understanding and managing bias in investment clients

TRANSCRIPT

Fortuna Favi et Fortus Ltd.

Fortuna Favi et Fortus Ltd.- excellence through knowledge

Investor Behavior- towards Understanding Clients

Customer Types & Characteristics

Know Your Client Rule

It is required that dealer members and their investment advisors:

• Learn the essential facts relative to every client and to every order or

account accepted – the know your client rule.

• Ensure that the acceptance of any order for any account is within the

bounds of good business practice.

• Ensure that recommendations made for any account are appropriate for the

client and in keeping with his or her investment objectives, personal

circumstances and tolerance to bearing risk – the suitability principle.

Know-Your-Client: Prudence and

legislation is required as the cardinal

rule in making investment

recommendations.

All relevant information about a

client must be known in order to

ensure that the registrant’s

recommendations are suitable.

Know Your Client Rule

Client/Investor Bias

Bias In Clients

A bias can be described as a preference or an inclination (especially

one that inhibits impartial judgment) or an unfair act or policy

stemming from prejudice.

Behavioral biases fall into two broad categories - Cognitive and

Emotional

• Cognitive bias can be technically defined as basic statistical,

information processing or memory errors that are common to all

human beings. They can be thought of also as “blind spots” or

distortions in the human mind.

• Emotional biases: opposite

side of the spectrum from

illogical or distorted reasoning.

Emotions are physical

expressions, often involuntary,

related to feelings, perceptions

or beliefs about elements,

objects or relations between

them, in reality or in the

imagination.

Bias in Clients

• Impulse

• Intuition

• Feeling

Identification of Bias In Clients- types of Bias

Overconfidence - Bias:

Unwarranted faith in one’s intuitive reasoning, judgments, and cognitive

abilities – i.e. investors are overconfident in their investing abilities.

Specifically, the confidence intervals that investors assign to their investment

predictions are too narrow.

Leads to underestimation of downside risk, trading too frequently and/or

trading in pursuit of the next hot stock, and holding an under diversified

portfolio all pose serious hazards to your wealth

Representativeness Bias:

In order to derive meaning from life experiences, people have developed an

innate propensity for classifying objects and thoughts.

When clients are faced by a new phenomenon that is inconsistent with any of

their pre-constructed classifications, clients subject such ‘new phenomenon’ to

the same classifications anyway, relying on a rough best-fit approximation to

determine which category should house and, thereafter, form the basis for their

understanding of the new element e.g., Sample size neglect

Cognitive Dissonance Bias

Cognitions, in psychology, represent attitudes, emotions, beliefs, or values;

and cognitive dissonance is a state of imbalance that occurs when

contradictory cognitions intersect.

When newly acquired information conflicts with preexisting understandings,

people often experience mental discomfort - a psychological phenomenon

known as cognitive dissonance.

Thus, When people modify behaviors or cognitions to achieve cognitive

harmony, however, the modifications that they make are not always rationally

in their self-interest.

Advice: investors must address feelings of unease at their source and take an

appropriate rational action.

Availability Bias

This is a rule of thumb, or mental shortcut, that allows people to estimate the

probability of an outcome based on how prevalent or familiar that outcome

appears in their lives.

People exhibiting this bias perceive easily recalled possibilities as being more

likely than those prospects that are harder to imagine or difficult to

comprehend.

Investors ignore potentially beneficial investments because information on

those investments is not readily available, or they make investment decisions

based on readily available information, avoiding diligent research.

Availability Bias

Categories of Availability bias that apply to investors include:

(1) Retrievability,

(2) Categorization,

(3) Narrow range of experience

(4) Resonance

1, Retrievability - Ideas that are retrieved most easily also seem to be the

most credible, though this is not necessarily the case.

2, Categorization - People attempt to categorize or summon information that

matches a certain reference.

Different tasks require different search sets, but; when it is difficult to put

together a framework for a search, people often mistakenly conclude that the

search simply references a more meager array of results.

E.g., if a French person simultaneously tries to come up with a list of quality

U.S. vineyards and a corresponding list of French vineyards, the list of U.S.

vineyards is likely to prove difficult to create.

The French person, as a result, might predict that high-quality U.S. vineyards

exist with a lower probability than famous French vineyards, even if this is not

necessarily the case.

Availability Bias

Availability Bias

3, Narrow range of experience - When a person possesses a too restrictive

frame of reference from which to formulate an objective estimate, then

narrow range of experience bias often results.

4, Resonance - The extent to which certain, given situations resonate vis-à-vis

the individuals’ own, personal situations can also influence judgment.

For example, fans of classical music might be likely to overestimate the

portion of the total population that also listens to classical music.

Anchoring and Adjustment Bias

When required to estimate a value with unknown magnitude, people generally

begin by envisioning some initial, default number—an anchor—which they

then adjust up or down to reflect subsequent information and analysis.

The anchor, once fine-tuned and reassessed, matures into a final estimate.

Investors exhibiting this bias are often influenced by purchase points—or

arbitrary price levels or price indexes—and tend to cling to these numbers

when facing questions such as:

Should I buy or sell this security?

Is the market overvalued or undervalued right now?

Self-Attribution Bias

Refers to that tendency of individuals to ascribe their successes to innate

aspects, such as talent or foresight, while blaming failures on outside

influences, such as bad luck.

E.g., athletes often reason that they have simply performed to reflect their own

superior athletic skills if they win a game, but they might allege unfair calls by

a referee when they lose a game. Can be of two types:

Self-enhancing bias represents people’s propensity to claim an irrational

degree of credit for their successes.

Self-protecting bias represents the corollary effect—the irrational denial of

responsibility for failure.

Self-Attribution Bias – Contd’

Implications for Investors: Irrationally attributing successes and failures can

impair investors by:

A, people who aren’t able to perceive mistakes they’ve made are,

consequently, unable to learn from those mistakes.

B, investors who disproportionately credit themselves when desirable

outcomes do arise can become detrimentally overconfident in their own

market savvy.

Illusion of Control Bias

The illusion of control bias describes the tendency of human beings to believe

that they can control or at least influence outcomes when, in fact, they cannot.

E.g., Casino patrons swear that they are able to impact random outcomes such

as the product of a pair of tossed dice.

Implications for Investors:

Investors might trade more than is prudent and maintain under-diversified

portfolios.

They use limit orders and other such techniques in order to experience a false

sense of control over their investments.

In general, it contributes to investor overconfidence.

Conservatism Bias

Conservatism bias is a mental process in which people cling to their prior

views or forecasts at the expense of acknowledging new information.

E.g, an investor receives some bad news regarding a company’s earnings and

that this news negatively contradicts another earnings estimate issued the

previous month. The investor might underreact to the new information,

maintaining impressions derived from the previous estimate rather than acting

on the updated information.

NB: Not to be confused with representativeness bias whereby people

overreact to new information.

Conservatism Bias contd’

Implications:

This bias might make investors cling to a view or forecast, behaving too

inflexibly despite being presented with new information.

It makes reactions to changes slow.

Might relate to an underlying difficulty in processing new information.

Ambiguity Aversion Bias

People do not like to gamble when probability distributions seem uncertain. In

general, people hesitate in situations of ambiguity- referred to as ambiguity

aversion.

Implications for Investors:

It may cause investors to demand higher compensation for the perceived risks

of investing in certain assets. Also, it may restrict investors to their own

national indexes (e.g., Standard & Poor’s 500) because these indexes are more

familiar than foreign ones.

Investors might believe their employers’ stocks are safer investments than

other companies’ stocks because investments in other companies are

ambiguous.

Endowment Bias

These clients value an asset more when they hold property rights to it than

when they don’t.

It is in line with standard economic theory, which asserts that a person’s

willingness to pay for a good or an object should always be equal to the

person’s willingness to accept dispossession of the good or the object, when

the dispossession is quantified in the form of compensation.

However it has been found that the minimum selling prices that people state

tend to exceed the maximum purchase prices that they are willing to pay for

the same good.

Effectively, then, ownership of an asset instantaneously endows the asset with

some added value.

Endowment Bias

Endowment bias can affect attitudes

toward items owned over long

periods of time or can crop up

immediately as the item is acquired.

Investors prove resistant to change

once they become endowed with

(take ownership of) securities.

Studies have shown that clients are

usually reluctant to sell inherited

securities.

Self-Control Bias

This bias is a human behavioral tendency that causes people to consume today

at the expense of saving for tomorrow.

E.g., Would you rather contribute N300 per month over the course of the next

12 months to some savings account earmarked for year-end tax payment?

Or

would you rather increase your federal income tax withholding by N300 each

month, sparing you the responsibility of writing out one large check at the end

of the year?

Rational economic thinking suggests that you should prefer the savings

account approach because your money would accrue interest and you would

actually net more than N3,600.

However, many taxpayers choose the withholding option because they realize

that the savings account plan would be complicated in practice by a lack of

self-control.

Self-control bias can also be described as a conflict between people’s

overarching desires and their inability, stemming from a lack of self-

discipline, to act concretely in pursuit of those desires.

This theory can be extended to the savings and consumption pattern in

individuals.

It is wise to espouse the pros & Cons of ‘saving today for the future’ both

verbally and with financial with models.

Self-Control Bias

Optimism Bias

Perception of the world through ‘rose tinted glasses’. Investors, too, tend to be

overly optimistic about the markets, the economy, and the potential for

positive performance of the investments they make.

Many overly optimistic investors believe that bad investments will not happen

to them—they will only afflict others.

Such oversight can damage portfolios because people fail to mindfully

acknowledge the potential for adverse consequences in the investment

decisions they make.

Instances of optimism bias include: overloading self with company stock, the

feeling of getting market-like returns etc.

Implications for Investors. Undue optimism can be financially harmful

because it creates, for investors, the illusion of some unique insight or

upper hand.

Financial advisors should understand investor optimism and respond by

counseling the pitfalls of overinvesting in company stock. Such advice

includes:

• Live below your means, and save regularly.

• Asset allocation is the key to a successful portfolio.

• Compounding contributes significantly to long-term financial success.

• Encourage the use of a financial advisor.

Optimism Bias

Mental Accounting Bias

This bias describes people’s tendency to code, categorize, and evaluate economic

outcomes by grouping their assets into any number of non-fungible (non-

interchangeable) mental accounts. According to Shefrin and Thaler : people

mentally allocate wealth over three classifications:

(1) current income, (2) current assets, (3) future income.

The propensity to consume is greatest from the current income account, while

sums designated as future income are treated more conservatively.

Thus people put money in separate “mental accounts” when presented with a

financial decisions. E.g., participants value cash more highly than credit card

remittances, though the source of both is identical

E.g., participants value cash more highly than credit card remittances, even

though both forms of payment draw, ultimately, from the participant’s own

money

Implications for Investors:

• Envisioning distinct accounts to correspond with financial goals, however,

can cause investors to neglect positions that offset or correlate across

accounts. This can lead to suboptimal aggregate portfolio performance.

• Investors to irrationally distinguish between returns derived from income

and those derived from capital appreciation.

Mental Accounting Bias

• Mental accounting bias can

cause investors to allocate

assets differently when

employer stock is involved.

• Mental accounting bias can

cause investors to hesitate to

sell investments that once

generated significant gains but,

over time, have fallen in price.

Mental Accounting Bias

Confirmation Bias

A type of selective perception that emphasizes ideas that confirm our beliefs,

while devaluing whatever contradicts our beliefs. i.e. it refers to our all-too-

natural ability to convince ourselves of whatever it is that we want to believe.

Thus, Investors often fail to acknowledge anything negative about investments

they’ve just made, even when substantial evidence begins to argue against

these investments.

E.g., Chat roomers who harass anyone that voiced a negative opinion of the

company they invested in. They seek confirmations of their beliefs rather than

try to glean insight into their company through other investors,

Hindsight Bias

“I knew it all along!” - Once an event has elapsed, people tend to perceive that

the event was predictable—even if it wasn’t.

This is because actual outcomes are more readily grasped by people’s minds

than the infinite array of outcomes that could have but didn’t materialize.

This is usually in an attempt to alleviate the embarrassment of being caught

off-guard under peculiar circumstances, blunting the ugliest of surprises and

populating our horizon

– i.e., it is the tendency of people, with the benefit of hindsight following an

event, to falsely believe that they predicted the outcome of that event in the

beginning.

Based on an assumption that the outcome observed is, in fact, the only

outcome that was ever possible.

There is an underestimation of the uncertainty preceding the event in question

and underrates the outcomes that could have materialized but did not.

Implications for Investors: It gives investors a false sense of security when

making investment decisions which, can manifest as excessive risk taking

behavior, and place people’s portfolios at risk.

Hindsight Bias

Loss Aversion Bias

According to D. Kahneman and A. Tversky, ..” people generally feel a

stronger impulse to avoid losses than to acquire gains.” Loss aversion can

prevent people from unloading unprofitable investments, even when they see

little to no prospect of a turnaround.

Implications for Investors.: Loss aversion is a bias that simply cannot be

tolerated in financial decision making. It instigates the exact opposite of what

investors want: increased risk, with lower returns. Manifestations include:

• Investors holding on to losing investments for too long.

• Investors to selling winners too early, in the fear that their profit will

evaporate unless they sell.

• Can also be the reason for

holding an unbalanced

portfolios.

E.g., if several investment

positions fall in value and

the investor is unwilling to

sell due to loss aversion, an

imbalance can occur.

Loss Aversion Bias

Recency Bias

Refers to a cognitive predisposition that causes people to more prominently

recall and emphasize recent events and observations than those that occurred

in the near or distant past.

Implications for Investors.

• Investors extrapolate patterns and make projections based on historical data

samples that are too small to ensure accuracy.

• Investors ignore fundamental value and focus only on recent upward price

performance.

• Investors ignore proper asset allocation and the need for portfolio re-

balancing.

Regret Aversion Bias

Displayed by clients that avoid taking decisive actions because of the hindsight

fear that, whatever course of action selected will prove to be less than optimal.

This bias seeks to prevent the pain of regret associated with poor decision

making.

Regret Aversion usually manifests as:

• Undue apprehension about breaking into financial markets that have

recently generated losses

• Causing clients to hold onto losing positions too long in order to avoid

admitting errors and realizing losses.

• Can cause “herding behavior” because, for some investors, buying into an

apparent mass consensus can limit the potential for future regret.

Framing Bias

A decision frame is the decision maker’s subjective conception of the acts,

outcomes, and contingencies associated with a particular choice.

The frame that a decision maker adopts is controlled partly by the formulation

of the problem and partly by the norms, habits, and personal characteristics of

the decision maker.

Implications for Investors:

An individual’s willingness to accept risk can be influenced by how

questions/scenarios are framed i.e. positively or negatively.

E.g., the subjective difference between the statement -“25 percent of patients

will be saved” and “75 percent of patients will die.”

Framing bias can cause communication

of responses to questions about risk

tolerance that are either unduly

conservative or unduly aggressive –

i.e. wording or the context in which

options are presented directly impact (or

frame) our selections.

*Bear in mind is that framing bias and

loss aversion bias can and do work

together.

Framing Bias

Status Quo Bias

This is a bias that prejudices clients facing an array of choice options to elect

whatever option ratifies or extends the existing condition (i.e., the “status

quo”) in lieu of alternative options that might bring about change. i.e.

preference for things to stay relatively the same.

Implications for Investors:

• By taking no action, clients could end up holding investments

inappropriate to their own risk/return profiles.

• Investors/clients might hold onto hold securities, either inherited or

purchased, because of an aversion to transaction costs associated with

selling.

Bias - Summary

Cognitive Biases: include Representativeness, Overconfidence, Anchoring and

Adjustment, Cognitive Dissonance, Availability, Self-Attribution, Illusion of

Control, Conservatism, Ambiguity Aversion, Mental Accounting, Confirmation,

Hindsight, Recency, Framing.

Emotional Biases: include Endowment, Self-Control, Optimism, Loss

Aversion, Regret Aversion, Status Quo

KNOW – YOUR – CLIENT!

Learning About Clients

Client Interviews:

Information gathering usually begins with a client interview during which the

investment advisor can learn about the client’s life and dreams and can

identify any issues or problems.

The initial interview is also a good opportunity for the advisor and client to

share their philosophies about investing to determine whether they will be able

to work together compatibly.

E.g., it ‘may not be’ appropriate for an aggressive investor to have an advisor

who is used to dealing with conservative investors.

Client Interviews (contd)

The investment advisor may find that some clients have difficulty expressing

certain concepts in words.

E.g., while many individual investors know where they want to be financially

in 10, 20, or 30 years, most have a hard time explaining how much risk they

are willing to accept to reach their goals.

To help obtain information that may not come out in an interview, most

investment advisors and firms use a standardized or customized client

questionnaire.

Learning About Clients

Interviewing Skills

• Guided Discussion: collect the required information e.g. checklist

• Probing:

Use both closed-ended and open-ended questions.

Do not fi re a barrage of questions at clients.

Remember that a question’s usefulness does not end when an answer has

been given.

When asking for personal information, use a lead-in to establish why they

need the information.

• Attending - respect for clients needs and express real interest in helping

achieve individual objectives.

Securing a comfortable and private area for conversation

Routing incoming calls through voice mail or having an assistant take

them

Facing the client squarely and openly and establishing direct eye

contact

Focusing the conversation on the client’s needs and interests

• Active Listening: listen for the core meaning and relate it to other

information about the client before deciding on its significance and an

appropriate response.

• Empathy: be able to enter imaginatively into another’s world to understand

how the other person feels.

Interviewing Skills

Client Questionnaires:

Can be multiple choice (clients select from a pre-determined list of responses)

or open-ended (the client must write down the answer).

Some questionnaires focus on only one type of information needed to develop

a client’s investment policy, particularly the client’s attitudes toward risk,

while others gather a broader range of information.

Risk questionnaires are popular tools because of the difficulty clients have in

expressing their tolerance for risk.

A scoring system is normally utilized to evaluate client responses.

Learning About Clients

Questionnaires - Advantages

Questionnaires can be used to specify and prioritize generic financial and

lifestyle goals. - specifications about client goals and to express which goals

are more important than others.

Questionnaires can be used to pinpoint areas for client education. –

questionnaires can uncover inconsistencies in a client’s understanding

Family members can fill out additional questionnaires - separate questionnaires

can identify potential conflicts between two or more family members.

Questionnaires - Disadvantages

Clients may not understand some of the questions or may think

they understand them when they do not.

Do not automatically assume your client is as knowledgeable as

you are about investing.

Clients may think they can predict how they will react in certain

instances, but real life situations may produce entirely different

reactions. – when an actual market decline occurs, many investors

are not as bold as they formally thought.

Questionnaires - Disadvantages

Questionnaires are based on the assumption that clients take a holistic

approach to their assets. - Questionnaires, apply a single set of questions

to all client accounts as if each investor viewed all assets in the same

way.

What Advisors Need to Know

Information needed for the Investment policy statement IPS, is

divided into four categories:

• Personal situation

• Financial situation

• Personal and financial goals

• Attitudes toward risk

The Clients’ Personal Situation

• Age

• Marital status (single, married, divorced, separated)

• Number of dependents

• Employment details (type of work, job stability)

• Educational background (certification, post-graduate)

• Investing experience (number of years, types of securities)

• If married, all of the above information for the spouse

• If married, who makes the investment decisions

Client Financial Situation

•Amount of investable assets

•Annual income from all sources (other than investment income)

•Annual savings target (or a list of annual expenses)

•Type of investment accounts (cash accounts, margin accounts, registered

retirement plans)

•Other investments (company pension, employee stock options)

•Real estate (home, cottage)

Client Personal and Financial Goals

• Desired retirement age

• Desired retirement income

• Plans for major expenditures (vacation property, paying for a

child’s education, annual vacations)

• Gifting of assets (during lifetime or on death)

Attitudes Toward Risk

How do clients define risk –

(is it as income shortfall,

delayed retirement, less

wealth?)

• Client’s willingness to take

on risk

Attitude Behavior(Its really

a two-

way

street)

Communication Skills For Advisors

• Speak clearly and slowly and be prepared to repeat what they say,

particularly if the client has any physical incapacity that limits their ability

to hear or understand.

• Avoid jargon and choose language appropriate to the client’s level of

understanding of investment-related matters.

• Be aware of cultural differences that may affect communications,

particularly non-verbal language that may be interpreted differently in

different cultures.

• Set aside any preconceptions when listening to clients, particularly about

appearance, ethnicity, social background, intellectual capacity, and age.

• Eliminate distractions from their environment as much as possible.

• Commit to getting to know the client from the client’s point of view.

• Monitor non-verbal communication for possible meanings.

• Separate the content from the emotion of messages and analyze each

one.

• Use empathy to make the relationship less distant.

Communication Skills For Advisors

Investor Behaviour

Standard finance theory assumes that investors are:

• Are risk-averse

• Have rational expectations

• Manage their portfolios as a whole

Behavioral finance theory, on the other hand, suggests that investors:

• Can be risk-averse or risk-seeking, depending on the situation

• Have biased expectations

• Practice mental portfolio accounting

Risk Aversion versus Risk Seeking

Standard Finance, investors are assumed to be risk-averse, that is, given

the choice between two investments with identical expected returns, they

will invest in the one with the least amount of risk, as measured by the

standard deviation of returns. But in reality, clients faced with the

possibility of a loss, are often risk seeking rather than risk averse.

In dealing with gains, people tend to be risk averse, but when dealing

with losses, they tend to be risk seeking.

This asymmetric attitude toward risk can help explain why some

investors are unwilling to sell securities that have gone down in value.

Rather than sell and realize the

losses, investors sometimes hold on

in the hope of a recovery, even if

there is a chance that the loss could

become even bigger.

• Standard deviation : is a

statistical measure of risk that

measures the extent to which

returns differ from the average or

expected level of return.

(*commit to memory)

Risk Aversion vs. Risk Seeking (1)

Biased Expectations

Standard finance assumes that investors have rational expectations, that

is, they all gather and act on information in an efficient and unbiased

way.

-i.e the “rational economic human being” is a model of human economic

behavior that hypothesizes that three principles rule economic decisions

made by individuals:

• Perfect rationality

• Perfect self-interest

• Perfect information

Behavioral finance commonly defined as the application of

psychology to understand human behavior in finance or investing. It

claims that most people vastly overstate their abilities.

E.g., in a magazine study a group of adult men were asked three

questions:

• How would you rate your ability to get along with others?

• How would you rate your ability as a leader?

• How would you rate your athletic ability?

Biased Expectations

In terms of their ability to interact with others, and no fewer than 25% said

they were in the top 1%.

A full 70% of the men placed themselves in the top quartile of leadership

ability, and 60% answered that they were in the top quartile as athletes.

Thus, people are can be a poor judge of their own abilities. Investment

advisors must keep this in mind when they assess client responses to questions

in interviews and on questionnaires.

Overconfidence may cause investors to believe they are more tolerant of risk

than they really are.

Biased Expectations

Mental Accounting

Standard finance assumes that investors consider their entire portfolio when

they make decisions.

Behavioral finance, suggests that people compartmentalize their portfolio

into different accounts.

Mental accounting refers to the phenomenon whereby people do not treat

their assets as a single portfolio, but keep track of them separately (Ref: earlier

referenced slides).

In practical terms, this means that an investor who made N6,000 investing in

one stock, but lost N5,000 investing in another, is likely to dwell on the

N5,000 loss, despite the fact that the investor’s overall wealth increased by

N1,000.

Investor Personality Types

Eight Investor Personality Types (IPTs) with three personality

dimensions:

• Idealism versus Pragmatism (I vs. P)

• Framing versus Integrating (F vs. N)

• Reflecting versus Realism (T vs. R)

Visual Depiction of Personality Dimensions

Idealism (I)

Framing (F)

Reflecting (T)

Pragmatism (P)

Realism (R)

Integrating (N)

Combinations of the three different personality dimensions results in

Eight Possible Investor Personality Types.

These are: IFT, IFR, INT, INR, PFT, PFR, PNT and PNR.

Idealism Versus Pragmatism (I vs. P)

Clients that fall into the “idealist” end of the I vs. P spectrum

overestimate their investing abilities, display excessive optimism about

the capital markets and do not seek out information that contradicts their

views.

E.g, many investors continued buying technology stocks even as they fell

during the meltdown in 2000, eternally optimistic that these stocks

would make a comeback - discerning patterns where none exist, and

believing their above-average market acumen gives them an exaggerated

degree of control over the outcomes of their investments.

Such clients are disinclined to thorough research and they can fall prey to

speculative market fads.

Idealists are susceptible to overconfidence, optimism, availability, self-

attribution, illusion of control, confirmation, recency and representativeness

biases.

On the other hand, Pragmatists, display a realistic grasp of their own skills and

limitations as investors - are not too overconfident about the capital markets and

demonstrate a healthy dose of skepticism regarding their investing abilities.

They understand that investing is an undertaking based on probabilities, and

research to confirm their beliefs.

Idealism Versus Pragmatism (I vs. P)

Framing Versus Integrating (F vs. N)

Framers: evaluate each of their investments individually and do not

consider how each investment fits into an overall portfolio plan. They are

rigid in their mental approach to analyzing problems.

Also they perceive their portfolio as composed of ‘unique’ money, rather

than a composite of well-managed investments.

E.g., these clients typically have different allocations for “retirement

money”, “vacation money” and “university savings”. This is not

necessarily a bad thing, but advisors need to watch for content overlap

amongst allocations to guard clients against over-concentrations in an asset

class.

Framers also subconsciously “anchor” their estimates of market or security

price levels, clinging to arbitrary purchase “points”, which leads to bias in

future calculations.

But Integrators, are characterized by an ability to contemplate broader

contexts and externalities. Correctly viewing their portfolios as systems

whose components can interact and balance one another out.

Integrators understand the correlations between various financial

instruments and structure their portfolios accordingly, and are also flexible

in their approach to the market and security price levels.

Framing Versus Integrating (F vs. N)

Framers may be susceptible to

the following biases: anchoring,

conservatism, mental accounting,

framing and ambiguity aversion.

Integrators are investors who are

typically not susceptible to the

aforementioned biases.

Framing Versus Integrating (F vs. N)

Reflecting Versus Realism (T vs. R)

Reflectors have difficulty living with the consequences of their decisions and

have difficulty taking action to rectify their behaviors - justifying and

rationalizing incorrect actions and hesitating to own up to decisions that have not

worked out beneficially.

They are also prone to decision paralysis because they dread the sensation of

regret should they miscalculate.

E.g., holding inherited securities – out of a sense of loyalty to a deceased relative

– which may not be a good fit in a diversified portfolio in the current investment

environment.

Realists, on the other hand, have less trouble coming to terms with the

consequences of their choices. They don’t tend to scramble for excuses in

order to justify incorrect actions, and responsibility for their mistakes.

They don’t experience regret as acutely and, therefore, don’t dread it ahead

of time.

Reflectors may be susceptible to the following biases: cognitive

dissonance, loss aversion, endowment, self-control, regret aversion, status

quo and hindsight.

Realists are investors who are typically not susceptible to the

aforementioned biases.

Reflecting Versus Realism (T vs. R)

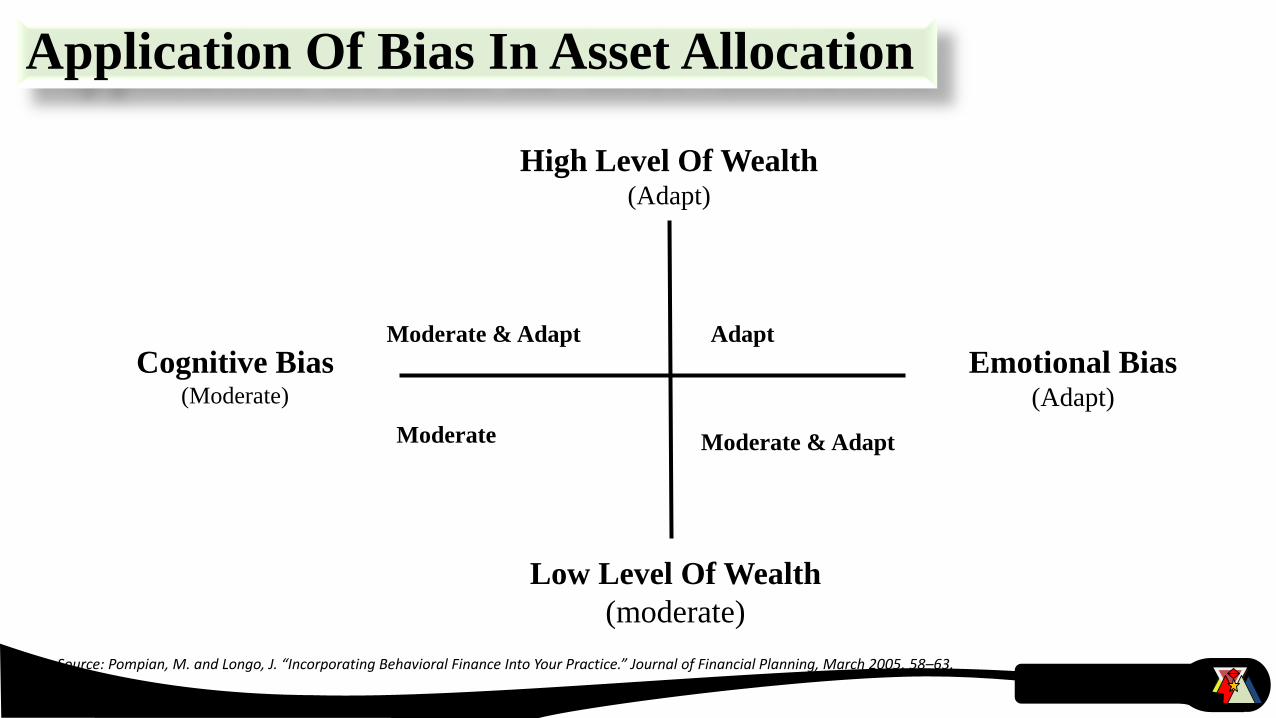

Application Of Bias In Asset Allocation

Low Level Of Wealth

(moderate)

High Level Of Wealth(Adapt)

Emotional Bias(Adapt)

Cognitive Bias(Moderate)

Moderate & Adapt

Moderate & Adapt

Adapt

Moderate

Source: Pompian, M. and Longo, J. “Incorporating Behavioral Finance Into Your Practice.” Journal of Financial Planning, March 2005, 58–63.

Individual Clients may be better served by moving them up or down

the efficient frontier (a set of optimal portfolios), adjusting risk and

return levels depending upon the clients behavioral tendencies i.e.

client’s best practical allocation – Micheal Pompian

A best practical allocation may slightly underperform over the long

term and have lower risk, but is an allocation that the client can

comfortably adhere to over the long run.

Many clients, in response to a market downturn, want to sell in a

panic.

Incorporation of Bias In Asset Allocation

Incorporation of Bias In Asset Allocation

2 principles for constructing a best practical allocation, in light of client

behavioral biases:

• Moderate biases in less-wealthy clients; adapt to biases in wealthier ones -

client outliving his assets constitutes a far graver investment failure than his

inability to accumulate the greatest possible wealth.

• Moderate cognitive biases; adapt to emotional ones – emotional biases

originate from impulse or intuition rather than conscious calculation, they are

difficult to rectify. Whilst, cognitive biases stem from faulty reasoning, better

information and advice – they can be corrected.

Fortuna Favi et Fortus Ltd.,

:118 Old Ewu Road, Aviation Estate, Lagos,

:07032530965 | www.ffavifortus.com | [email protected]