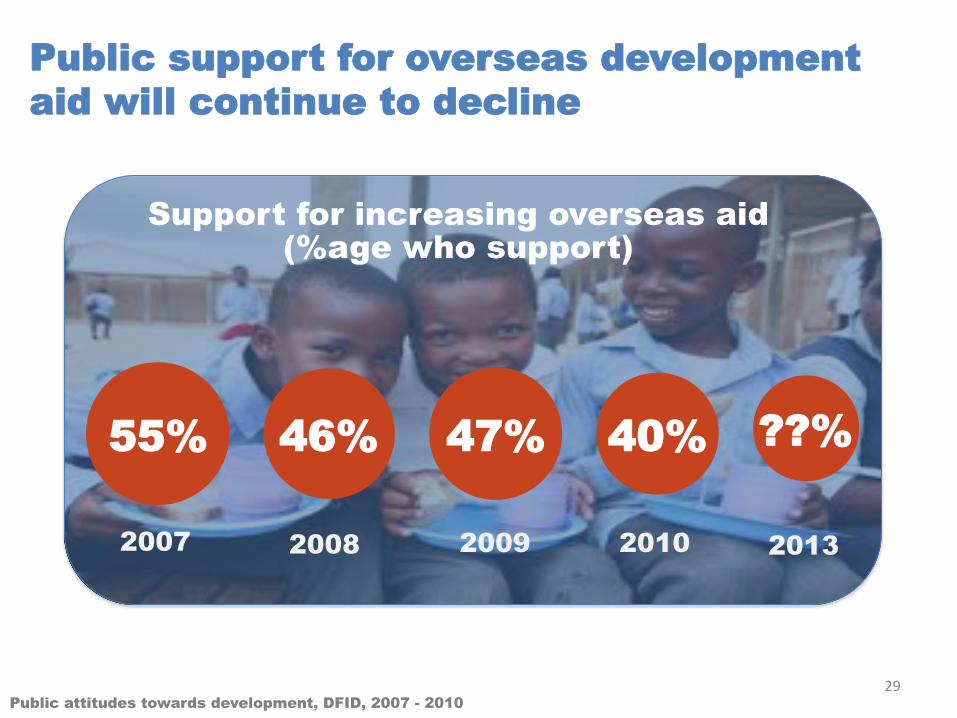

Public support for overseas development aid will continue to decline

Support for increasing overseas aid (%age who support)

55% 47% 46% 40% ??%

2008 2007 2009 2010 2013

29 Public attitudes towards development, DFID, 2007 - 2010

A significant minority might continue to reject charity advertising

Banks

Brand reputation

Advertising rejectors

Charities Utility companies

37% -67% -55%

31% 28% 31%

Brand reputation from Public Opinion and the Evolving state report YouGov, Sep 2013 Advertising rejectors from The Consumer connections survey, Carat, 11000 sample, July 2012/Marketing week

30

You can overcome the challenges…

31

Ensure your brand can show that it ‘cares’. Allow it to tap into people’s spirituality

32

Evolve your brand around understanding which emotions lead to action

Will the public act more if it keeps feeling distraught?

Will the public act more if it feels celebratory about

the outcomes?

33

Use cognitive psychology breakthroughs to target and nudge audiences

34

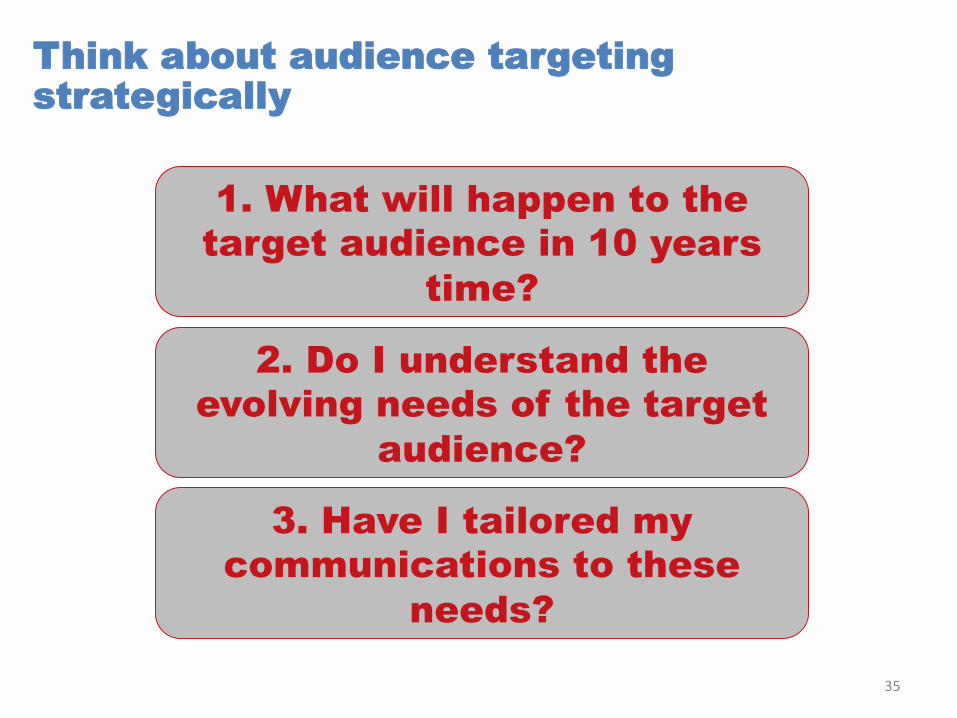

Think about audience targeting strategically

1. What will happen to the target audience in 10 years

time?

2. Do I understand the evolving needs of the target

audience?

3. Have I tailored my communications to these

needs?

35

Develop fundraising and marketing ideas around people’s desire to experience

Charities weathering the storm?, Ben Page, CEO Ipsos-Mori, All Adults, April 2012; 1,004 British Adults

36

Set up a direct

debit

Sponsored Walk/

Cycle/ run

What I have been asked

to do to donate

Would I would prefer to do to make a donation

60%

58% 49%

41%

Gap

-9%

+19%

Develop fundraising and marketing ideas around people’s desire to experience

Can brands make us happier?/The Guardian, based on Mood of the Nation research, Jan 2013 in the UK, nationally representative UK sample of 2,141 people.

Charity creates

experience

Empowered supporter

Happy person

More receptive to charity marketing

37

Ensure you personalise your approach to your target audiences

Big data

9% of people do 66% of the charitable activity

38 Britain’s Civic Core – Who are the people powering Britain’s charities?, CAF, Sep 2013

Part 2: Technological trends

39

There is good news…

40

Technological make up of the home is being enhanced

80%

Internet

51%

smartphone

24%

tablet

56%

Laptop/ netbook

Year on year

100% on

2011

118% yoy

Penetration amongst UK adults

41 Ofcom Communications Market report, Aug 2013

Media multi-tasking will eventually become the norm

Regular media multi-taskers

53% 49% 25%

Regular ‘meshers’

Regular ‘stackers’

Ofcom Communications Market report, Aug 2013

UK Adults

42

Technology has made instant and impulsive giving easier than ever

58% 42%

Traffic from mobile devices

Traffic from traditional desktop

computers

“We can see that mobile is driving unprecedented levels of generosity”

Anna Kuriakose, Head of product, JustGiving

43 Marathon runners hot mobile giving milestone, JustGiving, 22 April 2013

Social media, technology & stories will continue to get people to raise money independently

$67 million

44 http://www.giveforward.com/p/cancer-fundraising

There are challenges…

45

TV, which is an expensive marketing tool, will remain the most consumed medium

104h a month

122h a month

2004 2012

46 Ofcom Communications Market report, Aug 2013

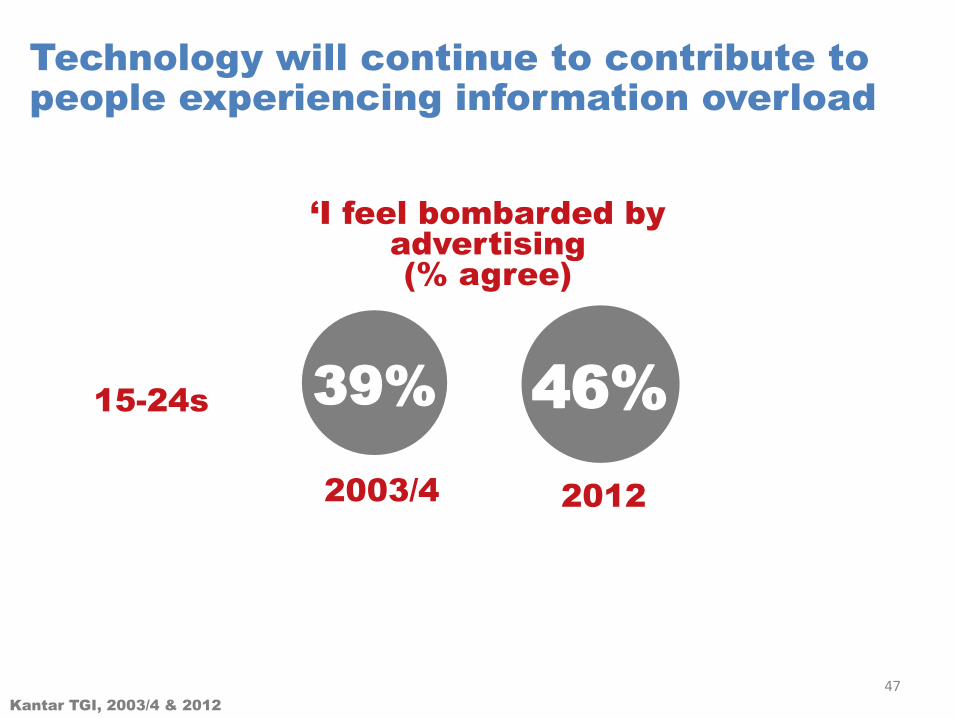

Technology will continue to contribute to people experiencing information overload

15-24s

‘I feel bombarded by advertising (% agree)

2003/4 2012

46% 39%

Kantar TGI, 2003/4 & 2012 47

48

Understanding what is going on!

You can overcome the challenges…

49

Clarity and simplicity are going to be key to brand success

50 Health leaflets at a GP reception in SW London – no message stands out

Ensure your brand has a strong digital pulse

“How brands overcome risk of rejection”, Marketing Week; 26 July 2012 By David Burrows 51

% who visit profile or fan pages of brands

% who interact with a brand online

Ad

Rejectors UK

Adults

11%

21% 16%

19%

Opportunity

+5%

+6%

Innovate for portable internet enabled devices, particularly for Tablets

52

Think in terms of integrated marketing to reflect changing behaviour

53% 74% 81%

“I am a regular media multi-tasker whilst I watch TV”

UK Adults

Smartphone users

Tablet users

53 Ofcom Communications Market report, Aug 2013

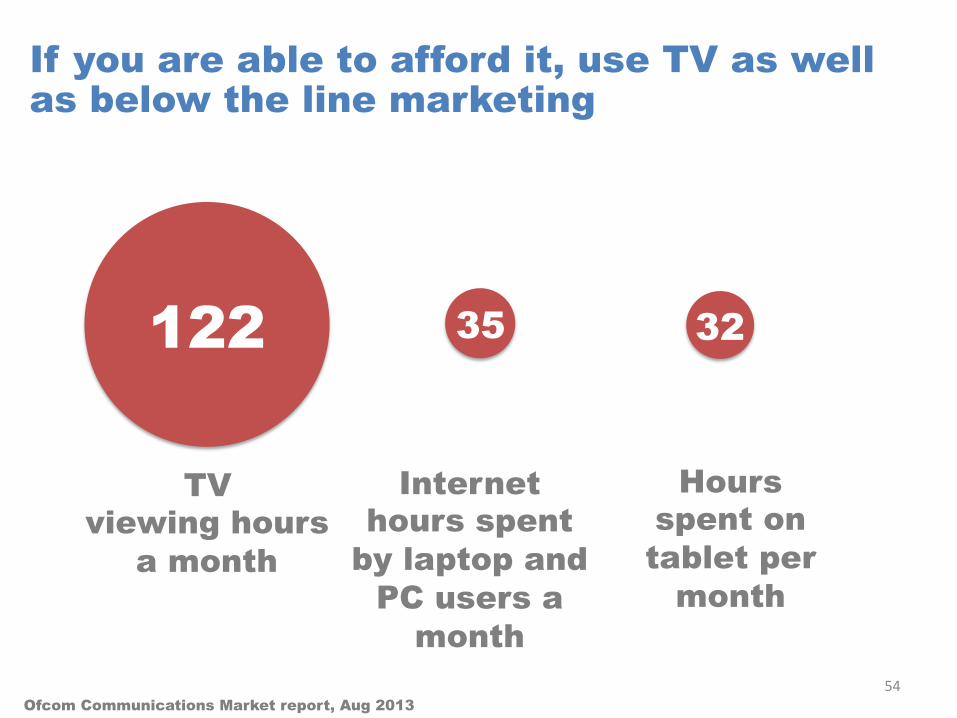

If you are able to afford it, use TV as well as below the line marketing

122

TV viewing hours

a month

35

Internet hours spent

by laptop and PC users a

month

32

Hours spent on tablet per

month

Ofcom Communications Market report, Aug 2013 54

Part 3: Economic trends

55

There is good news…

56

The general mood will continue to be less pessimistic and for some groups more optimistic

57

Unemployment numbers are falling and this is forecast to continue

58

House prices and mortgages are likely to continue their rises in the short term

59

Pensioner incomes look set to continue their recent increases

60

There are challenges…

61

Another housing boom could be followed by an inevitable bust

62

Another housing boom could be followed by an inevitable bust

63

Another housing boom could be followed by an inevitable bust

64

Another housing boom could be followed by an inevitable bust

65

Another housing boom could be followed by an inevitable bust

66

Fewer and fewer young people will live in family owned homes

67

Just under 70%

(1992) Just over

40% (2012)

25-34 Year olds

68

The multiple pressures on young people will remain

British family and disposable incomes are experiences an unprecedented squeeze

69

Inequalities will continue to grow

70

Inequalities will continue to grow

71

72

The economic danger of a sharp rise in interest rates will be a constant worry

Daily Telegraph on the Office of Budget Responsibility report - Economic and Fiscal Outlook, March 2013

£1,286 bn National Debt (2013/14)

£71bn Cost of interest payments payments in 2017/18

73 Office of Budget Responsibility, Economic and Fiscal Outlook, March 2013

£1,637 bn National Debt (2017/18)

The economic danger of a sharp rise in interest rates will be a constant worry

74

The public sector will continue to face austerity.

The public will continue to scrutinise charity funds

% agree “Ensure a reasonable proportion of

donations get to end cause”

43% 42% 32% 30%

2005 2008 2010 2012

Is the top driver of trust and confidence 75

Charities weathering the storm?, Ben Page, CEO Ipsos-Mori, All Adults, April 2012; 1,004 British Adults

76

Public donations will continue to be under pressure

£11bn £9.3bn

2010/11 2011/12

Amount donated to charities by adults

down in cash terms

£1.7bn

Source: UK Giving 2012, NCVO/CAF

down in real terms

£2.3bn

You can overcome the challenges…

77

Acknowledge the public’s sustained top concerns in brand comms to stay relevant

Top 10 Worries in 2012

Money/ Bank balance/

debt

49% 38% 35% 24%

19% 16%

23%

19%

Family/ Friends

Physical Health

Job Security

Appearance/ Ageing

23%

Workplace issues

Ability to cope emotionally

Domestic Politics

World Affairs

14%

Mortgage/ Rent/

Housing 78

YouGov survey for The Samaritans, Nov 2012; 2,162 UK Adults

Pay greater attention to customer service and journeys’ online and face to face

79 YouGov Survey for Sirportly, Feb 2013; 2,099 UK Adults

80

Build on the the last decade’s success in generating earned income

21

14

11

3 2

15

Earned Income

Voluntary income

Investment income

2000/01 (£bn 2011 prices)

2011/12 (£bn, 2011 prices)

+92%

NCVO, UK Civil Society Almanac, http://data.ncvo-vol.org.uk/a/almanac13/almanac/databank/income-2/

Change

+3%

-23%

Innovate and don’t apologise for it

81

Plan actively manage your investments

82

Plan actively manage your investments

83

Don’t forget high net worth individuals

84

85

Engage in companies who want to partner to unlock their potential

Why companies & NGOs engage in relationships win each other (top 3 reasons)

91%

67%

63%

100%

83%

65%

Reputation/Credibility

Innovation

Access to Knowledge

Reputation/Credibility

Access to People/ Contacts

Access to Funds

Companies NGOs

Marketing Week, Two heads are better than one, 12 September 2013 http://www.marketingweek.co.uk/trends/why-two-heads-are-better-than-one/4007792.article

Part 4: Political trends

86

There is good news…

87

The public will continue to have a stronger connection with local politics

I want a great deal or some influence over

26% 16%

Local decision making

National decision making

25% 14% 2009

2013

88 Hansard Society, Audit of Political Engagement, 2013

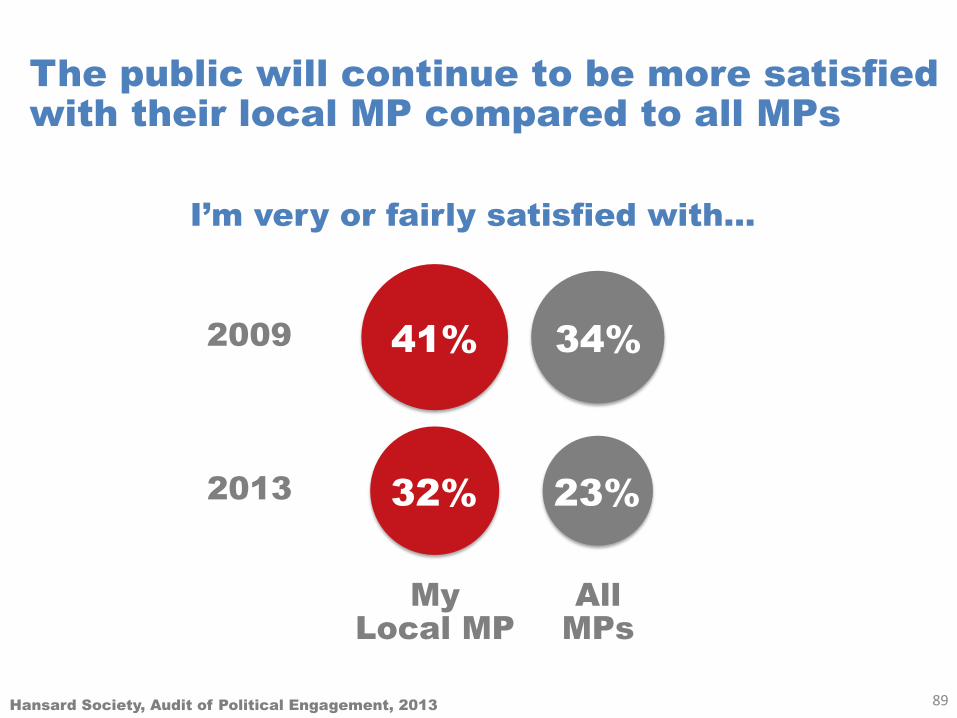

The public will continue to be more satisfied with their local MP compared to all MPs

I’m very or fairly satisfied with…

My Local MP

All MPs

41% 34%

32% 23%

2009

2013

89 Hansard Society, Audit of Political Engagement, 2013

The ethnic difference in interest in politics will continue to be non-existent

White Ethnic Minorities

2004

2013

I am very or fairly interested in politics

52%

45%

27%

41%

25%

4%

Difference

90 Hansard Society, Audit of Political Engagement, 2013

There are challenges…

91

92

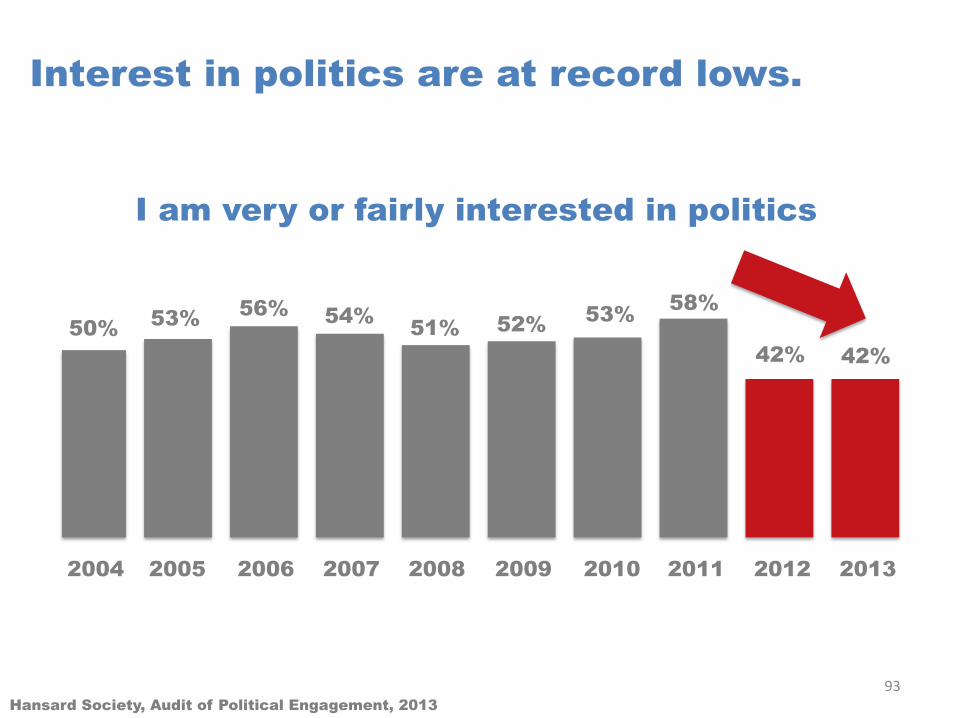

The disenchantment with politics is likely to continue

Interest in politics are at record lows.

50% 53% 56% 54% 51% 52% 53% 58%

42% 42%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

I am very or fairly interested in politics

93 Hansard Society, Audit of Political Engagement, 2013

There is a real danger that less than 50% of the electorate will vote in the 2015 election

65% 69% 69%

64% 66% 69%

57%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

I am absolutely certain or high likely to vote in an immediate general election

2014 2015

52% 50%

??

67%

GE: 65%

66%

GE: 61%

94 Hansard Society, Audit of Political Engagement, 2013

Despite preferences for their local MP, very few can name their local MP

Correctly named their local MP

44% 42% 38% 22% 44%

2004 2007 2010 2011 2013

95 Hansard Society, Audit of Political Engagement, 2013

Politics is fragmenting with smaller parties getting more votes

35% 28% 24% 19% 11%

1970 1979 1992 2001 2010 2020

??

Non Conservative/ Labour votes in General Elections

96 AKAS analysis of General Election results

Charities are not as influential as others

Have a fair amount of influence on government policy, 2013

Charities Trade Unions

Private Companies Consultants

68% 53% 51% 19%

97 YouGov survey for Acevo, 2013; 1,660 Adults, http://www.thirdsector.co.uk/Policy_and_Politics/article/1210189/public-trusts-charities-lobby-good-society-lobbyists-says-acevo/

In fact, the majority thinks charities have no influence on government policy

Influence of charities on government policy, 2013

Fair amount of influence

No influence

63% 19%

98 YouGov survey for Acevo, 2013; 1,660 Adults, http://www.thirdsector.co.uk/Policy_and_Politics/article/1210189/public-trusts-charities-lobby-good-society-lobbyists-says-acevo/

You can overcome the challenges…

99

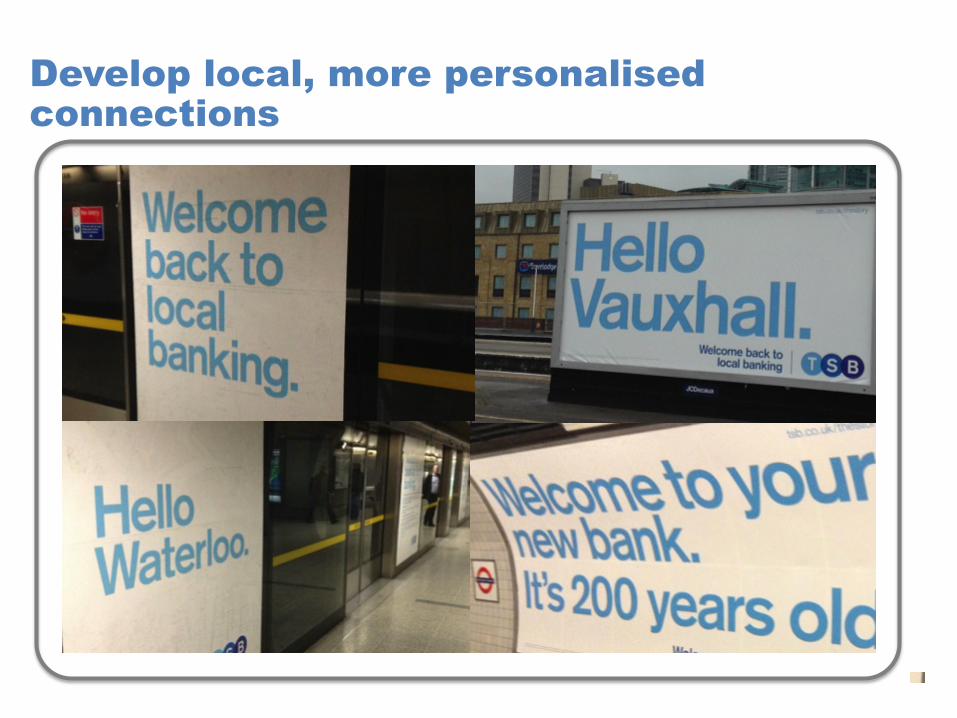

Develop local, more personalised connections

100

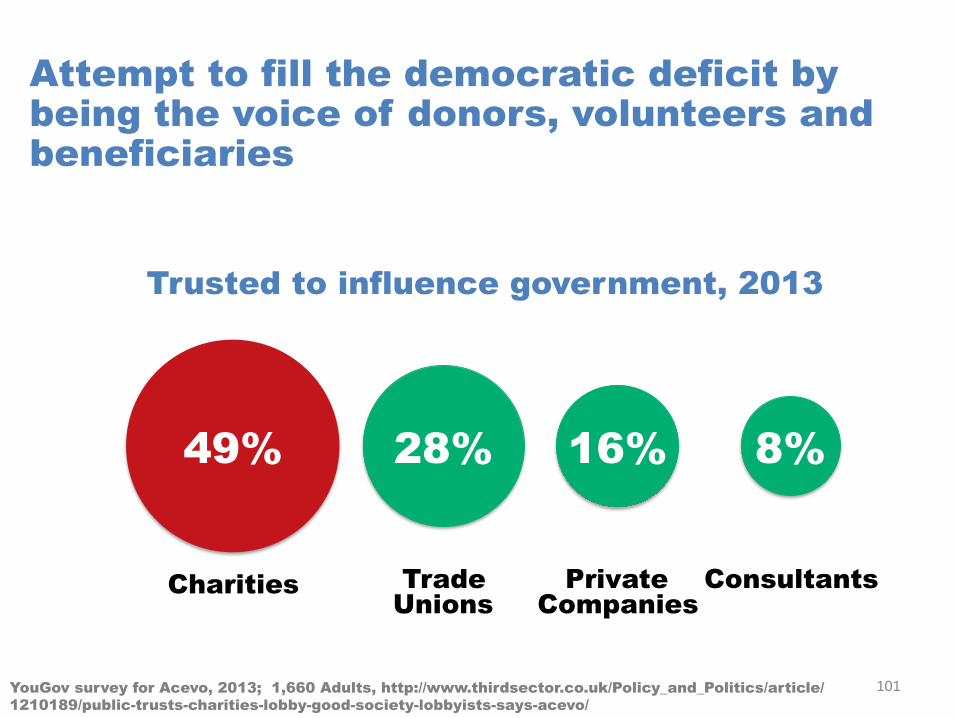

Attempt to fill the democratic deficit by being the voice of donors, volunteers and beneficiaries

Trusted to influence government, 2013

49% 28% 16% 8%

Charities Trade Unions

Private Companies

Consultants

101 YouGov survey for Acevo, 2013; 1,660 Adults, http://www.thirdsector.co.uk/Policy_and_Politics/article/1210189/public-trusts-charities-lobby-good-society-lobbyists-says-acevo/

102

Speak to a wide range of parties

103

And finally…

Sofia, Bulgaria in 1997 – What I learned…

104

Be Flexible Adapt Scan

Connect Relate

Innovate Plan

In difficult times you need to…

Be Optimistic