ubs (lux) institutional sicav ii

TRANSCRIPT

UBS (Lux) Inst i tut ional S ICAV I I

Investment company under Luxembourg law (the "Company")

June 2015 Sales prospectus Shares in the Company may be acquired on the basis of this sales prospectus (the “Sales Prospectus”), the Company's Articles of Incorporation, the latest annual report and, if it has already been published, the subsequent semi-annual report. Only the information contained in the Sales Prospectus and the aforementioned documents shall be deemed to be valid. The shares of the sub-funds of the Company are intended to be placed with the public unless set forth anything to the contrary in this Sales Prospectus, investors may be offered the shares in the Company on a public or private placement basis and in accordance with applicable laws and regulations. The shares of the sub-funds of the Company are not listed on the Luxembourg Stock Exchange. The issue and redemption of shares of the Company are subject to the regulations prevailing in the concerned country of distribution. The Company keeps all investor information confidential, unless otherwise required by statutory or regulatory provisions, by any competent authority or by any competent court. Any reference in this Sales Prospectus to "EUR" refers to the European currency unit, any reference to "USD" refers to the Unites States Dollars, any reference to "CHF" refers to the Swiss Franc, any reference to "GBP" refers to the UK Pound Sterling, any reference to "RMB" or "CNY" or "CNH" refers to the People's Republic of China Renminbi, and any reference to "SGD" refers to the Singapore Dollar. Shares of the sub-funds mentioned in this Sales Prospectus may not be offered, sold or delivered within the United States of America. Shares of these sub-funds may not be offered, sold or delivered to citizens and/or residents of the United States of America and/or other persons or entities whose income and/or revenue is subject to US income tax, irrespective of its origin, including those deemed to be US persons under Regulation S of the US Securities Act of 1933 and/or the US Commodity Exchange Act, as amended.

Legal framework The Company is an undertaking for collective investment pursuant to Part II of the Luxembourg law of 17 December 2010 relating to undertakings for collective investment ("Law of 2010"), transposing EU Directive 2009/65/EC into Luxembourg law, as well as an alternative investment fund pursuant to the law of 12 July 2013 ("Law of 2013"), transposing EU Directive 2011/61/EU into Luxembourg law, and Commission Delegated Regulation (EU) No 231/2013 of 19 December 2012 supplementing Directive 2011/61/EU of the European Parliament and of the Council with regard to exemptions, general operating conditions, depositaries, leverage, transparency and supervision (referred to jointly with the Law of 2013 as the "AIFM Rules"). Management and Administration Registered office 33A avenue J.F. Kennedy, L-1855 Luxembourg. Board of Directors of the Company (the "Board of Directors") Chairman Tobias Meyer,

Executive Director, UBS AG, Basel and Zurich

Members

Thomas Portmann, Executive Director, UBS Fund Management (Switzerland) AG, Basel

2

Kai Gammelin, Executive Director, UBS AG, Basel and Zurich

Management Company and external AIFM of the Company UBS Fund Management (Luxembourg) S.A., R.C.S. Luxembourg 154.210 (the "Management Company", the “external AIFM”). The Management Company was incorporated in Luxembourg on 1 July 2010 in the legal form of a public limited company (Société Anonyme) for unlimited duration. Its registered office is at 33A avenue J.F. Kennedy, L-1855 Luxembourg. The articles of incorporation of the Management Company were published by reference on 16 August 2010 in the «Mémorial, Recueil des Sociétés et Associations» (the "Mémorial") and most recently amended on 14 January 2014. The consolidated version of the articles of incorporation of the Management Company has been deposited for inspection with the Luxembourg company's and trade register (Registre de Commerce et des Sociétés). The corporate object of the Management Company is, inter alia, the management of Luxembourg undertakings for collective investment as well as the issue and redemption of units of these products. At the date of this Sales Prospectus, in addition to the Company, the Management Company also manages other undertakings for collective investment. In order to cover its potential professional liability risks associated with professional negligence during the performance of relevant operations, the Management Company has a fully paid-up capital of EUR 13,000,000. UBS Fund Management (Luxembourg) S.A. is a management company pursuant to Chapter 15 of the Law of 2010 and is the external AIFM of the Company pursuant to Chapter 2 of the Law of 2013. The Management Company will take all reasonable steps to identify conflicts of interest that arise in the course of managing funds and will maintain and operate effective organisational and administrative arrangements with a view to taking all reasonable steps designed to identify, prevent, manage and monitor conflicts of interest in order to prevent them from adversely affecting the interests of the funds and their investors. With a view to adequately detect and manage conflicts of interests, the Management Company applies a policy of conflict of interests that contains: - a methodology for identification of potential conflicts situations; - standards on organizational arrangements to prevent, adequately manage or disclose conflicts of interests. The Management Company keeps and updates periodically a register with the details of established or potential conflicts of interest that may have arisen or are likely to arise. The Management Company will ensure that conflicts of interest cannot result in a risk of damage to the investors' interests and, if the Management Company is not confident that a conflict does not trigger any adverse effect to investors, the Management Company will disclose the relevant source of conflicts to the investors via internet at www.ubs.com/lu/en/asset_management/investor_information.html Board of Directors of the Management Company

Chairman Andreas Schlatter,

Group Managing Director, UBS AG, Basel and Zurich

3

Members Martin Thommen, Managing Director, UBS AG, Basel and Zurich

Gilbert Schintgen, Managing Director, UBS Fund Management (Luxembourg) S.A., Luxembourg

Christian Eibel, Executive Director, UBS AG, Basel and Zurich

Executive Board of the Management Company Members Gilbert Schintgen,

Managing Director, UBS Fund Management (Luxembourg) S.A., Luxembourg

Valérie Bernard, Executive Director, UBS Fund Management (Luxembourg) S.A., Luxembourg

Portfolio Management The external AIFM has delegated the portfolio management function of the sub-funds to UBS Global Asset Management (Singapore) Ltd and UBS Global Asset Management (Hong Kong) Limited (the “Portfolio Manager(s)”). The Portfolio Manager of the sub-fund UBS (Lux) Institutional SICAV II – China A Opportunity (USD) is UBS Global Asset Management (Singapore) Ltd. UBS Global Asset Management (Singapore) Ltd has delegated the portfolio management of part or all of the assets of this sub-fund to UBS Global Asset Management (Hong Kong) Limited. The Portfolio Manager of the sub-fund UBS (Lux) Institutional SICAV II – Mainland China Fixed Income (USD) is UBS Global Asset Management (Hong Kong) Limited. UBS Global Asset Management (Hong Kong) Limited has delegated the portfolio management of part or all of the assets of this sub-fund to UBS Global Asset Management (Singapore) Ltd. The Portfolio Manager of the sub-fund UBS (Lux) Institutional SICAV II – China Income (RMB) is UBS Global Asset Management (Hong Kong) Limited. UBS Global Asset Management (Hong Kong) Limited has delegated the portfolio management of part or all of the assets of this sub-fund to UBS Global Asset Management (Singapore) Ltd. All or most of the investment in the PRC is intended to be made and held through the QFII and/or RQFII quota of UBS Global Asset Management (Singapore) Ltd and/or UBS Global Asset Management (Hong Kong) Limited. The Portfolio Managers are commissioned to manage the securities portfolio under the supervision and responsibility of the external AIFM, and to carry out all relevant transactions while adhering to the prescribed investment restrictions of the relevant sub-fund. The Portfolio Management units of UBS Global Asset Management may transfer their mandates, fully or partially, to associated Portfolio Managers within UBS Global Asset Management, subject to the AIFM Rules. Responsibility in each case remains with the aforementioned Portfolio Manager assigned by the external AIFM.

4

Pooling of assets The Company may permit internal pooling and/or joint management of assets from particular sub-funds in the interests of efficiency. In this case, assets from different sub-funds will be managed together. The assets under joint management are referred to as a "pool". Pools are used exclusively for internal management purposes, are not separate units and cannot be accessed directly by shareholders. Pooling The Company may invest and manage all or part of the portfolio assets held by two or more sub-funds (for this purpose called "participating sub-funds") in the form of a pool. Such an asset pool is created by transferring to it cash and other assets (if these assets are in line with the investment policy of the pool concerned) from each of the participating sub-funds to the asset pool. The Company can then make further transfers to the individual asset pools. Equally, assets can also be transferred back to a participating sub-fund up to the amount of the participation of the sub-fund concerned. The participation of a participating sub-fund in an asset pool is evaluated by reference to notional units of the same value in the relevant asset pool. When an asset pool is created, the Company shall specify the initial value of the notional units (in a currency that the Company considers appropriate) and allot to each participating sub-fund notional units having an aggregate value equal to the amount of the cash (or other assets) it has contributed. Thereafter, the value of the notional units will then be determined by dividing the net assets of the asset pool by the number of existing notional units. If additional cash or assets are contributed to or withdrawn from an asset pool, the notional units assigned to the participating sub-fund concerned will increase or diminish, as the case may be, by a number, which is determined by dividing the amount of cash or the value of assets contributed or withdrawn by the current value of the participating sub-fund's participation in the asset pool. If cash is contributed to the asset pool, for calculation purposes it is reduced by an amount that the Company considers appropriate in order to take account of any tax expenses as well as the closing charges and acquisition costs relating to the investment of the cash concerned. If cash is withdrawn, a corresponding deduction may be made in order to take account of any costs related to the disposal of securities or other assets of the asset pool. Dividends, interests and other income-like distributions, which are obtained from the assets of an asset pool, are allocated to the asset pool concerned and thus lead to an increase in the respective net assets. If the Company is liquidated, the assets of an asset pool are allocated to the participating sub-funds in proportion to their respective share in the asset pool. Joint management In order to reduce operating, administrative and management costs and at the same time to permit broader diversification of investments, the Company may decide to manage part or all of the assets of one or more sub-funds in combination with assets that belong to other sub-funds or to other undertakings for collective investment. In the following paragraphs, the term "jointly managed entities" refers globally to the Company and each of its sub-funds and all entities with or between which a joint management agreement would exist; the term "jointly managed assets" refers to the entire assets of these jointly managed entities which are managed according to the same aforementioned agreement. As part of the joint management agreement, the relevant Company's portfolio manager(s) will, on a consolidated basis for the relevant jointly managed entities, be entitled to make decisions on investments and sales of assets which have an influence on the composition of the Company's and its sub-funds' portfolio. Each jointly managed entity holds a portion in the jointly managed assets corresponding to the proportion of its net assets to the total value of the jointly managed assets. This proportionate holding (for this purpose called the "participation arrangement") applies to each and all investment categories which are held or acquired in the context of joint management. Decisions regarding investments and/or sales of investments have no effect on this participation arrangement: further investments will be allotted to the jointly managed entities in the same proportions and, in the event of a sale of assets, these will be subtracted proportionately from the jointly managed assets held by the individual jointly managed entities. In the case of new subscriptions in one of the jointly managed entities, the subscription proceeds are to be allocated to the jointly managed entities in accordance with the changed participation arrangement resulting from the increase in net assets of the jointly managed entity having benefited from the subscriptions. The level of the investments will be modified by the transfer of assets from one jointly managed entity to the other, and thus adapted to suit the changed participation arrangement. Similarly, in the case of redemptions for one of the jointly managed entities, the necessary liquid funds shall be taken from the liquid funds of the jointly managed entities in accordance with the changed participation arrangement resulting from the

5

reduction in net assets of the jointly managed entity which has been the subject of the redemptions, and in this case the particular level of all investments will be adjusted to suit the changed participation arrangement. Shareholders should be aware that the joint management agreement may result in the composition of the assets of a particular sub-fund being affected by events which concern other jointly managed entities, e.g. subscriptions and redemptions, unless the members of the Company or one of the duly appointed agents of the Company resort to special measures. If all other aspects remain unchanged, subscriptions received by an entity under joint management with the sub-fund will therefore result in an increase in the cash reserve of this sub-fund. Conversely, redemptions of an entity under joint management with the sub-fund will result in a reduction of the cash reserve of this sub-fund. However, subscriptions and redemptions can be executed on the special account that is opened for each jointly managed entity outside the joint management agreement and through which subscriptions and redemptions must pass. Because of the possibility of posting extensive subscriptions and redemptions to these special accounts, and the possibility that the Company or one of the duly appointed agents of the Company may decide at any time to terminate the participation of the sub-fund in the joint management agreement, the sub-fund concerned may avoid having to rearrange its portfolio if this could adversely affect the interests of the Company, its sub-funds and its shareholders. If a change in the portfolio composition of the Company or one or several of its relevant sub-funds as a result of redemptions or payments of fees and expenses referring to another jointly managed entity (i.e. which cannot be counted as belonging to the Company or the sub-fund concerned) might result in a violation of the investment restrictions applying to the Company or the particular sub-fund, the relevant assets will be excluded from the joint management agreement before implementing the change so that they are not affected by the resulting adjustments. Jointly managed assets of a particular sub-fund will only be managed in common with assets intended to be invested according to the same investment objectives that apply to the jointly managed assets in order to ensure that investment decisions are compatible in all respects with the investment policy of the particular sub-fund. Jointly managed assets may only be managed in common with assets for which the same portfolio manager is authorised to make decisions in investments and the sale of investments, and for which the Depositary also acts as a depositary so as to ensure that the Depositary is capable of performing its functions and responsibilities in accordance with the Law of 2010 and statutory requirements in all respects for the Company and its sub-funds. The Depositary must always keep the assets of the Company separate from those of the other jointly managed entities; this allows it to determine the assets of the Company and of each individual sub-fund accurately at any time. Since the investment policy of the jointly managed entities does not have to correspond exactly with that of a sub-fund, it is possible that their joint investment policy may be more restrictive than that of that sub-fund. The Company may decide to terminate the joint management agreement at any time without giving prior notice. Shareholders may enquire at any time at the Company's registered office as to the percentage of jointly managed assets and entities with which there is a joint management agreement at the time of their enquiry. The composition and percentages of jointly managed assets must be stated in the annual reports. Joint management agreements with non-Luxembourg entities are permissible if (i) the agreement in which the non-Luxembourg entity is involved is governed by Luxembourg law and Luxembourg jurisdiction or (ii) each jointly managed entity is equipped with such rights that no creditor and no insolvency or bankruptcy administrator of the non-Luxembourg entity has access to the assets or is authorised to freeze them. Depositary and Main Paying Agent UBS (Luxembourg) S.A., 33A avenue J.F. Kennedy, L-1855 Luxembourg is the depositary and principal paying agent of the Company (the “Depositary”) under a depositary agreement entered into between the external AIFM, the Company and the Depositary for an unlimited period of time (the “Depositary Agreement”). The Depositary holds all liquid assets and securities of the Company to the extent entrusted to the Depositary for safekeeping. The Depositary performs all customary banking duties relating to the Company’s accounts and securities as well as all routine administrative work in connection with the Company’s assets and prescribed by Luxembourg law. All assets of the Company which are financial instruments that can be held in custody will be held in custody by the Depositary or by third parties to which the Depositary has delegated such functions in accordance with the AIFM Rules (“Sub-custodians”) on segregated accounts. Vis-à-vis all other assets, the Depositary will keep a record of those assets for which it has verified that the ownership

6

over the relevant assets effectively belongs to the Company. The verification of ownership will be based on information and documents provided by the Company, the external AIFM and/or one of their service providers or representatives as well as on external evidence, to the extent available. The Depositary will keep its records up-to-date. The portfolio management function or the risk management function cannot be entrusted to the Depositary or a Sub-custodian. These functions can also not be delegated to them further to sub-delegations. The Depositary may not re-use the assets in its safekeeping without the prior agreement of the Company and/or external AIFM. The liability of the Depositary shall in principle not be affected by any delegation(s) of its custody function. Exceptions can be made in accordance with applicable laws. These include (i) where it has contractually discharged its responsibility in compliance with article 19 (13) of the Law of 2013; (ii) where the laws of a third country requires that certain financial instruments be held by a local entity and there are no local entities that satisfy the delegation requirements and (iii) where the Company and the external AIFM insist on maintaining an investment in a particular jurisdiction despite warnings by the Depositary as to the increased risk this presents. Administrative Agent UBS Fund Services (Luxembourg) S.A., 33A avenue J.F. Kennedy, L-1855 Luxembourg. UBS Fund Services (Luxembourg) S.A. as the administrative agent is responsible for the general administrative duties involved in managing the Company and prescribed by Luxembourg law. These administrative services mainly include domiciliation, calculation of the net asset value per share and the keeping of the Company’s accounts as well as reporting. External Valuer The external AIFM has delegated the valuation function of the Company’s assets to the Administrative Agent (the “External Valuer”). Auditor of the Company PricewaterhouseCoopers, société coopérative, 2, rue Gerhard Mercator, L-2182 Luxembourg. Sales Agencies UBS (Luxembourg) S.A., 33A avenue J.F. Kennedy, L-1855. Luxembourg, as well as the other authorised sales agencies in the various countries. Distributor The external AIFM has delegated the distribution of the Company’s shares to UBS AG, Basel and Zurich, Switzerland. Delegation and description of the main legal implications of contractual relationships entered into for the purpose of investment of Company assets The delegation of any type of service which the external AIFM provides for the account of its investors shall be based on a written agreement between the external AIFM and the respective service provider. Delegation agreements shall be entered into in accordance with the AIFM Rules and will cover the legal relationships between the external AIFM and the respective delegate. The legal instruments providing for the enforcement of the Company's rights are those prescribed by Luxembourg civil law (code civil). These agreements are subject to Luxembourg law and the jurisdiction of the Luxembourg courts. The Depositary Agreement shall be entered into by the external AIFM, the Company and the Depositary, and shall comply with all applicable regulations. The conditions set out above shall apply mutatis mutandis to this agreement. The above-mentioned service providers may only delegate the functions transferred to them by the Company or the external AIFM to third parties subject to the AIFM Rules. If the task of valuating the Company's assets is delegated by the external AIFM to an external service provider in accordance with the AIFM Rules, this task cannot be sub-delegated. The original liability towards investors remains unaffected by the delegation of functions.

7

Profile of the typical investor The sub-funds and share classes presently offered are suitable as an investment for retail and/or institutional clients that have a long-term investment horizon and want to invest in a broadly diversified portfolio. Risk profile Sub-fund investments may be subject to substantial fluctuations and no guarantee can be given that the value of a share will not fall below its value at the time of acquisition. Factors that can trigger such fluctuations or can influence their scale include but are not limited to:

changes affecting specific companies;

changes in interest rates;

changes in exchange rates;

changes in the prices of raw materials and energy resources;

changes affecting economic factors such as employment, public expenditure and indebtedness, inflation;

changes in the legal situation;

changes in the confidence of investors in certain asset classes (e.g. equities), markets, countries, industries and sectors; and

changes in securities lending rates. By diversifying investments, the Portfolio Manager endeavours to partially reduce the negative impact of such risks on the value of the shares. The Company Legal Aspects The Company offers investors a range of one or more sub-funds (umbrella structure) which invest in accordance with the investment policies described in this Sales Prospectus. This Sales Prospectus, which contains specific details on each sub-fund, will be updated on the inception of each new sub-fund. Name of the Company: UBS (Lux) Institutional SICAV II Legal form: open-ended investment company in the legal form of a Société

d’Investissement à Capital Variable ("SICAV")

Date of Incorporation: 30 March 2006 Number in the Luxembourg company's and trade register:

R.C.S. B 115.356

Financial year: 1 February to 31 January Annual General Meeting: Yearly on 20 April at 10.00 a.m. CET at the registered office of the Company.

If the aforementioned day is not a bank business day in Luxembourg, the annual general meeting will be held on the next Luxembourg bank business day.

Articles of Incorporation: First publication 20 April 2006 Published in the Mémorial

Amendments 28 January 2011 Published in the Mémorial 9 May 2011 Published in the Mémorial Management Company and external AIFM:

UBS Fund Management (Luxembourg) S.A.; R.C.S. Luxembourg B 154.210

Each amendment of the Company's articles of incorporation (the "Articles of Incorporation") shall be published in the Mémorial, in a Luxembourg daily newspaper and, if necessary, in the official publications specified for the respective countries in which shares of the Company are sold. Such amendments become legally binding in respect of all shareholders subsequent to their approval by the general meeting of shareholders. The Company draws the investors’ attention to the fact that any investor will only be able to fully exercise his investor rights directly against the Company, notably the right to participate in general meetings of shareholders, if he is registered himself and in his own name in the shareholders’ register of the Company. In cases where an investor invests in the Company through an intermediary investing into the Company in its own name but on behalf of the investor, it may not always be possible for the investor to exercise certain shareholder rights. Investors are advised to take advice on their rights.

8

The following sub-funds are available:

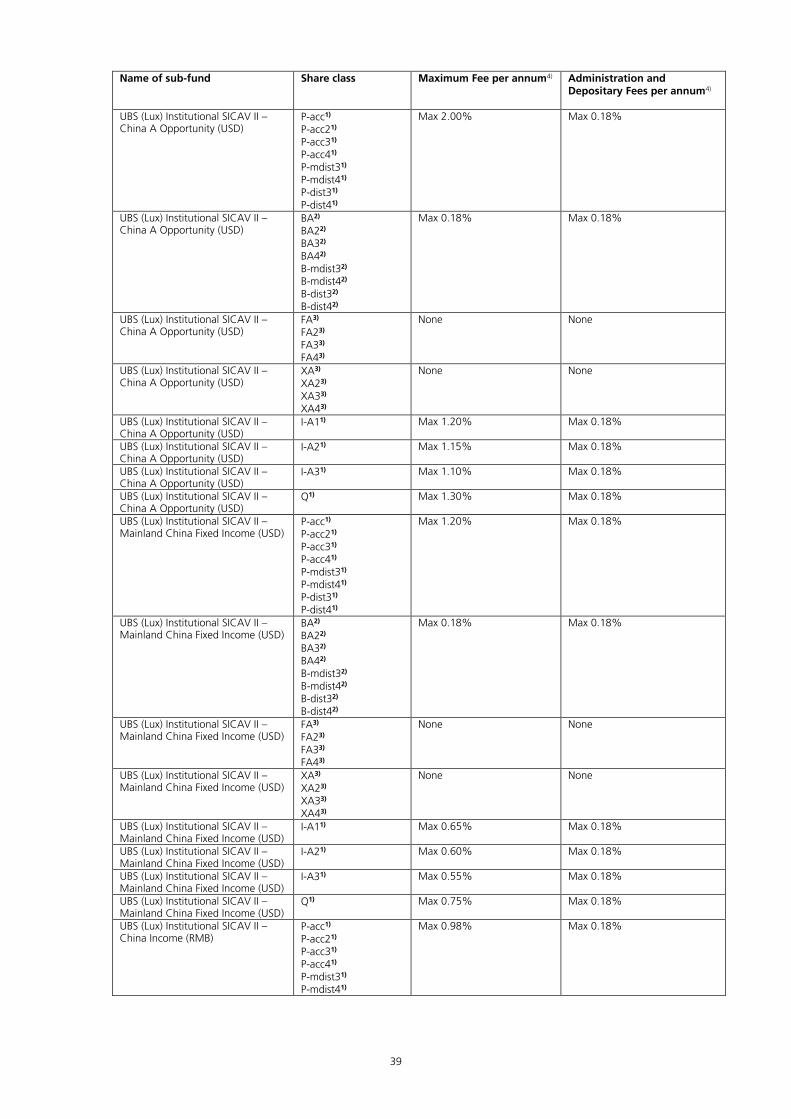

sub-fund name currency of account used UBS (Lux) Institutional SICAV II – China A Opportunity (USD) USD UBS (Lux) Institutional SICAV II – Mainland China Fixed Income (USD) USD UBS (Lux) Institutional SICAV II – China Income (RMB) CNY Share Classes The Company can issue several share classes for each of the sub-funds. All share classes are issued in registered form only. Currently, the following share classes are offered in all sub-funds of the Company: P-acc BA FA XA I-A1 Q P-acc2 BA2 FA2 XA2 I-A2 - P-acc3 BA3 FA3 XA3 I-A3 - P-acc4 BA4 FA4 XA4 - - P-mdist3 B-mdist3 - - - - P-mdist4 B-mdist4 - - - - P-dist3 B-dist3 - - - - P-dist4 B-dist4 - - - -

• Share classes P-acc, P-acc2, P-acc3, P-acc4, P-mdist3, P-mdist4, P-dist3 and P-dist4 for which the management, distribution, administration and depositary fees are charged to the relevant share class. These share classes are available for all investors.

• Share classes BA, BA2, BA3, BA4, B-mdist3, B-mdist4, B-dist3 and B-dist4 for which the

management and distribution fees are charged to the relevant investors (and not to the relevant share class) outside the Company, on the basis of an agreement concluded between the investor and UBS Global Asset Management or one of its authorised delegates. Administration and depositary fees are charged to the relevant share classes. These share classes are reserved to institutional investors having concluded an agreement (such as, but not limited to a portfolio management agreement) with UBS Global Asset Management or one of its authorised delegates.

• Share classes FA, FA2, FA3 and FA4, for which the management, distribution, administration and

depositary fees are charged to the relevant investors (and not to the relevant share class) outside the Company, on the basis of an agreement concluded between the investor and UBS Global Asset Management or one of its authorised delegates. These shares will have an issue price of 10,000 (in each sub-fund’s reference currency). These share classes aim exclusively at financial products (i.e. fund-of-funds or other pooled structures according to various legislations). These share classes have a high initial value aiming at facilitating day-to-day operations of these pooled structures. In addition, they feature the same characteristics as the share classes XA, XA2, XA3 and XA4.

• Share classes XA, XA2, XA3 and XA4, for which the management, distribution, administration and

depositary fees are charged to the relevant investors (and not to the relevant share class), on the basis of an agreement concluded between the investor and UBS Global Asset Management or one of its authorised delegates. These share classes are reserved to institutional investors having concluded an agreement (such as, but not limited to a portfolio management agreement) with UBS Global Asset Management or one of its authorised delegates.

• Share classes with "I-A1" in their name for which the management, distribution, administration and

depositary fees are charged to the relevant share class. These share classes are exclusively reserved for institutional investors within the meaning of Article 174(2)(c) of the Law of 2010. Their smallest tradable unit is 0.001. Unless the Company decides otherwise, the initial issue price of these shares amounts to AUD 100, CAD 100, CHF 100, CZK 2,000, EUR 100, GBP 100, HKD 1,000, JPY 10,000, PLN 500, RMB 1,000, RUB 3,500, SEK 700, SGD 100 or USD 100.

• Share classes with "I-A2" in their name for which the management, distribution, administration and

depositary fees are charged to the relevant share class. These share classes are exclusively reserved for institutional investors within the meaning of Article 174(2)(c) of the Law of 2010. Their smallest tradable unit is 0.001. Unless the Company decides otherwise, the initial issue price of these shares

9

amounts to AUD 100, CAD 100, CHF 100, CZK 2,000, EUR 100, GBP 100, HKD 1,000, JPY 10,000, PLN 500, RMB 1,000, RUB 3,500, SEK 700, SGD 100 or USD 100. The minimum subscription amount for these shares amounts to AUD 10 million, CAD 10 million, CHF 10 million, CZK 200 million, EUR 5 million, GBP 5 million, HKD 80 million, JPY 1 billion, PLN 50 million, RMB 70 million, RUB 350 million, SEK 70 million, SGD 10 million or USD 10 million. Upon subscription, (i) a minimum subscription must be made pursuant to the list above or (ii) be based on a written agreement of the institutional investor with UBS AG - or with one its

authorised counterparties - for total assets managed by UBS or its portfolio in collective capital investments of UBS must be more than CHF 30 million (or the corresponding currency equivalent).

• Share classes with "I-A3" in their name for which the management, distribution, administration and

depositary fees are charged to the relevant share class. These share classes are exclusively reserved for institutional investors within the meaning of Article 174(2)(c) of the Law of 2010. Their smallest tradable unit is 0.001. Unless the Company decides otherwise, the initial issue price of these shares amounts to AUD 100, CAD 100, CHF 100, CZK 2,000, EUR 100, GBP 100, HKD 1,000, JPY 10,000, PLN 500, RMB 1,000, RUB 3,500, SEK 700, SGD 100 or USD 100. The minimum subscription amount for these shares amounts to AUD 30 million, CAD 30 million, CHF 30 million, CZK 600 million, EUR 20 million, GBP 20 million, HKD 240 million, JPY 3 billion, PLN 150 million, RMB 210 million, RUB 1,050 billion, SEK 210 million, SGD 30 million or USD 30 million. Upon subscription, (i) a minimum subscription must be made pursuant to the list above or (ii) be based on a written agreement of the institutional investor with UBS AG - or with one its

authorised counterparties - for total assets managed by UBS or its portfolio in collective capital investments of UBS must be more than CHF 100,000,000 (or the corresponding currency equivalent).

• Share classes with "Q" in their name for which the management, distribution, administration and

depositary fees are charged to the relevant share class. These share classes are available 1) for distribution from an eligible country as defined by “List A”; or 2) to investors domiciled in other countries, if they are professionals of the financial sector and a

written agreement exists with UBS AG; and who make the following investments in their own name and: (a) on their own behalf; (b) on behalf of their clients within a (discretionary) asset management agreement; or (c) on behalf of their clients within the framework of an advisory relationship established in

writing, in return for payment; or (d) on behalf of a collective investment managed by a professional of the financial sector. In cases (b), (c) and (d), said professional has been duly authorised by the supervisory authority to which he/she is subject to carry out such transactions, and is domiciled in an eligible country as defined by “List B” or is operating in their own name and on behalf of another professional of the financial sector who has been authorised in writing by UBS AG and is domiciled in one of the countries covered by “List B” or “List C” in cases (b) and (c) respectively. Admission of investors in further distribution countries (changes to lists A, B and C) shall be decided by the Company at its sole discretion and disclosed on www.ubs.com/funds.

Additional characteristics of share classes:

Currency The share classes may be denominated in AUD, CAD, CHF, CZK, EUR, GBP, HKD, JPY, PLN, RMB, RUB, SEK, SGD or USD.

"hedged" For share classes whose reference currencies are not identical to the currency of account of the sub-fund ("share classes in foreign currencies"), the fluctuation risk of the reference currency price for those share classes is hedged against the currency of account of the sub-fund. Provision is made for the amount of the hedging to be in principle between 90% and 110% of the total net assets of the share class in foreign currency. Changes in the market value of the portfolio, as well as in subscriptions and redemptions of share classes in foreign currencies, can result in the hedging temporarily surpassing the aforementioned range. The hedging described has no effect on possible currency risks resulting from investments denominated in a currency other than the respective sub-fund's currency of account.

RMB denominated

Investors should note that the Renminbi (ISO 4217 currency code: CNY), abbreviated RMB, the official currency of the People's Republic of China (the "PRC"), is traded on two markets,

10

share classes namely as onshore RMB (CNY) in mainland China and offshore RMB (CNH) outside mainland China. Share classes denominated in RMB are shares whose net asset value is calculated in offshore RMB (CNH). Onshore RMB (CNY) is not a freely convertible currency and is subject to foreign exchange control policies and repatriation restrictions imposed by the PRC government. Offshore RMB (CNH), on the other hand, may be traded freely against other currencies, particularly EUR, CHF and USD. This means the exchange rate between offshore RMB (CNH) and other currencies is determined on the basis of supply and demand relating to the respective currency pair. RMB convertibility between offshore RMB (CNH) and onshore RMB (CNY) is a regulated currency process subject to foreign exchange control policies and repatriation restrictions imposed by the PRC government in coordination with offshore regulatory or governmental agencies (e.g. the Hong Kong Monetary Authority). Prior to investing in RMB classes, investors should bear in mind that the requirements relating to regulatory reporting and fund accounting of offshore RMB (CNH) are not clearly regulated. Furthermore, investors should be aware that offshore RMB (CNH) and onshore RMB (CNY) have different exchange rates against other currencies. The value of offshore RMB (CNH) can potentially differ significantly from that of onshore RMB (CNY) due to a number of factors including, without limitation, foreign exchange control policies and repatriation restrictions imposed by the PRC government at certain times, as well as other external market forces. Any devaluation of offshore RMB (CNH) could adversely affect the value of investors' investments in the RMB classes. Investors should therefore take these factors into account when calculating the conversion of their investments and the ensuing returns from offshore RMB (CNH) into their target currency. Prior to investing in RMB classes, investors should also bear in mind that the availability and tradability of RMB classes, and the conditions under which they may be available or traded, depend to a large extent on the political and regulatory developments in the PRC. Thus, no guarantee can be given that offshore RMB (CNH) or the RMB classes will be offered and/or traded in future, nor can there be any guarantee as to the conditions under which offshore RMB (CNH) and/or RMB classes may be made available or traded. In particular, since the currency of account of the relevant sub-funds offering the RMB classes would be in a currency other than offshore RMB (CNH), the ability of the relevant sub-fund to make redemption payments in offshore RMB (CNH) would be subject to the sub-fund's ability to convert its currency of account into offshore RMB (CNH), which may be restricted by the availability of offshore RMB (CNH) or other circumstances beyond the control of the Management Company. Potential investors should be aware of the risks of reinvestment, which could arise if the RMB class has to be liquidated early due to political and/or regulatory circumstances. This does not apply to the reinvestment risk due to liquidation of a share class and/or the sub-fund in accordance with the section "Liquidation of the Company, its sub-funds and share classes".

"acc" For share classes with "-acc" in their name, income is not distributed unless the Company decides otherwise.

"dist" For share classes with "-dist" in their name, income is distributed unless the Company decides otherwise.

"mdist" Shares in classes with "-mdist" in their name may make monthly distributions excluding fees and expenses. They may also make distributions out of capital and realised capital gains. Distributions out of capital shall result in the reduction of an investor’s original capital invested in the sub-fund. Also, any distributions from the income and/or involving the capital and/or capital gains result in an immediate reduction of the net asset value per share of the sub-fund. Investors in certain countries may be subject to higher tax rates on distributed capital than on any capital gains from the sale of fund units. Some investors may therefore choose to invest in the accumulating (-acc) instead of the distributing (-dist, -mdist) share classes. Investors may be taxed at a later point in time on income and capital arising on accumulating (-acc) share classes compared to distributing (-dist) share classes. Investors should seek their own tax advice.

The sum of the sub-funds' net assets forms the total net assets of the Company, which at any time corresponds to the share capital of the Company and consists of fully paid in and non-par-value shares

11

(the "shares"). At general meetings, the shareholder has the right to one vote per share held, irrespective of the difference in value of shares in the respective sub-funds. Shares of a particular sub-fund or class carry the right of one vote per share held when voting at meetings affecting this sub-fund or class. The Company is a single legal entity. For the purpose of the relations as between the shareholders, each sub-fund is deemed to be a separate entity, separate from the others. The assets of a sub-fund are exclusively available to satisfy the requests of that sub-fund and the right of creditors whose claims have arisen in connection with that sub-fund. The Company is empowered to establish new sub-funds and/or to liquidate existing ones at any time or to establish various share classes with specific characteristics within these sub-funds. The current Sales Prospectus shall be updated following the establishing of a new sub-fund or new share class. The Company is unlimited with regard to duration and total assets. Rights of investors vis-à-vis the service providers of the Company Without prejudice to any potential right of action in tort or any potential derivative action, investors in the Company may not have a direct right of recourse against any service providers appointed by the Company or the Management Company as such right of recourse will lie with the relevant contracting counterparty rather than the investors. Equal treatment of shareholders The external AIFM will ensure that investors in the Company are treated fairly. The participation of each shareholder in the Company is represented by shares. Each shares pertaining to the same share class within the same sub-fund bears the same rights and obligations. Therefore equal treatment of all shareholders of the Company holding shares of the same share class within the same sub-fund is ensured. The external AIFM (or any of its delegates) will not enter into any side letter or side arrangement granting a preferential treatment to any investor which, in the reasonable opinion of the external AIFM, could result in an overall material disadvantage to other investors. Investment Objective and Investment Policy of the sub-funds A. UBS (Lux) Institutional SICAV II – China A Opportunity (USD) The investment objective of the sub-fund UBS (Lux) Institutional SICAV II – China A Opportunity (the “sub-fund”) is to achieve high capital gains and a reasonable return, while giving due consideration to capital security and to the liquidity of assets. The sub-fund will invest at least 70% of its total net assets in equities, cooperative society shares and participation shares, participation certificates and warrants of companies which are domiciled in or are chiefly active in the People’s Republic of China (“PRC”). The majority of net assets are invested in Chinese A-shares (as further defined below). Chinese A-shares are shares that are traded at the local Chinese stock market and only Chinese investors or selected institutional investors (which have gained Qualified Foreign Institutional Investor status, “QFII” and/or RMB Qualified Foreign Institutional Investor status, "RQFII") are entitled to invest. The sub-fund may use standardised and non-standardised (customised) derivative financial instruments for hedging purposes. It may conduct such transactions on a stock exchange or other regulated market open to the public, or directly with a bank or financial institution specialising in these types of business as counterparty (OTC trading). The base currency of the sub-fund is USD. The sub-fund is allowed to borrow up to 10% of its net assets for the purpose of cash management only; the short selling of transferable securities is not allowed. A detailed description of the risks connected with an investment in this sub-fund is given under the following sections ‘General Risk Warnings’ and ’Specific Risks when investing in China’. This sub-fund is only suitable for investors who are willing to accept these risks. The maximum amount of leverage for this sub-fund, calculated based on the commitment approach, is 200%. B. UBS (Lux) Institutional SICAV II – Mainland China Fixed Income (USD) The investment objective of the sub-fund UBS (Lux) Institutional SICAV II – Mainland China Fixed Income (USD) (the “sub-fund”) is to achieve capital appreciation and to generate current income by investing primarily in the mainland China fixed income market via QFII / RQFII investment quotas.

12

To achieve its investment objective, the sub-fund shall invest at least 70% of its total net assets in RMB denominated fixed income instruments issued by Chinese government and government-related agencies, Chinese institutions as well as corporations domiciled in China or carrying out a substantial part of their business in China which are traded on an exchange or in the over-the-counter (interbank) market. The sub-fund is further allowed to invest in fixed income securities with attached and/or embedded derivatives. The sub-fund may invest up to 30% of its total net assets in fixed income and money-market instruments issued or dealt in on exchanges or over-the-counter outside of the PRC. The sub-fund is authorised to invest up to 100% of its total net assets in securities and money market instruments from various issues that are guaranteed or issued by Chinese government, government-related agencies or Chinese institutions. These securities or money market instruments must be divided into at least six different issues, with securities or money market instruments from a single issue not exceeding 30% of the total net assets of the sub-fund. The sub-fund shall not invest more than 10% of its net assets in securities issued by the same issuer. Required rating of the securities shall be at least AA (or its equivalent) by a recognised onshore credit rating agency. Where an issue rating from an onshore rating agency is unavailable, the issuer rating will apply. In the absence of both, or in the case of non-mainland China traded instruments, a minimum rating (issue or issuer) of B- (Standard & Poor's or Fitch) or B3 (Moody's) is required. The investments may be made directly and indirectly via derivatives dealt in or on a regulated market or over-the-counter, including but not limited to futures, deliverable and non-deliverable interest rate and currency swaps, currency forwards and credit default swaps. The sub-fund is allowed to borrow up to 10% of its net assets for the purpose of cash management only; the short selling of transferable securities is not allowed. In addition, the sub-fund may invest in or hold on an ancillary basis cash, cash equivalent and money market instruments, including money market funds. The investments in or holding of these asset classes may not exceed 20% of the sub-fund’s total net assets. The maximum amount of leverage for this sub-fund, calculated based on the commitment approach, is 200%. C. UBS (Lux) Institutional SICAV II – China Income (RMB) The investment objective of the sub-fund UBS (Lux) Institutional SICAV II – China Income (RMB) (the “sub-fund”) is to achieve capital appreciation and to generate income by investing primarily in the onshore China fixed income market via QFII/RQFII investment quotas, with a primary focus on RMB denominated fixed income instruments issued by governments, institutions and corporations in China that are traded in the China interbank bond market ("CIBM") or the exchange traded bond market. To achieve its investment objective, the sub-fund shall invest at least 90% of its total net assets in RMB denominated fixed income instruments that are traded in the CIBM or in the exchange traded market. These instruments may include, but are not limited to, securities issued by governments, government related entities, banks, corporate entities and other institutions within China that are permitted to be traded in the CIBM or the exchange traded market via RQFII quota. The sub-fund is authorised to invest up to 10% of its total net assets in cash or fixed income instruments issued or listed outside mainland China. The sub-fund is authorised to invest up to 100% of its total net assets in securities and money market instruments from various issues that are guaranteed or issued by Chinese government, government-related agencies or other Chinese entities. These securities or money market instruments must be divided into at least six different issues, with securities or money market instruments from a single issue not exceeding 30% of the total net assets of the sub-fund. The sub-fund shall not invest more than 10% of its net assets in securities issued by the same issuer.

13

Required rating of the securities shall be at least AA- (or its equivalent) by a recognised onshore credit rating agency. Where an issue rating from an onshore rating agency is unavailable, the issuer rating will apply. In the absence of both, or in the case of non-mainland China traded instruments, a minimum rating (issue or issuer) of B- (Standard & Poor's or Fitch) or B3 (Moody's) is required. The maximum amount of leverage for this sub-fund, calculated based on the commitment approach, is 110%. The sub-fund is allowed to borrow up to 10% of its net assets for the purpose of cash management only; the short selling of transferable securities is not allowed. Procedures for changing the investment strategy and/or policy of the Company or sub-funds UBS has established internal departments tasked with monitoring and, where applicable, changing the investment strategy and/or policy of the sub-funds. If the performance of certain sub-funds is unsatisfactory and this does not appear to be a temporary trend, the Product Development department shall initiate changes to the investment strategy and/or policy of the sub-fund in question to the degree deemed necessary. The changes contemplated by the Product Development department shall be presented to the internal departments and/or functions (in particular the Portfolio Management, Operations, Legal and Compliance departments) involved in the investment strategy and/or policy amendment process in order to assess their feasibility. Insofar and as soon as the feasibility of the contemplated changes has been confirmed by all relevant departments, the initiative shall be presented and submitted for approval to the Company's Board of Directors. Insofar and as soon as this approval has been granted, the intended changes shall be submitted to the CSSF. Insofar and as soon as the CSSF gives its approval, the affected investors shall be notified of the intended changes and, where applicable, granted a one-month period in which they may choose to redeem their shares free of charge, in accordance with the provisions of the section entitled "Information to shareholders". Hedged share classes Where undertaken, the effects of hedging will be reflected in the net asset value and, therefore, in the performance of such share class. Similarly, any expenses arising from such hedging transactions will be borne by the share class in relation to which they have been incurred. Such hedging is undertaken with the intention of protecting investors in the relevant share class against a decrease in the value of the reference currency of the relevant sub-fund against the currency of this share class. On the other hand, currency hedging may preclude investors from benefiting from an increase in the value of the reference currency of the sub-fund. It is to be noted that hedging at share class level does not aim at hedging fluctuations in the currencies of the investments held by the relevant sub-fund. Use of derivatives While observing the restrictions stipulated in the chapter "Investment Restrictions", the Company may employ derivative financial instruments for each sub-fund. Derivative financial instruments are instruments that derive their value from other finance instruments (so-called underlyings). Derivatives may be conditional or unconditional. Conditional derivatives (contingent claims) are those that give a party to the legal transaction the right, but not the obligation, to use a derivative instrument (e.g. an option). Unconditional derivatives (future commitments) impose the obligation on both parties to provide the service owed at a specific time defined in the contract (e.g. forwards, futures, swaps).The derivatives are traded on stock exchanges (exchange-traded derivatives), as well as over the counter (OTC derivatives). In the case of derivatives traded on a stock exchange (e.g. futures), the stock exchange itself is one of the parties in each transaction. While these transactions are cleared and settled through a clearing house, OTC derivatives (e.g. forwards and swaps) are entered into, cleared and settled directly by the parties to the transaction. Risk management Risk management in accordance with the commitment approach is applied pursuant to the applicable laws and regulatory provisions. A description of additional risk management techniques (e.g. management of counterparty risk) can be found in the relevant sections of the Sales Prospectus. Liquidity management Within the framework of liquidity management, the Management Company shall ensure that the Company's liquidity profile remains in line with its investments and that the redemption orders of investors - with the exception of the special cases provided for by the supervisory authority or this Sales Prospectus - can be

14

processed at all times. A description of additional liquidity management techniques (e.g. temporary suspension in the processing of redemption orders under certain circumstances and processes regarding the regular subscription, redemption and conversion cycles) can be found in the relevant sections of the Sales Prospectus. Collateral Management If the Company enters into OTC transactions, it may be exposed to risks related to the creditworthiness of the OTC counterparties: when the Company enters into forwards contracts, OTC options or uses other OTC derivative techniques, it is subject to the risk that an OTC counterparty may not meet (or cannot meet) its obligations under a specific or multiple contracts. Counterparty risk can be reduced by depositing a security (“collateral”, see above). Collateral may be provided in the form of cash in highly liquid currencies, highly liquid equities and first- class government bonds. The Company will only accept such financial instruments as collateral that would allow it (after objective and appropriate valuation) to liquidate them within an appropriate time period. The Company, or a service provider appointed by the Company, must valuate the value of the collateral at least once a day. The value of the collateral must be higher than the value of the position of the respective OTC counterparty. However, this value may fluctuate between two consecutive valuations. After each valuation, however, it is ensured (where appropriate by calling additional collateral) that the collateral is increased by an amount sufficient to reach the value of the respective OTC counterparty's exposure (mark-to-market). In order to adequately take into account the risks related to the collateral in question, the Company determines whether the value of the collateral to be received should be increased, or whether the value of the collateral received is to be cut by an appropriate, conservatively measured amount (haircut). The larger the collateral's value may fluctuate, the higher the haircut must be. The haircut is highest for equities. Securities deposited as collateral must not have been issued by the OTC counterparty with which the relevant OTC transaction is to be entered into or have a high correlation with it. For this reason, shares from the finance sector are not accepted as collateral. Securities deposited as collateral are held by the Depositary in favour of the Company and may not be sold, invested or pledged by the Company. Collateral may not be re-used. Bankruptcy and insolvency events or other credit events with the Depositary or within their sub-custodian/correspondent bank network may result in the rights of the Company in connection with the security to be delayed or restricted in other ways. If the Company is owed a security pursuant to an applicable agreement, then any such security is to be transferred to the OTC counterparty as agreed between the Company and the OTC counterparty. Bankruptcy and insolvency events or other credit events with the OTC counterparty, the Depositary or within their sub-custodian/correspondent bank network may result in the rights or recognition of the Company in connection with the security to be delayed, restricted or even eliminated, which would go so far as to force the Company to fulfil its obligations in the framework of the OTC transaction, in spite of any security that had previously been made available to cover any such obligation. The Company shall decide on an internal framework agreement that determines the details of the above-mentioned requirements and values, particularly regarding the types of collateral accepted, the amounts to be added to and subtracted from the respective collateral, as well as the investment policy for liquid funds that are deposited as collateral. This framework agreement is reviewed and adapted where appropriate by the Company on a regular basis. Leverage For the purpose of this Sales Prospectus, "Leverage" means any method by which the exposure of the Company or a sub-fund is increased through borrowing of cash or securities, or leverage embedded in derivative position or by any other means. The Company may employ external funds within the framework of the maximum permissible leverage per sub-fund. The profit and loss potential is thereby increased, meaning that the value appreciation of these investments leads to the Company's net assets growing more quickly than would have been the case without leverage. Conversely, a decrease in value causes the Company's assets to fall more quickly than without leverage. The maximum permitted amount of the leverage that can be built up by each sub-fund and which is calculated using the commitment approach can be found in the investment policy of the relevant sub-fund. General Risk Warnings Market Risk: The investments of the Company are subject to normal market fluctuations and the risks inherent in equity or fixed-income securities and similar instruments and there can be no assurances that appreciation will occur. The price of shares can go down as well as up and investors may not realise their initial investment.

15

Although the Portfolio Manager will attempt to restrict the exposure of the Company to market movements, there is no guarantee that this strategy will be successful. Emerging Markets: Emerging markets are at an early stage of development and suffer from increased risk of expropriation, nationalisation and social, political and economic insecurity. There follows an overview of the general risks entailed by involvement in the emerging markets: - Counterfeit securities - due to the weakness in supervisory structures, securities purchased by the

sub-fund may be counterfeit. Hence it is possible to suffer losses. - Liquidity difficulties - the buying and selling of securities can be costlier, lengthier and in general

more difficult than is the case in more developed markets. Difficulties with liquidity can also increase price volatility. Many emerging markets are small, have low trading volumes and suffer from low liquidity and high price volatility.

- Currency fluctuations - the currencies of countries in which the sub-fund invests, compared with the currency of account of the sub-fund, can undergo substantial fluctuations once the sub-fund has invested in these currencies. Such fluctuations may have a significant effect on the relevant sub-fund's income. It is not possible to apply currency risk hedging techniques to all currencies in emerging market countries.

- Currency export restrictions - it cannot be excluded that emerging markets limit or temporarily suspend the export of currencies. Consequently, it may not be possible for the sub-fund to repatriate sales proceeds without delays.

- Settlement and custody risks - the settlement and custody systems in emerging market countries are not as well developed as those in developed markets. Standards are not as high and the supervisory authorities not as experienced. Consequently, settlement may be delayed, thereby posing disadvantages for liquidity and securities.

- Restrictions on buying and selling - in some cases, emerging markets can place restrictions on the buying of securities by foreign investors. Some securities are thus not available to the sub-fund because the maximum number allowed to be held by foreign unitholders has been exceeded. In addition, the participation of foreign investors in the net income, capital and distributions may be subject to restrictions or government approval. Emerging markets may also limit the sale of securities by foreign investors. Should the sub-fund be barred due to such a restriction from selling its securities in an emerging market, it will try to obtain an exceptional approval from the authorities responsible or to counter the negative impact of this restriction through its investments in other markets. The sub-fund will only invest in markets in which the restrictions are acceptable. However, it is not possible to prevent additional restrictions from being imposed.

- Accounting - the accounting, auditing and reporting standards, methods, practices and disclosures required by companies in emerging markets differ from those in developed markets in respect of content, quality and the deadlines for providing information to investors. It may thus be difficult to correctly evaluate the investment options.

For these reasons, sub-funds having a high degree of exposure to emerging markets are especially suitable for risk-conscious investors. Currency Risk: The shares may be denominated in different currencies and shares will be issued and redeemed in those currencies. Certain of the assets of the Company may, however, be invested in securities and other investments which are denominated in other currencies. Accordingly, the value of such assets may be affected favourably or unfavourably by fluctuations in currency rates. The Company will be subject to foreign exchange risks. The Company may engage in currency hedging but there can be no guarantee that such a strategy will prevent losses. In addition, prospective investors whose assets and liabilities are predominantly in other currencies should take into account the potential risk of loss arising from fluctuations in value between the reference currency of a sub-fund and such other currencies. Risks connected with the use of derivatives: Investments in derivatives are subject to general market risk, settlement risk, credit risk and liquidity risk. However, the nature of these risks may be altered as a result of the special features of the derivative financial instruments, and may in some cases be higher than the risks associated with an investment in the underlying instrument. For this reason, the use of derivatives requires not only an understanding of the underlying instrument, but

16

also in-depth knowledge of the derivatives themselves. With derivatives, the credit risk is the risk that a party may not meet (or cannot meet) its obligations under a specific or multiple contracts. The credit risk for derivatives traded on a stock exchange is, generally speaking, lower than that of derivatives traded over-the-counter on the open market, because the clearing agent that acts as counterparty of every market-traded derivative (see above) accepts a settlement guarantee. To reduce the overall risk of default, the guarantee is supported by a daily payment system maintained by the clearing agent, in which the assets required for cover are calculated (see below). Despite derivatives not possessing any such settlement guarantee, their default risk is generally limited by the investment restrictions set out in the section entitled "Investment Restrictions".. Even in cases where the difference between the mutually owed payments (e.g. interest rate swaps, total return swaps) is owed, as opposed to the delivery or exchange of the underlying assets (e.g. options, forwards, credit default swaps), the sub-fund's potential loss is limited to this difference in the event of default by the counterparty. The credit risk can be reduced by depositing collateral. To trade derivatives on a stock exchange, participants must deposit collateral with a clearing agent in the form of liquid funds (initial margin). The clearing agent will evaluate (and settle, where appropriate) the outstanding positions of each participant, as well as re-evaluate the existing collateral on a daily basis. If the collateral's value falls below a certain threshold (maintenance margin), the participant in question will be required by the clearing agent to bring this value up to its original level by paying in additional collateral (variation margin). With OTC derivatives, this credit risk may also be reduced by the respective counterparty providing collateral (see below), by offsetting different derivative positions that were entered into with this counterparty, as well as through a careful selection process for counterparties (see the section entitled "Investment Restrictions"). There are also liquidity risks, as it may be difficult to buy or sell certain instruments. When derivative transactions are particularly large, or the corresponding market is illiquid (as may be the case with derivatives traded over-the-counter on the open market), it may in some cases not always be possible to fully execute a transaction, or else it may only be possible to liquidate a position subject to high costs. Other risks associated with the use of derivatives include the risk of incorrectly valuing or determining the price of derivatives. There is also the possibility that derivatives do not completely correlate with their underlying assets, interest rates or indices. Many derivatives are complex and are frequently subjectively valued. Inappropriate valuations can result in higher cash payment requirements in relation to counterparties or in a loss of value for the respective sub-fund. Short selling: Short selling can involve greater risk than investment based on a long position. A short sale of a security involves the risk of a theoretically unlimited increase in the market price of the security, which could result in an inability to cover the short position and a theoretical loss up to the whole investment in the relevant sub-fund. Credit Risk: Sub-funds will be subject to credit risk with respect to the counterparties with which it enters into any transactions. If a counterparty becomes insolvent or otherwise fails to perform its obligations, the sub-fund may experience significant delays in obtaining any recovery in an insolvency, bankruptcy, or other reorganization proceeding. The sub-fund may obtain only a limited recovery or may obtain no recovery in such circumstances, at all. Specific Risks when investing in China For the purposes of this section, references to the sub-fund refers to each relevant sub-fund investing in QFII/ RQFII permissible securities through Portfolio's Manager(s)' QFII and/or RQFII quota. a) China Market Risk Investing in the securities markets in the PRC is subject to the risks of investing in emerging markets generally and the risks specific to the PRC market. Many of the PRC economic reforms are unprecedented or experimental and are subject to adjustment and modification, and such adjustment and modification may not always have a positive effect on foreign investment in joint stock companies in the PRC or in listed securities such as Chinese A-shares ("A-shares").

17

A sub-fund is not a bank deposit and is not guaranteed. There is no guarantee of the repayment of the principal investment. The profitability of the investments of a sub-fund could be adversely affected by a worsening of general economic conditions in the PRC or global markets. Factors such as PRC government policy, fiscal policy, interest rates, inflation, investor sentiment, the availability and cost of credit, the liquidity of the PRC financial markets and the level and volatility of equity prices could significantly affect the value of a sub-fund's underlying investments and thus the share price. The choice of A-shares currently available to the Portfolio Manager may be limited as compared with the choice available in other markets. There may also be a lower level of liquidity in the A-share markets, which are relatively smaller in terms of both combined total market value and the number of shares which are available for investment as compared with other markets. This could potentially lead to severe price volatility. The national regulatory and legal framework for capital markets and joint stock companies in the PRC are still developing when compared with those of developed countries. However, the effects of such reform on the A-share market as a whole remain to be seen. In addition, there is a relatively low level of regulation and enforcement activity in these securities markets. Settlement of transactions may be subject to delay and administrative uncertainties. Further, regulations continue to develop and may change without notice which may further delay redemptions or restrict liquidity. There may not be regulation and monitoring of the Chinese securities markets and activities of investors, brokers and other participants equivalent to that in certain more developed markets. PRC companies are required to follow PRC accounting standards and practice which, to a certain extent, follow international accounting standards. However, there may be significant differences between financial statements prepared by accountants following PRC accounting standards and practice and those prepared in accordance with international accounting standards. Both the Shanghai and Shenzhen securities markets are in the process of development and change. This may lead to trading volatility, difficulty in the settlement and recording of transactions and difficulty in interpreting and applying the relevant regulations. The PRC government has been developing a comprehensive system of commercial laws and considerable progress has been made in the promulgation of laws and regulations dealing with economic matters such as corporate organization and governance, foreign investment, commerce, taxation and trade. Because these laws, regulations and legal requirements are relatively recent, their interpretation and enforcement involve uncertainties. In addition, the PRC laws for investor protection are still in developing stage and may be less sophisticated than those in developed countries. Investments in the PRC will be sensitive to any significant change in political, social or economic policy in the PRC. Such sensitivity may, for the reasons specified above, adversely affect the capital growth and thus the performance of these investments. The PRC government’s control of currency conversion and future movements in exchange rates may adversely affect the operations and financial results of the companies invested in by a sub-fund. In light of the above mentioned factors, the price of A-shares may fall significantly in certain circumstances. b) QFII / RQFII Risk QFII / RQFII Quota Under the prevailing regulations in the PRC, foreign investors can invest in the A-share market and other QFII / RQFII permissible securities through institutions that have obtained qualified status such as QFII and/or RQFII status in the PRC. The current QFII and RQFII regulations impose strict restrictions (such as investment guidelines) on A-share investments. The sub-funds themselves are not a QFII nor RQFII, but may invest directly in A-shares and other QFII / RQFII permissible securities via the QFII and/or RQFII status of the Portfolio Manager. All or most of the sub-fund's investments in the PRC will be made and held through the Portfolio Manager(s)' QFII and/or RQFII quota. All or most of the China A Opportunity (USD) sub-fund’s investment in the PRC are intended to be made and held through the (i) QFII quotas of both UBS Global Asset Management (Singapore) Ltd. and UBS Global

18

Asset Management (Hong Kong) Limited, and/or (ii) the RQFII quota of UBS Global Asset Management (Hong Kong) Limited. All or most of the Mainland China Fixed Income (USD) sub-fund’s investment in the PRC is intended to be made and held through the QFII quota and/or RQFII quota of UBS Global Asset Management (Hong Kong) Limited. All or most of the China Income (RMB) sub-fund’s investment in the PRC is intended to be made and held through the QFII and/or RQFII quota of UBS Global Asset Management (Hong Kong) Limited. Potential investors should note that there is no guarantee that any of the sub-funds will continue to benefit from the QFII / RQFII quota(s) of the relevant Portfolio Manager nor that it will be made exclusively available to any of the sub-funds. The sub-fund may also seek exposure to QFII/RQFII permissible securities through QFII / RQFII quotas granted to other QFIIs / RQFIIs. The Portfolio Manager has assumed dual roles as the Portfolio Manager of the sub-fund and the holder of the QFII / RQFII quota applicable to the sub-fund. The Portfolio Manager will ensure all transactions and dealings will be dealt with having regard to the constitutive documents of the sub-fund as well as the relevant laws and regulations applicable to the Portfolio Manager. In the event that conflicts of interest arise, the Company will in conjunction with the Depositary and PRC Sub-Custodian (as defined below) seek to ensure that the sub-fund is managed in the best interests of shareholders and the shareholders are treated fairly. There can be no assurance that the Portfolio Manager will be able to allocate a sufficient portion of its QFII and/or RQFII quota to meet all applications for subscription to the sub-fund, or that redemption requests can be processed in a timely manner due to adverse changes in relevant laws or regulations, including changes in QFII / RQFII repatriation restrictions. Such restrictions may result in suspension of dealings of the sub-fund. QFII / RQFII restrictions on investment apply to the quota granted to a QFII / RQFII as a whole and not simply to investments made by the sub-fund. Consequently, investors should be aware that violations of the QFII / RQFII regulations on investment arising out of activities related to portions of the investment quota allocated to another client of the QFII / RQFII or another sub-fund through whom the sub-fund invests could result in the revocation of or other regulatory action in respect of the investment quota of the QFII / RQFII as a whole, including any portion utilised by the sub-fund. Likewise, limits on investment in A-shares, and the regulations relating to the repatriation of capital and profits may apply in relation to the quota held by the Portfolio Manager as a whole. Hence the ability of the sub-fund to make investments and/or repatriate monies from the Portfolio Manager's QFII and/or RQFII quota may be affected adversely by the investments, performance and/or repatriation of monies invested by other investors or other sub-fund(s) utilising the Portfolio Manager's QFII and/or RQFII quota. Should the Portfolio Manager lose its QFII / RQFII status or retire or be removed, or the Portfolio Manager’s QFII / RQFII quota be revoked or reduced, the sub-fund may not be able to invest in A-shares or other QFII / RQFII permissible securities through the Portfolio Manager’s QFII / RQFII quota, and the sub-fund may be required to dispose of its holdings, which would likely have a material adverse effect on such sub-fund. Investors should note that the Portfolio Manager's QFII and/or RQFII quota is subject to a minimum asset allocation (as a percentage of aggregate investment in QFII / RQFII permissible securities or otherwise required/agreed/prescribed by PRC regulators) as required/agreed/prescribed by PRC regulators. Accordingly for sub-funds that invest in QFII / RQFII permissible securities, the implementation of their respective investment policy is restricted by such asset allocation requirement which applies at an aggregated level among all sub-funds utilizing the same Portfolio Manager's QFII and/or RQFII quota. For example, without limitation, the QFII quota of UBS Global Asset Management (Hong Kong) Limited is currently subject to a minimum allocation in equity or equity related securities (in terms of aggregate investment in QFII permissible securities) as required/agreed/prescribed by PRC regulators and with respect to the Mainland China Fixed Income (USD) sub-fund: (i) it could be restricted from making further investments in fixed income products in the PRC; or (ii) it is required to, without prior notification to the shareholders, liquidate its investments in fixed income products in the PRC regardless of the prevailing market conditions and compulsorily redeem the shares of the Mainland China Fixed Income (USD) sub-fund on a pro rata basis among shareholders, if the QFII quota of

19