the mid-year update

TRANSCRIPT

THE MID-YEAR UPDATEAUGUST 17, 2000

22

THE MAIN POINTS

• SembCorp Industries’ interim PATMI grew 10% against 1H99 to $67.3m

• Interim turnover fell 25% to $1.4b due to lower sales reported by Marine and Construction, the dilution of our shareholding in SCS and the divestment of non-core businesses

• Construction, Logistics, Engineering and Food businesses showed earnings growth, while Marine, ISP and Building Materials performed below 1H99 levels

• We succeeded in our bid for SEMAC

33

THE FINANCIALSTHE FINANCIALS

44

$M

1H00 1H99 %

Turnover 1,397.0 1,854.0 (25)

PBT (before Assocs & JVs) 118.3 121.9 (3)

Contribution from Assocs/JVs 15.4 10.8 43

PBT (after Assocs & JVs) 133.7 132.7 1

PATMI 67.3 61.1 10

EI 100.9 228.9 (56)

Profit Attributable to Shareholders 168.1 290.0 (42)

PROFIT & LOSS PROFIT & LOSS SUMMARYSUMMARY

55

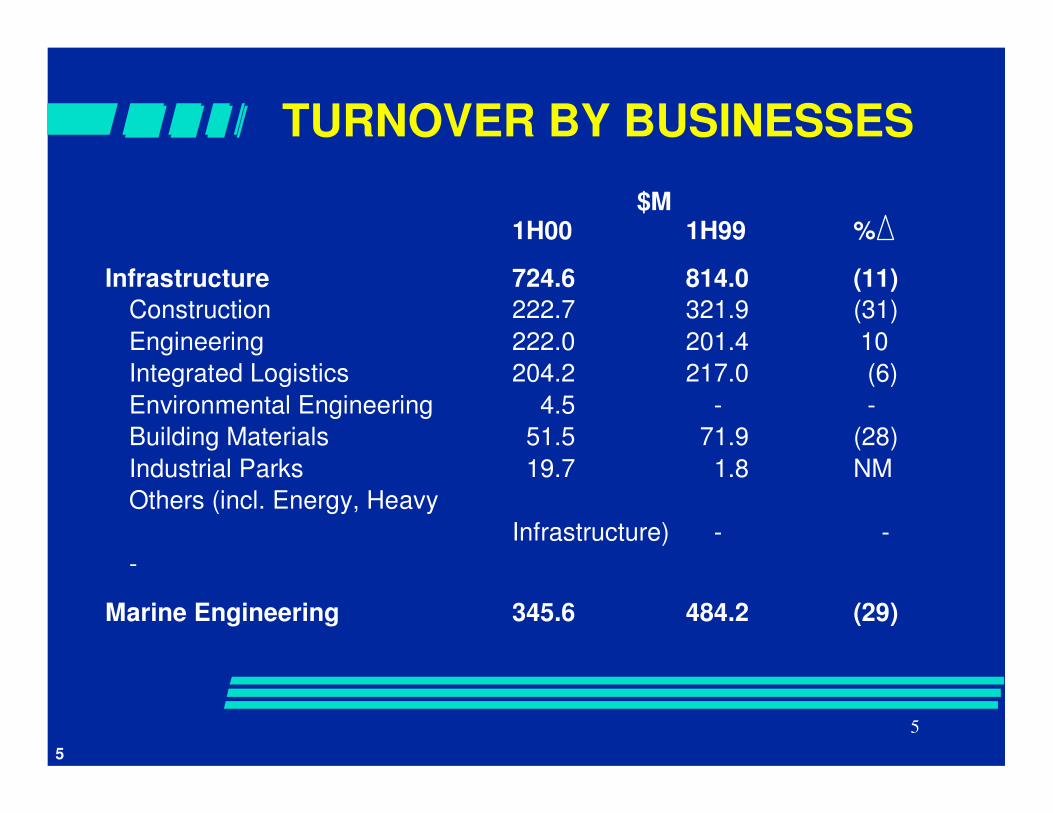

$M1H00 1H99 %

Infrastructure 724.6 814.0 (11)Construction 222.7 321.9 (31)Engineering 222.0 201.4 10Integrated Logistics 204.2 217.0 (6)Environmental Engineering 4.5 - -Building Materials 51.5 71.9 (28)Industrial Parks 19.7 1.8 NMOthers (incl. Energy, Heavy

Infrastructure) - --

Marine Engineering 345.6 484.2 (29)

TURNOVER BY BUSINESSES

66

$M1H00 1H99 %

Information Technology 93.4 240.0 (61)Internet Service Provider - 29.4 -IT Services 93.4 210.6 (56)

Lifestyle (non-core) 225.6 314.2 (28)Food Processing & Distribution 172.4 145.2 19 Food Retailing - 69.5 -Travel & Retail 2.0 43.0 (95)Minting 29.2 21.2 38Properties, Financial Services& Hotels / Resorts 22.0 35.3 (38)

Corporate & Others 7.8 1.5 NM

TOTAL 1,397.0 1,853.9 (25)

TURNOVER BY BUSINESSES

77

$M1H00 1H99 %

Infrastructure 37.8 34.9 8Construction 14.5 13.8 5Engineering 7.3 3.9 87Integrated Logistics 16.0 12.7 26Environmental Engineering 0 - -Building Materials (3.5) 0.7 NMIndustrial Parks 3.1 2.2 41Others (incl. Energy, Heavy

Infrastructure) 0.4 1.6(75)

Marine Engineering 20.7 24.2 (14)

PATMI CONTRIBUTIONBY BUSINESSES

88

$M1H00 1H99 %

Information Technology 1.8 5.2 (65)Internet Service Provider (0.2) 1.5 NMIT Services 2.0 3.7 (46)

Lifestyle (non-core) 12.2 19.6 (38)Food Processing & Distribution 8.7 9.8 (11)Food Retailing - 3.0 -Travel & Retail 0.4 1.3 (69)Minting 3.5 2.7 30Properties, Financial Services

& Hotels / Resorts (0.4)2.8 NM

Corporate & Others (5.2) (22.8) 77

TOTAL 67.3 61.1 10

PATMI CONTRIBUTIONBY BUSINESSES

99

1H00 $M

Gain/(Loss) on Disposals:SCS 179.2 JTIC 3.6Others 1.9Sub-total 184.7

Write-backs:Sun Cruise 3.9Bungalow at La Salle Street 1.1Sub-total 5.0

EXTRAORDINARY ITEMS

1010

1H00 $M

Provisions for Foreseeable Losses:Hotels & Resorts - Indonesia (20.5)

- Vietnam (8.6)- China (47.0)

China Theme Parks (6.0)Others (6.7)Sub-total (88.8)

TOTAL 100.9

EXTRAORDINARY ITEMS

1111

1H00 1H99 %Annualised ROE (%) 11.03 14.56 (24)

Annualised ROTA (%) 4.70 4.46 5

EPS - before EI (cents) 4.12 3.79 9

EPS - after EI (cents) 10.41 18.29 (43)

Interest Cover (times) 4.40 3.68 20

Net Gearing (times) 0.53 0.74 28

EVA ($m) (26) (45) 42

NTA per share ($) 72.7 59.8 22

CAPEX ($m) 87.0 87.7 (1)

WACC (%) 9.13 9.25 (1)

FINANCIAL INDICATORS

1212

CAPEX

1H00 $MTop 3 investment items - SembCorp Logistics India 7.0- SembCorp Air Products 5.5- SembCorp Gas 2.5

Top 3 fixed asset items- Capital Work-in-progress 29.1- Vessels 14.1- Plant and Machinery 6.6

1313

EXTERNAL BORROWINGS(excluding SembCap)

Currencies Amount ($M) Total S$M As a % ST LT Equivalent of total

S$ 453 846 1,299 82

US$ 114 45 276 17

Others (INR, THB,AUD, BND & £) 17 1

Total 1,592 100

(Average interest rates for S$ and US$ were 5.55% and 5.46% p.a.respectively).

1414

NET BORROWINGS(excluding SembCap)

$MAs at As at

Jun 30, 2000 Dec 31, 1999 %

Short-term 654.3 307.1 NM

Long-term 938.1 1,219.3 (23)

Gross 1,592.4 1,526.4 4

Less Cash (622.3) (644.5) (3)

Net 970.1 881.9 10

1515

BUSINESS REVIEW BUSINESS REVIEW & &

DEVELOPMENTSDEVELOPMENTS

1616

ENGINEERINGEngineering• Full-year PATMI growth is positive and on targetEPC• Interim PATMI was $5.3m ( 13%)• Current order book stands at $253m. Book-to-bill is 0.4BOO• Interim PATMI was $3.2m ( 33%)• SUT and PPU contributed $2.9m and $0.6m respectively, while

SembCorp Air Products showed a small loss of $0.2m• In the process of acquiring JTCI’s 20% stake in SUT. Targeting

completion by 4Q00 • SUT full-year PATMI contribution expected to grow over 40%

against FY99. PPU will continue to show a small contribution while SembCorp Air Products’ losses will narrow significantly over FY99

1717

CONSTRUCTION• Experiencing weak conditions this year but expected to do

better in 2001

• Current order book is about $773m. Book-to-bill is 1.26

• Full-year PATMI likely to be comparable to last year’s

BUILDING MATERIALS• Facing difficult conditions due to weakness in construction

industry

• Negotiation on a strategic alliance with a regional partner is now underway, possible conclusion in 2H00

1818

LOGISTICS

• On track for healthy FY00 growth

• Building Asia-wide logistics network

• Global alliance programme is progressing well

• Mechanism will either be a cross-holding or merger collaboration

• Our shareholding in SembCorp Logistics will be at least 51%

• Working towards announcing a deal by year-end

1919

ENVIRONMENTALENGINEERING

Semac• Won tender at a bid price of $120m - valued at about 1%

below their March 31 NTA of $121.5m• Rationale:

- gives us a much bigger share of the domestic and industrial / commercial waste collection market as Semac is Singapore’s largest and most established waste collection company

- puts us in a good position to bid for the remaining 7 municipal collection zones that will eventually be privatized by end-2000

- provides feedstock for the incineration plants

2020

ENVIRONMENTALENGINEERING

Semac• SembCorp SITA will assume ownership of Semac before

end-2000• Assets include 5 depots, 176 trucks, 447 compactors and

96 prime movers

• Plan to rationalize the company with SITA and attain an investment IRR (unfunded) of 11%

• Positive earnings will flow from Semac to our Group this year

2121

ENVIRONMENTALENGINEERING

Pacific Waste Management

• Work underway to set up common systems and processes at PWM

• PATMI contribution by PWM in 1H00 was $0.6m (1 month).

• Contribution over 7 months will be about $5m

2222

INDUSTRIAL PARKS• PATMI breakdown:

1H00 1H99 %BIP 5.4 5.3 2BIE (0.4) (0.5) 20VSIP (0.7) (0.5) (40)WSIP (1.3) (1.9) 32KIC - (0.3) -VSIP Power (0.4) - -SPM/Mgt Cos. 0.5 0.1 NMTOTAL 3.1 2.2 41

• Aiming to list our Industrial Park operation within 2 years on the SGX

2323

ENERGY

Kwinana Power Plant

• Acquired 30% stake in a co-generation power plant in Perth from Edison Mission Energy for approximately A$25m

• Plant capacity: 116MW of electricity and 2,800 tons/day of steam

• Has 25-year offtake contracts with Western Power and BP

• Investment IRR is 13% with payback period of 7 years

• Earnings to be consolidated from 4Q00

2424

MARINE ENGINEERING

• Faces difficult operating conditions and expects to show a profit level similar to FY99 with exceptional items

• Brazilian JV moving along well. Conclusion likely in September / October

• Actively seeking to acquire a shiprepair yard in China, targeted for completion in FY2001

2525

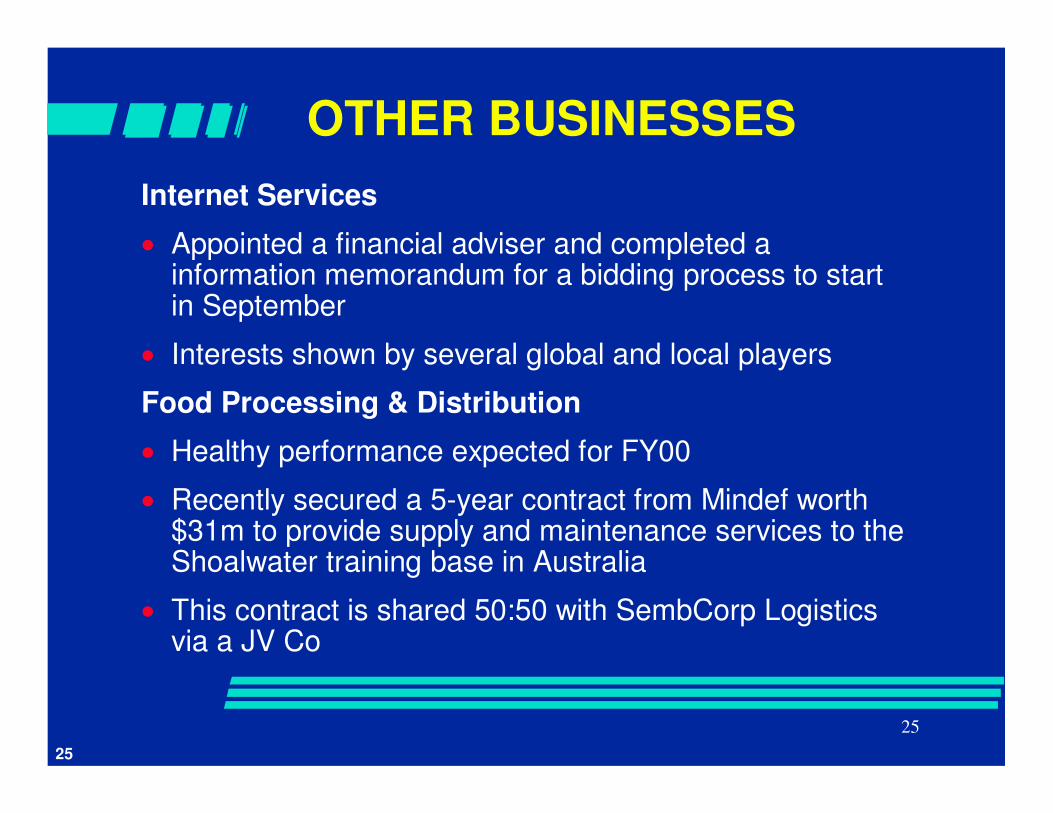

OTHER BUSINESSESInternet Services

• Appointed a financial adviser and completed a information memorandum for a bidding process to start in September

• Interests shown by several global and local players

Food Processing & Distribution

• Healthy performance expected for FY00

• Recently secured a 5-year contract from Mindef worth $31m to provide supply and maintenance services to the Shoalwater training base in Australia

• This contract is shared 50:50 with SembCorp Logistics via a JV Co

2626

ADMIRALTY LAND

• Made an application to the authorities last year for rezoning of the land to residential use

• Response from the authorities was not encouraging

• Now in the process of resubmitting our application and if granted, the development will still be 5 -10 years away

• Property development will remain a non-core business of SembCorp Industries

2727

MEDIUM TERM NOTES (MTN)PROGRAMME

• A $500m 10-year MTN programme is expected to be signed within September. Citicorp and OUB are the arrangers

- MTN is a more flexible programme allowing us to tap funds at a lower cost from time to time

- we expect a partial issuance within this year, depending on market conditions and our investment needs

2828

MOVING AHEADMOVING AHEAD

2929

MOVING AHEAD• Despite general economic recovery, our Construction,

Building Materials, Industrial Parks, Marine Engineering and ISP operations will continue to face difficult conditions through this year

• For FY00, we expect to at least maintain last year’s profit level

• We will push ahead with our global alliance plans for our E&C, Logistics and ISP operations

• There will be further rationalization of our core businesses

• We will grow PATMI contribution from our non-listed core operations

3030

MOVING AHEAD• Prospects for 2001 likely to improve considerably

• Construction and Marine Engineering industry will be riding on an up-cycle

• Earnings contribution from SUT, Gas and Cogen will be strong

• Environmental Engineering’s earnings contribution will come on stream progressively

• We can also expect upsides in earnings from E&C and Logistics units when they complete their strategic alliance or merger programmes