the future of the diamond industry - bruce cleaver, de beers group

TRANSCRIPT

T H E F U T U R E O F T H E D I A M O N D I N D U S T R Y

Bruce Cleaver, Executive Head of Strategy

D I A M O N D S I N C O N T E X T

The De Beers Group of Companies

Source: The De Beers Group of Companies; World Gold Council 2014; Johnson Matthey

D I A M O N D S O U R C E S F O R D I A M O N D S V S . G O L D A N D P L AT I N U M – 2 0 1 3(Per cent)

99

44

8

48

33

21

9

37

Jewellery

Industrial

Investment

Autocatalyst

Diamonds Gold Platinum

2

“In CONTRAST with precious metals

and other natural resources industries,

which rely on MULTIPLE sources of demand,

the diamond industry derives practically

all its VALUE from CONSUMERS’ demand for diamond jewellery”

(Per cent of brides receiving a diamond)

1939 1940 1945 1950 1955 1960 1965 1970 1975 1980 1990 2000 2010 2011 2013

10

20

30

40

50

60

70

80

USA

Japan

China (Tier 1)

D E B E E R S : B U I L D I N G T H E D I A M O N D E N G A G E M E N T T R A D I T I O N

The De Beers Group of Companies 3

C O M PA N Y O V E R V I E W

The De Beers Group of Companies

GlobalExploration1

Canada(100%)

South Africa(74%)

DebswanaDiamond Company

(50%)

NamdebHoldings

(50%)

NamdebDiamond

Corporation(land)

DebmarineNamibia

(sea)

Element SixTechnologies2

(100%);Abrasives (c.60%)

GlobalSightholder

Sales(100%)

Sightholder SalesSouth Africa

(74%)

DTC Botswana(50%)

Namibia DTC(50%)

Auction Sales(100%)

Forevermark(100%)

De BeersJewellers(50%)

M I N I N G S U P E R M AT E R I A L S

P R O D U C T I O NO P E R AT I O N SE X P L O R AT I O N R O U G H D I A M O N D S A L E S B R A N D S / R E TA I L

A N G L O A M E R I C A N 8 5 %

D E B E E R S

G O V E R N M E N T O F T H E R E P U B L I C O F B O T S WA N A 1 5 %

1. Exploration is undertaken through a number of controlled subsidiaries of De Beers

2. Element Six is made up of two businesses: Technologies, which is 100%

by De Beers, and Abrasives, which is c.60% owned by De Beers

Wholly-owned or controlledsubsidiaries and divisions

Joint ventures

4

D E B E E R S ’ S T R AT E G Y A C R O S S T H E P I P E L I N E

The De Beers Group of Companies

U P S T R E A MOptimise core business

E X P L O R AT I O N A N D P R O J E C T S : • In-house exploration

• Accelerated exploration project decision making

M I N I N G : • Flexible operations

to maximise value

through the demand cycle

• Asset optimisation across

operations

D I S T R I B U T I O N : • Build the smartest

distribution system

to maximise the value

of each rough carat

D O W N S T R E A M : • Support consumer preference for diamonds in main

consumer markets through branded propositions

• Consumer and trade intelligence

• Better understanding of polished diamonds

M I D S T R E A MUnique value proposition

D O W N S T R E A MDemand generation and future growth platform

ConsumersJewellery

manufacturingJewellery

retail

Polished manufacturing

and trading

Rough distributionand tradingMining

Explorationand projects

T E C H N O L O G Y & I N N O VAT I O N : TA L E N T & L E A D E R S H I P

5

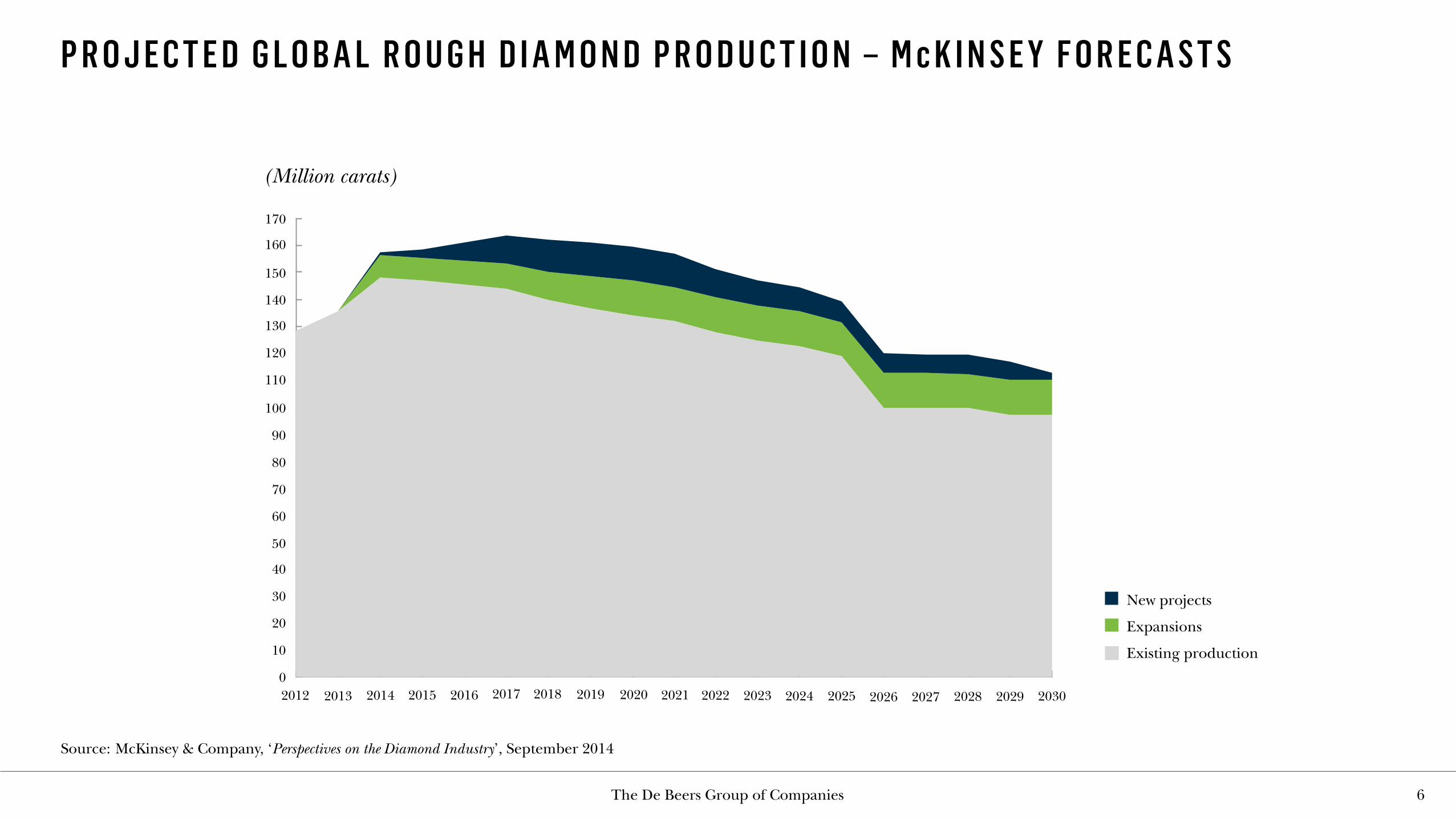

P R O J E C T E D G L O B A L R O U G H D I A M O N D P R O D U C T I O N – M c K I N S E Y F O R E C A S T S

The De Beers Group of Companies

Source: McKinsey & Company, ‘Perspectives on the Diamond Industry’, September 2014

(Million carats)

New projects

Expansions

Existing production

6

The De Beers Group of Companies

M I D S T R E A M P R E S S U R E S

M I D S T R E A M

Upward pressure on

rough price due to higher

production costs

Downward pressure on

polished price as retailers

look to maintain price points

Changing industry stock-

holding patterns pushes

burden of inventory to

cutting centres

Financing challenges as

banks require greater

transparency and

financial strength

7

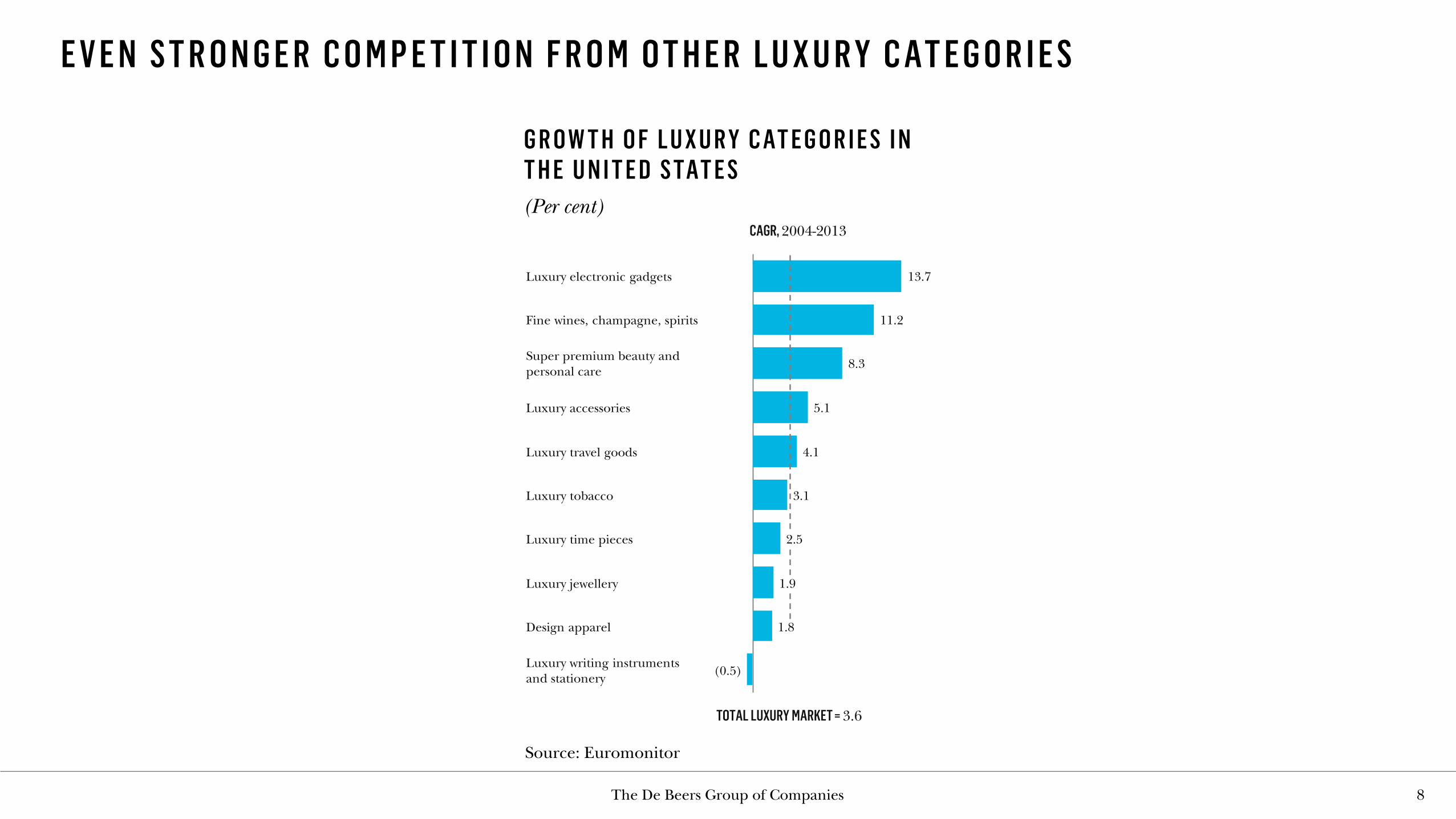

E V E N S T R O N G E R C O M P E T I T I O N F R O M O T H E R L U X U R Y C AT E G O R I E S

The De Beers Group of Companies

Source: Euromonitor

G R O W T H O F L U X U R Y C AT E G O R I E S I N T H E U N I T E D S TAT E S(Per cent)

8

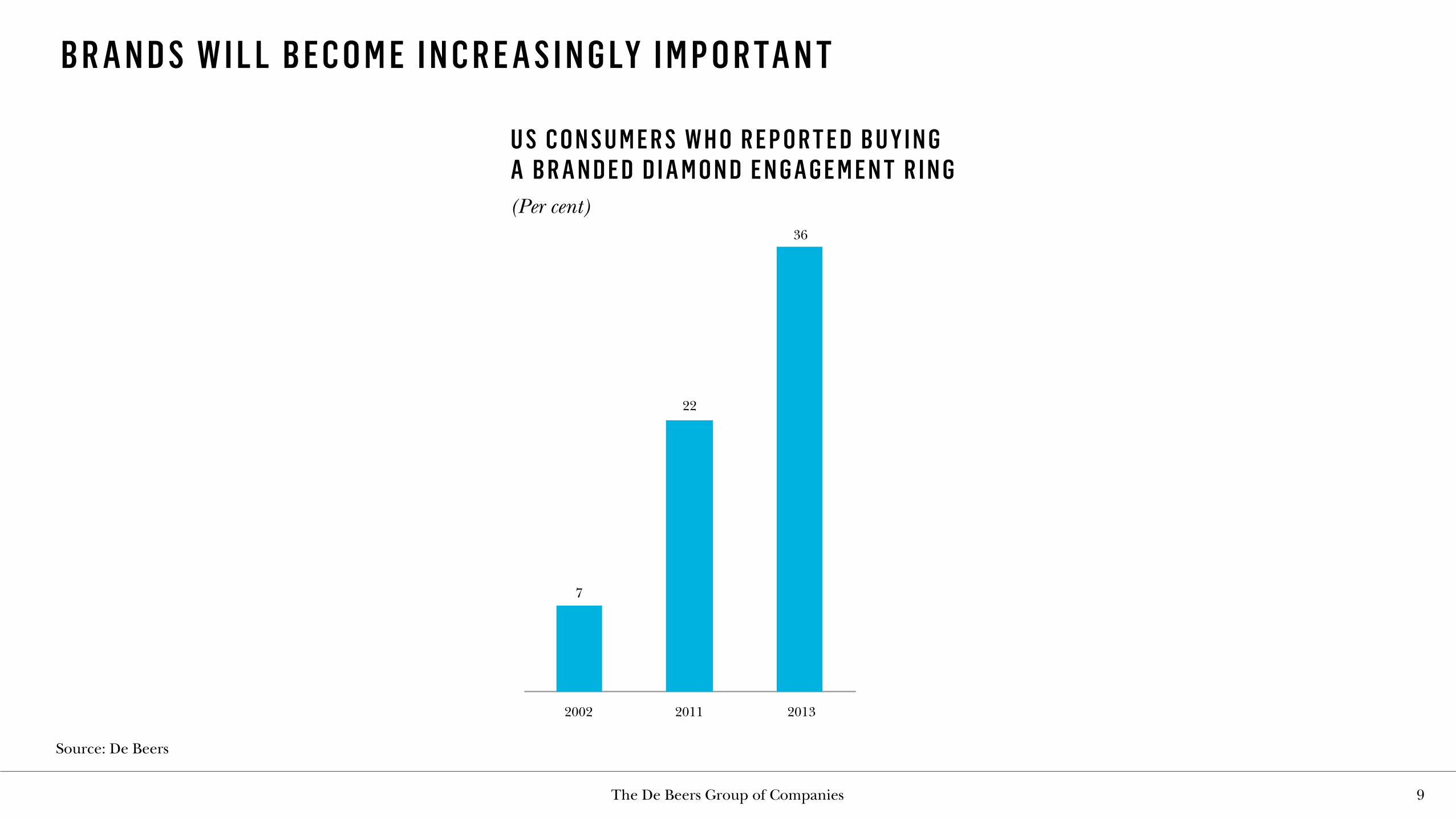

B R A N D S W I L L B E C O M E I N C R E A S I N G LY I M P O R TA N T

The De Beers Group of Companies

Source: De Beers

U S C O N S U M E R S W H O R E P O R T E D B U Y I N G A B R A N D E D D I A M O N D E N G A G E M E N T R I N G(Per cent)

9

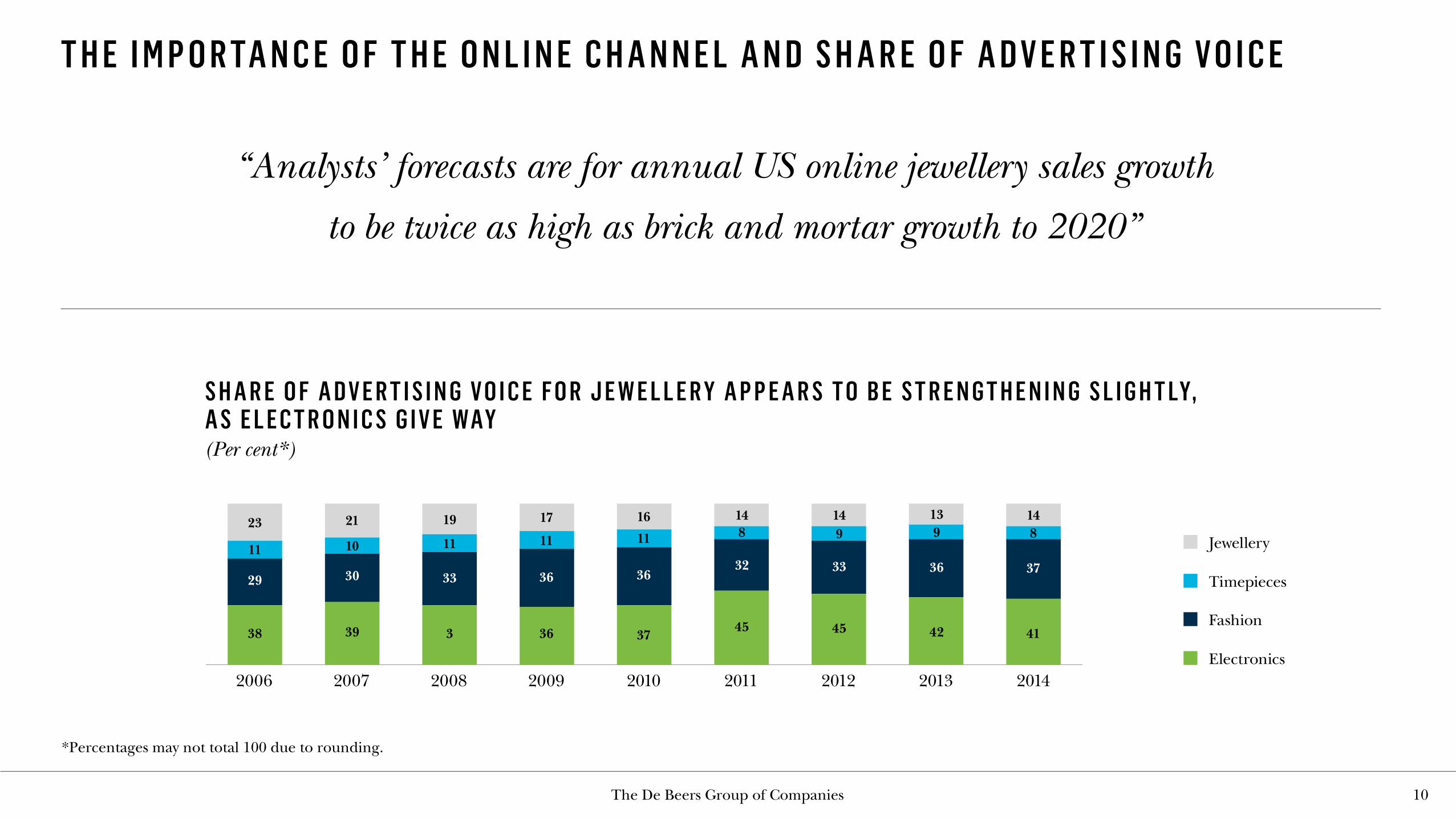

T H E I M P O R TA N C E O F T H E O N L I N E C H A N N E L A N D S H A R E O F A D V E R T I S I N G V O I C E

“Analysts’ forecasts are for annual US online jewellery sales growth

to be twice as high as brick and mortar growth to 2020”

*Percentages may not total 100 due to rounding.

21

10

30

39

17

11

36

36

23

11

29

38

19

11

33

3

148

32

45

139

36

42

148

37

41

16

11

36

37

149

33

45

Jewellery

Timepieces

Fashion

Electronics

S H A R E O F A D V E R T I S I N G V O I C E F O R J E W E L L E R Y A P P E A R S T O B E S T R E N G T H E N I N G S L I G H T LY, A S E L E C T R O N I C S G I V E WAY(Per cent*)

2006 2007 2008 2009 2010 2011 2012 2013 2014

The De Beers Group of Companies 10

T H E U S A N D C H I N A W I L L R E M A I N T H E K E Y M A R K E T S F O R D I A M O N D C O N S U M P T I O N F O R T H E F O R E S E E A B L E F U T U R E

The De Beers Group of Companies

1. Greater China includes China, Hong Kong and Macau

Source: De Beers Group Strategy analysis

USA 42%

China 16%

India 8%

Japan 5%

Gulf 8%

EU 28%

ROW 13%

USA 40%

Greater China1 19%

India 9%

Japan 4%

Gulf 7%

ROW 20%

2 0 1 8 F2 0 1 4

Main trends:• Global consumer demand is forecast to grow at an annual average of 4-5% in US$ nominal terms (through to 2018)

• The US is expected to remain the largest market for polished diamonds with roughly the same share by 2018 as in 2014

• Continued Asian and especially Chinese middle class growth should support demand growth for diamonds with Greater China1 expected to account for approximately 19% of world total demand by 2018

• India is set to remain an important market but its trajectory is currently more uncertain

11

P R O J E C T E D G R O W T H O F M I D D L E C L A S S E S I N E M E R G I N G M A R K E T S S H O U L D S E E C O N T I N U E D G L O B A L D E M A N D G R O W T H F O R D I A M O N D S

The De Beers Group of Companies

Source: Oxford Economics

Brazil 27%

Russia 49%

Turkey 33%

South Africa 69%

Mexico 27%

Indonesia 164%

India 72%

China 129%

2 0 1 4

• Total number of US households with annual income >US$35,000 approximately 100mn in 2013 (75% of US households)

• Middle class households in emerging markets defined as those with annual income >US$20,000, except in India where it is >US$10,000

P R O J E C T E D G R O W T H O F M I D D L E C L A S S E S I N E M E R G I N G M A R K E T S(Per cent change 2013A-2018F)

N U M B E R O F P R O J E C T E D A D D I T I O N A L M I D D L E C L A S S H O U S E H O L D S I N 2 0 1 8 F V S . 2 0 1 3 A (Millions)

13

6

10

4

2

5

11

27

99

USA

Bra

zil

Ru

ssia

Tu

rkey

So

uth

Afr

ica

Mexic

o

Ind

on

esi

a

Ind

ia

Ch

ina

12

S U P P LY / D E M A N D C U R V E B A S E D O N M c K I N S E Y F O R E C A S T S

The De Beers Group of Companies

Source: McKinsey Global Insitute; McKinsey & Company, ‘Perspectives on the Diamond Industry’, September 2014

(Index base 100 in 2014)

2014F 2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2024F

60

80

100

120

140

160

180

Demand forecast

Production forecast

13

S A F E G U A R D I N G C O N S U M E R C O N F I D E N C E

The De Beers Group of Companies

The AMS is a compact, automated version of DiamondSure that enables 360 small stonesper hour to be tested completely automatically

14

• Various companies have the ability to manufacture gem-quality synthetic diamonds utilising different technologies (HPHT and CVD, principally)

• Trading in undisclosed or misrepresented gem synthetics risks damage to consumer con�dence, so accurate descriptions and clear disclosure are fundamentally important

• De Beers has invested around US$65m (in today’s values) to develop sophisticated detection technology including DiamondSure™ and DiamondView™ that can readily identify all types of gem synthetics

• Latest generation of technology from De Beers includes the Automated Melée Screening device (AMS), to scan colourless and near-colourless melée (small diamonds) quickly and cost-effectively

• With De Beers’ leadership, the industry has so far been successful in safeguarding consumer con�dence. Continual investment in developing and deploying technology will be required to sustain that success in the future

T H E F U T U R E O F T H E D I A M O N D I N D U S T R Y

Bruce Cleaver, Executive Head of Strategy