technology and banking final project done done

TRANSCRIPT

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 1/31

1

INTRODUCTION

The term ―banking technology‖ refers to the use of sophisticated information and

communication technologies together with computer science to enable banks to

offer better services to its customers in a secure, reliable, and affordable manner,

and sustain competitive advantage over other banks. In the five decades since

independence, banking in India has evolved through four distinct phases.

During Fourth phase, also called as Reform Phase, Recommendations of the

Narasimham Committee (1991) paved the way for the reform phase in the banking.

Important initiatives with regard to the reform of the banking system were taken in

this phase. Important among these have been introduction of new accounting and

prudential norms relating to income recognition, provisioning and capital

adequacy, deregulation of interest rates & easing of norms for entry in the field of

banking.

Entry of new banks resulted in a paradigm shift in the ways of banking in India.The growing competition, growing expectations led to increased awareness

amongst banks on the role and importance of technology in banking. The arrival of

foreign and private banks with their superior state-of-the-art technology-based

services pushed Indian Banks also to follow suit by going in for the latest

technologies so as to meet the threat of competition and retain their customer base.

Indian banking industry, today is in the midst of an IT revolution.

A combination of regulatory and competitive reasons has led to increasing

importance of total banking automation in the Indian Banking Industry.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 2/31

2

Information Technology has basically been used under two different avenues in

Banking. One is Communication and Connectivity and other is Business Process

Reengineering. Information technology enables sophisticated product

development, better market infrastructure, implementation of reliable techniques

for control of risks and helps the financial intermediaries to reach geographically

distant and diversified markets.

In view of this, technology has changed the contours of three major functions

performed by banks, i.e., access to liquidity, transformation of assets and

monitoring of risks. Further, Information technology and the communication

networking systems have a crucial bearing on the efficiency of money, capital and

foreign exchange markets.

The Software Packages for Banking Applications in India had their beginnings in

the middle of 80s, when the Banks started computerizing the branches in a limited

manner. The early 90s saw the plummeting hardware prices and advent of cheap

and inexpensive but high-powered PCs and servers and banks went in for what was

called Total Branch Automation (TBA) Packages.

The middle and late 90s witnessed the tornado of financial reforms, deregulation,

globalization etc coupled with rapid revolution in communication technologies and

evolution of novel concept of 'convergence' of computer and communication

technologies, like Internet, mobile / cell phones etc.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 3/31

3

OBJECTIVE OF THE STUDY

1. The study is based on Role and Evolution of technology in banking

2. The study is based on Positive and Negative effects of technology in banking

METHODOLOGY OF THE STUDY

This study is based on primary and secondary data

LIMITATIONS OF THE STUDY

The study is based on general bank and not any specific public and private sectors

banks

CHAPTER ARRANGEMENT

Chapter I deals with introduction

Chapter II gives Role and Evolution of technology in banking

Chapter III gives Positive and Negative Effects of technology in banking

Chapter IV deals with Conclusion

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 4/31

4

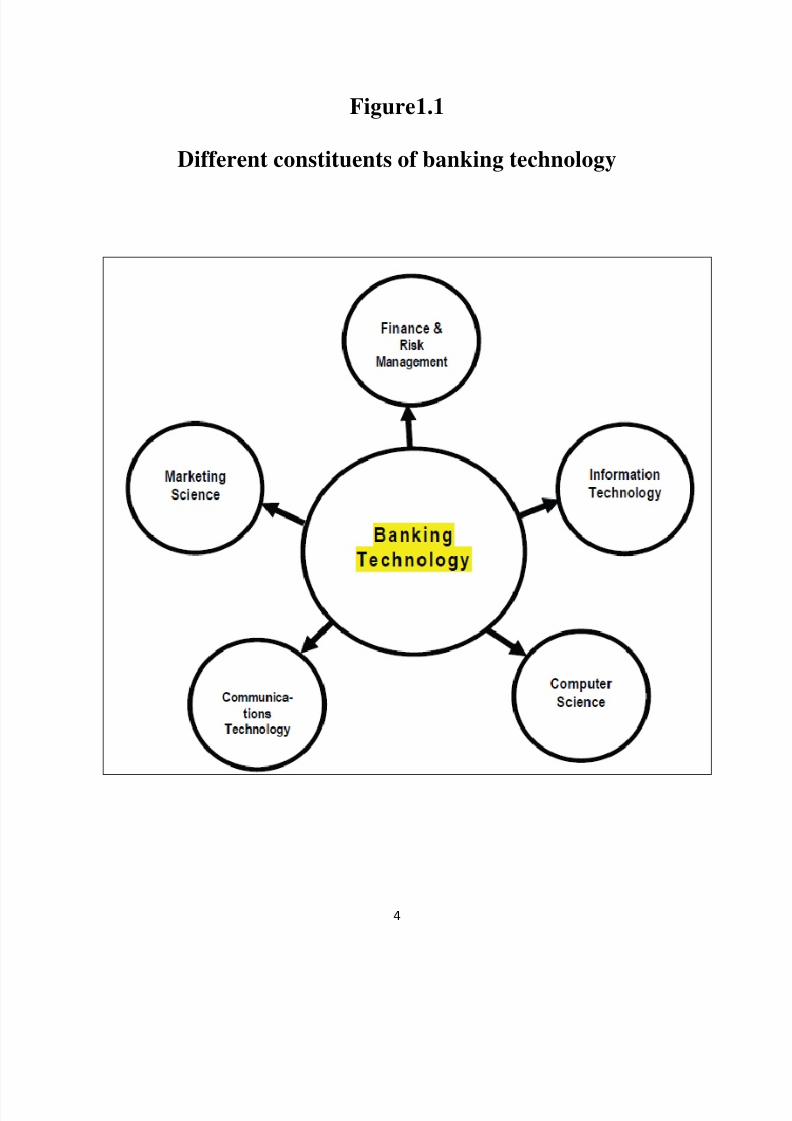

Figure1.1

Different constituents of banking technology

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 5/31

5

EVOLUTION AND ROLE OF TECHNOLOGY IN

BANKING

Evolution

Despite the enormous changes the banking industry has undergone through during

the past 20 years let alone since 1943 one factor has remained the same: the

fundamental nature of the need customers have for banking services. However, the

framework and paradigm within which these services are delivered has changed

out of recognition. It is clear that people‘s needs have not changed, and neither hasthe basic nature of banking services people require. But the way banks meet those

needs is completely different today.

They are simply striving to provide a service at a profit. Banking had to adjust to

the changing needs of societies, where people not only regard a bank account as a

right rather than a privilege, but also are aware that their business is valuable to the

bank, and if the bank does not look after them, they can take their businesselsewhere.

Indeed, technological and regulatory changes have influenced the banking industry

during the past 20 years so much so that they are the most important changes to

have occurred in the banking industry, apart from the ones directly caused by the

changing nature of the society itself. In this book, technology is used

interchangeably with information and communication technologies together with

computer science. The relationship between banking and technology is such that

nowadays it is almost impossible to think of the former without the latter.

Technology is as much part of the banking industry today as a ship‘s engine is part

of the ship. Thus, like a ship‘s engine, technology drives the whole thing forward

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 6/31

6

Technology in banking ceased being simply a convenient tool for automating

processes. Today banks use technology as a revolutionary means of delivering

services to customers by designing new delivery channels and payment systems.

For example, in the case of ATMs, people realized that it was a wrong approach to

provide the service as an additional convenience for privileged and wealthy

customers. It should be offered to the people who find it difficult to visit the bank

branch. Further, the cost of delivering the services through these channels is also

less. Banks then went on to create collaborative ATM networks to cut the capital

costs of establishing ATM networks, to offer services to customers at convenient

locations under a unified banner.

People interact with banks to obtain access to money and payment systems they

need. Banks, in fact, offer only what might be termed as a secondary level of utility

to customers, meaning that customers use the money access that banks provide as a

means of buying the things they really want from retailers who offer them a

primary level of utility. Customers, therefore, naturally want to get the interaction

with their bank over as quickly as possible and then get on with doing something

they really want to do or with buying something they really want to buy. That

explains why new types of delivery channels that allow rapid, convenient, accurate

delivery of banking services to customers are so popular.

Nowadays, customers enjoy the fact that their banking chores are done quickly and

easily. This does not mean that the brick-and-mortar bank branches will

completely disappear. Just as increasing proliferation of mobile phones does not

mean that landline telephone kiosks will disappear, so also the popularity of high-

tech delivery channels does not mean that physical branches will disappear

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 7/31

7

altogether. It has been found that corporate and older persons prefer to conduct

their business through bank branches.

The kind of enormous and far-reaching developments discussed above have taken

place along with the blurring of demarcations between different types of banking

and financial industry activities. Five reasons can be attributed to it:

1. Governments have implemented philosophies and policies based on an increase

in competition in order to maximize efficiency. This has resulted in the creation of

large new financial institutions that operate simultaneously in several financial

sectors such as retail, wholesale, insurance, and asset management.

2. New technology creates an infrastructure allowing a player to carry out a wide

range of banking and financial services, again simultaneously.

3. Banks had to respond to the increased prosperity of their customers and to

customers‘ desire to get the best deal possible. This has encouraged banks to

extend their activities into other areas.

4. Banks had to develop products and extend their services to accommodate the

fact that their customers are now far more mobile. Therefore demarcations are

breaking down.

5. Banks have every motivation to move into new sectors of activity in order to try

to deal with the problem that, if they only offer banking services, they are

condemned forever to provide only a secondary level of utility to customers.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 8/31

8

Role of Technology in Banking

Technology is no longer being used simply as a means for automating processes.

Instead it is being used as a revolutionary means of delivering services to

customers. The adoption of technology has led to the following benefits: greater

productivity, profitability, and efficiency; faster service and customer satisfaction;

convenience and flexibility; 24x7 operations; and space and cost savings. Harrison

Jr., chairman and chief executive officer of Chase Manhattan, which pioneered

many innovative applications of ICT in banking industry, observed that the

Internet caused a technology revolution and it could have greater impact on change

than the industrial revolution.

Technology has been used to offer banking services in the following ways :

1. ATMs are the cash dispensing machines that can be seen at banks and other

locations where crowd proximity is more. ATMs started as a substitute to a

bank to allow its customers to withdraw cash at anytime and to provide services

where it would not be viable to open another physical branch. The ATM is the

most visited delivery channel in retail banking, with more than 40 billion

transactions annually worldwide. In fact, the delivery channel revolution is said

to have begun with the ATM. It was indeed a pleasant change for customers to

be in charge of their transaction, as no longer would they need to depend on an

indifferent bank employee. ATMs have made banks realize that they could

divert the huge branch traffic to the ATM. The benefits hence were

mutual.Once banks realized the convenience of ATMs, new services started to

be added.

2. The phenomenal success of ATMs had made the banking sector develop more

innovative delivery channels to build on cost and service efficiencies. As a

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 9/31

9

consequence, banks have introduced telebanking, call centers, Internet banking,

and mobile banking. Telebanking is a good medium for customers to make

routine queries and also an efficient tool for banks to cut down on their

manpower resources. The call center is another channel that captured the

imagination of banks as well as customers. At these centers, enormous amount

of information is at the fingertips of trained customer service representatives. A

call center meets a bank‘s infrastructural, as well as customer service

requirements. Not only does a call center cut down on costs, it also results in

customer satisfaction. Moreover, it facilitates 24x7 working and offers the

―human touch‖ that customers seek. The call center has large potential

dividends by way of improved customer relationship management (CRM) and

return on investment (ROI).

3. With the Internet boom, banks realized that Internet banking would be a good

way to reach out to customers. Currently, some banks are attempting to harness

the benefits of Internet banking, while others have already made Internet

banking an important and popular paymet system. Internet banking is on the

rise, as is evident from the statistics. Predictions of Internet banking to go the

ATM way have not materialized as much as anticipated; many reasons can be

cited for this. During 2003, the usage of the Internet as a banking channel

accounted for 8.5%. But this was due to the false, unrealistic expectations tied

to it. Some of the factors that were detrimental in bringing down, or rather, not

being supportive, are low Internet penetration, high telecom tariffs, slow

Internet speed and inadequate bandwidth availability, lack of extended

applications, And lack of a trusted environment.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 10/31

10

4. Mobile banking however is being regarded in the industry as ―the delivery

channel of the future‖ for various reasons. First and foremost is the convenience

and portability afforded. It is just like having a bank in the pocket. Other key

reasons include the higher level of security in comparison to the Internet and

relatively low costs involved. The possibility that customers will adopt mobile

banking is high, considering the exponential growth of mobile phone users

worldwide. Mobile banking typically provides services such as the latest

information on account balances, previous transactions, bank account debits and

credits, and credit card balance and payment status. They also provide their

online share trading customers with alerts for pre-market movements and post-

market information and stock price movements based on triggers. Fallout of the

ICT-driven revolution in the banking industry is the Centralized Banking

Solution (CBS). A CBS can be defined as a solution that enables banks to offer

a multitude of customer-centric services on a 24x7 basis from a single location,

supporting retail as well as corporate banking activities, as well as all possible

delivery channels existing and proposed. The centralization thus afforded

makes a ―one-stop‖ shop for financial services a reality. Using CBS, customers

can access their accounts from any branch, anywhere, irrespective of where

they physically opened their accounts.

Information technology has not only helped banks to deliver robust and reliable

services to their customers at a lower cost, but also helped banks make better

decisions. Here a data warehouse plays an extremely important role. It essentially

involves collecting data from several disparate sources to build a central data

warehouse to store and analyze the data. A data warehouse in a bank typically

stores both internal data and data pertaining to its competitors. Data mining

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 11/31

11

techniques can then be applied on a data warehouse for knowledge discovery

(Hwang, Ku, Yen, & Cheng, 2004). Data warehousing also allows banks to

perform time series analysis and online analytical processing (OLAP) to answer

various business questions that would put the banks ahead of their competitors.

Technology Products:

(1). INTERNET BANKING

(2). CREDIT CARD

(3). MOBILE BANKING

(4). ELECTRONIC FUND TRANSFER

(5). ONLINE PAYMENT OF EXCISE AND SERVICE TAX

(6) TELEPHONE BANKING

(7). MICR (magnetic ink character recognition)

(8). BANKNET

(9) INFINET

(10) SWIFT

(11) ELECTRONIC DATA INTERCHANGE

(12) ELECTRONIC CLEARING SERVICES (ECS)

(13) ATM‘S

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 12/31

12

INTERNET BANKING

E-Banking is defined as the automated delivery of new and traditional banking

products and services directly to customers through electronic, interactive

communication channels. E-banking includes the systems that enable financial

institution customers, individuals or businesses, to access accounts, transact

business, or obtain information on financial products and services through a public

or private network, including the Internet.

Customers access e-banking services using an intelligent electronic device, such as

a personal computer (PC), personal digital assistant (PDA), automated teller

machine (ATM), kiosk, or Touch Tone telephone. While the risks and controls are

similar for the various e-banking access channels, this booklet focuses specifically

on Internet- based services due to the Internet‘s widely accessible public network.

Accordingly, this booklet begins with a discussion of the two primary types of

Internet websites: informational and transactional.

CREDIT CARD ONLINE

A credit card is part of a system of payments named after the small plastic card

issued to users of the system. It is a card entitling its holder to buy goods and

services based on the holder's promise to pay for these goods and services. The

issuer of the card grants a line of credit to the consumer (or the user) from which

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 13/31

13

the user can borrow money for payment to a merchant or as a cash advance to the

user.

MOBILE BANKING

The kind of banking and financial service that gives a real-time mobile access to

customer on the move is called mobile banking the services being offered through

mobile phone. Mobile banking to the banking activity that are carried out on

mobile (cell) phones that is banking is enabled even while a person is on the move

In modern times, information exchange takes place at great speed. The

dependence of people on computing devices such as computers, cellular phone,

pager, facsimile machine, e-mail and internet is growing at galloping rate. Such as

growth has made the real time exchange of information a reality. At the same time

it has also thrown challenges to modern enterprises. Which prompt them to act in a

proactive manner so as to stay competitive in the business world? The constant

innovation happening in the realm of electronic banking and financial services has

contributed to a new development called ‗mobile banking‘ this may be attributed to

the forth coming demand from the mobile workforce. The increasingly growing

number of mobile workforce has really given a cutting edge to the progress of the

electronic banking.

The mobile banking refers to the facility allowed by certain banks in India whereby

the mobile phone holder can undertake certain banking transaction through their

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 14/31

14

mobile phones. This value added services has very little human interface and

private banks like ICICI, HDFC etc. have started offering this service. The

customer is required to type a text message on the mobile phone which travel

through the server of the cell phone service provider to bank‘s internet service;

information is retrieved and routed back the same way in 15-30 second. To avail

the service, the client has to fill up form at any of bank‘s branches and bank

informs the cellular service provider to activate the module instantly.

The information which includes checking of account balance, request for a Cheque

book, stop payment instruction, changing primary operation account, request for

current periods‘ account statement to the mailed and access summaries of last three

transactions performed on the account.

The number of people using mobile banking services has increased. While the

trend is growing, lack of awareness of services, apart from perceived security

issues are inhibiting faster takeoff. ―-Dataquest.

It was clear at the start itself that this would be a battle focused not on technology,

but on the mindset of the target audience. Over two years after the launch of

mobile banking services in the country, that bridge has been reached and many are

beginning to walk those cautious steps across it. Yes, the usage of mobile banking

services is increasing, and fast against Dataquest‘s estimated user base of under

10,000 for mobile banking services in 2000, there are over 120,000 today who

SMS from their banking. Even our survey despite targeting a respondent profile

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 15/31

15

that would bring in more positive answers than negative (see methodology), threw

up very low usage numbers.

Also, e-commerce as a medium of purchasing and transacting has not really caught

on, and the basket of mobile banking offerings is, in itself, very limited. The good

news the technology backbone is in place, and getting better. There‘s CDMA,

there‘s GSM. Forget their battles on the mobile telephony front from the

consumer‘s point of view; he never had it so good.

The recent price cuts are also likely to help, ―say banking experts, adding that this

will lead to ―increasing willingness to move on to mobile, and therefore, to the

value-added services that most operators offer today‖

The Internet is revolutionizing the way the financial industry conducts business,empowering organization with new business model and new ways to interact with

customers. The ability to perform banking transactions online banks and brokers

who offer personalized services through their web portals.

This increased competition is driving traditional financial institutions to find new

ways to add value to their product and services, gain competitive advantage and

increase customer loyalty while also attracting new, high-value client.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 16/31

16

ELECTRONIC FUND TRANSFER

Electronic funds transfer or EFT is the electronic exchange or transfer of money

from one account to another, either within a single financial institution or across

multiple institutions, through computer-based systems.

The term is used for a number of different concepts:

1. Cardholder-initiated transactions, where a cardholder makes use of a payment

card

2. Direct deposit payroll payments for a business to its employees, possibly via

a payroll service bureau

3. Direct debit payments, sometimes called electronic checks, for which a business

debits the consumer's bank accounts for payment for goods or services

4. Electronic bill payment in online banking, which may be delivered by EFT or

paper check

5. Transactions involving stored value of electronic money, possibly in a private

currency

6. Wire transfer via an international banking network (generally carries a higher

fee)

7. Electronic Benefit Transfer

In 1978 U.S. Congress passed the Electronic Funds Transfer Act to establish the

rights and liabilities of consumers as well as the responsibilities of all participants

in EFT activities in the United States.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 17/31

17

ONLINE PAYMENT OF EXCISE AND SERVICE TAX

For taxpayers who opt to maintain account with the concerned bank and willing to

use Internet banking facility:

1. Taxpayer logs on to the bank‘s web site.

2. The bank‘s site allows the taxpayer to enter into the secure banking area

after verifying the user ID and password provided to the taxpayer by the

bank;

3. Once in the secure banking area of the bank, the tax payer can select the

―Pay Tax‖ menu which will further offer option to select various taxes he

can pay on-line;

4. Once opted for CBEC (Indirect Tax), the taxpayer is guided to the challan

form for filling up the details;

5. There will be an on-line validation for Assessee Code, Location Code,

Account Head against the masters provided to the bank from the concerned

Pay and Accounts Office. The validation is mandatory and only successful

entrants will be allowed to proceed further;

6. Banks will obtain and keep only such Assessee Codes, in their master, which

belongs to the Assessee who falls under the Commission rates for which the

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 18/31

18

bank is authorized to collect Indirect Tax revenue. This will ensure that the

bank is not collecting and accounting indirect tax revenue for a

Commissioner ate for which it is not authorized;

7. On successful validation of the details in the challan format, the taxpayer is

guided to a ‗make payment screen‘ showing the payment details filled in by

the taxpayer on the challan format;

8. The taxpayer gets an option to ―Continue‖ or ―Cancel‖;

9. On selecting ―Cancel‖, the taxpayer is prompt for entering his user ID and

password to enter into the bank‘s e-transaction module;

10. On selecting ―continue‖, the taxpayer is prompt for entering his user ID and

password to enter into the bank‘s transaction module;

11. This screen further leads the taxpayer to the page describing his account

details with the bank;

12. Taxpayer selects the account to be debited;

13. Authorize the payment transaction;

14. On successful payment transaction, the account of the taxpayer gets debited

and taxpayer gets a unique system generated payment confirmation number;

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 19/31

19

15. The concerned Focal Point Bank prints the challan and include in the scroll

on a day to day basis and forward to the concerned PAO and, to the Range

Officer as per the existing procedure and ensures two copies of the challan in

delivered to the taxpayer;

16. Fund transaction and settlement with Government will be the exclusive

responsibility of the bank as per the existing procedure.

TELEPHONE BANKING

Telephone banking is a service provided by a financial institution, which allows its

customers to perform transactions over the telephone. Most telephone banking

services use an automated phone answering system with phone keypad response or

voice recognition capability.

To guarantee security, the customer must first authenticate through a numeric orverbal password or through security questions asked by a live representative (see

below).

With the obvious exception of cash withdrawals and deposits, it offers virtually all

the features of an automated teller machine: account balance information and list

of latest transactions, electronic bill payments, funds transfers between a

customer's accounts, etc.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 20/31

20

Usually, customers can also speak to a live representative located in a call centre or

a branch, although this feature is not always guaranteed to be offered 24/7. In

addition to the self-service transactions listed earlier, telephone banking

representatives are usually trained to do what was traditionally available only at the

branch: loan applications, investment purchases and redemptions, Cheque book

orders, debit card placements, change of address, etc.

Banks which operate mostly or exclusively by telephone are known as phone

banks. They also help modernize the user by using special technology.

MICR (magnetic ink character recognition)

1. Magnetic Ink Character Recognition

2. Introduced in 1987 in the four metros

3. 1,047 Clearing Houses; 42 with MICR

4. SB/CA Cheque leaves standardized size (8 X 3 2/3‖) are pre-printed with the

bank-branch code and account type in MICR strip, while the amount is read

manually and fed into the system using the encoders for funds settlements

5. Speeds up clearing work

6. BC/DW/TC/DD/PO/GC/IW/RW/SI...

BANKNET

1. Set up in 1991 by RBI

2. Meant to facilitate transfer of inter-bank/ inter-branch messages within India

by Public Sector banks who are members of this network

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 21/31

21

3. Wide connectivity - Major Centers like Mumbai, Delhi, Calcutta, Madras,

Nagpur, Bangalore, Hyderabad, Pune, Ahmedabad, Kanpur, Lucknow,

Chandigarh, Kochi, Jaipur, Bhopal, Patna, Bhubaneswar,

Thiruvananthapuram, Guwahati, Panaji, Jammu, etc

INFINET

1. Indian Financial network

2. Set up by RBI in June 1999

3. Satellite based WAN using VSAT ( Very small Aperture Terminal ) technology

4. The hub and network Management System of INFINET are located in the

institute for development and research in banking Technology.

SWIFT

1. Society for worldwide Inter- bank financial institutions

2. HQ La Hulpe, Brussels, Belgium

3. Provides reliable, fast telecommunication facilities for exchange of financial

messages all over the world between banks and FIs

4. As non-profit making co-operative society in 1973 by 239 banks in 15

countries

5. Hubs in Brussels, New York and Netherlands

6. Rules in 1975; first message in 1977

7. >7,000 members in 200 countries now

8. Handles over 7 million messages every day

9. India – a member since 1991

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 22/31

22

10. 88 Indian banks are members as on date

11. Any Bank / FI can become a member

12. Allots an address called Bank Identi-fication Code (BIC) of 8 characters

13. Enables members to send secure and reliable messages – authenticated...

14. Correspondent bank arrangements...

15. Advantages: 24 hours service, system based – fraud-free – faster – accurate

– confidential – funds/LCs/Guara

ELECTRONIC DATA INTERCHANGE

1. Facilitates transfer of banking transactions using agreed protocol and standard

data structure b/w computers

2. Norms developed in respect of specific messages for transmission of business

transactions which are electronic equivalents of commercial invoices, purchase

orders, transport bookings, payment instructions etc

3. Appropriate message formats and standards for financial applications in EDI

developed by Message Development Group-Finance (constituted by IBA)

ELECTRONIC CLEARING SERVICE

1. Electronic Clearing Scheme (ECS) operated by the RBI since 1996-97

2. Utilizes BANKNET and INFINET

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 23/31

23

3. Facilitates payment from a single account at a bank branch to any number

of accounts maintained with the branches of the same or other banks – Eg.,

Payment of dividends

4. RBI has also launched ECS – Debit for payment to utility companies like

Telephones, Electricity etc

AUTOMATED TELLER MACHINES

1. ATMs or 24 hour Tellers – Electronic Terminals - allow to bank at any

time...

2. On-site (near branch) and Off-site ATM

3. ATMs facilitate withdrawal/deposit....

4. Customer provided with a PIN / Card

5. Introduced in India by Foreign Banks

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 24/31

24

POSITIVE AND NEGATIVE EFFECTS OF TECHNOLOGY

IN BANKING, SOLUTIONS

Positive Effects of Technology

Competition — Studies show that competitive pressure is the chief driving force

behind increasing use of Internet banking technology, ranking ahead of cost

reduction and revenue enhancement, in second and third place respectively. Banks

see Internet banking as a way to keep existing customers and attract new ones to

the bank.

Cost Efficiencies — National banks can deliver banking services on the

Internet at transaction costs far lower than traditional brick-and-mortar branches.

The actual costs to execute a transaction will vary depending on the delivery

channel used. For example, according to Booz, Allen & Hamilton, as of mid- 1999,

the cost to deliver manual transactions at a branch was typically more than a dollar,

ATM and call center transactions cost about 25 cents, and Internet transactions cost

about a penny. These costs are expected to continue to decline.

National banks have significant reasons to develop the technologies that will help

them deliver banking products and services by the most cost-effective channels.

Many bankers believe that shifting only a small portion of the estimated 19-billion

payments mailed annually in the U.S. to electronic delivery channels could save

banks and other businesses substantial sums of money. However, national banks

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 25/31

25

should use care in making product decisions. Management should include in their

decision making the development and ongoing costs associated with a new product

or service, including the technology, marketing, maintenance, and customer

support functions. This will help management exercise due diligence, make more

informed decisions, and measure the success of their business venture.

Geographical Reach — Internet banking allows expanded customer contact

through increased geographical reach and lower cost delivery channels. In fact

some banks are doing business exclusively via the Internet — they do not have

traditional banking offices and only reach their customers online. Other financial

institutions are using the Internet as an alternative delivery channel to reach

existing customers and attract new customers.

Branding — Relationship building is a strategic priority for many national banks.

Internet banking technology and products can provide a means for national banks

to develop and maintain an ongoing relationship with their customers by offering

easy access to a broad array of products and services. Internet Banking 4

Comptroller‘s Handbook By capitalizing on brand identification and by providing

a broad array of financial services, banks hope to build customer loyalty, cross-sell,

and enhance repeat business.

Customer Demographics — Internet banking allows national banks to offer a

wide array of options to their banking customers. Some customers will rely on

traditional branches to conduct their banking business. For many, this is the most

comfortable way for them to transact their banking business. Those customers

place a premium on person-to-person contact. Other customers are early adopters

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 26/31

26

of new technologies that arrive in the marketplace. These customers were the first

to obtain PCs and the first to employ them in conducting their banking business.

The demographics of banking customers will continue to change. The challenge to

national banks is to understand their customer base and find the right mix of

delivery channels to deliver products and services profitably to their various

market segments.

Benefits to customer

1.

More convenience & flexi timings2. Better awareness of products & services

3. Up-to-date information on accounts

4. Low cost of accessing the accounts

Negative Effects of Technology

While ICT provides so many advantages to the banking industry, it also poses

security challenges to banks and their customers. Even though Internet banking

provides ease and convenience, it is most vulnerable to hackers and cyber

criminals. Online fraud is still big business around the world.

Even though surveillance cameras, guards, alarms, security screens, dye packs, and

law enforcement efforts have reduced the chances of criminal stealing cash from a

bank branch, criminals can still penetrate the formidable edifice like the banking

industry through other means. Using Internet banking and high tech credit card

fraud, it is now possible to steal large amounts of money anonymously from

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 27/31

27

financial institutions from the comfort of your own home, and it is happening all

over the world.

Further, identity theft, also known as phishing, is one of the fastest growing

epidemics in electronic fraud in the world. Identity theft occurs when ―fraudsters‖

gain access to personal details of unsuspecting victims through various electronic

and non-electronic means.

This information is then used to open accounts (usually credit card), or initialize

loans and mobile phone accounts or anything else involving a line of credit.

Account theft, which is commonly mistaken for identity theft, occurs when

existing credit or debit cards or financial records are used to steal from existing

accounts. Although account theft is a more common occurrence than identity theft,

financial losses caused by identity theft are on average greater and usually require

a longer period of time to resolve.

Spam scams involve fraudsters sending spam e-mails informing customers of some

seemingly legitimate reason to login to their accounts. A link is provided in the e-

mail to take the user to a login screen at their bank site; however the link that is

provided actually takes the user to a ghost site, where the fraudster can record the

login details. This information is then used to pay bills and or transfer balances for

the fraudster‘s financial reward.

Card skimming refers to the use of portable swiping devices to obtain credit card

and EFT card data. This data is rewritten to a dummy card, which is then usually

taken on elaborate shopping sprees. As the fraudster can sign the back of the card

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 28/31

28

himself or herself, the merchant will usually be unaware that they have fallen

victim to the fraud. One can curb these hi-tech frauds by using equally hi-tech

security mechanisms such as biometrics and smart cards.

The key focus in minimizing credit card and electronic fraud is to enable the actua

er of the account to be correctly identified. The notion of allowing a card to prove

your identity is fast becoming antiquated and unreliable. With this in mind, using

biometrics to develop a more accurate identification process could greatly reduce

fraud and increase convenience by allowing consumers to move closer to a ―no

wallet‖ society.

Many industry analysts such as the American Bankers Association are proposing

that the smart payment cards are finally poised to change the future of electronic

payments. The smart card combines a secure portable payment platform with a

selection of payment, financial, and nonfinancial applications.

The reach of the smart card potentially goes beyond the debit and credit card

model. Instead of a smart card, ISO uses the term ‗integrated circuit card‘ (ICC),

which includes all devices where an integrated circuit is contained within the card.

The benefits provided by smart cards to consumers include: convenience (easy

access to services with multiple loading points), flexibility (high/low value

payments with faster transaction times), and increased security. The benefits

offered to merchants include: immediate guaranteed cash flow, lower processing

costs, and operational convenience.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 29/31

29

CONCLUSION

This report describes in a nutshell the evolution of banking and defines banking

technology as a Consortium of several disciplines, namely finance subsuming risk

management, information and communication technology, computer science, and

marketing science. It also highlights the quintessential role played by these

disciplines in helping banks:

(1) Run their day-to-day operations in offering efficient, reliable, and secure

services to customers;

(2) Meet their business objectives of attracting more customers and thereby

making huge profits; and

(3) Protect themselves from several kinds of risks. The role played by smart cards,

storage area networks, data warehousing, customer relationship management,

cryptography, statistics, and artificial intelligence in modern banking is very well

brought out.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 30/31

30

The report also highlights the important role played by data mining algorithms in

helping banks achieve their marketing objectives, fraud detection, anti-money

laundering, and so forth.

In summary, it is quite clear that banking technology has emerged as a separate

discipline in its own right. As regards future directions, the proliferating research

in all fields of Technology and computer science can make steady inroads into

banking technology because any new research idea in these disciplines can

potentially have a great impact on banking technology.

8/3/2019 Technology and Banking Final Project Done Done

http://slidepdf.com/reader/full/technology-and-banking-final-project-done-done 31/31

31

BIBLIOGRAPHY

www.google.com

www.wikipedia.com