the outlook for energy - louisiana state university · the outlook for energy ... increase fuel...

TRANSCRIPT

David E. DismukesCenter for Energy StudiesLouisiana State University

The Outlook for Energy

Presentation to the Sunshine Rotary ClubBaton Rouge, Louisiana

April 28, 2005

Crises of the past rooted in geopolitical strife and regulatory confusion.

Center for Energy Studies

$0

$10

$20

$30

$40

$50

$60

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

WTI

- $/

Bbl

$0

$1

$2

$3

$4

$5

$6

Nat

ural

Gas

Wel

lhea

d - $

/Mcf

West Texas Intermediate

US Natural Gas Wellhead Price

Arab OilEmbargo

Past and Current Crises

IranianRevolution

Source: Federal Reserve Bank of St. Louis

Past and Current Crises

While geopolitical issues are aggravating today’s energy markets, the fundamental source of the problem is clearly rooted in economic fundamentals.

• Most basic energy markets are global, and prices are driven by what goes on in global markets.

– Capital is mobile across the globe for energy production decisions.

– Production and output are global in destination markets.

– Prices are traded on recognized hubs, and through recognized institutions, throughout the globe.

– While natural gas has been primarily continental, the development of LNG is pushing these markets towards globalization as well.

Center for Energy Studies

World Oil Demand

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1991-1999

Average

2000 2001 2002 2003 2004 2005 2006

Mill

ion

Bar

rels

per

Day

Rest of World

China

US

Source: Energy Information Administration

Projections

World oil demand growth currently surging at relatively high ratesand continues to be strong through 2006

Center for Energy Studies

China’s demand

increases 173 percent from 2003

to 2004

World Oil Production1980-2002

Source: Energy Information Administration

0

10

20

30

40

50

60

70

80

90

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

Milli

on B

arre

ls p

er D

ay

Center for Energy Studies

Eastern Europe & Former USSR

United States

Middle East

Rest of World

Rank Order of World’s Largest Oil Producers2004

Source: Energy Information Administration

0 2 4 6 8 10 12

Brazil

Iraq

UK

Nigeria

Kuwait

UAE

Canada

Norway

China

Mexico

Iran

United States

Russia

Saudi Arabia

Million Barrels per Day

Center for Energy Studies

World Oil Spare Production Capacity

Source: Energy Information Administration

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1991-1999

Average

1998 1999 2000 2001 2002 2003 2004 2005 2006

Mill

ion

Bar

rels

per

Day

Projections

Spare capacity hit its lowest level in 30 years in 2004 and remains fairly low

Center for Energy Studies

World Oil Reserves by CountryAs of January 1, 2004

Source: Oil and Gas Journal

0 50 100 150 200 250 300

Rest of WorldOman

AzerbaijanBrazil

KazakhstanNorwayAlgeria

QatarMexico

ChinaUnited States

NigeriaUnited States (with ANWR)

LibyaRussia

VenezuelaKuwait

UAEIraqIran

CanadaSaudi Arabia

Billion Barrels

World Total:1,266 Billion Barrels

(1,276 with ANWR)

Center for Energy Studies

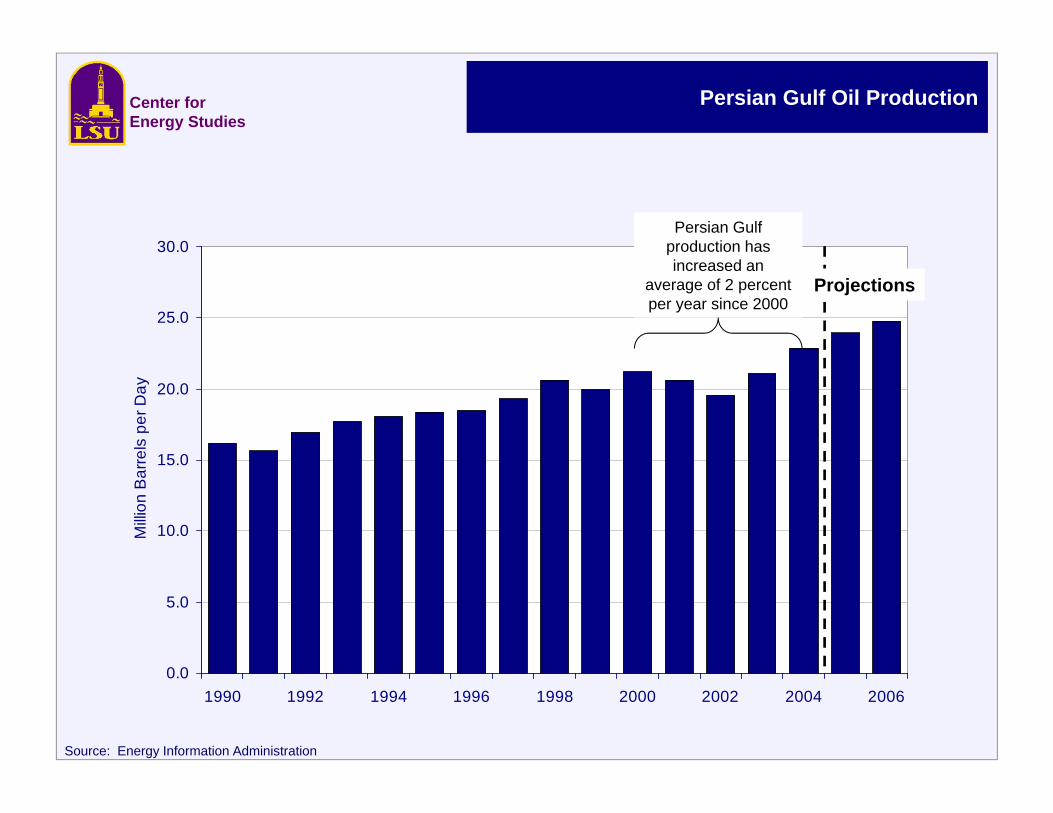

Persian Gulf Oil Production

Source: Energy Information Administration

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1990 1992 1994 1996 1998 2000 2002 2004 2006

Milli

on B

arre

ls p

er D

ay

Projections

Center for Energy Studies

Persian Gulf production has increased an

average of 2 percent per year since 2000

Are Things as Bad as They Seem?Real Gasoline Pump Price, Annual Average 1919-2006Center for

Energy Studies

$0

$50

$100

$150

$200

$250

$300

$35019

1919

2219

2519

2819

3119

3419

3719

4019

4319

4619

4919

5219

5519

5819

6119

6419

6719

7019

7319

7619

7919

8219

8519

8819

9119

9419

9720

0020

0320

06

Cen

ts p

er G

allo

n

Real Price(2005=1)

NominalPrice

Projections

Source: Energy Information Administration

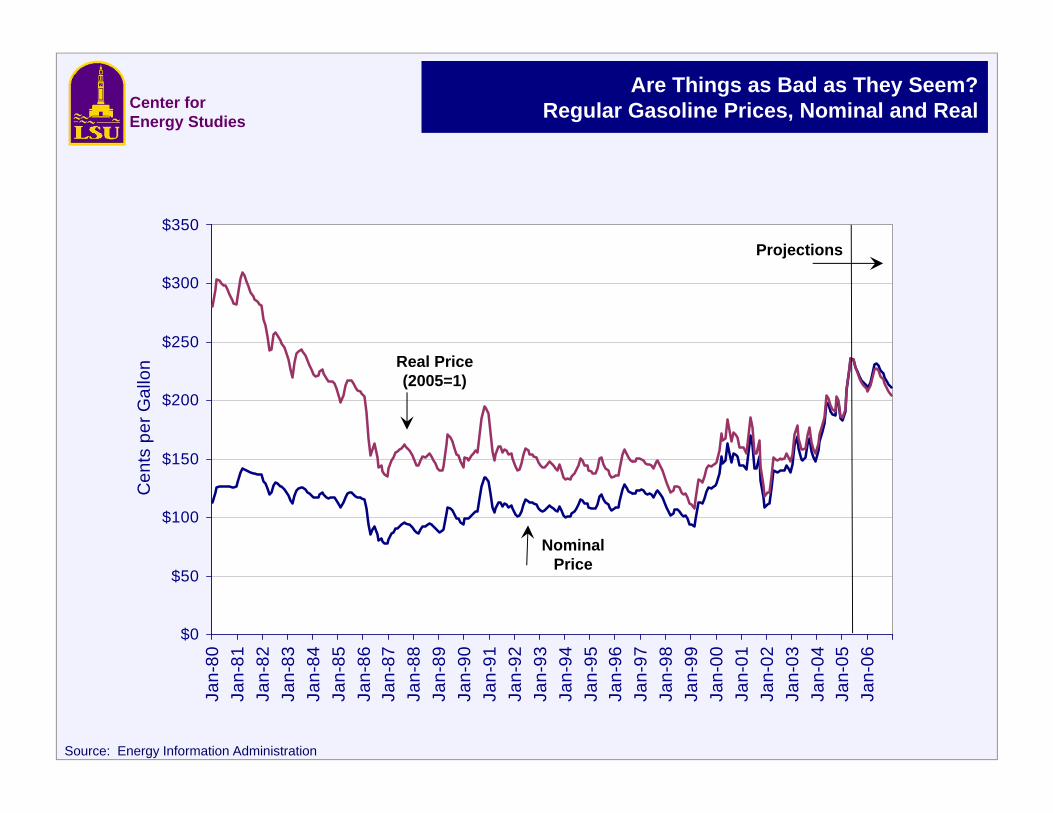

Are Things as Bad as They Seem?Regular Gasoline Prices, Nominal and RealCenter for

Energy Studies

$0

$50

$100

$150

$200

$250

$300

$350Ja

n-80

Jan-

81Ja

n-82

Jan-

83Ja

n-84

Jan-

85Ja

n-86

Jan-

87Ja

n-88

Jan-

89Ja

n-90

Jan-

91Ja

n-92

Jan-

93Ja

n-94

Jan-

95Ja

n-96

Jan-

97Ja

n-98

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Cen

ts p

er G

allo

n Real Price(2005=1)

NominalPrice

Projections

Source: Energy Information Administration

Are Things as Bad as They Seem?Imported Crude Oil Prices, Nominal and RealCenter for

Energy Studies

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100Ja

n-80

Jan-

81Ja

n-82

Jan-

83Ja

n-84

Jan-

85Ja

n-86

Jan-

87Ja

n-88

Jan-

89Ja

n-90

Jan-

91Ja

n-92

Jan-

93Ja

n-94

Jan-

95Ja

n-96

Jan-

97Ja

n-98

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Pric

e P

er B

arre

l Real Price(2005=1)

NominalPrice

Projections

Source: Energy Information Administration

US Household Energy Expenditure as aPercent of Real Disposable Personal IncomeCenter for

Energy Studies

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1978 1980 1981 1982 1984 1987 1990 1993 1997 2001

Selected Years

Per

cent

Source: Energy Information Administration; and Bureau of Economic Analysis, US Department of Commerce

US Energy Expendituresas a Percent of GDP (1970-2000)Center for

Energy Studies

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Per

cent

Source: Energy Information Administration; and Bureau of Economic Analysis, US Department of Commerce

What are the Solutions?

1. Increase domestic production capabilities – but recognizing that we will NEVER be energy independent.

2. Increase fuel diversity through market based approaches – coal, nuclear, renewables.

3. Increase energy efficiency through market based mechanisms

a. households

b. businesses

c. industry

Center for Energy Studies

Center for Energy Studies

Source: Natural Gas: Can We Produce Enough?” Independent Petroleum Association of America, website: http://www.ipaa.org/govtrelations/factsheets/NaturalGasProdEnough.asp.

Resource Estimates –Restricted Areas Estimated

Percentage Restricted

ANWR = 3.5 TCF

ANS = 35 TCF

US Natural Gas Production by Source1990-2025

0

5

10

15

20

25

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

Trilli

on C

ubic

Fee

t

Source: Energy Information Administration

Projected

Center for Energy Studies

Lower 48 onshore non-associated conventional

Lower 48 onshore non-associated unconventional

Lower 48 associated-dissolved

Lower 48 offshore non-associated

Alaska

Projected US gas production is driven by a number of uncertain sources

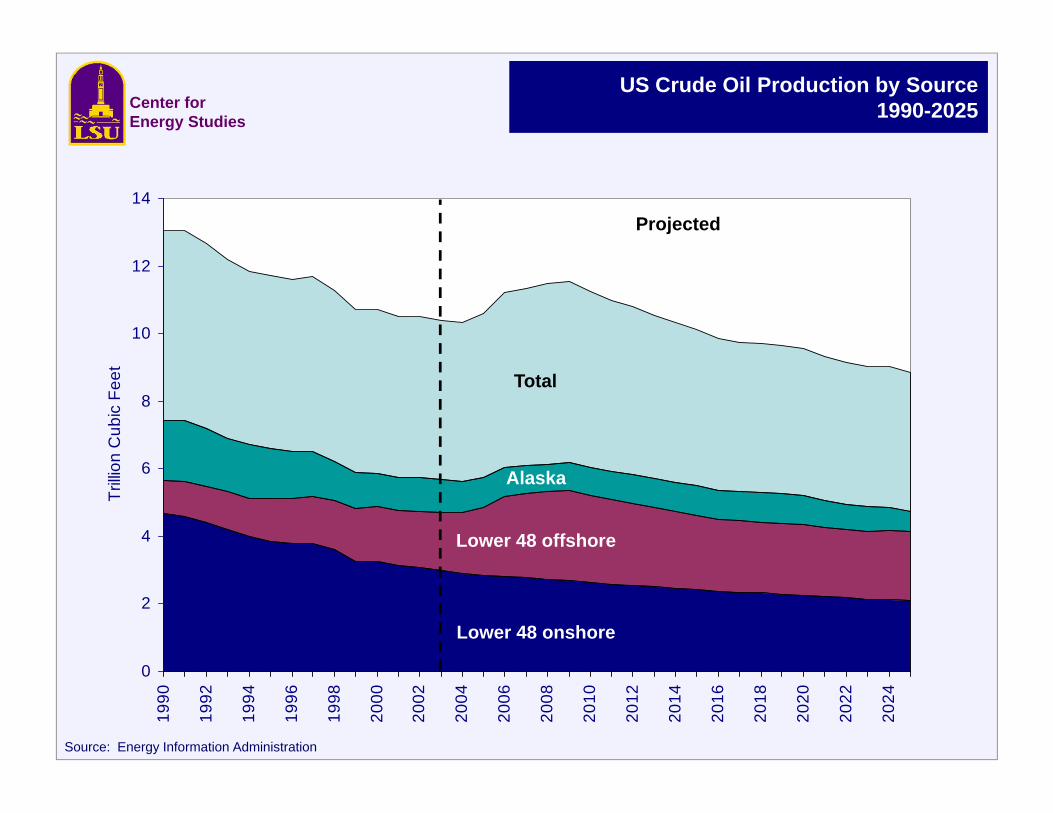

US Crude Oil Production by Source1990-2025

0

2

4

6

8

10

12

14

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

Trilli

on C

ubic

Fee

t

Projected

Center for Energy Studies

Lower 48 onshore

Lower 48 offshore

Alaska

Total

Source: Energy Information Administration

Existing and ProposedLNG Terminals

Source: Federal Energy Regulatory Commission

Center for Energy Studies

US Electric Generation Capacity by Fuel Type1993 and 2003

Coal43%

Natural Gas19%

Nuclear14%

Petroleum Liquids

10%

Other Renewables

2% Other3%

Hydro11%

Coal41%

Petroleum Liquids

5%

Natural Gas28%

Nuclear13%

Other Renewables

2% Other0%

Hydro11%

1993 2003

Source: Energy Information Administration

Center for Energy Studies

Generation shares have moved significantly to natural gas

Electricity Generation Capacity Additionsby Fuel Type, (2004-2025)Center for

Energy Studies

0

10

20

30

40

50

60

70

2004-2005 2006-2010 2011-2015 2016-2020 2021-2025

GW

Natural Gas

Coal

Renewables

Note: Includes combined heat and power.Source: Energy Information Administration

States with Renewable Portfolio Standardsand State Mandates, 2004

Source: Energy Information Administration

Note: In Colorado and Florida the RPS is not statewide. In a few states, such as Hawaii and Illinois, the RPS is voluntary.

Center for Energy Studies

Outlook for renewables improves with required standards

Short Term OutlookHenry Hub Natural Gas Spot Price

$4

$5

$6

$7

$8

$9

$10

0 1 2 3 4 5 6 7 8 9

EIA2005 $6.95

EIA2006 $6.90

CurrentYTD-2005Average

$6.95

EEA2006 $7.40

RW Beck2005$6.40

Goldman Sachs2005$6.75

Goldman Sachs2006$7.00

EEA2005 $6.84

Center for Energy Studies

Source: Energy Information Administration; and various trade press

Short Term OutlookWTI Crude Oil Price

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

0 1 2 3 4 5 6 7 8

EIA2005

$54.74

EIA2006

$54.83CurrentYTD-2005Average$49.77

BarclaysCapital

2005$47.80

Goldman Sachs2005

$50.00

Goldman Sachs2006

$55.00

Center for Energy Studies

Merrill Lynch & Co2005

$46.00

Source: Energy Information Administration; and various trade press

Short Term OutlookGasoline Prices

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

$2.10

$2.20

$2.30

$2.40

$2.50

0 0.5 1 1.5 2 2.5

EIASummer

2005 $2.28

CurrentYTD-2005Average

$1.94

Center for Energy Studies

Source: Energy Information Administration; and various trade press

World Marketed Energy Consumption by Region1970-2025

0

50

100

150

200

250

300

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2010 2025

Qua

drilli

on B

tu

IndustrializedEastern Europe/Former Soviet UnionDeveloping World

45%

43%

12%

2025 Share of

World Total

Center for Energy Studies

53%

(Developing World)

23%(Eastern Europe)

1987Share of

World Total

24%

Long run sees significant increase in usage for developing world

Source: Energy Information Administration

Persian Gulf Oil Productive Capacity by Country2001 and 2025

Source: Oil and Gas Journal

0.8

5

5.2

6.6

4.9

22.5

0.6

2.4

2.7

2.8

3.7

10.2

0 5 10 15 20 25

Qatar

Kuwait

UAE

Iraq

Iran

Saudi Arabia

Million Barrels per Day

2001

2025

Center for Energy Studies

Persian Gulf will have to step up to meet required production challenges

0

5

10

15

20

25

30

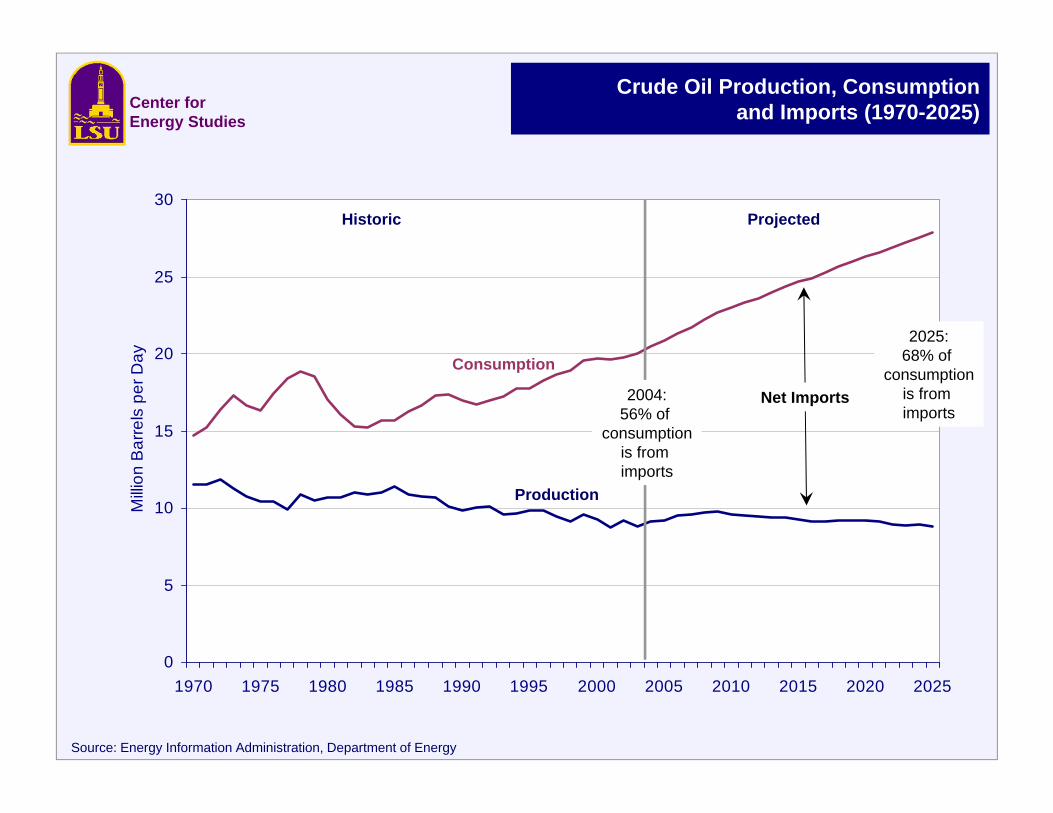

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Milli

on B

arre

ls p

er D

ay

Source: Energy Information Administration, Department of Energy

Crude Oil Production, Consumptionand Imports (1970-2025)

Consumption

Production

Historic Projected

Center for Energy Studies

Net Imports2004:56% of

consumptionis from imports

2025:68% of

consumptionis from imports

0

5

10

15

20

25

30

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Tcf

Source: Energy Information Administration, Department of Energy

Natural Gas Production, Consumptionand Imports (1970-2025)

Consumption

Production

Historic Projected

Net Imports

3.4

0.2

3.3

2.22.4

4.8

0

1

2

3

4

5

Tcf

Pipeline Imports LNG Imports

Natural Gas Net Imports, 2001, 2010, 2025

Center for Energy Studies

Center for Energy Studies

• Continued high prices in near term

• Developed world will rely on imports more heavily

• Continued demand will put increased pressure on global energy markets

• US dependence on foreign energy will increase

• Overall problem in real terms is not severe but we are nearing the pressure point

Conclusions