the global african investment summit · following the inaugural global african investment summit in...

TRANSCRIPT

THE GLOBAL AFRICAN INVESTMENT SUMMIT

www.theworlDfolio.com

OCTOBER 20 & 21, 2014

Featuring articles and interviews with government ministers and ceos From:

ANGOLA I GHANA I RwANdA I UGANdA I NIGERIA I TANzANIA I

GRIDCo is ready to help power Ghana forward into its

next phase of development. With thousands of additional

megawatts expected to be added to Ghana’s power generation

capacity over the next few years, GRIDCo will ensure it has

the necessary transmission facilities in place to evacuate this

power to the various load centres across the country.

TRANSMITTING GHANA INTO THE FUTURE

Ghana-TGAIS-Gridco.indd 1 9/18/14 10:46 AM

TABLE OF CONTENTS

06 Introduction to The Global African Investment Summit

08 Speaker List TGAIS

HEADS OF STATE AND COUNTRY OVERVIEWS

10 GHANA: President John Dramani Mahama

11 Ghana Country Overview

12 RWANDA: President Paul Kagame

13 Rwanda Country Overview

14 TANZANIA: Prime Minister Mizengo Pinda

15 Tanzania Country Overview

16 UGANDA: President Yoweri Museveni

17 Uganda Country Overview

PRODUCTIVE SECTORS

18 NATURAL RESOURCES

22 Interview: Alex Mould, CEO, Ghana National Petroleum Corporation

24 Interview: Hon.Irene Muloni, Minister of Energy

& Minerals, Uganda

26 AGRIBUSINESS

30 Interview: Tress Bucyanayandi, Minister of Agriculture, Uganda

32 Interview: Hon. Amelia Anne Kyambadde,

Minister of Trade & Industry, Uganda

34 POWER

36 Interview: Mr. William Amuna, CEO, GRIDCo, Ghana

38 INFRASTRUCTURE

42 Interview: Hon. Augusto da Silva Tomás, Minister of Transport, Angola

CONTINENT-WIDE ISSUES

46 FINANCE AFRICA

49 PROTECTING INVESTORS

53 THE U.S.’ “POWER AFRICA” INITIATIVE

56 AFRICA’S RISING MIDDLE CLASS

(The interviews in this special issue of The Worldfolio magazine are edited ver-sions of ones which previously appeared

in The Worldfolio’s online edition)

TABLE OF CONTENTS

TGAISWorldfolio

Special issue:

TABLE OF CONTENTS3

Contributing writers to this special issue of TheWorldfolio magazine:

Nathalie Bourgeois, a freelance journalist based in the UK, contributed the articles on electrical power in Af-rica (P. 34)and on Africa´s Rising Middle Class (p.56). A former reporter for the Associated Press and Elle magazine in Paris, she writes for a variety of publica-tions, in French and in English.

Benjamin Jones is a veteran journalist and a former correspondent for the New York Times in Madrid. In this special issue of Worldfolio, he writes about the new trends in agribusiness across Africa. (p.26)

Robert Latona, who contributed the story on President Barack Obama´s “Power Africa” initiative (p.54), is a freelance journalist in Madrid who writes about poli-tics, current affairs and the arts for a number of print and online publications.

Richard Middleton, author of the article on Legal Protection for Investors (p.49), is a London-based freelance journalist who has written across business topics, including the global drinks industry and the international TV market. He has also worked for The Independent newspaper and BBC Sport Online.

Rob Train, another freelance journalist resident in Madrid, wrote the articles on the Infrastructure sec-tor (p. 38) and on Finance in Africa (p.46). Rob is a former staff member of the English language edition of El País, Spain’s leading daily newspaper.

ABOUT THE AUTHORS

ÁLVARO LLARYORAChairman, The Worldfolio

ALEXI FERNÁNDEZExecutive Director, The Worldfolio

EDWARD HOLLANDEditor, Worldfolio magazine

KRISTIN KJELLGARDHead of Journalism Dept.

Graphic design: EDUARDO BERTONE, TAÍNA ALMODOVAR, ANTONIO ROMÁN & SHERGIO SERRANO

Illustration:TAÍNA ALMODOVAR

Printed By: Jomagar

Staff 4

Following the inaugural Global African Investment Summit in London 2014, The Government of Nigeria are partnering with dmg:events to bring the global investment market to Abuja in September 2015.

The Global African Investment Summit Nigeria will be run with the support, patronage and backing of The Federal Government of Nigeria, ECOWAS, The Nigerian Investment and Promotion Council, The Nigeria Economic Summit Group and Nigerian Export Promotion Council.

The summit will deliver a unique angle and opportunity. In a period with so many conferences The Global African Investment Summit has a very unique position. It distances itself from talk and focuses purely as a platform for transaction on bankable projects across Africa.

The Global African Investment Summit is the only African Summit that acts as a platform for transaction. Whilst the world has huge access to finance, the summit will focus on bankable projects for active investors looking to execute on transaction in Sub Saharan Africa. The summit will put you in front of fund managers and banks controlling in excess of USD235 Billion and present 75 projects seeking investment.

TGAIS-TheWF-TGAIS.indd 1 9/26/14 5:42 PM

A quick look at the headlines on Africa these days gives the im-pression of a continent mired in desperation. From the Ebola out-break in Guinea, Sierra Leone and other West African nations, to the criminal fanaticism of Boko Haram in Nigeria or the pro-longed drought in Somalia, the entire continent would seem to be permanently roiled by war, disease or famine.

But beyond the headlines lies a continent with some of the fastest-growing economies in the world, with untapped mineral wealth whose extent is only now beginning to be known and natural wonders that rival any on the planet. Half a century af-ter colonialism ended, Africa has yet to realise the promise of its enormous human and natural resources. Part of the reason has been the reluctance of investors to put their money behind proj-ects which could provide the basics that any country needs to cre-ate a sustainable economy – among them electricity, transport and communication infrastructure, and food production.

The Global African Investment Summit, a first-time ever event, is meant to bridge the gap between decision-makers in the investment world and leaders from around Africa who are promoting the projects their countries urgently need to assure economic and social development. Their objective is to convince money managers that putting funds into Africa is not a charitable enterprise but a profitable business venture.

The delegates from the finance side together represent more than $265 billion in funds under management, all of it looking for viable investment alternatives. The African delegates, for their

part, include presidents, government ministers and CEOs of state-owned companies. They will present more than 130 projects from four key sectors: natural resources, agribusiness, electric power and critical infrastructure. These range in size from a $13.5 billion international railway connecting Kenya, Uganda and Rwanda to a $200,000 tomato processing facility in Ghana. Among the others are a solar power plant in Kenya, a new airport in Rwanda and an oil refinery in Uganda.

The depth and variety of the projects gives an idea of just how enormous and varied are Africa´s needs. The goal of TGAIS is to connect the promoters with the financiers who can turn these plans into realities.

As a media partner of TGAIS, AFA Press is proud to offer this special edition of The Worldfolio magazine to provide context for the event and the sectors that will be in focus. We also offer a number of interviews with some of the key players in these sec-tors, including government ministers and CEOs.

We begin with profiles of the four African heads of state who will be attending TGAIS and overviews of their respective coun-tries: Ghana, Rwanda, Tanzania and Uganda. Leadership is key to the success of any project; hearing these heads of state will certainly go a long way to convincing investors of the viability of their proposals.

Next, we examine the four sectors that will be in focus at the meeting, beginning with natural resources, specifically oil and gas, and minerals.

THE GLOBAL AFRICA INVESTMENT SUMMIT: BRINGING FINANCE AND DEVELOPMENT TOGETHERBY Edward Holland, Editor, Worldfolio

Intro TGAIS 6

Our netwOrk Of cOrrespOndents each year is present in an average Of 80 lOcatiOns arOund the glObe in mOre than 50 cOuntries

every year Our cOrrespOndents cOnduct an average Of 3,000 One-On-One interviews with gOvernment Officials and seniOr business peOple

www.theworlDfolio.com oUr NewS, YoUr BUSiNeSS

Natural Resources. It may come as a surprise that oil and gas production in sub-Saharan Africa today accounts for more than 7% of world output, surpass-ing North Africa. While Nigeria, Angola and Equatorial Guinea have long been a presence in the world oil market, re-cent hydrocarbons discoveries in Ghana and Uganda show that these countries will soon be taking their place on the energy stage. Interviews with the CEO of the Ghana National Petroleum Cor-poration and with Uganda´s Minister of Energy and and Minerals Development, reveal how their respective countries intend to develop this bonanza and what they need to do so.

Agribusiness. The farm sector em-ploys more than 70 percent of Africa´s people and provides 25 percent of its Gross Domestic Product. The continent holds abundant water resources and more than half the world’s arable land. However, only a small portion of it has been put to use and some resource-rich

countries such as Angola import nearly all the food they consume. Our article takes a look at how innovation and pri-vate sector financing for agribusiness are beginning to change this. In separate interviews, Uganda´s Minister for Agri-culture and its Minister for Trade and In-dustry tell what advantages their country offers in the farm sector and for investors across the board.

Power. Africa’s needs in terms of elec-trical power are daunting. Think about this: the installed electricity generation capacity of the entire continent is equal to that of Belgium - and to what China installs every two years. Our article tells how, across Africa, this need is being ad-dressed with new projects that draw upon a range of energy sources, including solar, wind, geothermal and volcanic gases. In a separate interview, Wiliam Amuna, head of Ghana´s GRIDCo, tells about the large-scale investment that is needed to increase his country´s electrical capacity, in order to meet the 12% annual increase in demand.

Infrastructure of all kinds – roads, railways, seaport and airports – are needed for transport of people and commerce across the continent. Angola´s Transport Minister explains how his country intends to connect air, land and sea links to become a regional transportation hub.

In addition to presentations on these four sectors, the TGAIS confer-ence will include sessions on legal pro-tection for investors in Africa, on the continent´s capital markets and on its emerging middle class. We offer articles on all these topics, as well as one on U.S. President Barack Obama’s plan to “Power Africa,” by boosting its electrical energy capacity through a combination of pubic and private investment.

We hope you will find this special edition of TheWorldfolio magazine in-teresting and a useful accompanying document for the Global African In-vestment Summit. We also invite you to take a look at Worldfolio online, at WWW.THEWORLDFOLIO.COM

TGAIS Intro7

Our netwOrk Of cOrrespOndents each year is present in an average Of 80 lOcatiOns arOund the glObe in mOre than 50 cOuntries

every year Our cOrrespOndents cOnduct an average Of 3,000 One-On-One interviews with gOvernment Officials and seniOr business peOple

www.theworlDfolio.com oUr NewS, YoUr BUSiNeSS

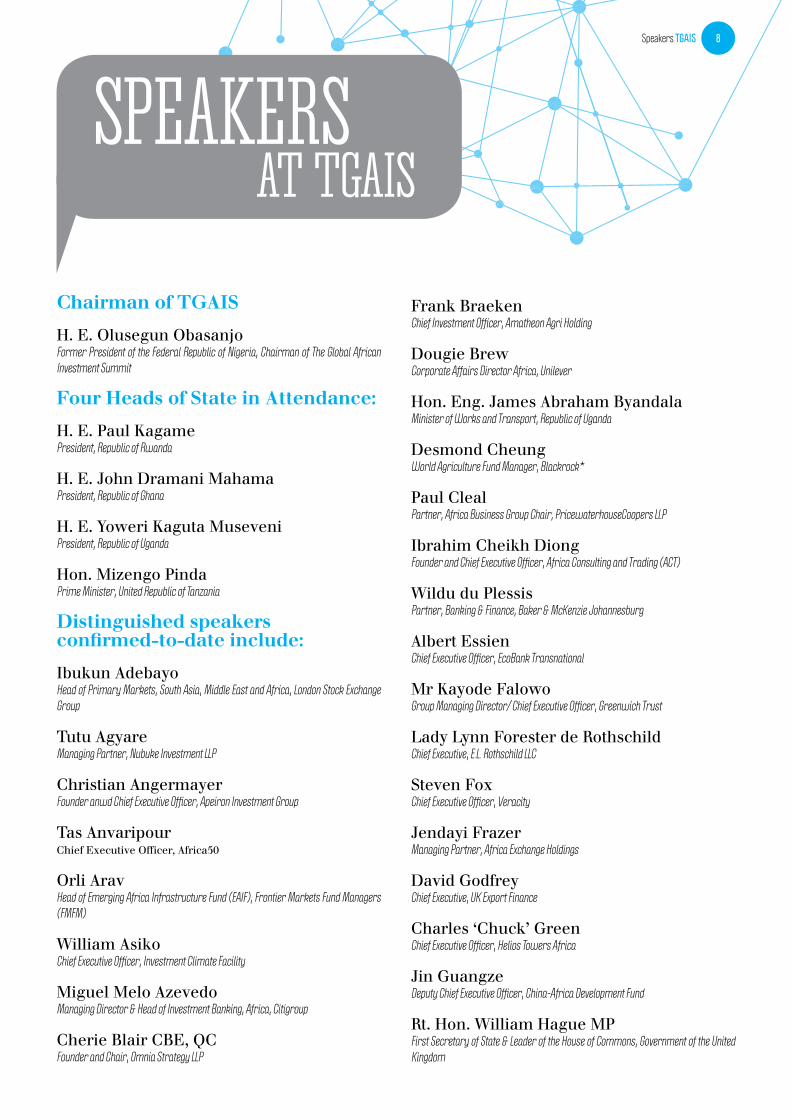

Chairman of TGAIS

H. E. Olusegun ObasanjoFormer President of the Federal Republic of Nigeria, Chairman of The Global African Investment Summit

Four Heads of State in Attendance:

H. E. Paul KagamePresident, Republic of Rwanda

H. E. John Dramani MahamaPresident, Republic of Ghana

H. E. Yoweri Kaguta MuseveniPresident, Republic of Uganda

Hon. Mizengo PindaPrime Minister, United Republic of Tanzania

Distinguished speakers confirmed-to-date include:

Ibukun AdebayoHead of Primary Markets, South Asia, Middle East and Africa, London Stock Exchange Group

Tutu AgyareManaging Partner, Nubuke Investment LLP

Christian AngermayerFounder anwd Chief Executive Officer, Apeiron Investment Group

Tas AnvaripourChief Executive Officer, Africa50

Orli AravHead of Emerging Africa Infrastructure Fund (EAIF), Frontier Markets Fund Managers (FMFM)

William AsikoChief Executive Officer, Investment Climate Facility

Miguel Melo AzevedoManaging Director & Head of Investment Banking, Africa, Citigroup

Cherie Blair CBE, QCFounder and Chair, Omnia Strategy LLP

Frank BraekenChief Investment Officer, Amatheon Agri Holding

Dougie BrewCorporate Affairs Director Africa, Unilever

Hon. Eng. James Abraham ByandalaMinister of Works and Transport, Republic of Uganda

Desmond CheungWorld Agriculture Fund Manager, Blackrock*

Paul Cleal Partner, Africa Business Group Chair, PricewaterhouseCoopers LLP

Ibrahim Cheikh DiongFounder and Chief Executive Officer, Africa Consulting and Trading (ACT)

Wildu du PlessisPartner, Banking & Finance, Baker & McKenzie Johannesburg

Albert EssienChief Executive Officer, EcoBank Transnational

Mr Kayode FalowoGroup Managing Director/ Chief Executive Officer, Greenwich Trust

Lady Lynn Forester de RothschildChief Executive, E.L. Rothschild LLC

Steven FoxChief Executive Officer, Veracity

Jendayi FrazerManaging Partner, Africa Exchange Holdings

David GodfreyChief Executive, UK Export Finance

Charles ‘Chuck’ GreenChief Executive Officer, Helios Towers Africa

Jin GuangzeDeputy Chief Executive Officer, China-Africa Development Fund

Rt. Hon. William Hague MPFirst Secretary of State & Leader of the House of Commons, Government of the United Kingdom

Speakers TGAIS 8

SpeakerSat tgaiS

Dr. A.B.C. OrjiakoChairman, Seplat

Sipho PhiriExecutive Chairman, Western Power Limited*

Monica PintoDirector, Anthemis

Romain PyExecutive Head of Transactions, AIIM

Jonathan RosenthalAfrica Editor, The Economist

Nic RudnickChief Executive Officer, Liquid Telecom

Kevin RyderHead: Investment Banking, Nedbank Capital

Akwasi SarpongCorrespondent, BBC World Services

Ifie SekiboManaging Director & CEO, Heritage Bank

Daniel ShakhaniRDS Capital, Chief Executive Officer

Kamran Rashid SiddiqiGroup Executive CEMEA, Visa Inc.

Matt SmithManaging Director, Rwanda Trading Company

Venkataramani SrivathsanManaging Director Africa & Middle East, Olam

Ravi SuriRegional Head, Corporate Finance MENAP & Regional Head, Project & Export Finance MENA, South Asia, Europe, & Africa, Standard Chartered, Africa

Lord David TriesmanDirector, Salamanca Group

John UlimwenguSenior Advisor to the Prime Minister in charge of Agriculture and Rural Development, Democratic Republic of Congo

Rt. Hon. Alderman Fiona WoolfThe Lord Mayor, City of London

Andrew HerscowitzCoordinator, US Power Africa

Robert HersovChairman and Founder, Invest Africa

Grace HightowerChief Executive Officer, Grace Hightower & Coffees of Rwanda

Jingdong HuaVice President and Treasurer, International Finance Corporation (IFC)

Phil JenkinsChief Financial Officer Africa, Diageo

Afsane JethaManaging Director of the Africa Private Equity, Duet Group

Rosalind Kainyah MBEManaging Director, Kina Advisory Limited

Mikael KarlssonChief Executive Officer, Globeleq

Jyrki KoskeloManaging Director, High Growth Emerging Markets, Atlas Mara

Charles LeveyVice President, PW Power (Mitsubishi Heavy Industries)

Scott MackinManaging Partner, Denham Capital Management LP

Monica MandelliHead of Strategic Relationships, Investment Banking Division, Goldman Sachs

Colin MelvinChief Executive Officer, Hermes Equity Ownership Services Ltd

Charles MorrisonPartner, International Head of Finance and Projects, DLA Piper

Dr. James Mwangi CBSChief Executive Officer and Managing Director, Equity Bank Group

Bimpe NkontchouDirector, Lagos Court of Arbitration

Douglas E. NordlingerPartner, Energy and Infrastructure Projects, Skadden

C. Charles OkeahalamManaging Director & Chief Executive Officer, AGH Capital Group

TGAIS Speakers9

10GHANA

PRESIDENT John Dramani mahama

“The Global African Investment Summit helps Ghana and other-leading African nations to deve-lop global investment into public-private partnerships. I commend and commit Ghana and my Offi-ce to the summit wholeheartedly. We welcome you all to what is the continent’s most significant economic summit.”

H.E. John Dramani Mahama, President of Ghana

Minister of Communications. During his tenure as MoC, Mahama also served as the Chairman of the National Communi-

cations Authority, in which capacity he played a key role in stabilising Ghana’s

telecommunications sector after it was deregulated in 1997.

Mahama would go on to serve a further two terms as a Member of Parliament for his constituency before becoming Vice President in 2009, as well as serving as the

Minority Spokesman for Com-munications in Parliament from 2001 to 2004 and the Minority

Spokesperson on Foreign Affairs from 2005 to 2008. He was also the Direc-tor of Communications of the National De-mocratic Caongress and played a key role in giving voice to the party’s positions on matters of governance and social signifi-cance when the party was in opposition.

On the passing of President John Atta Mills on 24th July 2012, John Mahama took over the reins of Government and led the country to bid a befitting farewell to a leader who was much loved and respected Ghanaian icon.

President Mahama is an avid reader, author and historian and has written for many newspapers and publications. In 2012 he published his first book, a me-moir entitled “My First Coup D’etat and other true stories from the lost decades of Africa”. Mr. Mahama has attributed the combination of his studies in history, communications and social psychology as having a profound effect on the shaping of his philosophy, his thoughts and his un-derstanding, contributing significantly to making him the person he is today. His love of communicating is also apparent in the fact that he is one of Africa’s most-followed leaders on the social networking sites, Twitter and Facebook.

Having ascended to the Presidential offi-ce in June 2012, following the untimely death of his predecessor John Atta Mills, John Dramani Mahama was officia-lly elected as President of Ghana in December 2012 after serving the remaining five months of the late President Mills’ term.

A communication expert, historian, and writer, President Mahama had previously served as the Vice President (since 2009) and before that as a Member of Parliament, as well as completing a spell as Minister of Communica-tions between 1998 and 2001.

Born in 1958 in Damongo, Ghana, Mahama went on to study at the University of Ghana, where he read His-tory, and received his Bachelor of Arts De-gree in 1981. He furthered his education by doing Post Graduate Studies in Commu-nication, also at the University of Ghana. Mahama’s great thirst for knowledge also compelled him to take advantage of the op-portunity to study a post graduate diploma in social psychology from the Institute of Social Sciences in Moscow.

Upon his return to Ghana he worked as the Information, Culture and Research Officer at the Embassy of Japan in Accra between 1991 and 1995, before moving on to become the International Relations, Sponsorship, Communication and Grants Manager at the Ghana Office of PLAN In-ternational, an international development charity that has committed itself to allevia-ting child poverty and improving the lives of children all over the world.

Mahama was first elected to the Par-liament of Ghana in the 1996 elections to represent the Bole/Bamboi constituen-cy for a four-year term, in which time he was also appointed as Deputy Minister of Communications and later the substantive

11 GHANA

Over the last two decades, Ghana has evolved into a model for politi-cal and economic reform in Africa, as well as a beacon of progress, de-mocracy and stability.

As the first place in sub-Saharan Africa where Europeans arrived to tra-de, Ghana later became the first nation in the region to achieve independence from a colonial power – in this case Britain – and following years of mostly-military rule, the 1992 constitution that allowed for a multi-party system ushe-red in a new era of democracy.

Today it is one of most stable coun-tries on the continent thanks to its good performance on democratic governan-

ce, arising from its strong multi-party political system, growing media plura-lism and strong civil society activism. The positive effects of improvements in governance, the effectiveness of pu-blic institutions, as well as persistent economic growth have also resulted in Ghana attaining the status of a lower middle income country, according to the World Bank.

One of the Africa’s fastest growing economies, Ghana is expected to maintain robust growth over the me-dium term, bolstered by improved oil and gas production, increased private-sector investment, improved public infrastructure development and sus-

tained political stability. The country continues to be the world’s second largest cocoa producer behind Ivory Coast, Africa’s biggest gold miner after South Africa, as well as the continent’s newest oil producer.

Aside from its notable economic growth, Ghana has also made impres-sive gains in the area of social deve-lopment, making substantial progress in meeting the World’s Bank’s Millen-nium Development Goals. Targets for the reduction of extreme poverty and access to safe drinking water have been achieved, while other objectives on hunger, education and gender are well on track.

2013

2012

PRINCIPALECONOMICINDICATORS

GNI per capita Atlas method (US$) 1760

FDI, net inflow 6.7% (% of GDP)

GDP (US$) 47.93

Population 25.90 Population

Population 11.6% Inflation

GDP growth 7.1%

61Life Expectancy

(years)

3.6Unemployment

(% of total labour force)

2010

Literacy rate (% of people 15 and above)

2006

Poverty headcount ratio at national poverty line

(% of population)

GhaNa overview

Source: World Bank, World Development Indicators

the country from the autocratic and divisive order that had been established since its in-

dependence. With Kagame at the helm of the RPF, in July 1994 the army

went on to bring down the geno-cidal government whose Hutu death squads had killed some 800,000 Tutsis and moderate Hutus. Today, the RPF are cre-dited with setting Rwanda on its current path towards recon-ciliation, nation building and socio-economic development.

Rwanda’s economy has grown rapidly under Kagame’s

presidency, with per-capita gross domestic product (purchasing power parity) estimated at US$1,592 in 2013,

compared with $567 in 2000. Annual growth between 2004 and 2010 averaged 8% per year. Kagame’s economic policy is based on liberalising the economy, pri-vatising state owned industries, reducing red tape for businesses, and transfor-ming the country from an agricultural to a knowledge-based society. This objective is central to the President’s Vision 2020; an ambitious programme of national develo-pment which also includes the goals of in-frastructure and transport improvements, private sector development, and health and education development.

Aside from his economic achieve-ments in Rwanda, President Kagame has also received recognition for his leadership in peace building and national reconcilia-tion, good governance and advancement of education and ICT. He is widely sought after to address regional and international audiences on a range of issues including African development, leadership, and the potential of ICT as a dynamic industry.

PRESIDENT Paul Kagame

“People who want to see Afri-ca develop come to Rwanda particularly because we have set up a very good environ-ment that makes things work for us and for our partners who come to invest with us.”

Paul Kagame, President of Rwanda

Paul Kagame, the sixth President of Rwanda, is currently serving his second seven-year term after being re-elected in August 2010. He initially took offi-ce in 2000 when his predecessor, Pasteur Bizimungu, resigned.

Kagame previously com-manded the rebel force that ended the 1994 Rwandan geno-cide and since then has widely been considered Rwanda’s de facto leader. He officially ser-ved as Vice President and Mi-nister of Defence until parlia-ment elected him as the country’s new head of state at the start of the new millennium.

As president, Kagame has prio-ritised national development, laun-ching a programme to develop Rwanda as a middle income country by 2020. When the country ranked as the world’s top reformer in the World Bank’s Doing Business Report in 2010, he was lauded by economists as an economic visionary.

Born in October, 1957 in Rwanda’s Southern Province, Kagame and his fa-mily fled pre-independence ethnic per-secution and violence in 1960, crossing into Uganda, where he would spend thir-ty years as a refugee. During the 1980s, Kagame fought in Yoweri Museveni’s group of guerrilla fighters who laun-ched a campaign to free Uganda from dictatorship. After Museveni’s military victories eventually carried him to the Ugandan presidency, Kagame become a senior Ugandan army officer under the new government.

After returning to Rwanda in 1990, Mr. Kagame helped lead the Rwandan Patriotic Front’s (RPF) four-year struggle to liberate

12RWANDA

13 RWANDA

A small, landlocked country in east-central Africa, Rwanda has managed to achieve im-pressive development progressive over the last 20 years, considering that it continues to recover from the ethnic strife and civil war that culminated in genocide during the mid-1990s.

Rwanda has traditionally been troubled by ethnic tension associated with the rela-tionship between the dominant Tutsi minority and the majority Hutus. When a Hutu upri-sing prompted around 200,000 Tutsis to flee to neighbouring countries in 1959, lingering resentment led to periodic massacres of Tutsis in the decades to follow, the most notorious of which began in April 1994. The death of the Hutu leader and President of Rwanda Juvenal Habyarimana in a plane crash caused by a rocket attack ignited a period fof intense and

systematic massacres. The killings - as many as 1 million people are estimated to have pe-rished - shocked the international community.

By July 1994, the Tutsi-led Rwandan Patriotic Front (RPF) which launched the mi-litary campaign to control the country, achie-ved its goal and prompted some two million Hutus to flee to Zaire, now the Democratic Republic of the Congo.

Having experienced a long and pain-ful process of recovery that is still underway, Rwanda has remarkably managed to achieve stability as well as consolidate gains in social development and economic growth. Rwanda’s long-term development goals are embedded in its Vision 2020 which seeks to transform the country from a low-income agriculture-based economy to a knowledge-based, service-

oriented economy by 2020. These goals build on Rwanda’s development success over the last two decades including high growth, ra-pid poverty reduction and reduced inequality. Reforms have recently been implemented successfully to improve the business environ-ment and reduce the cost of doing business in the country. As a result, Rwanda was named top performer in the World Bank´s Doing Bu-siness 2014 report, as well as being named as the second-easiest place to do business in sub-Saharan Africa.

During 2013, major steps were also taken to further enhance political rights and civil li-berties. Three new pieces of legislation were ratified to improve media regulation, promote transparency and encourage citizens’ econo-mic and political participation.

2013

2012

PRINCIPAL ECONOMICINDICATORS GNI per capita Atlas method (US$) 620

FDI, net inflow 1.5% (% of GDP)

GDP (US$) 7.452Population 11.78 Population

Population 4.6% GDP growth

Inflation 4.2%

63Life Expectancy

(years)

0.6Unemployment

(% of total labour force)

2010

Literacy rate (% of people 15 and above)

66

2011

Poverty headcount ratio at national poverty line

(% of population)

RWANDA overview

SouRce: World Bank, World Development Indicators

14TANZANIA

Prime minister Mizengo Pinda

After serving as Clerk to thCabinet from 1996 to 2000 , Pinda then decided to go into politics himself. In the 2000 general election, he was elected as a

Member of Parliament for Mpanda East constituency and in the same

year also became Deputy Minis-ter in the Prime Minister’s Offi-ce for Regional Administration and Local Governments.

Promoted to the rank of Minister in the Prime Minister’s Office, while also remaining in charge of regio-

nal administration and local governments in the Cabinet, Pinda would not have to wait long for his rise up the political ladder to continue. Following

the resignation of Prime Minister Edward Lowassa, President Jaka-ya Kikwete nominated Pinda as his replacement on February 8th 2008, and was confirmed nearly unanimously by the Tanzanian parliament on the same day.

As part of his government’s anti-corruption drive in 2010, Pin-da became the first senior govern-ment official to publicly declare his assets. “I have three small houses, have no shares in any company and do not even own a private car apart from the one loaned to me as a member of parliament,” he said in a press conference at the time.

With Pinda as Prime Minister, Tanzania has continued its push, as outlined by the government’s Vision 2025), to transform itself from a low-productivity, agricul-tural country to a semi-industria-lized one, with the aim of laying solid foundations for a more com-petitive and dynamic economy.

A member of the Tanzanian par-liament since 2000, Mizengo Pin-da has been Prime Minister of the country since 2008. Following his appointment, he declared in his first speech that he would conti-nue to be a peasant’s son, a sen-timent that resonated with the majority of Tanzanians. Un-der the Presidency of Jakaya Kikwete, the government has gained much international praise for its management of the economy, steering the country towards a free-market system without totally rejec-ting the socialist principles of Tanzania’s founder, President Julius Nyerere. Meanwhile, Pinda’s party – Tanzania CCM (the longest-reigning party in Africa) has recently set out an ambitious agenda for faster and sustained economic expansion. With an expected GDP growth rate of around 7% this year, Tan-zania has maintained its position as one of the world’s fastest- growing economies.

Born in 1948, Pinda progres-sed from humble beginnings to attend Tanzania’s prestigious Pugu Secondary School before taking a Bachelor Degree in Law (LLB) at the University of Dar es Salaam, graduating in 1974. Upon completion of his degree, he became State Attorney in the Ministry of Justice. Four years later, he moved to the State Hou-se, where he would be chosen as the Assistant Private Secretary to then-President Julius Nyerere and afterwards to his successor, Ali Hassan Mwinyi, until 1995.

“Tanzania has been implementing economic reforms to boost local and foreign private investment as one of the prerequisites for the attainment of Vision 2025. The target of the re-forms has been to improve the busi-ness and investment climate, resul-ting in increased investor appetite for the numerous investment opportuni-ties available in Tanzania. We have witnessed increased Foreign Direct Investment in various sectors inclu-ding mining, oil and gas, manufac-turing, construction and services” Prime Minister of the United Republic of Tanzania, Mizengo Pinda

15 TANZANIA

Although it remains one of the poorest coun-tries in the world, Tanzania has fortunately avoided the internal strife that has hindered many African states, while its political stabi-lity has managed to bring success in attrac-ting donors and investors as its economy to-day continues to achieve high growth rates.

Tanzania attained independence from colonial rule in 1961, forming a union bet-ween the mainland territory, Tanganyika, and the island of Zanzibar in 1964, although the latter still maintains a semi-autonomous government and legislature.

When founding president Julius Nyerere’s socialist policies failed to bring economic prosperity during his two decades in charge, his successors Ali Hassan Mwinyi

and Benjamin Mkapa helped to raise pro-ductivity and attract foreign investment and loans by dismantling government con-trol of the economy.

Tanzania’s fourth democratically elec-ted President, Jakaya Kikwete, has managed to maintain economic expansion and regio-nal peace. The annual GDP growth rate has averaged 6.7% since 2006, one of the best in sub-Saharan Africa, while the economy is projected to grow by around 7% in 2014 and 2015, driven by transport, communications, manufacturing and agriculture and suppor-ted by public investment in infrastructure.

Tourism is an important revenue ear-ner; Tanzania’s attractions include Africa’s highest mountain, Kilimanjaro, and wildli-

fe-rich national parks such as the Serengeti. Meanwhile, gold earnings have been rising, and the find of a major offshore gas field also is very promising.

Tanzania is currently in the advanced stages of preparing a new constitution, which is expected to be in place before the next general election in 2015. The dominant issues during the constitutional reforms have included: the structure of the union between mainland Tanzania and Zanzibar, the presidential powers, natural resources management and political reforms such as the independence of the electoral com-mission, greater representation for women and a provision for independent candidates to run for election.

2013

2012

GNI per capita Atlas method (US$) 630 FDI, net inflow 5.6% (% of GDP)

GDP (US$) 33.23Population 49.25 Population

Population 7.9% Inflation

GDP Growth 7.0%

61Life Expectancy

(years)

3.5Unemployment

(% of total labour force)

2010

28.2Literacy rate (% of people 15 and above)

68

2012

Poverty headcount ratio at national poverty line

(% of population)

PRINCIPALECONOMICINDICATORS

tAnZAniA overview

Source: World Bank, World Development Indicators

16UGANDA

PRESIDENT Yoweri Museveni

Mr. Museveni introduced democra-tic reforms and was also credited with substantially improving human rights,

notably by reducing abuses by the army and the police.

Having enjoyed the support of the international community in order to revitalize the collapsed economy of which he inherited, he first initiated economic po-licies designed to combat key problems such as hyperinflation and the balance of payments.

Thereafter, Museveni even-tually embraced the neo-liberal

structural adjustments advocated by the World Bank and the Inter-national Monetary Fund (IMF). Museveni has won praise from

Western governments for his adherence to IMF Structural adjustment programs, such as privatising state enterprises, cut-ting government spending and urging African self-reliance.

Museveni is a staunch supporter of Pan-Africanism. He was elected chairper-son of the Organisation of African Uni-ty (OAU) in 1991 and 1992, and has attribu-ted Uganda’s interventionist foreign policy in Sudan and the Democratic Republic of Congo to the values of Pan-Africanism. Uganda is currently helping to bring peace in Somalia, where the country is providing the vanguard of the peace-keepers.

Perhaps Museveni’s most widely noted accomplishment has been his government’s successful campaign against AIDS. During the 1980s, Uganda had one of the highest rates of HIV infec-tion in the world, but now Uganda’s rates are comparatively low, and the country stands as a rare success story in the global battle against the virus.

President Yoweri Museveni first came to power after a successful five-year gue-rrilla struggle during the 1980s. He has stood for, and won, four democratic elections since then, making notable economic and social improvements to Uganda along the way.

Born to a family of cattle farmers in western Uganda in 1944, Mr. Museveni attended missionary schools as a child before leaving for Tanzania to study political science and eco-nomics at the University of Dar es Salaam. There, he became chairman of a leftist student group allied with African liberation move-ments and also fought in the Front for the Liberation of Mozambique (Frelimo), where he learned the tech-niques of guerrilla warfare.

When the Ugandan dictator Idi Amin came to power in Uganda in 1971, Museveni founded the Front for National Salvation, which helped overthrow Amin in 1979. He then went on to hold posts in transitional governments and in 1980 ran for president of Uganda. However, when the elections – which were widely believed to have been rigged – were won by Milton Obote, Museveni formed the National Re-sistance Movement which eventually sei-zed control of the country in 1986. After declaring himself as President, his Na-tional Resistance Movement ran Uganda as a one-party state until a referendum brought back multi-party politics in 2005. His current term began in 2011.

President Museveni has been credi-ted with restoring stability and economic growth to Uganda following years of civil war and repression under Milton Obote and Idi Amin before him.

Given our abundant natural resources, given that we are establishing law and order, and given that we are freeing the asphyxiating bureaucra-tic grip over the economy, fo-reign investors will come here in their own interest because they can make money out of their coming to Uganda.”

Yoweri Museveni, President of Uganda

2013

2012

GNI per capita Atlas method (US$) 510 FDI, net inflow 5.3% (% of GDP)

GDP (US$) 21.48 Population 37.58 Population

Population 5.8% GDP growth

Inflation 5.5%

59Life Expectancy

(years)

4.2Unemployment

(% of total labour force)

73

2010

Literacy rate (% of people 15 and above)

24.5

2009

Poverty headcount ratio at national poverty line

(% of population)

PRINCIPALECONOMICINDICATORS

17 UGANDA

Since the late 1980s Uganda has reco-vered from the horror of civil war and economic disaster to become a relatively peaceful, stable and prosperous nation.

During the 1970s and 1980s Ugan-da was notorious for human rights abu-ses resulting from the military dicta-torship of Idi Amin between 1971 and 1979 and then again with the return to power of Milton Obote, who had been driven out by Amin eight years before. It is estimated that half a million people were killed in this dark period of state-sponsored violence.

After becoming president in 1986 after a coup d’état, Yoweri Museveni helped put the country on the path to peace, democracy and socio-economic

development. Following Western-bac-ked economic reforms that produced solid growth and falls in inflation, the country established a strong record of prudent macroeconomic management and structural reform between the 1990s and 2000s, becoming one of the first sub-Saharan African countries to proceed with liberalisation and pro-market policies. The discovery of oil and gas in the west of the country has also done much to boost confidence and development.

While the global economic turn-down of 2008 hit Uganda hard, in 2013 Uganda saw the consolidation of ma-croeconomic stability and a gradual recovery of economic activity, with

real GDP growth projected to reach 6.6% in 2014. Strong economic growth has also enabled substantial poverty reduction over the last two decades, meaning the country remains on track towards reaching this category of the World Bank’s Millennium Develop-ment Goals (MDGs).

Aside from Uganda’s recent dis-covery of oil, the country also benefits from its wealth in a variety of other na-tural resources, including fertile soils, regular rainfall, small deposits of cop-per, gold, and other minerals. Agricul-ture is the most important sector of the economy, employing over 80% of the work force, with coffee accounting for the bulk of export revenues.

UGANDA overview

SoUrce: World Bank, World Development Indicators

AFRICA’S WIDE-RANGINGNATURAL RESOURCES ARE READY TO

WORLD DEMANDAfrica´s mineral resources are vast and varied, from the deepwater oil wells off the coast of Nigeria to phos-phate deposits in Togo and the diamond mines in the interior of Angola. Developing all these resources will require financing and governments are turning in-creasingly to private sources or mixed public-private partnerships as the solution.

Sub-Saharan Africa contains nearly 63 billion barrels of proved crude oil reserves, and produces about 6 million barrels of oil per day (bpd), accounting for about 7% of global produc-tion, a greater share than North Africa. Traditionally led by Nige-ria and Equatorial Guinea, the region has seen the emergence of several new producers in re-cent years, with Angola already exporting large amounts of hy-drocarbons and significant re-sources being found in Mozam-bique, Tanzania, Kenya, Uganda and Ghana, and potential pros-pects being explored in several more countries.

In Uganda, delivering on the promise of an estimated 3.5 billion barrels of oil reserves in the Lake Albert basin will require at least $20 billion in invest-ments, an amount roughly equal to the country’s GDP, according to Tullow Uganda. With numerous sites moving from the explo-ration phase toward production, after oil was first discovered in 2006, several multibillion-projects are currently being offered for bidding, including an estimated total of $13 billion of invest-ments in the development of 17 oilfields and a $2.5 billion oil refinery project.

An initial call for investors in the refinery attracted a total of 75 firms, including China’s Petroleum Pipeline Bureau and Ja-pan’s Marubeni Corporation. Final bids from South Korea’s SK Energy Co. and Russia’s RT-Global Resources are now being con-sidered, with the winner expected to be announced by the end of the year. The awardee will finance and operate the project, in exchange for a 60% stake in the 60,000 bpd refinery and a 205-km pipeline connected to the plant, with the Ugandan government holding the remaining 40% of equity.

18Productive sectors NaTURaL RESOURCES

By J.J. Gallagher

MEET GROWING

Organizers expect construction to begin in 2015, with an initial 30,000 bpd of capacity becoming operational by 2018, rising to 60,000 bpd by 2020. When completed, the refinery will send petroleum products to increasingly resource hungry markets in Uganda, Congo, South Sudan, Rwanda, Burundi, Kenya, and Tanzania. Oil production in Uganda is expected to begin within the next two to three years. The country’s maximum output is forecast to reach 200,000 bpd, spurring further devel-opment in power and transport infra-structure, as well as manufacturing, transportation and logistics.

The oil discoveries in Uganda have also created the impetus for the devel-opment for a 784-kilometre pipeline that will connect the country to Ke-nya and Rwanda, and serve markets in Tanzania, Burundi, South Sudan and the Democratic Republic of Congo. The two-phase project will replace the costly lorry transport now required to ship fuel between those countries, a process blamed for supply interrup-tions and the relative costliness of fuel in Rwanda. A 350 km section of the con-

19 NaTURaL RESOURCES Productive sectors

IN ADDITIoN To ITs oIl AND gAs re-sources, AfrIcA holDs some of The worlD’s rIchesT DeposITs of mINer-Als AND precIous sToNes.

duit will first connect an existing pipe-line in Eldoret, Kenya, with the Ugan-dan capital of Kampala. The remaining 434 km will provide service to Kigali, Rwanda’s largest city. Planned proj-ects for mainline pumps, intermediate pump stations, loading facilities and pipeline services will add significant opportunities for oil service and trans-port companies, according to the Joint Coordinating Commission set up by the three countries to oversee the project.

The pipeline is the centerpiece of several significant projects agreed to by the East African Community (EAC)—comprised of Kenya, Tanza-nia, Uganda, Rwanda and Burundi—including a new road network, a new railway that will link four of the five countries to a port in Mombassa, as well as regulatory initiatives intended to integrate the area’s economies and facilitate trade.

While other countries in the region move closer to producing hydrocarbons, Rwanda looks to explore potential re-serves located beneath Lake Kivu on the country’s western border. The country

began oil exploration when the govern-ment entered into an agreement with Canadian firm, Vanoil Energy, which is currently carrying out seismic studies in the area.

Tanzania is also soliciting receiving bids from companies for new blocks off-shore and at Lake Tanganyika as part of its Fourth Licensing Round that closed in May of this year. The country received five bids for just half of the eight oil and gas blocks it offered in its latest bidding round, including from China’s CNOOC Ltd, Russia’s state-run Gazprom Nor-way’s Statoil and U.S.-based ExxonMobil. Tanzania possesses 46.5 billion trillion cubic feet of gas and has inked 25 pro-duction sharing agreements between 17 international energy companies so far.

Productive deepwater fields are continuing to come online in Angola, even as the country approaches 2 million bpd in crude production. A total of ten separate projects led by Eni, Total, Chev-ron, ExxonMobil and BP are scheduled to begin production by 2017, and expect eventual peak production together total-ing more than 1.1 million bpd. With most

exploration activity in Angola being con-ducted in deepwater offshore areas, the estimated costs of developing each wall range from $20 million to $50 million. In addition, exploration in pre-salt for-mations is expected to accelerate, as the country plans to auction an additional 10 onshore blocks believed to hold pre-salt prospects. At least 17 pre-salt blocks are currently being explored, according to the Energy Information Administration. In addition to the major international oil companies, Somoil—a privately-held Angolan company-represents the only non-public enterprise operating in the country, producing small amounts of oil from onshore fields.

In Nigeria, a shift by large interna-tional oil companies into deeper offshore blocks has helped open the door to in-dependent domestic oil companies, who now own the rights more than 100 oil-producing blocks across the country. The $500 million raised by Nigerian oil and gas company Seplat at its IPO earlier this year shows the industry’s potential, as firms including South Atlantic Petroleum and First Hydrocarbon Nigeria are set to

20Productive sectors NaTURaL RESOURCES

bid on potentially lucrative blocks being sold in the country by Chevron.

In addition to its oil and gas re-sources, Africa holds some of the world’s richest deposits of minerals and precious stones. Eleven African countries rank among the top ten sources worldwide for at least one major mineral. Africa possesses 88% of the world’s platinum, 84% of the global chromium supply 60% of the world’s diamonds and about half of its cobalt, in addition to a significant share of the world’s bauxite, gold, phos-phate, and uranium deposits. As the demand for mined commodities grows in the coming decades to meet the de-mands of increased urbanization and

infrastructure in India, China and other major emerging economies, in addition to existing demand in the developed economies, Africa will need to play a sig-nificant role in meeting that demand.

In the mining sector, the govern-ment of Togo has been working with the World Bank to privatize or enter into joint ventures with private companies to manage the country’s phosphate mines and build a fertilizer factory. Currently, the national mining company controls the country’s phosphate mines. In ad-dition, the government is expected to award a concession for a 250,000 ton per year manganese mine to UK-based Ferrex PLC by the end of the year. Man-

ganese is a key component in the pro-duction of steel and other non-ferrous alloys. Ferrex has also completed study on a proposed facility to produce about 60,000 tons per year of a ferromanganese alloy product in the country, according to Mining Weekly.

In Ghana, already Africa’s second-largest gold producer, the recently-formed venture Asanko Gold is currently developing two separate projects that were merged together when the com-pany bought PMI Gold earlier this year. Currently under construction, the new combined mine is estimated to produce 200,000 ounces of gold per year by the second quarter of 2016.

IN ugANDA, DelIver-

INg oN The promIse of

AN esTImATeD 3.5 bIl-

lIoN bArrels of oIl

reserves IN The lAke

AlberT bAsIN wIll re-

quIre AT leAsT $20 bIl-

lIoN IN INvesTmeNTs,

AN AmouNT roughly

equAl To The couN-

Try’s gDp.

21 NaTURaL RESOURCES Productive sectors

22Interview OIL & GAS

INTERVIEWwith

GNPC SEES ITS FUTURE AS AN INDEPENDENT OPERATOR

Alex Mould, CEO, Ghana National Petroleum Corporation

WF: Could you tell us about the impact of the Jubilee discovery in the everyday life of the Ghanaian people and the role of GNPC both in the discovery and the upstream aspects?I see the discovery of crude oil as in-cremental income for the government. It is a new source of revenue the go-vernment did not have before. But at the same time for the people of Ghana and for industry, it is going to change the lives of many people in the western region, not just the oil but also the gas. As a country we need to produce a lot of electricity. Akosombo dam produced 60% of our electricity, and the demand for electricity in five years is supposed to be almost doubled. This means that we need to be building power plants nearly every three months. That can only happen if two things are possible. First of all, you should have the raw material to produce electricity, and the raw material is gas, because it is the most economical and the most envi-ronmental-friendly as well. We know that we do have gas fields out there. We have associated gas from Jubilee, we have associated and non-associated gas coming in from the TEN project and also from the ENI Sankofa area pro-ject. We have a lot of gas, so we need

to tap that gas; we need to be able to bring it onshore for them to process it into electricity. This is going to create jobs, because we are going to have two plants processing the gas and pumping it through the pipeline to the power generation plants. It is also going to create more production of electricity; IPP’s (Independent Power Producers) are going to be formed where they will be able to now have bankable transac-tions, being able to bring in the raw material at a relatively modest cost to produce electricity at relatively modest cost for the people of Ghana.

WF: We know that GNPC is well posi-tioned to enter into strategic alliances with world-class oil companies, to ex-plore and develop this potential for their mutual benefit. What is the need for spe-cialized financial institutions in the oil and gas sector to ensure a long term commitment and a successful experien-ce for the investors?This is a finance business, we do use a lot of technology to find, transport and produce oil. The deals have to be bankable, so you have to work with fi-nancial institutions that are willing to take the risk and are trusting in the players. So for us, as much as it is im-

portant that we want investments in the country, we are looking for players that really know what they are doing. We want people who have expertise in deep and ultra-deep water exploration, like you have in the Gulf of Mexico. We are discussing with Shell, with Che-vron, and with all the big players. A few years ago nobody would have look at Ghana, but they realized that the ba-sin that we have is a world-class basin. What has changed over these years is the technology, so we have to be as-sociated with companies that are the forefront of technology. Most of these are the U.S. companies, but there are also companies from other countries who are investing on this. We are loo-king at encouraging and giving place to a diverse number of players. We have the Russians, the Americans, the English, and Nigerians. We are really screening if they have the competen-ce, and if they have the technical and financial backing.

The U.S. investors we are looking at have the right practices. The foreign corruption acts (U.S. Foreign Corrupt Practices Act) are very important. For us is not only having the money, but you need to have the technical capabi-lity to do the work.

Ghana´s potential as an oil producer has been evident since the discovery of the offshore Jubilee

field in 2007. Alex Mould, CEO, Ghana National Petroleum Corpo-ration, talks about GNPC’s plan to become a “full operator” with 15 years, developing its oil resources independently. He also discusses the important role of finance in the company´s planned expansion.

23 OIL & GAS Interview

WF: Which internal and external factors have changed and what are the reasons behind the five-year plans in changing GNPC’s strategy?Our strategy is quite simple. In GNPC, within five to seven years we want to be operators. That is a huge step forward. To be an operator means you need to have the muscle and the expertise to do these kinds of things. But we are pacing ourselves; we will start as a joint operator, because you have to walk before you run. We be-lieve that in about fifteen years we are going to be a full operator, operating most of our fields. We are also looking at the Volta basin, which is the next biggest thing to happen. That is the basin that is going to project Ghana forward. Here is where GNPC is taking a step forward to do most of the ex-ploration itself, especially the initial seismic work to sell the data to the companies that are coming to explore.

WF: It is evident that this is the time for an investor to invest in Ghana, before you start doing things on your own. Do you think your vast financial experience is a major backup for this strategy?This is a financial play, and it is impor-tant to have the right financial structu-res so as to move forward. We have set up a company in GNPC and that com-pany is going to be the commercial (arm) of GNPC, and is going to be able to raise money on its own in a future to do explorations and take a certain percen-tage of every field we give out. GNPC, on behalf of the government, has a normal 10% carry, but if you really believe your fields are that good you should be able to take some money and put it as a bet there as well, and that is what GNPC is going to do. So we have talked to a num-ber of financial institutions about what the strategy is for GNPC in this commer-cial endeavor and we are working with them to see how we can raise money. If

any of the players or partners is selling down we will be looking to see if we can join with other players and take over some of those equity portions that they are selling.Our strategy is quite simple. We have to replace our green reserves, catalyze the local content development, have a building capacity, and expand our acti-vities. You can’t continue being a 10% participant and expand your activities. So, together with the technology and the advisors we have, we will be looking at opportunities to buy real estate to do the major exploration activities.

Some investors may feel marginal. We are looking at various technologies over the world. To buy one FBSO (Floa-ting Production,Storage and Offloading) to do a field, you are talking about spen-ding around 45 billion dollars. So if you have a field that is not economical, you may have partners that give it up. So yes, I think you are looking at financial play, the ability to put a financial structures to-gether, to be able to raise money and take advantage of such opportunities.

“THE dEAls HAvE TO bE bANkAblE, sO yOu HAvE

TO wOrk wiTH fiNANCiAl iNsTiTuTiONs THAT ArE

williNG TO TAkE THE risk ANd ArE TrusTiNG

iN THE PlAyErs.”

“We believe that in about fifteen years We are going to be

a full operator, operating most of our fields.”

WF: How much petroleum has been discov-ered in Uganda and when do you expect to see the first production?We have confirmed over 3.5 billion bar-rels of oil in place, out of which we expect to recover between 1.2 billion to 1.7 billion barrels of oil. Three companies are cur-rently licensed to undertake petroleum exploration, development and production, and these are: China National Oil Off-shore Corporation (CNOOC), Total E&P, and Tullow Oil. We expect to see the first oil production between 2016 and 2017 for power generation. The huge hydro power projects will take up to five years to be com-pleted and therefore should electricity de-mand outstrip the current capacity before then, we can use some of the crude oil for power generation as an interim measure. We have agreed on the commercialization plan with the licensed companies, which includes crude oil for power generation in the interim.

WF: What is the next step in terms of com-mercialization?The next step is the development of a refin-ery in the country. We intend to construct a refinery with a capacity for 60,000 barrels a day. We will do this in phases, starting with 30,000 barrels per day. This will ensure that the refinery comes on stream quicker and will enable the country to build capacity in aspects of refining earlier, before expan-sion to 60,000 barrels per day. The first phase of the refinery is expected to be up and running by end of 2017.

WF: We understand that there is a third des-tination for the crude oil.The third destination is export of crude oil to the international market.

WF: What are your general expectations for these projects?A lot of work is being undertaken to de-velop the required infrastructure as the country prepares to go into commercial production. These activities are expected to generate many investment opportunities in terms of logistics, equipment, materials, EPC contracts, consultancies, among oth-ers for investors.

WF: What sort of preparations have you done on the legislative side of things?We have enacted two new laws for the up-stream and midstream sectors. We already have existing laws for the downstream sec-tor. We have a robust legal, regulatory, and institutional framework for the petroleum

sector which provides a predictable envi-ronment for investment.In line with the new laws, we are putting in place new institutions, namely a Petroleum Authority to regulate the sector, and a Na-tional Oil Company (NOC) to do business on the behalf of government. We expect the appointment of Board Members soon to take forward the establishment of these new institutions.

WF: How would you evaluate the success factor in drilling?Uganda has an unprecedented drilling suc-cess rate of over 85%, which is one of the highest in the world. In addition, the cost of finding oil in Uganda is among the low-est in the world, at less than $1 per barrel. This, coupled with the drilling success rate, attests to the attractiveness of investing in Uganda’s oil and gas sector.

WF: Things look bright for the Ugandan oil sector.As a country, we are really looking forward to developing this resource (petroleum) be-cause it will contribute to transforming this economy into a first world economy.

WF: What are your thoughts on the econom-ic inclusiveness that will bring the rational use of the oil resources?We want all Ugandans to benefit from this resource because it belongs to us all. As such, we want to plough the revenues from this resource into development of in-frastructure that supports other productive

IntervIewOIL DISCOVERIES PUT UGANDA ON THE PATH TO BECOMING A “FIRST-WORLD ECONOMY”

Hon. Irene Muloni, Minister of Energy and Minerals Develop-ment of Uganda, talks about her country´s vast mineral wealth, which goes far beyond oil, a resource she says could transform the Ugandan economy.

“The reTurn on invesT-

menT here is really,

high, abouT 18% ThaT is

no small feaT. you can-

noT find ThaT kind of

roi jusT anywhere.”

Hon. Irene Muloni, Minister of Energy and Minerals Development of Uganda

Interview NaTUral resoUrces 24

sectors of the economy, including roads, railway, electricity, airport, water and sanitation, education, health, services, and modernizing agriculture. This way, we will ensure that all Ugandans benefit from their natural resource. We want to transform the “black gold” into the “green gold” for our country.This would lay the foundation on which Ugandans can build their capacity to create wealth. For instance, through setting up small-scale industries in the rural areas that can add value to what we are producing, as an agricultural economy we create more jobs and increase per capita income. This will enable us to shift to a middle-income, and then to a high income country.

WF: What can you tell us about the Ugandan mining sector?As I have said, Uganda is very blessed. It has plenty of minerals. When you look at the minerals map of this country, the minerals that are here are amazing. We need to tap into this resource, add value to it, and generate wealth for this country. This should help support the transformation process.

In terms of mineral resources, we have already confirmed the occurrence of various minerals (both metallic and industrial). Under metallic minerals, we have beryl, bismuth, chromite, cobalt, cop-per, gold, iron ore, lead, lithium, manganese, columbite-tantalite or

coltan, tin, tungsten or wolfram, and so on. Our industrial minerals include asbestos, phosphates, clay, diatomite, feldspar, limestone, granite, marble, mica, rock salt, silica sand, talc, vermiculite, graph-ite, kaolin, kyanite, rare earth, uranium, and so on. It is also a known fact that Uganda is extremely rich when it comes to gold, as well.A lot of work is being done. We have conducted airborne magnetic surveys in 80% of this country. By being able to identify things better, we are in a better position for investors to come, conduct explora-tions and add value.

Further investigations have revealed a wealth of mineral poten-tial in this country.

WF: certain progress has been made with certain minerals.Yes, we have copper. This is in Kilembe. There is an investor who is already developing the place. It has an estimated capacity of 6 mil-lion tonnes, with a grade of 1.77%. We also have about 5.5 million tonnes of cobalt, with an estimated grade of 0.17%. Beryl and chro-mite are still under investigation.

If you look at iron ore, we have about 300 million tonnes of prov-en reserves. The potential for rare earth, on the other hand, has a potential of about 74 million tonnes, with a grade of 0.32%.

We have about three billion tonnes of aluminous clays with a grade of about 23% REE and 27% Alumina. Regarding phosphates, we have about 300 million tonnes, with a grade of 13.1%. We already have an investor on the ground.

We have 55 million tonnes of vermiculite—one of the biggest in the world. There is already an investor for this particular area, but we need value-addition.

We have about 3 million tonnes of kaolin, 2 million tonnes of gypsum, 22 million tonnes of salt, 2 million tonnes of really high quality glass sand (at 99.95%), as well as silicon oxide (with a grade of 99.9%).For limestone, we have about 27 million tonnes, with 15 million tonnes in Hima and 12 million tonnes in Dura. Under this, we have two cement factories—one in the west and another in the east.

Gold occurs in various parts of this country. Measured and indi-cated reserves have been established at Busia (SE Uganda), Mashon-ga, Kitaka, Kampono (SW Uganda) and Kisita and Kamalenge (Cen-tral Uganda). Indeed, a goodamount of work has gone into this area already. We need to add value before exporting it.

Another area of investment could be the dimension stones for the construction of tiles. We have about 300 million tonnes of it. There are just so many to highlight.

WF: How do you intend to export this to the world?The first step is to let the world know that we have these reserves. The next step is to attract those interested investors. They set up machin-ery to add value. It is going to be a win-win situation.You see, the return on investment (ROI) here is really high at about 18%. That is no small feat. You cannot find that kind of ROI just any-where. Depending on how you do the investment, you are bound to get this amount or more.

“WE arE rEally lookIng forWarD to DEvElopIng tHIs rEsoUrcE (oIl) bEcaUsE It WIll contrIbUtE to trans-forMIng tHIs EconoMy Into a fIrst-WorlD EconoMy.”

“UganDa Has an UnprEcEDEntED DrIllIng sUccEss ratE of ovEr 85%, WHIcH Is onE of tHE HIgHEst In tHE WorlD. In aDDItIon, tHE cost of fInDIng oIl In UganDa Is aMong tHE loWEst In tHE WorlD, at lEss tHan $1 pEr barrEl.”

NaTUral resoUrces Interview 25

INNOVATION ANDPRIVATE SECTOR FINANCINGARE TRANSFORMING AGRIbuSINESS IN

AFRICA

New global markets for everything from bananas and cocoa to cut flowers and or-ganic vegetables, green energy generated by locally-grown biomass and a new em-phasis on sustainable, yet profitable, farm-ing techniques are all helping to transform Africa’s agribusiness industry. This year marks two significant milestones for the continent and its ambitious efforts to transform the agricultural and agribusi-ness sectors: 2014 is the Year of Agricul-ture in Africa and the tenth anniversary of the Comprehensive Africa Agriculture De-velopment Programme aimed at ensuring food security for Africa’s one billion people. “Agriculture forms a significant portion of

the economies of all African countries,” notes Dr. Nkosazana Dlamini Zuma, the Chairperson of the African Union Com-mission. “It can therefore contribute towards major continental priorities such as eradicating poverty and hunger, boosting intra-African trade and investments, rapid industrializa-tion and economic diversification, sustain-able resource and environmental manage-ment, and creating jobs, human security and shared prosperity,” she says. Africa certainly has the potential to be-come a world agricultural power. The con-tinent has more than half of the world’s ag-riculturally suitable, yet unused, land and

its vast water resources have hardly been tapped. Agribusiness , whether multinational or Af-rican, is becoming an important player in realising this potential. Indeed, the World Bank reports that “private sector interest in African agribusiness is unprecedented.”But the challenge is for all stakehold-ers to channel investment intelligently to guarantee jobs, increase opportunities for Africa’s millions of farming smallholders, ensure the rights of local communities and protect the continent’s sometimes fragile environment.More specifically, African farmers, large and small, need to boost production, espe-

Organic farming and ethanOl frOm sugar cane are just sOme Of the innOvatiOns that are helping tO transfOrm the agricultural sectOr acrOss africa. hOwever, ensuring fOOd security fOr the cOntinent´s One billiOn peOple remains the first priOrity.

By Benjamin Jones

Productive Sectors AgriBusiness 26

africa, with half the wOrld´s agriculturally usable land and vast water resOurces, has the pOtential tO becOme a wOrld agricultural pOwer.

AgriBusiness Productive Sectors 27

cially crops destined for export and become more competitive on the world market; irrigation, transport, storage and processing infrastructure must improve to cut costs and raise revenue; and there must be a reversal of past policies such as state interven-tion in agricultural markets and the lack of public investment in the sector. Other goals include more financing tools for farmers, a strength-ening of land administration systems, better access to modern agricultural inputs and technology, and stronger safety mecha-nisms for investors considering a stake in Africa. “African farmers and businesses must be empowered through good policies, increased public and private investments and strong public-private partnerships,” says Gaiv Tata, World Bank Director for Financial and Private Sector Development in Africa. “A strong agribusiness sector is vital for Africa’s economic future.”International organizations are keen to help through financing and other measures. The World Bank Group has boosted its annual agricultural in-vestment from $4 billion to $6 billion over the past five years, while the International Finance Corporation (IFC) has pledged to increase its investments in African agribusiness over the next five years to $2 billion. “The IFC is stepping up efforts to support Africa’s agribusiness sector,” the organisation says. “We are developing new products such as local currency financing, risk sharing facilities and com-prehensive support to farmers through intermediaries.”At the same time, the IFC is working to further integrate its advisory services with investments to provide more compre-hensive support. “An efficient and competitive private agribusiness sector in Afri-ca will have a strong impact on reducing poverty and improving lives since most of sub-Saharan Africa’s poor live in rural areas that depend on agriculture,” the organisation says. The World Bank has identified five core areas to ensure higher and sustained growth: facilitating agricultural markets and trade; improving agricultural productivity; investing in public infra-structure for agricultural growth; reducing rural vulnerability and insecurity; and improving agricultural policy and institutions.Multinationals and non-governmental organisations can and are playing a role in most of these areas and many have already taken the plunge into the African agribusiness sector with large invest-ments that will help not only the corporate bottom line, but also the continent’s people, its future and its economic sustainability.

In Ghana, rice producer and distributor GADCO, with help from Western investment funds, banks and charitable organ-isations, focuses on high-quality local output, the creation of a modern value chain and assisting small farmers. With 1,000 hectares of rice under cultivation and a milling facility in the Volta Region, GADCO is on its way to becoming the country’s largest rice producer. Eventually, it plans to supply both domestic and regional con-sumers as it sees Africa has a definite growth market driven by urbanisation, population growth and rising incomes. “Ghana relies on imports for 70 percent of its rice consumption and demand continues to grow,” the company says. “Most local-ly-produced rice is grown by smallholder farmers, and with lim-ited access to modern seed and agricultural inputs, productivity tends to be low.”Through its outgrower project, GADCO provides these local smallholders with inputs, extension programmes, training and the use of its modern mill. The company then buys their rice for marketing so they benefit from high-quality processing and value chain integration, which means higher earnings. Another company betting on Africa is Addax Bioenergy, a sub-sidiary of the Malta-based energy and investment group AOG,

“A strong Agribusiness sector is vitAl for AfricA’s economic future.” - gaiv tata, World bank Di-rector for financial and Private sector Development in Africa.

Productive Sectors AgriBusiness 28

which has developed a sugarcane bio-ethanol and renewable electric power facility in Sierra Leone. GADCO is developing a greenfield 10,000-hectare sugarcane plantation, the construction of a bioethanol refinery and a biomass-fuelled co-generation plant which began operating this year. By 2017, the project is scheduled to turn out 85,000 m3 of bioethanol a year and produce sufficient “green power” that will eventually account for 20 percent of Sier-ra Leone’s total electricity requirements.“This is a great achievement for the people of Sierra Leone,” President Dr. Ernest Bai Koroma said. “The Addax Bioenergy initiative is the largest private sector investment in Sierra Leone’s ag-ricultural sector to date and provides a great example of successful investment in our country.”“Green” innovations in African agribusi-ness is also the trend in Uganda, where conventional agricultural methods are

giving way to organic production with enthusiastic support from the president, central government agencies, agricul-tural associations, NGO’s, exporters and universities. Uganda, known as “The Pearl of Africa,” is blessed with a varied climate and the right terrain to grow just about anything, either for export to lucrative foreign markets where the demand for organic produce is growing by leaps and bounds or for local and regional consumption. In the decade since the country adopted the Uganda Organic Standard in 2004 it has become the model for Africa and the world in this agricultural subsector. With more than 400,000 internationally certified organic farmers, the country is the first in Africa in this category and the second in the world after India. And what do these environmentally-friendly farmers produce? Coffee, fresh and dried fruit, avocados, vanilla, cot-ton, chillies, honey and a host of other

products with a total value of around $600 million per year.Praising the country’s organic farming sector, the United Nations Environment Programme said: “Uganda has taken an apparent liability – limited access to chem-ical inputs – and turned this into a com-parative advantage by growing its organic agricultural base, generating revenue and income for smallholder farmers.”As Africa advances in so many areas to meet the needs of its burgeoning popula-tion, join in on globalization and take its rightful place in the world, agribusiness will play a vital role as an investment magnet, a job generator and, most impor-tantly of course, a provider of food.

uganda has becOme a mOdel fOr africa and the wOrld in Organic farming.

AgriBusiness Productive Sectors 29

30 Interview Agribusiness

WF: uganda´s agriculture industry faces some challenges, such as adding value to raw materials or finding new markets. What are the key priorities that your min-istry is has set in order to exploit the po-tential of the agricultural sector?First of all, in a broader sense, my min-istry is in charge of two responsibilities. First, to ensure we produce sufficient food to feed our 35 million people. Af-ter meeting our own food requirements as a country, we can send some to our neighboring countries in East Africa. Second, to ensure our export commodi-ties are up, because this is where we get foreign exchange. Food crops are varied, but cash crops are fewer, mainly coffee, cotton, tea, and cocoa. That is on the side of cash crops. Then, if we go into some sectors, we have to differentiate the crop sector, the animal sector, and the fisher-ies sector.

Most of our food and export comes from the crop sector. In the livestock sec-tor, we have a lot of cattle –at the moment 14 million head. We are producing about 2 billion liters of milk annually, which we want to export. We will consume our production, and export surplus. In the past, we imported powdered milk from Europe. That is history now. We are now self-sufficient, and want to export some. We have got industries processing milk for export. Apart from milk, we want to export beef, and we are trying to ensure we get some investors to put up plants for adequate processing of meat in order to export. We have that potential.

If I shift to fisheries, the total capture of fish has increased as a country both from natural lakes, and from aquacul-ture. We think that aquaculture is very

important. Fishes in lakes are very dif-ficult to control, and we might not have sufficient control. In aquaculture, we have got a controlled environment. That is an addition to the lake’s resources. That is the direction.

WF: In what areas do you hope to attract in-vestment in agriculture? In raising crops, in food processing?In terms of investment, there are three levels where we want investors to come. First, investors could come, grow com-modities and add value to that commod-ity up to processing, and export. That is one category of entry.

The second category is to come, install machinery, and add value. You don’t have to be in farming, but only do processing. We produce a lot of coffee. Much of this is exported in beans, and

processed in Europe. We would like to see an investor coming, setting up ma-chinery, and doing roasters, and packag-ing here. That kind of entry, to handle products here, would be good.

We have a lot of vegetables and food. The Ugandan pineapple is the sweetest in the world. We have bananas, tea, and coffee. Someone could set up a factory and start in that entry point. Others could come and provide services to the agri-cultural sectors. Our soils are rich and fertile, but to a point. Some of them are now poor and degraded because of high exploitation. Providing the service of soil fertilizing is another possible service. We need fertilizers. We are trying to attract others to exploit carbonates. We hope to be manufacturing nitrogen fertilizers. These are companies providing services for agriculture. We also need vaccines.

Hon. Tress Bucyanayandi, Minister of Agriculture, Animal Industry and Fisheries of the Repub-lic of Uganda, talks about the agricultural sector in his country, the different entry points for investors and the huge potential of the sector for expansion. Among its products, he says, is “the sweetest pineapple in the world.”

INTERVIEWwith HON. TRESS BUCYANAYANDI, MINISTER OF AgRICUlTURE,