uk hotels forecast 2017

TRANSCRIPT

Facing the future

UK hotels forecast 2017

www.pwc.co.uk/hospitality-leisure

HBAA

6th October 2016

Liz Hall

PwC

Agenda

UK and global economic prospects

A mixed travel outlook

Hotel demand and supply snapshot

Latest London and regional hotels forecast

October 2016 Facing the future

Slide 2

PwC

UK and global economic prospects

October 2016 Facing the future

1 PwC

PwC

Slightly higher global growth expected in 2017, but significant divergence remains

October 2016 Facing the future

9

PwC September 2016 Global Economy Watch

Russia

Germany

UK

US

Brazil

India

Spain

Key

Canada

Mexico

South Africa

Australia

Japan

Italy

Greece

Ireland

France

= GDP growth in 2017

China

1.0

1.4

0.7 1.9

2.2

2.7

0.0 1.0

7.7

6.5

0.5

2.8

1.0 2.3

1.5

3.3

X.X

0.3

PwC

The UK is projected to remain one of the fastest growing G7 economies in 2016, but to lag behind in 2017 due to the impact of the Brexit vote

Source: ONS for 2015, PwC main scenario for 2016

5

October 2016 Facing the future

0.0

0.5

1.0

1.5

2.0

2.5

United Kingdom United States Canada Germany France Italy Japan

Real G

DP

gro

wth

(%

)

Real GDP growth (%)

2016 2017 (p)

PwC

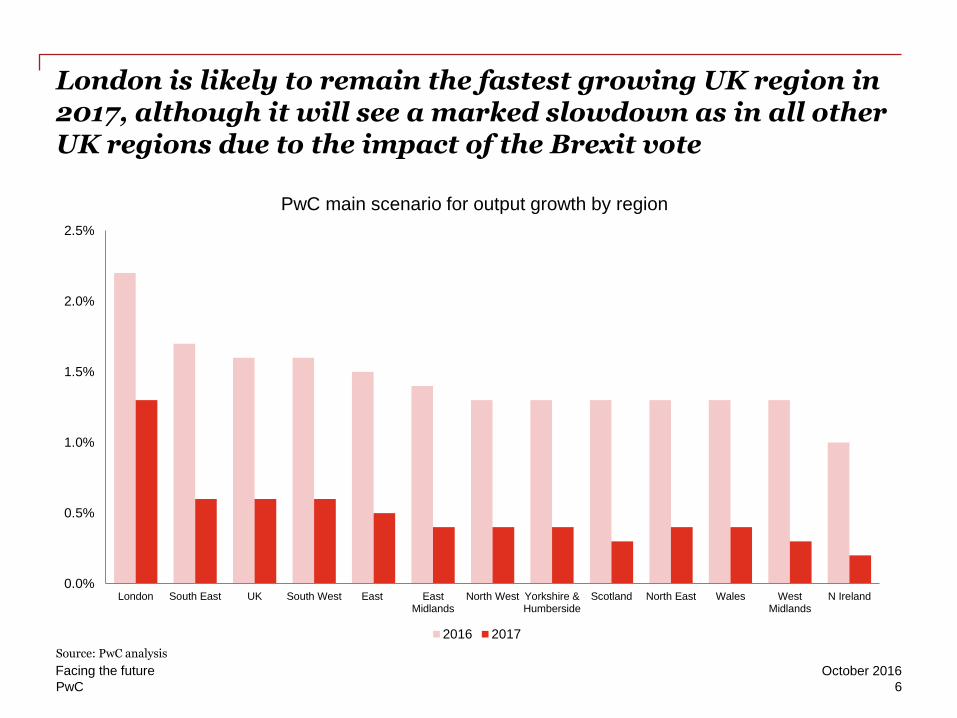

London is likely to remain the fastest growing UK region in 2017, although it will see a marked slowdown as in all other UK regions due to the impact of the Brexit vote

Source: PwC analysis

6

October 2016 Facing the future

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

London South East UK South West East EastMidlands

North West Yorkshire &Humberside

Scotland North East Wales WestMidlands

N Ireland

PwC main scenario for output growth by region

2016 2017

PwC

We project a marked decline in real earnings growth in 2017 as CPI inflation picks up while nominal earnings growth is dampened by the post-Brexit economic slowdown

Source: ONS, PwC analysis

7

October 2016 Facing the future

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% c

hange p

er

annum

CPI inflation vs nominal earnings growth

CPI Average weekly earnings (excl bonus)

CPI

Earnings

Projections

Real squeeze

PwC

Brexit: What has happened so far?

Facing the future

Pound has fallen – To c.$1.30-1.35 and €1.15-1.20

Political turbulence – Resignations/Leadership election; new PM and gov’t formed; opposition in turmoil

Increased uncertainty. Confidence indicators weakened in July but have since bounced back

Mixed economic indicators – Consistent with slower growth but not recession

No clarity on exit process until plan is developed, Article 50 is triggered and negotiations begin

Despite general air of uncertainty, businesses continuing to operate as normal, pending more policy clarity

October 2016

5

PwC

A mixed travel outlook

October 2016

Facing the future

11 PwC

PwC

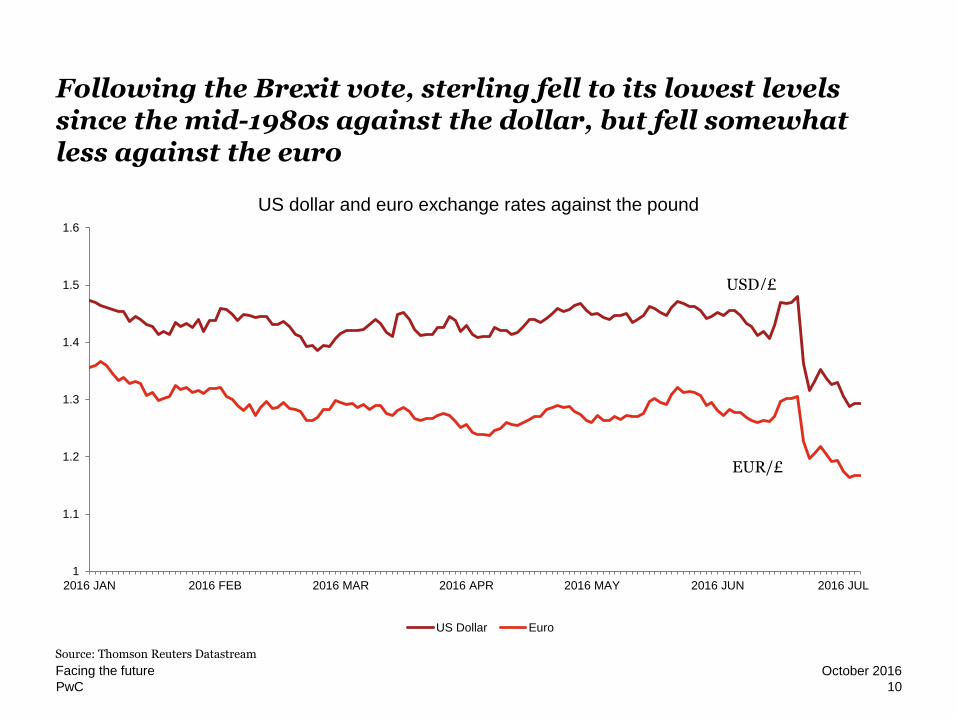

Following the Brexit vote, sterling fell to its lowest levels since the mid-1980s against the dollar, but fell somewhat less against the euro

Source: Thomson Reuters Datastream

10

October 2016 Facing the future

1

1.1

1.2

1.3

1.4

1.5

1.6

2016 JAN 2016 FEB 2016 MAR 2016 APR 2016 MAY 2016 JUN 2016 JUL

US dollar and euro exchange rates against the pound

US Dollar Euro

USD/£

EUR/£

PwC

Inbound travel is at record levels overall But divergence between segments

March 2002 22m

11

Nov 2012 31m

Jan ‘86 14m

Overseas visitors to UK - rolling 12 month total

June 2010 29m

Source: IPS, ONS Oct 2016

July 2016 36.5m

October 2016 Facing the future

PwC

Conferences and meetings trends at PwC The return of cost reduction

October 2016 Facing the future

Slide 12

• Away days were making a return but ‘Brexit’ has changed this

• Uncertainty is creeping into the market

• Cost reduction is back

• Reduction in banks and oil corporates - roll-over into meetings

• More corporates negotiating terms and conditions in advance

• Working internal space harder to incorporate more meetings and reduce cost

• Larger meetings may seem more cost effective but UK does not have huge capacity for meetings above 500 pax

PwC

Hotel demand and supply snapshot

October 2016 Facing the future

11 PwC

PwC

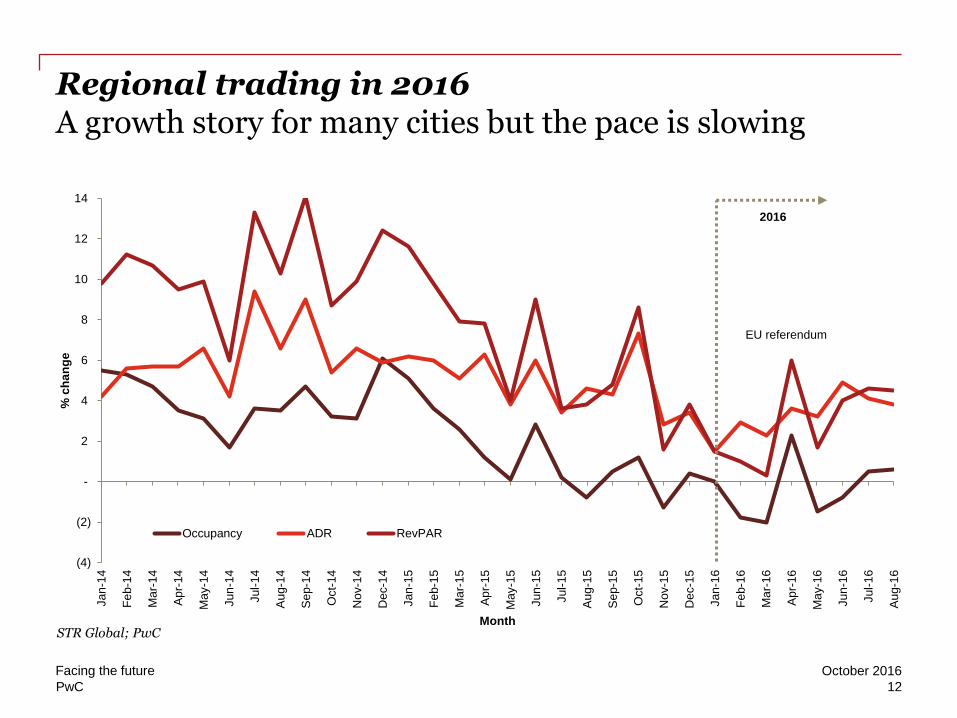

Regional trading in 2016 A growth story for many cities but the pace is slowing

October 2016 Facing the future

12

(4)

(2)

-

2

4

6

8

10

12

14

Jan

-14

Fe

b-1

4

Ma

r-1

4

Ap

r-14

Ma

y-1

4

Jun

-14

Jul-

14

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan

-15

Fe

b-1

5

Ma

r-1

5

Ap

r-15

Ma

y-1

5

Jun

-15

Jul-

15

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan

-16

Fe

b-1

6

Ma

r-1

6

Ap

r-16

Ma

y-1

6

Jun

-16

Jul-

16

Au

g-1

6

% c

ha

ng

e

Month

Occupancy ADR RevPAR

EU referendum

STR Global; PwC

2016

PwC

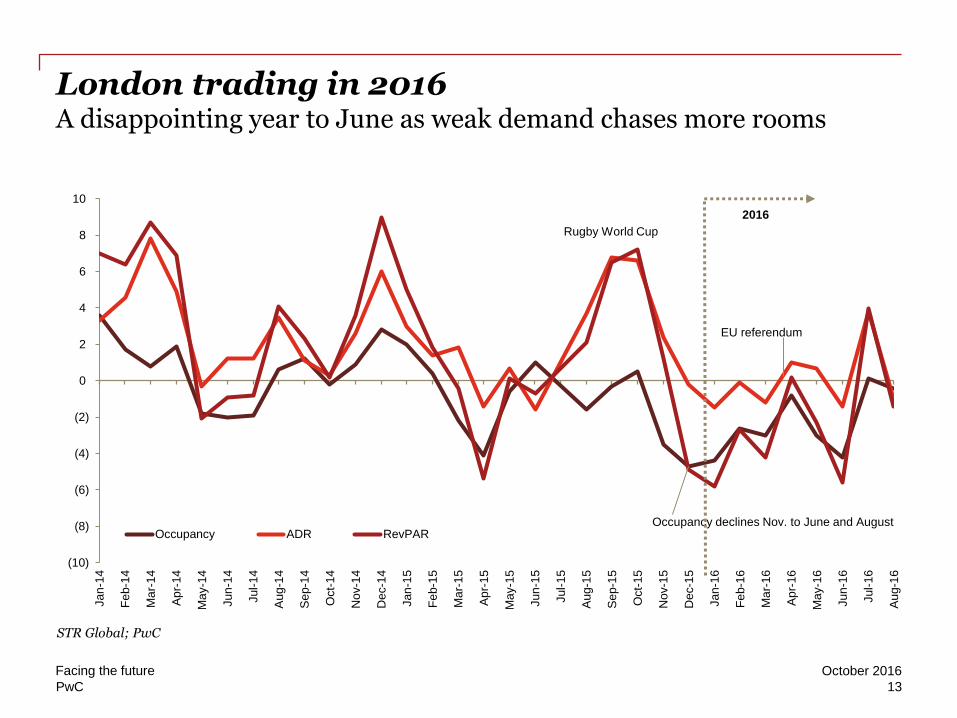

London trading in 2016 A disappointing year to June as weak demand chases more rooms

October 2016 Facing the future

13

(10)

(8)

(6)

(4)

(2)

0

2

4

6

8

10

Jan

-14

Fe

b-1

4

Ma

r-1

4

Ap

r-14

Ma

y-1

4

Jun

-14

Jul-

14

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan

-15

Fe

b-1

5

Ma

r-1

5

Ap

r-15

Ma

y-1

5

Jun

-15

Jul-

15

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan

-16

Fe

b-1

6

Ma

r-1

6

Ap

r-16

Ma

y-1

6

Jun

-16

Jul-

16

Au

g-1

6

Occupancy ADR RevPAR

EU referendum

Occupancy declines Nov. to June and August

Rugby World Cup

STR Global; PwC

2016

PwC

London: Build them and they will come? 5,000 rooms (66 hotels) opened in 2015 and to 1st Sept 2016

October 2016 Facing the future

14

PwC

London: Build them and they will come? 5,000 rooms (66 hotels) opened in 2015 and to 1st Sept 2016

October 2016 Facing the future

15

Source: AM PM

Within a 10 mile radius of central London

PwC

..and then build some more Another 8,770 rooms (67 hotels) to open in rest of 2016 and 2017

October 2016 Facing the future

16

PwC

..and then build some more Another 8,770 rooms (67 hotels) to open in rest of 2016 and 2017

October 2016 Facing the future

17

Within a 10 mile radius of central London

Source: AM PM

PwC

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2010 2011 2012 2013 2014 2015 2016F 2017F

London Regions

Growth above the long term average London leads the pipeline charge but there are regional hot spots

October 2016 Facing the future

18

Source: AMPM database

London 2.3% Regions 1.5%

20 year long term average

PwC

Latest London and Provincial forecast 2016 and 2017

October 2016 Facing the future

19 PwC

PwC

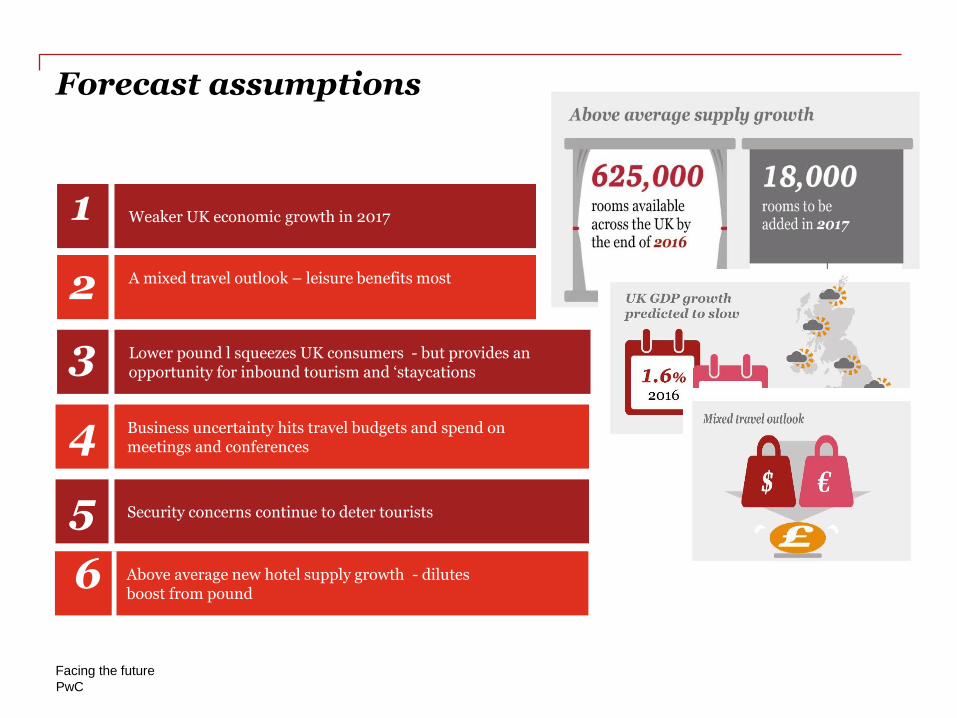

Forecast assumptions

Facing the future October 2016

10

Weaker UK economic growth in 2017

A mixed travel outlook – leisure benefits most

Lower pound l squeezes UK consumers - but provides an opportunity for inbound tourism and ‘staycations

1

2

3

Business uncertainty hits travel budgets and spend on meetings and conferences

Security concerns continue to deter tourists

4

5

6 Above average new hotel supply growth - dilutes boost from pound

6

PwC

London forecast 2016 and 2017 A cautious outlook

October 2016 Facing the future

21

PwC

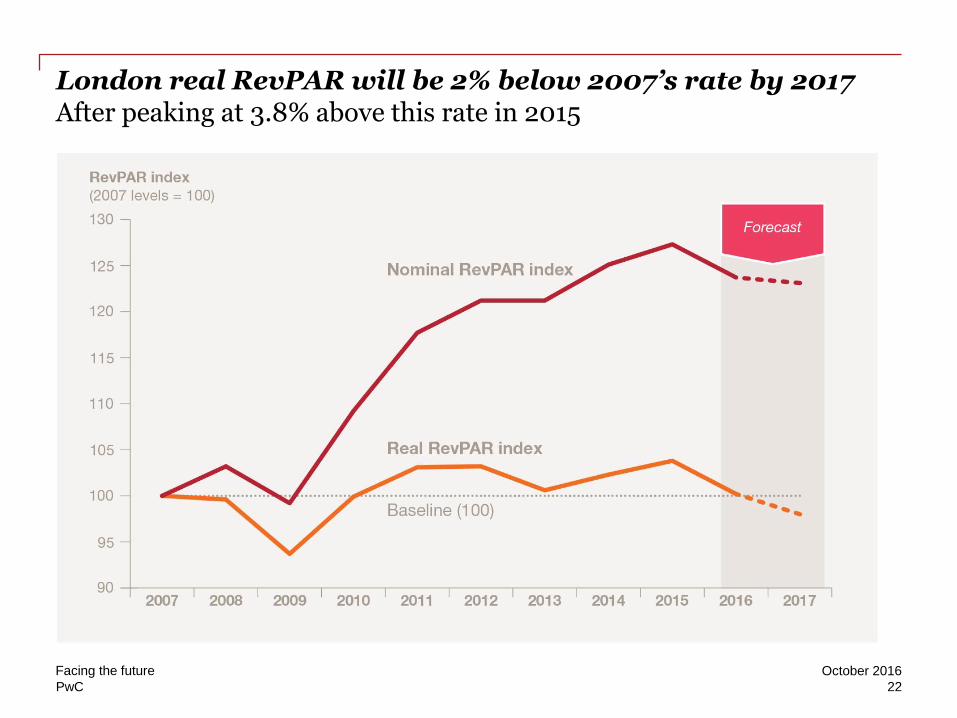

London real RevPAR will be 2% below 2007’s rate by 2017 After peaking at 3.8% above this rate in 2015

October 2016 Facing the future

22

PwC

Provinces forecast 2016 and 2017 More growth at a more sedate pace

October 2016 Facing the future

23

PwC

Still making up ground lost in 2007 By 2017, Provincial real RevPAR will be 4.5% below 2007’s rate

October 2016 Facing the future

24

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the

information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the

accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members,

employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to

act, in reliance on the information contained in this publication or for any decision based on it.

© 2016 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to the UK member firm, and may sometimes refer to the PwC

network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

161003-095700-LH-OS

Thank you!