table of contents - texas tech...

TRANSCRIPT

1

Table of Contents Executive Summary .............................................................................2

Accounting Analysis.......................................................................... 4 Ratio Analysis Forecast Financials...................................................... 5 Analysis Evaluations ......................................................................... 6

Overview of ADM and the Industry .....................................................8 Five Forces Model ............................................................................ 9 Rivalry Among Existing Firms ............................................................ 10 Threat of New Entrants .................................................................... 14 Threat of Substitute Products............................................................ 15 Bargaining Power of Buyers .............................................................. 17 Bargaining Power of Suppliers........................................................... 18 Characterization of Industry.............................................................. 18 Key Success Factors ......................................................................... 19 Competitive Advantage Analysis ........................................................ 22

Accounting Analysis.............................................................................26 Key Accounting Policies .................................................................... 26 ADM Pension Benefits....................................................................... 28 Accounting Flexibility........................................................................ 30 Evaluating Accounting Strategy ......................................................... 32 Quality of Disclosure ........................................................................ 33 Core Expense Manipulation Diagnostics.............................................. 39 Sales of Manipulation Diagnostics ...................................................... 39 Potential “Red Flags”........................................................................ 43 Fixing Accounting Distortions ............................................................ 44

Ratio Analysis Forecast Financials .......................................................45 Ratio Analysis .................................................................................. 45 Profitability Analysis ......................................................................... 54 Capital Structure Analysis ................................................................. 62 Extended Ratio Analysis.................................................................... 66 SGR and IGR Analysis....................................................................... 76 Forecasting...................................................................................... 77

Analysis of Valuations..........................................................................80 Valuation Models.............................................................................. 80 Methods of Comparables .................................................................. 81 Cost of Capital ................................................................................. 86 Intrinsic Valuation Models ................................................................. 88 Altman Z-Score ................................................................................ 95

Appendix..............................................................................................97 Works Cited………………………………………………………………………...114

2

Executive Summary Archer Daniels Midland Investment Recommendation: Over-valued, Sell 11/1/2006

ADM- NYSE $36.61 EPS Forecast 52 Week Range $23.37 - $46.71 2006(A) 2007E 2008E 2009E Revenue (2006) $37.4 Bil. EPS $2.32 $1.56 $1.69 $1.84 Market Capitalization $22.89 Bil. Shares Outstanding 657,250,000 Method of Comparables ADM Industry Trailing P/E 15.25 15.14 Dividend Yield 1.10% Forward P/E 18.30 24.77 3-month Avg Daily Trading Volume 5,365,840 PEG 91.76 73.07

Percent Institutional Ownership 68% P/B 1.13 1.11 P/S 0.66 1.14

Enterprise value to EBITDA 11.94 19.82 Enterprise value to Recurring NOPAT 19.38 15.74

Book Value Per Share (mrq) $15.656 Valuation Estimates ROE 13.38% ROA 6.17% Actual Current Price $36.61 Estimated 5-yr EPS Growth Rate Ratio Based Valuations Cost of Capital Est. R^2 Beta Ke P/E Trailing $24.30 Ke Estimated 9.53% P/E Forward $49.57 10-year .1777 .8846 9.53% PEG Forward $29.15

7-year .1771 .8830 10.22%

P/B $35.84 P/S $63.75 Enterprise value to EBITDA $69.49 Enterprise value to Recurring NOPAT $36.98

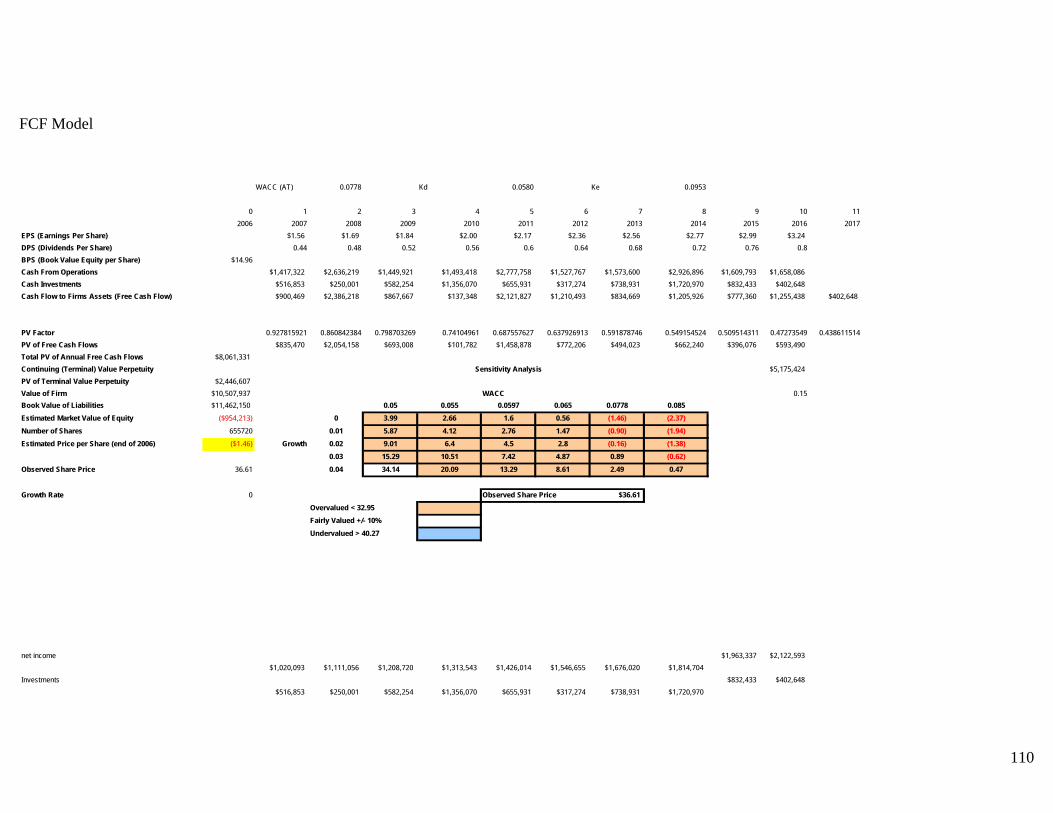

5-year .1746 .8754 9.28% 1-year .1728 .8732 9.53% Published .97 Intrinsic Based Valuations Discounted Dividends $7.25 Kd 5.8% Free Cash Flows ($1.46) WACC 7.78% Residual Income $14.71 Abnormal Earnings Growth $17.04 Altman Z-score 3.853 Long-Run Residual Income Perpetuity $26.46

3

Archer Daniels Midland Company is one of the largest agricultural processors in

the world. They take crops and process them to make food ingredients and

renewable fuels. ADM has manufacturing facilities all over world, and has its

headquarters located in Decatur, Illinois. It was founded in 1902, and is one of

the oldest agricultural processors around. ADM’s competitors include Bunge

Limited, Cargill Incorporated, and ConAgra Foods Inc. The threat of new

competitors is low in this industry due to several factors including large capital

investments and the fact that there are few sellers and buyer, so the entrant of a

new firm would over populate the supply. Being that this industry is an oligopoly

in nature, this business leaves a relatively low amount of competitors but a high

amount of competition.

There are a few of ADM’s product that could be under the threat of substitution.

One of those products is the high fructose corn syrup, which has been

discovered to be a leading cause in the American battle with obesity, which

results in Type II diabetes. Because of its negative affects on the human body,

the use of high fructose corn syrup could decrease while the use of sugar could

increase. The other product under threat of substitution is corn-ethanol. There

is shortage a corn, resulting in researchers looking for alternative ways to

produce ethanol.

Customers in the commodity industry have the bargaining power because they

are the ones that are able to shop around and find who they would like to

purchase from. ADM has managed to be a cost leader due to its vertical

integration system they have set up. Cost leadership is crucial and is valued as a

long term advantage in maintaining customer loyalty and repeat customers.

Companies in this industry have no real potential for pure growth, so it is

important for them to have a strong customer base, which is a key success

4

factor for this industry. Another factor is being able to maintain economies of

scope, which ADM is able to do by making such large orders and keeping the

cost per unit down. It is also key for ADM to understand all the sectors of it

company to maintain specialization as a competitive advantage. This falls under

the key success factors of economies of scale and delegation of managerial

responsibilities.

Accounting Analysis

When evaluating ADM’s key accounting policies, it was important to take into

account its key success factors. ADM had several major accounting factors that

were included in its 10-K. In a commodity industry, it is important for ADM to

have derivatives and futures to set off the risk due to unpredictable weather,

planting, changes in global demand, and many other risks. Some other key

accounting policies include ADM’s employee benefit plans and pension plans,

which are good tools to give its employees motivation to do a good quality job.

Because ADM is capital intensive and has many assets that contribute to its

production, a major accounting policy for ADM to focus on is its asset write-

downs and asset abandonment.

ADM is believed to follow conservative accounting policies while preparing its

financial statements in conformity with generally accepted accounting principles

(GAAP). The quality of a firm’s disclosure on its financial statements helps an

analyst understand the business and gives a sense of transparency. ADM’s 10-K

however, did a poor job of separating the company base, though much of the

specific information is disclosed regarding the industry. Sector information is

available, but no information is disclosed about specific assets or location of

operations. Overall, ADM did not nothing special to its 10-K to make it as a

guide for investors.

5

By running ADM’s sales and expense ratios, we were able to evaluate any

potential “red flags” found in its 10-K. There was only one ratio that showed

some strange results, which was the expense diagnostic of cash flow from

operations over operating income in year 2004. After some research into ADM’s

10-K we noticed that ADM had an unusually large write off that year which

depressed its cash flow from operations. Therefore, ADM had no unusual

accounting distortions.

Ratio Analysis and Forecast Financials

By analyzing ADM’s ratios that examined its liquidity and operating efficiency,

profitability, and capital structure we were able to get a better understanding of

where it stands within the agricultural processing industry, compared to

competitors. By evaluating ADM’s liquidity and operating efficiency ratios, they

showed that ADM appeared to be growing more liquid overtime, while

experiencing a decrease in its operating efficiency. The fact that ADM is losing

operating efficiency is a sign that they may lose a competitive advantage in the

foreseeable future. As for the profitability ratios, they all improve in ADM’s favor

almost every year. This illustrates management’s ability to focus and maintain

constantly increasing levels of profitability each year. When evaluating ADM’s

capital structure, we were concerned by the debt service margin, which went

through some significant changes due to volatile fluctuations in cash flows from

operations.

There are extended ratios that help get an even better understanding of how

ADM is doing and what its future may hold, which include recurring NOPAT

margin, EBITDA margin, net long-term asset turnover, PP&E turnover, operating

cash flow ratio, and dividend payout ratio. All of the ratios seemed to be in favor

of ADM, except the recurring NOPAT margin, EBITDA margin, and the operating

cash flow ratio. The recurring NOPAT margin seems be low due to the hedging

6

contracts that ADM has and the volatility of commodity prices. It has been

experiencing exceptional gains, but still leaves doubt if they can maintain them.

The decline of ADM’s EBITDA margin is believed to be a direct result of the

slowing economy, but also shows that management was ineffective in combating

the slowing growth despite its dominate market position. The last ratio that

concerned us was the operating cash flow ratio which was way too erratic for a

company of this maturity. The erratic ness was due to both the operating cash

flows and the current maturities of long term debt, which is hoped to not

manifest into the future. Overall, the future of ADM seems promising with a few

issues that it should work to improve.

Analysis Evaluations

Determining whether the stock price of ADM is undervalued, fairly valued, or

overvalued can be done through several methods. Not all the methods we used

to evaluate ADM are equally reliable, so we had to go through the methods and

decide whether they were accurate or not. One of the methods that we believed

was accurate for ADM was the price to book ratio. This method gave us a stock

price of $35.84, compared with the observed stock price of $36.61, to result in a

fairly valued evaluation. Another method that we believed to be fairly accurate

was the enterprise value to recurring NOPAT margin. The estimated price of

$36.98 is the closest to the observed share price of $36.61 out of any model that

we have used due to the fact that it more accurately reflect companies that are

heavily based in fixed assets, such as ADM. Even though these methods were

believed to be the most accurate out of the method of comparables ratios, we

still do not rely on them because ADM is considered to be an overvalued

company, not fairly valued as stated in the outcome of these two ratios.

For the rest of our intrinsic value models, it was necessary for us to find the cost

of equity, cost of debt, and the weighted average cost of capital. We then

7

carried on to the Discounted Dividend Model, Free Cash Flows Model, Residual

Income Model, Abnormal Earnings Growth Model, and the Long Run Residual

Income Perpetuity Model. Again, not all of these models were believed to be

accurate. We found the Long-run Residual Income Perpetuity to be our most

accurate model, with the Residual income and Abnormal Earnings Growth Models

close behind, which all resulted in overvalued estimations. Overall, we believe

that ADM should be valued lower than the observed market price of $36.61 with

a sell opportunity due to this prevalent theme across most of our intrinsic

valuation models.

8

Overview of ADM and the Industry

Archer Daniels Midland Company is one of the largest agricultural processors in

the world. It serves as one of the most important links between farmers and

consumers. ADM takes inputs and processes them to make food ingredients,

renewable fuels, and naturally derived alternatives to industrial chemicals.

Archer Daniels Midland was founded in 1902 and incorporated in 1923. ADM’s

headquarters are in Decatur, Illinois and they operate processing and

manufacturing facilities across the United States and worldwide. ADM’s

competitors include Bunge Limited, Cargill Incorporated, and ConAgra Foods Inc.

(ADMworld.com).

0

10

20

30

40

2001 2002 2003 2004 2005 2006

ADM's Total Sales (in billions)

Sales

ADM is an S&P 500 company, which gives them a valued weighted index where

they make up 2.8 % of the total S&P 500 according to share price. ADM’s sales

volume has continued to increase in the past five years ending in 2001 with 19.5

billion dollars and currently at 36.4 billion dollars. Sales grew from 2001 to 2004,

excessively from 19 billion to 36 billion then in 2005 going down to 35 billion, yet

pulling it up to its current sales of 36 billion. This gives ADM an annual growth

percentage of about 28%. Not only are they a continuously growing company,

they are the current leader in the market against its direct competitors, Bunge

Ltd., Cargill Incorporated (privately held), and ConAgra Foods Inc. With a 25

9

billion dollar market capitalization, ADM is 13 billion dollars larger than ConAgra

Foods Inc., its closest competitor. For the overall food industry, ADM is ranked

fourth of the top eight, trailing behind Unilever NV, who leads the industry, by 44

billion dollars. This puts ADM as a strong leader in the market. ADM does trail by

44 billion dollars to Unilever NV; however, ADM’s stock price is over 14 dollars

higher and they have 2 million more shares in volume. ADM asset value has

gone from 14.3 billion in 2001 to 21.3 billion in 3rd quarter of 2006. Since ADM is

growing and leading the industry, it is investing more, expanding, and increasing

its inventory. The company’s ability to lead the industry has increased its stock

from roughly 12 dollars in April of 2001 to its current closing price of 38 dollars,

with only one split of 105/100 in August 2001(MorningStar.com). ADM is a

diverse company that produces a variety of food ingredients including corn syrup,

specialty flowers, cocoa, and sweeteners. ADM also produces products such as

ethanol, fertilizer, and common household products. Because ADM has such a

wide variety of products they compete in numerous markets, including consumer

food industry, farm product industry, and bio-diesel industry (ADMworld.com).

Five Forces Model

Rivalry among

existing firms

Threat of New

Entrants

Threat of

Substitute

Products

Bargaining

Power of

Buyers

Bargaining

Power of

Suppliers

High Low Average Low Low

The Five Forces Model shows us in great detail the opportunities that face firms,

in a particular industry. In an attempt to analyze the profitability of industry,

there are several important areas to consider. Breaking down the analysis of an

industry into five forces allows specific attention to be given to any area in which

abnormal profits are able to be made. The degree of competition among

existing firms determines the strength of any particular company in relation to its

10

competitors. The availability of new entrants into an industry shows potential for

profit maximization or the converse, long term losses. Substitution of a

company’s product is always a concern that needs to be analyzed in order to

determine future profitability of a company. A company’s ability to negotiate

prices and terms with suppliers, as well as customers, is essential to the long

term success of a business. Analysts need to be aware of the threats and

opportunities that face any company in regards to its industry.

Rivalry Among Existing Firms

Company Market Share (In Billions)

ADM 22.89

BG 8.38

CAG Privately Held

Industry 19.30

Industry Growth

Potential growth is an important aspect to consider within an industry. The

ability of a company to take advantage of growth opportunities can broaden

market share and boost earnings. In the commodity processing industry,

chances for growth are few but strong. Rising demand for an ever expanding

global marketplace, as well as overpopulated countries give rise to levels of

demand scarce seen in history. Furthermore, the diversity of such commodities,

such as corn, is being pushed to the limits with developments in corn ethanol,

bio-diesel, and even plastics. The chances for growth within the industry are as

limitless as a company’s imagination when considering all of the innovation and

emerging markets for agricultural processors. The few companies that are in the

commodities industry make this industry a high concentrated market because the

11

potential for growth within the industry is rising especially with ethanol

production.

Concentration

Agricultural processing is an oligopoly industry in which ADM is the largest public

corporation. ADM’s other main competitors include Bunge Ltd. and Cargill

Incorporated. Although ADM is the largest publicly traded company in the

American agricultural sector, the second largest privately held company in the

United States, Cargill Incorporated, sits at the top. Even though Cargill’s revenue

almost doubles ADM’s revenue, ADM by far has the largest market cap among

the publicly traded firms. There are several other food manufacturing firms such

as ConAgra Foods Inc., Kraft Foods Inc., and Unilever that contribute only small

portions of their firms to agricultural processing (finance.yahoo.com). These

firms compose the majority of the rest of the industry. In conclusion, ADM is

one of the largest companies in a highly concentrated industry.

Differentiation and Switching Costs

Differentiation is a helpful strategy for a company to use in order to remain

ahead of the competition that can increase profits. Differentiation includes

offering products and services that the competition does not. Since the

agricultural processing industry is highly dependent on commodity goods,

differentiation is extremely low. Even when considering industrial outputs, the

end product is still in natural a commodity. Because of this, ADM and its

competitors focus on controlling and lowering price levels. In addition to having

commodity goods as raw materials, the industry also produces commodity goods.

Knowing that it is common that ADM’s products are easily substituted by

competitor’s products, ADM has low switching costs in regards to its customers.

Even though ADM spends time innovating within the industry, special attention

12

must be given to the readiness of its customers to switch to a different company

for their supplies. Given the commodity nature of both the inputs and outputs

for agriculturally processing firms, switching costs remain high and need to be

given special attention or else customer base will be lost. In conclusion, with

these factors in mind ADM is positioning itself to set the pace for its competitors

being a high concentrated market.

Fixed-Variable Costs

To become a price leader in the industry, one must reduce the variable cost as

much as possible, and ADM puts a great deal of effort into finding ways to keep

variable costs low. Therefore, the high fixed to variable cost ratio in this market

forces firms to sell high quantities of products at lower costs to turn higher

profits. Processing plants, joint elevators, elevators, and warehouses make up

the bulk of ADM’s fixed cost. Alone, fixed costs for the company are high, but

massive production provides for a low fixed cost per unit. Also, the massive

production and processing per plant makes for a low variable cost per unit.

ADM’s competitors in this field take full advantage of their size and ability to

produce in bulk helping make most players in this industry focus on low costs to

maintain profits.

Excess Capacity

Excess capacity is the result of high inventories, which can burden a company

with unnecessary costs (Palepu 2-3). Excess capacity is not a major concern to

ADM. In the agricultural processing industry, creating enough demand is not a

problem. The ingredients produced by ADM and its competitors are so widely

used, demand is higher than what the industry is capable to produce. This is in

part due to the fact that the industry relies heavily on crop production and the

farmers’ ability to grow enough to keep up with demand. Excess capacity rarely

13

is an issue for companies in this field, but if such an occasion does arise, a

system of checks and balances are in place to prevent it from adversely affecting

the company. Storage, such as grain silos, and the ability to open up to new

markets oversees helps to quickly diminish any excess the company might

experience. If or when there is excess capacity in the industry, smaller firms

suffer and die out, not the major firms like ADM. Since ADM has a high degree

of bargaining power with customers, excess capacity does not hinder company’s

ability to sell its products due to a variety of distribution options.

Exit Barriers

Exit barriers can keep a suffering firm in an industry because it is more

expensive to leave. Exit barriers leave the option of “bad eggs” to be chosen in

an area where they are suffering. In the agricultural processing industry, exit

barriers are relatively low for smaller firms but increasingly become higher the

larger the firm. Smaller or dying firms are easily taken over by larger firms in

the industry. Furthermore, less is invested in the fixed assets of a smaller

company, making it easier for a company to sell off everything and leave that

particular field. Larger firms can expand by taking over or buying out firms

wanting out of the industry. Contracts, relationships with farmers, and other

partnerships built over several decades by large companies, such as ADM, make

exit barriers higher for those firms. Legal contracts that exist go years into the

future, which ADM has to satisfy whether or not it is still in that field. It is

difficult for other companies to take the market share over when a large

company attempts to exit the industry, because of the relationships and

company identification established by the larger companies. Overall, exit barriers

are relatively high, but for the few exceptions of the smaller firms, adding to the

degree of commitment needed for any serious competitor.

14

Threat of New Entrants

A new business entering into the agricultural industry is not very likely. Since

Archer Daniels Midland has been in the agricultural business since 1902, it has a

first mover advantage. This first mover advantage is easily illustrated by the

expansion of ADM into other countries, or perhaps into fields still in

development, such as ethanol. ADM is vertically integrated with 240 processing

plants, and is now a global company. The degree of vertical integration varies

from ADM’s own transportation services, to bring in its raw materials, to the

plants that actually refine the final products, and trucks to ship those goods out.

ADM was the innovator of two different types of technologies, the separation

technology and fermentation. Separation technology involves rendering raw

materials, such as corn, into a variety of different products, for food and

industrial uses. An example of fermentation is turning corn into ethanol, lactic

acids, or other products. Also, ADM pioneered the development of textured soy

protein.

The agricultural business industry has developed into an oligonomy, meaning

there are few sellers and buyers. These few players dominate the industry and

collectively change the rules. The industry’s largest producers settled to fix

prices and fix market share. Because of this, a company trying to enter the

lysine industry would lead to an overproduction of lysine, and this would yield

below normal profits. New entrants would be driven out quickly. The large

companies are constantly looking for disruptive new companies, attempting to

enter the industry. Because entering the industry is very difficult, innovators

tend to have two choices; get bought out by a larger company, or get destroyed

by the rival companies that steal the innovative ideas. Many new and smaller

businesses try to establish a new idea, knowing that large companies have a

difficult time doing this, and then will simply cash out of the industry. Other

15

companies use what is called the boutique approach and never get big enough

to attract the large companies’ attention.

A large capital investment also tends to be a problem for potential entrants into

the industry. For example, entry into the corn syrup industry is difficult because

the construction of a corn wet milling facility generally takes more than two

years to complete. These two years, or more, is from the time the site is

selected to the production of commercial quantities. For a company to build a

plant at the same level as ADM, it would have to invest more than $150 million.

An amount of money most businesses do not have. There are also high technical

and knowledge barriers. Research and development barriers become a sunk cost

for new entrants, since technology is not freely available.

Finally, there are numerous regulations in the agriculture industry. For a

company that is wishing to produce ethanol, it must abide by the Renewable

Fuels Association’s regulations. This association promotes policies, regulations,

and research and development initiatives that will lead to an increase in ethanol

production. To receive the permits and regulatory requirements, a company

could wait up to a year to be processed. There are also tight environment

regulations. To stay in compliance with the environment regulations, a company

has to have the most recent technology that is the most environmentally safe,

which tends to be the most expensive. (ADMworld.com)

Threat of Substitute Products

Substitute Products are products and services that are interchangeable

depending on factors such as the state of the economy, income level, and wants

and needs of the consumers. Substitute products have the potential to

undermine a company’s profitability and overall growth potential. (Palepu 2-4)

High fructose corn syrup is used as a sweetener for items such as jellies, baked

16

goods, canned food, dairy products, and beverages including soft drinks. The

reason for using a high fructose corn syrup in these items is because it is

cheaper than sugar, due to the impact of sugar tariffs. The corn syrup has a

long shelf life, and a liquid is easier to transport and blend into the product. Due

to the make up of high fructose corn syrup, honey would be a good substitute

because it is another product that is a mixture of different types of sugars, small

amount of compounds, and water. High fructose corn syrup and honey have a

similar fructose and glucose ratio.

With high fructose corn syrup consumption on the rise in America for the past 30

years, scientists and nutritionists have been studying the effects of it to the

human body. It has been discovered that high fructose corn syrup is one of the

leading causes of obesity, which results in Type II Diabetes. Numerous lab tests

show that a diet high in high fructose corn syrup leads to copper deficiencies in

growing bodies, which can result in the swelling of vital organs, including the

heart and liver. With this new knowledge about high fructose corn syrup, the

consumption of sugar could increase.

Another product that is under the threat of a substitute is corn-ethanol. The rise

of corn-ethanol is resulting in a shortage of corn. Farmers can only produce so

much corn at a time before it becomes too damaging to the land. Because ADM

is a global company, the shortage of corn has put a strain on not only the

farmers but also management decision within ADM. Archer Daniels Midland has

to choose whether to produce corn-ethanol or use the corn as a food product.

Due to the shortage, researchers have been looking into different ways to

produce ethanol. Brazil now produces ethanol made from sugar cane. The

sugar-based ethanol has a 30% lower production costs than corn-ethanol.

Critics state that the reason it is cheaper is because sugar is cheaper in Brazil

than it is in the United States. But since there is only so much corn that can be

produced at a time, the price of corn is increasing. Because of this, oil and

17

gasoline companies are looking for alternative ways to receive ethanol.

Therefore, due to a rising threat of substitute products entering into the industry,

ADM needs to focus on what works best for the end user. (ADMworld.com)

Bargaining Power of Buyers

Bargaining power of buyers is the ability to influence prices when there are

numerous competitors offering many substitutes. (Palepu 2-5) This is an

important factor for ADM considering the emphasis that it placed on lowering

cost to entice and keep their customers. Archer Daniels Midland is one of the

world leaders in oilseed production. ADM is also the world’s largest corn

processing company. Not only does ADM have a majority of market share in

these fields, but they also are a cost leader due to the vertical integration of its

business structure. Despite the fact that ADM has three major components that

contribute to the bottom line, all of these components can be analyzed as one

since all of these segments are commodities. ADM is able to undercut most

competitors on price to maintain customers, which are mainly in the food

processing business, but also include fertilizers. Since ADM is dealing in a

commodity business, cost leadership is crucial and is valued as a long term

advantage in maintaining customer loyalty and repeat customers. In a

commodity related field, the customer is usually the one who can shop around

for the lowest price, giving the customer an advantage over the supplier. With

the vertical integration system ADM has set up, it will continue to be a cost

leader in this sector for the foreseeable future. Even though the customer has

most of the bargaining power in the commodity field, ADM is positioned well due

to its cost leadership.

18

Bargaining Power of Suppliers

When an organization has few suppliers to choose from and there are high

switching costs, the supplier has power over the organization. When suppliers

have power over the buyers, the organization has fewer options on how to

increase revenue. (Palepu 2-5) However, in any commodity related business the

supplier has little room to vary its price. Because there are numerous suppliers

within the agricultural industry, suppliers are forced to be inflexible. Due to

marketing equilibrium, if one farmer increases the price of a product, the farmer

will lose all buyers because there are other farmers Archer Daniels Midland can

buy from. This is strength for ADM because ADM remains in control of the

prices. The suppliers are not bound to ADM’s bargaining power, but rather

economic conditions that will not allow for any extraordinary profit gain. This

simple principle illustrates ADM’s ability to search for the lowest price among its

suppliers. Regardless of ADM’s market leadership, any bargaining power

regarding suppliers falls in ADM’s favor.

Characterization of Industry

Overall the agricultural processing and refinement industry has a dominant

advantage in cost leadership. In addition, the industry shows signs of having

advantage in differentiation. Since this is a commodity based industry cost

leadership might be the only way to achieve superior performance (Palepu 2-7).

There are many ways to achieve cost leadership, including economies of scale

and scope, economies of learning, efficient production, and lower input costs

(Palepu 2-8).

Economies scale is when average cost declines with increase in output. This can

be accomplished by companies within the industry producing mass quantities for

consumers. An economy of scope is achieved when average total costs are

19

lowered due to a rise in the amount of different items being produced. When

companies within the agricultural processing industry introduce different items

into their production lines, such as bio-diesel or ethanol, this can achieve an

economy of scope. An economy of learning is when there is a decrease in

average cost arising from accumulating experience.

Efficient production is an individual measurement of how effective a company

can produce its product. This can be accomplished by decreasing wasted time,

wasted materials, and work in progress. In the agricultural processing industry,

lower input costs are achieved by establishing sound relationships with suppliers,

in this case farmers.

Differentiation in the industry is shown by investments made in research and

development. For example, the research teams are developing new ways to

derive food and chemicals from renewable resources in order to continue to

produce animal feed products.

With these factors in mind, we believe the agricultural industry is predominately

a cost leader and shows a possible sign of differentiation. It is important to

understand the characterization of the industry because it gives a benchmark of

the valuation of individual firms within the industry.

Key Success Factors

Defining key success factors enable a company to understand how it can better

develop for future performance. This gives investors an advantage in deciding

which companies to endow. The key success factors play an important role in

maintaining a competitive edge and supplier relations.

Bargaining Power

20

The presence of bargaining power usually arises from an established industry

with reputable companies. Bargaining power gives a company the competitive

advantage because of the relationships between suppliers and buyers. Due to

the long established field of agricultural refinement, the market is satiated with

firms struggling to compete for customer base. This leaves no room for pure

growth in the industry, but rather a struggle to steal customers from

competitors. Thus the relationship between companies and their suppliers, as

well as customers, is essential to the overall success of a firm. Long established

companies have a competitive edge in this regard due to their partnerships and

relationships with clients built over years of experience. Without bargaining

power, firms have no chance of success and will be smothered within this highly

competitive industry.

Cost leadership in Commodity Field

Cost leadership requires a company to be the lowest cost producer, while

continuing to produce a higher quality product. In order to be successful within

this industry, a company must find ways to keep cost at a minimum. (Palepu 2-

7) One way is by avoiding unnecessary cost. This can be completed by being

knowledgeable about the production, as well as being skilled in the

manufacturing process. Vertical integration and finding lower cost materials are

additional ways to lower production costs. Cost leadership has the ability to

target broad markets. Failure to be a cost leader in a commodity market can

result in continual loss of customers and ultimately profits.

Economies of Scale

An economy of scale occurs when a company has the ability to lower the cost

per unit when it increases the amount of production. A result of this marginal

21

profit increases per additional unit of production. This is possible because a

company can buy and produce materials in mass as well as maintain a high level

of efficient production. The company also is able to improve efficiency since

large productions of similar items require specialized and expensive equipment

that can efficiently allocate and utilize its resources. When a company

successfully improves efficiency using resources, they have the ability to control

cost of production.

Economy of Scope

An economy of scope is achieved when average total cost are lowered due to a

rise in the amount of different items being produced. A company must

understand the industry it belongs to, so it will not loose focus. A company that

chooses to market a particular product has a competitive advantage when it

understands the customers the product will be marketed to. Specialization of a

company can help it to maintain focus in a highly diversified market such as the

agricultural processing industry. A company remains competitive when it

understands that company objectives must be specialized, and the company is

willing to adapt to these specialties to better satisfy its clients.

Delegation of Managerial Responsibilities

Delegating managerial responsibilities empowers management to make decisions

and organize goals. By delegating the right task to the correct person, multiple

tasks can be completed efficiently and in a timely manner. Because this industry

is dominated by only a few companies that are large, firms must rely upon their

management staff to make regional and sector specific decisions. Without doing

so, companies in this field run the risk of not being efficient in each of the

echelons of the refining process. Remaining competitive in cost is essential in

22

commodity fields, and efficient managerial programs are necessary in attaining

that goal.

In conclusion, it’s important for a company to address these factors when

determining how it can better compete against competitors within the industry.

These factors make-up what companies in the commodity industry

Competitive Advantage Analysis

The agricultural processing industry consists of few major companies, therefore

making this a competitive cost leadership industry. As previously discussed, to

achieve competitive advantage ADM must learn to be efficient in the factors that

make up the industry.

ADM Key Success Factors

Bargaining

Power

Cost

Leadership

Economies of

Scale

Economies of

Scope

Delegation of

Management

Fair Excellent Excellent Good Good

Bargaining Power

Bargaining power, a company’s ability to control prices among buyers and

sellers, is an essential factor for an industry dominated by commodities since it is

one of the few ways to truly minimize costs while optimizing profit. ADM is an

agricultural food processing company, however; they focus on maintaining a

strong relationship between farmers and consumers. Therefore, its partnership

with farmers has become essential to ADM’s overall market. ADM fully utilizes

this partnership through hedging contracts, futures, and options. While ADM’s

top competitor Cargill Inc. focuses mainly on relationships with its customers and

23

the effect their products have on them. ADM is restricted to bargaining with its

customers mainly because of price competition and market sensitivity to product

substitution. For example, some of ADM’s goods are commodity in nature, such

as corn syrup, which leads to an inability to negotiate on price. Furthermore,

substitutions threaten ADM’s product line in areas such as corn ethanol, where

sugar ethanol could be an easy replacement. ADM spends most of their time

and effort enhancing their relationship with their suppliers rather than

customers. This gives ADM a power of bargaining because with their superior

supplier relationship, they are able to get products at a lower cost without

expending significant resources into customer relations. Having the power of

bargaining gives ADM a competitive advantage over their competitors with

regards to inputs; however, we believe ADM’s lack of sufficient customer

bargaining power can be considered a weakness.

Cost Leadership in Commodity Field

Cost leadership is a crucial success driver in any commodity industry since it is

one of few areas where any true profit can be squeezed out of markets defined

by undifferentiated products. By implementing vertical integration ADM cuts out

any unnecessary costs, such as a middle man. The fact that ADM owns its own

transportation routes helps mitigate any excess costs or volatility in pricing due

to recent fuel concerns and fluctuations in the trucking industry. With ADM

being located all over the world, it is important for them to be able to minimize

their costs when they are distributing their products. The fact that they are able

to lower costs of transportation, allows them to gain cost leadership by being

able to produce more all over the world at a lower cost per unit. “Flexibility,

efficiency, reliability, and quality”, are four words ADM uses to describe their

transportation system. They currently own and operate 20,500 railcars, 2,300

tractor trailers, 2,100 barges, 30 tow boats, and 29 line boats. (ADMworld.com)

With such extensive focus on lowering costs through transportation and vertical

24

integration ADM has become a cost leader giving them higher profits and more

market share than competitors.

Economies of Scale

ADM is able to reduce fixed cost by large scale production, known as economies

of scale, which provides them a competitive advantage. They possess

manufacturing, distribution, and sales facilities located in 40 different states of

the US, in Canada, Africa, Europe, Asia, and Latin America.

(www.admworld.com) By being located all over the world, ADM has the

capabilities to process its products in massive quantities. Cost per unit is

lowered by spreading fixed costs across a larger product base. For instance, they

have 137 processing plants in the United States, giving ADM the resources to

increase its total production. Overall, ADM’s sheer size and processing clout,

lowers its total operating costs allowing them to be price competitive within the

industry.

Economy of Scope

Economy of scope is the ability to focus on a particular field without spreading a

company too thin across other markets, causing them to lose profits. Maintaining

ADM’s core competencies by focusing on agricultural processing, the company

continues to be a contender due to its ability to consistently innovate. This stays

consistent with their mission statement, “To unlock the potential of nature to

improve the quality of life”. (ADMworld.com) ADM is able to consistently

compete with its new products because they know a great deal about the

industry, in which they are one of the prime leaders. With ADM’s wide range of

products, they have been able to develop unique products such as corn based

ethanol within the corn processing industry. ADM has become the leader in

production of the renewable fuels called ethanol and bio-diesel. This is one of

25

the many ways that ADM proves to be focused in the industry, but still expand

into other areas of the corn processing market. With much investment in

research and development, in areas such as corn ethanol, and the creation of

these innovative products, the company is able to have a competitive advantage

with economies of scope.

Delegation of Managerial Responsibilities

Similar to the economies of scope, mangers need to be specialized in the field

they are overseeing. It is extremely important for the management staff of ADM

to be able to make regional and sector specific decisions. Just last year, ADM

underwent some major management changes, switching current managers to

different managing positions. ADM seems to be efficient in delegating

managerial responsibilities by having numerous managers for every aspect of the

company. They are very specific as to what each manager is responsible for; for

example, some management titles consist of Vice President with responsibilities

for global cocoa business, Vice President with responsibilities for compensation

and benefits, and Vice President with responsibilities for global oilseed

businesses. With such highly specialized managers, ADM is able to quickly react

and adapt to any problem that may incur within the company. By separating the

responsibilities throughout the company, ADM is able to carry a competitive

advantage by having each of its managers highly skilled in the responsibilities

they oversee.

26

Accounting Analysis

Key Accounting Policies

Accounting analysis is vital for a firm in order to evaluate its current financial

position and forecast its future performance, which will allow the firm and

investors to be aware of what is expected from the company in the future.

When performing an accounting analysis, there are several key steps to follow in

order to evaluate the firm’s accounting quality. First, is identifying key

accounting policies. When identifying key accounting policies, it is important to

take into account its key success factors and evaluate if ADM supports them in

its accounting policies and uses them as critical value drivers. As previously

discussed, ADM is able to be a cost leader due to the fact that it is vertically

integrated. This allows ADM to produce globally at a relatively lower cost per

unit. Many estimates are made when preparing the financial statements which

involve knowledge of historical and current facts in order to make decisions for

its position in the future. For example, because ADM owns its own

transportation, it must make estimates such as the amount of depreciation.

Therefore, it is important for ADM to be able to make educated estimates to

ensure that its financial statements will be properly stated.

Inventories and derivatives are considered a key success factor and a critical

accounting policy because ADM is able to pay fixed prices through its futures and

options contracts which set off many risks of the business. Some of ADM’s

agricultural inventories consist of “forward fixed-price purchase and sale

contracts and exchange-traded futures and options contracts that are valued at

an estimated market value” (ADM’s 10-K). Using exchange-quoted prices that

are adjusted for local market differences is how ADM estimates the market value.

In the statement of earnings under cost of products sold, the changes in the

27

market value of inventories and contracts is documented. For the derivatives

contracts, which are an agreement for an asset at a future date for an agreed

upon price, ADM designates them as cash flow hedges. When these hedged

items are recognized, gains and losses from the transactions are recorded in

other comprehensive income, net of income taxes. (ADM’s 10-K) This is found in

the statement of earnings under the cost of product sold. It is important for

ADM to cover itself with futures contracts since they run a risk in its commodity

business due to unpredictable weather, planting, changes in global demand, and

many other risks.

Employee Benefit Plans

Another critical accounting policy is employee benefit plans, which ADM provides

for selected international locations and all employees in the United States. ADM

employee benefit plans consist of defined contribution plans and defined benefit

plans. The defined contribution plan is where companies agree to contribute

fixed amounts today to cover future benefits. This requires very little forecasting

to estimate their annual cost since the firm’s obligation is limited to its annual

obligation to contribute to the employees’ retirement plans. (Palepu 4-40)

Whereas defined benefit plans use estimates to forecast future benefit needs.

Roughly 79 percent of ADM’s pension plans are made of defined benefit plans.

(ADM’s 10-K)

28

ADM Pension Benefits

2004 2005 2006

Defined Benefits 88,521 105,955 114,417

Defined Contribution 23,622 25,046 26,616

As of June 30, 2006, ADM employed about 26,800 employees, which indicates

how many estimates have to be made in order to predict benefit plans required

to cover all of their employees. Many estimates are taken into consideration

when measuring the pension, postretirement health care, and life insurance

benefits, which consist of “interest rates used to discount certain liabilities, rates

of return on assets set aside to fund these plans, rates of compensation

increases, employee turnover rates, anticipated mortality rates, and anticipated

future health care costs” (ADM’s 10-K) The rate at which pensions are estimated

for future expenses is called the “discount rate.” The return on assets uses the

net profit margin and asset turnover ratio to ensure its assets are able to

continually contribute to the pension funds. With the help of third-party

specialist, ADM is able to estimate the expenses and funded condition for the

employee benefit plans. It is vital as a firm to have these incentives of benefits

for employees to give them something to want to work for and keep them loyal,

which will in effect produce efficient and high quality performance. Incorrect

measurements of these expenses could result in incorrect estimates in the future

that leave them financially unprepared to supply its employees with benefits, so

it is important that ADM is as certain as possible for the amounts it records in the

financial statements.

Since ADM’s business is extremely capital intensive with many assets involved all

over the world, it is key that they realize when it is time for asset abandonment

29

and write-downs to make sure they are able to conduct their production

efficiently. One of ADM’s key success factors is how ADM operates its own

transportation, and does not have to worry about the fuel concerns and

fluctuations in the trucking industry. This brings on the next critical accounting

policy which is asset abandonment and write-downs. ADM’s assets, such as

property, plant, and equipment, are monitored for impairment as they are being

depreciated. When the assets are no longer of use to the company, they can be

abandoned, use for something alternatively within the company, or sold in order

to recover the carrying value. Repairs are expensed as they are incurred. As for

depreciation, the straight line method is used for financial reporting and the

accelerated method is used for income tax purposes. ADM recorded a 61 million

dollar charge to cost of products sold related to abandonment and write-offs

which led to a nine million dollar loss in equity in earnings. It is important that

the estimates and depreciation ADM records on its financial statements are

correct because they affect several years in the future and could lead to

overstating or understating the value of ADM.

It is essential that ADM’s estimates are correct or close to correct measurements

when valuing these critical policies and all other accounting inputs, because

there are many penalties that could result if it appears that ADM is trying to

overestimate or underestimate its financial statements. There are many ways in

which firms can do this, which will be examined in future sections. Identifying

key accounting policies is just the beginning of the accounting analysis and it is a

way to see how ADM treats its key success factors on the accounting side and

see what its critical value drivers are. Once this is completed, analysts can

determine the amount of accounting flexibility within the company’s financial

statements.

30

Accounting Flexibility

Archer Daniels Midland prepares its financial statements in compliance with SEC

regulations as well as the generally accepted accounting principles (GAAP.)

While ADM must follow the basic guidelines, management does have the choice

to use an amount of flexibility to its advantage. An example of this flexibility is

how ADM chooses to disclose its estimations. The use of tax depreciation

estimates the asset lives, salvage values, and amortization rates. Assets are

likely to amortize more rapidly than justifiable, given the assets’ economic

usefulness, leading to long term asset understatements. (Palepu 4-13) Choices

such as whether a company wants to be conservative or aggressive with its

accounting can determine future revenues and expenses. Based on the choices

evident in ADM’s 10-K, we feel that ADM follows conservative accounting

policies. One of ADM’s key success factors, managerial delegation, gives the

managers the power to make decisions regarding which accounting policies to

disclose and which are kept private within the company. Since accountants are

naturally predisposed toward conservative accounting, ADM’s managers

delegated the responsibility for choosing whether or not to follow conservative

policies to its accounting department. We believe that ADM does not have a

sufficient reason to keep from disclosing most of its financial statements and see

this as a weakness within the company’s policies regarding conservatism.

Inventory, a key success factor through its variable cost, is valued at the

estimated market value. These estimates are made by management and are

based on the exchange-quoted price. If management changes inventory

methods or market value changes, it must be noted within the financial reports.

At this point in time, ADM is using the LIFO method for its inventory. This

means the last items put into inventory are taken out of inventory first. When

LIFO is used, cost of goods sold is higher, which results in a lower income and

lower retained earnings. However, LIFO lowers taxes, which raises income.

31

Businesses do not look as well off using LIFO as they would using FIFO, first

inventory in is the first inventory out, which lowers cost of goods sold, increasing

income. It should be noted however that ADM uses FIFO as well as a Market

Inventory system to account for its commodity inventories.

ADM records property, plant, and equipment at cost, which is a conservative

accounting method, mandated by GAAP. This is important to understand

because GAAP regulates how often firms are able to revalue the long term assets

to ensure the quality of accounting. While ADM uses the straight line

depreciation method for its financial reporting, it uses accelerated methods for

income tax purposes. Because of accounting flexibility, a company can have

separate “books” for financial reports and income tax purposes. For ADM,

management has decided to depreciate buildings for 10 to 50 years and

equipment for 3 to 30 years.

Goodwill is an intangible asset that’s innately hard to value but can most readily

be described as the amount paid in excess of market value, when acquiring

another company. If a company, like ADM does not revaluate Goodwill in the

balance sheet, the company could be inaccurately stating an important asset.

According to GAAP requirements, firms must revalue their goodwill accounts

annually. The flexibility regarding goodwill can manifest itself when managers

must mark down goodwill to market value. Managers can be tempted to

manipulate this data to show higher earnings in following periods. When looking

at ADM’s financial statements it seems to have accurately stated impairments,

acquisitions, and disposals correctly in the goodwill account. (ADM’s 10-K) The

fact that ADM accurately represents its goodwill in the financial statements gives

a sense of confidence that it is honestly representing the company’s true value.

32

Evaluating Accounting Strategy

Looking at ADM’s recent 10K that was filed in September of 2006, we notice that

ADM uses Last-in First-out (LIFO) to classify inventory. This means that in a

period of rising prices, this method yields a lower ending inventory, a higher cost

of goods sold, a lower gross profit (assuming constant price), and a lower

taxable income. ADM prepares its financial statements in conformity with

generally accepted accounting principles (GAAP). Following generally accepted

accounting principles requires management to make estimates and assumptions

that affect amounts reported on their financial statements (10-K). Based on

ADM’s past financial statements, they prove to have a conservative approach to

accounting due to the fact that ADM spends more time recognizing losses than

gains. ADM’s top competitors are Bunge Ltd, Cargill Inc., and ConAgra Foods

who all use similar accounting policies. Having competitors use similar

accounting policies sets everyone at a level playing field with accounting

strategies.

According to ADM’s 10-K report, it has had one fairly recent change in its

accounting policy. In March of 2005, the Financial Accounting Standards Board

(FASB) issued FIN 47, Accounting for Conditional Asset Retirement Obligations,

an interpretation of FASB statement No. 143. FIN 47 clarifies how to handle the

legal obligation to perform asset retirement activity. ADM adopted FIN 47 on July

1, 2005. The result of implementing FIN 47 was positive, giving ADM a $3

million increase in property, plant and equipment. Also, hedging is a means of

insuring a company’s inventory by countering any losses (gains) by providing

gains (losses) through setting future commodity prices. This is particularly useful

in a field with highly fluctuating commodity prices, such as ADM’s. After looking

at ADM’s accounting strategies, there appears to be no reason to raise questions

concerning the policies they put into practice. ADM’s strategies can be justified

for the type of commodity industry in which they operate.

33

Quality of Disclosure

The quality of a firm’s financial statements helps one to clearly see into the inner

workings of a business. A level of transparency is gained with high quality

disclosures that help analysts to truly understand a business down to every

detail. The ability to accurately understand a firm is crucial to estimating the

value of a firm.

Qualitative

The bulk of a company’s financial information is found in a company’s 10-K

annual report. This report should disclose everything that is needed to know

about the company from both a qualitative and quantitative viewpoint. ADM

does a poor job of disaggregating the company base, though much of the

specific information is disclosed regarding industry. Sector information is

available, but no information is disclosed about specific assets or location of

operations. Overall, ADM did not do anything to set their financial statements as

a guide for investors.

From a Qualitative standpoint, the information provided gave a general

impression of the company’s inner workings and departments. However, we feel

that specifics were lacking. ADM is reluctant to give any information that dealt

with particular regions of the business, leaving an overall feeling of

disappointment. What we want to see is information broken down

geographically. We would also like to see information regarding fixed assets.

Considering both of these factors are largely important to the operations of ADM,

we feel investors need to know more about these segments of the company.

The lack of some information and overall vagueness of the qualitative section

leaves investors vulnerable and confused when it comes to truly understanding

34

ADM. Overall, we give the qualitative section of ADM’s financial statement a fair

rating; it seems the company only gives the required information for a 10-K

when there are clearly areas where ADM should go into further depth.

Quantitative

Quantitative information is rather direct, raw numbers expressing a company’s

performance. Quantitative information is just as important, if not more

important than qualitative sections. The numbers of a company can tell you its

history, its performance, its strategy; the numbers of a company can tell you as

much of a story as words themselves.

In the following section, we ran some ratios on ADM and two of its main

competitors. Cargill is also a main competitor, but since the company is privately

held, financial information gathering is all but impossible. Also Bunge Limited

has only been publicly traded over the past three years, so any previous

information not gathered is due to the same reason.

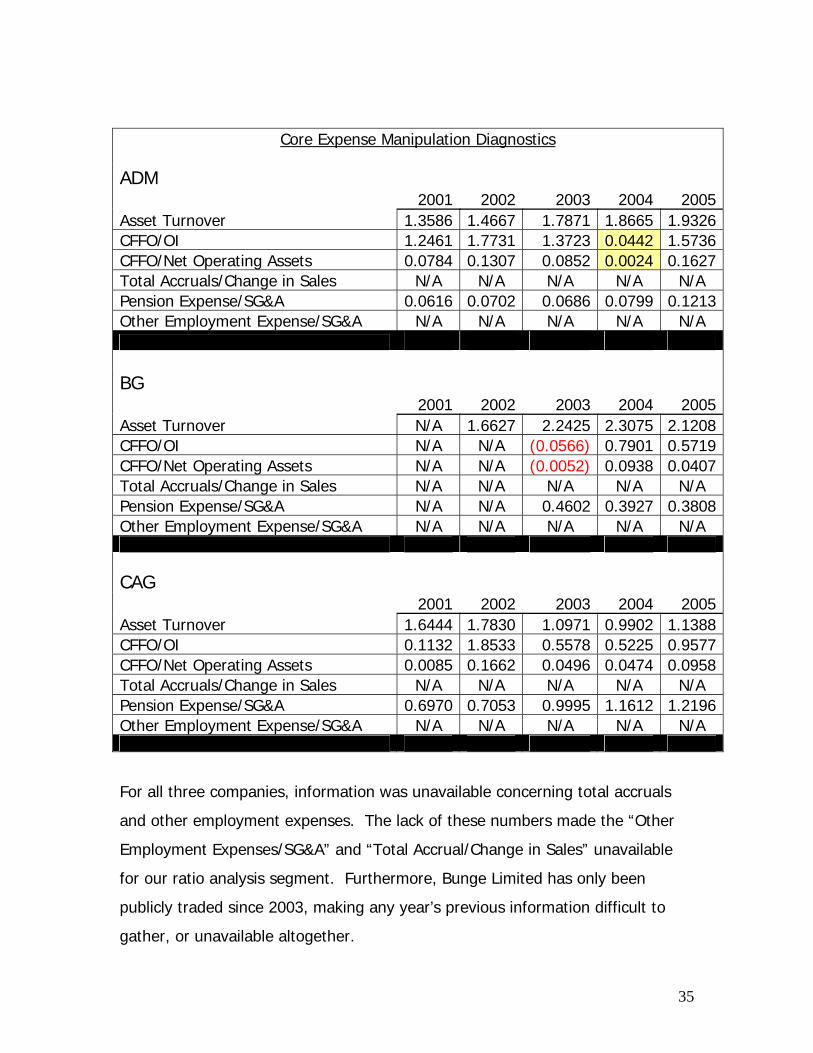

Core Expense Manipulation Diagnostics

The following information represents the core measurements of detecting

possible accounting irregularities regarding expenses. Since ADM is in a highly

cost competitive field, cost manipulations are key areas to investigate. There are

a few areas of concern regarding the financial information we ran these ratios on

that will be further discussed in a later section.

35

For all three companies, information was unavailable concerning total accruals

and other employment expenses. The lack of these numbers made the “Other

Employment Expenses/SG&A” and “Total Accrual/Change in Sales” unavailable

for our ratio analysis segment. Furthermore, Bunge Limited has only been

publicly traded since 2003, making any year’s previous information difficult to

gather, or unavailable altogether.

Core Expense Manipulation Diagnostics

ADM 2001 2002 2003 2004 2005Asset Turnover 1.3586 1.4667 1.7871 1.8665 1.9326 CFFO/OI 1.2461 1.7731 1.3723 0.0442 1.5736 CFFO/Net Operating Assets 0.0784 0.1307 0.0852 0.0024 0.1627 Total Accruals/Change in Sales N/A N/A N/A N/A N/A Pension Expense/SG&A 0.0616 0.0702 0.0686 0.0799 0.1213 Other Employment Expense/SG&A N/A N/A N/A N/A N/A BG 2001 2002 2003 2004 2005Asset Turnover N/A 1.6627 2.2425 2.3075 2.1208 CFFO/OI N/A N/A (0.0566) 0.7901 0.5719 CFFO/Net Operating Assets N/A N/A (0.0052) 0.0938 0.0407 Total Accruals/Change in Sales N/A N/A N/A N/A N/A Pension Expense/SG&A N/A N/A 0.4602 0.3927 0.3808 Other Employment Expense/SG&A N/A N/A N/A N/A N/A

CAG 2001 2002 2003 2004 2005Asset Turnover 1.6444 1.7830 1.0971 0.9902 1.1388 CFFO/OI 0.1132 1.8533 0.5578 0.5225 0.9577 CFFO/Net Operating Assets 0.0085 0.1662 0.0496 0.0474 0.0958Total Accruals/Change in Sales N/A N/A N/A N/A N/A Pension Expense/SG&A 0.6970 0.7053 0.9995 1.1612 1.2196 Other Employment Expense/SG&A N/A N/A N/A N/A N/A

36

Asset Turnover (Sales/Assets)

0.0000

0.5000

1.0000

1.5000

2.0000

2.5000

2001 2002 2003 2004 2005

ADMBGCAG

An asset diagnostic is crucial to the understanding of the capital intensive Archer

Daniels Midland. The steady growth rate is promising for ADM compared to its

more volatile competitors. This is a strong sign of reliability for ADM. The sale

of a division from CAG explains the extreme drop in 2003. Since BG is such a

small and growing company, its ratio is understandingly volatile in growth, but

appears to be leveling off.

37

Cash Flow from Operations/Operating Income

(0.5000)

0.0000

0.5000

1.0000

1.5000

2.0000

2001 2002 2003 2004 2005

ADMBGCAG

This particular ratio is alarming at first due to the varying ratio levels across the

board. For ADM, the severe drop in 2004 is directly related to a massive level of

inventory write-offs, which in turn reduced cash flows from operations

significantly. ADM takes considerable actions to hedge any inventory losses. For

the year 2004, ADM realized a gain of nine million dollars as a direct result of

their hedging activities, as well as a gain of 83 million dollars in “other

comprehensive income.” (www.Morningstar.com) According to ADM’s financials,

hedging activities can materialize in the “other comprehensive income section”.

The gain in hedging for 2004, considering an inventory loss, is a sign of good

hedging activities on part of the company. There was no correlation in 2004 to

such an extensive inventory write-off in competing firms.

38

CFFO/Net Operating Assets

(0.0250)

0.0000

0.0250

0.0500

0.0750

0.1000

0.1250

0.1500

0.1750

0.2000

2001 2002 2003 2004 2005

ADMBGCAG

As with the previous graph, the high degree of volatility illustrated in this ratio is

due to the drastic change in cash flows from operations. Net operating assets

themselves are not the volatile element in this ratio.

39

Pension Expense/SG&A Expense

0.0000

0.2000

0.4000

0.6000

0.8000

1.0000

1.2000

1.4000

2001 2002 2003 2004 2005

ADMBGCAG

The Pension Expense Ratio foreshadows a company’s ability to handle employee

costs in the future. The trend for this ratio is similar across the board; a raising

ratio in reference to pension expense is to be expected in today’s economy with

high concerns regarding retirement benefits and the uncertainty in that field.

The consistency of growth per company, and within the industry is within

reasonable expectations. The stability of this ratio is reassuring that ADM is

planning well in regards to pension expenses.

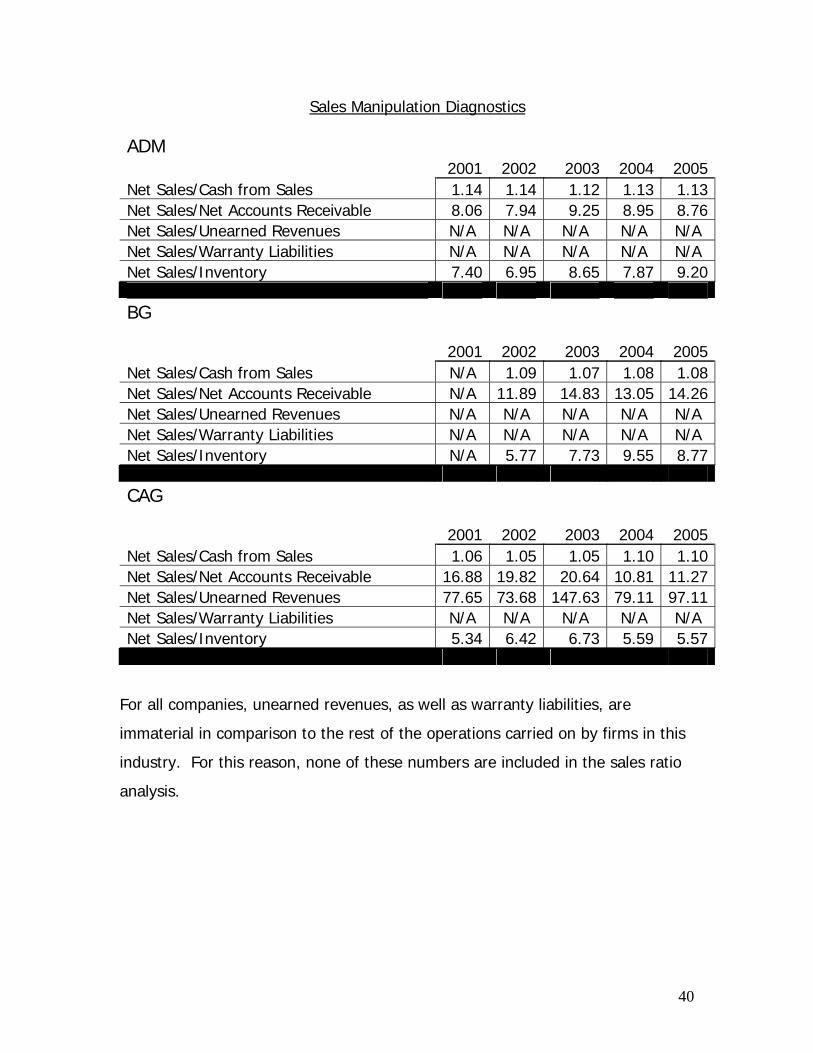

Sales Manipulation Diagnostics

Sales manipulation is something of a concern for most firms since managers are

typically tempted to inflate sales for the sake of self interest. Managers often

can gain bonuses directly related to sales. With this in mind we ran ratios of

ADM’s sales with respect to two of its competitors.

40

Sales Manipulation Diagnostics

ADM 2001 2002 2003 2004 2005Net Sales/Cash from Sales 1.14 1.14 1.12 1.13 1.13 Net Sales/Net Accounts Receivable 8.06 7.94 9.25 8.95 8.76 Net Sales/Unearned Revenues N/A N/A N/A N/A N/A Net Sales/Warranty Liabilities N/A N/A N/A N/A N/A Net Sales/Inventory 7.40 6.95 8.65 7.87 9.20

BG 2001 2002 2003 2004 2005Net Sales/Cash from Sales N/A 1.09 1.07 1.08 1.08 Net Sales/Net Accounts Receivable N/A 11.89 14.83 13.05 14.26 Net Sales/Unearned Revenues N/A N/A N/A N/A N/A Net Sales/Warranty Liabilities N/A N/A N/A N/A N/A Net Sales/Inventory N/A 5.77 7.73 9.55 8.77

CAG 2001 2002 2003 2004 2005Net Sales/Cash from Sales 1.06 1.05 1.05 1.10 1.10 Net Sales/Net Accounts Receivable 16.88 19.82 20.64 10.81 11.27 Net Sales/Unearned Revenues 77.65 73.68 147.63 79.11 97.11 Net Sales/Warranty Liabilities N/A N/A N/A N/A N/A Net Sales/Inventory 5.34 6.42 6.73 5.59 5.57

For all companies, unearned revenues, as well as warranty liabilities, are

immaterial in comparison to the rest of the operations carried on by firms in this

industry. For this reason, none of these numbers are included in the sales ratio

analysis.

41

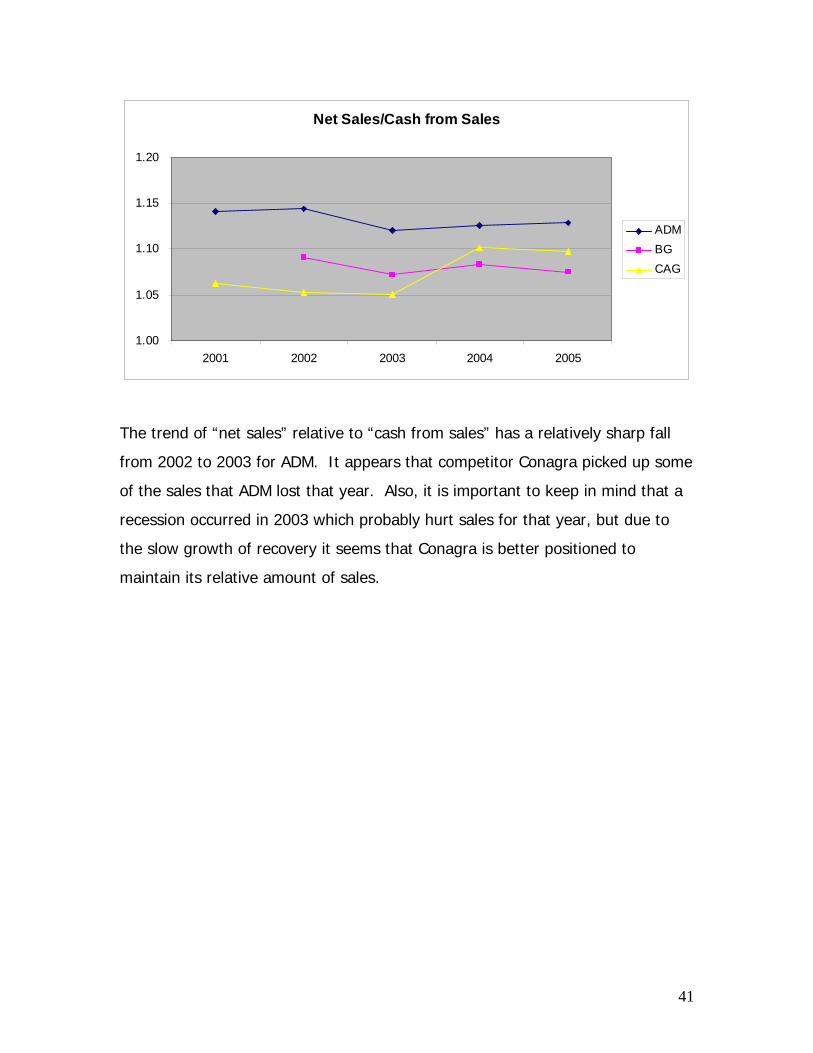

Net Sales/Cash from Sales

1.00

1.05

1.10

1.15

1.20

2001 2002 2003 2004 2005

ADMBGCAG

The trend of “net sales” relative to “cash from sales” has a relatively sharp fall

from 2002 to 2003 for ADM. It appears that competitor Conagra picked up some

of the sales that ADM lost that year. Also, it is important to keep in mind that a

recession occurred in 2003 which probably hurt sales for that year, but due to

the slow growth of recovery it seems that Conagra is better positioned to

maintain its relative amount of sales.

42

Net Sales/Net Accounts Receivable

0.00

5.00

10.00

15.00

20.00

25.00

2001 2002 2003 2004 2005

ADMBGCAG

ADM is very consistent in the field of accounts receivables, leaving little room for

suspicion. ADM seems to be steadier than its competitors in this area, although

it should be mentioned that the sale of one of Conagra’s divisions could explain

some of the distorted ratios in the period between 2003 and 2004. The

consistency of ADM’s ratio is reassuring to the reliability of the company’s

performance.

43

Net Sales/Inventory

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2001 2002 2003 2004 2005

ADMBGCAG

Net Sales with respect to inventory is the most important sale ratio to look at for

ADM considering the company’s relatively large amount of fixed assets. There is

a cyclical pattern for ADM whereas Conagra and Bunge Limited seem to have

more volatile numbers. We feel this only reinforces ADM’s maturity in this field,

especially with respect to BG.

Potential “Red Flags”

When assessing companies’ financial statements, ratio analysis is a common tool

used to determine if any degree of accounting distortion is being used to mislead

the casual investor. Any accounting distortions that are discovered are

commonly referred to as “red flags”. These red flags alert company evaluators

that some deception may be occurring. It is crucial to find and asses red flags

whenever discovered as to prevent misleading investors for their protection.

After running sales and expense ratios on ADM financial statements going back

for the past five years, most of the ratios were in line with expectations.

However, when addressing the expense diagnostic of cash flow from operations

44

over operating income, some alarming numbers were found. The ratio itself was

extremely low in 2004 compared to the previous and following years. After some

initial investigation, it appears that CFFO was the number that was severely

depressed. Following up this discovery, the Cash Flow Statement disclosed an

unusually high inventory write off, 750 million dollars higher than the previous

year (ADM’s 10-K). Despite all of these alarming indicators, ADM managed to

hedge this loss with nearly 92 million dollars of revenue through contracts. At

first glance this gain seems minimal in comparison to the inventory write-off in

2004, but the hedging activities served their purpose by providing income in a

year of loss.

All of this leads us to believe that ADM has a team of experienced veterans in

control of hedging contracts for the firm. This is a highly valued asset in regards

to ADM’s industry and we view it as a strong competitive advantage and value

added for the firm.

Fixing Accounting Distortions

After investigation of ADM’s financial statements concerning the alarmingly low

CFFO in 2004, we found no indication of accounting distortions. At first glance

the numbers seem suspicious; however, after studying inventory management,

we found that this discrepancy was due to hedging contracts. In conclusion,

ADM’s financial statements seem accurate and true to form, adding another

degree of confidence regarding ADM’s business practices.

45

Ratio Analysis & Forecast Financials

Ratio Analysis

Profitability and growth are determining factors of the value of the firm. By

reviewing the ratios as well as forecasting the financial statements ten years in

the future, we can gain an understanding of ADM’s past financial performance,

as well as where the firm is going in the future. The ratios help examine the

firm’s liquidity & operating efficiency, profitability, and capital structure, as well

as give a better understanding of where ADM stands within the agricultural

processing industry, compared to competitors. Analyzing ADM, and the industry

in general, is important because it allows us to have a better understanding of

the information the company provides to see where the company has been, and

where the company is going relative to the industry.

Trend and Cross Sectional Analysis

The objective of a trend analysis is to make a reasonable forecast from the data

given by identifying any trends that exists. It is a tool to analyze not only the

firm, but also the overall industry. By revealing any trends that might be

occurring, we can begin to understand where the firm and industry will go.

During this trend analysis, we will review the past five years of financial

information for ADM and its competitors. Once the information is analyzed, it

will then be used to reasonably forecast information in future years. This

information will let us know if ADM is operating efficiently and effectively and

how it compares to its competitors and the overall industry.

Liquidity and Operating Efficiency Analysis Liquidity ratios attempt to measure the firm’s ability to repay its’ current liabilities

(Palepu 5). Liquidity is broken down into five separate ratios including: current

ratio, quick asset ratio, inventory turnover, receivable turnover and working

46

capital turnover. Current ratio and quick asset ratio show the firm’s liquidity

which is the cash equivalence of assets. Inventory turnover, receivables

turnover, and working capital turnover show the firm’s operating efficiency.

These liquidity ratios measure the firm’s ability to maintain sufficient cash

resources to cover current obligations.

Liquidity Analysis

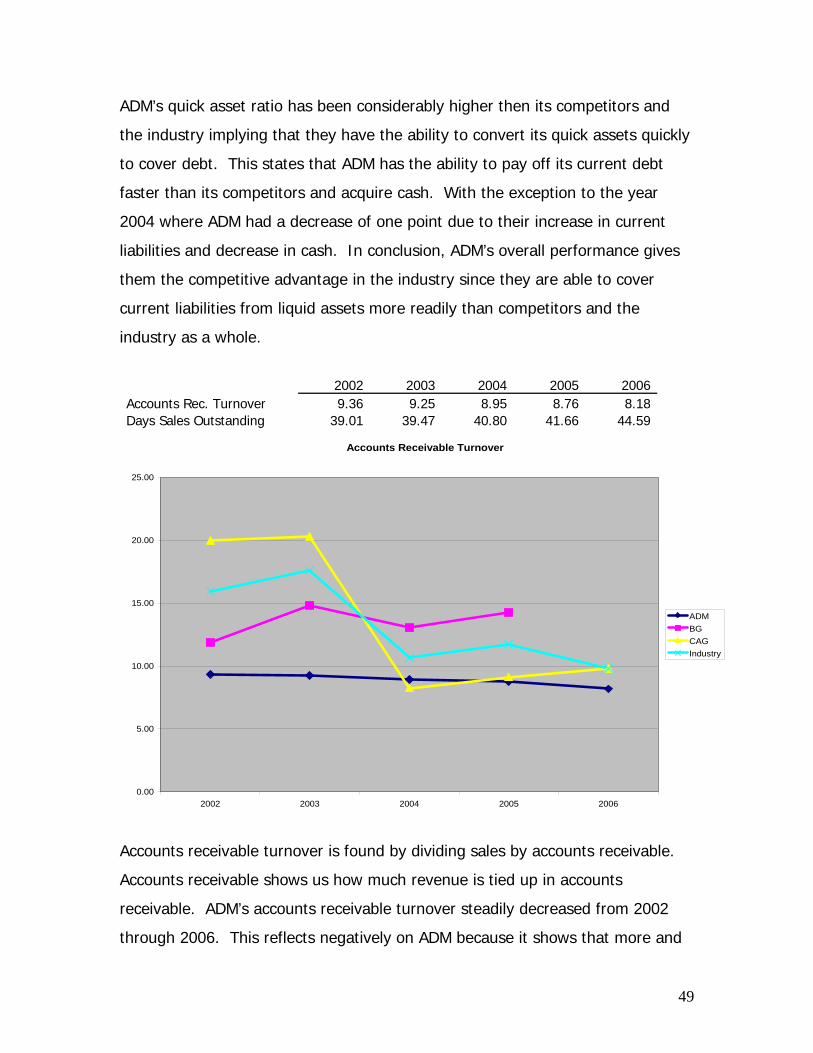

2002 2003 2004 2005 2006 Current Ratio 1.59 1.64 1.53 1.81 1.92 Quick Asset Ratio 0.80 0.79 0.68 0.86 0.91 Accounts Rec. Turnover 9.36 9.25 8.95 8.76 8.18 Days Supply Receivables 39.01 39.47 40.80 41.66 44.59 Inventory Turnover 8.86 8.16 7.41 8.58 7.19 Days Supply Inventory 41.19 44.71 49.29 42.55 50.77 Working Capital Turnover 9.90 9.38 10.07 8.27 6.46

Overall, ADM seems to be growing more liquid over time, providing a greater

ease for which the company can pay off immediate liabilities and acquire future

loans. Furthermore, the operating efficiency of the company is failing in the

recent years shown in the decline of the efficiency ratios. Although ADM is able

to grow more liquid, we foresee the loss in efficiency as a negative reflection on

ADM’s competitive advantage.

47

2002 2003 2004 2005 2006 Current Ratio 1.59 1.64 1.53 1.81 1.92

Current Ratio

1.00

1.10

1.20

1.30