u.s. & charlotte economic outlook: what’s ahead for 2014 mark vitner, managing director &...

TRANSCRIPT

U.S. & Charlotte Economic Outlook: What’s Ahead for 2014

Mark Vitner, Managing Director & Senior EconomistJanuary 30, 2014

Economic Outlook 2

Key Macroeconomic Trends

Uncertainty

The budget deal and start of the Fed taper have removed some of the uncertainty hanging over the economy. Simmering policy debates continue to weigh on investment and hiring decisions.

Below Trend Growth

Below trend real GDP growth bolsters the case for the “new normal”. Expectations have been reset.

UnconventionalMonetary Policy

QE has boosted asset prices more than it has the economy’s underlying fundamentals.

Global Economy Recent data on the global economy are slightly

more positive but remain mixed.

Growth is Uneven Energy and technology have been notable bright

spots in this otherwise disappointing economic recovery.

Economic Outlook 3

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2000 2002 2004 2006 2008 2010 2012 2014

U.S. Real GDP Bars = CAGR Line = Yr/Yr Percent Change

GDP - CAGR: Q3 @ 4.1%

GDP - Yr/Yr Percent Change: Q3 @ 2.0%

Forecast

U.S. GDP

We see economic growth gradually regaining

momentum as the housing recovery takes hold and the

drag from fiscal belt tightening gradually wanes

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

Economic Outlook 44

Consumer

Rising stock prices have helped bolster household finances at a time when real incomes are barely growing. Personal income growth remains sluggish and gains

are heavily skewed toward lower and upper income households, reflecting transfer payments and capital gains.

Source: U.S. Department of Commerce, Conference Board and Wells Fargo Securities, LLC

Personal IncomeHousehold Wealth

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

Household AssetsTrillions of Dollars

Financial Assets: Q3 @ $63.9 Trillion

Household Real Estate Holdings: Q3 @ $19.0 Trillion

Other Tangible Assets: Q3 @ $8.0 Trillion

-10%

-5%

0%

5%

10%

15%

-10%

-5%

0%

5%

10%

15%

92 94 96 98 00 02 04 06 08 10 12 14

PI vs. PI Less Transfer Payments

PI Less Transfer Payments: Nov @ 1.2%

Year-over-Year Percent Change: Nov @ 2.3%

Client/Prospect Name

Percent change in Personal Income Q3 2012-Q3 2013

ID4.8

AR 3.5

AL3.6

ME3.0

KS4.8

SD8.6

OH3.8

WI4.4

AZ4.5

NH3.7

MT4.1

MS4.6

OK4.8

NV4.3 IL

3.5

GA3.6

FL4.1

CO4.8

CA3.4

NE3.9

MO4.0

UT5.2

NM2.9

WA4.1

IA4.6

MI4.0

LA2.1

VA2.4

TX4.9

PA3.1

IN2.2

NC3.2

MN2.8

KY3.1

VT4.2

TN3.0

OR4.1 NY

3.0

WV2.8

ND6.5

SC3.0

WY3.8

AK2.2

CT3.5

DE5.4

HI4.1

MA3.5

MD2.4

NJ3.3

RI3.3

DC3.2

U.S. = 3.6%

Greater than 4.5%

Less than 3%

4.1%–4.5%3.6%–4.0%3.0%–3.5%

Economic Outlook 66

Consumer

Sluggish income growth has weighed on consumer confidence, which has held back consumer spending. Retail sales at the lower end have also been negatively impacted by tax increases. With gasoline prices falling, some of this headwind is

now clearing.

Source: Conference Board , U.S. Department of Commerce and Wells Fargo Securities, LLC

Core Retail Sales vs. Disposable IncomeConsumer Confidence

20

40

60

80

100

120

140

160

20

40

60

80

100

120

140

160

87 89 91 93 95 97 99 01 03 05 07 09 11 13

Consumer Confidence IndexConference Board

Confidence Yr/Yr % Chg: J an @ 38.1%Confidence: J an @ 80.712-Month Moving Average: J an @ 75.1

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

96 98 00 02 04 06 08 10 12 14

Retail Sales Ex. Auto & Gas Stations vs. Disp. Income3-Month Moving Average, Year-over-Year Percent Change

Disposable Personal Income: Nov @ 2.4%

Retail Sales Ex. Motor Vehicles & Gasoline Stations: Dec @ 4.1%

Economic Outlook 77

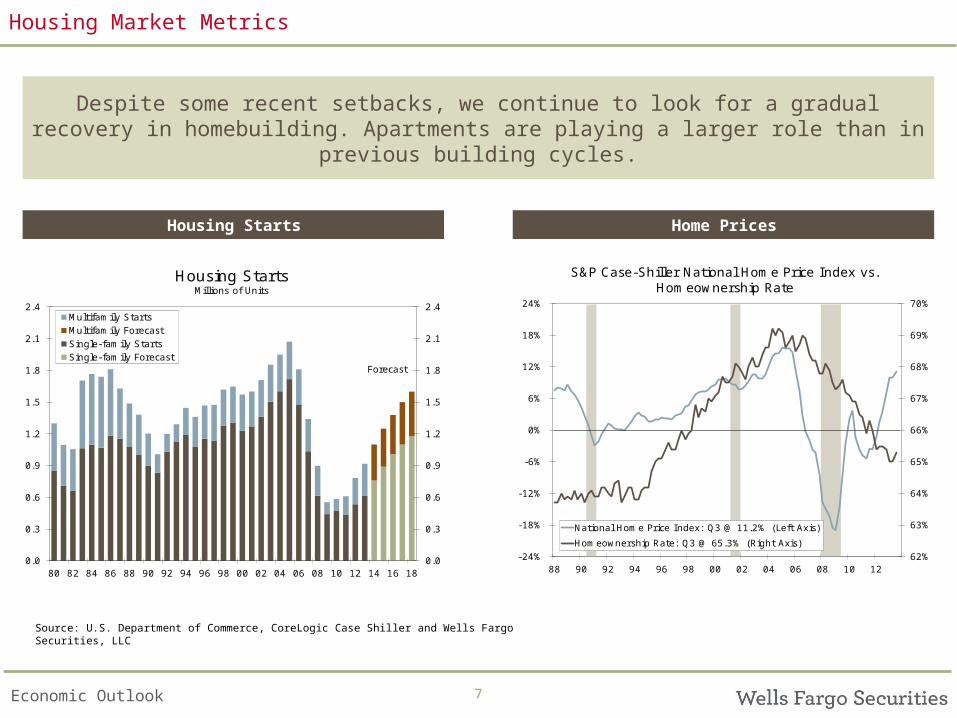

Housing Market Metrics

Despite some recent setbacks, we continue to look for a gradual recovery in homebuilding. Apartments are playing a larger role than in previous building

cycles.

Source: U.S. Department of Commerce, CoreLogic Case Shiller and Wells Fargo Securities, LLC

Home PricesHousing Starts

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

Th

ou

san

ds

Housing StartsMillions of Units

Multifamily StartsMultifamily ForecastSingle-family StartsSingle-family Forecast

Forecast

62%

63%

64%

65%

66%

67%

68%

69%

70%

-24%

-18%

-12%

-6%

0%

6%

12%

18%

24%

88 90 92 94 96 98 00 02 04 06 08 10 12

S&P Case-Shiller National Home Price Index vs. Homeownership Rate

National Home Price Index: Q3 @ 11.2% (Left Axis)

Homeownership Rate: Q3 @ 65.3% (Right Axis)

Economic Outlook 88

Small Business Confidence

With revenues growing slowly, small business owners have been reluctant to commit to significant investment in capital equipment or hire permanent workers.

Source: Gallup, Wells Fargo Bank and Wells Fargo Securities, LLC

Capital Spending GapSmall Business Confidence

-40

-20

0

20

40

60

-40

-20

0

20

40

60

04 05 06 07 08 09 10 11 12 13

Wells Fargo Small Business SurveyPresent Situation

Present Situation: Q4 @ 7

-40

-30

-20

-10

0

10

20

30

-40

-30

-20

-10

0

10

20

30

03 04 05 06 07 08 09 10 11 12 13

Capital Spending Allotment GapDifference Between "Increase" and "Decrease" Over Past 12 Mo.

Allocated Capital Spending Gap: Q4 @ -5

North Carolina & Charlotte

Economic Outlook 1010

North Carolina – Labor Market

North Carolina’s labor market is gradually improving. The unemployment rate has declined significantly over the past year.

December 2013

-4% -2% 0% 2% 4% 6% 8% 10%

Information

Other Services

Construction

Financial Activities

Leisure and Hospitality

Manufacturing

Prof. & Bus. Svcs.

Educ. & Health Services

Government

Trade, Trans. & Utilities

Total Nonfarm

North Carolina Employment Growth By IndustryYear-over-Year Percent Change, 3-MMA

Number of Employees

Less

More

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

UnemploymentEmployment

2%

4%

6%

8%

10%

12%

2%

4%

6%

8%

10%

12%

90 92 94 96 98 00 02 04 06 08 10 12 14

North Carolina vs. U.S. Unemployment RateSeasonally Adjusted

Unemployment Rate: Dec @ 6.9%United States: Dec @ 6.7%

Economic Outlook 11

North Carolina Nonfarm Employment Growth

Source: US Department of Labor and Wells Fargo Securities, LLC

Raleigh-Cary

Winston-Salem

Hickory

Fayetteville

Charlotte

Durham

Asheville

Burlington

Greensboro

Wilmington

Greenville

JacksonvilleRocky Mount

Goldsboro

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

-2% -1% 0% 1% 2% 3% 4%

3-M

onth

Annualiz

ed P

erc

ent

Change

Year-over-Year Percent Change

North Carolina Employment Growth3-Month Moving Averages, December 2013

Population

500 Thousand +

200 - 500 Thousand

100 - 200 Thousand

Recovering Expanding

Contracting Decelerating

Economic Outlook

Unemployment Rate by County

North Carolina – Unemployment Rate Composition

North Carolina Unemployment RateNovember 2013

Greater than 10.5%

Less than 7.5%

7.5% to 8.5%

9.5% to 10.5%

8.5% to 9.5%

Source: US Department of Labor and Wells Fargo Securities, LLC

Economic Outlook 1313

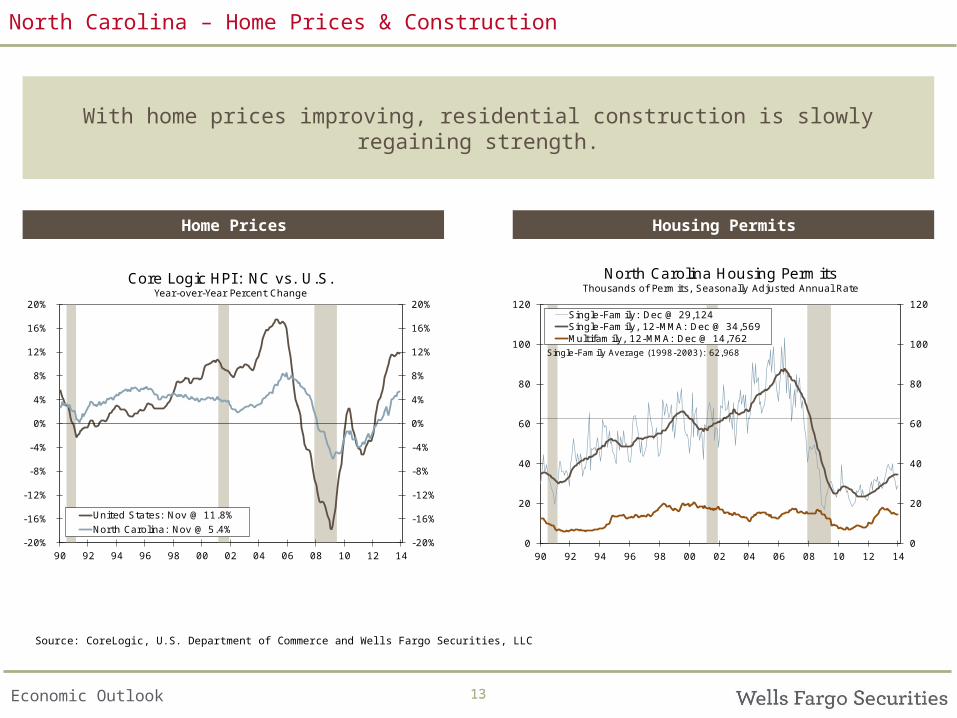

North Carolina – Home Prices & Construction

With home prices improving, residential construction is slowly regaining strength.

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

90 92 94 96 98 00 02 04 06 08 10 12 14

Core Logic HPI : NC vs. U.S.Year-over-Year Percent Change

United States: Nov @ 11.8%

North Carolina: Nov @ 5.4%

Source: CoreLogic, U.S. Department of Commerce and Wells Fargo Securities, LLC

Housing PermitsHome Prices

0

20

40

60

80

100

120

0

20

40

60

80

100

120

90 92 94 96 98 00 02 04 06 08 10 12 14

Thou

sand

s

Thou

sand

s

North Carolina Housing PermitsThousands of Permits, Seasonally Adjusted Annual Rate

Single-Family: Dec @ 29,124Single-Family, 12-MMA: Dec @ 34,569Multifamily, 12-MMA: Dec @ 14,762

Single-Family Average (1998-2003): 62,968

Economic Outlook 14

Charlotte – Labor Market

Charlotte’s labor market continues to see improvement. Employment was likely slightly understated and may be revised upward.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

91 93 95 97 99 01 03 05 07 09 11 13

Charlotte MSA Nonfarm Employment

QCEW: Yr/Yr Pct. Change: J un @ 2.8%Nonfarm: Yr/Yr Pct. Change: Dec @ 2.7%Household: Yr/Yr Pct. Change: Nov @ 1.5%

3-Month Moving Averages

Source: U.S. Department of Labor and Wells Fargo Securities, LLC

Unemployment RateEmployment

0%

2%

4%

6%

8%

10%

12%

14%

0%

2%

4%

6%

8%

10%

12%

14%

91 93 95 97 99 01 03 05 07 09 11 13

Charlotte MSA Unemployment Rate

Unemployment Rate: Nov @ 7.5%12-Month Moving Average: Nov @ 8.7%

Seasonally Adjusted

Economic Outlook 15

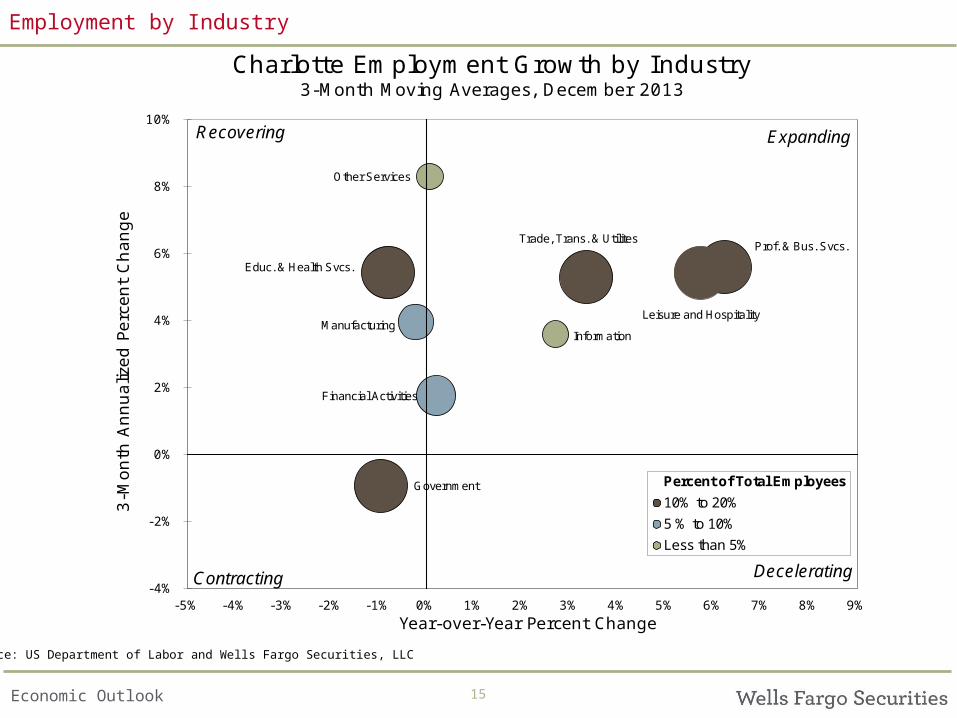

Employment by Industry

Source: US Department of Labor and Wells Fargo Securities, LLC

Government

Educ. & Health Svcs.

Other Services

Prof. & Bus. Svcs.

Leisure and Hospitality

Financial Activities

Trade, Trans. & Utilites

ManufacturingInformation

-4%

-2%

0%

2%

4%

6%

8%

10%

-5% -4% -3% -2% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

3-M

onth

Ann

ualiz

ed P

erc

ent

Change

Year-over-Year Percent Change

Charlotte Employment Growth by Industry3-Month Moving Averages, December 2013

Percent of Total Employees

10% to 20%

5 % to 10%

Less than 5%

Recovering Expanding

Contracting Decelerating

Economic Outlook 1616

Charlotte – Home Prices & Construction

Homebuilding in Charlotte has gained some momentum in the past year, and prices are rising.

40

60

80

100

120

140

160

180

200

220

40

60

80

100

120

140

160

180

200

220

90 92 94 96 98 00 02 04 06 08 10 12

Home Price Index: Charlotte MSAIndex, 2000=100, Not Seasonally Adjusted

National: Nov @ 164.3

Charlotte: Nov @ 139.1

Source: CoreLogic, U.S. Department of Commerce and Wells Fargo Securities, LLC

Housing PermitsHome Prices

0

5

10

15

20

25

30

0

5

10

15

20

25

30

90 92 94 96 98 00 02 04 06 08 10 12

Thou

sand

s

Thou

sand

s

Charlotte MSA Housing Permits

Single-Family: Dec @ 8,376Single-Family, 12-MMA: Dec @ 8,736Multifamily, 12-MMA: Dec @ 5,500

Single-Family Average (1998-2003): 14,936

Thousands of Permits, Seasonally Adjusted Annual Rate

Economic Outlook 1717

Charlotte – Market Fundamentals

Charlotte has seen relatively strong population growth. Financial activities are a major driver of the metro’s economy.

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

Charlotte MSA Population GrowthIn Thousands

Source: U.S. Department of Commerce and Wells Fargo Securities, LLC

GSPPopulation Growth

Nat. Res. & Mining< 1%

Other Svcs.2%

Construction3%

Leis. & Hosp.3%

Educ. & Health5%

Information6%

Government8%

Trade, Trans. & Utilities

12%Manufacturing

14%

Prof. & Bus. Svcs.13%

Financial Activities

34%

Charlotte MSA GSP Composition2012

Economic Outlook 1818

Charlotte – CRE

Charlotte’s apartment market has been one of the robust markets in the nation. The office market, however, has yet to gain traction in this recovery.

Source: Reis, Inc. and Wells Fargo Securities, LLC

OfficeApartment

-2.0

-1.0

0.0

1.0

2.0

3%

6%

9%

12%

15%

2006 2007 2008 2009 2010 2011 2012 2013

Charlotte Apartment Supply & DemandPercent, Thousands of Units

Apartment Completions: Q3 @ 904 Units (Right Axis)

Apartment Net Absorption: Q3 @ 738 Units (Right Axis)

Apartment Vacancy Rate: Q3 @ 4.8% (Left Axis)-1.0

-0.5

0.0

0.5

1.0

1.5

4%

8%

12%

16%

20%

24%

2006 2007 2008 2009 2010 2011 2012 2013

Charlotte Office Supply & DemandPercent, Millions of SF

Office Completions: Q3 @ 0 SF (Right Axis)

Office Net Absorption: Q3 @ -69,000 SF (Right Axis)

Office Vacancy Rate: Q3 @ 17.6% (Left Axis)

Economic Outlook 1919

Charlotte – CRE

Warehouse is seeing a decline in vacancy rates due to stronger absorption and little new construction activity. Retail remains relatively stagnant.

Source: Reis, Inc., PPR and Wells Fargo Securities, LLC

RetailWarehouse

-2,000

-1,000

0

1,000

2,000

4%

6%

8%

10%

12%

2006 2007 2008 2009 2010 2011 2012 2013

Charlotte Warehouse Supply & DemandPercent, Thousands of Units

Warehouse Net Absorption: Q3 @ 130,000 SF (Right Axis)Warehouse Completions: Q3 @ 32,000 SF (Right Axis)Warehouse Vacancy Rate: Q3 @ 7.9% (Left Axis)

-600

-400

-200

0

200

400

0%

3%

6%

9%

12%

15%

2006 2007 2008 2009 2010 2011 2012 2013

Charlotte Retail Supply & DemandPercent, Thousands of Units

Retail Completions: Q3 @ 0 SF (Right Axis)Retail Net Absorption: Q3 @ -13,000 SF (Right Axis)Retail Vacancy Rate: Q3 @ 10.0% (Left Axis)

Economic Outlook 20

China Slowdown

InvestorHome Buying

Credit Availability & Financial Reform

ManufacturingCompetitiveness

Deleveraging

Monetary/FiscalPolicy Uncertainty

Immigration ReformEnergy/Commodity

Price Swings

Issues to Watch

Economic Outlook 21

Our Forecast

Wells Fargo U.S. Economic Forecast

2011 2012 2013 2014 2015

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Real Gross Domestic Product 1 1.1 2.5 4.1 3.5 2.0 2.2 2.8 2.9 1.8 2.8 1.9 2.8 3.0

Personal Consumption 2.3 1.8 2.0 3.7 2.1 2.1 2.2 2.3 2.5 2.2 2.0 2.4 2.4

Inflation Indicators 2

PCE Deflator 1.4 1.1 1.1 0.9 1.0 1.5 1.5 2.0 2.4 1.8 1.1 1.5 2.2

Consumer Price Index 1.7 1.4 1.6 1.2 1.3 1.8 1.6 1.9 3.1 2.1 1.5 1.6 2.1

Industrial Production 1 4.1 1.2 2.3 6.2 5.2 4.3 4.4 4.5 3.4 3.6 2.6 4.4 4.7

Corporate Profits Before Taxes 2 2.1 4.5 5.7 5.0 4.1 5.4 5.5 5.6 7.9 7.0 4.3 5.2 5.9

Trade Weighted Dollar Index 3 76.2 77.5 75.2 76.4 78.0 79.0 80.0 80.5 70.9 73.5 75.9 79.4 80.6

Unemployment Rate 7.7 7.5 7.2 7.0 6.8 6.7 6.6 6.5 8.9 8.1 7.4 6.7 6.3

Housing Starts 4 0.96 0.87 0.88 0.97 0.98 1.07 1.18 1.21 0.61 0.78 0.94 1.10 1.25

Quarter- End Interest Rates 5

Federal Funds Target Rate 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.44Conventional Mortgage Rate 3.57 4.07 4.49 4.46 4.70 4.80 4.80 4.90 4.46 3.66 3.98 4.80 5.0510 Year Note 1.87 2.52 2.64 3.04 3.00 3.03 3.07 3.14 2.78 1.80 2.35 3.06 3.33

Forecast as of: J anuary 15, 20141 Compound Annual Growth Rate Quarter-over-Quarter2 Year-over-Year Percentage Change3 Federal Reserve Major Currency I ndex, 1973=100 - Quarter End4 Millions of Units5 Annual Numbers Represent Averages

2013

Actual Forecast

2014

ForecastActual

Appendix

Economic Outlook 23

Recent Special Commentary

Wells Fargo Economics Group Publications

To view any of our past research please visit:

http://www.wellsfargo.com/economics

To join any of our research distribution lists please

visit:http://www.wellsfargo.com/

economicsemail

Date Title Authors

J anuary- 10 Will The European Central Bank Ease Further? BrysonJ anuary- 07 Housing Data Wrap- Up: December 2013 Vitner, Khan & SilvermanJ anuary- 02 Singapore GDP Fell in Q4, But Underlying Trend is Solid BrysonJ anuary- 02 Argentine Economy Remains Strong in Q3 Aleman

December- 31 Colorado 2014 Economic Outlook Vitner & SilvermanDecember- 31 The Labor Market and Credit Risk Silvia,Iqbal & ZacharyDecember- 24 North Carolina's Unemployment Rate Tumbles in November VitnerDecember- 24 Texas: Frequently Asked Questions Vitner & WolfDecember- 24 Our Favorite Charts of 2013December- 20 Hotel Demand Remains Solid, but Cooling Is Expected Khan, Zachary & MillerDecember- 20 California Posts Another Big J ob Gain in November VitnerDecember- 20 Florida's J obless Rate Falls to 6.4 Percent in November Vitner & SilvermanDecember- 20 Georgia 2014 Economic Outlook Vitner & SilvermanDecember- 18 FOMC: Improving Economy, Low Inflation, Tapering to Start Silvia & HouseDecember- 18 Pennsylvania: Five Issues for 2014 Vitner & WolfDecember- 18 Office Fundamentals Show Modest Improvement Khan & ZacharyDecember- 17 Korea: Shifting Drivers of Growth Quinlan & MillerDecember- 17 Swedish Riksbank Eases Policy Again BrysonDecember- 17 Florida Economic Outlook: December 2013 Vitner & SilvermanDecember- 16 Uncharted Territory: A Completed Federal Budget? Silvia & BrownDecember- 16 Mexican Petroleum Sector Takes a Step Forward AlemanDecember- 16 Economic Growth in China Has Stabilized BrysonDecember- 11 2014 Economic OutlookDecember- 09 Minnesota Outlook: December 2013 Vitner & WolfDecember- 09 Is U.S. Growth Sensitive to Foreign Growth? Bryson, Iqbal & MillerDecember- 06 Housing Chartbook: November 2013 Vitner, Khan & SilvermanDecember- 05 California Economic Outlook: December 2013 Vitner & SilvermanDecember- 05 Brazilian Economy Weakens in Q3 AlemanDecember- 03 Reforms Affect Mexican Construction Sector AlemanDecember- 03 RBA on Hold Despite "Uncomfortably High" Aussie Dollar QuinlanDecember- 03 Prospects of Tapering and Commodity Prices AlemanDecember- 03 Swedish GDP Inched Higher in Q3- 2013 BrysonDecember- 02 Swiss GDP Growth in Q3 Not as Strong as Headline Suggests BrysonDecember- 02 Indian GDP Growth Remaind Lackluster in Q3 Bryson

November- 26 Florida Consumer Sentiment Bounces Back in November Vitner & SilvermanNovember- 25 New J ersey: Frequently Asked Questions Vitner & WolfNovember- 25 J apan's Economy & Structural Reform QuinlanNovember- 22 California Adds 39,800 J obs in October Vitner & SilvermanNovember- 22 Florida Leads the Nation in J ob Growth in October Vitner & SilvermanNovember- 22 Texas Labor Market Still Strong Vitner & Wolf

A Sampling of Our Recent Special, Regional & Industry Commentary

Economic Outlook

Wells Fargo Securities, LLC Economics Group

24

John E. Silvia … ...................... . … [email protected]

Global Head of Research and Economics

Diane Schumaker-Krieg ………………… ………[email protected] Head of Research & Economics

Chief Economist

Mark Vitner, Senior Economist……………....………. . .

Jay H. Bryson, Global Economist …………………....……….

Sam Bullard, Senior Economist [email protected]

Nick Bennenbroek, Currency Strategist ……[email protected]

Eugenio J. Alemán, Senior Economist……………….

Anika R. Khan, Senior Economist … . [email protected]

Senior Economists

Zachary Griffiths, Economic Analyst [email protected]

Sara Silverman, Economic Analyst [email protected]

Mackenzie Miller, Economic Analyst [email protected]

Blaire Zachary, Economic Analyst [email protected]

Economists

Azhar Iqbal, Econometrician………………………………[email protected]

Tim Quinlan, Economist …………………………………[email protected]

Michael A. Brown, Economist ………………… [email protected]

Sarah Watt House, Economist…………………………….

Michael T. Wolf, Economist …………………… .

Economic Analysts

Administrative Assistants

Wells Fargo Securities Economics Group publications are produced by Wells Fargo Securities, LLC, a U.S broker-dealer registered with the U.S. Securities and Exchange Commission, the Financial Industry Regulatory Authority, and the Securities Investor Protection Corp. Wells Fargo Securities, LLC, distributes these publications directly and through subsidiaries including, but not limited to, Wells Fargo & Company, Wells Fargo Bank N.A., Wells Fargo Advisors, LLC, Wells Fargo Securities International Limited, Wells Fargo Securities Asia Limited and Wells Fargo Securities (Japan) Co. Limited. Wells Fargo Securities, LLC. (“WFS”) is registered with the Commodities Futures Trading Commission as a futures commission merchant and is a member in good standing of the National Futures Association. Wells Fargo Bank, N.A. (“WFBNA”) is registered with the Commodities Futures Trading Commission as a swap dealer and is a member in good standing of the National Futures Association. WFS and WFBNA are generally engaged in the trading of futures and derivative products, any of which may be discussed within this publication. The information and opinions herein are for general information use only. Wells Fargo Securities, LLC does not guarantee their accuracy or completeness, nor does Wells Fargo Securities, LLC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice, are for general information only and are not intended as an offer or solicitation with respect to the purchase or sales of any security or as personalized investment advice. Wells Fargo Securities, LLC is a separate legal entity and distinct from affiliated banks and is a wholly owned subsidiary of Wells Fargo & Company © 2014 Wells Fargo Securities, LLC.

SECURITIES: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE

Important Information for Non-U.S. Recipients

For recipients in the EEA, this report is distributed by Wells Fargo Securities International Limited (“WFSIL”). WFSIL is a U.K. incorporated investment firm authorized and regulated by the Financial Conduct Authority. The content of this report has been approved by WFSIL a regulated person under the Act. WFSIL does not deal with retail clients as defined in the Markets in Financial Instruments Directive 2007. The FCA rules made under the Financial Services and Markets Act 2000 for the protection of retail clients will therefore not apply, not will the Financial Services Compensation Scheme be available. This report is not intended for, and should not be relied upon by, retail clients. This document and any other materials accompanying this document (collectively, the “Materials”) are provided for general informational purposes only.

Peg Gavin, Executive Assistant.

Cyndi Burris, Senior Administrative Assistant [email protected]