the deloitte consumer tracker confidence suffers …...uk consumer confidence suffered a setback in...

TRANSCRIPT

Q4 2013

A Deloitte Insight Report

The Deloitte Consumer TrackerConfidence suffers a setback

Contents

About this researchThe Deloitte Consumer Tracker is based on a consumer survey carried out by independent market research agency, YouGov, on our behalf. This survey was conducted online with a nationally representative sample of over 3,000 UK adults aged 18+ between 3 and 5 January 2014.

A note on the methodologySome of the figures in this research show the results in the form of a net balance. This means that in a survey of 100 respondents, assume that 30 reported they are spending more, 50 reported no change and 20 reported they are spending less. The net balance is calculated by subtracting the number that reported they spent less from the number that reported they spent more, i.e. 30 – 20 = 10. This means 10 per cent of consumers reported that they spent more rather than less.

The Deloitte Consumer Tracker 1

Confidence suffers a setback 2

Downward pressure on discretionary spending continues to ease 4

The outlook remains positive 7

Contacts 9

UK consumer confidence suffered a setback in the fourth quarter of 2013 according to the latest edition of the Deloitte Consumer Tracker.

The Tracker shows that consumer confidence slowed in Q4, halting 2013’s upward trajectory. Consumers were less optimistic about their level of disposable income, their job and their level of debt in the fourth quarter, highlighting some of the headwinds still facing the consumer recovery.

Household budgets remain under pressure, with real disposable income remaining flat since 2009. In fact, recent gains in consumer spending have been largely fuelled by a mixture of historically low interest rates, consumers dipping into their savings, easier access to credit and lower inflation.

The Deloitte Consumer TrackerQ4 2013

Key findings:

• All measures of confidence slowed in the fourth quarter, following a 12-month upward trend, highlighting that there are still some headwinds facing the consumer recovery.

• In an illustration of the uneven nature of the recovery the Tracker shows that downward pressure on discretionary spending continued to ease, with categories such as going out, clothing and electricals seeing a net improvement year-on-year.

• Our data also shows that both expansionary and defensive behaviours have been growing simultaneously, as consumers continue to trade selectively at both the premium and value end of the market.

• Entering 2014, we would expect consumer confidence to return to an upwards trajectory, as lower inflation and an improving labour market combine to help lift real incomes and provide the conditions for sustained growth in the consumer market.

Figure 1. UK consumer confidence

Net % of UK consumers who said that their level of confidence has improved during the pastthree months

-20%

-15%

-10%

-5%

0%

Q42013

Q32013

Q22013

Q12013

Q42012

Q32012

Q22012

Q12012

Q42011

Q32011

-18%

-15%-14% -15%

-13%-15%

-12%

-10%

-8%

-11%

The Tracker also shows that consumers have been reducing their spending in essential categories as a result of lower inflation, which has allowed them to increase spending in more discretionary areas. Categories such as going out, clothing and electricals saw a net improvement year-on-year.

In addition, the data highlights that both expansionary behaviours such as trading up and buying more, and defensive behaviours such as trading down have been growing simultaneously, although expansionary behaviours are growing at a faster rate.

The example of the retail market can explain this paradox where we have seen growth at both the premium and value end of the market, often with the same consumers shopping at both ends. The net effect is that the middle has been squeezed.

Entering 2014, we would expect consumer confidence to return to an upwards trajectory, as lower inflation and an improving labour market combine to help lift real incomes and provide the conditions for sustained growth in the consumer market.

Deloitte Consumer Tracker Q4 2013 1

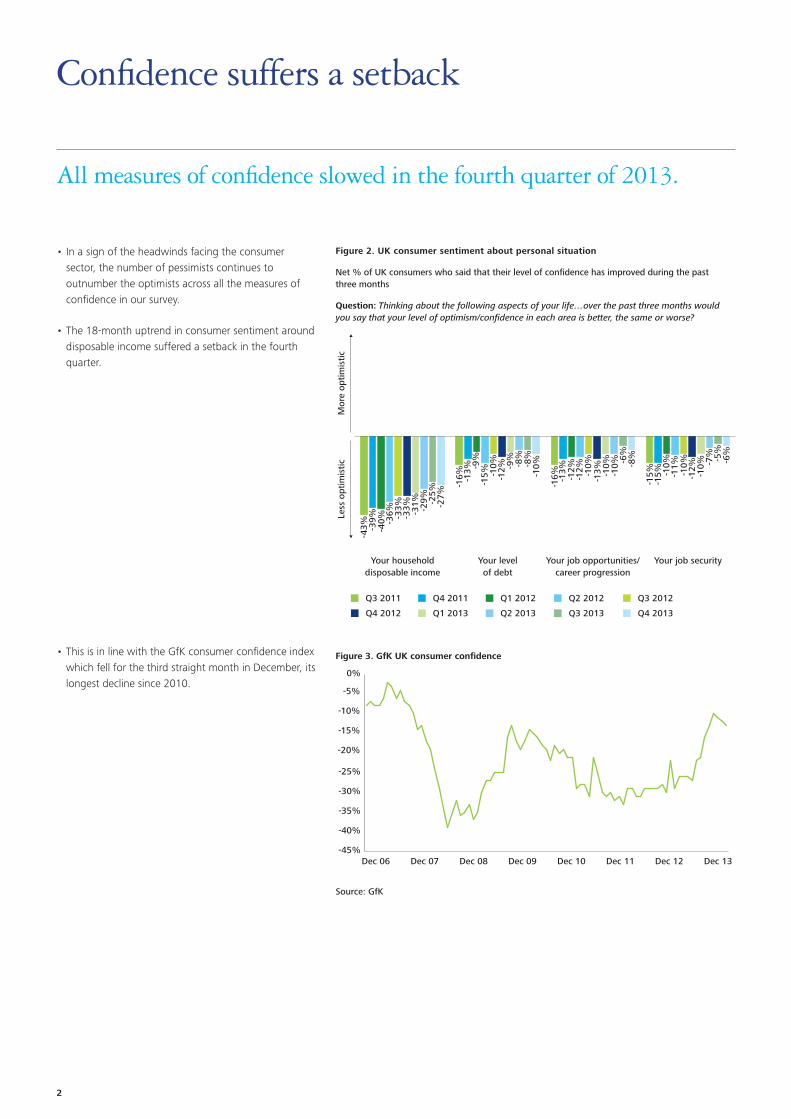

• In a sign of the headwinds facing the consumer sector, the number of pessimists continues to outnumber the optimists across all the measures of confidence in our survey.

• The 18-month uptrend in consumer sentiment around disposable income suffered a setback in the fourth quarter.

Figure 2. UK consumer sentiment about personal situation

Net % of UK consumers who said that their level of confidence has improved during the past three months

Question: Thinking about the following aspects of your life…over the past three months would you say that your level of optimism/confidence in each area is better, the same or worse?

Your job securityYour job opportunities/career progression

Your levelof debt

Your householddisposable income

-43%

Less

opt

imis

tic

Mor

e op

tim

isti

c

-40%

-39% -3

6% -33%

-33% -31% -29% -2

5%-2

7%

-16%

-9%

-13%

-15% -1

0%-1

2% -9%

-8%

-8%

-10%

-16% -1

2%-1

3%

-12% -10%

-13% -1

0%-1

0% -6%

-8%

-15% -1

0%-1

5% -11%

-10%

-12%

-10% -7

% -5%

-6%

Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012

Q4 2013Q4 2012 Q1 2013 Q2 2013 Q3 2013

• This is in line with the GfK consumer confidence index which fell for the third straight month in December, its longest decline since 2010.

Figure 3. GfK UK consumer confidence

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Dec 06 Dec 07 Dec 08 Dec 09 Dec 10 Dec 11 Dec 12 Dec 13

Source: GfK

Confidence suffers a setback

All measures of confidence slowed in the fourth quarter of 2013.

2

• The Tracker results also show that there was a slight increase in the number of people reporting a reduction or loss of income, while fewer started a new job in the fourth quarter.

Figure 4. Changes in personal household circumstances in the past three months

% of UK consumers

Question: Thinking about your household circumstances in the past three months, which of the following apply to you or someone in your household?

Being laid off/made redundant Started a new job Received a pay rise or a bonusReduction/loss of some income

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q4 2013Q3 2013Q2 2013Q1 2013Q4 2012Q3 2012Q2 2012Q1 2012Q4 2011

• Official employment figures improved in the last two years.

Figure 5. UK unemployment rate (16 and over)

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Sep03

Sep04

Sep05

Sep06

Sep07

Sep08

Sep09

Sep10

Sep11

Sep12

Sep13

UK LFS: Unemployment rate, all aged 16 & over SADJ

• Despite the recent growth in employment, economic commentators agree that much of the weakness in household incomes is attributable to low real wage growth since the onset of the economic downturn.

Figure 6. Average earnings growth and UK national inflation

-4

-3

-2

-1

0

1

2

3

4

5

6

Dec

07

Mar

08

Jun

08Se

p 08

Dec

08

Mar

09

Jun

09Se

p 09

Dec

09

Mar

10

Jun

10Se

p 10

Dec

10

Mar

11

Jun

11Se

p 11

Dec

11

Mar

12

Jun

12Se

p 12

Dec

12

Mar

13

Jun

13Se

p 13

Dec

13

CPI Harmonised inflation Average earnings after tax

Source: ONS

Deloitte Consumer Tracker Q4 2013 3

Downward pressure on discretionary spending continues to ease

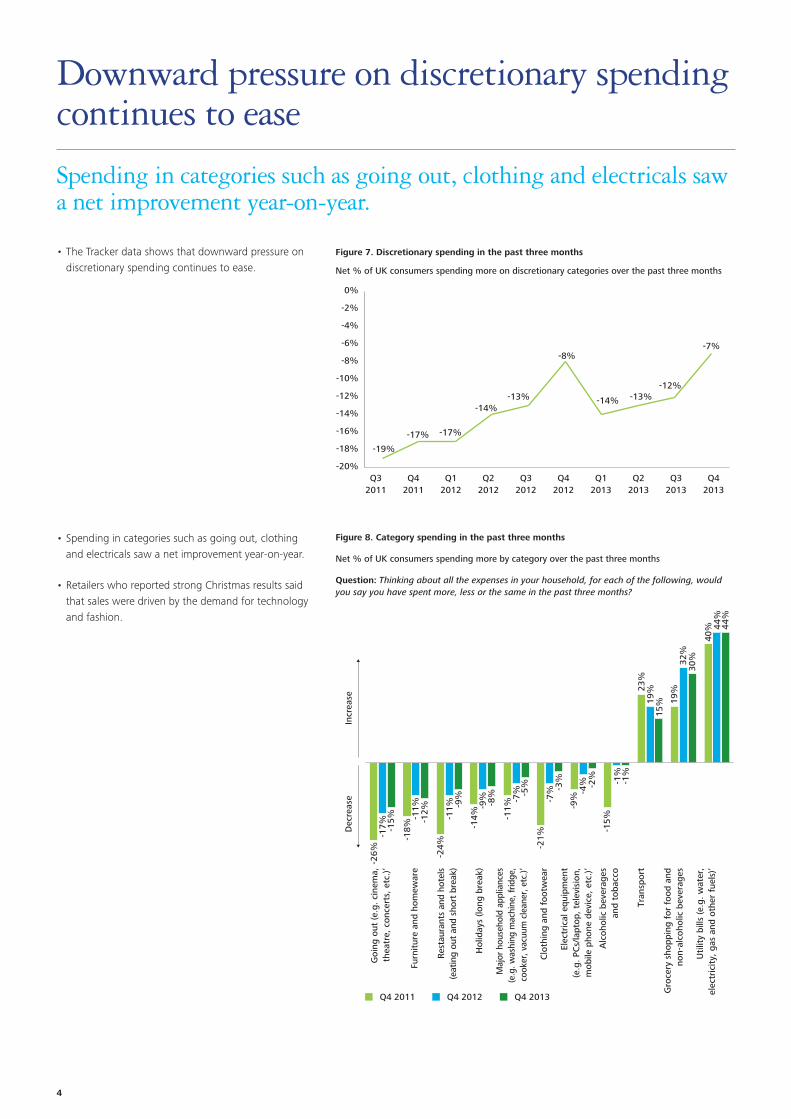

• The Tracker data shows that downward pressure on discretionary spending continues to ease.

Figure 7. Discretionary spending in the past three months

Net % of UK consumers spending more on discretionary categories over the past three months

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

-19%

-17% -17%

-14%-13%

-8%

-14% -13%-12%

-7%

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

• Spending in categories such as going out, clothing and electricals saw a net improvement year-on-year.

• Retailers who reported strong Christmas results said that sales were driven by the demand for technology and fashion.

Figure 8. Category spending in the past three months

Net % of UK consumers spending more by category over the past three months

Question: Thinking about all the expenses in your household, for each of the following, would you say you have spent more, less or the same in the past three months?

Q4 2011 Q4 2012 Q4 2013

Dec

reas

eIn

crea

se

Goi

ng o

ut (e

.g. c

inem

a,th

eatr

e, c

once

rts,

etc

.)’

Furn

itur

e an

d ho

mew

are

Res

taur

ants

and

hot

els

(eat

ing

out

and

shor

t br

eak)

Hol

iday

s (lo

ng b

reak

)

Maj

or h

ouse

hold

app

lianc

es(e

.g. w

ashi

ng m

achi

ne, f

ridge

, co

oker

, vac

uum

cle

aner

, etc

.)’

Clo

thin

g an

d fo

otw

ear

Tran

spor

t

Gro

cery

sho

ppin

g fo

r fo

od a

nd

non-

alco

holic

bev

erag

es

Uti

lity

bills

(e.g

. wat

er,

elec

tric

ity,

gas

and

oth

er f

uels

)’

Elec

tric

al e

quip

men

t (e

.g. P

Cs/

lapt

op, t

elev

isio

n,

mob

ile p

hone

dev

ice,

etc

.)’

Alc

ohol

ic b

ever

ages

and

toba

cco

-26%

-17%

-18%

-11%

-11%

-11%

-7%

-7% -3

%

-4% -2

% -1%

23%

19%

19%

32%

30%

40% 44

%44

%

15%

-1%

-21%

-5%

-9%

-9%

-9%

-8%

-12%

-14%

-15%

-24%

-15%

Spending in categories such as going out, clothing and electricals saw a net improvement year-on-year.

4

• The steady growth in discretionary spending has been partly fuelled by falling inflation in utility and food prices.

Figure 9. UK CPI categories

Dec 12 Dec 07Dec 13

-15 -10 -5 0 5 10 15 20

Food & Non-alcoholic beverages

Alcoholic beverages, Tobacco & Narcotics

Clothing & Footwear

Housing, Water & Fuels

Furn, HH equip & Repair of the house

Health

Transport

Communication

Recreation & Culture

Education

Hotels, Cafes & Restaurants

Miscellaneous goods & Services

Total inflation

19.7 8.6

2 2.7 3.1

0.322.6

2.3

3.32.2

0.51.1

0.1

2.52.8

2.1

1.40.90.8

3.73.9

14.3

1.6

5.86

4.4

1.93.8

10.4

0.8-10.3

-3.4

10.3

0.80.7

-1.2

3.23.6

Source: ONS

• Our research also shows that this increase in spending was driven by growth in volume rather than by price inflation.

Figure 10. Reasons consumers spent less in the past three months

% of UK consumers spending more

Question: You just mentioned you spent more in the last three months, which of the following reasons apply to you?

Buying more items More expensive

20%

25%

30%

35%

40%

45%

50%

Q42013

Q32013

Q22013

Q12013

Q42012

Q32012

Q22012

Q12012

Q42011

Q32011

Deloitte Consumer Tracker Q4 2013 5

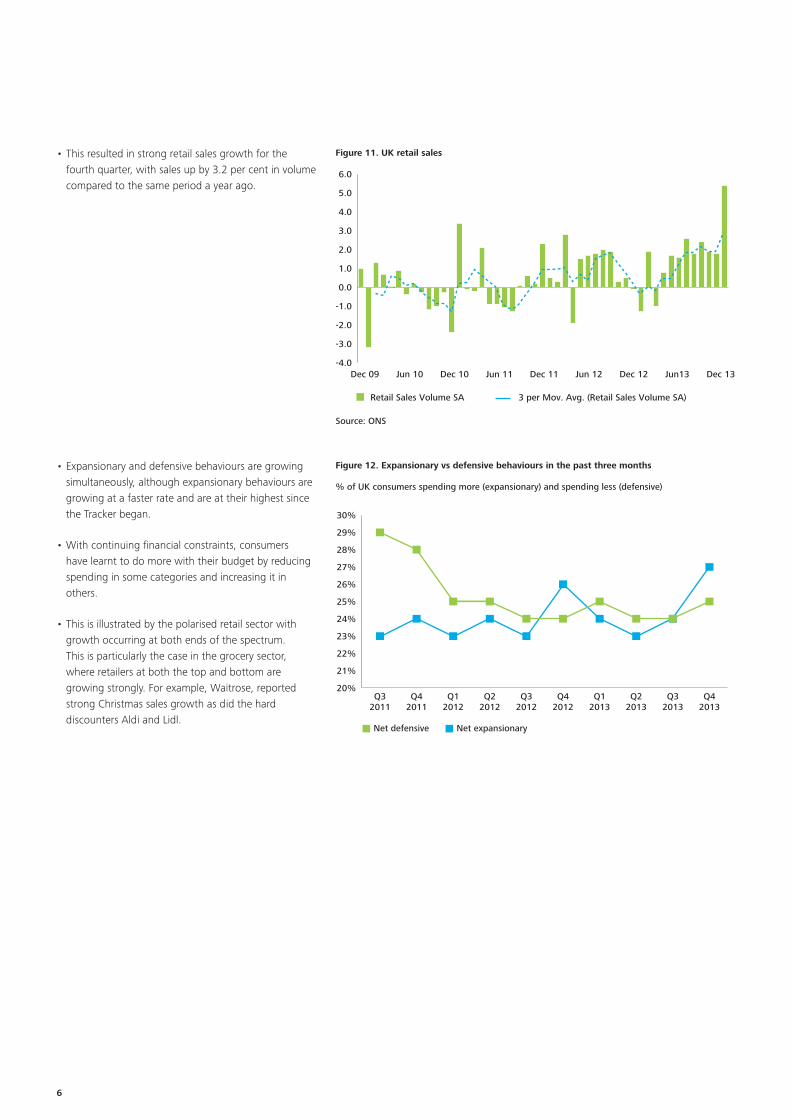

• This resulted in strong retail sales growth for the fourth quarter, with sales up by 3.2 per cent in volume compared to the same period a year ago.

Figure 11. UK retail sales

Retail Sales Volume SA 3 per Mov. Avg. (Retail Sales Volume SA)

Dec 09 Jun 10 Jun 11 Jun 12 Jun13Dec 10 Dec 11 Dec 12 Dec 13-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Source: ONS

• Expansionary and defensive behaviours are growing simultaneously, although expansionary behaviours are growing at a faster rate and are at their highest since the Tracker began.

• With continuing financial constraints, consumers have learnt to do more with their budget by reducing spending in some categories and increasing it in others.

• This is illustrated by the polarised retail sector with growth occurring at both ends of the spectrum. This is particularly the case in the grocery sector, where retailers at both the top and bottom are growing strongly. For example, Waitrose, reported strong Christmas sales growth as did the hard discounters Aldi and Lidl.

20%

21%

22%

23%

24%

25%

26%

27%

28%

29%

30%

Q42013

Q32013

Q22013

Q12013

Q42012

Q32012

Q22012

Q12012

Q42011

Q32011

Net defensive Net expansionary

Figure 12. Expansionary vs defensive behaviours in the past three months

% of UK consumers spending more (expansionary) and spending less (defensive)

6

The outlook remains positive

Further growth in consumer spending expected as conditions continue to improve in the consumer market.

• While our data shows that consumers are expecting to spend less in the grocery and transport categories in the first quarter of this year, the trend towards increasing discretionary spending is expected to continue.

• Compared to the same time last year more consumers are planning major purchases such as buying a car or a property this quarter.

Q4 2011 Q4 2012 Q4 2013

Dec

reas

eIn

crea

se

Goi

ng o

ut (e

.g. c

inem

a,th

eatr

e, c

once

rts,

etc

.)

Furn

itur

e an

d ho

mew

are

Res

taur

ants

and

hot

els

(eat

ing

out

and

shor

t br

eak)

Hol

iday

s (lo

ng b

reak

)

Maj

or h

ouse

hold

app

lianc

es(e

.g. w

ashi

ng m

achi

ne, f

ridge

, co

oker

, vac

uum

cle

aner

, etc

.)

Clo

thin

g an

d fo

otw

ear

Tran

spor

t

Gro

cery

sho

ppin

g fo

r fo

od a

nd

non-

alco

holic

bev

erag

es

Uti

lity

bills

(e.g

. wat

er,

elec

tric

ity,

gas

and

oth

er f

uels

)

Hou

sing

(e.g

. ren

t,m

ortg

age,

mai

nten

ance

)

Elec

tric

al e

quip

men

t (e

.g. P

Cs/

lapt

op, t

elev

isio

n,

mob

ile p

hone

dev

ice,

etc

.)

Alc

ohol

ic b

ever

ages

and

toba

cco

-20%

-24%

-24%

-25% -23% -2

1%

-22%

-23% -2

0%

-23%

-22% -1

9%

-21%

-22%

-16%

-20% -1

6% -14%

-19% -1

7%-1

3%

-8%

-8%

-4%

5%9%

4%

10%

10%

7%

1%4%

8%

17%

30%

31%

Figure 13. UK consumer sentiment about disposable income by income groups

Net % of UK consumers spending more by category over the next three months

Question: And now thinking about all the expenses in your household in the next three months, for each of the following, would you say you will spend more, less or the same compared to four to six months ago?

Figure 14. UK consumer planning major purchases in the next three months

% of UK consumers

Question: Are you planning any of the following in the next three months?

Upgrading:moving into alarger home

Buying a property

Buying a carBuying a major piece of furniture

Buying anexpensive electricalitem (e.g. iPhone,

flat screen TV, computer/

laptop,etc.)

7% 7%

9%

7% 7%8%

5% 5%6%

3% 3%

5%

3%2%

4%

Q4 2011 Q4 2012 Q4 2013

Deloitte Consumer Tracker Q4 2013 7

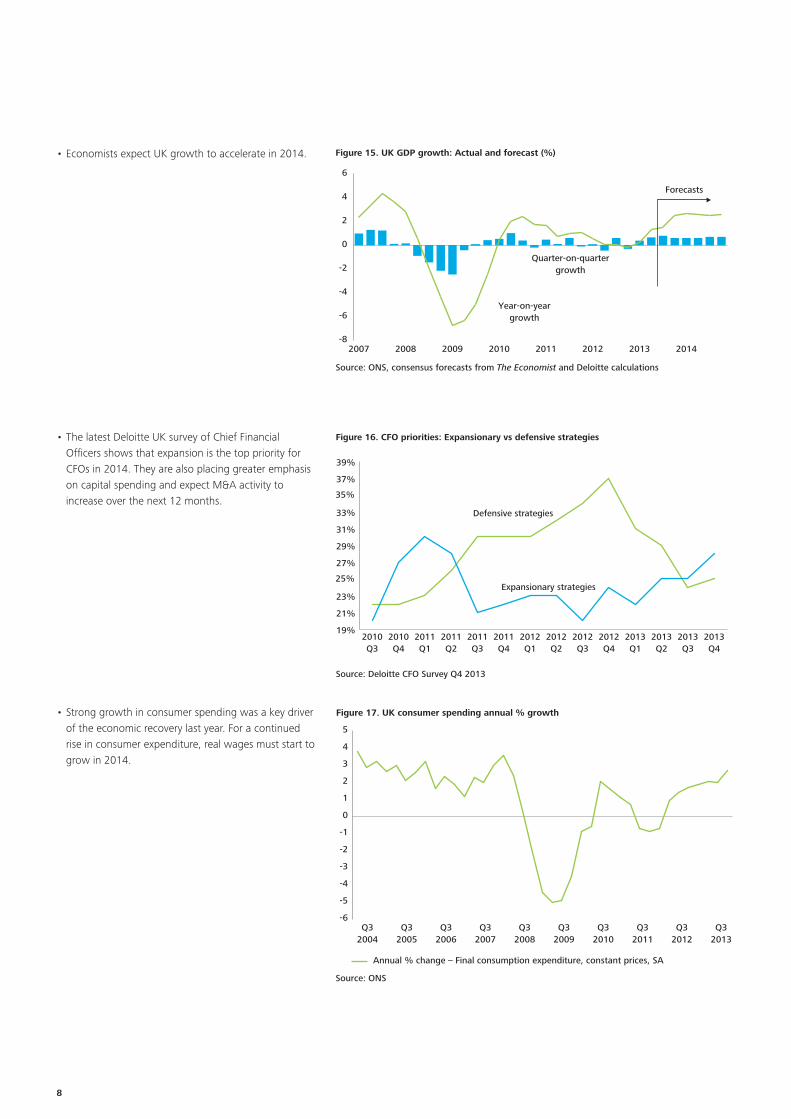

• Economists expect UK growth to accelerate in 2014.

• The latest Deloitte UK survey of Chief Financial Officers shows that expansion is the top priority for CFOs in 2014. They are also placing greater emphasis on capital spending and expect M&A activity to increase over the next 12 months.

• Strong growth in consumer spending was a key driver of the economic recovery last year. For a continued rise in consumer expenditure, real wages must start to grow in 2014.

Figure 15. UK GDP growth: Actual and forecast (%)

Quarter-on-quartergrowth

Year-on-yeargrowth

20142013201220112010200920082007-8

-6

-4

-2

0

2

4

6

Forecasts

Source: ONS, consensus forecasts from The Economist and Deloitte calculations

19%

21%

23%

25%

27%

29%

31%

33%

35%

37%

39%

2013Q4

2013Q3

2013Q2

2013Q1

2012Q4

2012Q3

2012Q2

2012Q1

2011Q4

2011Q3

2011Q2

2011Q1

2010Q4

2010Q3

Defensive strategies

Figure 16. CFO priorities: Expansionary vs defensive strategies

Source: Deloitte CFO Survey Q4 2013

Expansionary strategies

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

Figure 17. UK consumer spending annual % growth

Q32004

Q32005

Q32006

Q32007

Q32008

Q32009

Q32010

Q32011

Q32012

Q32013

Annual % change – Final consumption expenditure, constant prices, SA

Source: ONS

8

Authors

Ben PerkinsHead of Research, Consumer Business020 7307 [email protected]

Céline FenechResearch Manager, Consumer Business020 7303 [email protected]

Aino PietikainenResearch Manager, Consumer Business020 7007 [email protected]

Leadership team

Nigel WixceyIndustry Leader, Consumer Business020 7303 [email protected]

Ian GeddesLead Partner, UK Retail020 7303 [email protected]

Graham PickettLead Partner, UK Travel, Hospitality and Leisure01293 [email protected]

Contacts

Deloitte Consumer Tracker Q4 2013 9

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2014 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

Designed and produced by The Creative Studio at Deloitte, London. 32472A