topic - media- · pdf filemining cvc corporate venture capital evca european private equity...

TRANSCRIPT

EMMA Conference 2015

Hamburg, 28-29 May 2015

Hosted by the Business School of the University Hamburg

Development and Sustainability in Media Business

Topic:

New Business Development in the Media Industry: An Analysis of Media Firms Corporate Venture Capital Investments

II

Topic:

New Business Development in the Media Industry: An analysis of Media Firms Corporate Venture Capital Investments

Keywords: Corporate Venturing, Corporate Venture Capital, Private Equity, Innovation, Digitalization, Strategy

Table of Content Table of Figures ....................................................................................................................... III

Abbreviations ........................................................................................................................... III

Abstract ...................................................................................................................................... 1

1 Introduction ............................................................................................................................. 1

2 The Market of Corporate Venture Capital .............................................................................. 2

2.1 Structure, Participants and Objectives .................................................................. 2

2.2 History of Corporate Venture Capital .................................................................. 4

3 Methodology ........................................................................................................................... 5

3.1 Data Source .......................................................................................................... 6

3.2 Data Set ................................................................................................................ 7

4 The Upswing of Media CVC .................................................................................................. 8

4.1 General Development ........................................................................................... 8

4.2 Organizational Mode ............................................................................................ 9

4.3 Industry Focus .................................................................................................... 12

5. Discussion ............................................................................................................................ 13

6. Further Research .................................................................................................................. 14

Appendix A: Stage of Finance ................................................................................................. 16

Reference List .......................................................................................................................... 17

III

Table of Figures

Figure 1: Simplified Structure of CVC- & VC-Investments .......................................... 4

Figure 2: Longitudinal Analysis of CVC Deals ............................................................. 9

Figure 3: Organizational Structure of CVC Investments ............................................. 10

Figure 4: Transaction Structure of CVC Investments .................................................. 11

Figure 5: Stage of Financing of CVC Investments ...................................................... 12

Figure 6: Industry Sectors of CVC investments ........................................................... 13

Figure 7: Non-Internet vs. Internet-related CVC investments ..................................... 13

Abbreviations

CRSIP-DM Cross Industry Standard Process of Data-

Mining

CVC Corporate Venture Capital

EVCA European Private Equity & Venture

Capital Association

IfM German Institute of Media and

Communication Policy

NVCA National Venture Capital Association

PE Private Equity

TIME Telecommunication, Information, Media

and Entertainment

VC Venture Capital

1

Abstract

The fast changing and highly competitive media environment forces media firms to

overcome their technology-avers behavior and adapt emerging technologies and business

models. To do so, media firms use corporate venture capital (CVC) as an investment approach

to cooperate with young and innovative start-ups. The presented paper examines the structure,

patterns and investment focus of media firms and shows the increasing importance of CVC

activities for media firms to deal with the requirements of the increasing cost, speed and

complexity of a technology driven industry. The paper closes by highlighting the importance

of CVC research for the field for strategic media management and describing the needs of

further analysis.

1 Introduction

The highly technology-driven media industry (Lojewski, 2010, p. 20) faces new

challenges and far-reaching structural changes along the whole media value chain (Hass, 2011,

p. 48). Emerging technologies allow new market entries, blur established market and industry

boundaries and lead to an increasing competition between established media firms (print, TV,

radio) as well as between new and old media sectors (Clasen, 2013, p. 42; Lojewski, 2010,

p. 21; Sullivan & Yuening, 2010, p. 26). While start-ups already use the technology

developments to target customers that once primary belonged to mass media (van Weezel,

2010, p. 47), established media firms still struggle with the new and rapidly changing media

environment (Hirt & Willmott, 2014, p. 1; Picard, 2011, p. 5). One example is the success of

content-sharing platforms and social networks, which shows that media firms misinterpret

technology changes, even if they attack their traditional business models. Often firms from

related industries, like the TIME-sector, use the technology developments to develop new

media businesses (Baumann & Hasenpusch, 2014, p. 11).

An innovative management approach to develop new and adjust old business models is

corporate entrepreneurship with its sub-segment corporate venturing (Brockmann, 1998, p. 88;

Fuchs, 2013, p. 62). To cope with the increasing speed, cost and complexity of a technology-

driven industry (Vanhaverbeke, Duysters, & Noorderhaven, 2002) and to overcome their

technology-averse behavior (Hipp, 2003, pp. 251–252; Knyphausen-Aufseß, 2005, p. 27),

media companies increased their external corporate venturing activities (Shao, 2010, p. 22). A

special venture form for uncertain market conditions is corporate venture capital (Hass, 2011,

p. 57). Referring to the structural changes within the media sector, it is not surprising that the

2

corporate venture capital (CVC) investments increased significantly within the last years

(PWC, 2013; Rzesnitzek, Buchwaldt, Ha, & Rupertl, 2013). Despite the growing practical

relevance and the potential of corporate venturing for new products and market entries,

corporate venturing has still been a neglected topic within media (entrepreneurship) literature

(Hang & van Weezel, 2007, p. 64). While empirical studies investigating patterns of CVC

investments on the whole (e.g. BCG, 2012; Gompers & Lerner, 1998; Knyphausen-Aufseß,

2005; Macmillan, Roberts, Livada, & Wang, 2008; PWC, 2013; Siegel, Siegel, & Macmillan,

1988; Sykes, 1990), industry focused studies are rare or, in case of media (entrepreneurship)

literature, are limited to case studies (e.g. Bernhardt, 2009; Hass, 2011; Hipp, 2003). The author

believes that a comprehensive summary of media firms CVC activities will help to understand

the entrepreneurial behavior of media companies and support future research projects within

the field. Furthermore, it highlights how the aforementioned changes due to the digitalization

(blurring boundaries, increasing competition, new market participants etc.) in combination with

the characteristics of media firms (e.g. absence of classic R&D units) affect CVC investments.

Therefore, the aim of the paper is to analyze the structure, patterns and investment focus of

media firms CVC activities.

To capture media firms CVC investments, the author conducts a data-mining project

based on secondary data provided by the Thomson Reuters private equity database1. The

Thomson Reuters database is widely accepted as a scientific resource and used by most of CVC

studies (BCG, 2012; Dushnitsky, 2011; Macmillan et al., 2008).

The paper starts with describing the CVC market incl. its historical development, so that

all results can be evaluate against past developments. After the market description, the paper

describes and explains the methodology including all underlying data criteria. The following

result section present the findings regarding structure, patterns and investment focus showing

the increasing importance of media CVC investments to overcome media firms technology-

avers behavior. The paper closes with a discussion of the findings and interests of further

research.

2 The Market of Corporate Venture Capital

2.1 Structure, Participants and Objectives

Corporations involved in CVC activities act on the private equity (PE) market. The

European Private Equity and Venture Capital Association (EVCA) defines PE as a “form of

equity investments into private companies not listed on the stock exchange” (EVCA, o.J.b).

1 Previously known as VentureXpert

3

Besides equity investment, PE investments receive managerial support of the investee company

and include venture capital (VC) as well as buyout investments. As a sub-form of PE, venture

capital is a high-risk, but calculable investment type with high-reward opportunities

(Neubecker, 2006, p. 12; Picard, 2011, p. 187). In contrast to PE, VC-investments describe

minority stake investments into young entrepreneurial companies in their early development

phases (EVCA, o.J.a, p. 10; Freese, 2006, p. 12; Maula, Autio, & Murray, 2005, p. 5; Poser,

2003, p. 36).

The VC market divides into a formal and informal market (Brinkrolf, 2002, p. 17) with

dependent and independent participants (Maula et al., 2005, p. 4). While the informal market

only covers investments by private individuals (family, friends, founders, and business angels)

the formal market subdivides into CVC as a dependent, corporation-backed investment-type

and VC as independent participants backed by financial institutions (banks, financial service

companies etc.).1 Therefore, CVC investments are defined as minority equity investments in

entrepreneurial and innovative start-up companies by established corporations (Dushnitsky &

Shaver, 2009, p. 1046; Napp & Minshall, 2011, p. 27; Narayanan, Yang, & Zahra, 2009, p. 59;

Van de Vrande, Vareska & Vanhaverbeke, 2013, p. 1020).

According to the origin of capital, VC & CVC firms focus on different objectives

(financial vs. strategic). While VC firms aim to increase their financial performance, CVCs

activities are mainly led by strategic objectives (Knyphausen-Aufseß, 2005, p. 15; Macmillan

et al., 2008, p. 1; Neubecker, 2006, p. 1).2 The most cited strategic objectives are: window on

technology, supporting existing business, window on new markets, develop new products,

diversification, increasing demand and commercialization of idle resources and competences

(Macharzina & Wolf, 2012, p. 763; Macmillan et al., 2008, p. 9; Neubecker, 2006, p. 57). Even

so financial issues are less relevant to evaluate CVCs overall performance, it is definitely

significant for internal justification to compare CVC to other development approaches (Sykes,

1990, pp. 45–46). Furthermore, it sounds logical that financial and strategic success are

correlated even so scientific literature has discordant opinions (Neubecker, 2006, pp. 63–64).

According to the described differences, CVC and VC firms have advantages and

disadvantages for start-up companies and therefore, are often seen as complements (Maula et

al., 2005, p. 4). While CVC offer additional reputation, a distribution network, industry contacts

1 Governmental or public investment firms are additional participants of the formal VC market, but will not be

covered in this study due to the focus on CVC investments 2 Besides financial and strategic objectives, CVC has a third objective: social responsibility. The reasoning is that

the increasing availability of corporate venture capital lead to more employment. This macroeconomic point of view is not part of this study.

4

and R&D activities (Knyphausen-Aufseß, 2005, p. 25), VC firms have better contacts and

access to capital markets (Neubecker, 2006, p. 110).

Figure one shows - in a simplified manner - the investment possibilities for established

corporations to engage on the VC market. To invest, corporations can set up an external CVC-

unit or an internal business unit to search for and execute deals. Furthermore, corporations can

act on the VC market through subsidiaries (e.g. Bertelsmann via RTL Ventures). All three CVC

investment forms are direct investments because of a direct connection between the parent

company and the start-up. Another indirect opportunity to act on the VC market is as an investor

of a VC firm (limited partnership). Both forms have several advantages and disadvantages for

parent companies. If new on the VC market, it might be a good idea to focus on indirect

investments to get to know the VC business before setting up a CVC unit. The disadvantages

of these indirect investments are a lack of control as well as more difficulties to interact with

the start-up and create strategic synergies. Overall, only 10 percent of CVC investments are

indirect investments by dedicated or non-dedicated funds (Macmillan et al., 2008, p. 7). A

further investment type are syndicate investments. In syndicate investments more than one

venture capital party (whether VC, CVC or private individuals) invest in one start-up at the

same time. This is another way to interact and learn from venture capitalists by combining the

advantages and disadvantages of both investment types for CVCs.

Figure 1: Simplified Structure of CVC- & VC-Investments Source: According to Neubecker (2006, p. 22)

2.2 History of Corporate Venture Capital

CVC activities correlate with the stock market and therewith have a similar cyclical

curve (Morris, Kuratko, & Covin, 2007, p. 85). Besides stock markets and the general economic

well-being the engaging of established companies via CVC investments depends mainly on

political decisions (e.g. tax regulations) as well as technology developments (Bygrave, Hay, &

5

Peeters, 1999, p. 262; Bygrave & Timmons, 1992, p. 281). Therefore, analyzing the historical

developments of CVC activities shows a cyclical structure affected by the aforementioned

factors (BCG, 2012, p. 4; Dushnitsky, 2011, pp. 48–49). Thereby, the development between

USA and Europe is very similar (Freese, 2006, p. 2) and divided in four waves (BCG, 2012).

The first wave started at the beginning of 1960 and was driven by strategic objectives

(Neubecker, 2006, p. 53) to enhance established companies innovation capabilities (Macharzina

& Wolf, 2012, p. 757). The triggers for this wave were the success of independent VC firms in

combination with an ongoing growth on the US stock market (BCG, 2012, p. 4). However, due

to missing organizational integration, established companies failed to raise the strategic

potential and started to disinvest (Stein & Klein, 2005, pp. 588–589). Nevertheless,

corporations realized the financial benefits, which in combination with tax allowances and a

new regulation of pension funds (BCG, 2012, p. 4; Rind & Kenneth W., 1981, p. 171) led nearly

directly to a second wave in the mid-70s (Neubecker, 2006, p. 53). The second wave ended

with the economic crisis 1987 (Stein & Klein, 2005, pp. 588–589) just to recover in the 90s due

to the internet leading to a massive increase of the stock market, ending in the internet bubble

burst in 2001 (Stein & Klein, 2005, pp. 588–589). While the first wave was motivated by

strategic and the second by financial interest this third wave combined both objectives

(Neubecker, 2006, p. 53).

Since 2003 the last wave of CVC activities is going on (BCG, 2012, p. 4; Dushnitsky,

2011, pp. 48–49) with a short downturn in 2007, according to the financial crisis. The indicators

for this last wave are: globalization, technology development, missing internal capabilities for

new innovations (BCG, 2012, p. 4) and growing market intensity (Fulghieri & Sevilir, 2009,

p. 1292). These characteristics align with the ongoing strategic challenges of media firms and

therefore, an analysis of media firms CVC activities looks promising to provide insides into the

strategic behavior of media firms. Furthermore, the ongoing activities and the start of CVC just

after the economic downturn in 2007 (Battistini, Hacklin, & Baschera, 2013, p. 32; Dushnitsky,

2011) indicate that CVC activities start to become a serious innovation and development tool

(BCG, 2012, p. 12).

3 Methodology

The aim of this research project is to describe the overall CVC activities of media firms.

Therefore, the paper implement an empirical investigation of secondary data. In most instances,

secondary-data analysis are less time-consuming than primary data collections and are preferred

whenever suitable to answer a given research question (Kuß, Wildner, & Kreis, 2014, p. 37).

In contrast to the advantages of secondary analysis regarding the easy, fast and cheap access to

6

excessive data (Bruhn, 2014), secondary data is usually been collected for a different or general

purpose and therewith, do not fit to answer precise research questions as primary data collection

would. Furthermore, a lot of time and effort is needed to understand the methods, accuracy and

aggregation level of the provided data (Kuß et al., 2014, pp. 28–29). Therefore, secondary-data

analysis are suitable to state general propositions about overall strategic trends and

developments. To investigate the underlying motivation or intend behind a strategic decision,

primary-data analysis including in-depth interviews should be preferred. For the aim of this

paper to explore the general usage media CVC activities, an extensive secondary analysis fits

best.

The results of a secondary-data analysis depend highly on the quality of the available

data set. Thereby, the quality is as important as the handling (e.g. data preparation, cleaning) of

the provided data set. To create a high-quality data set, the paper follows the cross industry

standard process of data-mining (CRSIP-DM). The CRSIP-DM is a non-proprietary, well-

documented and free data-mining process developed by industrial companies and over 200

data-mining experts. The aim of the CRISP-DM is to provide a guideline for data-mining

projects to enhance their quality. (Shearer, 2000, p. 13) To do so, the process differentiates

between the steps: business understanding, data understanding, data preparation, modelling,

and evaluation/ deployment. While section 2 provided the business understanding, section 3

covers data understanding and preparation, before the results are presented (section 4) and

evaluated (section 5).

3.1 Data Source

The data for this data-mining project is provided by the Thomson Reuters PE database.1

It is the most used database for PE scientific research (Dushnitsky & Lavie, 2010, p. 32;

Dushnitsky & Lenox, 2005a, p. 952; Krebs, 2012, pp. 193–194; Krohmer, 2008, p. 7; Landau,

p. 249; Zipser, 2008, p. 100). Despite the acceptance, there are numerous of limitations. Firstly,

the database documents only between 30 to 50 percent of all investments (Neubecker, 2006,

p. 183). Secondly, analysis showed that data for the European market is only reliable covered

since 1997 (Dushnitsky & Shaver, 2009, pp. 1050–1051; Hege, Palomino, & Schwienbacher,

2006, p. 9; Neubecker, 2006, p. 183). Reasons for this might be the increasing (scientific)

interest in CVC (Zipser, 2008, p. 109), the ongoing technological developments for databases

as well as increasing European market activities. To sum up, the data set provided by Thomson

Reuters shows a tendency to current investments of the US and European market. Despite the

1 Previously known as VentureXpert

7

limitations, data samples based on the PE module are representative for the PE and VC market

(Zipser, 2008, p. 111).

3.2 Data Set

Starting point for the data sample are the CVC activities of the worldwide top 50 media

firms according to their revenues in the year 2014 and the definition by the institute of media

and communication policy (IfM).1 Covering the biggest media conglomerates regarding

revenues ensures that all included media firms have enough financial power to act on the VC

market. Additionally, it reduces regional or sector differences by assuming that the top 50 media

conglomerates are spread across the world and act in all media sub-sectors (print, TV, radio

etc.).

The underlying assumption of the compiled data set is that strategic and not financial

interests are the reason for the increasing media firms CVC activities. This assumption is based

on the characteristics of the actual wave of CVC activities (see section 2), the strategic

challenges media firms face in the digital age (Jung, 2009, p. 46; Küng, 2009, pp. 82–83) and

the empirical evidence that CVC activities are mostly execute for strategic reasons (BCG, 2012;

Knyphausen-Aufseß, 2005; Macmillan et al., 2008; Sykes, 1990). Regarding the assumption,

the study includes only direct CVC investments between 2002 and 2014. Direct investments

are per definition a direct connection between parent companies and start-ups and therefore,

show the highest strategic intend of all CVC investments (Neubecker, 2006). Buyout deals as

part of the PE market as well as indirect investments and investments via pension funds or

evergreens are not part of this study.2 While buyout deals have a slightly different strategic

motivation, indirect investments as well as for example pension funds are strongly motivated

by financial interests and therefore incompatible with the underlying assumption of this paper.

The chosen timeframe from 2002 to 2014 covers the last and still ongoing wave of CVC,

which is characterised by strategic investment decisions according to changes in technology

and market environment (see section 2). Therefore, the timeframe perfectly fits the underlying

assumption of this paper. Additionally, the timeframe do not interfere with the limitations of

the provided data regarding the coverage of European CVC activities (see section 3.1)

1 The IfM define media firms as mass media companies who provide publicist content and earn most of their

revenues via licensing, property rights or advertising. Further on, companies are covered which have a high influence on communication, because of extensive production and distribution power (Institut für Medien- und Kommunikationspolitik, 2014)

2 Even so, dedicated funds financed by parent companies and managed by VC firms might be strategic relevant, the author has the opinion that the strategic value of indirect investments is insignificant compared to direct investments. Furthermore, only 10 percent of all CVC deals are indirect investments according to MacMillan et al. (2008). Therefore, the author excluded indirect investments no matter if via dedicated or non-dedicated funds from the study.

8

For the purpose of investigation of all transactions1 of business units, subsidiaries and

external CVC units of media firms the author aggregates the data on the firm and industry level.

With reference to the ownership structure of media firms and the fact that the database only

offers the actual parent company of a subsidiary, the author investigated changes in the

ownership structure of subsidiaries to ensure the right mapping between each transaction and

the parent company. Respecting all data criteria, 24 of the top 50 media firms were involved in

CVC deals during the covered timeframe investing in 628 start-ups through 906 deals resulting

in 961 transactions.

The next section compares media firms CVC activities with the overall CVC industry2

regarding structure, patterns and investment focus. Furthermore, the paper refers to a study

conducted by Macmillan et al. (2008) in cooperation with the National Venture Capital

Association (NVCA). The study investigates general CVC activity with the purpose of

innovation by using industry data (provided by Thomson Reuters) as well as survey data to

describe trends and characteristics between 2004 and 2006. The overlapping timeframe as well

as a similar database allows a comparison between this paper and the study conducted by

Macmillan et al. (2008).3

4 The Upswing of Media CVC

4.1 General Development

Comparing the historical development of media firms CVC activities with the overall

development (see section 2.2) confirms the widely cyclical nature for media firm investments

(see figure 2). However, closer investigation of the last CVC wave (2002 - today) shows that

media firms’ activities are not as heavily affected by the financial crisis as the remaining firms.

While the general deal activity dropped by 44 percent, media firms deal activity remained

stable. Furthermore, after the financial crisis general deal activity only increased by 81 percent

while media firms’ activities increased by 226 percent. One reason for this is the dominant role

of Google Inc. on the (media) CVC market. Google Inc. is responsible for about 40 percent of

media firms’ transactions per year since 2010.4 Since 2011, Google and Yahoo Inc. classify as

media firms according to the IfM. Before, the two firms were classified as internet companies.

1 Because more than one firm can be involved in a deal (see section 2: syndicate investment), a differentiation is

necessary between deals and transactions. One deal might have more than one transaction, according to the number of firms involved in the deal. If not explicitly said, further statistics are based on transactions.

2 The sample of the CVC industry underlies the same criteria as the media firm sample 3 Regarding the ongoing and daily updating of the Thomson Reuters private equity database, a comparison between

studies from different years – even so they use similar criteria – needs to be still handed carefully 4 Since 2010, Google Ventures was involved in 264 transactions.

9

According to the dominant role, in addition with the classification as internet companies, the

author excludes Google Inc. and Yahoo from further analysis. Therewith, the paper focuses on

“old” media firms- This restriction is in line with the assumption that media firms do CVC for

strategic and innovative reasons to deal with the changing environment and new market

participants.1 However, even after excluding “internet-based” media firms, media firms’ deals

increased by 126 percent since 2009 and therewith still indicate the over proportional

importance of CVC for media firms. Without Google and Yahoo, the sample contains 22 media

firms’ investing in 427 start-ups through 641 deals (686 transactions).

Figure 2: Longitudinal Analysis of CVC Deals Source: Own illustrations based on Thomson Reuters PE (Selection: All VC Deals of Corporate PE/ Venture)

4.2 Organizational Mode

As described in section 2.1 corporate venture capitalists have different opportunities to

pursue CVC investments. According to the National Venture Capital Association (2014, p. 1)

a differentiation between investment vehicles is important due to the increasing role of

corporate investors.2 Only a few earlier studies already differentiate between investment

vehicles like business unit, subsidiary, external unit or limited partnership. Relying on direct

investments, the paper distinguish between business unit, subsidiary and external CVC unit. To

do so, the author analyzed the acquiring fund of each transactions. According to the acquiring

fund name and a web-research, the author assigned one of the above-mentioned organizational

1 Google Inc. as well as Yahoo Inc. might be interesting case study. Furthermore, enlarging the sample with more

internet-based media firms might give further insights into the media CVC market (see section 6: further research)

2 The NVCA is about to change its methodology by 2015 to consider the increasing role of corporate investors and the organizational mode.

10

forms to get deeper insights into the organizational structure of media firms CVC activities.1

The assumption is that an external unit shows a more comprehensive CVC approach as e.g. the

set-up of an internal business unit. Therefore, the more external units are in the data sample, the

higher the strategic importance of CVC for media firms.

Figure 3: Organizational Structure of CVC Investments

Source: Own illustrations based on Thomson Reuters PE

Each of the investigated media firms has at least one dedicated business or external

CVC-unit to act on the venture capital market. The most used organizational form is an external

CVC unit (42%) followed by business units (36%) and subsidiaries (7%). Therewith, media

firms have more external units than the overall CVC industry (35 %) as examined by Macmillan

et al. (2008, p. 11). The installment of an external CVC unit indicates a high commitment to

CVC and explains the over-proportional percentage of transactions conducted by this

investment vehicle (82%).

Most of the investments with media firms involved are syndicate investments (88%).

Thereby, 13 percent of all transactions were deals with two or more media firms involved, while

75 percent of all transaction were in cooperation with other investors (see figure 4). This result

matches with the overall CVC practice were less than half of CVC invest alone (Macmillan et

al., 2008, p. 16). One reason for the high number of syndicate investments of CVC firms is, that

more than 85 percent use cooperations with independent VC firms as their main source for

investments (Macmillan et al., 2008, p. 15)

1 For Example: If the fund name included a legal status and differed from the parent company, the fund is a

subsidiary or external unit. To confirm these assumptions, the author conducted a web-research regarding the fund name.

11

Figure 4: Transaction Structure of CVC Investments

Source: Own illustrations based on Thomson Reuters PE

Regarding the strategic objectives of CVC investment it is further necessary to

investigate the financial stage of investments and therewith, if a firm invest in companies with

a more or less proven concept (Macmillan et al., 2008, p. 3).1 Compared with the rest of CVC

firms, media firms conduct less seed but over proportional early-stage investments. Therefore,

it cannot be said – by referring to the stage of financing – that media firms CVC investments

are less or more risky than of the rest of the CVC industry. Furthermore, media firms undo

fewer investments in the expansion or later-stage (see figure 5). Therefore, media firms need

more than a good sounding concept for investments, but once a first prototype or commercially

viable product exist, they are willing to invest. The slightly under-proportional number of

investments in the expansion stages is surprising, because companies in the expansion stage

need increasing marketing activities and know-how, a field where media companies with their

market power could really help to make the investment successful.

1 The literature proposes different definitions and concepts to subdivide financial stages. This paper follow the

classification suggested by the NAVCA and Thomson Reuters (see appendix 1)

12

Figure 5: Stage of Financing of CVC Investments

Source: Own illustrations based on Thomson Reuters PE

4.3 Industry Focus

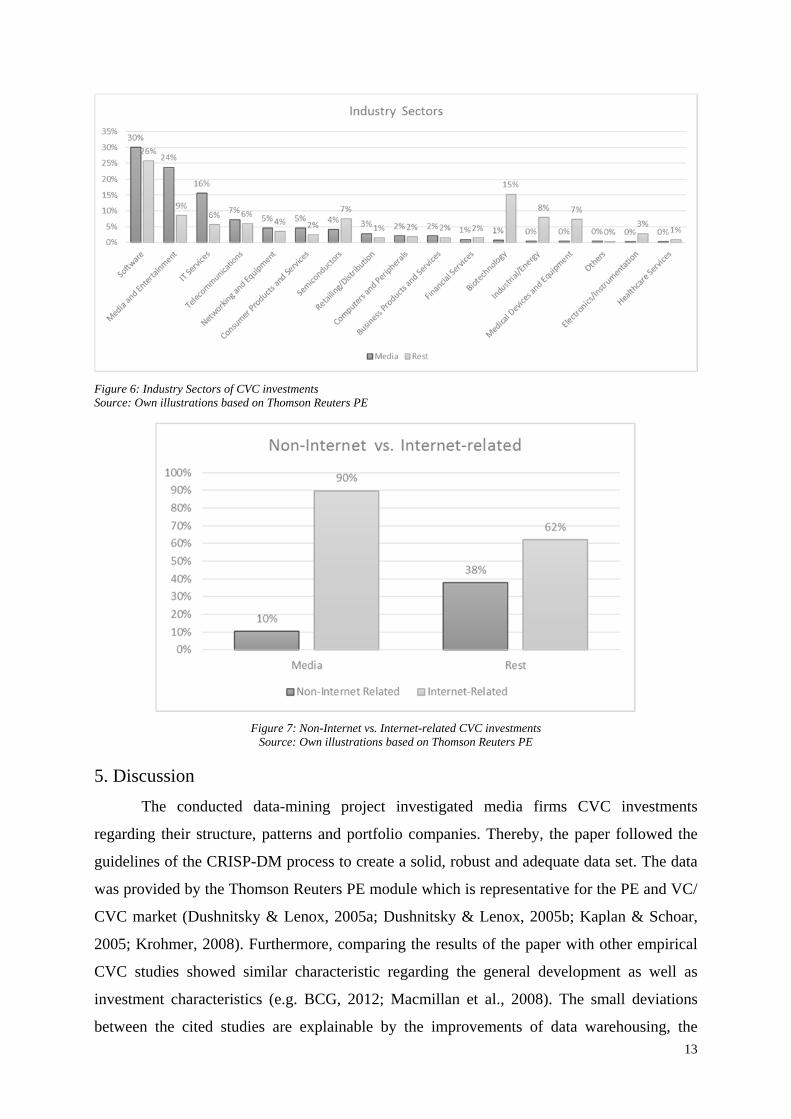

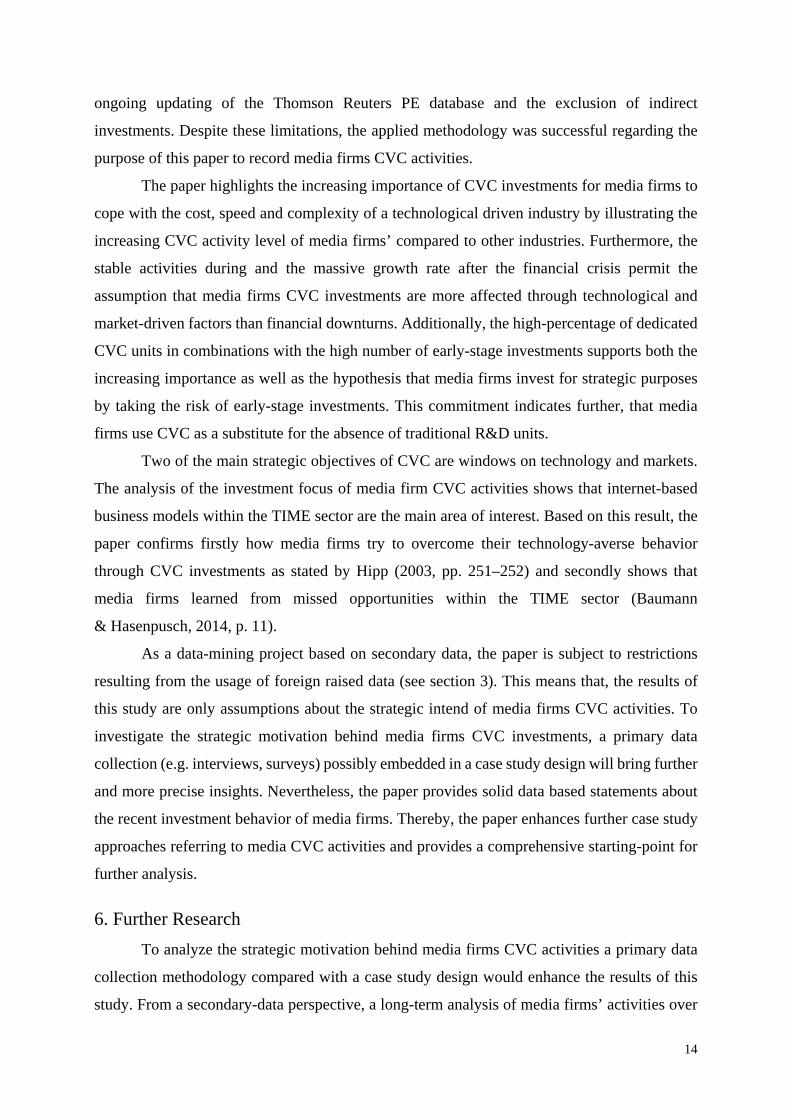

As important as analysing when and how media firms pursue CVC investments, it is to

investigate the targeted start-ups (see figure 6). Looking at the industry sectors1 of start-ups

supported by media firms’ shows that about 80 percent of all investments belong to the

telecommunication, information, media and entertainment (TIME) sector. Only nearly a quarter

of all investments belong to the media and entertainment branch (24%), which is the second

most invested sector behind software (30%) and before IT services (16%). Compared to the rest

of CVC firms, media companies invest over proportional into software, IT services and media-

related companies and ignore unrelated business sectors like biotechnology, industrial/energy

or medical devices and equipment. Additionally, the focus on a broad range of IT investments

shows the comparison of start-ups regarding their internet involvement (see figure 7). About 90

percent of all start-ups supported by media firms provide internet-based business while only 62

percent of the remaining CVC industry activities are investments in internet-related companies.

1 The industry structure is based on a definition of the NVCA and Thomson Reuters due to the VEIC branch codes.

13

Figure 6: Industry Sectors of CVC investments Source: Own illustrations based on Thomson Reuters PE

Figure 7: Non-Internet vs. Internet-related CVC investments

Source: Own illustrations based on Thomson Reuters PE

5. Discussion

The conducted data-mining project investigated media firms CVC investments

regarding their structure, patterns and portfolio companies. Thereby, the paper followed the

guidelines of the CRISP-DM process to create a solid, robust and adequate data set. The data

was provided by the Thomson Reuters PE module which is representative for the PE and VC/

CVC market (Dushnitsky & Lenox, 2005a; Dushnitsky & Lenox, 2005b; Kaplan & Schoar,

2005; Krohmer, 2008). Furthermore, comparing the results of the paper with other empirical

CVC studies showed similar characteristic regarding the general development as well as

investment characteristics (e.g. BCG, 2012; Macmillan et al., 2008). The small deviations

between the cited studies are explainable by the improvements of data warehousing, the

14

ongoing updating of the Thomson Reuters PE database and the exclusion of indirect

investments. Despite these limitations, the applied methodology was successful regarding the

purpose of this paper to record media firms CVC activities.

The paper highlights the increasing importance of CVC investments for media firms to

cope with the cost, speed and complexity of a technological driven industry by illustrating the

increasing CVC activity level of media firms’ compared to other industries. Furthermore, the

stable activities during and the massive growth rate after the financial crisis permit the

assumption that media firms CVC investments are more affected through technological and

market-driven factors than financial downturns. Additionally, the high-percentage of dedicated

CVC units in combinations with the high number of early-stage investments supports both the

increasing importance as well as the hypothesis that media firms invest for strategic purposes

by taking the risk of early-stage investments. This commitment indicates further, that media

firms use CVC as a substitute for the absence of traditional R&D units.

Two of the main strategic objectives of CVC are windows on technology and markets.

The analysis of the investment focus of media firm CVC activities shows that internet-based

business models within the TIME sector are the main area of interest. Based on this result, the

paper confirms firstly how media firms try to overcome their technology-averse behavior

through CVC investments as stated by Hipp (2003, pp. 251–252) and secondly shows that

media firms learned from missed opportunities within the TIME sector (Baumann

& Hasenpusch, 2014, p. 11).

As a data-mining project based on secondary data, the paper is subject to restrictions

resulting from the usage of foreign raised data (see section 3). This means that, the results of

this study are only assumptions about the strategic intend of media firms CVC activities. To

investigate the strategic motivation behind media firms CVC investments, a primary data

collection (e.g. interviews, surveys) possibly embedded in a case study design will bring further

and more precise insights. Nevertheless, the paper provides solid data based statements about

the recent investment behavior of media firms. Thereby, the paper enhances further case study

approaches referring to media CVC activities and provides a comprehensive starting-point for

further analysis.

6. Further Research

To analyze the strategic motivation behind media firms CVC activities a primary data

collection methodology compared with a case study design would enhance the results of this

study. From a secondary-data perspective, a long-term analysis of media firms’ activities over

15

all CVC waves will help to evaluate the presented findings regarding the general differences

between media firm investments and other industry sectors.

Due to the market challenges of media firms (new participants, increasing competition,

and blurring boundaries), a segmentation between media sectors (print, TV, radio) as well as

between new and old media will give deeper insights into strategic objectives and usage of CVC

to overcome these obstacles. By the exclusion of “internet-based” media firms (Google and

Yahoo Inc.), the study already indicates that media firms’ CVC activity rates differ widely

between media firms, which supports a segmentation approach. Therefore, enlarging the data

set in terms of number of firms as well as with more criteria about media conglomerates

regarding ownership structure (e.g. family business, financial investors, formerly VC-backed

etc.), financial indicators (e.g. turnover), core business (new old media; TV, print, radio,

internet) and general information (e.g. region) looks promising.

From a networking perspective, a topic of interest may be the interlocking of media

firms through CVC investments. Do the same media firms act as co-investors repeatedly? Do

they form some kind of CVC alliances? Has it any consequences regarding regulation issues?

In summary, media corporate venturing is still a neglected topic and especially the usage

of CVC as special investment form is an underexplored research field. Thereby, the usage of

CVC by media firms will help to understand the development of the media sector as well as

single strategic firm approaches, which will not only be relevant for media conglomerates, but

also for firms and industries facing similar challenges.

16

Appendix A: Stage of Finance

Stage of Finance Stage Definitions Seed Stage This stage is a relatively small amount of capital

provided to an inventor or entrepreneur to prove a concept. This involves product development and market research as well as building a management team and developing a business plan, if the initial steps are successful. This is a pre-marketing stage.

Early Stage This stage provides financing to companies completing development where products are mostly in testing or pilot production. In some cases, product may have just been made commercially available. Companies may be in the process of organizing or they may already be in business for three years or less. Usually such firms will have made market studies, assembled the key management, developed a business plan, and are ready or have already started conducting business.

Expansion Stage This stage involves working capital for the initial expansion of a company that is producing and shipping and has growing accounts receivables and inventories. It may or may not be showing a profit. Some of the uses of capital may include further plant expansion, marketing, working capital, or development of an improved product. More institutional investors are more likely to be included along with initial investors from previous rounds. The venture capitalist’s role in this stage evolves from a supportive role to a more strategic role.

Later Stage Capital in this stage is provided for companies that have reached a fairly stable growth rate; that is, not growing as fast as the rates attained in the expansion stages. Again, these companies may or may not be profitable, but are more likely to be than in previous stages of development. Other financial characteristics of these companies include positive cash flow. This also includes companies considering IPO.

Source: National Venture Capital Association (2014, p. 115)

17

Reference List

Battistini, B., Hacklin, F., & Baschera, P. (2013). The State of Corporate Venturing: Insights from a Global Study. Research-Technology Management, 56(1), 31–39. Retrieved January 29, 2014.

Baumann, S., & Hasenpusch, T. C. (2014). Konvergierende Technologien - Konvergierende Geschäftsmodelle: Hybrid TV und Multiscreen. In C. Goutrié, S. Falk-Bartz, & I. Wuschig (Eds.), Think CROSS - Change MEDIA. Crossmedia im Jahr 2014 - Eine Standortbestimmung. Eine Standortbestimmung im Jahr 2014 (1st ed., pp. 11–27). Norderstedt: Books on Demand.

BCG (2012). Corporate Venture Capital: Avoid the Risk, Miss the Rewards. Retrieved February 11, 2014.

Bernhardt, V. (2009). Strategische Erneuerung von Medienunternehmen: Entwicklung dynamischer Fähigkeiten im Kontext radikalen Wandels. Bamberg: Difo-Druck GmbH.

Brinkrolf, A. (2002). Managementunterstützung durch Venture-Capital-Gesellschaften (Gabler Edition Wissenschaft). Wiesbaden: Deutscher Universitätsverlag.

Brockmann, M. (1998). Unternehmer in die Konzerne. impulse, (4), 88–92.

Bruhn, M. (2014). Marketing: Grundlagen für Studium und Praxis (12., überarb. Aufl). Wiesbaden: Springer Gabler.

Bygrave, W. D., Hay, M., & Peeters, J. B. (Eds.) (1999). The venture capital handbook. London: Financial Times.

Bygrave, W. D., & Timmons, J. A. (1992). Venture capital at the crossroads. Boston, Mass: Harvard Business School Press.

Clasen, N. (2013). Lost in Disruption? Media Innovator's Dilemma. Wie Medienunternehmen Technologiebrüche managen. MedienWirschaft, 10(4), 38–46.

Dushnitsky, G. (2011). Riding The Next Wave Of Corporate Venture Capital. Business Strategy Review, 2011(22), 44–49. Retrieved February 01, 2014.

Dushnitsky, G., & Lavie, D. (2010). How alliance formation shapes corporate venture capital investment in the software industry: a resource-based perspective. Strategic Entrepreneurship Journal, 4(1), 22–48. Retrieved June 02, 2014.

Dushnitsky, G., & Lenox, M. J. (2005a). When do firms undertake R&D by investing in new ventures? Strategic Management Journal, 26(10), 947–965. Retrieved June 02, 2014.

Dushnitsky, G., & Lenox, M. J. (2005b). When do incumbents learn from entrepreneurial ventures? Corporate venture capital and investing firm innovation rates. Research Policy, 34(5), 615–639. Retrieved June 02, 2014.

Dushnitsky, G., & Shaver, J. M. (2009). Limitations to interorganizational knowledge acquisition: the paradox of corporate venture capital. Strategic Management Journal, 30(10), 1045–1064. Retrieved April 16, 2014.

EVCA (o.J.a). The Little Book of Private Equity. Brüssel (BE). Retrieved March 12, 2015.

EVCA (o.J.b). What is private equity? Retrieved March 12, 2015, from http://www.evca.eu/about-private-equity/private-equity-explained/.

Freese, B. (2006). Corporate-Venture-Capital-Einheiten als Wissensbroker: Empirische Untersuchung interorganisationaler Beziehungen zwischen Industrie- und Start-up-Unternehmen. Gabler Edition Wissenschaft. Wiesbaden: Deutscher Universitäts-Verlag | GWV Fachverlag GmbH Wiesbaden.

18

Fuchs, A. (2013). Das strategische Management von Corporate Entrepreneurship: Empirische Kausalanalysen am Beispiel der deutschen Automobilindustrie. Wiesbaden: Springer.

Fulghieri, P., & Sevilir, M. (2009). Organization and Financing of Innovation, and the Choice between Corporate and Independent Venture Capital. Journal of Financial and Quantitative Analysis, 44(06), 1291. Retrieved April 16, 2014.

Gompers, P., & Lerner, J. (1998). The Determinants of Corporate Venture Capital Success: Organizational Structure, Incentives, and Complementarities. In R. K. Morck (Ed.), NBER-Conference Report. Concentrated Corporate Ownership (pp. 17–50). Chicago: University of Chicago Press.

Hang, M., & van Weezel, A. (2007). Media and Entrepreneurship: What Do We Know and Where Should We Go? Journal of Media Business Studies, 4(1), 51–70.

Hass, B. H. (2011). Intrapreneurship and Corporate Venturing in the Media Business: A Theoretical Framework and Examples From the German Publishing Industry. Journal of Media Business Studies, 8(1), 47–68.

Hege, U., Palomino, F., & Schwienbacher, A. (2006). Venture Capital Performance in Europe and the United States: A Comparative Analysis. SSRN,

Hipp, H. A. (2003). Corporate Venture Capital als Innovationsmotor in einem Medienunternehmen. In F. Habann (Ed.), Innovationsmanagement in Medienunternehmen. Theoretische Grundlagen und Praxiserfahrungen (pp. 249–273). Wiesbaden: Gabler Verlag.

Hirt, M., & Willmott, P. (2014). Strategic principles for competing in the digital age. Retrieved May 21, 2014.

Institut für Medien- und Kommunikationspolitik (2014). Ranking - Die 50 größten Medienkonzerne 2014. Retrieved January 19, 2015, from http://www.mediadb.eu/rankings/intl-medienkonzerne-2014.html.

Jung, J. (2009). Strategic Management in the Media: Theory to Practice, by Lucy Küng. International Journal on Media Management, 11(1), 46–47. Retrieved July 06, 2014.

Kaplan, S. N., & Schoar, A. (2005). Private Equity Performance: Returns, Persistence, and Capital Flows. The Journal of Finance, 60(4), 1791–1823. Retrieved January 16, 2015.

Knyphausen-Aufseß, D. zu (2005). Corporate Venture Capital: Who Adds Value? Venture Capital, 7(1), 23–49. Retrieved August 18, 2014.

Krebs, J. (2012). Syndizierung von Venture-Capital-Investitionen: Eine Analyse der Zusammenhänge mit dem Beteiligungserfolg. Schriften zum europäischen Management. Wiesbaden: Gabler Verlag.

Krohmer, P. (2008). Essays in Financial Economics: Risk and Return of Private Equity, Johann Wolfgang Goethe Universität, Frankfurt am Main. Retrieved January 15, 2015.

Küng, L. (2009). Strategic management in the media: From theory to practice (Reprinted). Los Angeles: SAGE Publ.

Kuß, A., Wildner, R., & Kreis, H. (2014). Marktforschung: Grundlagen der Datenerhebung und Datenanalyse (5., vollst. überarb. u. erw. Aufl. 2014). Wiesbaden, s.l: Springer Fachmedien Wiesbaden.

Landau, C. Wertschöpfungsbeiträge durch Private-Equity-Gesellschaften (1. Aufl. 2010). Gabler Research. Wiesbaden, Erlangen-Nürnberg: Gabler Verlag / Springer Fachmedien Wiesbaden GmbH Wiesbaden.

19

Lojewski, G. von (2010). Rundfunk und Fernsehen im digitalen Zeitalter. In M. Friedrichsen, J. Wendland, & G. Woronenkowa (Eds.), Schriften zur Medienwirtschaft und zum Medienmanagement: Vol. 26. Medienwandel durch Digitalisierung und Krise. Eine vergleichende Analyse zwischen Russland und Deutschland (1st ed., pp. 19–25). Baden-Baden: Nomos-Verl.-Ges.

Macharzina, K., & Wolf, J. (2012). Unternehmensführung: Das internationale Managementwissen ; Konzepte - Methoden - Praxis (8., vollst. überarb. und erw. Aufl). Lehrbuch. Wiesbaden: Springer Gabler.

Macmillan, I. C., Roberts, E., Livada, V., & Wang, A. (2008). Corporate Venture Capital (CVC) Seeking Innovation and Strategic Growth: Recent patterns in CVC mission, structure, and investment. Virginia (U.S.). Retrieved June 02, 2014.

Maula, M., Autio, E., & Murray, G. (2005). Corporate Venture Capitalists and Independent Venture Capitalists: What do they know, Who do They Know and Should Entrepreneurs Care? Venture Capital, 7(1), 3–21. Retrieved February 03, 2014.

Morris, M. H., Kuratko, D. F., & Covin, J. G. (2007). Corporate entrepreneurship and innovation: Entrepreneurial development within organizations (2. ed). Mason, Ohio: Thomson/South-Western.

Napp, J. J., & Minshall, T. (2011). Corporate Venture Capital Investments for Enhancing Innovation: Challenges and Solutions. Research-Technology Management, 54(2), 27–36. Retrieved April 16, 2014.

Narayanan, V., Yang, Y., & Zahra, S. A. (2009). Corporate venturing and value creation: A review and proposed framework. Research Policy, 38(1), 58–76. Retrieved February 04, 2014.

National Venture Capital Association (2014). NVCA Yearbook 2014. Arlington (U.S.). Retrieved November 10, 2014.

Neubecker, J. (2006). Finanzierung durch Corporate Venture Capital und Venture Capital (1. Aufl). Wiesbaden, Dresden: Gabler Verlag / GWV Fachverlage GmbH Wiesbaden.

Picard, R. G. (2011). The economics and financing of media companies (2nd ed). New York: Fordham University Press.

Poser, T. B. (2003). The Impact of Corporate Venture Capital: Potentials of Competitive Advantages for the Investing Company (Gabler edition Wissenschaft). Wiesbaden: Deutscher Universitätsverlag.

PWC (2013). MoneyTree Report. Retrieved March 01, 2014.

Rind, & Kenneth W. (1981). The Role of Venture Capital in Corporate Development. Strategic Management Journal, 2(2), 169–180. Retrieved December 15, 2014.

Rzesnitzek, M., Buchwaldt, A. von, Ha, S., & Rupertl, F. (2013). Neues-Kerngeschäft: Nicht-markenbezogene Online-Aktivitäten von Verlagen und TV-Sendern. Düsseldorf. Retrieved May 06, 2014.

Shao, G. (2010). Venturing Through Acquisitions or Alliances? Examing U.S. Media Companies Digital Strategy. Journal of Media Business Studies, 7(3), 21–39. Retrieved December 29, 2013.

Shearer, C. (2000). The CRISP-DM Model: The News Blueprint for Data Mining. Journal of Data Warehousing, 5(4), 13–23. Retrieved February 11, 2015.

20

Siegel, R., Siegel, E., & Macmillan, I. C. (1988). Corporate Venture Capitalists: Autonomy, Obstacles, and Performance. Journal of Business Venturing, 3(3), 233–247. Retrieved June 02, 2014.

Stein, L., & Klein, H. (2005). Corporate Venturing - Wie deutsche Großunternehmen Innovationsbarrieren überwinden. In H. Hungenberg (Ed.), Handbuch strategisches Management (2nd ed.). Wiesbaden: Gabler.

Sullivan, D., & Yuening, J. (2010). Media Convergence and the Impact of the Internet on the M&A Activity of Large Media Companies. Journal of Media Business Studies, 2010(7), 21–40. Retrieved November 28, 2013, from http://web.ebscohost.com/ehost/pdfviewer/pdfviewer?sid=8c127eb7-f857-4053-a772-db6fcaf6659d%40sessionmgr4003&vid=2&hid=4109.

Sykes, H. B. (1990). Corporate venture capital: Strategies for success. Journal of Business Venturing, 5(1), 37–47. Retrieved April 14, 2014.

Van de Vrande, Vareska, & Vanhaverbeke, W. (2013). How Prior Corporate Venture Capital Investments Shape Technological Alliances: A Real Options Approach. Entrepreneurship Theory and Practice, 37(5), 1019–1043. Retrieved April 16, 2014.

van Weezel, A. (2010). Creative Destruction: Why Not Researching Entrepreneurial Media? International Journal on Media Management, 12(1), 47–49. Retrieved February 28, 2014.

Vanhaverbeke, W., Duysters, G., & Noorderhaven, N. (2002). External Technology Sourcing Through Alliances or Acquisitions: An Analysis of the Application- Specific Integrated Circuits Industry. Organizational Science, 2002(16), 714–733. Retrieved January 13, 2014.

Zipser, D. (2008). Wertgenerierung von Buyouts (1. Aufl. 2008). Wiesbaden, Vallendar: Gabler Verlag / Springer Fachmedien Wiesbaden GmbH Wiesbaden.