want to manage the impact of volatility in your portfolio? report... · rex volmaxx long vix weekly...

TRANSCRIPT

powershares.com | @PowerShares

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund’s return may not match the return of the Underlying Index. The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the Fund.In general, equity values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.Volatility: is a statistical measurement of the magnitude of up and down asset price fluctuations over time.

Investments focused in a particular industry are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.The Fund is non-diversified and may experience greater volatility than a more diversified investment.There is no assurance that the Fund will provide low volatility.Shares are not individually redeemable and owners of the shares may acquire those shares from the Funds and tender those shares for redemption to the Funds in Creation Unit aggregations only, typically consisting of 50,000 shares.Shares are not FDIC insured, may lose value and have no bank guarantee.

Invesco PowerShares Capital Management LLC and Invesco Distributors, Inc. are indirect, wholly owned subsidiaries of Invesco Ltd.

Before investing, investors should carefully read the prospectus/summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the Fund call 800 983 0903 or visit invescopowershares.com for the prospectus/summary prospectus.

US4327 04/15

S&P 500® Low Volatility

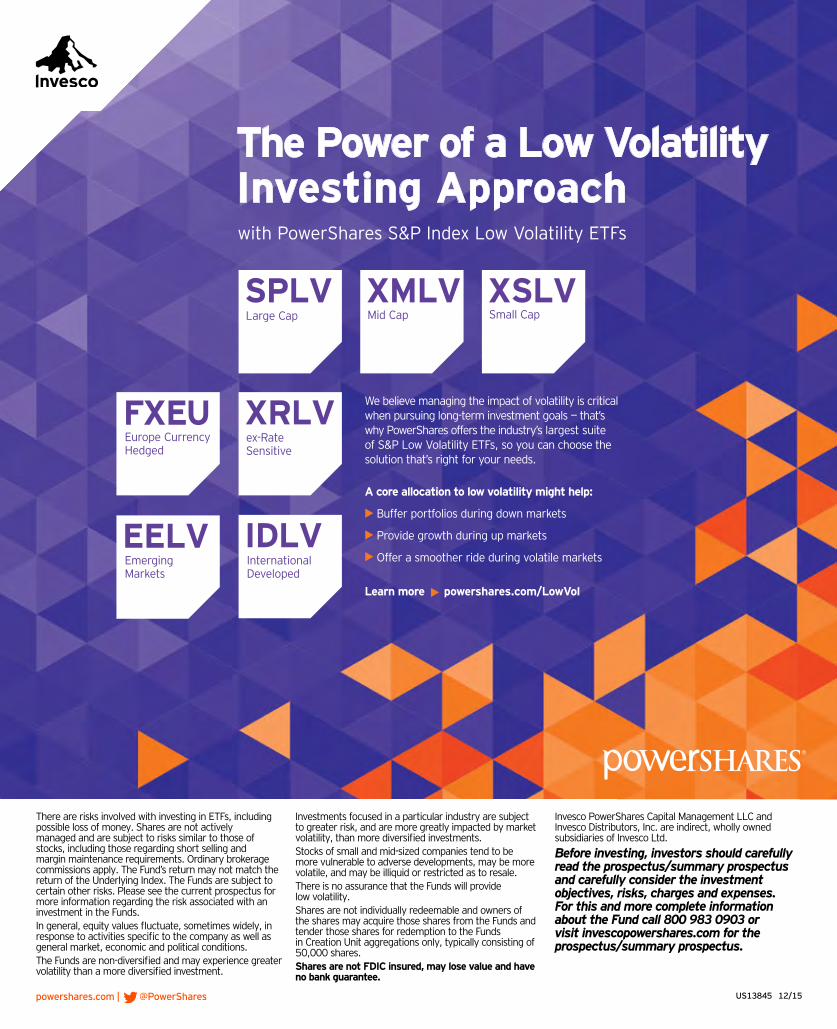

We believe managing the impact of volatility is critical when pursuing long-term investment goals — that’s why PowerShares offers the industry’s largest suite of S&P Low Volatility ETFs, including SPLV, so you can choose the solution that’s right for your needs.

A core allocation to low volatility might help:

Buffer portfolios during down markets

Provide growth during up markets

Offer a smoother ride during volatile markets

Learn more powershares.com/LowVol

Want to Manage the Impact of Volatility in Your Portfolio?

A D V E R T I S E M E N T

ADVERTISEMENT

powershares.com | @PowerShares

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund’s return may not match the return of the Underlying Index. The Funds are subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the Funds.In general, equity values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.The Funds are non-diversified and may experience greater volatility than a more diversified investment.

Investments focused in a particular industry are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.Stocks of small and mid-sized companies tend to be more vulnerable to adverse developments, may be more volatile, and may be illiquid or restricted as to resale.There is no assurance that the Funds will provide low volatility.Shares are not individually redeemable and owners of the shares may acquire those shares from the Funds and tender those shares for redemption to the Funds in Creation Unit aggregations only, typically consisting of 50,000 shares.Shares are not FDIC insured, may lose value and have no bank guarantee.

Invesco PowerShares Capital Management LLC and Invesco Distributors, Inc. are indirect, wholly owned subsidiaries of Invesco Ltd.

Before investing, investors should carefully read the prospectus/summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the Fund call 800 983 0903 or visit invescopowershares.com for the prospectus/summary prospectus.

US13845 12/15

Mid Cap Small Cap

International Developed

Large Cap

Emerging Markets

Europe Currency Hedged

ex-Rate Sensitive

We believe managing the impact of volatility is critical when pursuing long-term investment goals — that’s why PowerShares offers the industry’s largest suite of S&P Low Volatility ETFs, so you can choose the solution that’s right for your needs.

A core allocation to low volatility might help:

Buffer portfolios during down markets

Provide growth during up markets

Offer a smoother ride during volatile markets

Learn more powershares.com/LowVol

with PowerShares S&P Index Low Volatility ETFs

The Power of a Low Volatility Investing Approach

FXEU

ADVERTISEMENT

One Strong Core

www.spdji.com/indexology

The interlocking might of U.S. Mid and Small Caps strengthens a Large Cap core. Assemble your winning strategy with S&P DJI-based ETFs and mutual funds to push your core forward.

S&P 500®

S&P MidCap 400®

S&P SmallCap 600®

indexology®

powers purpose

© S&P Dow Jones Indices LLC, a division of S&P Global 2016. All rights reserved. S&P® and Indexology® and Indexology® ® are registered trademarks of Standard & Poor’s Financial Services LLC. ® are registered trademarks of Standard & Poor’s Financial Services LLC. ®

Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. It is not possible to invest directly in an index. S® is a registered trademark of Dow Jones Trademark Holdings LLC. It is not possible to invest directly in an index. S® &P Dow Jones Indices receives compensation for licensing its indices to third parties. S&P Dow Jones Indices LLC does not make investment recommendations and does not endorse, sponsor, promote or sell any investment product or fund.

© 2016 ETF.com. All rights reserved. The text, images and other materials contained or displayed are proprietary to ETF.com, except where otherwise noted, and constitute valuable intellectual property. No material from any part of any ETF.com publication, product, service, report, email or website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of ETF.com. For permission to photocopy and use material electronically, please contact [email protected] or call 646-558-6985.

VOLUME 16 | NO. 7 Contents

PUBLISHER, GLOBAL HEAD OF SALESNoel d’Ablemont Smith, 646-558-6985

CHIEF EXECUTIVE OFFICER David Lichtblau

REPRINT SALESKevin Kelly, 646-582-9040

EDITOR Drew Voros

MANAGING EDITOR Heather Bell

COPY EDITOR Lisa Barr

HEAD OF DESIGN Patrick Hamaker

ETF.com222 Sutter Street, Ste. 700

San Francisco, CA 94108www.ETF.com

Want to reach ETF-using advisors and RIAs? Post your ad in the ETF Report Marketplace! Contact Kevin Kelly @ 646.582.9040 to learn more.

ETF Report MARKETPLACE

4 New ETF Launches Global X ETF is first to target millennials. Plus: Our monthly look at launches and closures.

5 ETF Explainer: TAN Our ETF Explainer looks at the ups and downs of the best-known solar power fund.

6 Profile Beaumont Capital Management has mastered the art of the defensive portfolio.

29 Fintech In Focus Bronfman E.L. Rothschild’s Jill Lizzi highlights the versatility of the Tamarac Advisor Suite.

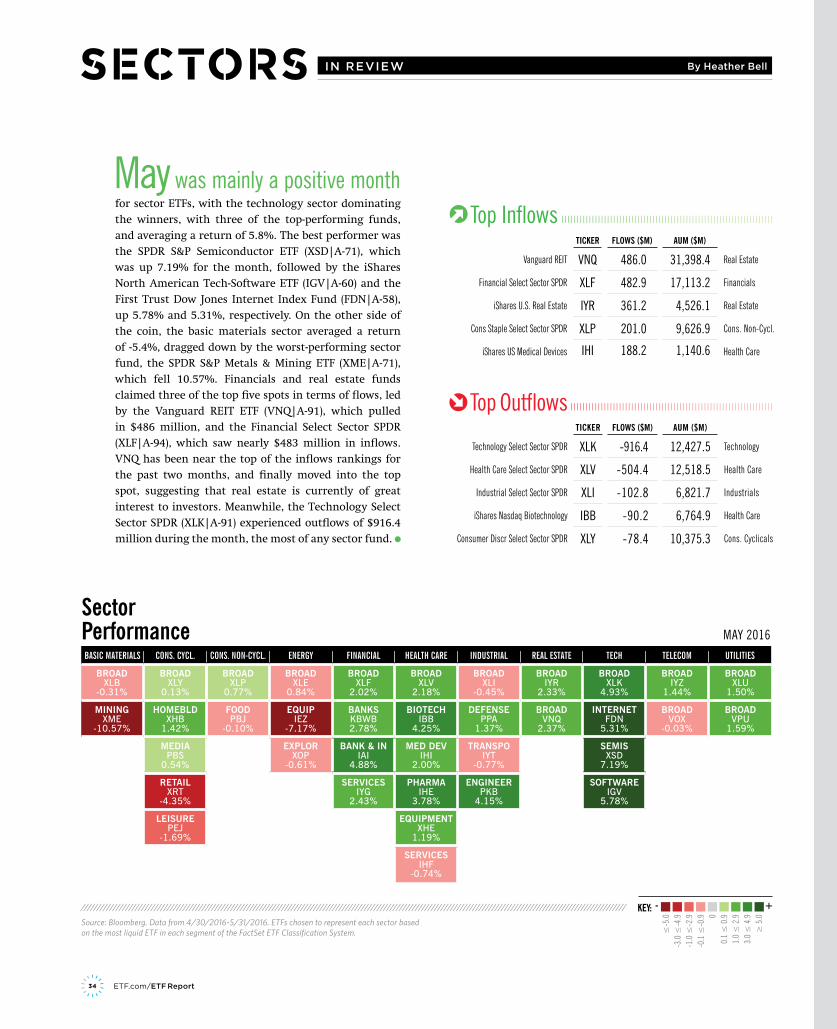

34 Sectors Technology had the best month of any sector, while basic materials stocks struggled.

DEPARTMENTS

Midyear’s Leaders & LosersPrecious metals miners dominate the top 10 ETFs in terms of performance in 2016 after gold has a stellar first five months of 2016.

Where The Money Went Gold and minimum-volatility funds pulled in billions of dollars year-to-date.

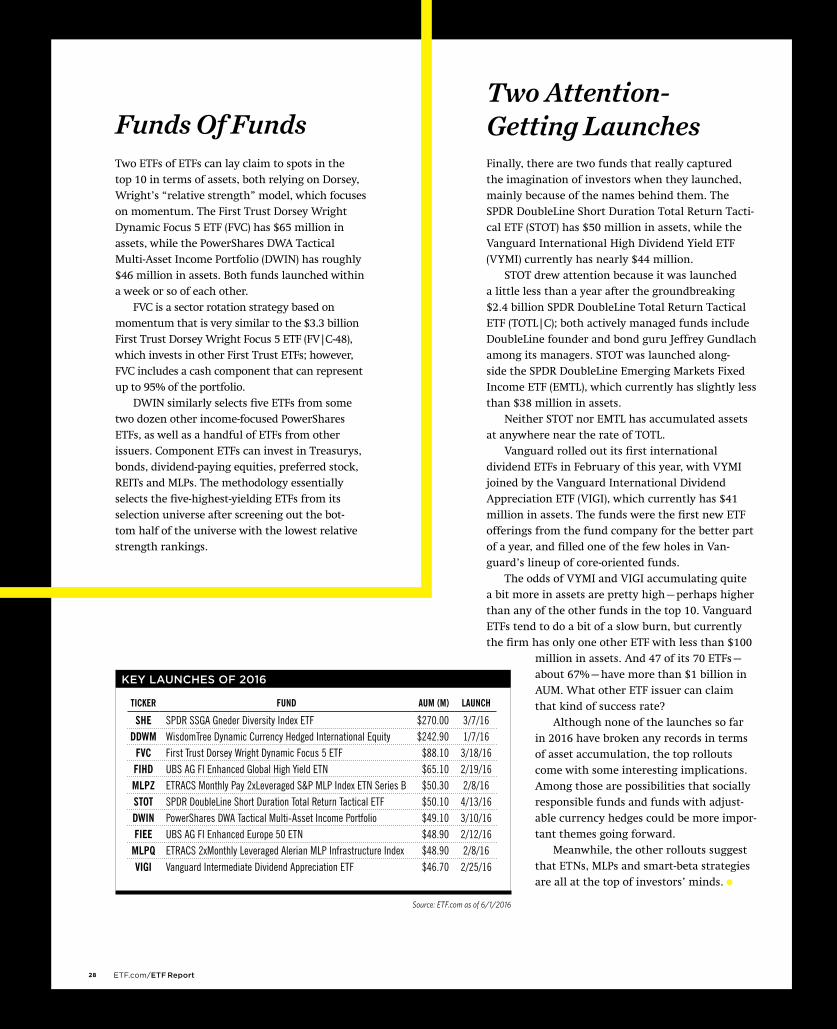

Key Launches Of 2016The first five months of this year didn’t have any runaway hits in the ETF space, but there were several notable rollouts.

Smart-Beta SupplementiShares’ Rob Nestor on the demand and design that goes into multifactor sectors. Plus: The smart-beta launches page, along with the leading funds in the smart-beta space.

10182630

FEATURES

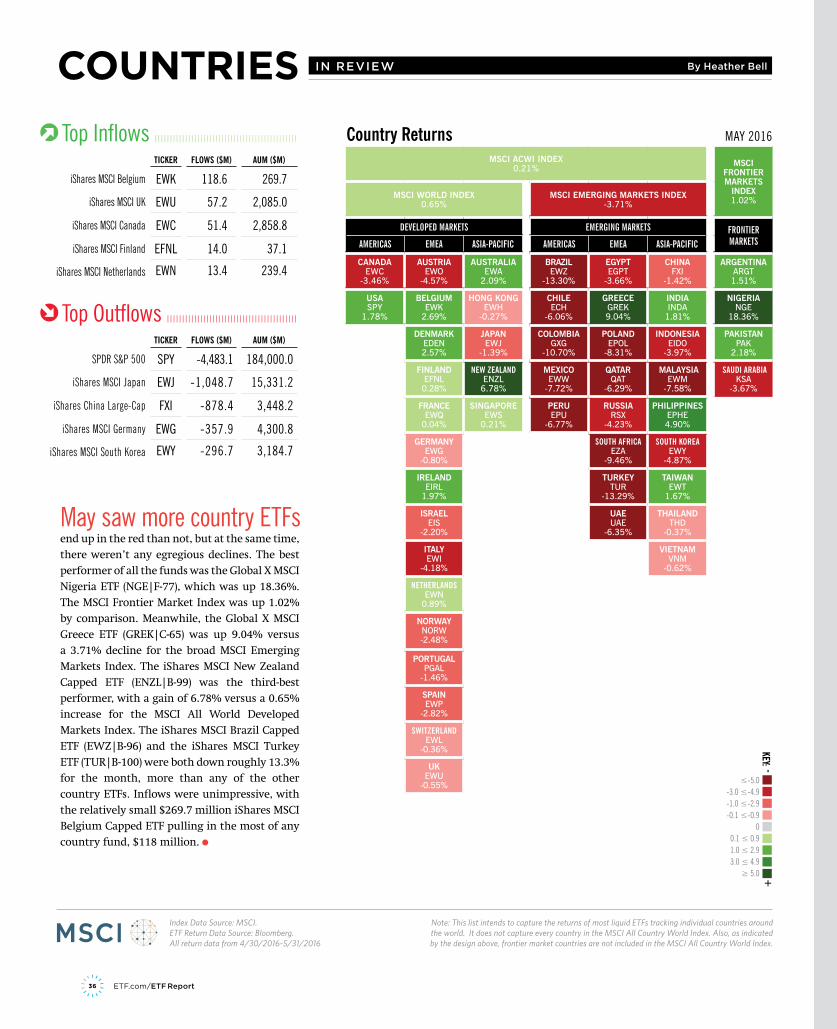

36 Countries The Global X Nigeria ETF outperformed all the other country funds in May.

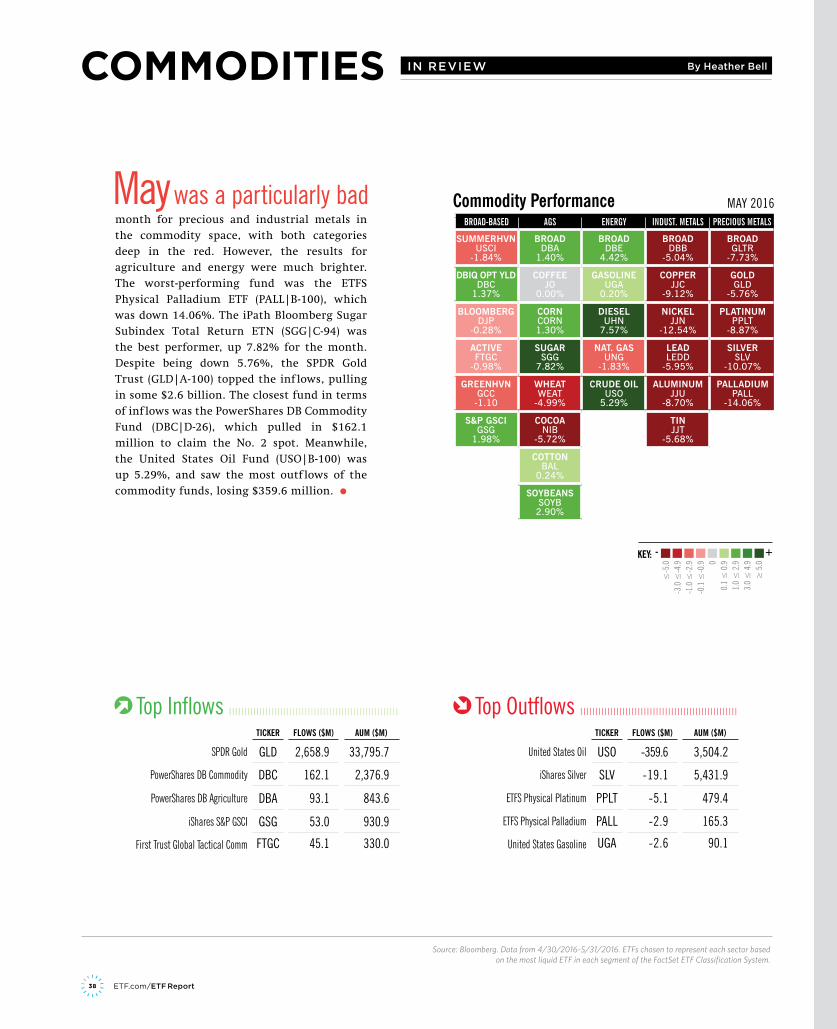

38 Commodities May was a bad month for commodities, with metals funds ending up deep in the red.

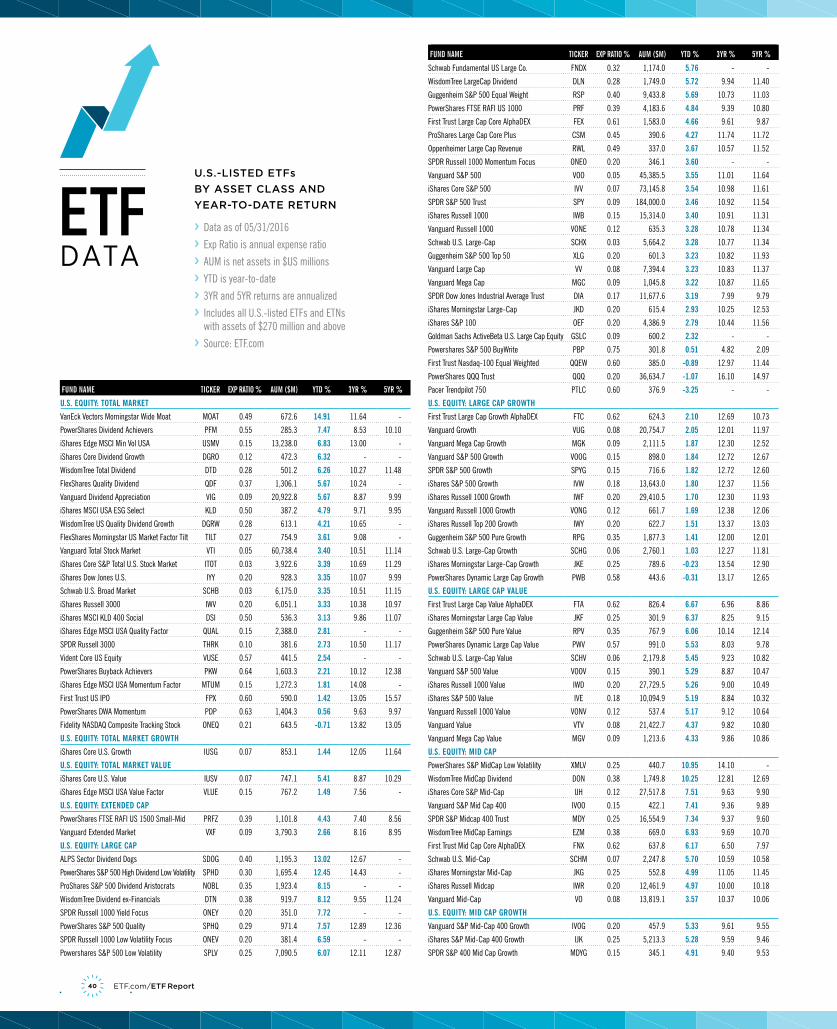

40 ETF Data Our monthly databank breaks down ETF returns for every market segment.

45PAGE

4 ETF.com/ETF Report

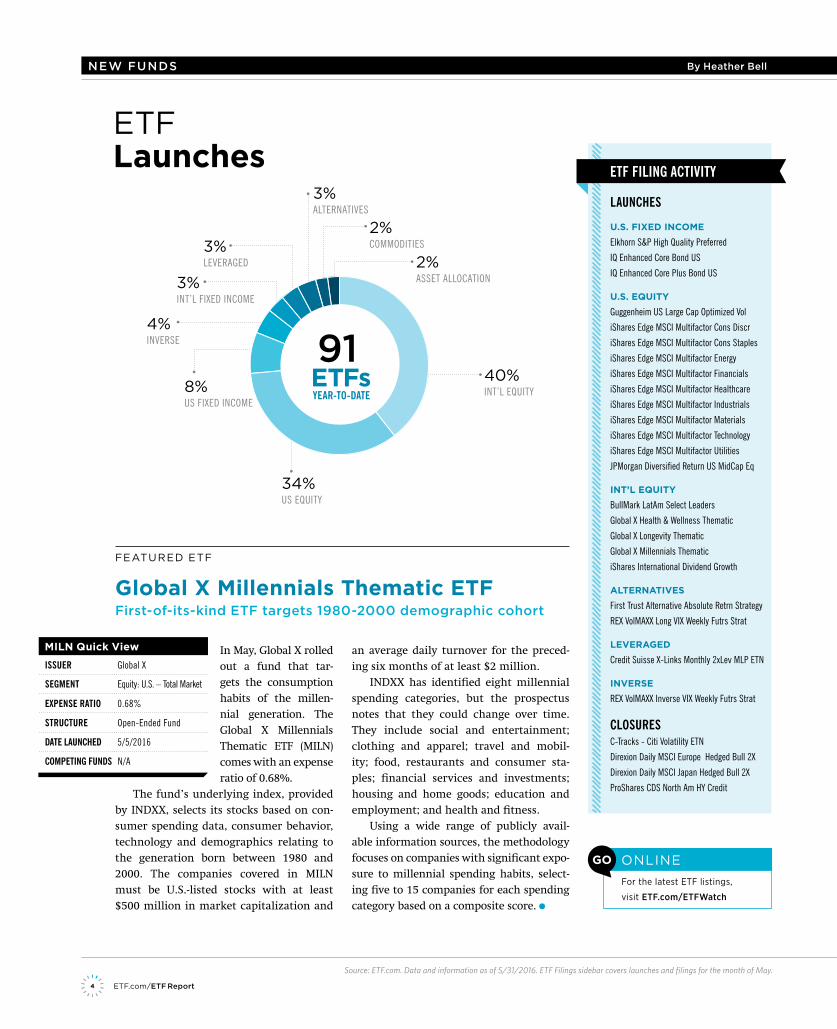

Global X Millennials Thematic ETFFirst-of-its-kind ETF targets 1980-2000 demographic cohort

an average daily turnover for the preced-ing six months of at least $2 million.

INDXX has identified eight millennial spending categories, but the prospectus notes that they could change over time. They include social and entertainment; clothing and apparel; travel and mobil-ity; food, restaurants and consumer sta-ples; financial services and investments; housing and home goods; education and employment; and health and fitness.

Using a wide range of publicly avail-able information sources, the methodology focuses on companies with significant expo-sure to millennial spending habits, select-ing five to 15 companies for each spending category based on a composite score.

Source: ETF.com. Data and information as of 5/31/2016. ETF Filings sidebar covers launches and filings for the month of May.

ETFLaunches

FEATURED ETF

NEW FUNDS By Heather Bell

In May, Global X rolled out a fund that tar-gets the consumption habits of the millen-nial generation. The Global X Millennials Thematic ETF (MILN) comes with an expense ratio of 0.68%.

The fund’s underlying index, provided by INDXX, selects its stocks based on con-sumer spending data, consumer behavior, technology and demographics relating to the generation born between 1980 and 2000. The companies covered in MILN must be U.S.-listed stocks with at least $500 million in market capitalization and

ETF FILING ACTIVITY

LAUNCHES

U.S. FIXED INCOME

Elkhorn S&P High Quality Preferred

IQ Enhanced Core Bond US

IQ Enhanced Core Plus Bond US

U.S. EQUITY

Guggenheim US Large Cap Optimized Vol

iShares Edge MSCI Multifactor Cons Discr

iShares Edge MSCI Multifactor Cons Staples

iShares Edge MSCI Multifactor Energy

iShares Edge MSCI Multifactor Financials

iShares Edge MSCI Multifactor Healthcare

iShares Edge MSCI Multifactor Industrials

iShares Edge MSCI Multifactor Materials

iShares Edge MSCI Multifactor Technology

iShares Edge MSCI Multifactor Utilities

JPMorgan Diversified Return US MidCap Eq

INT’L EQUITY

BullMark LatAm Select Leaders

Global X Health & Wellness Thematic

Global X Longevity Thematic

Global X Millennials Thematic

iShares International Dividend Growth

ALTERNATIVES

First Trust Alternative Absolute Retrn Strategy

REX VolMAXX Long VIX Weekly Futrs Strat

LEVERAGED

Credit Suisse X-Links Monthly 2xLev MLP ETN

INVERSE

REX VolMAXX Inverse VIX Weekly Futrs Strat

CLOSURESC-Tracks - Citi Volatility ETN

Direxion Daily MSCI Europe Hedged Bull 2X

Direxion Daily MSCI Japan Hedged Bull 2X

ProShares CDS North Am HY Credit

MILN Quick View

ISSUER Global X

SEGMENT Equity: U.S. – Total Market

EXPENSE RATIO 0.68%

STRUCTURE Open-Ended Fund

DATE LAUNCHED 5/5/2016

COMPETING FUNDS N/A

GO

For the latest ETF listings,

visit ETF.com/ETFWatch

ONLINE

34%US EQUITY

8% US FIXED INCOME

40% INT’L EQUITY

4% INVERSE

3% LEVERAGED 2%

ASSET ALLOCATION

2% COMMODITIES

3% ALTERNATIVES

3% INT’L FIXED INCOME

ETFs91

YEAR-TO-DATE

5JULY 2016

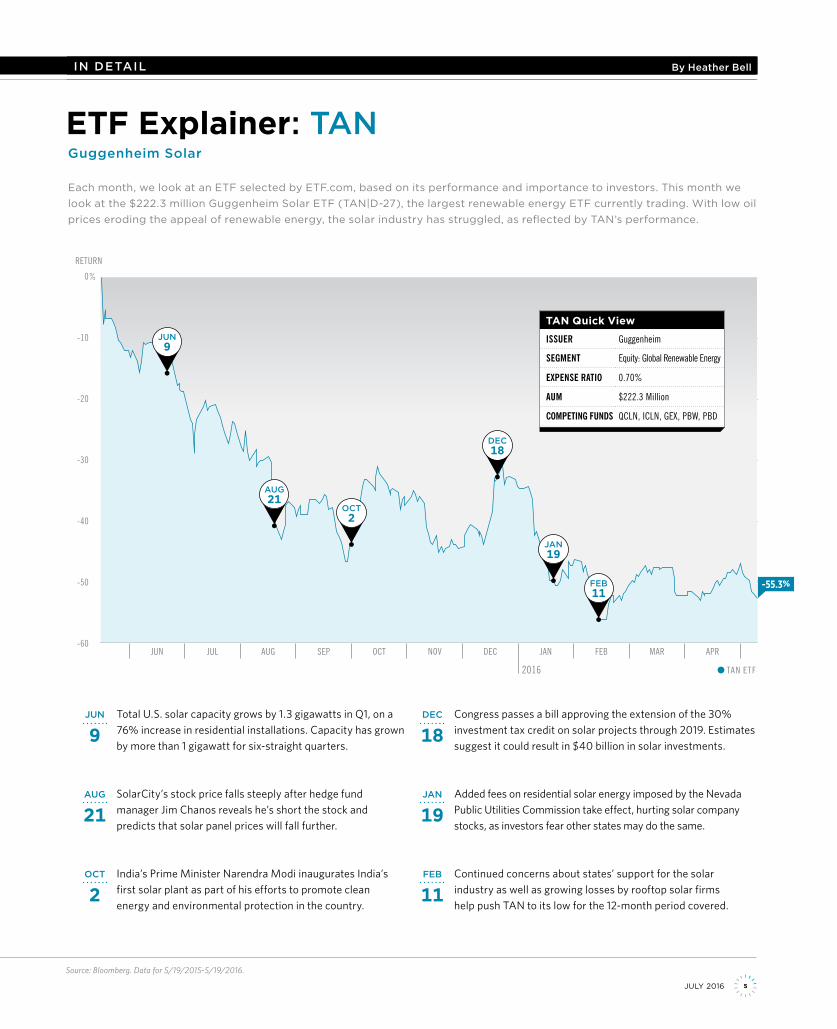

Guggenheim Solar

Each month, we look at an ETF selected by ETF.com, based on its performance and importance to investors. This month we look at the $222.3 million Guggenheim Solar ETF (TAN|D-27), the largest renewable energy ETF currently trading. With low oil prices eroding the appeal of renewable energy, the solar industry has struggled, as reflected by TAN’s performance.

Source: Bloomberg. Data for 5/19/2015-5/19/2016.

ETF Explainer: TAN

JUN Total U.S. solar capacity grows by 1.3 gigawatts in Q1, on a 76% increase in residential installations. Capacity has grown by more than 1 gigawatt for six-straight quarters.

9DEC Congress passes a bill approving the extension of the 30%

investment tax credit on solar projects through 2019. Estimates suggest it could result in $40 billion in solar investments.

18

AUG SolarCity’s stock price falls steeply after hedge fund manager Jim Chanos reveals he’s short the stock and predicts that solar panel prices will fall further.

21JAN Added fees on residential solar energy imposed by the Nevada

Public Utilities Commission take effect, hurting solar company stocks, as investors fear other states may do the same.

19

OCT India’s Prime Minister Narendra Modi inaugurates India’s first solar plant as part of his efforts to promote clean energy and environmental protection in the country.

2FEB Continued concerns about states’ support for the solar

industry as well as growing losses by rooftop solar firms help push TAN to its low for the 12-month period covered.

11

IN DETAIL By Heather Bell

JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR APR

2016

0

-10

-20

-30

-40

-50

-60

%

RETURN

TAN ETF

-55.3%

TAN Quick View

ISSUER Guggenheim

SEGMENT Equity: Global Renewable Energy

EXPENSE RATIO 0.70%

AUM $222.3 Million

COMPETING FUNDS QCLN, ICLN, GEX, PBW, PBD

JUN9

AUG21

OCT2

DEC18

JAN19

FEB11

6 ETF.com/ETF Report

Smoothing ThePath For Investors

BEAUMONT CAPITAL MANAGEMENT (BCM) is an all-ETF offshoot of Beaumont Financial Partners, a firm that’s been around for more than 30 years, offering comprehensive wealth management—including tax preparation, financial planning and investment

management—for high net worth individuals, as well as institutions in 401(k) profit-sharing and other retirement plans.

The decision to create BCM as a separate division stemmed from client demand for access to the institutional defensive tools and strategies Beaumont was known for, at a time when the market was facing its worst downturn since the Great Depression. BCM was started in

2009, and today it boasts nearly $3 billion in assets under management, with roughly $4 billion as a firm.

Managing Partner David Haviland discusses his firm’s approach and how it helps investors achieve their goals.

By Cinthia Murphy

LIMITING LOSSES TO KEEP INVESTORS MOVING FORWARD

FIRM Beaumont Capital Management

FOUNDED 2009

LOCATION Needham, MA

AUM/AUA $2.8 Billion*

% OF ETFs 100%*

Advisor Quick View

6 ETF.com/ETF Report

DAVID HAVILAND Managing Partner

* refers to ETF strategist division

PROFILE

7JULY 2016

Why is defense the best offense when it comes to investing?

I learned a long time ago, from my father, that what clients care the most about is not losing a lot of money. And it is borne out in the philosophy of our firm: The No. 1 rule of successful long-term investing is to avoid large losses that become present in bear markets.

We’ve been around since 1981, and we’ve lived through the 2001-02 and the 2008-09 downturns. Our clients asked us if we could institutionalize our defen-sive philosophy in managing money, and so in 2009, we started Beaumont Capital Management, where we used long-only ETFs and some rules-based systems to provide this defensive capability during downturns.

Is 2009, then, the first time you used ETFs in your practice?

No, we’d used them before. We find ETFs to be a very easy and beneficial vehicle to form investment strategies with. You need to learn how to trade them, but once you do, the trading and liquidity is tremendous. You avoid individual company risk, and you can get both passive and active management within ETFs. It’s low cost. ETFs are a great tool, particularly for BCM, where we’re 100% dedicated to providing tactical and dynamic investment strategies.

In a vast world of investment managers, what sets BCM apart?

Having an investment advisory background really gives us some unique perspectives on managing money. To be clear, at BCM, we don’t compete against our investment advisor client base. But what sets us apart is Beaumont’s long history of being an advisor, and sitting down with clients. We’ve got a very good understanding of what cli-ents want and/or need. And when we bring this perspec-tive to asset management, it allows us to bring many advantages.

Let me give you an example. In the 401(k) space, when we’re working with a client, we’ve literally been in each and every role within the 401(k) space. We’ve been an advisor to a plan. We’ve been an advisor to a participant. We’ve been an advisor to a sponsor. We’re a sponsor. And now we’re a fund manager in the 401(k) space. That gives us unique perspective when it comes to managing money.

Let’s talk about one of your flagship approaches, which is centered on sector rotation. Why do you

think that’s a good way to go?Sector rotation, and momentum-based investing, have been around for at least 50 years.

We’re seeking to take advantage of how sectors per-form in different stages of the business cycle, and the stock market cycle. There are times when various sec-tors are going to outperform, and times they’re going to underperform.

When you’re in a roaring bull market, almost all the sectors are on. But in a market like we’re in right now, we’re only invested in some sectors in U.S. large-cap. We’re able to avoid the volatility that’s been present in the energy and materials sectors. That goes to our process, where we’re taking advantage of momentum in each sec-tor. There are more inputs involved, but if the momentum and price movement of a sector is positive, it’s likely we’ll own it. And we equal-weight them in the portfolio.

How are your clients using these sector strategies in their portfolios?

Many of our advisor clients use the U.S. sector rotation as a core holding, and as a substitute to the S&P 500, tak-ing advantage of the fact that their clients are looking for an automatic sale process before you get too deep into a rout such as 2008 or 2009. Remember that it’s all about being defensive, so in these strategies, we’re getting out of the way before sectors see large losses. In fact, recently, we were as much as 75% cash during a market downturn, but we got invested fairly quickly as the momentum was re-established.

You also have a separate series called Decathlon. How is that one different?

The momentum-based sector rotation series is tactically constrained, meaning it’s constrained to the indices where each of those sectors resides, and uses cash as the defensive mechanism. The Decathlon series is tactically unconstrained. It uses pattern recognition technology to seek investment opportunities that are positive, regard-less of where they are. And by “unconstrained,” I mean they’re unconstrained across geography, asset class and market capitalization—we have currency funds, com-modity funds, real estate funds; there’s a plethora of choices in equity and bonds.

8 ETF.com/ETF Report

BCM has attracted some $3 billion since 2009, becoming one of the biggest strategists in the

space. To what do you attribute your success? Philosophy? A really strong distribution network and marketing? At its core, our philosophy of not losing large amounts of money resonates well with other financial profes-sionals, because we design our products to meet their clients’ needs. This is backed up by behavioral finance. Investors feel losses far more powerfully than gains. It’s this response to negative returns that drives most inves-tors to do the worst possible things at the worst possible times, which is to sell during the capitulation stage of bear markets. And then, they compound their error by waiting three, five, seven years until the markets have “proven” that it’s safe to get back in, and they invest at or near the top of that next cycle.

What all of our systems do—our momentum-based, sector rotation series, as well as our Decathlon series—is seek to avoid the vast majority of those losses and smooth the ride for investors, so that everyone can con-centrate on doing the right thing, which is get out of the way of the large losses, but stay invested during “nor-mal” market action.

BCM is a tactical shop. How should investors use tactical managers?

A properly constructed portfolio should involve strate-gic as well as tactical components. To be very simplistic, if you were building a portfolio, and you were to put one-third into strategic equity, one-third into strategic fixed income and one-third into tactical, we’d take each of those buckets and then divide again in half.

In the strategic, you would have half in index-based passive investments, and half in the best strategic man-ager you can find; for example, S&P 500 and Will Danoff of Contrafund, because Will is one of eight managers that has beaten the S&P on a one-, three-, five-, 10-, 20- and 25-year basis.

On the fixed-income side, we would suggest using something like the iShares Core U.S. Aggregate Bond ETF (AGG|A-98), and then maybe the SPDR DoubleLine Total Return Tactical ETF (TOTL|C), which is Jeffrey Gundlach’s fund, which is actively managed and has the ability to generate alpha in a rising-interest-rate environment.

Then you have your tactical allocation, which we recommend be divided into two managers. The idea is to build a robust portfolio that focuses on both active and

passive, and it’s diversified. If either the bond or stock part of the portfolio goes into a period of market failure, the tactical manager can rotate out of the way or raise cash. It’s all about smoothing out the ride for the inves-tor, and keeping them invested over a full market cycle.

How do you choose ETFs? Are you provider-agnostic?

We are provider-agnostic, with a notable exception to the obvious: In our sector rotation, we offer the State Street SPDRs as our flagship. That’s who we started with originally. For customers who clear through Fidelity, we use the Fidelity ETFs, because currently, they’re trading commission-waived, at the lowest embedded expense ratio. So if you’re supersensitive to expense, then the Advantage series is the preferred family. And we’re also using some First Trust ETFs, which have their own quan-titative process.

In our Decathlon series, the process uses price his-tory as part of the system, and tries to avoid overcon-centration. So the pool is primarily made up of iShares ETFs. It has a broad selection of ETFs with long track records and diverse attributes.

As the strategist space grows, do you feel pressured to innovate?

We’ve got a very well-defined, three-year rolling strate-gic plan as a business. And we’re continuing to expand within the 401(k) and retirement markets. That is our current strategic initiative. We also just became a model manager on a mutual fund, and are in negotiations on a second fund.

In the near future, we will be getting into more of the institutional market. But the opportunity within the 401(k) space and these other markets is something we’re looking to grow in. I don’t feel any pressure, though. I think our strategies and the benefits they provide speak for themselves.

As an ETF strategist, what’s the opportunity you see in the 401(k) space?

I believe it’s massive. And the reason it’s so large is because of the shortcomings of the first generation of target-date funds out there. We offer target-date funds that are among the lowest-cost target-date fund fami-lies in the industry. Our total expense ratio, all in, is less than half of the average of actively managed tar-get-date funds used in 401(k)s today.

PROFILE

8 ETF.com/ETF Report

ADVERTISEMENT

S:8”

You wear many hats fulfi lling your responsibility to your clients. But the biggest challenge you face is managing their investment expectations. We share the belief that long-term, low-cost investing is the right approach. That’s why Vanguard offers you research, low-cost ETFs, and over 40 years of indexing experience to help make managing your clients’ expectations exactly that. More manageable.

For the support you deserve, visit our Financial Advisors siteat advisors.vanguard.com/BD today.

800 414-4684

Are you Vanguarding® your clients’ portfolios?

All investing is subject to risk, including the possible loss of the money you invest.

Vanguard ETF Shares can be bought and sold only through a broker (who may charge a commission) and cannot be redeemed with the issuing Fund. The market price of Vanguard ETF Shares may be more or less than net asset value.

For more information about Vanguard ETF Shares, visit advisors.vanguard.com/BD, call 800 414-4684, or contact your broker to obtain a prospectus. Investment objectives, risks, charges, expenses, and other important information are contained in the prospectus; read and consider it carefully before investing.

© 2016 The Vanguard Group, Inc. All rights reserved. Vanguard Marketing Corporation, Distributor. U.S. Patent Nos. 6,879,964; 7,337,138; 7,720,749; 7,925,573; 8,090,646; and 8,417,623.

Follow us @Vanguard_FA for important insights, news and education.

You don’t just manage portfolios. You manage expectations. That’s a huge responsibility.

PERFORMING ETFs OF 2016

MIDYEAR REPORT

&

top 10 nonleveraged/noninverse exchange-traded funds of the year all belong to a single group: gold and silver miners.

Miner ETFs, which had been beaten down for years amid falling gold prices and other industry-related woes, finally had things working in their favor when gold unexpectedly surged at the start of 2016.

Though concerns about misman-agement and high costs remain, for now, investors are looking past all that and seeing the industry as a leveraged bet on higher gold prices. With gold trending up, that’s a bet that’s paying off.

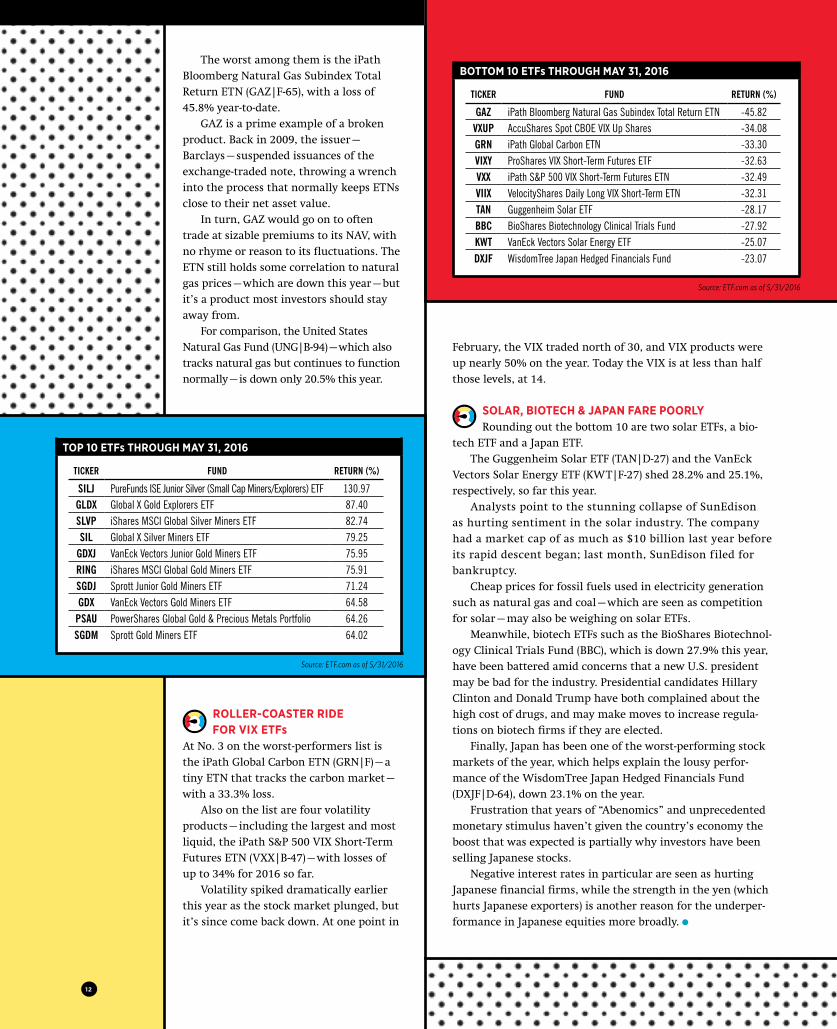

RETURNS OF 64% OR MOREThe threshold to be among

the top-performing ETFs is high. Each of the top 10 has gains rang-ing from 64% to 131%, with the PureFunds ISE Junior Silver ETF (SILJ|F-64) at the top of the pack.

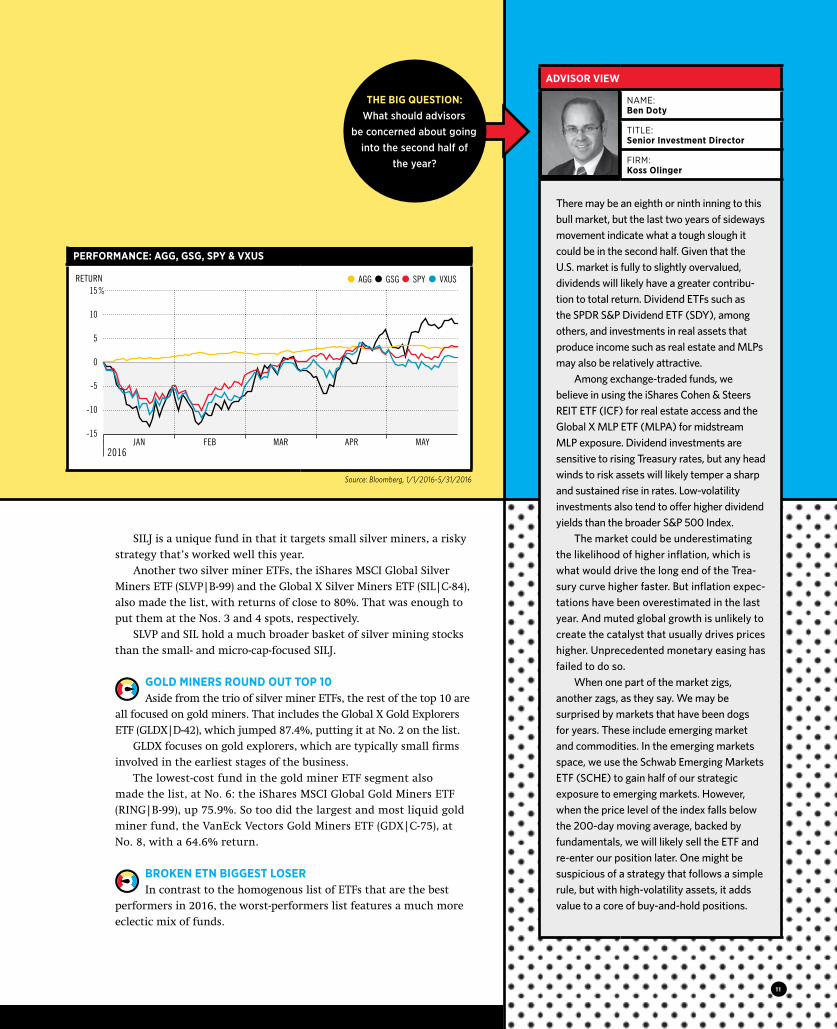

IT’S BEEN A GOOD YEAR FOR FINANCIAL MAR-KETS SO FAR IN 2016. After a bumpy start to the year, most major asset classes were up through the end of May, including stocks, bonds and commodities.

Even international stocks are hanging in there, with a slight gain for the year. As of this writing, the Vanguard Total International Stock ETF (VXUS|A-97) was up by 1.1% year-to-date.

U.S. stocks are doing a bit better—the SPDR S&P 500 ETF (SPY|A-97) is up 3.5%. That’s essentially the same return that bonds have given investors this year; the iShares Core U.S. Aggregate Bond ETF (AGG|A-98) has gained 3.3% on the year.

Meanwhile, leading all asset classes are commodities. The iShares S&P GSCI Commodity Indexed Trust (GSG|C-91) rallied 8.4% through the first five months of the year.

MINERS DOMINATE TOP PERFORMERS LISTThe strong gains in commodities are thanks to

a surprising rebound in the price of oil and gold. The United States Brent Oil Fund (BNO), for example, is up a cool 22.9% year-to-date, while the SPDR Gold Trust (GLD|A-100) is up about 14.4%.

But as impressive as the gains in those ETFs are, they aren’t even close to the top of the heap. The

BESTWORST

By Sumit Roy

10

SILJ is a unique fund in that it targets small silver miners, a risky strategy that’s worked well this year.

Another two silver miner ETFs, the iShares MSCI Global Silver Miners ETF (SLVP|B-99) and the Global X Silver Miners ETF (SIL|C-84), also made the list, with returns of close to 80%. That was enough to put them at the Nos. 3 and 4 spots, respectively.

SLVP and SIL hold a much broader basket of silver mining stocks than the small- and micro-cap-focused SILJ.

GOLD MINERS ROUND OUT TOP 10Aside from the trio of silver miner ETFs, the rest of the top 10 are

all focused on gold miners. That includes the Global X Gold Explorers ETF (GLDX|D-42), which jumped 87.4%, putting it at No. 2 on the list.

GLDX focuses on gold explorers, which are typically small firms involved in the earliest stages of the business.

The lowest-cost fund in the gold miner ETF segment also made the list, at No. 6: the iShares MSCI Global Gold Miners ETF (RING|B-99), up 75.9%. So too did the largest and most liquid gold miner fund, the VanEck Vectors Gold Miners ETF (GDX|C-75), at No. 8, with a 64.6% return.

BROKEN ETN BIGGEST LOSERIn contrast to the homogenous list of ETFs that are the best

performers in 2016, the worst-performers list features a much more eclectic mix of funds.

ADVISOR VIEW

NAME: Ben Doty

TITLE: Senior Investment Director

FIRM: Koss Olinger

There may be an eighth or ninth inning to this bull market, but the last two years of sideways movement indicate what a tough slough it could be in the second half. Given that the U.S. market is fully to slightly overvalued, dividends will likely have a greater contribu-tion to total return. Dividend ETFs such as the SPDR S&P Dividend ETF (SDY), among others, and investments in real assets that produce income such as real estate and MLPs may also be relatively attractive.

Among exchange-traded funds, we believe in using the iShares Cohen & Steers REIT ETF (ICF) for real estate access and the Global X MLP ETF (MLPA) for midstream MLP exposure. Dividend investments are sensitive to rising Treasury rates, but any head winds to risk assets will likely temper a sharp and sustained rise in rates. Low-volatility investments also tend to offer higher dividend yields than the broader S&P 500 Index.

The market could be underestimating the likelihood of higher inflation, which is what would drive the long end of the Trea-sury curve higher faster. But inflation expec-tations have been overestimated in the last year. And muted global growth is unlikely to create the catalyst that usually drives prices higher. Unprecedented monetary easing has failed to do so.

When one part of the market zigs, another zags, as they say. We may be surprised by markets that have been dogs for years. These include emerging market and commodities. In the emerging markets space, we use the Schwab Emerging Markets ETF (SCHE) to gain half of our strategic exposure to emerging markets. However, when the price level of the index falls below the 200-day moving average, backed by fundamentals, we will likely sell the ETF and re-enter our position later. One might be suspicious of a strategy that follows a simple rule, but with high-volatility assets, it adds value to a core of buy-and-hold positions.

THE BIG QUESTION: What should advisors

be concerned about going into the second half of

the year?

PERFORMANCE: AGG, GSG, SPY & VXUS

JAN FEB MAR APR MAY2016

Source: Bloomberg, 1/1/2016-5/31/2016

15

10

5

0

-5

-10

-15

% RETURN AGG GSG SPY VXUS

11

February, the VIX traded north of 30, and VIX products were up nearly 50% on the year. Today the VIX is at less than half those levels, at 14.

SOLAR, BIOTECH & JAPAN FARE POORLYRounding out the bottom 10 are two solar ETFs, a bio-

tech ETF and a Japan ETF. The Guggenheim Solar ETF (TAN|D-27) and the VanEck

Vectors Solar Energy ETF (KWT|F-27) shed 28.2% and 25.1%, respectively, so far this year.

Analysts point to the stunning collapse of SunEdison as hurting sentiment in the solar industry. The company had a market cap of as much as $10 billion last year before its rapid descent began; last month, SunEdison filed for bankruptcy.

Cheap prices for fossil fuels used in electricity generation such as natural gas and coal—which are seen as competition for solar—may also be weighing on solar ETFs.

Meanwhile, biotech ETFs such as the BioShares Biotechnol-ogy Clinical Trials Fund (BBC), which is down 27.9% this year, have been battered amid concerns that a new U.S. president may be bad for the industry. Presidential candidates Hillary Clinton and Donald Trump have both complained about the high cost of drugs, and may make moves to increase regula-tions on biotech firms if they are elected.

Finally, Japan has been one of the worst-performing stock markets of the year, which helps explain the lousy perfor-mance of the WisdomTree Japan Hedged Financials Fund (DXJF|D-64), down 23.1% on the year.

Frustration that years of “Abenomics” and unprecedented monetary stimulus haven’t given the country’s economy the boost that was expected is partially why investors have been selling Japanese stocks.

Negative interest rates in particular are seen as hurting Japanese financial firms, while the strength in the yen (which hurts Japanese exporters) is another reason for the underper-formance in Japanese equities more broadly.

The worst among them is the iPath Bloomberg Natural Gas Subindex Total Return ETN (GAZ|F-65), with a loss of 45.8% year-to-date.

GAZ is a prime example of a broken product. Back in 2009, the issuer—Barclays—suspended issuances of the exchange-traded note, throwing a wrench into the process that normally keeps ETNs close to their net asset value.

In turn, GAZ would go on to often trade at sizable premiums to its NAV, with no rhyme or reason to its fluctuations. The ETN still holds some correlation to natural gas prices—which are down this year—but it’s a product most investors should stay away from.

For comparison, the United States Natural Gas Fund (UNG|B-94)—which also tracks natural gas but continues to function normally—is down only 20.5% this year.

TOP 10 ETFs THROUGH MAY 31, 2016

TICKER FUND RETURN (%)

SILJ PureFunds ISE Junior Silver (Small Cap Miners/Explorers) ETF 130.97GLDX Global X Gold Explorers ETF 87.40SLVP iShares MSCI Global Silver Miners ETF 82.74SIL Global X Silver Miners ETF 79.25

GDXJ VanEck Vectors Junior Gold Miners ETF 75.95RING iShares MSCI Global Gold Miners ETF 75.91SGDJ Sprott Junior Gold Miners ETF 71.24GDX VanEck Vectors Gold Miners ETF 64.58

PSAU PowerShares Global Gold & Precious Metals Portfolio 64.26SGDM Sprott Gold Miners ETF 64.02

BOTTOM 10 ETFs THROUGH MAY 31, 2016

TICKER FUND RETURN (%)

GAZ iPath Bloomberg Natural Gas Subindex Total Return ETN -45.82VXUP AccuShares Spot CBOE VIX Up Shares -34.08GRN iPath Global Carbon ETN -33.30VIXY ProShares VIX Short-Term Futures ETF -32.63VXX iPath S&P 500 VIX Short-Term Futures ETN -32.49VIIX VelocityShares Daily Long VIX Short-Term ETN -32.31TAN Guggenheim Solar ETF -28.17BBC BioShares Biotechnology Clinical Trials Fund -27.92KWT VanEck Vectors Solar Energy ETF -25.07DXJF WisdomTree Japan Hedged Financials Fund -23.07

ROLLER-COASTER RIDE FOR VIX ETFs

At No. 3 on the worst-performers list is the iPath Global Carbon ETN (GRN|F)—a tiny ETN that tracks the carbon market—with a 33.3% loss.

Also on the list are four volatility products—including the largest and most liquid, the iPath S&P 500 VIX Short-Term Futures ETN (VXX|B-47)—with losses of up to 34% for 2016 so far.

Volatility spiked dramatically earlier this year as the stock market plunged, but it’s since come back down. At one point in

Source: ETF.com as of 5/31/2016

Source: ETF.com as of 5/31/2016

12

ADVERTISEMENT

SMALL CAPS WITH

GRITJANUS SMART GROWTH™ ETFs

Exposure to small and mid-cap growth has been a valuable source of investor return, but not without the risks that can surround some young, growing companies. Drawing on a legacy of equity investing experience, our systematic strategy identifi es resilient companies poised for long-run, sustainable growth while avoiding those companies on a riskier path.

We call our approach Smart Growth.™

Learn more at Janus.com/SmartGrowthETFs.

Please consider the charges, risks, expenses, and investment objectives carefully before investing. For a prospectus containing this and other information, please call 877.33JANUS (52687) or download the fi le from janus.com/ETFs. Read it carefully before you invest or send money. Past performance is no guarantee of future results.

OBJECTIVES: JSMD and JSML seek investment results that correspond generally, before fees and expenses, to the performance of their underlying indices, the Janus Small/Mid Cap Growth Alpha and Janus Small Cap Growth Alpha Indices, respectively. They pursue their investment objectives by using a passive index-based approach, normally investing at least 80% of its net assets in securities that comprise their underlying indices.

There are risks involved with investing, including possible loss of principal. Performance depends upon the underlying index in which it invests. Smaller capitalization companies may be less stable and more susceptible to adverse developments, and their securities may be more volatile and less liquid than larger capitalization companies.

Performance for very short time periods may not be indicative of future performance. JSMD and JSML are new ETFs and have less than one year of operating history.

ETF shares are not individually redeemable and owners of the shares may acquire those shares from the Fund and tender those shares for redemption to the Fund in Creation Units only, typically consisting of aggregations of 50,000 shares.

Ordinary brokerage commissions apply and will reduce returns.

Janus Capital Management LLC is the investment adviser and ALPS Distributors, Inc. is the distributor. ALPS is not affi liated with Janus or Janus Index & Calculation Services LLC.

Janus is a registered trademark of Janus International Holding LLC. ©Janus International Holding LLC. Janus Distributors LLC.

C-0216-106972 05-30-17

JNS112

32346 Janus GRIT Print Ad_ETFReport_APR16.indd 1 3/1/16 9:45 AM

The high-fee business model of hedge funds is under pressure, but the use of alternative invest-ment processes remains a valuable opportunity for diversifying portfolios. It is increasingly pos-sible to explain the returns to hedge fund styles using simple, well-known strategies and to explain why such strategies (or “premia”) should have positive expected returns. These systematic return drivers explain a large portion of the common risk of hedge fund managers of a given type and have hence been termed “alternative beta” or “hedge fund beta.”

We define alternative beta premia as factors with positive expected return and uncorrelated to traditional beta market risks. Their compensation can be explained using arguments based on behav-ioral biases, market anomalies and systematic deviations from equilibrium, or rational risk preferences. Remarkably, the majority of these factors are liquid in nature and thus can be delivered with trans-parency and low cost without the need for the illiquidity of assets typical in the hedge fund industry.

Ultimately, the growing knowledge around the concept of alternative beta must lead to the reclassification of a significant portion of what is today considered “alpha.” Furthermore,

The Democratization Of Hedge Funds ALTERNATIVE BETA: ACCESSING HEDGE FUND RETURNS

IN A LIQUID, LOW-COST AND TRANSPARENT MANNER

Yazann RomahiPortfolio Manager & Global Head of Quantitative Strategies & Research, Multi-Asset Solutions, J.P. Morgan Asset Management

Joe StainesQuantitative Researcher, Muti-Asset Solutions, J.P. Morgan Asset Management

Source: J.P. Morgan Asset Management

Figure 1

SP

ON

SO

RE

D C

ON

TE

NT

investors’ increased understanding of the factor risk exposures associated with different hedge fund styles will help in the pur-suit of better diversified portfolios with greater transparency.

Redefining Alpha & BetaConventionally, alpha is understood to be the excess return due to active management, while beta is thought to be the return due to the market. However, portfolio theory allows for any number of risk factors. Beta is in fact best defined as the portion of returns that can be attributed to one or more sys-tematic exposures to an economic premium. Alpha is then the portion of returns that cannot be explained by these system-atic exposures.

Since the 1970s, common risk factors have been acknowl-edged in traditional investments such as stocks and bonds. Prior to this, what seemed obvious to market participants was that one needed to know which stocks to buy. The idea that there was a risk premium attached to simply being exposed to the markets was alien to market participants. Yet today we take that concept entirely for granted. Increasingly, the same is happening to hedge funds. This evolution in the under-standing of alternative investment returns has the potential to change the industry on two fronts: firstly, by providing a benchmark for hedge fund managers; and secondly, by allow-ing direct investment in the alternative premia. This strategy of investment in premia provides a low-cost, transparent and liquid way to diversify portfolios.

Explaining & Reproducing Hedge Fund ReturnsBecause the average hedge fund contains market risk, first-gen-eration “hedge fund replication” strategies focused on replicating hedge fund index returns using a mix of traditional asset classes. Now that we know that hedge funds are exposed to long/short risk premia, it is clear why this early approach was doomed to fall short. It does, however, highlight how hedge fund return streams can be more accurately replicated by constructing hedge fund strategies from the bottom up. In other words, by investing in the same individual securities that the hedge fund manager would invest in, one is able to much better capture the true premium.

These systematic exposures have come to be known as “alternative beta.” Alternative beta and average hedge fund returns are analogous to equity beta and average equity man-ager returns. Below we show, for three popular hedge fund styles, how the average performance of the styles can be attrib-uted to systematic exposures to known premia and how a strat-egy combining those premia can make an attractive investment.

Equity Long/Short Alternative risk premia relating to equity long/short and equity-market-neutral hedge funds are very closely tied to the history of the development of the concept of beta itself. When equity beta was first introduced, some managers continued to outperform the traditional indexes simply by giving a value or size bias. When Fama and French articulated the idea of

risk premia compensating these types of exposures, the bar was raised on active managers. The perhaps-surprising result in the equity hedge fund world is that what we previously assumed was alpha is in fact a long/short variant of what we previously were already familiar with in the traditional world.

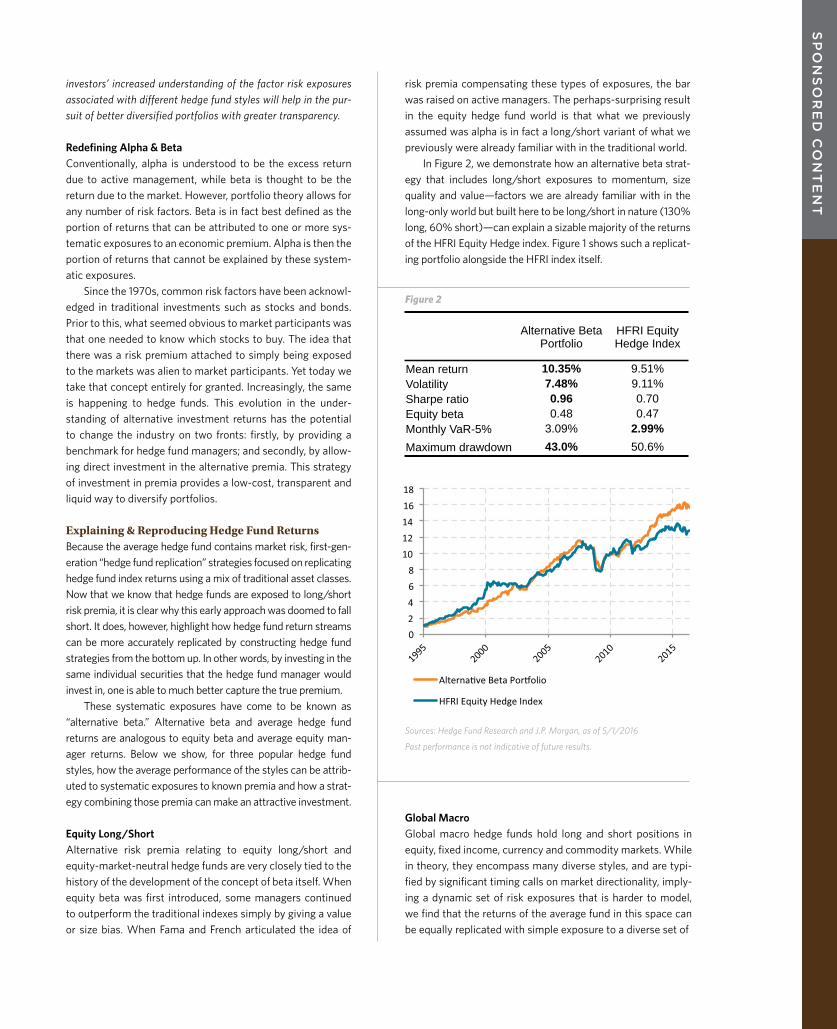

In Figure 2, we demonstrate how an alternative beta strat-egy that includes long/short exposures to momentum, size quality and value—factors we are already familiar with in the long-only world but built here to be long/short in nature (130% long, 60% short)—can explain a sizable majority of the returns of the HFRI Equity Hedge index. Figure 1 shows such a replicat-ing portfolio alongside the HFRI index itself.

Figure 2

SP

ON

SO

RE

D C

ON

TE

NT

Alternative Beta Portfolio

HFRI Equity Hedge Index

Mean return 10.35% 9.51% Volatility 7.48% 9.11% Sharpe ratio 0.96 0.70 Equity beta 0.48 0.47 Monthly VaR-5% 3.09% 2.99% Maximum drawdown 43.0% 50.6%

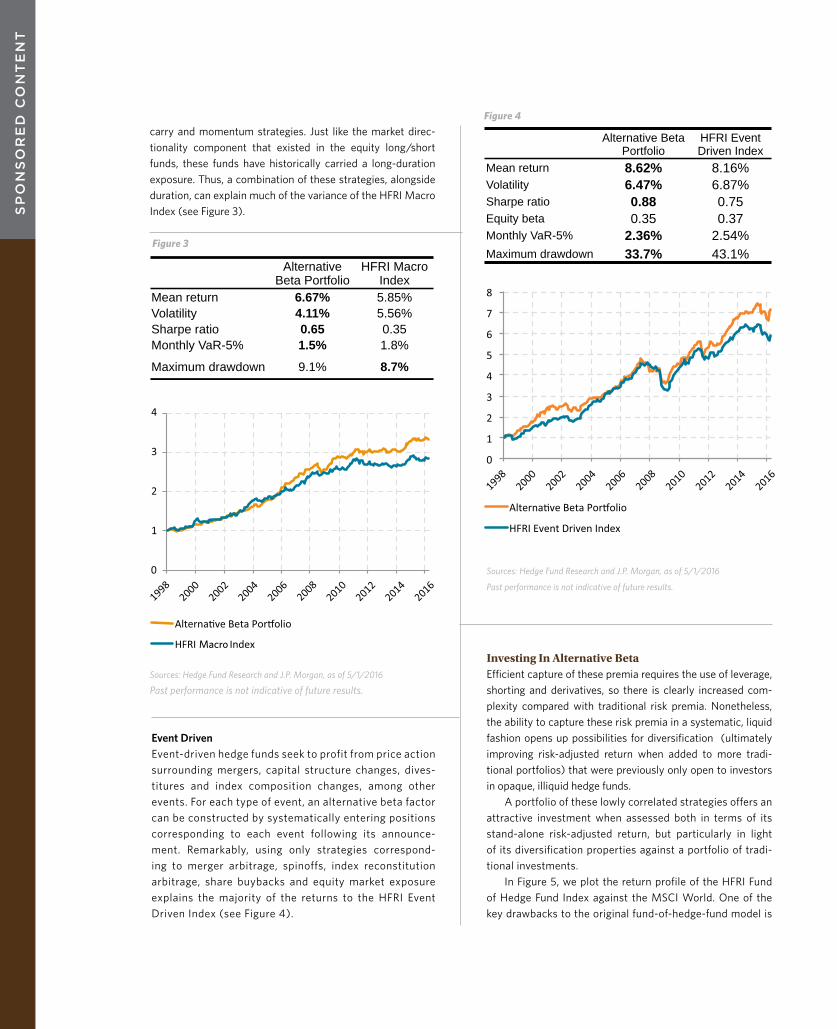

Global MacroGlobal macro hedge funds hold long and short positions in equity, fixed income, currency and commodity markets. While in theory, they encompass many diverse styles, and are typi-fied by significant timing calls on market directionality, imply-ing a dynamic set of risk exposures that is harder to model, we find that the returns of the average fund in this space can be equally replicated with simple exposure to a diverse set of

Sources: Hedge Fund Research and J.P. Morgan, as of 5/1/2016

Past performance is not indicative of future results.

carry and momentum strategies. Just like the market direc-tionality component that existed in the equity long/short funds, these funds have historically carried a long-duration exposure. Thus, a combination of these strategies, alongside duration, can explain much of the variance of the HFRI Macro Index (see Figure 3).S

PO

NS

OR

ED

CO

NT

EN

T

Investing In Alternative BetaEfficient capture of these premia requires the use of leverage, shorting and derivatives, so there is clearly increased com-plexity compared with traditional risk premia. Nonetheless, the ability to capture these risk premia in a systematic, liquid fashion opens up possibilities for diversification (ultimately improving risk-adjusted return when added to more tradi-tional portfolios) that were previously only open to investors in opaque, illiquid hedge funds.

A portfolio of these lowly correlated strategies offers an attractive investment when assessed both in terms of its stand-alone risk-adjusted return, but particularly in light of its diversification properties against a portfolio of tradi-tional investments.

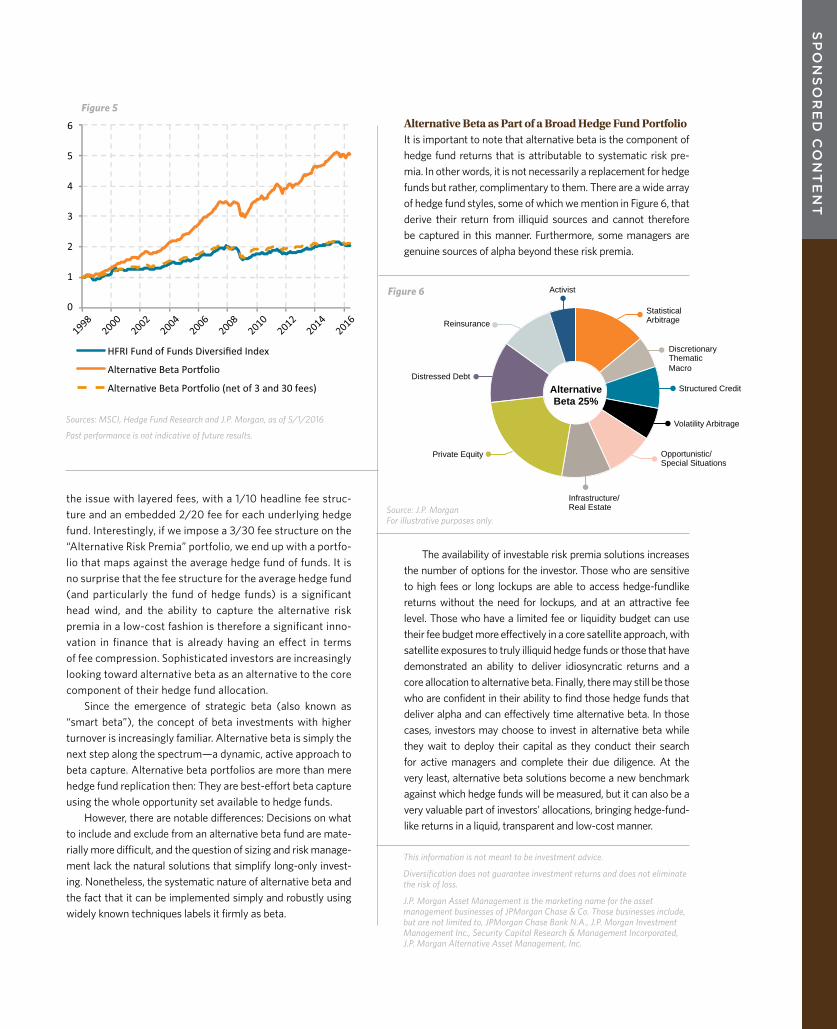

In Figure 5, we plot the return profile of the HFRI Fund of Hedge Fund Index against the MSCI World. One of the key drawbacks to the original fund-of-hedge-fund model is

Alternative Beta Portfolio

HFRI Macro Index

Mean return 6.67% 5.85% Volatility 4.11% 5.56% Sharpe ratio 0.65 0.35 Monthly VaR-5% 1.5% 1.8%

Maximum drawdown 9.1% 8.7%

Alternative Beta Portfolio

HFRI Event Driven Index

Mean return 8.62% 8.16% Volatility 6.47% 6.87% Sharpe ratio 0.88 0.75 Equity beta 0.35 0.37 Monthly VaR-5% 2.36% 2.54% Maximum drawdown 33.7% 43.1%

Event DrivenEvent-driven hedge funds seek to profit from price action surrounding mergers, capital structure changes, dives-titures and index composition changes, among other events. For each type of event, an alternative beta factor can be constructed by systematically entering positions corresponding to each event following its announce-ment. Remarkably, using only strategies correspond-ing to merger arbitrage, spinoffs, index reconstitution arbitrage, share buybacks and equity market exposure explains the majority of the returns to the HFRI Event Driven Index (see Figure 4).

Sources: Hedge Fund Research and J.P. Morgan, as of 5/1/2016

Past performance is not indicative of future results.

Sources: Hedge Fund Research and J.P. Morgan, as of 5/1/2016

Past performance is not indicative of future results.

Figure 3

Figure 4

Private Equity

Structured Credit Alternative Beta 25%

Statistical Arbitrage

Discretionary Thematic Macro

Opportunistic/Special Situations

Infrastructure/ Real Estate

Distressed Debt

Reinsurance

Activist

Volatility Arbitrage

This information is not meant to be investment advice.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

J.P. Morgan Asset Management is the marketing name for the asset management businesses of JPMorgan Chase & Co. Those businesses include, but are not limited to, JPMorgan Chase Bank N.A., J.P. Morgan Investment Management Inc., Security Capital Research & Management Incorporated, J.P. Morgan Alternative Asset Management, Inc.

SP

ON

SO

RE

D C

ON

TE

NT

the issue with layered fees, with a 1/10 headline fee struc-ture and an embedded 2/20 fee for each underlying hedge fund. Interestingly, if we impose a 3/30 fee structure on the “Alternative Risk Premia” portfolio, we end up with a portfo-lio that maps against the average hedge fund of funds. It is no surprise that the fee structure for the average hedge fund (and particularly the fund of hedge funds) is a significant head wind, and the ability to capture the alternative risk premia in a low-cost fashion is therefore a significant inno-vation in finance that is already having an effect in terms of fee compression. Sophisticated investors are increasingly looking toward alternative beta as an alternative to the core component of their hedge fund allocation.

Since the emergence of strategic beta (also known as “smart beta”), the concept of beta investments with higher turnover is increasingly familiar. Alternative beta is simply the next step along the spectrum—a dynamic, active approach to beta capture. Alternative beta portfolios are more than mere hedge fund replication then: They are best-effort beta capture using the whole opportunity set available to hedge funds.

However, there are notable differences: Decisions on what to include and exclude from an alternative beta fund are mate-rially more difficult, and the question of sizing and risk manage-ment lack the natural solutions that simplify long-only invest-ing. Nonetheless, the systematic nature of alternative beta and the fact that it can be implemented simply and robustly using widely known techniques labels it firmly as beta.

Alternative Beta as Part of a Broad Hedge Fund PortfolioIt is important to note that alternative beta is the component of hedge fund returns that is attributable to systematic risk pre-mia. In other words, it is not necessarily a replacement for hedge funds but rather, complimentary to them. There are a wide array of hedge fund styles, some of which we mention in Figure 6, that derive their return from illiquid sources and cannot therefore be captured in this manner. Furthermore, some managers are genuine sources of alpha beyond these risk premia.

Sources: MSCI, Hedge Fund Research and J.P. Morgan, as of 5/1/2016

Past performance is not indicative of future results.

Source: J.P. MorganFor illustrative purposes only.

The availability of investable risk premia solutions increases the number of options for the investor. Those who are sensitive to high fees or long lockups are able to access hedge-fundlike returns without the need for lockups, and at an attractive fee level. Those who have a limited fee or liquidity budget can use their fee budget more effectively in a core satellite approach, with satellite exposures to truly illiquid hedge funds or those that have demonstrated an ability to deliver idiosyncratic returns and a core allocation to alternative beta. Finally, there may still be those who are confident in their ability to find those hedge funds that deliver alpha and can effectively time alternative beta. In those cases, investors may choose to invest in alternative beta while they wait to deploy their capital as they conduct their search for active managers and complete their due diligence. At the very least, alternative beta solutions become a new benchmark against which hedge funds will be measured, but it can also be a very valuable part of investors’ allocations, bringing hedge-fund-like returns in a liquid, transparent and low-cost manner.

Figure 5

Figure 6

ing on low-volatility names. As InsideETFs CEO Matt Hougan wrote on ETF.com, “The beauty of USMV is that, by lowering the overall volatility of the portfolio, it should help investors ride out short-term volatility and therefore hold their positions for the long haul.”

In a way, demand for USMV speaks to investors’ desire to stay invested even when the market isn’t making it easy to do so in the short run.

When it came to equity expo-sure, large-cap equity ETFs weren’t all that popular in the first five months of the year. Developed-mar-ket equities, by and large, weren’t either. International equities—including emerging market stocks—were even less hot. As an asset class, foreign stock funds lost more than $14.6 billion in assets—the biggest net redemptions of any asset class tracked by FactSet in the period.

PLENTY HAS BEEN SAID ABOUT THE DANGERS OF READING TOO MUCH INTO ETF ASSET FLOWS. And yet there’s really no other way to slice it: ETF investors are playing it safe—defensively, even—in 2016.

Perhaps it’s because the equity market hasn’t done all that much. The S&P 500 rallied only some 3% in five months amid highly volatile, choppy action. In that period, U.S. equity ETFs gathered a paltry $3.9 bil-lion in fresh net inflows, a muted demand that largely centered on funds focused on things like dividends and value stocks—the more defensive-type fare within equity plays.

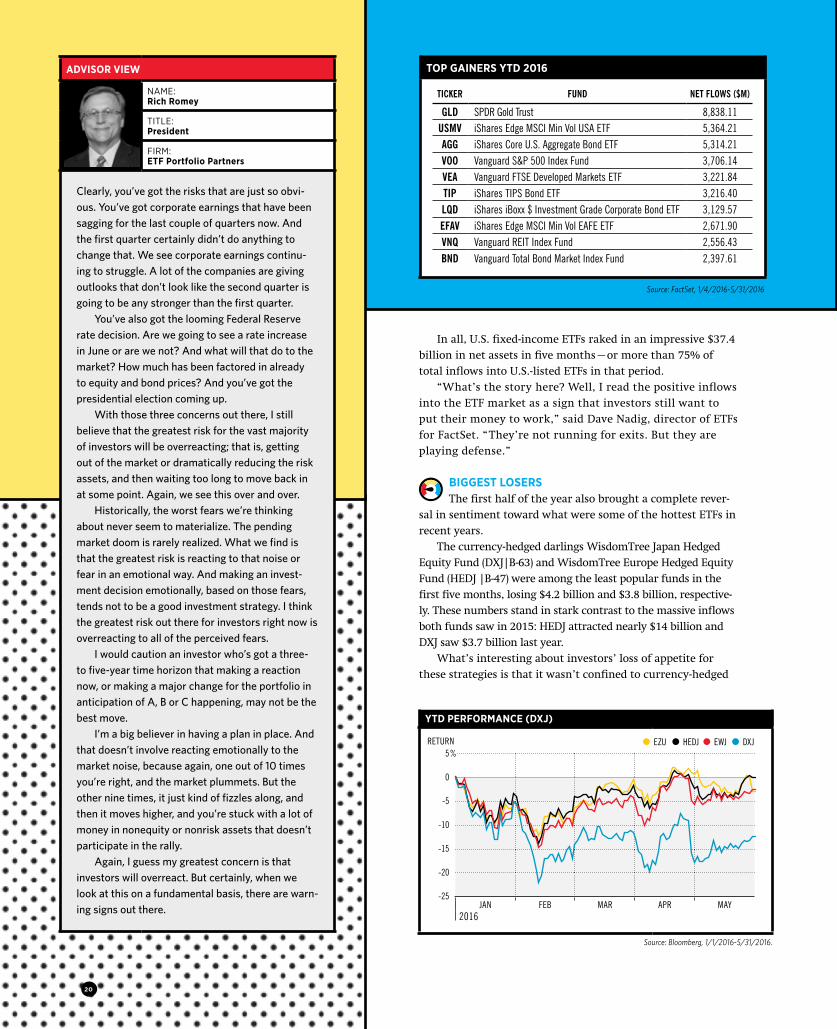

The most popular equity ETF so far this year, in fact, is the iShares Edge MSCI Min Vol USA ETF (USMV|A-69), attracting more than $5.3 billion in five months, accord-ing to FactSet data. USMV is only No. 2 in terms of assets gathered (within the entire 1,900-plus fund universe in 2016) to an even more risk-off play: the SPDR Gold Trust (GLD|A-100), which raked in more than $8.8 billion in net inflows in the January-to-May period.

‘THE BEAUTY OF USMV’USMV is a low-volatility strategy that looks to

capture as much upside in the equity as possible while protecting investors from downside action by focus-

RISK-OFF ETFs

ATTRACTING ASSETS

By Cinthia Murphy

MIDYEAR REPORT

18

But through it all, USMV reigned supreme, holding on to the No. 2 spot, with positive net creations month after month, growing to become a $13.25 billion ETF.

‘AGED AND OVERVALUED BULL MARKET’“The cyclical bull market is aged and

overvalued,” Steve Blumenthal, chairman and chief executive officer of CMG Capital Management, said of the risk aversion among investors. He noted that of the 36 cyclical bull market moves since 1900, the current cyclical bull is already the third-longest bull-run.

“The flows tell me that money is growing cautious. And it should,” Blumenthal said. “My personal view is that there’s a growing loss of confidence in central bank policy.”

Nothing suggests caution like a stampede into gold. GLD has been the most popular ETF so far this year, with $8.8 billion in inflows. And as investors rushed in, the fund didn’t disappoint, rallying more than 14% in five months.

Also hugely popular were broad, investment-grade fixed-income strategies such as the iShares Core U.S. Aggregate Bond ETF (AGG|A-98), the iShares TIPS Bond ETF (TIP|A-99) and the Van-guard Total Bond Market Index Fund (BND|A-94), or funds investing in Treasurys and TIPS.

ADVISOR VIEW

NAME: Tom Rampulla

TITLE: Head of U.S. Financial Intermediaries

FIRM: Vanguard

If I’m an advisor, I’m trying to just filter out the noise, and focus on the long-term needs of the client. An advisor’s biggest source of alpha, frankly, is discipline. You work with a client, you get goals and objectives put in place, and you agree on those. And then you put a plan in place. You make sure you minimize the costs.

Finally, it’s about discipline, and that’s working with your client to fil-ter out the noise, maintain discipline, rebalance the portfolio to your target asset allocation. And that’s where you’re going to add the most value.

I guess my biggest conversation with clients is: Don’t worry about “Brexit.” Look for the long term. If anything has changed in your par-ticular instance, then we might want to think about doing something. But filter out the noise. It’s so easy to get distracted by what’s happening in the news on a daily basis. Chasing markets and trying to time—we’ve done lots of research on that—are tough things to do.

If a client comes in the office saying, “I want to go to cash because of a potential Brexit,” you talk him out of that. If they come to you and say, “Hey, my wife’s pregnant with triplets,” then you’ve got to think that there are some things you might want to do from a financial planning perspective because of that. But don’t get distracted by what China’s doing this week.

So I say, focus on the big picture, long term, when it comes to asset allocation and your discipline. But of course, if the client’s situation changes, you’ll need to incorporate that into the advice you give them.

THE BIG QUESTION: What should advisors

be concerned about going into the second half of

the year?

GLD YTD PERFORMANCE

JAN FEB MAR APR MAY2016

Source: Bloomberg, 1/1/2016-5/31/2016

25

20

15

10

5

0

-5

-10

-15

% RETURN GLD USMV AGG SPY

19

YTD PERFORMANCE (DXJ)

JAN FEB MAR APR MAY2016

Source: Bloomberg, 1/1/2016-5/31/2016.

5

0

-5

-10

-15

-20

-25

% RETURN EZU HEDJ EWJ DXJ

In all, U.S. fixed-income ETFs raked in an impressive $37.4 billion in net assets in five months—or more than 75% of total inflows into U.S.-listed ETFs in that period.

“What’s the story here? Well, I read the positive inflows into the ETF market as a sign that investors still want to put their money to work,” said Dave Nadig, director of ETFs for FactSet. “They’re not running for exits. But they are playing defense.”

BIGGEST LOSERSThe first half of the year also brought a complete rever-

sal in sentiment toward what were some of the hottest ETFs in recent years.

The currency-hedged darlings WisdomTree Japan Hedged Equity Fund (DXJ|B-63) and WisdomTree Europe Hedged Equity Fund (HEDJ |B-47) were among the least popular funds in the first five months, losing $4.2 billion and $3.8 billion, respective-ly. These numbers stand in stark contrast to the massive inflows both funds saw in 2015: HEDJ attracted nearly $14 billion and DXJ saw $3.7 billion last year.

What’s interesting about investors’ loss of appetite for these strategies is that it wasn’t confined to currency-hedged

ADVISOR VIEW

NAME: Rich Romey

TITLE: President

FIRM: ETF Portfolio Partners

Clearly, you’ve got the risks that are just so obvi-ous. You’ve got corporate earnings that have been sagging for the last couple of quarters now. And the first quarter certainly didn’t do anything to change that. We see corporate earnings continu-ing to struggle. A lot of the companies are giving outlooks that don’t look like the second quarter is going to be any stronger than the first quarter.

You’ve also got the looming Federal Reserve rate decision. Are we going to see a rate increase in June or are we not? And what will that do to the market? How much has been factored in already to equity and bond prices? And you’ve got the presidential election coming up.

With those three concerns out there, I still believe that the greatest risk for the vast majority of investors will be overreacting; that is, getting out of the market or dramatically reducing the risk assets, and then waiting too long to move back in at some point. Again, we see this over and over.

Historically, the worst fears we’re thinking about never seem to materialize. The pending market doom is rarely realized. What we find is that the greatest risk is reacting to that noise or fear in an emotional way. And making an invest-ment decision emotionally, based on those fears, tends not to be a good investment strategy. I think the greatest risk out there for investors right now is overreacting to all of the perceived fears.

I would caution an investor who’s got a three- to five-year time horizon that making a reaction now, or making a major change for the portfolio in anticipation of A, B or C happening, may not be the best move.

I’m a big believer in having a plan in place. And that doesn’t involve reacting emotionally to the market noise, because again, one out of 10 times you’re right, and the market plummets. But the other nine times, it just kind of fizzles along, and then it moves higher, and you’re stuck with a lot of money in nonequity or nonrisk assets that doesn’t participate in the rally.

Again, I guess my greatest concern is that investors will overreact. But certainly, when we look at this on a fundamental basis, there are warn-ing signs out there.

TOP GAINERS YTD 2016

TICKER FUND NET FLOWS ($M)

GLD SPDR Gold Trust 8,838.11USMV iShares Edge MSCI Min Vol USA ETF 5,364.21AGG iShares Core U.S. Aggregate Bond ETF 5,314.21VOO Vanguard S&P 500 Index Fund 3,706.14VEA Vanguard FTSE Developed Markets ETF 3,221.84TIP iShares TIPS Bond ETF 3,216.40LQD iShares iBoxx $ Investment Grade Corporate Bond ETF 3,129.57EFAV iShares Edge MSCI Min Vol EAFE ETF 2,671.90VNQ Vanguard REIT Index Fund 2,556.43BND Vanguard Total Bond Market Index Fund 2,397.61

Source: FactSet, 1/4/2016-5/31/2016

20

ADVISOR VIEW

NAME: Aaron Izenstark

TITLE: Chief Investment Officer & Managing Partner

FIRM: Iron Financial

Our biggest concern right now is really the outlook for the macro space. We have a macro model that has turned down for the first time since 2011, thanks to a lot of GDP-type data for both the U.S. and international markets that aren’t looking that good.

For instance, large-cap earnings in the U.S. came out down 6-7% in the first quarter alone. That’s pretty big. You don’t see that very often, and we seem to be getting a lot of this type of news lately. That tends to cause pressure on equity prices, and it gets investors concerned, which ends up exacerbating market moves.

The yield curve, too, is at its flattest point since 2007-08. That doesn’t necessarily mean there’s a recession coming, but you don’t see that happening very often. The short end of the yield curve has been rising, and 10-year Treasury yields are stuck around 1.8%—the spread is narrowing, and that makes it more difficult for banks and financial institutions to make money. It’s the little things like that across the landscape that aren’t looking all that great.

One of the bigger-picture items we look at is oil prices, and the energy sector. What’s interesting about energy is that if it gets devastated—unlike the tech bust in the early 2000s—it actually helps other sectors, because energy prices go down. But there are still ripples associated with that type of move, even if they’re more focused on the periph-eral companies within the energy market and on default rates in high-yield bonds, for instance. So it’s a positive to see energy recovering.

But generally speaking, our biggest concern is how the global macro environment is shaping up, especially given that the Fed has a $4.5 trillion balance sheet. That’s kept interest rates—particu-larly in the five- to 10-year range—low, which has helped keep the yield curve flat. Markets are still being medicated by the Fed.

We are investing relatively defensively for now, and we’re doing that not by staying away from assets necessarily, but by doing more hedging—through things like total return swaps and futures contracts—to try to mitigate some of that risk.

ETFs. Their unhedged counterparts, the iShares MSCI Japan ETF (EWJ|B-95) and the iShares MSCI Eurozone ETF (EZU |A-84) were equally unpopular, facing net redemptions of $3.7 billion and $3.5 billion, respectively, in the same period. No one seemed to want exposure to Japan or to the eurozone, currency-hedged or not.

The outflows came as all four ETFs delivered negative performances to start the year.

These strategies, along with U.S. large-cap equity, tech stocks, China and even junk bonds, “are all classically ‘risk on’ positions, which are all clearly very much in ‘risk off’ mode,” Nadig said.

THE CURVEBALLDefense may be the best offense for most investors

this year, but that doesn’t mean everyone’s following this playbook. In fact, leveraged and inverse products have been relatively strong in the asset-gathering game.

Inverse ETFs have been particularly hot, attracting $5.7 billion in fresh net assets since Jan. 1. The ProShares Ultra-Short S&P500 (SDS)—serving up inverse exposure to the S&P 500—led the charge, with net creations of $1.0 billion in five months. That’s sizable considering the fund has total assets of $2.1 billion.

The Direxion Daily Gold Miners Bear 3x Shares (DUST), too, attracted some $774 million in the same period. Most of these

BIGGEST OUTFLOWS YTD 2016

TICKER FUND NET FLOWS ($M)

QQQ PowerShares QQQ Trust -4,879.44DXJ WisdomTree Japan Hedged Equity Fund -4,243.42

HEDJ WisdomTree Europe Hedged Equity Fund -3,809.92EWJ iShares MSCI Japan ETF -3,776.30EZU iShares MSCI Eurozone ETF -3,574.65SPY SPDR S&P 500 ETF Trust -3,520.51IWF iShares Russell 1000 Growth ETF -2,433.55XLF Financial Select Sector SPDR Fund -2,025.32FXH First Trust Health Care AlphaDEX Fund -2,012.82FBT First Trust NYSE Arca Biotechnology Index Fund -1,789.47

inflows aren’t sticky assets, as in long-term investment dollars; rather, they represent short-term, often single-day positions as these funds are designed to be. However, they still point to investor demand for ways to express their market views.

“We’ve seen strong flows into leveraged and inverse products,” said Nadig. “Because anytime the market goes into defense mode, like clockwork, speculators come out of the woodwork to try and prove it wrong.”

Source: FactSet, 1/4/2016-5/31/2016

21

The search for the best way to represent or gain exposure to the “market” had, until recently, experienced two major milestones:

• The first came in 1896, when Charles Dow created the original price-weighted stock index. For decades, it served as the accepted concept of the market until stock splits and corporate actions exposed the limitation of Dow’s methodology.

• The second came more than a half century later, in 1957, when Standard & Poor’s unveiled the S&P 500 Index, a market capitalization index that was broader in scope and more adaptable to corporate action.

Much has changed since 1957, yet the popularity of Standard & Poor’s mar-ket-capitalization-weighting methodology perseveres. An entire industry has been built on the concept that the S&P 500 Index provides the best rep-resentation of the U.S. equity market, and more than $2 trillion is currently invested in market-cap-weighted strategies.1 The confidence in market-cap weighting has endured even though there is not any research proving that it is the most ideal way to gain exposure to the equity market or the factors that drive equity performance. In fact, it’s been quite the contrary, as mar-ket-cap weighted indices have proven to expose investors to unintended concentrations of risk, often at inopportune times.

While investors were increasingly allocating more dollars to market-cap- weighted strategies, by the late 1990s teams of academics began uncov-ering a number of factors beyond broad market exposure—such as value, size, momentum and low volatility—that the historical evidence demonstrat-ed were even more significant and persistent drivers of equity returns over decades.

At the same time, the drawbacks of market-cap-weighted indices were being laid bare. Since market-cap-weighted indices are price driven, they give the highest priced stocks the largest weightings, and the lowest priced stocks the smallest. A company’s market capitalization at any point in time is not necessarily a true measure of its economic value, but rather an indicator of the prevailing market sentiment on that stock at the time. As former U.S. Federal Reserve Chairman Alan Greenspan famously noted, sentiment can sometimes become “irrationally exuberant.” When that happens, sector exposure in a market-cap-weighted portfolio can become skewed. Within the S&P 500 Index, for example, weightings often favor booming sectors. Energy was 30% of the index in 1980, technology 30% in 1999, and financials 22% in 2006, all on the eve of crises in each of these sectors.2 That presented concentration risk and, with that level of exposure, investors in passive portfolios that mirrored the index fully participated in the subsequent busts those sectors experienced.

Smart Beta Strategies Tap Other Return Drivers

Building on the work of the academics who identified the additional key return drivers, a new category of investments has emerged, called smart beta. Each of these smart beta strategies uses a different weighting methodology, with the goal of delivering better returns and less concentration risk.

The first generation of smart beta strategies employed style tilts, by focusing on growth or value stocks. The next generation directly targeted specific factors—such as momentum or low volatility—to determine stock weights, or they used a particular fundamental of a stock—such as earnings, dividends, or revenue—to weight securities and provide favorable tilts toward several of the key return drivers.

Which Stocks? Which Weighting Strategies?

It is important to note that the primary issue with market cap indices is not with the stocks they hold, but rather with the weightings those stocks are assigned. Investors who own market-cap-weighted strategies that track a major, well-known index are not being exposed to inferior stocks. In fact, it’s generally quite the opposite. To be included in the Standard & Poor’s indices, as an example, a company must meet multiple criteria, such as having four consecutive quarters of profits. That is an entirely reasonable—and effective–measure of quality.

To build a strategy that will capture, and possibly exceed, the returns available from a broad market, while mitigating risk, it is NOT necessary to create a new index with different securities. Using the securities in an already well-established index will provide investors with broad, diversified exposure to a market.

The problem with portfolios that aim to track a market, generally arises from the scheme used to weight securities, and market cap can cause investors to be excessively exposed to overvalued stocks. The risk of such overexpo-sure becomes heightened during stock market bubbles, which in the past 35 years have occurred three times.

If market capitalization isn’t the best weighting strategy, what is? Is it one that focuses on particular factor or a fundamental-weighting methodology that could provide favorable exposure to a combination of the return drivers?

To answer that question, investors and their advisors must first identify their objectives. What are they trying to accomplish?

• The highest possible return?

• The best risk-adjusted return?

• The lowest volatility?

• The most defensive portfolio?

A New Alternative to Passive Investing: A Revenue-Based Smart Beta StrategyBy Sharon French, Head of Beta Solutions and Vince Lowry, Leader Revenue Weighted Strategy Team

SPONSORED CONTENT SPONSORED CONTENT

All are worthy goals, but selecting factor tilts or fundamental weighting schemes that focus narrowly on any of these goals could bring unintended consequences, such as less diversification or significant style or market-cap drift away from the target market or index.

The goal with any smart beta strategy is to maintain the best aspects of a market-cap portfolio—including broad diversification—while avoiding the worst, including the tendency to focus on overvalued stocks and sectors. Ideally, a smart beta strategy should also not bring a significant style or market-cap drift away from the attributes of the broad market index. It must also offer a rules-based and transparent investment strategy and satisfy the practical matters of enabling any firm that offers a smart beta product to deliver a cost-efficient and liquid investment vehicle to investors.

Revenue Weighting Offers a Combination of Compelling Potential Benefits

One fundamental strategy–revenue weighting–can satisfy many of these criteria. A revenue-based portfolio weights companies according to their trailing 12-month sales revenue, and rebalances quarterly on the basis of the latest sales results. Revenue is the purest measure of performance on a company’s income statement, and it is difficult to manipulate. The potential benefits the strategy offers include:

1. Broad market diversification. Every company in the S&P 500 Index has sales, so revenue weighting will still provide full, diversified exposure to the market.

2. Minimal style and market cap drift from the original target. The result of the revenue weight is a large-cap core/value portfolio3 with a beta to the market of only slightly higher than 1.4

3. A transparent, rules-based investment process. Weighting by revenue is a straightforward approach. To see the weighting scheme in action, consider that the total trailing 12-month revenue of the S&P 500 Index on December 31, 2015 was $10.7 trillion, and Procter & Gamble’s was $69.3 billion. That level of sales relative to the whole universe of U.S. large-cap stocks would result in P&G having a 0.65% weighting in the

revenue-based portfolio at the end of 2015 versus a 1.21% weighting in the market-cap index.5 If, in future quarters, P&G’s revenues were to increase relative to the broad market, it would get a higher weighting in the revenue-weighted portfolio. Similarly, if its relative revenues declined, it would have a lower weighting.

Revenue weighting also provides potential risk benefits and improved valuation characteristics. The quarterly rebalancing is designed to pull the portfolio away from companies with faster growing market capitalizations relative to the market and toward companies with faster growing revenues relative to the market. The result of the quarterly rebalancing is that histori-cally the revenue-weighted portfolio has lower price-to-sales ratios than the market cap index across each of the 10 GICS (Global Industry Classification Standards) sectors.

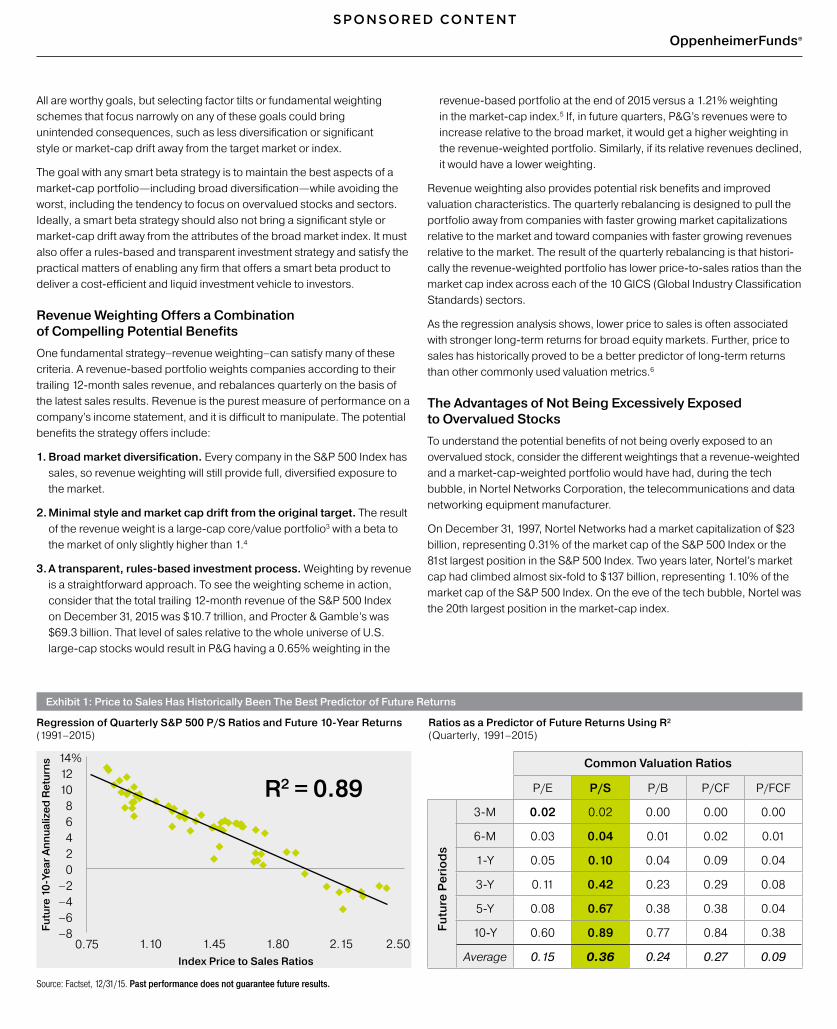

As the regression analysis shows, lower price to sales is often associated with stronger long-term returns for broad equity markets. Further, price to sales has historically proved to be a better predictor of long-term returns than other commonly used valuation metrics.6

The Advantages of Not Being Excessively Exposed to Overvalued Stocks

To understand the potential benefits of not being overly exposed to an overvalued stock, consider the different weightings that a revenue-weighted and a market-cap-weighted portfolio would have had, during the tech bubble, in Nortel Networks Corporation, the telecommunications and data networking equipment manufacturer.

On December 31, 1997, Nortel Networks had a market capitalization of $23 billion, representing 0.31% of the market cap of the S&P 500 Index or the 81st largest position in the S&P 500 Index. Two years later, Nortel’s market cap had climbed almost six-fold to $137 billion, representing 1.10% of the market cap of the S&P 500 Index. On the eve of the tech bubble, Nortel was the 20th largest position in the market-cap index.

OppenheimerFunds®

Exhibit 1: Price to Sales Has Historically Been The Best Predictor of Future Returns

Regression of Quarterly S&P 500 P/S Ratios and Future 10-Year Returns (1991–2015)

Ratios as a Predictor of Future Returns Using R² (Quarterly, 1991–2015)

Source: Factset, 12/31/15. Past performance does not guarantee future results.

Common Valuation Ratios

P/E P/S P/B P/CF P/FCF

3-M 0.02 0.02 0.00 0.00 0.00

6-M 0.03 0.04 0.01 0.02 0.01

1-Y 0.05 0.10 0.04 0.09 0.04

3-Y 0.11 0.42 0.23 0.29 0.08

5-Y 0.08 0.67 0.38 0.38 0.04

10-Y 0.60 0.89 0.77 0.84 0.38

Average 0.15 0.36 0.24 0.27 0.09

Futu

re P

erio

ds

Index Price to Sales Ratios

Futu

re 1

0-Ye

ar A

nnua

lized

Ret

urns

0.75 1.10 1.45 1.80 2.15 2.50–8–6–4–2

02468

101214%

R2 = 0.89

SPONSORED CONTENT SPONSORED CONTENT

Over that same period, Nortel’s revenues grew only slightly faster than those of the broad index. The weighting of Nortel in the revenue-based portfolio was significantly smaller than that of the market-cap index, ranging between 0.35% and 0.40% throughout the period.7

Nortel’s significant underperformance during the tech bust proved a significant drag on the performance of the S&P 500 Index, while its poor performance had much less of an impact on the revenue-weighted portfolio. Nortel is but one example of many information technology companies whose larger weightings in the market-capitalization index in the late 1990s were not justified by the companies’ fundamentals.

Revenue-Weighted Strategies Measure Well in the Factors that Drive Returns

Revenue weighting provides favorable tilts toward several of the key drivers of return. A regression analysis reveals the degree to which a hypothetical large-cap revenue-weighted strategy would have delivered on the return drivers over the past 43 years. The results are presented in pentagons, commonly known as radar or spider charts. (A plot point near the outer edge of the pentagon means a favorable tilt toward a particular attribute, a plot point closer to the center means a lower tilt.)

The S&P 500 Index “scores” in the mid-range for all of the factors that can drive returns, except for size.

Exhibit 2: Revenue vs. Market-Cap Weighting and the Drivers of Return

Sources: Ned Davis Research, CRSP, Kenneth French Data Library, 12/31/15.

The revenue-weighted approach provides more favorable tilts toward four of the five drivers of returns, as outlined below.

• Value By having sales determine the weightings, and not a consideration influenced by stocks’ prices, a revenue-based strategy will be more focused on companies with more attractive valuations, as measured by their price-to-book value.

• Size By eliminating the market-cap weighting that the index employs, a revenue-weighting strategy will own more companies with lower capitalizations than the index.