the bonds have been issued. now what? practical ... are post-issuance tax compliance procedures? 4...

TRANSCRIPT

Virginia Resources AuthorityGovernor’s Infrastructure

Financing ConferenceDecember 14-16, 2016

The Bonds Have Been Issued. Now What?

Practical Suggestions on Post-Issuance Compliance and

Navigating an IRS Audit:

The City of Winchester Experience

Mary M. Blowe

Chief Financial

Officer/Director of

Support Services

Winchester, VA

Christopher G. Kulp

Partner

Hunton & Williams LLP

Richmond, VA

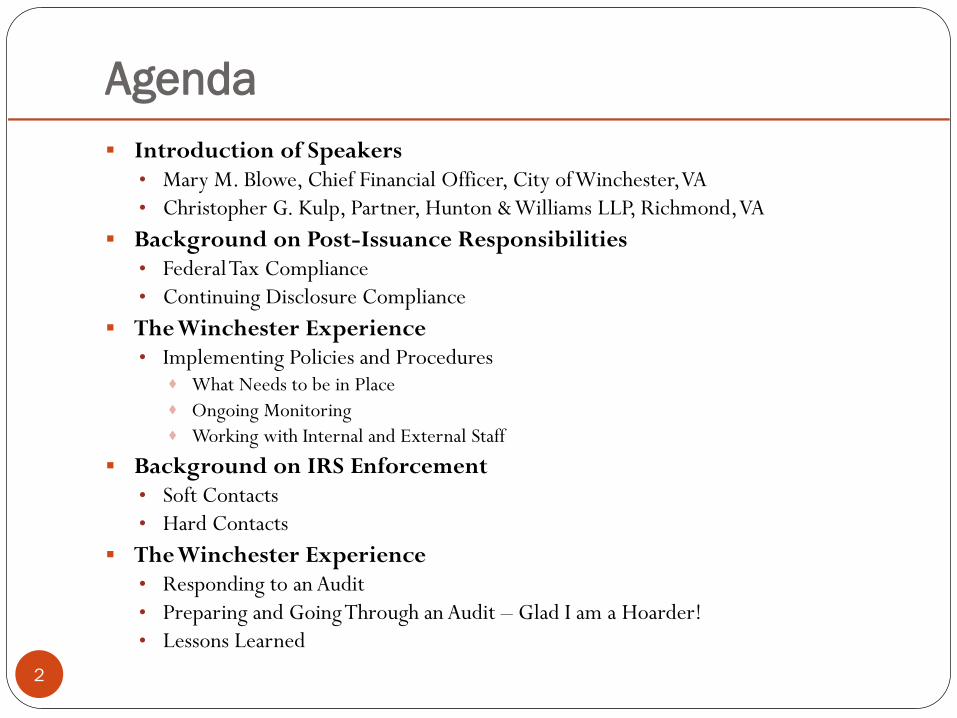

Agenda

2

Introduction of Speakers• Mary M. Blowe, Chief Financial Officer, City of Winchester, VA

• Christopher G. Kulp, Partner, Hunton & Williams LLP, Richmond, VA

Background on Post-Issuance Responsibilities• Federal Tax Compliance

• Continuing Disclosure Compliance

The Winchester Experience• Implementing Policies and Procedures

What Needs to be in Place

Ongoing Monitoring

Working with Internal and External Staff

Background on IRS Enforcement• Soft Contacts

• Hard Contacts

The Winchester Experience• Responding to an Audit

• Preparing and Going Through an Audit – Glad I am a Hoarder!

• Lessons Learned

Background on Post-Issuance

Responsibilities

Federal Tax Compliance

3

What are Post-Issuance Tax Compliance

Procedures?

4

Procedures that describe the actions to be taken by entity to maximize likelihood that tax rules will be followed for the life of a bond issue

Applicable to all bonds (includes all debt obligations such as bonds, notes, financing leases, etc.) issued on a “tax-advantaged” basis• Tax-exempt bonds• Taxable bonds for which bondholder receives federal tax credits or

issuer receives direct-pay bond subsidy payments (e.g., QZABs, BABs)

Procedures may be part of entity’s general debt management policies or in form of separate policies

Procedures may be adopted by formal action of governing body or incorporated by management

Why Create Written Policies &

Procedures?

5

Fulfill entity’s contractual obligation with bondholders to maintain tax-exempt or tax credit status

Default could lead to loss of tax-advantaged status (worst case); loss of federal subsidy for direct-paytax credit bonds

IRS has strongly encouraged governmental entities to create written procedures to manage tax compliance• Currently not a federal tax law requirement, but ignore at one’s peril• IRS Form 8038-G asks about written procedures to address arbitrage

compliance and remedial actions

Practical consideration that entity will have easier time responding to IRS enforcement action• Information related to bond likely to be retained and available• Lower probability of tax errors if ongoing monitoring in place

IRS Form 8038-G

Issuer Certifications

6

Form of Written Procedures

7

No particular industry standard

IRS has not mandated particular form of written

procedures

Use of common sense in developing written

procedures

• Be comprehensive but need to tailor procedures to particular

entity – taking into account size of entity, type of bond deals,

frequency of bond issuance, availability of resources

Reliance solely on closing documents is not likely to

be sufficient

Primary Elements of an Effective

Post-Issuance Tax Compliance Program

8

Primary Elements

9

Written policies and procedures

Individual(s) assigned to manage compliance process

Record retention

Arbitrage rebate and yield restriction compliance; final

allocation; and filings with IRS (as applicable)

Monitoring private business use

Staff training and education

Periodic review of procedures and awareness of VCAP and

other remedial actions

Create Written Policies & Procedures –

Where to Start?

10

Start by documenting current unwritten procedures

Use bond documents and published information materials as guides

• Bond documents: Non-Arbitrage Certificate, Arbitrage Rebate Compliance Instructions, Trust Indenture

requirements, etc.

• Gov’t Compliance Check Questionnaire – Form 14002 (https://www.irs.gov/pub/irs-tege/f14002.pdf)

• Direct Pay BABs Compliance Check Questionnaire – Form 14127 (https://www.irs.gov/pub/irs-

tege/form_14127.pdf)

• GFOA’s Alert – Developing and Implementing Procedures for Post-Issuance Tax Compliance for Issuers of

Governmental Bonds (https://www.gfoa.org/developing-and-implementing-procedures-post-issuance-tax-

compliance-issues-governmental-bonds)

• NABL’s Considerations for Developing Post-Issuance Tax Compliance Procedures (September 2016) (PDF – link

on GFOA alert above)

• NABL/GFOA Post-Issuance Compliance Checklist (www.gfoa.org/downloads/PostIssuanceCompliance.pdf)

• Advising Committee on Tax-Exempt and Government Entities (ACT) Paper – “After the Bonds Are Issued, Then

What?”

(www.irs.gov/pub/irs-tege/bonds_act_0607.pdf)

Review with bond counsel and financial advisor

Individuals Assigned to Manage

Compliance Process

11

Assign individual(s) (by title) who will be responsible for compliance management

• Depends on size of issuer

• Types of bond deals

Give primary point person broad authority to implement procedures, request information from other departments, participate in decisions by entity to change use of financed assets or sell financed assets

May require team effort

• Project/Facilities Coordinator

• Finance Department

• Outside Consultants – financial advisor, rebate consultant and bond counsel

Address succession issues

Record Retention

12

IRS Guidance – IRC Section 6001 – general rule for

proper retention of records for federal tax

purposes:

• Basic records (e.g., transcript)

• Documentation on expenditures of bond proceeds

• Documentation on use of bond-financed property (public vs.

private use, management contracts, research agreements)

• Documentation on all sources of payment or security for the

bonds

• Documentation on investment of bond proceeds

Record Retention (cont’d)

13

Sample records to retain:• Board minutes, resolutions• Feasibility studies, appraisals• Bond transcripts• Newspaper ads, miscellaneous correspondence• Investment records – bank statements, investment transaction

information (e.g., trade confirms), etc.• Expenditure history of bond proceeds – invoices, check images,

documents showing and supporting disbursements• IRS Filings – 8038-T (and related checks), 8038-CP• Records related to acquisition of investment agreements and interest rate

swaps• Payments for a letter of credit or standby bond purchase agreement• Arbitrage rebate and yield restriction compliance reports• Memos to file regarding bad use and other tax questions

Record Retention (cont’d)

14

IRS Tax-Exempt Bond FAQs(https://www.irs.gov/tax-exempt-bond-faqs-regarding-record-retention-requirements)

• Why keep records?

• Who may maintain records?

• What are basic records to maintain?

• Are these the only records to be maintained?

• In what format must records be kept?

• How long should records be kept?

• How does general rule apply to refundings?

• What happens if records are not maintained?

• Can failure to properly maintain records be corrected?

• Are there exceptions to the general rule regarding record retention for certain types of records?

Arbitrage Rebate and

Yield Restriction Compliance

15

Code Section 148 – Arbitrage and Yield

• Expenditure of bond proceeds (including investment earnings),

reimbursement of prior expenditures, final allocation

• Yield calculation – bond, investments

• Temporary periods

• Debt Service Reserve Fund and Bond Fund

• Rebate – spend-down exceptions, “small issuer” exemption

• Yield reduction payments

VA SNAP/Rebate Consultant

Monitoring Private Business Use

16

Federal tax law limits private use of tax-exempt financed facilities to 10% (or 5% for unrelated or disproportionate use)

• Average use measured over the life of the financed facility

Maintain records of private business activities

• e.g., rental of financed facilities for non-governmental functions

Legal counsel should review all management and service agreements, leases, sub-leases, naming rights contracts, etc.

Coordinate use of tax-exempt bond financed facilities with administrative team to ensure compliance

Remedial actions

Staff Training and Education

17

Educate staff about applicable rules, written procedures

Internal communication between departments

Procedures to train new staff

Continuing education – evolving regulatory landscape

Use of outside consultants

Regular Due Diligence

18

Don’t let a good plan sit on the shelf

Should review regularly (at least annually)

Ask questions and analyze whether noncompliance situations

exist

If problems are identified, initiate timely correction of

noncompliance situations

Consider VCAP and other remedial actions

Background on Post-Issuance

Responsibilities

Continuing Disclosure Compliance

19

Background — Rule 15c2-12

20

SEC Rule 15c2-12• Underwriters may not purchase bonds unless issuer has contractually

promised to provide specific continuing disclosure for the lifetime of the bonds Ongoing financial information

Filing notices of certain events

• Purpose is to provide ongoing information about the issuer in the secondary market

• SEC’s recent Municipalities Continuing Disclosure Corporation (“MCDC”) initiative in 2014 and other regulatory actions have focused attention on the need to have a reliable system in place to manage continuing disclosure

• Filings are made electronically at the Electronic Municipal Market Access (“EMMA”) portal (http://emma.msrb.org)

• Issuers may also choose voluntarily to post other information to EMMA for investor relations purposes

Primary Elements of an Effective

Post-Issuance Disclosure Program

21

Continuing Disclosure Agreement

22

The Continuing Disclosure Agreement (“CDA”)

• Developing the CDA terms

• Understanding the requirements set within document for

ongoing disclosure filings

“Annual Financial Information” filed by a certain date

“Event” notice filings

Who makes filing? – Issuer or “Material Obligated Person” (VRA and

VPSA contexts)

Required to file electronically at EMMA

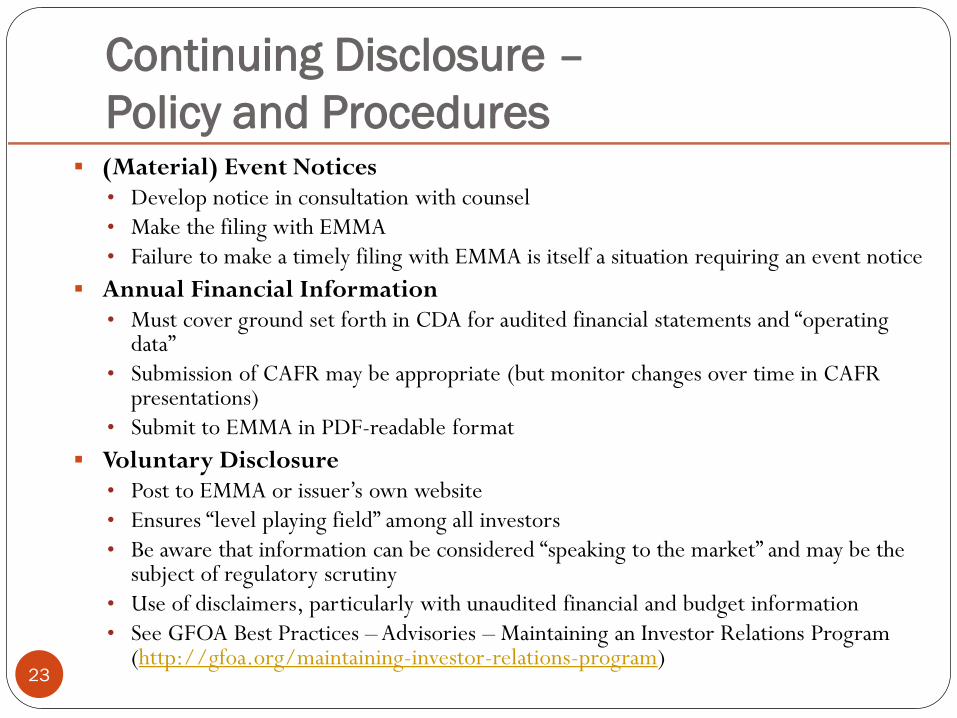

Continuing Disclosure –

Policy and Procedures

23

(Material) Event Notices• Develop notice in consultation with counsel

• Make the filing with EMMA

• Failure to make a timely filing with EMMA is itself a situation requiring an event notice

Annual Financial Information• Must cover ground set forth in CDA for audited financial statements and “operating

data”

• Submission of CAFR may be appropriate (but monitor changes over time in CAFR presentations)

• Submit to EMMA in PDF-readable format

Voluntary Disclosure• Post to EMMA or issuer’s own website

• Ensures “level playing field” among all investors

• Be aware that information can be considered “speaking to the market” and may be the subject of regulatory scrutiny

• Use of disclaimers, particularly with unaudited financial and budget information

• See GFOA Best Practices – Advisories – Maintaining an Investor Relations Program (http://gfoa.org/maintaining-investor-relations-program)

Continuing Disclosure —

Policy and Procedures (cont’d)

24

Identify person with overall responsibility for

overseeing continuing disclosure policy and

procedures

Consider whether to hire a dissemination agent

Develop a disclosure management policy

• Adopt a thorough disclosure policy

• Outline the disclosure practices of your entity

• Adhere to the practices

• Avoid material omissions

• Monitor telephone inquiries from investors

Educational Resources

25

Resources available at MSRB/EMMA

(http://emma.msrb.org/EmmaHelp):

MCDC

26

Municipalities Continuing Disclosure Cooperative (MCDC) Initiative• Self-reporting initiative available in 2014 to issuers and underwriters regarding

materially inaccurate statement in official statements relating to an issuer’s prior compliance with continuing disclosure agreements under SEC Rule 15c2-12

• Initiative concerned accuracy of representations (i.e., disclosure) made in official statements about prior continuing disclosure, not whether the issuer actually complied with its prior continuing disclosure undertakings

• First SEC enforcement action taken against California school district in July 2014, when MCDC initiative announced

• SEC filed enforcement actions against total of 72 municipal underwriting firms (June 2015, September 2015 and February 2016)

• In August 2016, SEC announced actions against 71 municipal issuers and other obligated persons for violating applicable securities laws by using offering documents that contained materially false statements or omissions about their compliance with prior continuing disclosure undertakings

• Expect continued emphasis from SEC (and hence underwriters) on continuing disclosure compliance by issuers

Case Study:

Winchester, VA

27

Learning to Know What

You Need to Know

28

Small city with around 26,000 residents and geographically approximately nine square miles

Six people in City’s Finance Department

Governmental bonds outstanding at June 30, 2016 is $91,122,575

During the past 10 years the City had four new money issuances and three very successful bond refundings

Also issued various revenue bonds through the Virginia Resources Authority for the City’s Utilities Enterprise Fund for water and sewer upgrade projects

Most of the City’s large construction projects have been to finance school remodeling or new construction

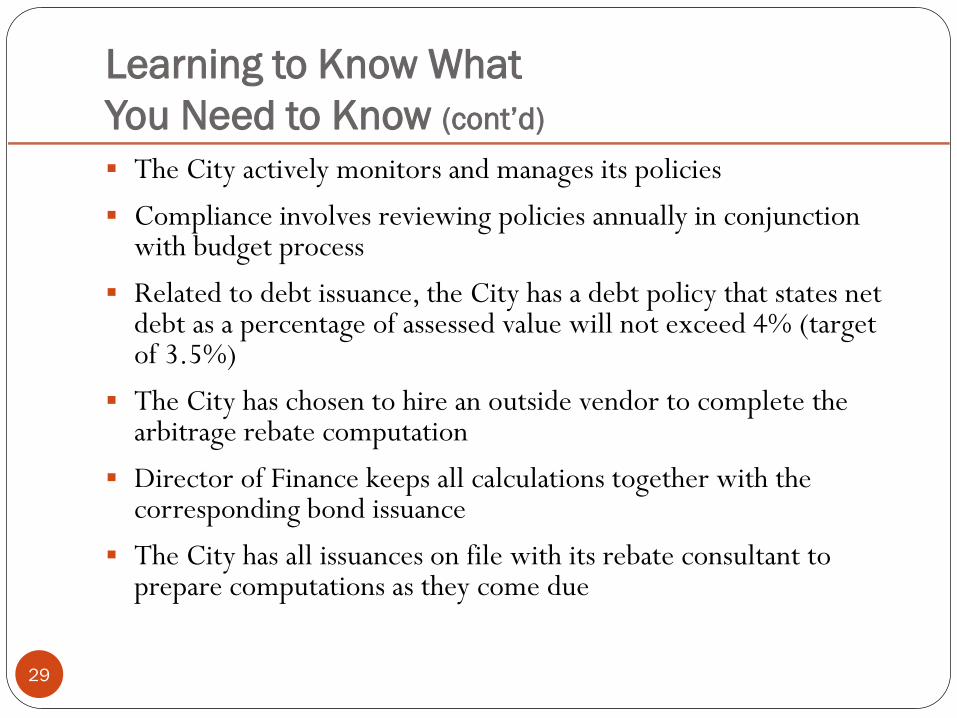

Learning to Know What

You Need to Know (cont’d)

29

The City actively monitors and manages its policies

Compliance involves reviewing policies annually in conjunction with budget process

Related to debt issuance, the City has a debt policy that states net debt as a percentage of assessed value will not exceed 4% (target of 3.5%)

The City has chosen to hire an outside vendor to complete the arbitrage rebate computation

Director of Finance keeps all calculations together with the corresponding bond issuance

The City has all issuances on file with its rebate consultant to prepare computations as they come due

Learning to Know What

You Need to Know (cont’d)

30

City of Winchester Team

• Finance Department Staff

• Financial Advisors

• Governing Body

Outside Professionals

• Bond Counsel

• Arbitrage Rebate Specialist

• Knowing when to call in the professionals

Learning to Know What

You Need to Know (cont’d)

31

Implementing Policies and Procedures

• Developing from scratch

• Using guidelines from Bond Counsel (National Association of

Bond Lawyers) and GFOA; Other localities – VGFOA listserve

• General sections of policy include:

Description of the debt issued

Compliance documentation

Compliance responsibilities

• Who prepared, who reviewed and dates when this was

accomplished

Sample of City of Winchester Policy

32

Description:

• The City utilizes general obligation bonds to finance long-term capital

assets such as City schools, municipal buildings, utilities projects and

other needs for our community

Compliance Documentation:

• Year-end audit

Compliance Responsibilities:

• The City utilizes the computer system EMMA for continuing

disclosure documentation and financial report postings that are

related to each individual CUSIP in the City’s bond issues

• EMMA can be accessed through emma.msrb.org. The Chief

Financial Officer has the sign on and password to access this system

Sample of City of Winchester Policy (cont’d)

33

Arbitrage calculations are prepared by an outside vendor. Vendor has all of our issues on his calendar to ensure all arbitrage deadlines are completed timely. Includes contact information for rebate specialist.

Certain tax covenants: the City has covenanted not to permit the proceeds of the Bonds or the facilities financed with the proceeds of the Bonds to be used for more than 5% of private use, without an opinion of bond counsel. Includes contact information for bond counsel.

The City utilizes an asset management system for its fixed assets to account for all assets whether or not they are financed through bonds or other sources.

Sample of City of Winchester Policy (cont’d)

34

The Chief Financial Officer will review annually the assets

referenced above to ensure the level of private use is

appropriate. Review annually any lease agreements that

affect any assets financed with tax-exempt bonds. Also, any

utility projects financed with tax-exempt bonds shall be

reviewed for any leases or reservations of capacity, or any

“special” rates that may affect the public use of the system.

Background on IRS Enforcement

35

Background on IRS Enforcement

36

IRS has two approaches to its enforcement efforts:

• Facilitate voluntary compliance (“soft contacts”)

• Enforce requirements of the law (“hard exams”)

Soft Contacts with Issuers

37

Compliance Check Questionnaires

• A compliance check is not an examination

• No penalty for failing to respond; however, refusal to participate

will likely lead to an examination

Focused Correspondence

• “We have been provided with certain information”

Hard Contacts with Issuers

38

Full Exams

• Random exams selected on Form 8038-G, Form 8038-CP,

Form 8038 data

• Program exams selected on type of bond purpose (e.g., multi-

family; advance refunding; jail facilities)

• Targeted exams for potential abuse

• “Examination” and “audit” mean the same thing

Recent IRS Efforts

(FY 2017 Work Plan Briefing Document)

39

Exam priority given to claims and referrals warranting examination resources, including whistleblower referrals

In FY 2016, TEB completed exams of 22 returns selected from referral information – principal issues involved private use of bond financed property and arbitrage compliance failure

For FY 2017, TEB will continue developing examination projects based on identified areas of past noncompliance - including prison financings and “small issue” bonds

For FY 2017, TEB will continue to identify market segments that have higher right of noncompliance

• In FY 2015 and FY 2016 – market segment focus included advance refunding issues (with variable interest rates or escrows funded with open market escrow securities) and solid waste financings for projects that included manufacturing processes

New IRS Internal Guidance

40

IRS announced in November 2016 new guidance to agents conducting IRS audits

Specific to the Information Document Request (IDR) process

Meant to be more “taxpayer friendly”

• Agent will discuss bond issue to be examined with issuer prior to issuing the IDR

• Agents required to make IDR more clear and specific as to what information is requested

• Agents required to follow a delinquency notice process if issuer does not timely provide information requested by IDR

Effective April 2017

Case Study:

Winchester, VA

41

Audits!

42

This wasn’t the letter I was expecting

• Don’t throw it in the back of the drawer

• Discuss with counsel

• Find paperwork affiliated with audit scope

• Contact the IRS

How to prepare

• Pull bond document(s) and any arbitrage (IRS) filings to date

• Collect spreadsheets with disbursements and interest earned

• Collect copies of all invoices and corresponding check copies

Audits! (cont’d)

43

What to do when the IRS is in your office – the City of

Winchester Experience:

• The City along with the Jail Authority chose to hire original bond

counsel to be legal representative.

• IRS corresponded with bond counsel and the City/Jail Authority gave

all documentation to bond counsel to return back to the IRS agent.

• IRS agent scheduled 3-4 day onsite visits in finance office.

• IRS agent went through spreadsheets and matched the disbursements

to the check copies.

• By reviewing the dates on spreadsheets, the IRS agent could see when

the funds were spent and how much interest was accrued (and

interest rates for each month).

Audits! (cont’d)

44

What the City learned:• Keep all information associated with the bond issuance• Keep all information updated; the City does this monthly• Hire an arbitrage compliance specialist and stay in contact • Upon each new bond issuance put that on their calendar!

What the City now does differently:• Work to train others on arbitrage compliance, particularly those

managing projects• Watch out for staff turnover and train accordingly and timely

Why it sounds worse than it is!• With the support of arbitrage specialists and good record-keeping, an

issuer will have fewer problems in responding to an audit• Speaking honestly and accurately are the best defenses

Conclusion

Questions?

For more information, contact:

Mary Blowe – (540) 667-1815 [email protected]

Chris Kulp – (804) [email protected]

45