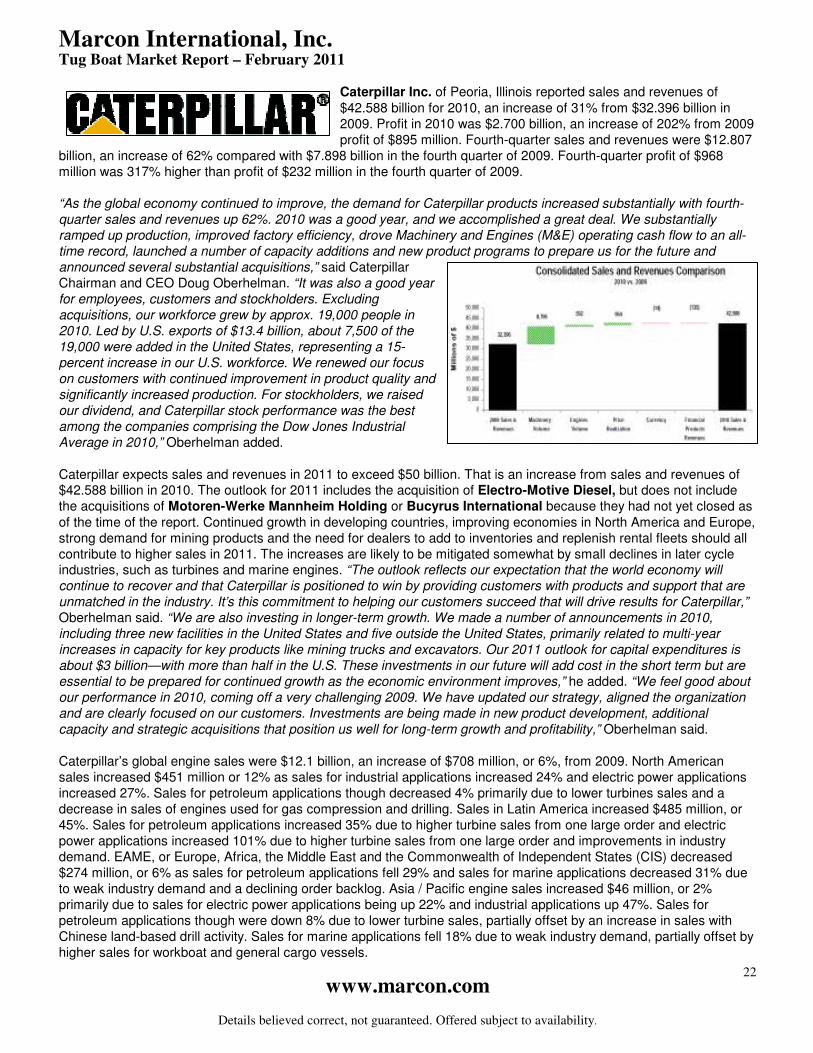

tug boat market report - february 2011.pdf

TRANSCRIPT

Marcon International, Inc. Vessels and Barges for Sale or Charter Worldwide

1 www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

P.O. Box 1170, 9 NW Front Street, Suite 201 Coupeville, WA 98239 U.S.A. Telephone (360) 678 8880 Fax (360) 678-8890 E Mail: [email protected] http://www.marcon.com

February 2011

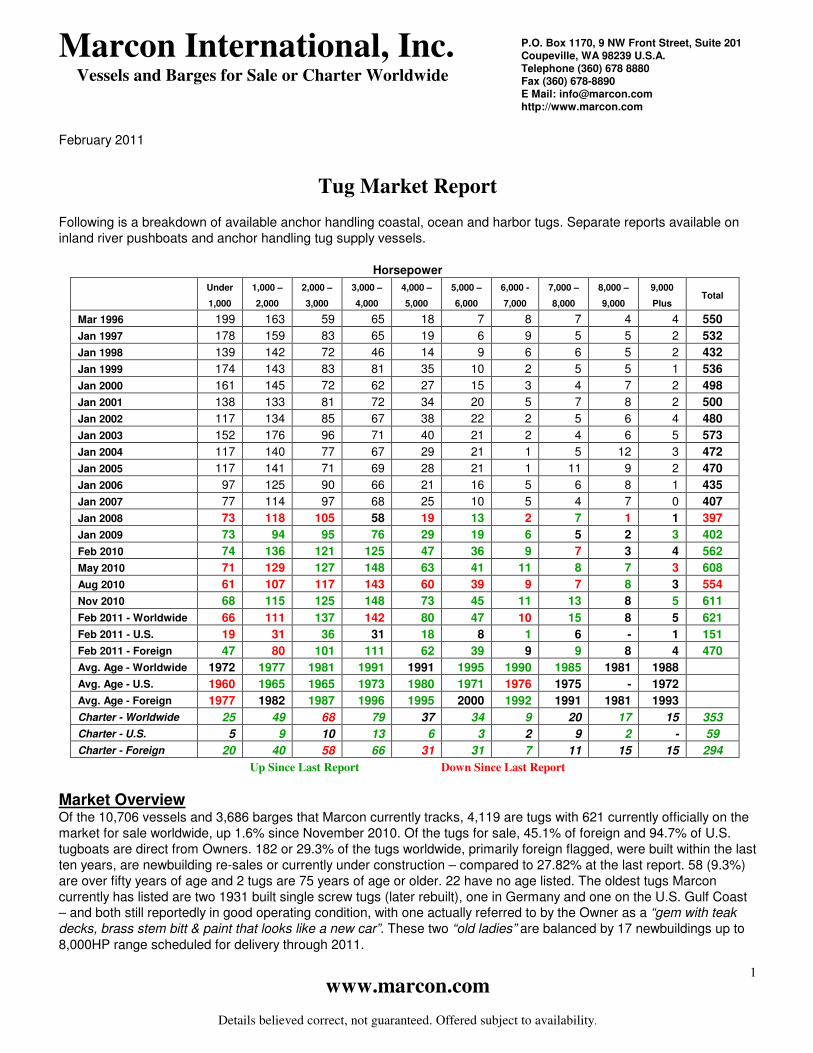

Tug Market Report Following is a breakdown of available anchor handling coastal, ocean and harbor tugs. Separate reports available on inland river pushboats and anchor handling tug supply vessels.

Horsepower

Under

1,000

1,000 –

2,000

2,000 –

3,000

3,000 –

4,000

4,000 –

5,000

5,000 –

6,000

6,000 -

7,000

7,000 –

8,000

8,000 –

9,000

9,000

Plus Total

Mar 1996 199 163 59 65 18 7 8 7 4 4 550

Jan 1997 178 159 83 65 19 6 9 5 5 2 532

Jan 1998 139 142 72 46 14 9 6 6 5 2 432

Jan 1999 174 143 83 81 35 10 2 5 5 1 536

Jan 2000 161 145 72 62 27 15 3 4 7 2 498

Jan 2001 138 133 81 72 34 20 5 7 8 2 500

Jan 2002 117 134 85 67 38 22 2 5 6 4 480

Jan 2003 152 176 96 71 40 21 2 4 6 5 573

Jan 2004 117 140 77 67 29 21 1 5 12 3 472

Jan 2005 117 141 71 69 28 21 1 11 9 2 470

Jan 2006 97 125 90 66 21 16 5 6 8 1 435

Jan 2007 77 114 97 68 25 10 5 4 7 0 407

Jan 2008 73 118 105 58 19 13 2 7 1 1 397

Jan 2009 73 94 95 76 29 19 6 5 2 3 402

Feb 2010 74 136 121 125 47 36 9 7 3 4 562

May 2010 71 129 127 148 63 41 11 8 7 3 608

Aug 2010 61 107 117 143 60 39 9 7 8 3 554

Nov 2010 68 115 125 148 73 45 11 13 8 5 611

Feb 2011 - Worldwide 66 111 137 142 80 47 10 15 8 5 621

Feb 2011 - U.S. 19 31 36 31 18 8 1 6 - 1 151

Feb 2011 - Foreign 47 80 101 111 62 39 9 9 8 4 470

Avg. Age - Worldwide 1972 1977 1981 1991 1991 1995 1990 1985 1981 1988

Avg. Age - U.S. 1960 1965 1965 1973 1980 1971 1976 1975 - 1972

Avg. Age - Foreign 1977 1982 1987 1996 1995 2000 1992 1991 1981 1993

Charter - Worldwide 25 49 68 79 37 34 9 20 17 15 353

Charter - U.S. 5 9 10 13 6 3 2 9 2 - 59

Charter - Foreign 20 40 58 66 31 31 7 11 15 15 294

Up Since Last Report Down Since Last Report

Market Overview Of the 10,706 vessels and 3,686 barges that Marcon currently tracks, 4,119 are tugs with 621 currently officially on the market for sale worldwide, up 1.6% since November 2010. Of the tugs for sale, 45.1% of foreign and 94.7% of U.S. tugboats are direct from Owners. 182 or 29.3% of the tugs worldwide, primarily foreign flagged, were built within the last ten years, are newbuilding re-sales or currently under construction – compared to 27.82% at the last report. 58 (9.3%) are over fifty years of age and 2 tugs are 75 years of age or older. 22 have no age listed. The oldest tugs Marcon currently has listed are two 1931 built single screw tugs (later rebuilt), one in Germany and one on the U.S. Gulf Coast – and both still reportedly in good operating condition, with one actually referred to by the Owner as a “gem with teak decks, brass stem bitt & paint that looks like a new car”. These two “old ladies” are balanced by 17 newbuildings up to 8,000HP range scheduled for delivery through 2011.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

2

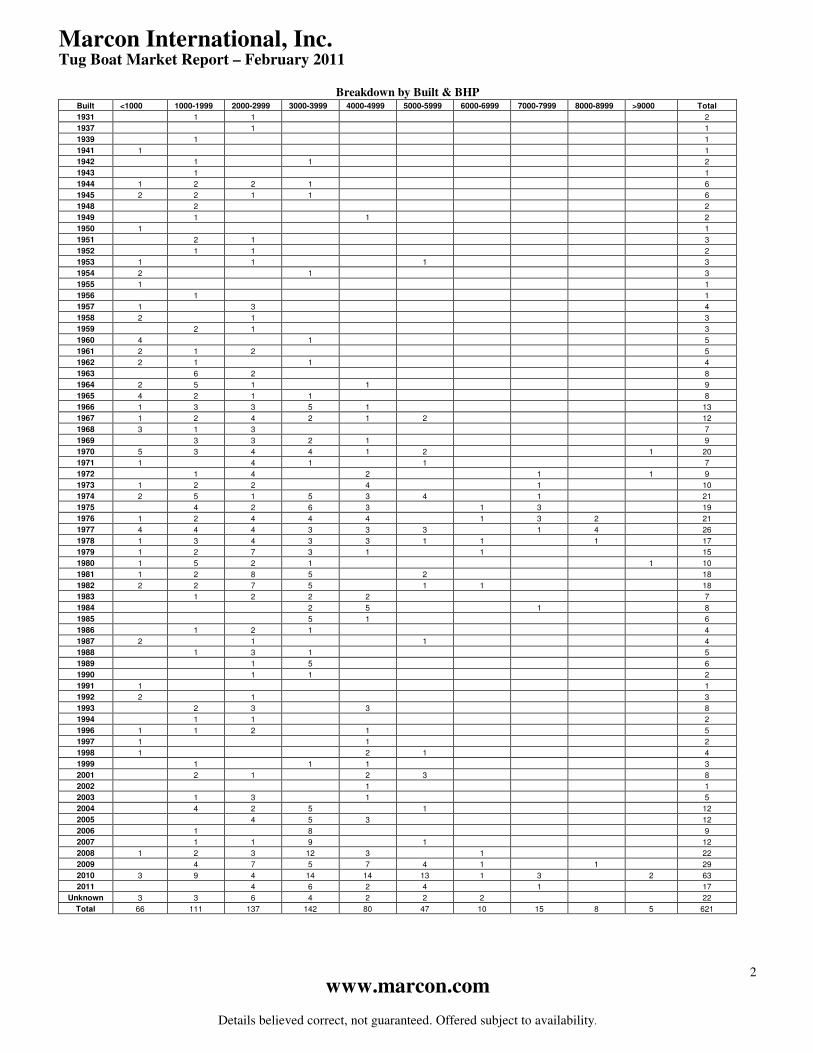

Breakdown by Built & BHP Built <1000 1000-1999 2000-2999 3000-3999 4000-4999 5000-5999 6000-6999 7000-7999 8000-8999 >9000 Total

1931 1 1 2

1937 1 1

1939 1 1

1941 1 1

1942 1 1 2

1943 1 1

1944 1 2 2 1 6

1945 2 2 1 1 6

1948 2 2

1949 1 1 2

1950 1 1

1951 2 1 3

1952 1 1 2

1953 1 1 1 3

1954 2 1 3

1955 1 1

1956 1 1

1957 1 3 4

1958 2 1 3

1959 2 1 3

1960 4 1 5

1961 2 1 2 5

1962 2 1 1 4

1963 6 2 8

1964 2 5 1 1 9

1965 4 2 1 1 8

1966 1 3 3 5 1 13

1967 1 2 4 2 1 2 12

1968 3 1 3 7

1969 3 3 2 1 9

1970 5 3 4 4 1 2 1 20

1971 1 4 1 1 7

1972 1 4 2 1 1 9

1973 1 2 2 4 1 10

1974 2 5 1 5 3 4 1 21

1975 4 2 6 3 1 3 19

1976 1 2 4 4 4 1 3 2 21

1977 4 4 4 3 3 3 1 4 26

1978 1 3 4 3 3 1 1 1 17

1979 1 2 7 3 1 1 15

1980 1 5 2 1 1 10

1981 1 2 8 5 2 18

1982 2 2 7 5 1 1 18

1983 1 2 2 2 7

1984 2 5 1 8

1985 5 1 6

1986 1 2 1 4

1987 2 1 1 4

1988 1 3 1 5

1989 1 5 6

1990 1 1 2

1991 1 1

1992 2 1 3

1993 2 3 3 8

1994 1 1 2

1996 1 1 2 1 5

1997 1 1 2

1998 1 2 1 4

1999 1 1 1 3

2001 2 1 2 3 8

2002 1 1

2003 1 3 1 5

2004 4 2 5 1 12

2005 4 5 3 12

2006 1 8 9

2007 1 1 9 1 12

2008 1 2 3 12 3 1 22

2009 4 7 5 7 4 1 1 29

2010 3 9 4 14 14 13 1 3 2 63

2011 4 6 2 4 1 17

Unknown 3 3 6 4 2 2 2 22

Total 66 111 137 142 80 47 10 15 8 5 621

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

3

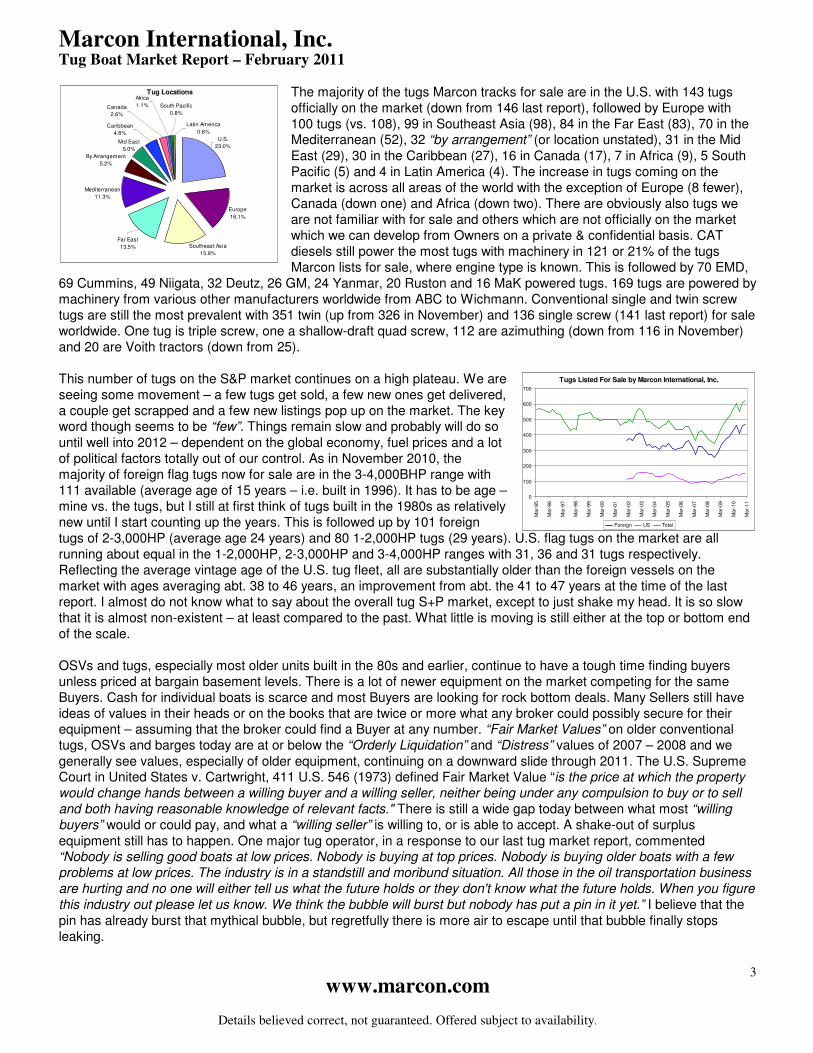

Tug Locations

U.S.

23.0%

Europe

16.1%

By Arrangement

5.2%

Caribbean

4.8%

Canada

2.6%

Far East

13.5%

Africa

1.1%

Southeast Asia

15.9%

Mediterranean

11.3%

Mid East

5.0%

Latin America

0.6%

South Pacific

0.8%

Tugs Listed For Sale by Marcon International, Inc.

0

100

200

300

400

500

600

700

Ma

r-9

5

Ma

r-9

6

Ma

r-9

7

Ma

r-9

8

Ma

r-9

9

Ma

r-0

0

Ma

r-0

1

Ma

r-0

2

Ma

r-0

3

Ma

r-0

4

Ma

r-0

5

Ma

r-0

6

Ma

r-0

7

Ma

r-0

8

Ma

r-0

9

Ma

r-1

0

Ma

r-1

1

Foreign US Total

The majority of the tugs Marcon tracks for sale are in the U.S. with 143 tugs officially on the market (down from 146 last report), followed by Europe with 100 tugs (vs. 108), 99 in Southeast Asia (98), 84 in the Far East (83), 70 in the Mediterranean (52), 32 “by arrangement” (or location unstated), 31 in the Mid East (29), 30 in the Caribbean (27), 16 in Canada (17), 7 in Africa (9), 5 South Pacific (5) and 4 in Latin America (4). The increase in tugs coming on the market is across all areas of the world with the exception of Europe (8 fewer), Canada (down one) and Africa (down two). There are obviously also tugs we are not familiar with for sale and others which are not officially on the market which we can develop from Owners on a private & confidential basis. CAT diesels still power the most tugs with machinery in 121 or 21% of the tugs Marcon lists for sale, where engine type is known. This is followed by 70 EMD,

69 Cummins, 49 Niigata, 32 Deutz, 26 GM, 24 Yanmar, 20 Ruston and 16 MaK powered tugs. 169 tugs are powered by machinery from various other manufacturers worldwide from ABC to Wichmann. Conventional single and twin screw tugs are still the most prevalent with 351 twin (up from 326 in November) and 136 single screw (141 last report) for sale worldwide. One tug is triple screw, one a shallow-draft quad screw, 112 are azimuthing (down from 116 in November) and 20 are Voith tractors (down from 25). This number of tugs on the S&P market continues on a high plateau. We are seeing some movement – a few tugs get sold, a few new ones get delivered, a couple get scrapped and a few new listings pop up on the market. The key word though seems to be “few”. Things remain slow and probably will do so until well into 2012 – dependent on the global economy, fuel prices and a lot of political factors totally out of our control. As in November 2010, the majority of foreign flag tugs now for sale are in the 3-4,000BHP range with 111 available (average age of 15 years – i.e. built in 1996). It has to be age – mine vs. the tugs, but I still at first think of tugs built in the 1980s as relatively new until I start counting up the years. This is followed up by 101 foreign tugs of 2-3,000HP (average age 24 years) and 80 1-2,000HP tugs (29 years). U.S. flag tugs on the market are all running about equal in the 1-2,000HP, 2-3,000HP and 3-4,000HP ranges with 31, 36 and 31 tugs respectively. Reflecting the average vintage age of the U.S. tug fleet, all are substantially older than the foreign vessels on the market with ages averaging abt. 38 to 46 years, an improvement from abt. the 41 to 47 years at the time of the last report. I almost do not know what to say about the overall tug S+P market, except to just shake my head. It is so slow that it is almost non-existent – at least compared to the past. What little is moving is still either at the top or bottom end of the scale. OSVs and tugs, especially most older units built in the 80s and earlier, continue to have a tough time finding buyers unless priced at bargain basement levels. There is a lot of newer equipment on the market competing for the same Buyers. Cash for individual boats is scarce and most Buyers are looking for rock bottom deals. Many Sellers still have ideas of values in their heads or on the books that are twice or more what any broker could possibly secure for their equipment – assuming that the broker could find a Buyer at any number. “Fair Market Values” on older conventional tugs, OSVs and barges today are at or below the “Orderly Liquidation” and “Distress” values of 2007 – 2008 and we generally see values, especially of older equipment, continuing on a downward slide through 2011. The U.S. Supreme Court in United States v. Cartwright, 411 U.S. 546 (1973) defined Fair Market Value “is the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts." There is still a wide gap today between what most “willing buyers” would or could pay, and what a “willing seller” is willing to, or is able to accept. A shake-out of surplus equipment still has to happen. One major tug operator, in a response to our last tug market report, commented “Nobody is selling good boats at low prices. Nobody is buying at top prices. Nobody is buying older boats with a few problems at low prices. The industry is in a standstill and moribund situation. All those in the oil transportation business are hurting and no one will either tell us what the future holds or they don't know what the future holds. When you figure this industry out please let us know. We think the bubble will burst but nobody has put a pin in it yet.” I believe that the pin has already burst that mythical bubble, but regretfully there is more air to escape until that bubble finally stops leaking.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

4

A lot of second-hand equipment changed hands or was built during the last decade. Prices climbed to record levels in 2007 - 2008, creating inflated book values for a lot of the older tonnage – especially units that are now surplus. In a stable or buoyant market, this price bubble could have been absorbed as new vessels gradually came on line. It is still a rude awakening though when borrowers are forced to re-adjust their book values in this fallen market – and also a rude awakening to their shareholders in publically traded companies. Many fleets are not worth what they were valued at when the loans were made. Existing and new lenders need to take a hard look at some of the equipment and determine whether an owner’s book values, like many home values, are underwater. We are getting close to the bottom, but the shake-out of surplus equipment has not finished. Some assets will still have to be sold at a loss in over the next couple of years.

“Merger mania”, discussed in our last November 2010 tug market report, has started. There are many larger operators now out there sitting on idle cash waiting for the market to hit the absolute bottom to make a move. Already there is an upward trend in mergers and acquisitions with Kirby Corporation’s purchase of the ship bunkering operations of Enterprise Marine Services,

distributer & service provider United Holdings LLC, and merger with tank barge & tug operator K-Sea Transportation; Signet Maritime’s purchase of Pascagoula, Mississippi based Colle Towing Company; Ensco

acquiring Pride International to create the second largest offshore driller in the world to name a few. The Royal Boskalis Westminster US$ 1.5 billion acquisition of Smit Internationale was a major event in 2010, but that had been percolating on and off for some time and I would not necessarily call it “merger mania”. The financial industry has also been digging its way out from the mess it found itself in the end of 2007 and until recently showed little desire to finance acquisitions until they could see a light at the end of the tunnel. That light is starting to appear. While financing is not as readily obtainable as it

was during the boom years - and rightfully so - some credit is becoming more readily available. Large, well-managed, publically-traded and private operators with proven track records and a competitive

edge will obviously be the first-in-line. Small companies though may find it hard to a secure a portion of the funds needed to grow, especially during a sluggish recovery. The projected world growth of about 4.4% in 2011 and 4.5% in 2012 will make it difficult for a vessel operator to grow organically, one contract or one vessel or

barge at a time. Instead we will see more take-overs of smaller rivals, especially those companies operating modern fleets, and even more especially those who may have loans coming due in 2011 on equipment built or

purchased during the boom years. Acquisitions have always been an attractive option for large corporations who have cash on their books and/or a good line of credit. Years ago, after the big 80’s slump, one of Tidewater’s execs said that it was easier to buy a company than an individual boat – plus there was an added benefit of eliminating a competitor and gaining market share during the economic lull. Tidewater was not the only one to recognize this fact and it still holds true today.

1985 directories of U.S. offshore tugs and offshore service vessels published by Fleet Data Service document 188 offshore tug fleets with over 1,400 tugs and 102 OSV fleets with 1,061 supply boats, AHTSs, survey and miscellaneous related vessels over 150’ in length in the United States. This was several years after the 1981 – 1982 recession officially ended. 125, or 66.5%, of those offshore tug and 78 (76.5%) of those OSV fleets named in the 1985 guides no longer exist today. Some went into bankruptcy in the 80s like Alaska Marine Towing, Faustug Marine, Marsea Agencies, Command Marine or Leam Transportation. Some fleets were taken over and later themselves became candidates for acquisition - like the original Hornbeck Offshore’s acquiring the majority of stock in Point Marine’s 13 vessel fleet in 1990 plus four boats from Garber Bros., and then being acquired themselves by Tidewater in 1996. There were also the multitude of companies bought out by Zapata Gulf, which was itself acquired by Tidewater in 1992. Some vessels were sold off into other markets, but most continued on, being rebuilt multiple times and operating under different ownership and/or flags as the various markets gradually improved. Of course, there are also a lot of successful new names today that were not in existence twenty-five years ago. Both domestic and international mergers and acquisitions will definitely continue as headline news in 2011 and 2012 across the world and not only in the maritime and energy sectors.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

5

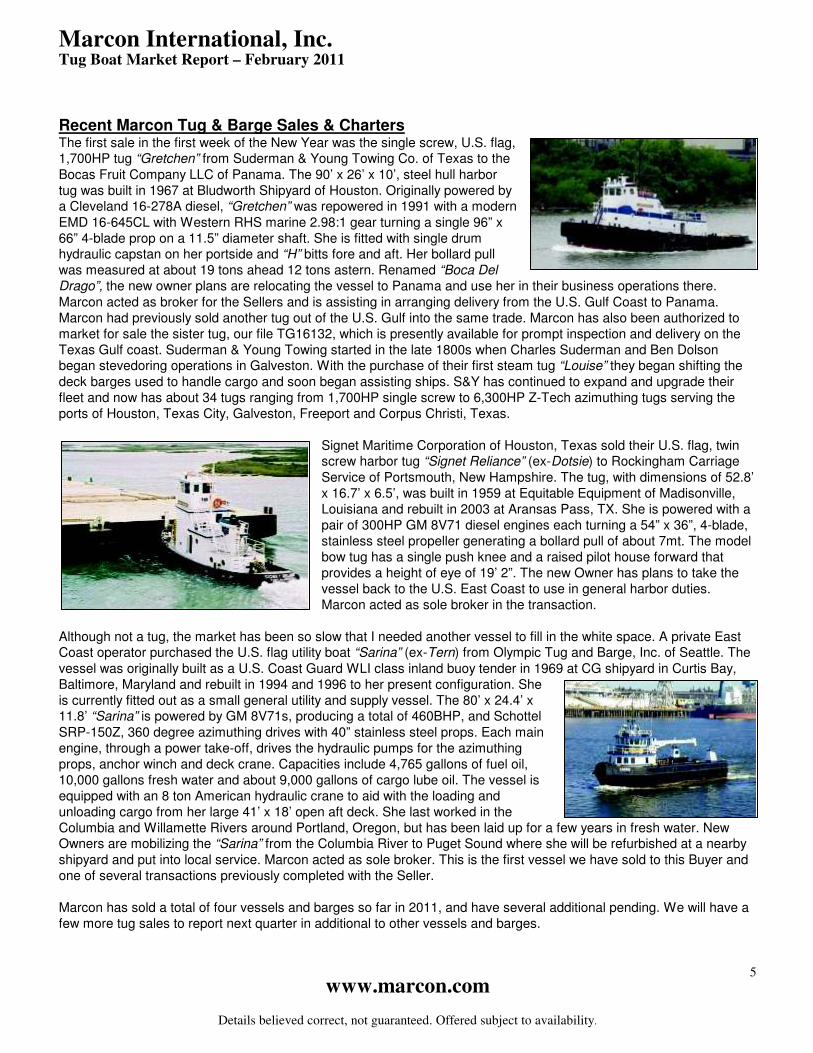

Recent Marcon Tug & Barge Sales & Charters The first sale in the first week of the New Year was the single screw, U.S. flag, 1,700HP tug “Gretchen” from Suderman & Young Towing Co. of Texas to the Bocas Fruit Company LLC of Panama. The 90’ x 26’ x 10’, steel hull harbor tug was built in 1967 at Bludworth Shipyard of Houston. Originally powered by a Cleveland 16-278A diesel, “Gretchen” was repowered in 1991 with a modern EMD 16-645CL with Western RHS marine 2.98:1 gear turning a single 96” x 66” 4-blade prop on a 11.5” diameter shaft. She is fitted with single drum hydraulic capstan on her portside and “H” bitts fore and aft. Her bollard pull was measured at about 19 tons ahead 12 tons astern. Renamed “Boca Del Drago”, the new owner plans are relocating the vessel to Panama and use her in their business operations there. Marcon acted as broker for the Sellers and is assisting in arranging delivery from the U.S. Gulf Coast to Panama. Marcon had previously sold another tug out of the U.S. Gulf into the same trade. Marcon has also been authorized to market for sale the sister tug, our file TG16132, which is presently available for prompt inspection and delivery on the Texas Gulf coast. Suderman & Young Towing started in the late 1800s when Charles Suderman and Ben Dolson began stevedoring operations in Galveston. With the purchase of their first steam tug “Louise” they began shifting the deck barges used to handle cargo and soon began assisting ships. S&Y has continued to expand and upgrade their fleet and now has about 34 tugs ranging from 1,700HP single screw to 6,300HP Z-Tech azimuthing tugs serving the ports of Houston, Texas City, Galveston, Freeport and Corpus Christi, Texas.

Signet Maritime Corporation of Houston, Texas sold their U.S. flag, twin screw harbor tug “Signet Reliance” (ex-Dotsie) to Rockingham Carriage Service of Portsmouth, New Hampshire. The tug, with dimensions of 52.8’ x 16.7’ x 6.5’, was built in 1959 at Equitable Equipment of Madisonville, Louisiana and rebuilt in 2003 at Aransas Pass, TX. She is powered with a pair of 300HP GM 8V71 diesel engines each turning a 54” x 36”, 4-blade, stainless steel propeller generating a bollard pull of about 7mt. The model bow tug has a single push knee and a raised pilot house forward that provides a height of eye of 19’ 2”. The new Owner has plans to take the vessel back to the U.S. East Coast to use in general harbor duties. Marcon acted as sole broker in the transaction.

Although not a tug, the market has been so slow that I needed another vessel to fill in the white space. A private East Coast operator purchased the U.S. flag utility boat “Sarina” (ex-Tern) from Olympic Tug and Barge, Inc. of Seattle. The vessel was originally built as a U.S. Coast Guard WLI class inland buoy tender in 1969 at CG shipyard in Curtis Bay, Baltimore, Maryland and rebuilt in 1994 and 1996 to her present configuration. She is currently fitted out as a small general utility and supply vessel. The 80’ x 24.4’ x 11.8’ “Sarina” is powered by GM 8V71s, producing a total of 460BHP, and Schottel SRP-150Z, 360 degree azimuthing drives with 40” stainless steel props. Each main engine, through a power take-off, drives the hydraulic pumps for the azimuthing props, anchor winch and deck crane. Capacities include 4,765 gallons of fuel oil, 10,000 gallons fresh water and about 9,000 gallons of cargo lube oil. The vessel is equipped with an 8 ton American hydraulic crane to aid with the loading and unloading cargo from her large 41’ x 18’ open aft deck. She last worked in the Columbia and Willamette Rivers around Portland, Oregon, but has been laid up for a few years in fresh water. New Owners are mobilizing the “Sarina” from the Columbia River to Puget Sound where she will be refurbished at a nearby shipyard and put into local service. Marcon acted as sole broker. This is the first vessel we have sold to this Buyer and one of several transactions previously completed with the Seller. Marcon has sold a total of four vessels and barges so far in 2011, and have several additional pending. We will have a few more tug sales to report next quarter in additional to other vessels and barges.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

6

Worldwide Existing Tugs By Age Group

45%

32%

19%

4%

<25 years 25+ years 35+ years 50+ years

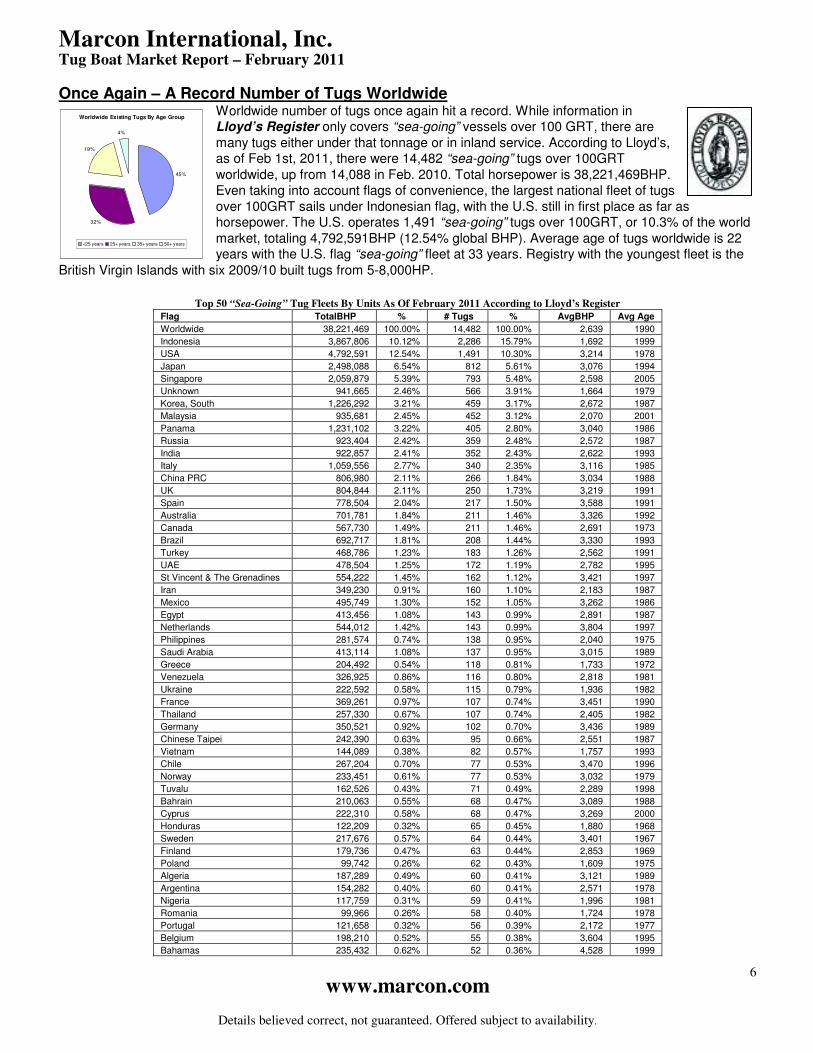

Once Again – A Record Number of Tugs Worldwide Worldwide number of tugs once again hit a record. While information in Lloyd’s Register only covers “sea-going” vessels over 100 GRT, there are many tugs either under that tonnage or in inland service. According to Lloyd’s, as of Feb 1st, 2011, there were 14,482 “sea-going” tugs over 100GRT worldwide, up from 14,088 in Feb. 2010. Total horsepower is 38,221,469BHP. Even taking into account flags of convenience, the largest national fleet of tugs over 100GRT sails under Indonesian flag, with the U.S. still in first place as far as horsepower. The U.S. operates 1,491 “sea-going” tugs over 100GRT, or 10.3% of the world market, totaling 4,792,591BHP (12.54% global BHP). Average age of tugs worldwide is 22 years with the U.S. flag “sea-going” fleet at 33 years. Registry with the youngest fleet is the

British Virgin Islands with six 2009/10 built tugs from 5-8,000HP.

Top 50 “Sea-Going” Tug Fleets By Units As Of February 2011 According to Lloyd’s Register

Flag TotalBHP % # Tugs % AvgBHP Avg Age

Worldwide 38,221,469 100.00% 14,482 100.00% 2,639 1990

Indonesia 3,867,806 10.12% 2,286 15.79% 1,692 1999

USA 4,792,591 12.54% 1,491 10.30% 3,214 1978

Japan 2,498,088 6.54% 812 5.61% 3,076 1994

Singapore 2,059,879 5.39% 793 5.48% 2,598 2005

Unknown 941,665 2.46% 566 3.91% 1,664 1979

Korea, South 1,226,292 3.21% 459 3.17% 2,672 1987

Malaysia 935,681 2.45% 452 3.12% 2,070 2001

Panama 1,231,102 3.22% 405 2.80% 3,040 1986

Russia 923,404 2.42% 359 2.48% 2,572 1987

India 922,857 2.41% 352 2.43% 2,622 1993

Italy 1,059,556 2.77% 340 2.35% 3,116 1985

China PRC 806,980 2.11% 266 1.84% 3,034 1988

UK 804,844 2.11% 250 1.73% 3,219 1991

Spain 778,504 2.04% 217 1.50% 3,588 1991

Australia 701,781 1.84% 211 1.46% 3,326 1992

Canada 567,730 1.49% 211 1.46% 2,691 1973

Brazil 692,717 1.81% 208 1.44% 3,330 1993

Turkey 468,786 1.23% 183 1.26% 2,562 1991

UAE 478,504 1.25% 172 1.19% 2,782 1995

St Vincent & The Grenadines 554,222 1.45% 162 1.12% 3,421 1997

Iran 349,230 0.91% 160 1.10% 2,183 1987

Mexico 495,749 1.30% 152 1.05% 3,262 1986

Egypt 413,456 1.08% 143 0.99% 2,891 1987

Netherlands 544,012 1.42% 143 0.99% 3,804 1997

Philippines 281,574 0.74% 138 0.95% 2,040 1975

Saudi Arabia 413,114 1.08% 137 0.95% 3,015 1989

Greece 204,492 0.54% 118 0.81% 1,733 1972

Venezuela 326,925 0.86% 116 0.80% 2,818 1981

Ukraine 222,592 0.58% 115 0.79% 1,936 1982

France 369,261 0.97% 107 0.74% 3,451 1990

Thailand 257,330 0.67% 107 0.74% 2,405 1982

Germany 350,521 0.92% 102 0.70% 3,436 1989

Chinese Taipei 242,390 0.63% 95 0.66% 2,551 1987

Vietnam 144,089 0.38% 82 0.57% 1,757 1993

Chile 267,204 0.70% 77 0.53% 3,470 1996

Norway 233,451 0.61% 77 0.53% 3,032 1979

Tuvalu 162,526 0.43% 71 0.49% 2,289 1998

Bahrain 210,063 0.55% 68 0.47% 3,089 1988

Cyprus 222,310 0.58% 68 0.47% 3,269 2000

Honduras 122,209 0.32% 65 0.45% 1,880 1968

Sweden 217,676 0.57% 64 0.44% 3,401 1967

Finland 179,736 0.47% 63 0.44% 2,853 1969

Poland 99,742 0.26% 62 0.43% 1,609 1975

Algeria 187,289 0.49% 60 0.41% 3,121 1989

Argentina 154,282 0.40% 60 0.41% 2,571 1978

Nigeria 117,759 0.31% 59 0.41% 1,996 1981

Romania 99,966 0.26% 58 0.40% 1,724 1978

Portugal 121,658 0.32% 56 0.39% 2,172 1977

Belgium 198,210 0.52% 55 0.38% 3,604 1995

Bahamas 235,432 0.62% 52 0.36% 4,528 1999

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

7

US Existing Tugs by Age Group

17%

44%

29%

10%

<25 years 25+ years 35+ years 50+ years

Seaweb Worldwide Seagoing Tugs

25,000,000

30,000,000

35,000,000

40,000,000

Jan-

07

Jan-

08

Apr-

08

Jul-

08

Oct-

08

Jan-

09

Apr-

09

Aug-

09

Nov-

09

Feb-

10

May-

10

Aug-

10

Nov-

10

Feb-

10

Ho

rsep

ow

er

10,000

11,000

12,000

13,000

14,000

15,000

Co

un

t

HP Count

Seaweb U.S. Seagoing Tugs

4,000,000

4,250,000

4,500,000

4,750,000

5,000,000

5,250,000

5,500,000

Jan-

07

Jan-

08

Apr-

08

Jul-08 Oct-

08

Jan-

09

Apr-

09

Aug-

09

Nov-

09

Feb-

10

May-

10

Aug-

10

Nov-

10

Feb-

10

Ho

rsep

ow

er

1,400

1,450

1,500

1,550

1,600

Co

un

t

HP Count

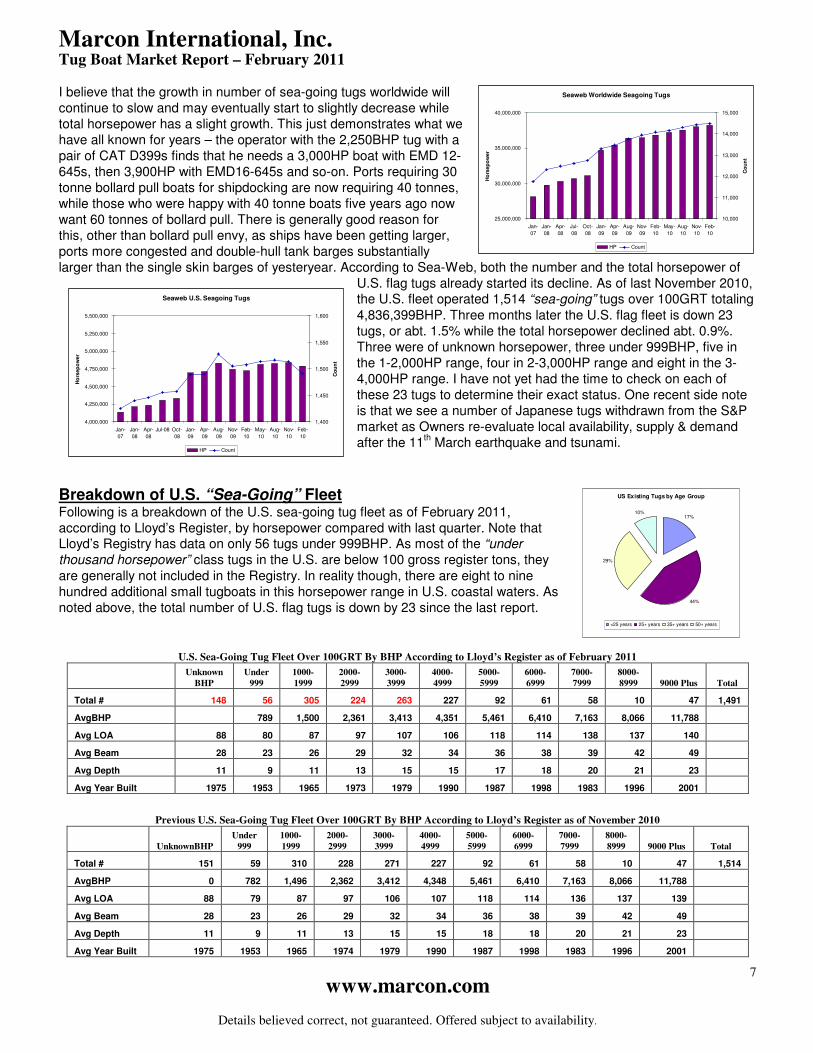

I believe that the growth in number of sea-going tugs worldwide will continue to slow and may eventually start to slightly decrease while total horsepower has a slight growth. This just demonstrates what we have all known for years – the operator with the 2,250BHP tug with a pair of CAT D399s finds that he needs a 3,000HP boat with EMD 12-645s, then 3,900HP with EMD16-645s and so-on. Ports requiring 30 tonne bollard pull boats for shipdocking are now requiring 40 tonnes, while those who were happy with 40 tonne boats five years ago now want 60 tonnes of bollard pull. There is generally good reason for this, other than bollard pull envy, as ships have been getting larger, ports more congested and double-hull tank barges substantially larger than the single skin barges of yesteryear. According to Sea-Web, both the number and the total horsepower of

U.S. flag tugs already started its decline. As of last November 2010, the U.S. fleet operated 1,514 “sea-going” tugs over 100GRT totaling 4,836,399BHP. Three months later the U.S. flag fleet is down 23 tugs, or abt. 1.5% while the total horsepower declined abt. 0.9%. Three were of unknown horsepower, three under 999BHP, five in the 1-2,000HP range, four in 2-3,000HP range and eight in the 3-4,000HP range. I have not yet had the time to check on each of these 23 tugs to determine their exact status. One recent side note is that we see a number of Japanese tugs withdrawn from the S&P market as Owners re-evaluate local availability, supply & demand after the 11

th March earthquake and tsunami.

Breakdown of U.S. “Sea-Going” Fleet Following is a breakdown of the U.S. sea-going tug fleet as of February 2011, according to Lloyd’s Register, by horsepower compared with last quarter. Note that Lloyd’s Registry has data on only 56 tugs under 999BHP. As most of the “under thousand horsepower” class tugs in the U.S. are below 100 gross register tons, they are generally not included in the Registry. In reality though, there are eight to nine hundred additional small tugboats in this horsepower range in U.S. coastal waters. As noted above, the total number of U.S. flag tugs is down by 23 since the last report.

U.S. Sea-Going Tug Fleet Over 100GRT By BHP According to Lloyd’s Register as of February 2011

Unknown

BHP

Under

999

1000-

1999

2000-

2999

3000-

3999

4000-

4999

5000-

5999

6000-

6999

7000-

7999

8000-

8999 9000 Plus Total

Total # 148 56 305 224 263 227 92 61 58 10 47 1,491

AvgBHP 789 1,500 2,361 3,413 4,351 5,461 6,410 7,163 8,066 11,788

Avg LOA 88 80 87 97 107 106 118 114 138 137 140

Avg Beam 28 23 26 29 32 34 36 38 39 42 49

Avg Depth 11 9 11 13 15 15 17 18 20 21 23

Avg Year Built 1975 1953 1965 1973 1979 1990 1987 1998 1983 1996 2001

Previous U.S. Sea-Going Tug Fleet Over 100GRT By BHP According to Lloyd’s Register as of November 2010

UnknownBHP

Under

999

1000-

1999

2000-

2999

3000-

3999

4000-

4999

5000-

5999

6000-

6999

7000-

7999

8000-

8999 9000 Plus Total

Total # 151 59 310 228 271 227 92 61 58 10 47 1,514

AvgBHP 0 782 1,496 2,362 3,412 4,348 5,461 6,410 7,163 8,066 11,788

Avg LOA 88 79 87 97 106 107 118 114 136 137 139

Avg Beam 28 23 26 29 32 34 36 38 39 42 49

Avg Depth 11 9 11 13 15 15 18 18 20 21 23

Avg Year Built 1975 1953 1965 1974 1979 1990 1987 1998 1983 1996 2001

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

8

Fairplay World Orderbook Vessels Over 299GRT

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Oct 06 Jan 07 Apr 07 Jul 07 Oct 07 Jan 08 Apr 08 Jul 08 Oct 08Jan 09 Apr 09 Jul 09 Nov 09 Feb

10

May

10

Aug

10

Nov 10 Feb

11

0

100

200

300

400

500

600

700

800

900

All Vessels Towing/Pushing

Worldwide Tugs On Order Over 299 GRT

0

25

50

75

100

125

150

175

Mala

ysia

Chin

a P

RC

Indonesia

Turk

ey

Spain

Vie

tnam

US

A

Bra

zil

Egypt

Rom

ania

Japan

Sin

gapore

Pola

nd

Russia

Iran

Saudi A

rabia

South

Afr

ica

United A

rab E

mirate

s

Cuba

Kore

a,

South

Serb

ia

Ukra

ine

Fra

nce

India

Italy

Neth

erlands

Canada

Chile

Lithuania

Thaila

nd

Arg

entina

Lib

ya

Peru

Phili

ppin

es

Credit: Fairplay Newbuildings Online 02/11

US Flag Tugs - Engine Types

EMD

33%

Caterpillar

30%

GM/DD

17%

Other

6%

Wartsila

2%

Fairbanks, Morse

4%

Alco

4%

M.T.U.

1%Cummins

3%

Credit: LR-Fairplay SeaWeb 02/01/11

U S F l a g T u g s - P r o p e l l e r T y p e s

T win Scr ew

5 3 %

Sin gle Scr ew

3 0 %

Azimut hin g

13 %

Voit h- Schn eider

2 %

T r iple Scr ew

2 %

Cr edi t : LR-Fai r pl ay SeaWeb

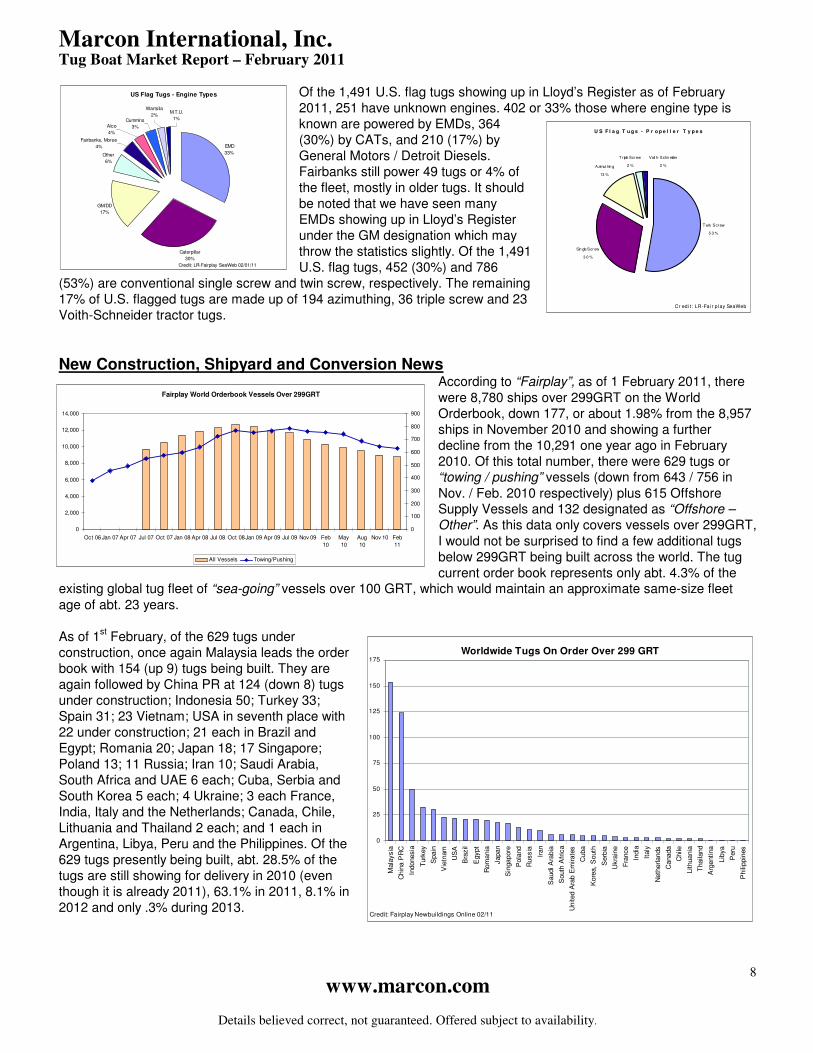

Of the 1,491 U.S. flag tugs showing up in Lloyd’s Register as of February 2011, 251 have unknown engines. 402 or 33% those where engine type is known are powered by EMDs, 364 (30%) by CATs, and 210 (17%) by General Motors / Detroit Diesels. Fairbanks still power 49 tugs or 4% of the fleet, mostly in older tugs. It should be noted that we have seen many EMDs showing up in Lloyd’s Register under the GM designation which may throw the statistics slightly. Of the 1,491 U.S. flag tugs, 452 (30%) and 786

(53%) are conventional single screw and twin screw, respectively. The remaining 17% of U.S. flagged tugs are made up of 194 azimuthing, 36 triple screw and 23 Voith-Schneider tractor tugs.

New Construction, Shipyard and Conversion News According to “Fairplay”, as of 1 February 2011, there were 8,780 ships over 299GRT on the World Orderbook, down 177, or about 1.98% from the 8,957 ships in November 2010 and showing a further decline from the 10,291 one year ago in February 2010. Of this total number, there were 629 tugs or “towing / pushing” vessels (down from 643 / 756 in Nov. / Feb. 2010 respectively) plus 615 Offshore Supply Vessels and 132 designated as “Offshore – Other”. As this data only covers vessels over 299GRT, I would not be surprised to find a few additional tugs below 299GRT being built across the world. The tug current order book represents only abt. 4.3% of the

existing global tug fleet of “sea-going” vessels over 100 GRT, which would maintain an approximate same-size fleet age of abt. 23 years. As of 1

st February, of the 629 tugs under

construction, once again Malaysia leads the order book with 154 (up 9) tugs being built. They are again followed by China PR at 124 (down 8) tugs under construction; Indonesia 50; Turkey 33; Spain 31; 23 Vietnam; USA in seventh place with 22 under construction; 21 each in Brazil and Egypt; Romania 20; Japan 18; 17 Singapore; Poland 13; 11 Russia; Iran 10; Saudi Arabia, South Africa and UAE 6 each; Cuba, Serbia and South Korea 5 each; 4 Ukraine; 3 each France, India, Italy and the Netherlands; Canada, Chile, Lithuania and Thailand 2 each; and 1 each in Argentina, Libya, Peru and the Philippines. Of the 629 tugs presently being built, abt. 28.5% of the tugs are still showing for delivery in 2010 (even though it is already 2011), 63.1% in 2011, 8.1% in 2012 and only .3% during 2013.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

9

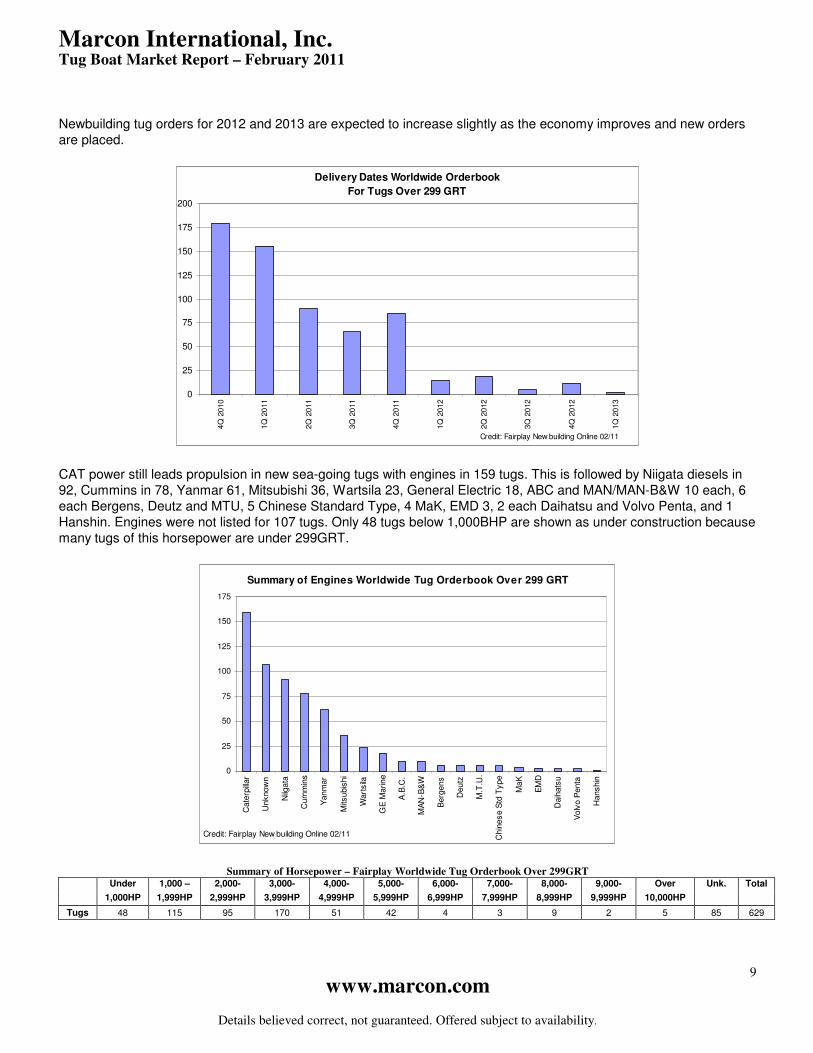

Newbuilding tug orders for 2012 and 2013 are expected to increase slightly as the economy improves and new orders are placed.

Delivery Dates Worldwide Orderbook

For Tugs Over 299 GRT

0

25

50

75

100

125

150

175

200

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

1Q

2013

Credit: Fairplay New building Online 02/11

CAT power still leads propulsion in new sea-going tugs with engines in 159 tugs. This is followed by Niigata diesels in 92, Cummins in 78, Yanmar 61, Mitsubishi 36, Wartsila 23, General Electric 18, ABC and MAN/MAN-B&W 10 each, 6 each Bergens, Deutz and MTU, 5 Chinese Standard Type, 4 MaK, EMD 3, 2 each Daihatsu and Volvo Penta, and 1 Hanshin. Engines were not listed for 107 tugs. Only 48 tugs below 1,000BHP are shown as under construction because many tugs of this horsepower are under 299GRT.

Summary of Engines Worldwide Tug Orderbook Over 299 GRT

0

25

50

75

100

125

150

175

Cate

rpillar

Unknow

n

Niig

ata

Cum

min

s

Yanm

ar

Mits

ubis

hi

Wart

sila

GE

Marine

A.B

.C.

MA

N-B

&W

Berg

ens

Deutz

M.T

.U.

Chin

es

e S

td T

ype

MaK

EM

D

Daih

ats

u

Vo

lvo P

enta

Hanshin

Credit: Fairplay New building Online 02/11

Summary of Horsepower – Fairplay Worldwide Tug Orderbook Over 299GRT Under 1,000 – 2,000- 3,000- 4,000- 5,000- 6,000- 7,000- 8,000- 9,000- Over

1,000HP 1,999HP 2,999HP 3,999HP 4,999HP 5,999HP 6,999HP 7,999HP 8,999HP 9,999HP 10,000HP

Unk. Total

Tugs 48 115 95 170 51 42 4 3 9 2 5 85 629

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

10

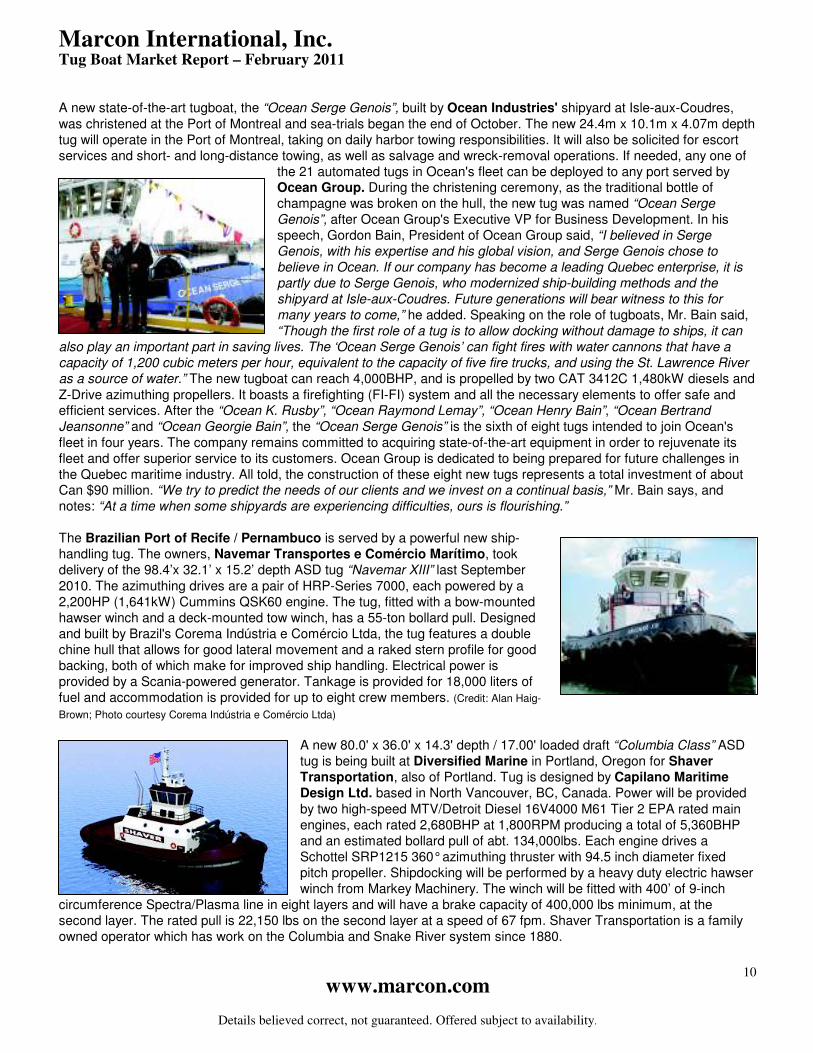

A new state-of-the-art tugboat, the “Ocean Serge Genois”, built by Ocean Industries' shipyard at Isle-aux-Coudres, was christened at the Port of Montreal and sea-trials began the end of October. The new 24.4m x 10.1m x 4.07m depth tug will operate in the Port of Montreal, taking on daily harbor towing responsibilities. It will also be solicited for escort services and short- and long-distance towing, as well as salvage and wreck-removal operations. If needed, any one of

the 21 automated tugs in Ocean's fleet can be deployed to any port served by Ocean Group. During the christening ceremony, as the traditional bottle of champagne was broken on the hull, the new tug was named “Ocean Serge Genois”, after Ocean Group's Executive VP for Business Development. In his speech, Gordon Bain, President of Ocean Group said, “I believed in Serge Genois, with his expertise and his global vision, and Serge Genois chose to believe in Ocean. If our company has become a leading Quebec enterprise, it is partly due to Serge Genois, who modernized ship-building methods and the shipyard at Isle-aux-Coudres. Future generations will bear witness to this for many years to come,” he added. Speaking on the role of tugboats, Mr. Bain said, “Though the first role of a tug is to allow docking without damage to ships, it can

also play an important part in saving lives. The ‘Ocean Serge Genois’ can fight fires with water cannons that have a capacity of 1,200 cubic meters per hour, equivalent to the capacity of five fire trucks, and using the St. Lawrence River as a source of water.” The new tugboat can reach 4,000BHP, and is propelled by two CAT 3412C 1,480kW diesels and Z-Drive azimuthing propellers. It boasts a firefighting (FI-FI) system and all the necessary elements to offer safe and efficient services. After the “Ocean K. Rusby”, “Ocean Raymond Lemay”, “Ocean Henry Bain”, “Ocean Bertrand Jeansonne” and “Ocean Georgie Bain”, the “Ocean Serge Genois” is the sixth of eight tugs intended to join Ocean's fleet in four years. The company remains committed to acquiring state-of-the-art equipment in order to rejuvenate its fleet and offer superior service to its customers. Ocean Group is dedicated to being prepared for future challenges in the Quebec maritime industry. All told, the construction of these eight new tugs represents a total investment of about Can $90 million. “We try to predict the needs of our clients and we invest on a continual basis,” Mr. Bain says, and notes: “At a time when some shipyards are experiencing difficulties, ours is flourishing.” The Brazilian Port of Recife / Pernambuco is served by a powerful new ship-handling tug. The owners, Navemar Transportes e Comércio Marítimo, took delivery of the 98.4’x 32.1’ x 15.2’ depth ASD tug “Navemar XIII” last September 2010. The azimuthing drives are a pair of HRP-Series 7000, each powered by a 2,200HP (1,641kW) Cummins QSK60 engine. The tug, fitted with a bow-mounted hawser winch and a deck-mounted tow winch, has a 55-ton bollard pull. Designed and built by Brazil's Corema Indústria e Comércio Ltda, the tug features a double chine hull that allows for good lateral movement and a raked stern profile for good backing, both of which make for improved ship handling. Electrical power is provided by a Scania-powered generator. Tankage is provided for 18,000 liters of fuel and accommodation is provided for up to eight crew members. (Credit: Alan Haig-

Brown; Photo courtesy Corema Indústria e Comércio Ltda)

A new 80.0' x 36.0' x 14.3' depth / 17.00' loaded draft “Columbia Class” ASD tug is being built at Diversified Marine in Portland, Oregon for Shaver Transportation, also of Portland. Tug is designed by Capilano Maritime Design Ltd. based in North Vancouver, BC, Canada. Power will be provided by two high-speed MTV/Detroit Diesel 16V4000 M61 Tier 2 EPA rated main engines, each rated 2,680BHP at 1,800RPM producing a total of 5,360BHP and an estimated bollard pull of abt. 134,000lbs. Each engine drives a Schottel SRP1215 360° azimuthing thruster with 94.5 inch diameter fixed pitch propeller. Shipdocking will be performed by a heavy duty electric hawser winch from Markey Machinery. The winch will be fitted with 400’ of 9-inch

circumference Spectra/Plasma line in eight layers and will have a brake capacity of 400,000 lbs minimum, at the second layer. The rated pull is 22,150 lbs on the second layer at a speed of 67 fpm. Shaver Transportation is a family owned operator which has work on the Columbia and Snake River system since 1880.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

11

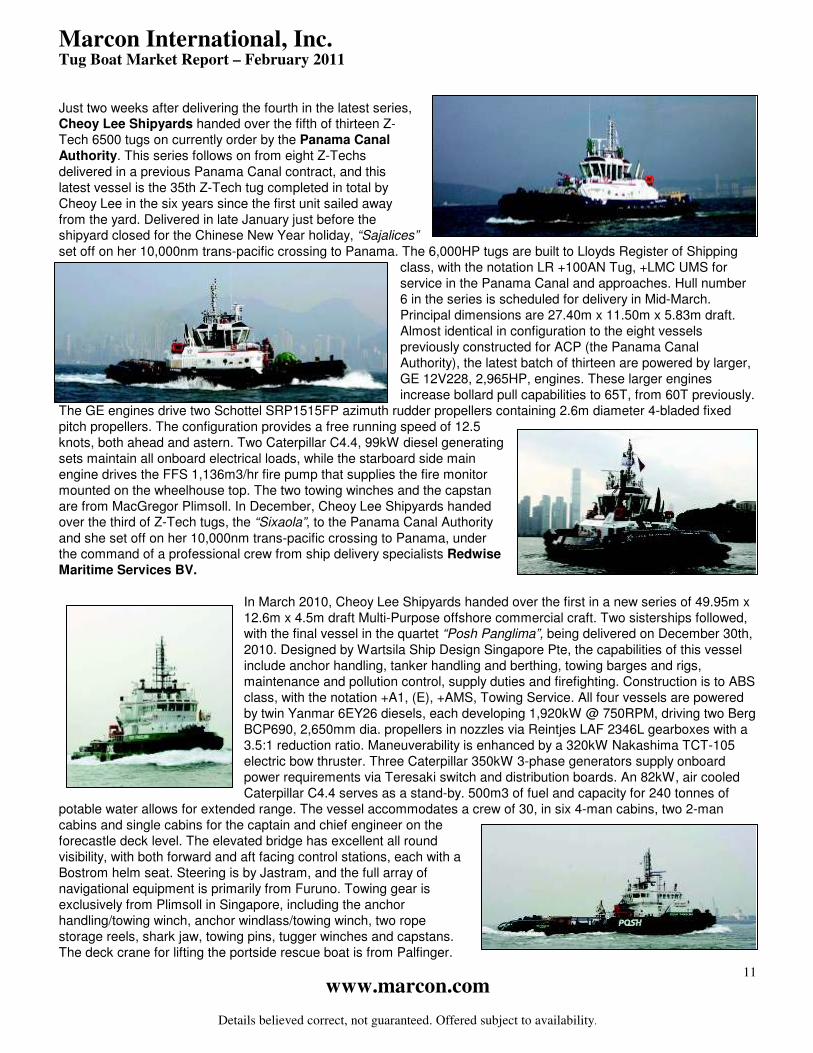

Just two weeks after delivering the fourth in the latest series, Cheoy Lee Shipyards handed over the fifth of thirteen Z-Tech 6500 tugs on currently order by the Panama Canal Authority. This series follows on from eight Z-Techs delivered in a previous Panama Canal contract, and this latest vessel is the 35th Z-Tech tug completed in total by Cheoy Lee in the six years since the first unit sailed away from the yard. Delivered in late January just before the shipyard closed for the Chinese New Year holiday, “Sajalices” set off on her 10,000nm trans-pacific crossing to Panama. The 6,000HP tugs are built to Lloyds Register of Shipping

class, with the notation LR +100AN Tug, +LMC UMS for service in the Panama Canal and approaches. Hull number 6 in the series is scheduled for delivery in Mid-March. Principal dimensions are 27.40m x 11.50m x 5.83m draft. Almost identical in configuration to the eight vessels previously constructed for ACP (the Panama Canal Authority), the latest batch of thirteen are powered by larger, GE 12V228, 2,965HP, engines. These larger engines increase bollard pull capabilities to 65T, from 60T previously.

The GE engines drive two Schottel SRP1515FP azimuth rudder propellers containing 2.6m diameter 4-bladed fixed pitch propellers. The configuration provides a free running speed of 12.5 knots, both ahead and astern. Two Caterpillar C4.4, 99kW diesel generating sets maintain all onboard electrical loads, while the starboard side main engine drives the FFS 1,136m3/hr fire pump that supplies the fire monitor mounted on the wheelhouse top. The two towing winches and the capstan are from MacGregor Plimsoll. In December, Cheoy Lee Shipyards handed over the third of Z-Tech tugs, the “Sixaola”, to the Panama Canal Authority and she set off on her 10,000nm trans-pacific crossing to Panama, under the command of a professional crew from ship delivery specialists Redwise Maritime Services BV.

In March 2010, Cheoy Lee Shipyards handed over the first in a new series of 49.95m x 12.6m x 4.5m draft Multi-Purpose offshore commercial craft. Two sisterships followed, with the final vessel in the quartet “Posh Panglima”, being delivered on December 30th, 2010. Designed by Wartsila Ship Design Singapore Pte, the capabilities of this vessel include anchor handling, tanker handling and berthing, towing barges and rigs, maintenance and pollution control, supply duties and firefighting. Construction is to ABS class, with the notation +A1, (E), +AMS, Towing Service. All four vessels are powered by twin Yanmar 6EY26 diesels, each developing 1,920kW @ 750RPM, driving two Berg BCP690, 2,650mm dia. propellers in nozzles via Reintjes LAF 2346L gearboxes with a 3.5:1 reduction ratio. Maneuverability is enhanced by a 320kW Nakashima TCT-105 electric bow thruster. Three Caterpillar 350kW 3-phase generators supply onboard power requirements via Teresaki switch and distribution boards. An 82kW, air cooled Caterpillar C4.4 serves as a stand-by. 500m3 of fuel and capacity for 240 tonnes of

potable water allows for extended range. The vessel accommodates a crew of 30, in six 4-man cabins, two 2-man cabins and single cabins for the captain and chief engineer on the forecastle deck level. The elevated bridge has excellent all round visibility, with both forward and aft facing control stations, each with a Bostrom helm seat. Steering is by Jastram, and the full array of navigational equipment is primarily from Furuno. Towing gear is exclusively from Plimsoll in Singapore, including the anchor handling/towing winch, anchor windlass/towing winch, two rope storage reels, shark jaw, towing pins, tugger winches and capstans. The deck crane for lifting the portside rescue boat is from Palfinger.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

12

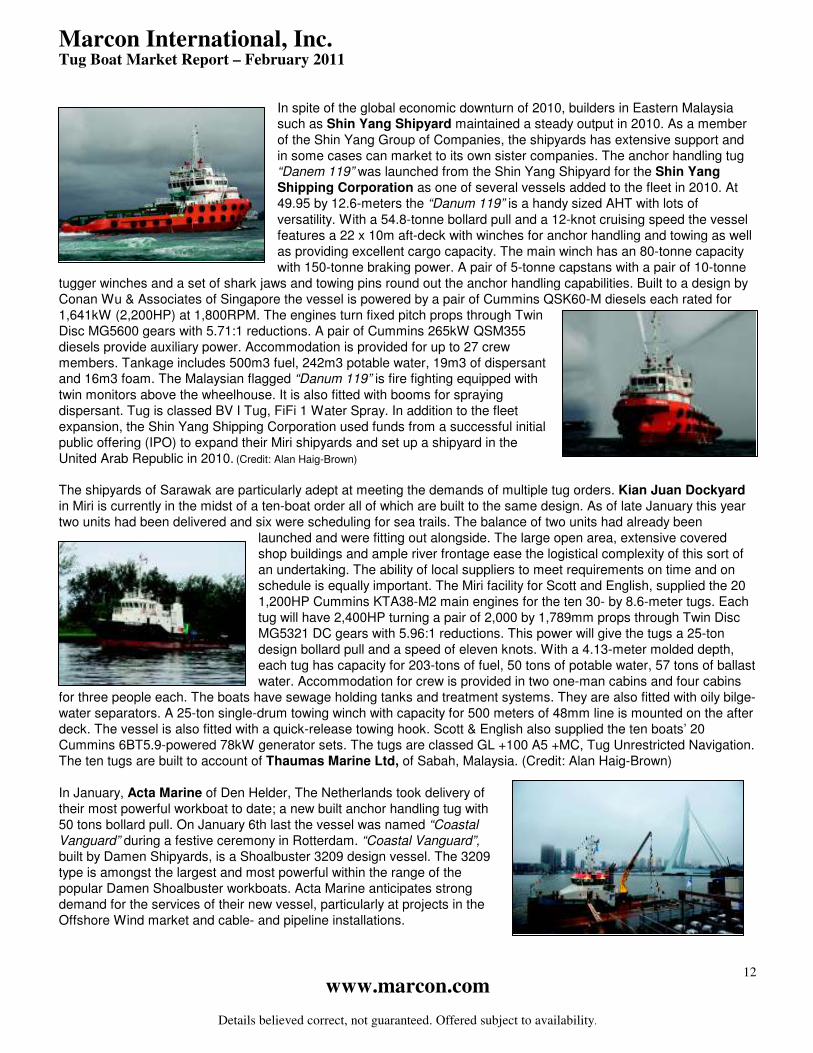

In spite of the global economic downturn of 2010, builders in Eastern Malaysia such as Shin Yang Shipyard maintained a steady output in 2010. As a member of the Shin Yang Group of Companies, the shipyards has extensive support and in some cases can market to its own sister companies. The anchor handling tug “Danem 119” was launched from the Shin Yang Shipyard for the Shin Yang Shipping Corporation as one of several vessels added to the fleet in 2010. At 49.95 by 12.6-meters the “Danum 119” is a handy sized AHT with lots of versatility. With a 54.8-tonne bollard pull and a 12-knot cruising speed the vessel features a 22 x 10m aft-deck with winches for anchor handling and towing as well as providing excellent cargo capacity. The main winch has an 80-tonne capacity with 150-tonne braking power. A pair of 5-tonne capstans with a pair of 10-tonne

tugger winches and a set of shark jaws and towing pins round out the anchor handling capabilities. Built to a design by Conan Wu & Associates of Singapore the vessel is powered by a pair of Cummins QSK60-M diesels each rated for 1,641kW (2,200HP) at 1,800RPM. The engines turn fixed pitch props through Twin Disc MG5600 gears with 5.71:1 reductions. A pair of Cummins 265kW QSM355 diesels provide auxiliary power. Accommodation is provided for up to 27 crew members. Tankage includes 500m3 fuel, 242m3 potable water, 19m3 of dispersant and 16m3 foam. The Malaysian flagged “Danum 119” is fire fighting equipped with twin monitors above the wheelhouse. It is also fitted with booms for spraying dispersant. Tug is classed BV I Tug, FiFi 1 Water Spray. In addition to the fleet expansion, the Shin Yang Shipping Corporation used funds from a successful initial public offering (IPO) to expand their Miri shipyards and set up a shipyard in the United Arab Republic in 2010. (Credit: Alan Haig-Brown)

The shipyards of Sarawak are particularly adept at meeting the demands of multiple tug orders. Kian Juan Dockyard in Miri is currently in the midst of a ten-boat order all of which are built to the same design. As of late January this year two units had been delivered and six were scheduling for sea trails. The balance of two units had already been

launched and were fitting out alongside. The large open area, extensive covered shop buildings and ample river frontage ease the logistical complexity of this sort of an undertaking. The ability of local suppliers to meet requirements on time and on schedule is equally important. The Miri facility for Scott and English, supplied the 20 1,200HP Cummins KTA38-M2 main engines for the ten 30- by 8.6-meter tugs. Each tug will have 2,400HP turning a pair of 2,000 by 1,789mm props through Twin Disc MG5321 DC gears with 5.96:1 reductions. This power will give the tugs a 25-ton design bollard pull and a speed of eleven knots. With a 4.13-meter molded depth, each tug has capacity for 203-tons of fuel, 50 tons of potable water, 57 tons of ballast water. Accommodation for crew is provided in two one-man cabins and four cabins

for three people each. The boats have sewage holding tanks and treatment systems. They are also fitted with oily bilge-water separators. A 25-ton single-drum towing winch with capacity for 500 meters of 48mm line is mounted on the after deck. The vessel is also fitted with a quick-release towing hook. Scott & English also supplied the ten boats’ 20 Cummins 6BT5.9-powered 78kW generator sets. The tugs are classed GL +100 A5 +MC, Tug Unrestricted Navigation. The ten tugs are built to account of Thaumas Marine Ltd, of Sabah, Malaysia. (Credit: Alan Haig-Brown) In January, Acta Marine of Den Helder, The Netherlands took delivery of their most powerful workboat to date; a new built anchor handling tug with 50 tons bollard pull. On January 6th last the vessel was named “Coastal Vanguard” during a festive ceremony in Rotterdam. “Coastal Vanguard”, built by Damen Shipyards, is a Shoalbuster 3209 design vessel. The 3209 type is amongst the largest and most powerful within the range of the popular Damen Shoalbuster workboats. Acta Marine anticipates strong demand for the services of their new vessel, particularly at projects in the Offshore Wind market and cable- and pipeline installations.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

13

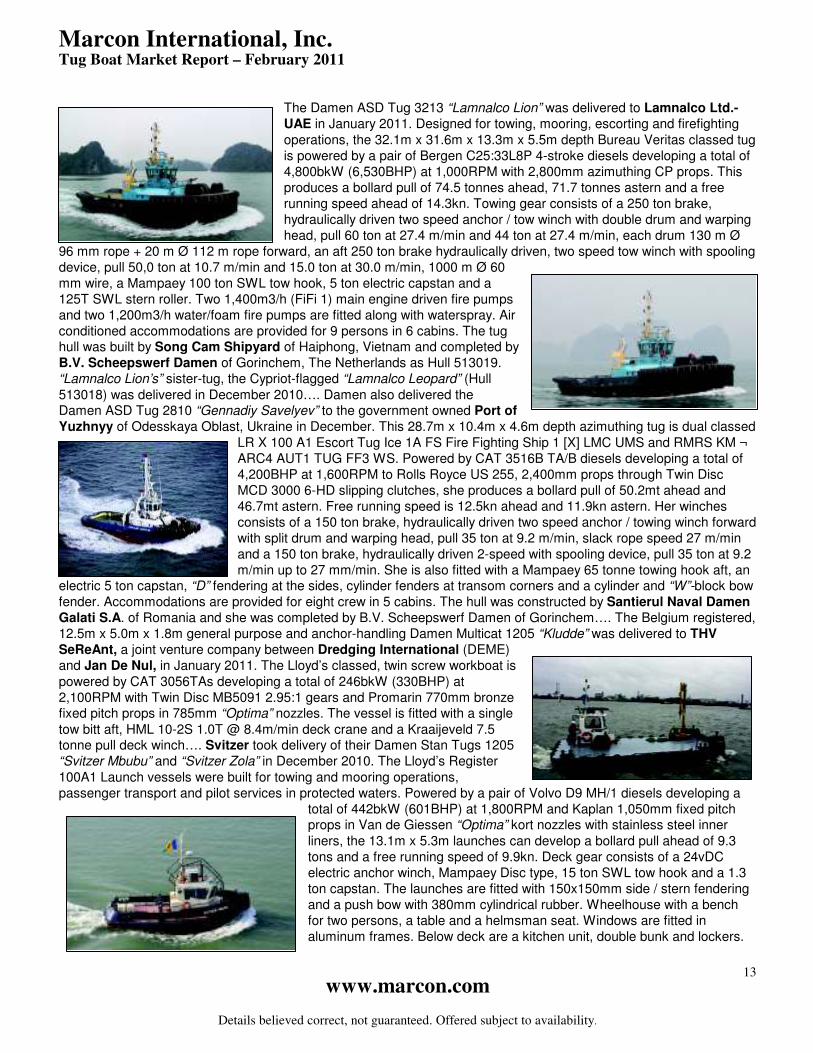

The Damen ASD Tug 3213 “Lamnalco Lion” was delivered to Lamnalco Ltd.-UAE in January 2011. Designed for towing, mooring, escorting and firefighting operations, the 32.1m x 31.6m x 13.3m x 5.5m depth Bureau Veritas classed tug is powered by a pair of Bergen C25:33L8P 4-stroke diesels developing a total of 4,800bkW (6,530BHP) at 1,000RPM with 2,800mm azimuthing CP props. This produces a bollard pull of 74.5 tonnes ahead, 71.7 tonnes astern and a free running speed ahead of 14.3kn. Towing gear consists of a 250 ton brake, hydraulically driven two speed anchor / tow winch with double drum and warping head, pull 60 ton at 27.4 m/min and 44 ton at 27.4 m/min, each drum 130 m Ø

96 mm rope + 20 m Ø 112 m rope forward, an aft 250 ton brake hydraulically driven, two speed tow winch with spooling device, pull 50,0 ton at 10.7 m/min and 15.0 ton at 30.0 m/min, 1000 m Ø 60 mm wire, a Mampaey 100 ton SWL tow hook, 5 ton electric capstan and a 125T SWL stern roller. Two 1,400m3/h (FiFi 1) main engine driven fire pumps and two 1,200m3/h water/foam fire pumps are fitted along with waterspray. Air conditioned accommodations are provided for 9 persons in 6 cabins. The tug hull was built by Song Cam Shipyard of Haiphong, Vietnam and completed by B.V. Scheepswerf Damen of Gorinchem, The Netherlands as Hull 513019. “Lamnalco Lion’s” sister-tug, the Cypriot-flagged “Lamnalco Leopard” (Hull 513018) was delivered in December 2010…. Damen also delivered the Damen ASD Tug 2810 “Gennadiy Savelyev” to the government owned Port of Yuzhnyy of Odesskaya Oblast, Ukraine in December. This 28.7m x 10.4m x 4.6m depth azimuthing tug is dual classed

LR X 100 A1 Escort Tug Ice 1A FS Fire Fighting Ship 1 [X] LMC UMS and RMRS KM ¬ ARC4 AUT1 TUG FF3 WS. Powered by CAT 3516B TA/B diesels developing a total of 4,200BHP at 1,600RPM to Rolls Royce US 255, 2,400mm props through Twin Disc MCD 3000 6-HD slipping clutches, she produces a bollard pull of 50.2mt ahead and 46.7mt astern. Free running speed is 12.5kn ahead and 11.9kn astern. Her winches consists of a 150 ton brake, hydraulically driven two speed anchor / towing winch forward with split drum and warping head, pull 35 ton at 9.2 m/min, slack rope speed 27 m/min and a 150 ton brake, hydraulically driven 2-speed with spooling device, pull 35 ton at 9.2 m/min up to 27 mm/min. She is also fitted with a Mampaey 65 tonne towing hook aft, an

electric 5 ton capstan, “D” fendering at the sides, cylinder fenders at transom corners and a cylinder and “W”-block bow fender. Accommodations are provided for eight crew in 5 cabins. The hull was constructed by Santierul Naval Damen Galati S.A. of Romania and she was completed by B.V. Scheepswerf Damen of Gorinchem…. The Belgium registered, 12.5m x 5.0m x 1.8m general purpose and anchor-handling Damen Multicat 1205 “Kludde” was delivered to THV SeReAnt, a joint venture company between Dredging International (DEME) and Jan De Nul, in January 2011. The Lloyd’s classed, twin screw workboat is powered by CAT 3056TAs developing a total of 246bkW (330BHP) at 2,100RPM with Twin Disc MB5091 2.95:1 gears and Promarin 770mm bronze fixed pitch props in 785mm “Optima” nozzles. The vessel is fitted with a single tow bitt aft, HML 10-2S 1.0T @ 8.4m/min deck crane and a Kraaijeveld 7.5 tonne pull deck winch…. Svitzer took delivery of their Damen Stan Tugs 1205 “Svitzer Mbubu” and “Svitzer Zola” in December 2010. The Lloyd’s Register 100A1 Launch vessels were built for towing and mooring operations, passenger transport and pilot services in protected waters. Powered by a pair of Volvo D9 MH/1 diesels developing a

total of 442bkW (601BHP) at 1,800RPM and Kaplan 1,050mm fixed pitch props in Van de Giessen “Optima” kort nozzles with stainless steel inner liners, the 13.1m x 5.3m launches can develop a bollard pull ahead of 9.3 tons and a free running speed of 9.9kn. Deck gear consists of a 24vDC electric anchor winch, Mampaey Disc type, 15 ton SWL tow hook and a 1.3 ton capstan. The launches are fitted with 150x150mm side / stern fendering and a push bow with 380mm cylindrical rubber. Wheelhouse with a bench for two persons, a table and a helmsman seat. Windows are fitted in aluminum frames. Below deck are a kitchen unit, double bunk and lockers.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

14

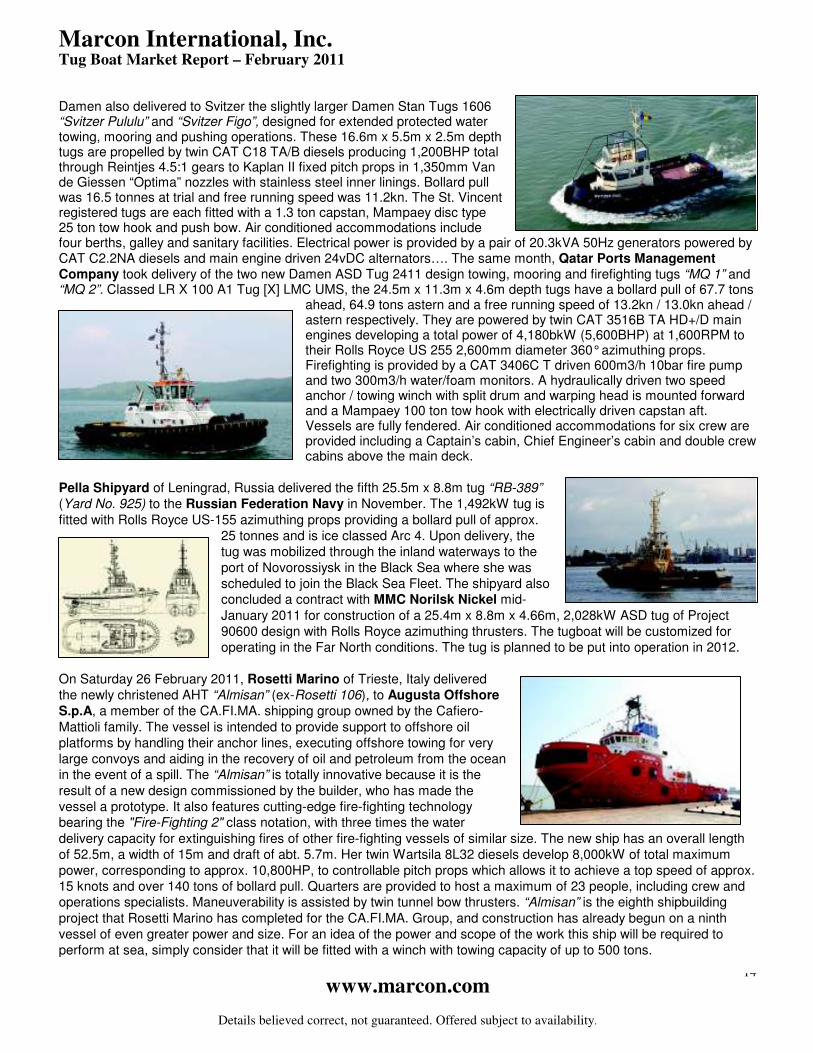

Damen also delivered to Svitzer the slightly larger Damen Stan Tugs 1606 “Svitzer Pululu” and “Svitzer Figo”, designed for extended protected water towing, mooring and pushing operations. These 16.6m x 5.5m x 2.5m depth tugs are propelled by twin CAT C18 TA/B diesels producing 1,200BHP total through Reintjes 4.5:1 gears to Kaplan II fixed pitch props in 1,350mm Van de Giessen “Optima” nozzles with stainless steel inner linings. Bollard pull was 16.5 tonnes at trial and free running speed was 11.2kn. The St. Vincent registered tugs are each fitted with a 1.3 ton capstan, Mampaey disc type 25 ton tow hook and push bow. Air conditioned accommodations include four berths, galley and sanitary facilities. Electrical power is provided by a pair of 20.3kVA 50Hz generators powered by CAT C2.2NA diesels and main engine driven 24vDC alternators…. The same month, Qatar Ports Management Company took delivery of the two new Damen ASD Tug 2411 design towing, mooring and firefighting tugs “MQ 1” and “MQ 2”. Classed LR X 100 A1 Tug [X] LMC UMS, the 24.5m x 11.3m x 4.6m depth tugs have a bollard pull of 67.7 tons

ahead, 64.9 tons astern and a free running speed of 13.2kn / 13.0kn ahead / astern respectively. They are powered by twin CAT 3516B TA HD+/D main engines developing a total power of 4,180bkW (5,600BHP) at 1,600RPM to their Rolls Royce US 255 2,600mm diameter 360° azimuthing props. Firefighting is provided by a CAT 3406C T driven 600m3/h 10bar fire pump and two 300m3/h water/foam monitors. A hydraulically driven two speed anchor / towing winch with split drum and warping head is mounted forward and a Mampaey 100 ton tow hook with electrically driven capstan aft. Vessels are fully fendered. Air conditioned accommodations for six crew are provided including a Captain’s cabin, Chief Engineer’s cabin and double crew cabins above the main deck.

Pella Shipyard of Leningrad, Russia delivered the fifth 25.5m x 8.8m tug “RB-389” (Yard No. 925) to the Russian Federation Navy in November. The 1,492kW tug is fitted with Rolls Royce US-155 azimuthing props providing a bollard pull of approx.

25 tonnes and is ice classed Arc 4. Upon delivery, the tug was mobilized through the inland waterways to the port of Novorossiysk in the Black Sea where she was scheduled to join the Black Sea Fleet. The shipyard also concluded a contract with MMC Norilsk Nickel mid-January 2011 for construction of a 25.4m x 8.8m x 4.66m, 2,028kW ASD tug of Project 90600 design with Rolls Royce azimuthing thrusters. The tugboat will be customized for operating in the Far North conditions. The tug is planned to be put into operation in 2012.

On Saturday 26 February 2011, Rosetti Marino of Trieste, Italy delivered the newly christened AHT “Almisan” (ex-Rosetti 106), to Augusta Offshore S.p.A, a member of the CA.FI.MA. shipping group owned by the Cafiero-Mattioli family. The vessel is intended to provide support to offshore oil platforms by handling their anchor lines, executing offshore towing for very large convoys and aiding in the recovery of oil and petroleum from the ocean in the event of a spill. The “Almisan” is totally innovative because it is the result of a new design commissioned by the builder, who has made the vessel a prototype. It also features cutting-edge fire-fighting technology bearing the "Fire-Fighting 2" class notation, with three times the water delivery capacity for extinguishing fires of other fire-fighting vessels of similar size. The new ship has an overall length of 52.5m, a width of 15m and draft of abt. 5.7m. Her twin Wartsila 8L32 diesels develop 8,000kW of total maximum power, corresponding to approx. 10,800HP, to controllable pitch props which allows it to achieve a top speed of approx. 15 knots and over 140 tons of bollard pull. Quarters are provided to host a maximum of 23 people, including crew and operations specialists. Maneuverability is assisted by twin tunnel bow thrusters. “Almisan” is the eighth shipbuilding project that Rosetti Marino has completed for the CA.FI.MA. Group, and construction has already begun on a ninth vessel of even greater power and size. For an idea of the power and scope of the work this ship will be required to perform at sea, simply consider that it will be fitted with a winch with towing capacity of up to 500 tons.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

15

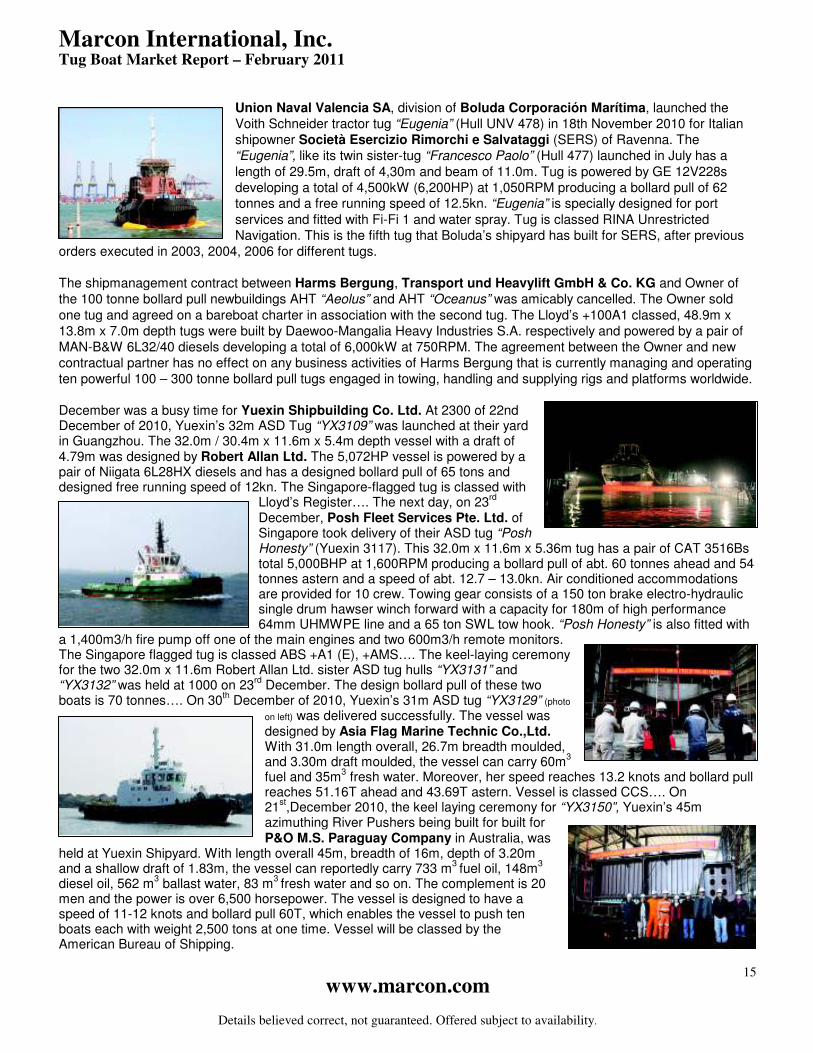

Union Naval Valencia SA, division of Boluda Corporación Marítima, launched the Voith Schneider tractor tug “Eugenia” (Hull UNV 478) in 18th November 2010 for Italian shipowner Società Esercizio Rimorchi e Salvataggi (SERS) of Ravenna. The “Eugenia”, like its twin sister-tug “Francesco Paolo” (Hull 477) launched in July has a length of 29.5m, draft of 4,30m and beam of 11.0m. Tug is powered by GE 12V228s developing a total of 4,500kW (6,200HP) at 1,050RPM producing a bollard pull of 62 tonnes and a free running speed of 12.5kn. “Eugenia” is specially designed for port services and fitted with Fi-Fi 1 and water spray. Tug is classed RINA Unrestricted Navigation. This is the fifth tug that Boluda’s shipyard has built for SERS, after previous

orders executed in 2003, 2004, 2006 for different tugs. The shipmanagement contract between Harms Bergung, Transport und Heavylift GmbH & Co. KG and Owner of the 100 tonne bollard pull newbuildings AHT “Aeolus” and AHT “Oceanus” was amicably cancelled. The Owner sold one tug and agreed on a bareboat charter in association with the second tug. The Lloyd’s +100A1 classed, 48.9m x 13.8m x 7.0m depth tugs were built by Daewoo-Mangalia Heavy Industries S.A. respectively and powered by a pair of MAN-B&W 6L32/40 diesels developing a total of 6,000kW at 750RPM. The agreement between the Owner and new contractual partner has no effect on any business activities of Harms Bergung that is currently managing and operating ten powerful 100 – 300 tonne bollard pull tugs engaged in towing, handling and supplying rigs and platforms worldwide.

December was a busy time for Yuexin Shipbuilding Co. Ltd. At 2300 of 22nd December of 2010, Yuexin’s 32m ASD Tug “YX3109” was launched at their yard in Guangzhou. The 32.0m / 30.4m x 11.6m x 5.4m depth vessel with a draft of 4.79m was designed by Robert Allan Ltd. The 5,072HP vessel is powered by a pair of Niigata 6L28HX diesels and has a designed bollard pull of 65 tons and designed free running speed of 12kn. The Singapore-flagged tug is classed with

Lloyd’s Register…. The next day, on 23rd

December, Posh Fleet Services Pte. Ltd. of Singapore took delivery of their ASD tug “Posh Honesty” (Yuexin 3117). This 32.0m x 11.6m x 5.36m tug has a pair of CAT 3516Bs total 5,000BHP at 1,600RPM producing a bollard pull of abt. 60 tonnes ahead and 54 tonnes astern and a speed of abt. 12.7 – 13.0kn. Air conditioned accommodations are provided for 10 crew. Towing gear consists of a 150 ton brake electro-hydraulic single drum hawser winch forward with a capacity for 180m of high performance 64mm UHMWPE line and a 65 ton SWL tow hook. “Posh Honesty” is also fitted with

a 1,400m3/h fire pump off one of the main engines and two 600m3/h remote monitors. The Singapore flagged tug is classed ABS +A1 (E), +AMS…. The keel-laying ceremony for the two 32.0m x 11.6m Robert Allan Ltd. sister ASD tug hulls “YX3131” and “YX3132” was held at 1000 on 23

rd December. The design bollard pull of these two

boats is 70 tonnes…. On 30th December of 2010, Yuexin’s 31m ASD tug “YX3129” (photo

on left) was delivered successfully. The vessel was designed by Asia Flag Marine Technic Co.,Ltd. With 31.0m length overall, 26.7m breadth moulded, and 3.30m draft moulded, the vessel can carry 60m

3

fuel and 35m3 fresh water. Moreover, her speed reaches 13.2 knots and bollard pull

reaches 51.16T ahead and 43.69T astern. Vessel is classed CCS…. On 21

st,December 2010, the keel laying ceremony for “YX3150”, Yuexin’s 45m

azimuthing River Pushers being built for built for P&O M.S. Paraguay Company in Australia, was

held at Yuexin Shipyard. With length overall 45m, breadth of 16m, depth of 3.20m and a shallow draft of 1.83m, the vessel can reportedly carry 733 m

3 fuel oil, 148m

3

diesel oil, 562 m3 ballast water, 83 m

3 fresh water and so on. The complement is 20

men and the power is over 6,500 horsepower. The vessel is designed to have a speed of 11-12 knots and bollard pull 60T, which enables the vessel to push ten boats each with weight 2,500 tons at one time. Vessel will be classed by the American Bureau of Shipping.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

16

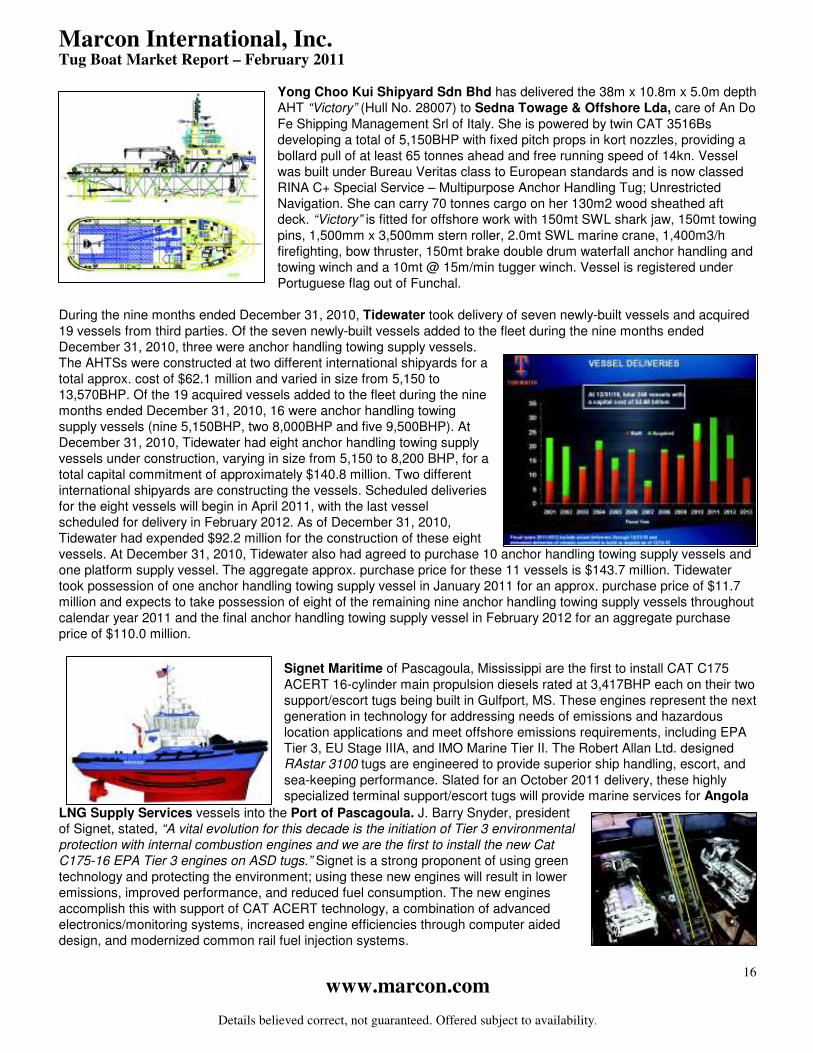

Yong Choo Kui Shipyard Sdn Bhd has delivered the 38m x 10.8m x 5.0m depth AHT “Victory” (Hull No. 28007) to Sedna Towage & Offshore Lda, care of An Do Fe Shipping Management Srl of Italy. She is powered by twin CAT 3516Bs developing a total of 5,150BHP with fixed pitch props in kort nozzles, providing a bollard pull of at least 65 tonnes ahead and free running speed of 14kn. Vessel was built under Bureau Veritas class to European standards and is now classed RINA C+ Special Service – Multipurpose Anchor Handling Tug; Unrestricted Navigation. She can carry 70 tonnes cargo on her 130m2 wood sheathed aft deck. “Victory” is fitted for offshore work with 150mt SWL shark jaw, 150mt towing pins, 1,500mm x 3,500mm stern roller, 2.0mt SWL marine crane, 1,400m3/h firefighting, bow thruster, 150mt brake double drum waterfall anchor handling and towing winch and a 10mt @ 15m/min tugger winch. Vessel is registered under Portuguese flag out of Funchal.

During the nine months ended December 31, 2010, Tidewater took delivery of seven newly-built vessels and acquired 19 vessels from third parties. Of the seven newly-built vessels added to the fleet during the nine months ended December 31, 2010, three were anchor handling towing supply vessels. The AHTSs were constructed at two different international shipyards for a total approx. cost of $62.1 million and varied in size from 5,150 to 13,570BHP. Of the 19 acquired vessels added to the fleet during the nine months ended December 31, 2010, 16 were anchor handling towing supply vessels (nine 5,150BHP, two 8,000BHP and five 9,500BHP). At December 31, 2010, Tidewater had eight anchor handling towing supply vessels under construction, varying in size from 5,150 to 8,200 BHP, for a total capital commitment of approximately $140.8 million. Two different international shipyards are constructing the vessels. Scheduled deliveries for the eight vessels will begin in April 2011, with the last vessel scheduled for delivery in February 2012. As of December 31, 2010, Tidewater had expended $92.2 million for the construction of these eight vessels. At December 31, 2010, Tidewater also had agreed to purchase 10 anchor handling towing supply vessels and one platform supply vessel. The aggregate approx. purchase price for these 11 vessels is $143.7 million. Tidewater took possession of one anchor handling towing supply vessel in January 2011 for an approx. purchase price of $11.7 million and expects to take possession of eight of the remaining nine anchor handling towing supply vessels throughout calendar year 2011 and the final anchor handling towing supply vessel in February 2012 for an aggregate purchase price of $110.0 million.

Signet Maritime of Pascagoula, Mississippi are the first to install CAT C175 ACERT 16-cylinder main propulsion diesels rated at 3,417BHP each on their two support/escort tugs being built in Gulfport, MS. These engines represent the next generation in technology for addressing needs of emissions and hazardous location applications and meet offshore emissions requirements, including EPA Tier 3, EU Stage IIIA, and IMO Marine Tier II. The Robert Allan Ltd. designed RAstar 3100 tugs are engineered to provide superior ship handling, escort, and sea-keeping performance. Slated for an October 2011 delivery, these highly specialized terminal support/escort tugs will provide marine services for Angola

LNG Supply Services vessels into the Port of Pascagoula. J. Barry Snyder, president of Signet, stated, “A vital evolution for this decade is the initiation of Tier 3 environmental protection with internal combustion engines and we are the first to install the new Cat C175-16 EPA Tier 3 engines on ASD tugs.” Signet is a strong proponent of using green technology and protecting the environment; using these new engines will result in lower emissions, improved performance, and reduced fuel consumption. The new engines accomplish this with support of CAT ACERT technology, a combination of advanced electronics/monitoring systems, increased engine efficiencies through computer aided design, and modernized common rail fuel injection systems.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

17

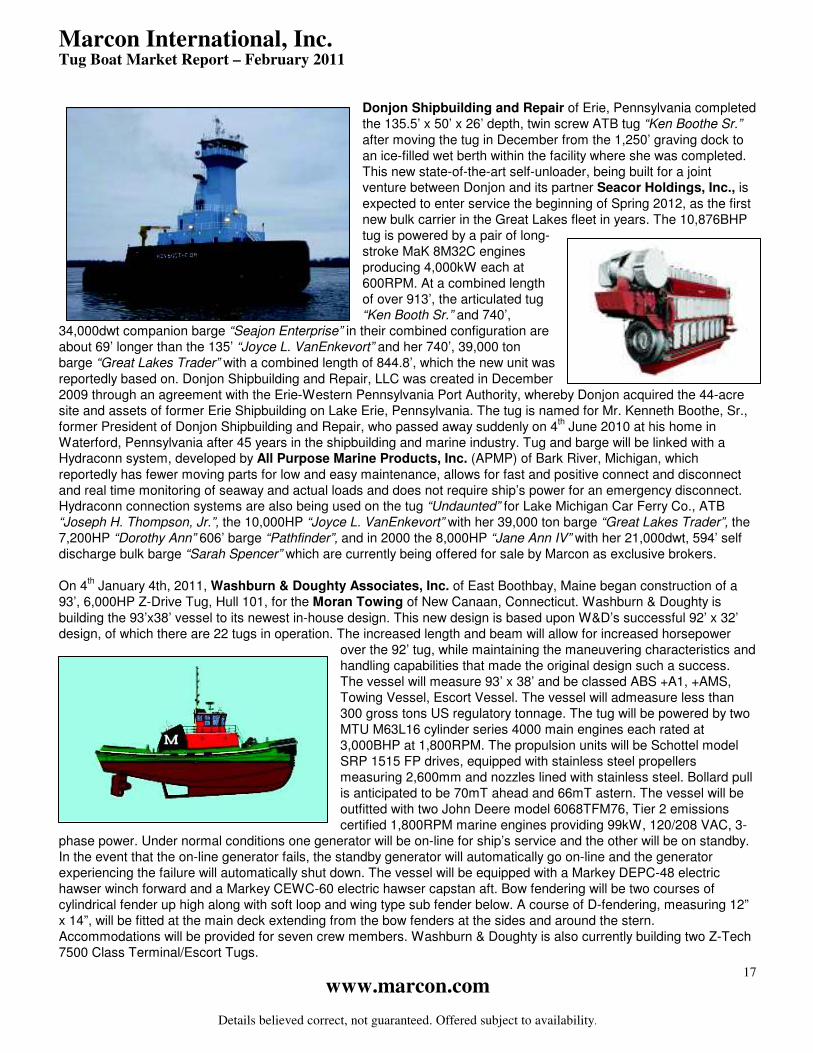

Donjon Shipbuilding and Repair of Erie, Pennsylvania completed the 135.5’ x 50’ x 26’ depth, twin screw ATB tug “Ken Boothe Sr.” after moving the tug in December from the 1,250’ graving dock to an ice-filled wet berth within the facility where she was completed. This new state-of-the-art self-unloader, being built for a joint venture between Donjon and its partner Seacor Holdings, Inc., is expected to enter service the beginning of Spring 2012, as the first new bulk carrier in the Great Lakes fleet in years. The 10,876BHP tug is powered by a pair of long-stroke MaK 8M32C engines producing 4,000kW each at 600RPM. At a combined length of over 913’, the articulated tug “Ken Booth Sr.” and 740’,

34,000dwt companion barge “Seajon Enterprise” in their combined configuration are about 69’ longer than the 135’ “Joyce L. VanEnkevort” and her 740’, 39,000 ton barge “Great Lakes Trader” with a combined length of 844.8’, which the new unit was reportedly based on. Donjon Shipbuilding and Repair, LLC was created in December 2009 through an agreement with the Erie-Western Pennsylvania Port Authority, whereby Donjon acquired the 44-acre site and assets of former Erie Shipbuilding on Lake Erie, Pennsylvania. The tug is named for Mr. Kenneth Boothe, Sr., former President of Donjon Shipbuilding and Repair, who passed away suddenly on 4

th June 2010 at his home in

Waterford, Pennsylvania after 45 years in the shipbuilding and marine industry. Tug and barge will be linked with a Hydraconn system, developed by All Purpose Marine Products, Inc. (APMP) of Bark River, Michigan, which reportedly has fewer moving parts for low and easy maintenance, allows for fast and positive connect and disconnect and real time monitoring of seaway and actual loads and does not require ship’s power for an emergency disconnect. Hydraconn connection systems are also being used on the tug “Undaunted” for Lake Michigan Car Ferry Co., ATB “Joseph H. Thompson, Jr.”, the 10,000HP “Joyce L. VanEnkevort” with her 39,000 ton barge “Great Lakes Trader”, the 7,200HP “Dorothy Ann” 606’ barge “Pathfinder”, and in 2000 the 8,000HP “Jane Ann IV” with her 21,000dwt, 594’ self discharge bulk barge “Sarah Spencer” which are currently being offered for sale by Marcon as exclusive brokers. On 4

th January 4th, 2011, Washburn & Doughty Associates, Inc. of East Boothbay, Maine began construction of a

93’, 6,000HP Z-Drive Tug, Hull 101, for the Moran Towing of New Canaan, Connecticut. Washburn & Doughty is building the 93’x38’ vessel to its newest in-house design. This new design is based upon W&D’s successful 92’ x 32’ design, of which there are 22 tugs in operation. The increased length and beam will allow for increased horsepower

over the 92’ tug, while maintaining the maneuvering characteristics and handling capabilities that made the original design such a success. The vessel will measure 93’ x 38’ and be classed ABS +A1, +AMS, Towing Vessel, Escort Vessel. The vessel will admeasure less than 300 gross tons US regulatory tonnage. The tug will be powered by two MTU M63L16 cylinder series 4000 main engines each rated at 3,000BHP at 1,800RPM. The propulsion units will be Schottel model SRP 1515 FP drives, equipped with stainless steel propellers measuring 2,600mm and nozzles lined with stainless steel. Bollard pull is anticipated to be 70mT ahead and 66mT astern. The vessel will be outfitted with two John Deere model 6068TFM76, Tier 2 emissions certified 1,800RPM marine engines providing 99kW, 120/208 VAC, 3-

phase power. Under normal conditions one generator will be on-line for ship’s service and the other will be on standby. In the event that the on-line generator fails, the standby generator will automatically go on-line and the generator experiencing the failure will automatically shut down. The vessel will be equipped with a Markey DEPC-48 electric hawser winch forward and a Markey CEWC-60 electric hawser capstan aft. Bow fendering will be two courses of cylindrical fender up high along with soft loop and wing type sub fender below. A course of D-fendering, measuring 12” x 14”, will be fitted at the main deck extending from the bow fenders at the sides and around the stern. Accommodations will be provided for seven crew members. Washburn & Doughty is also currently building two Z-Tech 7500 Class Terminal/Escort Tugs.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

18

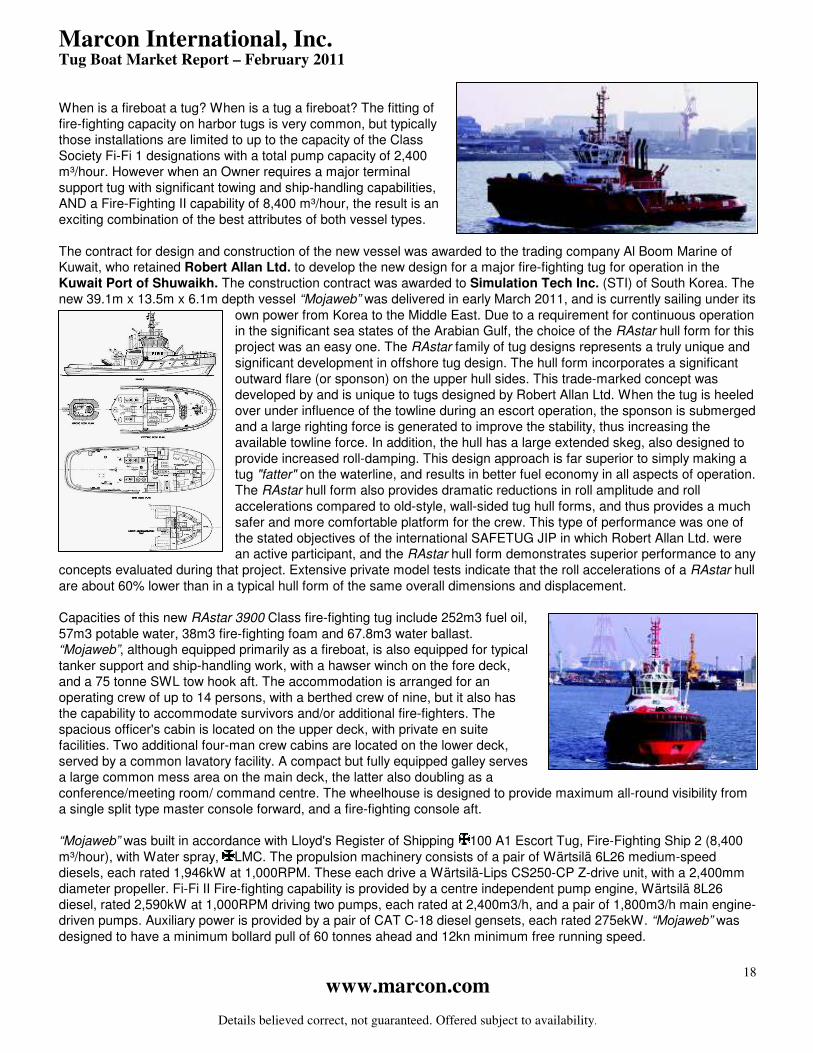

When is a fireboat a tug? When is a tug a fireboat? The fitting of fire-fighting capacity on harbor tugs is very common, but typically those installations are limited to up to the capacity of the Class Society Fi-Fi 1 designations with a total pump capacity of 2,400 m³/hour. However when an Owner requires a major terminal support tug with significant towing and ship-handling capabilities, AND a Fire-Fighting II capability of 8,400 m³/hour, the result is an exciting combination of the best attributes of both vessel types. The contract for design and construction of the new vessel was awarded to the trading company Al Boom Marine of Kuwait, who retained Robert Allan Ltd. to develop the new design for a major fire-fighting tug for operation in the Kuwait Port of Shuwaikh. The construction contract was awarded to Simulation Tech Inc. (STI) of South Korea. The new 39.1m x 13.5m x 6.1m depth vessel “Mojaweb” was delivered in early March 2011, and is currently sailing under its

own power from Korea to the Middle East. Due to a requirement for continuous operation in the significant sea states of the Arabian Gulf, the choice of the RAstar hull form for this project was an easy one. The RAstar family of tug designs represents a truly unique and significant development in offshore tug design. The hull form incorporates a significant outward flare (or sponson) on the upper hull sides. This trade-marked concept was developed by and is unique to tugs designed by Robert Allan Ltd. When the tug is heeled over under influence of the towline during an escort operation, the sponson is submerged and a large righting force is generated to improve the stability, thus increasing the available towline force. In addition, the hull has a large extended skeg, also designed to provide increased roll-damping. This design approach is far superior to simply making a tug "fatter" on the waterline, and results in better fuel economy in all aspects of operation. The RAstar hull form also provides dramatic reductions in roll amplitude and roll accelerations compared to old-style, wall-sided tug hull forms, and thus provides a much safer and more comfortable platform for the crew. This type of performance was one of the stated objectives of the international SAFETUG JIP in which Robert Allan Ltd. were an active participant, and the RAstar hull form demonstrates superior performance to any

concepts evaluated during that project. Extensive private model tests indicate that the roll accelerations of a RAstar hull are about 60% lower than in a typical hull form of the same overall dimensions and displacement. Capacities of this new RAstar 3900 Class fire-fighting tug include 252m3 fuel oil, 57m3 potable water, 38m3 fire-fighting foam and 67.8m3 water ballast. “Mojaweb”, although equipped primarily as a fireboat, is also equipped for typical tanker support and ship-handling work, with a hawser winch on the fore deck, and a 75 tonne SWL tow hook aft. The accommodation is arranged for an operating crew of up to 14 persons, with a berthed crew of nine, but it also has the capability to accommodate survivors and/or additional fire-fighters. The spacious officer's cabin is located on the upper deck, with private en suite facilities. Two additional four-man crew cabins are located on the lower deck, served by a common lavatory facility. A compact but fully equipped galley serves a large common mess area on the main deck, the latter also doubling as a conference/meeting room/ command centre. The wheelhouse is designed to provide maximum all-round visibility from a single split type master console forward, and a fire-fighting console aft. “Mojaweb” was built in accordance with Lloyd's Register of Shipping 100 A1 Escort Tug, Fire-Fighting Ship 2 (8,400 m³/hour), with Water spray, LMC. The propulsion machinery consists of a pair of Wärtsilä 6L26 medium-speed diesels, each rated 1,946kW at 1,000RPM. These each drive a Wärtsilä-Lips CS250-CP Z-drive unit, with a 2,400mm diameter propeller. Fi-Fi II Fire-fighting capability is provided by a centre independent pump engine, Wärtsilä 8L26 diesel, rated 2,590kW at 1,000RPM driving two pumps, each rated at 2,400m3/h, and a pair of 1,800m3/h main engine-driven pumps. Auxiliary power is provided by a pair of CAT C-18 diesel gensets, each rated 275ekW. “Mojaweb” was designed to have a minimum bollard pull of 60 tonnes ahead and 12kn minimum free running speed.

Marcon International, Inc. Tug Boat Market Report – February 2011

www.marcon.com

Details believed correct, not guaranteed. Offered subject to availability.

19

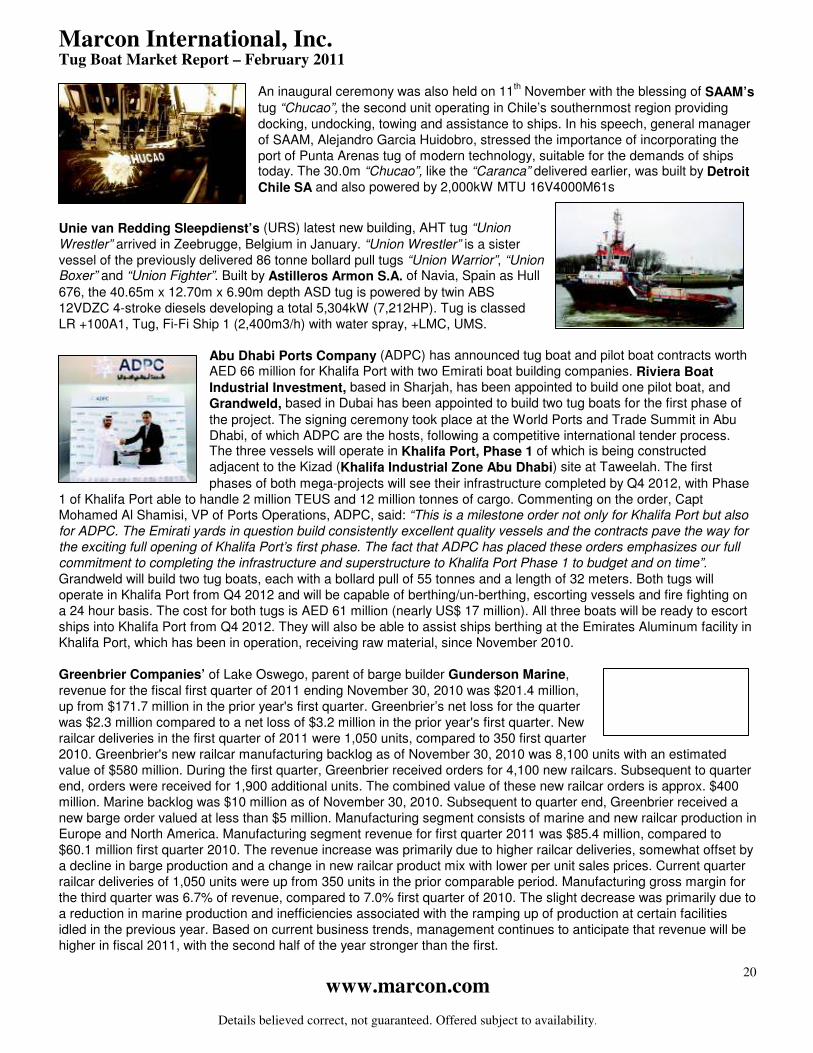

Multraship Towage & Salvage BV christened its two newest ASD multipurpose tugs in a special ceremony at the Portaal van Vlaanderen in Terneuzen, the Netherlands, on 4

th February. Joan Nuijten-Muller of Multraship performed the

christening ceremony on “Multratug 18”, which was delivered in 2009 by the Vega Shipyard in Bandirma, Turkey. “Multratug 18” is 35.7m x 11.50 m, and is designed for a multi-role capability for harbor, escort and sea towage as well as fire-fighting and salvage roles. It is chiefly employed in a deep-sea role, but can be deployed as and when needed in the River Scheldt area. “Multratug 18” has FiFi 1 fire-fighting, salvage, escort towage and oil recovery notations, and is powered by two ABC 8DZC diesels, which deliver 70 tons bollard pull. It has a double drum winch aft and a single drum winch forward and a free running speed of 13.5 knots. Tug is classed by Italian classification society RINA and is registered under the Dutch flag. Eline Muller of Multraship, meanwhile, christened “Multratug 3”, which was built in Vietnam by Damen Shipyards and delivered to Terneuzen in late December 2010. “Multratug 3” will mainly operate for Antwerp Towage NV, a 50/50 joint venture between Multraship and Fairplay Towage, but will also be available for emergency response work, including fire-fighting, in the River Scheldt area. With FiFi fire-fighting, a max bollard pull of 94.7 tonnes, an overall length of 32.14m and beam of 13.29 m, “Multratug 3” is capable of a speed of 14.7 knots. It is classed by Lloyd’s Register and is registered under Dutch flag. Powered by twin CAT C280-8s, she is currently the strongest tug in the area. Also on display at the christening ceremony was Multraship’s floating sheerlegs “Cormorant”, recently upgraded to 600 tonnes lifting capacity and with its new A-frame proudly in place.

Both new 28.3m x 12.0m x 6.0m draft, 90 tonne bollard pull URAG Unterweser Reederei GmbH RT-80r design tugs “Geeste” and “Hunte” are already in business in the port of Bremerhaven after the ships christening ceremony on 3rd of December 2010. Powered by three ABC 8DZC diesels driving three Schottel 1215 CP azimuthing thrusters, the Germanischer Lloyds classed Rotor tugs were built by ASL Shipyard Pte. Ltd. in Singapore. Since 1890 Unterweser-Schleppschifffahrtsgesellschaft - the present Unterweser Reederei GmbH - has operated on the river Weser with their tugs.