conocophillips valuation project - texas tech...

TRANSCRIPT

0

ConocoPhillips Valuation Project

Financially Korrect Inc. Brad Bryan

Jerry Peterson

Susannah Lee

Jay Messamore

Ryan Hartsell

1

Table of Contents:

1. ConocoPhillips Snapshot……………………………………………………………………2

2. Executive Summary………………………………………………………………………….3

3. Business and Industry Analysis………………………………………………………….5

a. Rivalry Among Existing Firms………………………..5

b. Threat of New Entrants………………………………..7

c. Threat of Substitutes……………………………………8

d. Bargaining Power of Buyers………………………….9

e. Bargaining Power of Suppliers………………………10

4. Value Chain Analysis……………………………………………………………………….11

5. Competitive Advantage……………………………………………………………………11

6. Identifying Key Accounting Policies…………………………………………………..12

7. Asses Accounting Flexibility……………………………………………………………..15

8. Accounting Strategy……………………………………………………………………….17

9. Quality of Disclosure……………………………………………………………………….20

10. Screening Ratios…………………………………………………………………………….21

11. Identify Potential Red Flags……………………………………………………………..26

12. Corrections to Accounting Distortions …………………………………………......27

13. Ratio Analysis and Forecasts……………………………………………………………28

14. Financial Ratio Analysis ………………………………………………………………….28

15. Cross Sectional Analysis………………………………………………………………….32

16. Financial Statement Forecast Analysis………………………………………………36

17. Valuation Analysis………………………………………………………………………….38

18. Summary of Valuations ………………………………………………………………….47

19. Appendix A……………………………………………………………………………………50

20. Appendix B……………………………………………………………………………………56

21. Appendix C……………………………………………………………………………………60

22. References…………………………………………………………………………………….70

2

Executive Summary Recommendation – Buy Date of Valuation 11/01/06

COP NYSE (11/01/06) $60.30

52 week range 54.90 - 72.50

Revenue (2005) 183.00B Book Value per Share $32.00 Market Capitalization $812,482,200.00 Return on Equity 25.66% Shares Outstanding $13,474,000.00 Return on Assets 12.64% Dividend & Yield 1.44 (2.10%) Ratios COP Avg Industry Comp Performance of COP Forward P/E 8.41 8.66 Trailing 3mo 6mo 12mo Forward PEG 0.26 0.65 Ret. On COP (0.12) (0.11) (0.07) Mkt/Bk 1.8844 Ret on S&P 500 0.08 0.05 0.14 Value Predictions: Cost of Capital Estimates R2 Beta Ke Actual Current Price (11/01) 60.30 Ke Estimated 0.11304 0.60462 0.08922 Residual Income Valuation 84.98 5-Year Beta (0.00596) 0.27731 0.06631 FCF Valuation 105.46 3-Year Beta 0.04029 0.81073 0.10365 AEG Valuation 71.13

2-Year Beta (0.00852) 0.62173 0.09042 Discounted Dividends Valuation 46.52

Published Beta EPS Forecast

Kd 0.0600 2005 Act 2006 Est'd 2007 Est'd 2008 Est'd

WACC 0.0817 EPS 8.21 6.63 7.56 8.24

Altman's Z-Score 2.2650

3

Executive Summary

ConocoPhillips’ is an integrated oil and gas company that recently merged to

form a successful partnership. The two companies consolidated in 2002, and now are a

formidable competitor in the industry. ConocoPhillips’ main competitors include large oil

producers such as: ExxonMobil, BP, and Chevron. Due to the large assets needed to

compete in this industry, ConocoPhillips’ threat of new competition is very minimal. The

oil and gas industry is very competitive with the current companies involved, and

ConocoPhillips must be very cautious when it comes to setting prices in this price

sensitive industry. This highly sensitive price market is the cause of ConocoPhillips to

become an integrated oil and gas company. By integrating its process from start to

finish, ConocoPhillips is able to keep production costs down to help achieve greater

profits in the end.

ConocoPhillips’ maintains a rather conservative accounting policy. Due to the

heavy reliance upon assumptions and estimations in the energy industry, managers

have the ability to fluff up their financial statements to make it appear as if the

company is very successful. ConocoPhillips stays away from this, and instead has a

very flexible accounting policy that allows for a more rational judgment about the

company’s current financial standing. Along with this conservative accounting strategy,

ConocoPhillips’ maintains a very transparent disclosure policy. This transparency allows

analysts to come to a more honest opinion about the company’s current value.

ConocoPhillips’ does not withhold the negative information about the company or any

potential shortcomings of the company. This open honesty shows management’s

confidence in the company and willingness to change what is wrong with itself.

After doing financial ratios on the company and other companies in the industry,

we were able to see how ConocoPhillips measured up to its competitors in the

integrated oil and gas business. Due to the merger of the two companies, many of the

ratios done varied significantly than what was going on in the industry. However, for

the most part ConocoPhillips is steadily recovering since the joining of the two

companies, and is near or above the industry average in many categories. For

example, before the merger, the two companies struggled with their inventory turnover,

4

and the companies were well below the industry average. However, after the union

between the two, ConocoPhillips has taken control of its inventory problem and is now

an industry leader in this category. Another financial aspect ConocoPhillips has been

recovering from after the merger is its creditworthiness. After the merger,

ConocoPhillips was near bankruptcy in terms of its Altman Z-score, but since then the

company has regained its worthiness. It appears that with time ConocoPhillips will be

able to recover from the amalgamation of the two companies.

After compiling financial data from the past five years, we forecasted financial

statements for the next ten years. In doing so, we were able to get a better

understanding of the position ConocoPhillips will be ten years from now. We

forecasted based upon the assumption that the company will continue to grow at the

rate it has been. The accuracy of these forecasts was of the utmost importance

because the valuation of the firm is based upon these forecasts.

By carefully forecasting future financial statements, we were then able to analyze

and do a variety of valuations on these statements. After this analysis, we came to the

judgment that the value of ConocoPhillips’ stock is undervalued by the market. All

valuation methods except for one, dividend growth method, showed ConocoPhillips to

be significantly undervalued. The dividend growth model is a very sensitive model that

is dependent upon very accurate growth rate forecasts; therefore, we believe that our

other valuation methods portray a more accurate assessment of the firm. The other

four valuation methods averaged an estimated value of $85.64 per share, which is well

above the observed price on November 1st 2006 of $60.30. Based upon these

valuations and forecasts, we believe that ConocoPhillips’ is considerably undervalued;

therefore, investors should purchase ConocoPhillips’ stock.

5

Stock Prices for past 5 years

Business and Industry Analysis

ConocoPhillips is an integrated energy company headquartered in Houston,

Texas, with operations in over 40 countries. Phillips Petroleum acquired Conoco Inc. on

August, 30 2002 to form ConocoPhillips, both Phillips Petroleum and Conoco Inc. has

over 100 years of history in the Oil and Gas industry. ConocoPhillips operates in four

core activities: petroleum exploration and production, petroleum refining and

marketing, natural gas gathering and processing, and chemicals and plastics

production. ConocoPhillips is the third largest integrated energy company in the United

States, based on market capitalization, and oil and gas proved reserves and production.

The integrated oil and gas industry is a $135 billion industry with competitors

that include Exxon Mobil, BP, and Chevron. With the rising prices of crude oil over the

past few years and strong demand from the U.S. and China markets, the industry is

experiencing sustained success. This success has enabled ConocoPhillips’ to experience

steady growth in the size of the company over the past five years. Since the merger

the company has increased its assets each year which has led to an exponentially larger

increase in the total sales for the company. This

increase in sales has since caused the stock price

to gradually rise since the collaboration of the two

companies.

ConocoPhillips currently has a market

capitalization of around $95 billion which is well

below the industry average.

Rivalry among existing firms

ConocoPhillips is one of 23 Integrated Oil and Gas companies. The Integrated Oil

and Gas Industry’s average sales in 2005 were $1.4 trillion. While 23 companies may

seem like a lot of competition, it is in fact relatively small when compared to the size of

the industry. ConocoPhillips’ average sales over the last 3 years were $142 billion; this

accounts for roughly 10% of the industry’s sales in 2005. It is also important to note

that ConocoPhillips’ sales are on the upturn, so this percentage is likely to increase.

6

Its main integrated oil competitors are Amerada Hess, ChevronTexaco,

ExxonMobil, Marathon, and Occidnetal. These companies deal in both up upstream and

downstream operations. Upstream operations involve exploration and production while

downstream operations include refining and marketing. ConocoPhillips has other

competitors whose entire business is focused on either downstream or upstream

operations. These competitors included Anadarko, Dynegy, Valero, and Halliburton just

to name a few. ConocoPhillips has a competitive advantage over these companies

because being involved in both downstream and upstream operations allows the

company to remain profitable when one operation lags. If prices or competition in one

operation becomes unfavorable, the other operation can cover the losses.

ConocoPhillips is the third largest integrated energy company in the United

States and second largest refiner in the United States. Worldwide, ConocoPhillips has

the fifth largest proved reserves and is the fourth largest refiner. ConocoPhillips

operates in more than 40 countries and has approximately 38,000 employees worldwide

and assets of $162 billion. Because of this, ConocoPhillips is one of the major players in

the 23 Integrated Oil and Gas companies and applies more pressure on competing firms

than it receives.

Because the energy business has very high demand and there are relatively few

competitors in the industry, existing firms do not engage in price wars. Instead, they

compete on non-price dimensions. One of the major non-price dimensions firms

compete on is the size and reach to which they can offer their products. In the Oil and

Gas Industry size is king. The larger your operations become, the higher probability

your firm will prosper. This is evident by the constant mergers and acquisitions that can

be observed in this industry. ConocoPhillips is no exception to this trend. Conoco and

Phillips66 merged in 2002 to create ConocoPhillips and have since acquired several

companies. ConocoPhillips also offers products other than oil and gas. They produce

Asphalts, Fuels, Lubricants, and Chemicals and Plastics. They also specialize in removal

of sulfur from oil. The degree of differentiation for ConocoPhillips and its competitors is

low, so their customers are ready to switch from one competitor to the other based on

price.

7

ConocoPhillips is among one of the largest integrated oil and gas companies

based in the U.S., with operations world wide. ConocoPhillips has competitors in both

the integrated and segmented energy industry, but has a competitive advantage over

most of these companies due to their size, vertical integration, and scope of operations.

Because existing firms do not engage in price wars, firms focus on increasing the size

and reach to which they can offer their products and offer other products such as

asphalts and chemicals. The degree of differentiation for ConocoPhillips and its

competitors is low, so their customers are ready to switch from one competitor to the

other based on price.

Threat of new entrants

The threat of new entrants is very minimal because the barriers to entry in this

industry restrain most prospects. The chances of another player of significant influence

entering the Market any time soon is highly unlikely. The make-up and operations of

this industry should remain around the same in the relevant future, which make

projection of what competition will be in the future rather easy. The existing energy

companies are so large and powerful that it would make it very difficult for a new

company to compete.

There are different barriers of entry to look at in this industry. One barrier to

entry, for example, is the hard to come by expertise that is needed to complete certain

jobs. Specialized workers are needed to operate equipment and determine key drilling

decisions, which would make it difficult for new companies to find the resources

necessary for exploration and production. Another barrier is the amount of money

needed to compete with existing oil companies. The machinery requirements alone for

a single drilling location can cost up to $1,000,000.

The threat of new entrants is again reduced by the practice of mergers and

acquisitions. Larger oil and gas companies regularly buy out smaller or bankrupt

companies to increase the scope of their business operations. These acquisitions would

range from actions such the merger of Chevron and Texaco, for example, to the

purchase of a small drilling or chemicals company by a large corporation. By the time a

8

new entrant begins to gain market share it will more than likely be bought out by one

of the major players.

New entrants will furthermore be at an extreme cost disadvantage because of

the economies of scale. New entrants would be forced to invest in a large capacity

which might not be utilized right away or to enter with less than optimum capacity.

Either way, a new entrant forced to invest this inefficiently would be at an extreme

disadvantage. With competing energy companies with assets totaling in the billions, it

would be near impossible for a new entrant to invest in enough assets to be able to

compete.

ConocoPhillips, along with its competitors, have established channels of

distribution that would act as another barrier. The large companies in this industry have

distribution centers, forms of transportation, and buyers and sellers all over the globe.

The large quantity at which these companies are doing business would make is difficult

for any new entrant to attract significant attention and find buyers and suppliers.

Simply put, the firms that are currently in the oil and gas company are far too

large and powerful for any new entrant to have a probable chance at surviving long

enough to compete. The expertise that is required for many operations of the business

are hard to come by and are already being employed by current players. The high cost

that it would take to become a new player in the oil and gas industry is another barrier

to entry. In addition, the competitive natures of the industry will more than likely lead

to the acquisition of any entering firm.

Threat of substitutes

The threat from substitutes consists of two components: product substitution

and technology substitution. Currently, the oil and gas industry is facing a rising threat

from alternative energy technologies replacing fossil fuels. The alternative energy

threat is small currently, but is a technology that must be considered when. The threat

of product substitution in the oil and gas industry currently is low, because without new

technology everything will remain linked to fossil fuels.

9

With ConocoPhillips being in the energy industry there are a number of

substitutes that the company needs to be wary of. The largest threat for the company

is the new energy conserving technologies that are being developed. These

technologies are present in a number of ways, some of which include more fuel efficient

vehicles or dual power vehicles. As new technologies arise there is the possibility they

will benefit the environment; however, this then causes need for concern for future

revenues within the industry. Due to the high costs of these new technologies that are

being introduced to replace oil and gas products, the immediate threat of these

technologies is not great; however, as these new technologies become more efficient

both in use and to produce, the impact of these technologies will be felt by the entire

oil and gas industry.

Another substitute that causes concern for the oil and gas industry is an increase

in the awareness and appeal of alternative fuels, such as ethanol, natural gas,

hydrogen, electricity and so on. These alternative fuels come strongly recommended

and are backed by many environmental groups to help try and stop the deterioration of

the environment. Other programs that serve as substitutes for the integrated oil and

gas industry can be classified as anything that leads to a lesser amount of fuel

consumption. The use of carpooling to work, as well as the HOV, lane both can be

included as substitutions. Mass transit systems, such as buses, trains, etc. also lead to

a lesser consumption of fossil fuel products.

Alternative fuel products are a threat to the oil and gas industry in the long run.

The alternative oil and gas threat has not been seriously felt by the industry yet;

however, oil and gas companies are making plans to prepare for the rise of the

alternative fuel threat. With consumption of fossil fuels at or near an all-time high over

the past 3 years, the threat of substitutions does not play a major factor in the

profitability of the industry.

Bargaining Power of Buyers

When considering the bargaining power of buyers, one must consider two

important factors: price sensitivity and comparitive bargaining power. Price sensitivity is

10

the extent on which ConocoPhillips cares to bargain on price and the bargaining power

is how influential ConocoPhillips can be in forcing the price down. Keeping these two

factors in check will ultimately lead to success in the oil and gas market

With the refinements of oil and gas, end products of this refinement are

undifferentiated. In a perfect case, buyers are more sensitive when the product they

are consuming is undifferentiated with little substitute. But the sensitivity of buyers is

one of unique case in the oil and gas field. As Americans, consumers have an extreme

dependence on oil and gas. The price sensitivity of consumers is at an all time high.

Due to low alternatives and low switching costs (Chevron/Texaco, Shell, etc.);

consumers are very dependent on current prices. The oil and gas industry’s lack of

bargaining is a direct result of their dependence on this raw material. The price

fluctuations that are experienced day to day at the pump are a cost that consumers

must pay in order to commute or engage in daily life. With little alternative to fossil

fuels and the increasing of China’s economy, the number of buyers is reaching all time

highs. The high numbers of buyers in combination with ample resources is the driving

force pushing these prices.

The bargaining powers of buyers in the oil and gas field are limited. Bargaining

power is the cost of one party not doing business with the other party. Consumers

(buyers) are without transportation if they choose to not do business. One level of

bargaining power that buyers have is legislation. With acts of Congress, legislation and

bills, and social pressure, buyers have the ability to put pressure on the oil and gas

industry to reduce their price per barrel down. Another option that consumers have is

to take part in the upcoming trend of total electric or hybrid vehicles. Less dependence

on gas would equal a consumption drop for oil and gas producers. This drop in

consumption would reduce revenue and drive prices down.

All in all, ConocoPhillps must maintain this fine line of price sensitivity and

bargaining power. With such power being limited in the oil and gas industry, any

adjustment towards the positive that ConocoPhillips could make would enhance their

overall productivity and output. This increased productivity will provide beneficial in

investors in the long run.

11

Bargaining Power of Suppliers

The bargaining power of suppliers is the exact same as the bargaining power

buyers turned 180 degrees. With this holding true, ConocoPhillips as well as their

suppliers have to find an agreed upon medium with which to exchange. This medium is

the key to success.

Since ConocoPhillips is an integrated oil and gas company, meaning it operates in

both the upstream and downstream portions of the industry, most of its suppliers are

countries with oil reserves. A major supply concern for ConocoPhillips is the politics in

oil producing countries. A large portion of ConocoPhillips proved oil reserves come from

foreign countries. Therefore, ConocoPhillips is highly affected by the prices of oil set by

organizations such as OPEC. ConocoPhillips is its own supplier for most of the major

assets the company uses to explore, produce, refine, and marketing. ConocoPhillips

strives hard to have open lines of communication with its suppliers to eliminate

problems. ConocoPhillips seeks suppliers that can uphold its core values and provide

the quality and service needed for the best cost. Additionally, ConocoPhillips recently

purchased one of its suppliers, Burlington Resources, and will help further cut costs.

In total, if ConocoPhillips can maintain the balance between itself and it's

suppliers, it will have lower costs and a leading edge in the industry . This leading edge

could enhance the value of ConocoPhillips not only to itself, but also to its shareholders

and investors. This investing increase could push ConocoPhillips to new heights

Value Chain Analysis/Key Success Factors for the Industry:

The Oil & Gas industry is a highly competitive market. The core products and

services in which this industry markets are Crude Oil, Natural Gas, Jet Fuels, and

Gasoline products. These stated products are commodities in which cost leadership

competitive advantage may be necessary for optimal performance for companies within

the oil and gas business. In order for a company to succeed in the energy industry,

they must obtain several key success factors. The industry’s companies must have

economies of scale and scope, efficient production, and little brand advertising.

Gasoline is a common need of automobile owners will always purchase gasoline

12

regardless of more emphasis on brand advertisement or not. In addition, Oil and gas

commodities are produced in mass quantities. In order for companies to compete for

cost leadership, the increased mass production with higher demands, the more efficient

(cheaper costs) production is necessary for maximized profits.

Competitive Advantage

One of the keys to ConocoPhillips success and its cost leadership strategy is its

efficient production by being able to operate in both the upstream and downstream

production of oil. By having both segments of the production process, ConocoPhillips is

able to cut down on the risk associated with price volatility. Either upstream or

downstream has to make up the difference for the lagging behind of the other.

Currently, with the merger of the two large companies, ConocoPhillips is able to handle

the risks associated with the market due to the size and assets of the company. By

having the upstream portion of the production process, they are able to sell the

unrefined good to a number of different refineries. When supplying crude oil to the

companies own refineries, the efficiency of production are increased. ConocoPhillips

was able to achieve both ends of the production by having the assets needed to be a

leader in both upstream and downstream production. This process would be hard to

duplicate due to the assets needed to explore and produce oil reserves. Because of the

dependency on oil and its by-products, the industry is unlikely to change.

Identifying Key Accounting Policies

ConocoPhillips is an integrated energy company with investments across several

businesses. In order for companies who develop and produce commodities, such as

ConocoPhillips, companies compete under a cost leadership strategy (as stated as a key

success factor). ConocoPhillips constantly strives to maintain an economy of scale and

scope, in addition to many other key success factors. Under accounting policies every

public company, regardless of industry, is required to submit financial statements which

require companies to estimate value and functions of the business. Under their

Management Discussion and Analysis, ConocoPhillips discuss five key areas of critical

13

accounting policies all of which are linked to key success factors of a commodity based

business. Aside from the basic accounting policies, ConocoPhillips has many policies

unique to the energy business. These key areas are divided in functions they

participate in for which they make estimations and value judgments. The five areas

are: [1] Oil and Gas Accounting (actual commodity accounting), [2] Impairment of

Assets, [3] Asset Retirement Obligations and Environmental Costs, [4] Business

Acquisitions, and [5] Projected Benefit Obligations. As each component is discussed,

understand ConocoPhillips’ goal is to improve through sustainable growth. They are still

a growing company and thought mergers, acquisitions and even asset development add

value to ConocoPhillips.

ConocoPhillips core business functions are focused upon the oil and gas

products. As a commodity business, ConocoPhillips is always trying to cut costs in order

to maintain cost leadership (KSF), as costs may be lowered, there must be some way to

keep record of the changes in value. There are special accounting rules that are unique

to the oil and gas industry. Prior to the discovery of proved reserves, attainment of

geological and geophysical seismic information is an expensed as incurred, similar to

research and development costs. Leasehold acquirement costs are capitalized on the

balance sheet until the reserves of oil or gas have been proven. Leasehold acquisition

costs are determinant upon exploration and drilling efforts as the probabilities for

proved reserves are calculated by management. The probability determinants are

heavily weighted in importance as pretax leasehold impairment expenses would be

dramatically affected. The probability percentage is divided by the contractual period of

the leasehold to determine a periodic leasehold impairment charge that is then reported

as an exploration expense. Expenses are important because if they are too high,

income will be understated as ConocoPhillips could potentially pay fewer taxes.

ConocoPhillips is also involved in a lot of exploration to seek out their raw materials for

their finished product. Crude oil, also known as petroleum, is a raw material which is

later sent to the refineries to be processed in to several finished products. These

finished products include: Gasoline, Jet fuel, Natural Gas, Power, and Pet Coke

(asphalt). As stated in the Management Discussion and Analysis, they claim “for

14

exploratory wells drilling costs are temporarily capitalized, or “suspended,” on the

balance sheet, pending a determination on whether potentially economic oil and gas

reserves have been discovered by the drilling effort.” So, wellheads and drilling projects

are not included on the balance sheet until they succeed and discover product. If a

well did not produce a sufficient amount of or any product, they well costs are

expensed as a ‘dry hole’ and reported as an exploration expense on the income

statement. Contrasting to the leasehold acquisition costs, there is no impairment

assessment (depreciation) of the suspended exploratory costs. Exploration is a key

success factor in the business because if they find more raw material for their goods,

than they increase their supply as it also drives the costs of goods sold down.

However, when exploration does not result successfully, the accounting policies of

ConocoPhillips will expense the costs.

ConocoPhillips has many long term assets which will deteriorate as those

depreciations must be accounted for. However, keep note ownership of long term

assets become cost efficient for ConocoPhillips. Although there exist dangers and

scrutiny of low maintenance on refineries, the lower maintenance costs continues to

lower costs. Lower cost is a large business driver especially in commodity industries.

For example, ConocoPhillips has not built a refinery since the 1970s; their refineries

have been around for a significant time period as those refineries (assets) should be

depreciating in value. Long-lived assets used in operations are assessed for impairment

occasionally only if expected future cash flows are significantly decreasing. If the

pretax cash flows are less than the carrying value of the asset group, they will begin to

use the fair value of the asset. ConocoPhillips’ oil and gas reserves are critical to the

business because they are the major assets and products of the company.

ConocoPhillips and every energy company in the oil and gas industry is always under

much scrutiny for environmental and health hazards. ConocoPhillips purpose (mission

statement) is to “responsibly deliver energy to the world”. Not only are there laws

involved with energy emissions from refineries, ConocoPhillips is making an additional

effort to exceed the environmental performance of other companies. ConocoPhillips

undergo large asset retirement obligations and environmental costs which must all be

15

accounted for. Their largest obligations involve removal and disposal of the offshore oil

and gas platforms as those costs are accrued at the installation of the asset. There are

several environmental laws, especially in Alaska, for cleaning of refineries as well as the

underground storage tanks in the U.S. These are all included in the costs of goods.

As a growing business, ConocoPhillips have gone through several mergers and

business acquisitions over the years. mergers and acquisitions of companies allows

ConocoPhillips to run increase efficient production, increasing cost leadership (KSF). In

2001, Conoco Company and Phillips Petroleum 66 merged as one company,

ConocoPhillips. Conoco and Phillips 66 merged in order to maintain their sustainable

growth and increase a significant part of the market share in the energy industry. As a

result of the merger, they recorded the intangible assets such as trademarks, air

emission permit credits, and permit to operate refineries with an indefinite useful life so

they were not amortized. The first step in their mergers, they calculate and compare

the fair value of any reporting units including any goodwill. Many acquisitions are

recorded as goodwill they conduct tests for impairments. ConocoPhillips participates in

a company contribution in their benefit plans. Projected benefit obligations are

recorded as amounts for such obligations (liabilities) on the Balance Sheet as it is also a

benefit expense on the income statement.

Although ConocoPhillips may have several solid accounting policies, some of the

estimations, such as probability of successful reserves, are left up to manager’s

discretion. All of the five areas of the critical accounting policies can be updated and

re-estimated yearly. All of the oil and gas accounting, impairment of assets, business

acquisitions, projected benefit obligations and asset retirement obligations accounting

policies are very clear concerning the process of accounting; however, the components

requiring judgment of manager’s may raise questions.

Assess Accounting Flexibility:

ConocoPhillips has some noticeable amount of accounting flexibility due some

special accounting rules unique to the oil and gas industry. ConocoPhillips, fortunately,

does an outstanding job at disclosing accounting information. The Oil and Gas industry

16

is a unique commodity trading business. As mentioned previously in Key Success

Factors, commodity trading businesses must perform under a cost leadership strategy.

Many cost leadership businesses may have issues with disclosing information in order to

privatize their secrets of efficient production. Because of the amount of accounting

flexibility related to ConocoPhillips’ key success factors the accounting information is

very informative.

Many of the costs relating to exploration and production of oil are estimated by

management, leaving room for flexibility. Acquisition costs that are relatively small are

estimated by management based on a percentage probability the prospect will fail to

find proved oil and gas reserves. The percentage probability is reassessed throughout

the contractual period of the lease and will be adjusted to 100 percent by the end of

the contract if the leasehold is expected to be abandoned or will be adjusted to zero

percent if there is an oil or gas discovery. The percentage probability was about 72

percent and amortized over almost 3 years. If the percentage probability were raised

by 5 percent the impairment expense would increase by $6 million. This leaves

significant room for flexibility when reporting exploration expense for ConocoPhillips.

According to the annual report, proved oil and gas reserves are based on

subjective judgments by engineers. There are authoritative guidelines that must be

met when reporting proved reserves; however, these numbers are inherently imprecise.

A red flag is raised in this area because the subjective judgment is the denominator in

the unit-of-production calculation of depreciation and amortization of the capitalized

costs for that asset. ConocoPhillips annual report states that, “If the judgmental

estimates of proved reserves had been lower by 5 percent pretax depreciation,

depletion and amortization would have been increased by about $131 million.”

ConocoPhillips uses outside actuarial firms to assist in the determination of

projected benefit plan obligations. Of the numerous judgments made on uncertain

future events, the most sensitive element is the judgment on benefit expense. High

quality bonds are used as discount rates are used to determine the benefit expense. A

decrease of 1 percent in the discount rate would increase annual benefit expense by

$105 million.

17

The largest asset retirement obligation is the disposal of offshore platforms,

production facilities in Alaska, and the asbestos reduction at refineries. Many of these

obligations are many decades in the future and involve vague descriptions about which

regulations must be met.

Business acquisitions inherently involve judgmental decisions on the fair value of

individual assets and most importantly goodwill and intangible assets. For determining

the fair value of most assets, ConocoPhillips uses on outside agency, which leaves less

room for flexibility. ConocoPhillips has an alarming amount of room for flexibility in

determining the fair market value of the goodwill from the companies it acquires.

Overall, ConocoPhillips does a fair job at reporting the reasons and expectations of its

valuing of intangible assets.

As mentioned above, the Exploration and Production segments record

depreciation on a unit-of-production basis, therefore depreciable life is varying in this

segment. In the refining and manufacturing segment, facilities are depreciated on a

straight line basis over 25 years, pipeline assets are depreciated over a 45 year life,

service stations and fixed improvements have a 30 year life. Inventories are accounted

for using the first in, first out (FIFO) method, which could lead to ConocoPhillips

reporting a higher net income. ConocoPhillips method for amortizing goodwill over an

estimated time period leaves room for flexibility.

While flexibility does exist in the accounting policies of ConocoPhillips, great care

seems to be made at disclosing the relevant information. Consistency and care are

made when using judgment to make decisions on the key success factors. The strict

guidelines stated when using judgment that affects accounting numbers eases the

concern over the amount of flexibility.

Accounting Strategy

As all companies, ConocoPhillips is required to prepare its financial statements in

conformity with generally accepted accounting principles. Adhering to these principles

requires managers to select accounting policies and make estimates and assumptions

that affect the reported amounts of assets, liabilities, revenues and expenses. It is

18

important to understand that accounting in the energy industry involves making many

estimations of values to future dates. Certain accounting policies that must adhere to

generally accepted accounting policies involve judgments and uncertainties to a degree

that it is likely for different amounts to have been reported if analyzed under different

conditions and assumptions. ConocoPhillips uses accounting flexibility to communicate

the firm’s economic situation and presents its financial status to the best of their ability.

ConocoPhillips uses a conservative approach to its accounting strategy. For example,

they do not record the exploratory drilling sites they own as assets until oil has been

proven to be at that location.

The acquisition of geological and geophysical seismic information, prior to the

discovery of proved reserves, is expensed as incurred. This can be compared to the

research and development expenses of other companies. Leasehold acquisitions costs

and exploratory well costs are capitalized on the balance sheet; pending determination

of whether proved oil and gas reserves have been discovered on the prospect. This is

similar to how other comparable companies account for the components mentioned

above.

As stated in its 2005 10-k, “individual assets are grouped for impairment

purposes based on a judgmental assessment of the lowest level for which there are

identifiable cash flows that are largely independent of the cash flows of other groups of

assets – generally on a field-by-field basis for exploration and production assets, at an

entire complex level for downstream assets, or at a site level for retail stores.” This

means that ConocoPhillips arranges its assets into similar groups, and then evaluates

them for impairment. They choose to do it this way because the business functions of

their assets are so different it would be inaccurate to write down assets as one large

group. The fair value of these assets are usually based on the present values of

expected future cash flows using discount rates in accordance with the risk associated

for that asset group.

When Acquiring companies such as Tosco corporation and Burlington resources,

as well as the merger of Conoco and Phillips, ConocoPhillips chooses to record

intangible assets for trade names and trademarks, air emission permit credits, and

19

permits to operate refineries at indefinite lives and are so not amortized. The recorded

intangible assets for trade names and trademarks, air emission permit credits, and

permits to operate refineries due to the stated mergers and acquisition above total

around $14 billion. During these mergers and acquisitions, a material amount of

goodwill was recoded, which under the accounting rule for goodwill is not amortized.

This means the company believes the intangible assets gained from these transaction

will not depreciate over time and keep their value. In accordance with accounting rules,

ConocoPhillips will have to review goodwill yearly for impairments.

ConocoPhillips uses the equity method for accounts of majority owned, controlled

subsidiaries and variable interest entities when they are the primary beneficiary. They

realize a weighted-average ownership share of a company’s net income each period

and recognize it as equity earnings on their financial statements. This is important to

ConocoPhillips accounting because the more they own of a company, the more earnings

are recognized on their statements. ConocoPhillips has increased its overall ownership

of their subsidiaries over recent years, such as their investment in Lukoil which now

reaches 16.1 percent. As a result, ConocoPhillips’ equity earnings in their financial

statements have been increasing. This has helped contribute to the increase in

ConocoPhillips value over recent years.

Since the merger of Conoco and Phillips in 2002, ConocoPhillips has made no

changes to their accounting policies. After analyzing the financial statements over the

last 5 years, it appears as if there have been no abnormal adjustments to

ConocoPhillips revenue and expenses from quarter to quarter or year to year. This

illustrates that ConocoPhillips Accounting practices have more than likely been

materially correct and honest, which is no surprise as they follow a conservative

accounting strategy. An increase in revenues and expenses is apparent over the past 5

years, but this is probably due to the company’s expansion.

Top executives are offered incentives to increase performance. The

compensation committee of the board of directors decides the appropriate structure of

incentives and amount of compensation for each executive by comparing their

performance to the others. In addition to salary, the top executives are offered long

20

term incentive in the form of stock options and restricted stock units under the

performance share program. The criteria evaluated for these incentives are based on

total shareholder return, improvements in return on capital, reduction of debt,

increased revenue, and overall financial performance.

ConocoPhillips uses their accounting strategy to communicate the firm’s

economic situation and presents its financial status to the best of their ability. It

recognizes its expenses in exploration and capitalizes it expenses that lead to the

discovery of proved oil reserves. It assesses its assets in functionality groups as to

properly value assets and record impairments, which give a clear picture of the

company’s true value. They have been acquiring new companies and recognizing

intangible assets and goodwill at indefinite lives. This has increased the company’s

assets and net income. ConocoPhillips also chooses to offer their executives strong

incentive plans that will improve the company’s financial performance.

Quality of Disclosure

The way a company discloses its information about its financial and accounting

data has a strong impact on the image the company portrays to its potential and

current investors. ConocoPhillips does a detailed job in disclosing its policies both

qualitatively and quantitatively. ConocoPhillips goes into great detail concerning exactly

what the company is doing and what its future plans are; therefore, investors are able

to obtain a fairly good understanding of the true value of the company.

ConocoPhillips operates in many different business segments, and they disclose

specific information about what is going on in each segment. They release information

regarding what percentage of each segment is reflected in the total assets portion of

the balance sheet as well as what contributions each segment adds to net income.

After the segmentation, ConocoPhillips then breaks down each segment to the different

geographical regions and departments that make up the segment.

In the disclosures, the company does reflect where potential negative outcomes

towards the company could arise. For example, ConocoPhillips shows that if they are

unable to find more reserves, the future crude oil and natural gas production would

21

decline. This would then cause a decrease in cash flows and results from operations.

They also state that the success of the company is directly related to the price of crude

oil, natural gas, and refining costs, and that decreases in the price of these would cause

negative operating results. However, the figure that the company has tied in with this

negative information does not include any quantitative data about the effects of this

potentially harmful data. The managers do not disclose information on neither the

probability of these possible negative effects nor the potential harm they could cause

the company. Nevertheless, by ConocoPhillips disclosing this negative information

shows that the company is not trying to embellish the information disclosed by

releasing only positive data to the public.

In ConocoPhillips’ financial statements they have a very detailed disclosure that

states all there procedures as far as stating how they handle foreign currency

conversion, asset retirement obligations, and goodwill. As a company ConocoPhillips is

very transparent based on the information in they release in their disclosures, which

allows for an easier judgment to be made about the proper value of the company.

Screening Ratios

The sales manipulation diagnostics listed below include three net sales

manipulations to help identify potential red flags in reporting sales. The core expense

manipulation listed below includes four core expense manipulations that will help

identify red flags.

Net Sales / Cash from Sales

1.05

1.10

1.15

1.20

1.25

1.30

2001 2002 2003 2004 2005

22

Net Sales / Cash from Sales

ConocoPhillips net sales to cash from sales ratio is decreasing steadily over the

past five years. Cash from sales is determined by subtracted the next year’s accounts

receivable and the current years account receivable from the current year’s net sales.

This diagnostic checks for unexplained increases in sales. Since, the trend decreasing

over the entire period no red flag is seen.

Net Sales / Net Accounts Receivables

0.00

5.00

10.00

15.00

20.00

25.00

2001 2002 2003 2004 2005

Net Sales / Accounts Receivables

Net sales to accounts receivables for ConocoPhillips fluctuates slightly over the

five year time period but remains in close range. The dip in ratio in 2002 is most likely

due to a dramatic increase in accounts receivable for the year. The net sales to

accounts receivable is looking for any asset distortions. The overall stability of the ratio

reduces any concerns over the yearly noise and eliminates any concern for a red flag.

Net Sales / Inventories

0.00

10.00

20.00

30.00

40.00

50.00

60.00

2001 2002 2003 2004 2005

23

Net Sales / Inventories

ConocoPhillips’ net sales to inventories have been steadily increasing over the

last five years. Concern is raised over sales manipulation when net sales are increasing

at a rate that significantly outpaces inventory growth. Upon closer examination the

significant net sales growth can be attributed to the dramatic rise in oil prices over the

last five years, which is typical of the oil and gas industry. The stability of the growth is

encouraging for ConocoPhillips.

Net Sales / Assets

0.000.200.400.600.801.001.201.401.601.80

2001 2002 2003 2004 2005

Net Sales / Assets

The net sales to assets ratio diagnostic is checking for a decreasing ratio that

would suggest a core expense manipulation. The fact that net sales to assets is

increasing over the time period would remove any red flag potential. Furthermore, the

fact that the net sales to assets ratio increases with net sales to inventories would be

ease concerns even more.

24

CFFO / OI

0.000.050.100.150.200.250.300.350.400.450.50

2001 2002 2003 2004 2005

Cash Flows from Operating Activities / Operating Income

Cash flows form operations is another core expense manipulation that would

raise concerns if dramatic changes were noticed. The slight decrease in the ratio can

be attributed to the faster growth in operating income. The increase in operating

income has already been explained in previous ratios by the increase in sales. The

slight movements in the ratio combined with the knowledge of the increase in net sales

raises no red flags.

CFFO / NOA

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

2001 2002 2003 2004 2005

25

Cash Flows from Operating Activities / Net Operating Assets

The overall increase in the cash flows from operations to net operating assets is

consistent with previous diagnostics. The decrease in 2002 is consistent, but more

obvious, with the net sales to assets model. The CFFO / NOA model should be close to

sales to assets and their consistency should ease concerns over any possible red flags.

The overall increase in the diagnostic reflects favorably on ConocoPhillips.

Pension Expense / SGA

0.00

0.20

0.40

0.60

0.801.00

1.20

1.40

1.60

1.80

2001 2002 2003 2004 2005

Pension Expense / SG&A

Pension expenses to SG&A expenses over the five year period remained mostly

stable. The slight decrease in the ratio is attributed with the slightly larger growth in

SG&A expenses. The overall stability reduces concerns over any core expense

manipulations. With no dramatic changes in the diagnostic no red flags are warranted.

Screening Ratio Conclusion

Overall the manipulation diagnostics warrants no red flags. The only possible

red flags noticed would be the increase in sales over the last five years. With the nearly

195% percent growth in crude oil prices since 2001, most of the increase in sales can

be answered. The excellent disclosure of information helps to further reduce concerns

26

over red flags. The manipulation diagnostic turns up no red flags and shows

ConocoPhillips performing well over the last five years.

Identify Potential Red Flags:

Throughout the past five years of evaluation, ConocoPhillips’ statements show

little deviation from one year to the next and in turn raise few red flags. These

statements are analogous with regards to evaluation techniques and inventory

accounting.

With regards to inventory, ConocoPhillips exercises the LIFO system for sale of

crude oil, petroleum products, and Canadian Syncrude inventories. This practice is on

par with other competitive firms in this industry. Also similar is ConocoPhillips’ FIFO

evaluation of marketing merchandise (t-shirts, mugs, umbrellas, etc.) This evaluation

method is also common among competitors. These methods have been used over the

previous four years and haven’t deviated thus resulting in accurate picture.

ConocoPhillips does not amortize goodwill. Instead, they evaluate goodwill at

least once a year and adjust goodwill according to fair market value. If goodwill is less

than the hypothetical purchase price, goodwill is then written down to the new amount.

ConocoPhillips acquired about $12,000 of goodwill from the merger of the two firms in

2002. In 2004, ConocoPhillips wrote off, for the first time, goodwill acquired through

the 2002 merger of Conoco and Phillips 66. If not, goodwill is not changed until the

next evaluation. What provides some comfort is the evaluation is at least once per year.

If goodwill tends to shift according to fair market value, the shift will be caught in a

subsequent evaluation. Other intangibles are depreciated with the straight line method.

A major factor in the operations of ConocoPhillips is the derivatives market.

This market is where one potential red flag arises. Due to the high volume of futures,

options, and other derivative trading that occurs, ConocoPhillips has the ability to hold

certain derivatives for the trading market. The gains or losses from trading activities

are recorded in sales or operating revenues. Similar to Enron, ConocoPhillips has the

ability to increase revenues without actually increasing profits, thus providing a false

27

picture. Statistical analysis of ConocoPhillips has proven against this fact, but the

option is always there which is a potential red flag.

Another red flag that arises is ConocoPhillips’ Pretax Leasehold Impairment

Expense or as reported on the Income Statement as Property Impairments. This

expense account is a potential red flag because it is evaluated by “exploratory

experience and management’s judgment.” Their judgment is based on whether they

believe exploration for oil and gas will prove to be successful (finding oil or gas) or if

exploration will be abandoned. If management “estimates” the failure percentage to be

low, the impairment expense will be less resulting in higher earnings and vice versa.

This substantial expense account is solely based on judgment and in turn is subject to

personal biases.

Although ConocoPhillips is equally comparable year after year, there are a few

red flags that exist. The red flags not only exist with accounting policy but also with

management’s judgment. Due to similar faults in the oil and gas industry, these red

flags should appear relatively quickly.

Corrections to Accounting Distortions:

After looking through ConocoPhillips’ financial statements, there were few

accounting policies that seemed to cause drastic concern. The company has not made

serious changes to their accounting procedures within the last few years. In several

cases the managers are given the duty to estimate values and probabilities.

One example that could be a potential accounting problem is the manager’s

compensation and incentive plans are based upon the performance shown on the

financial statements, a slight biased in the estimations could cause need for concern.

For example, the company’s use of estimations in their determining of potential oil and

gas reserve failure is one that could lead to a serious flaw on their financial statements.

If the manager was to understate the impairment of assets expense, this would cause

the net income of the company to be overstated. This would then cause the retained

earnings showing up in owner’s equity to be overstated as well, which leads to an

28

overstatement of the assets. The company would understate the impairment to show

shareholders an increase in value.

To correct this overstatement of assets, there would need to be a decrease in

assets to correct the asset portion, followed by an adjustment made to the equity

portion to reflect the after-tax cost of impairment. Tax effect adjustments would be

shown in then be shown in company’s deferred tax liability.

Since we could find few immediate threats shown by ConocoPhillips and their

accounting policies, only a few hypothetical situations would cause the need for

corrections to be made. By using less estimation in the future the company could cut

down on the need for potential adjustments to be made.

Ratio Analysis and Forecast

The purpose for the Ratio Analysis and Forecast section is to provide a window in

which to view ConocoPhillips in the past, present, and future based on factors of

liquidity, profitability, and capital structure. It will also show comparisons between

Exxon, Chevron, and BP as well as the industry average. The 10 year forecast of the

Income Statement, Balance Sheet, and Statement of Cash Flows will provide an

equitable evaluation of ConocoPhillips’ future financial performance. With the section

being divided into two sections: Financial Ratio Analysis section (trend and cross

sectional analysis) and the Forecasting Methodology Section, it will provide a

comprehensive and full future evaluation of ConocoPhillips.

Financial Ratio Analysis

The purpose of liquidity analysis is to provide the investor an idea of if the firm

can meet its liability demands. The purpose of the profitability analysis is to determine

how the firm is doing with the sales generated. The capital structure analysis lets

investors know how the firm raises capital. The financial ratio analysis is most

beneficial when comparing firms to other firms and industries.

29

Liquidity Analysis

2001 2002 2003 2004 2005 Current Ratio

(CA/CL) 1.35 0.85 0.80 0.96 0.92

Quick Asset Ratio

(QA/CL) 0.28 0.37 0.39 0.65 0.66

Accounts Receivable Turnover (Sales/AR)

22.27 13.06 21.00 15.58 15.36

Days Sales Outstanding (365/ARTO)

16.39 27.95 17.38 23.43 23.77

Inventory Turnover

(COGS/INV) 5.59 9.85 17.05 24.60 33.55

Day’s Supply of Inventory

(365/INVTO)

65.29 37.07 21.41 14.84 10.88

Working Capital

Turnover (Sales/CA-CL)

14.93 (29.90) (37.28) (242.33) (104.96)

Liquidity Analysis (contd.)

ConocoPhillips (COP) has recently had a large merger with Philips66 and has

recently acquired Burlington Resources. These two factors have affected COP’s liquidity

due to the lag time attributed to the lengthy process of closing such acquisitions. The

current ratio and quick asset ratio are on the rebound as well as their accounts

receivable turnover. COP has made a fine effort to turnover their inventory and

decrease their day’s supply of inventory which, as a result, has improved over the

industry average. The last thing affecting COP is working capital turnover. The

increasing of current liabilities in relation to current assets has had a negative affect for

30

COP from 2002 to 2004 but shows an improvement and the end of 2005. This

improvement is related to the large number of sales recognized in that year.

Profitability Analysis

2001 2002 2003 2004 2005 Gross Profit

Margin (GP/Sales)

34.67% 25.66% 29.00% 28.75% 27.20%

Operating Expense

Ratio (Operating

Expense/Sales)

3.67% 4.44% 2.65% 2.07% 1.59%

Net Profit Margin

(NI/Sales) 6.64% (0.52%) 4.45% 5.94% 7.38%

Asset Turnover (Sales/TA)

0.71 0.74 1.27 1.47 1.71

Return On Assets (NI/TA)

4.72% (0.38%) 5.67% 8.75% 12.64%

Return On Equity (NI/OE)

11.58% (1.00%) 13.62% 19.03% 25.66%

There are 4 major factors that contribute to the overall profitability of COP.

These 4 are: Operating Efficiency, Asset Productivity, Return on Assets, and Return on

Equity. The Operating Efficiency of COP has been on the decline over the past 5 years.

The Gross Profit Margin has slipped from 2001 to 2005 at almost 7.5%. The Net Profit

Margin has also fell with the exception of 2005 showing a slight increase. Mergers and

acquisitions as well as a high proportion of total sales derived from less profitable

product line could be attributed to this decline. Asset productivity has been a positive

factor for COP. With a steady increase over the past 5 years, current asset turnover

shows that each $1 of assets has produced $1.71 of sales. This trend is also seen by

the return on assets with the exception of 2002 in which the merger occurred which

31

resulted in a Net Loss for the year. The final factor affecting profitability is return on

equity. Again, despite the Net Loss experienced in 2002, ROE has increased extensively

from 2002 to 2005.

Capital Structure Analysis

2001 2002 2003 2004 2005

Debt To Equity Ratio (Total

Liability/Owner’s Equity)

1.41 1.57 1.37 1.15 1.01

Times Interest Earned

(EBIT/Interest Expense)

10.77 3.03 10.98 27.36 48.15

Debt Service Margin

(OPCF/NP) 80.89 5.86 6.50 18.92 10.03

The Capital Structure of COP refers to the sources of financing used to acquire

assets. When considering Capital Structure, an investor must consider two things: the

amount of debt to owner’s equity and the ability to pay the principal and interest on

debt. COP has shown improvement over the 5 year trend in relation of debt to equity.

At the end of 2005, COP has $1.01 of liabilities to every $1.00 of equity. This shows

that they have a slightly larger liability in comparison to owner’s equity. Times interest

earned relates to the amount of income from operations to cover interest charges on

debt. The debt service margin relates to cash provided by operations to cover the

installment payments on the principal. COP has managed to maintain positive numbers

in both respects showing that COP at the end of 2005 has $48.15 of income from

operations to pay every $1.00 of interest expense. Similarly, at the end of 2005 COP

has $10.03 of cash provided by operations to cover each $1.00 of long-term debt. In

respect to these two numbers, COP has the ability to cover the interest and the

principal of their debt incurred.

32

Sustainable and Internal Growth Rate

SGR = IGR (1 + Debt/Equity) IGR = ROE (1 – Dividend Payout Ratio)

The sustainable and internal growth rates are two ways to evaluate COP’s ratios

in a comprehensive manner. The sustainable growth rate is a rate in which a firm can

grow while keeping its profitability and financial policies unchanged. The internal

growth rate is the highest level of growth achievable without obtaining outside

financing. The 5 year trend represented by these ratios indicates that COP has the

ability to grow in the up coming years to a certain point. As usual, growth will

eventually succumb to outside factors at some point and reach its maximum point. The

SGR and IGR will help to provide an accurate forecast for COP in the upcoming years.

Cross-Sectional Analysis

The integrated oil and gas industry has a number of large companies in the

market that are fiercely competing for market share. After doing ratio analysis over a

few companies in the industry for the past five years, ConocoPhillips’ financial stance

varies with what is going on in the industry. ConocoPhillips’ is becoming better in some

areas, while struggling with others.

Internal Growth Rate

2001 2002 2003 2004 2005 Average

ROE 11.58% -1.00% 13.62% 19.03% 25.66% 13.78%

DPR 24.26% 231.86% 23.66% 15.16% 12.11% 61.41%

IGR 8.77% 1.32% 10.40% 16.15% 22.55% 11.84%

Sustainable Growth Rate

2001 2002 2003 2004 2005 AVG

IGR 8.77% 1.32% 10.40% 16.15% 22.55% 11.84%

D/E 1.41 1.57 1.37 1.15 1.01 1.30

SGR 21.14% 3.39% 24.65% 34.72% 45.33% 25.84%

33

Current Ratio

0.50

0.70

0.90

1.10

1.30

1.50

1.70

COP 1.35 0.85 0.80 0.96 0.92

Industry 0.96 0.96 1.09 1.28 1.31

BP 0.82 0.83 0.85 0.91 0.97

Chevron 0.89 0.89 1.21 1.52 1.37

ExxonMobil 1.18 1.15 1.20 1.40 1.58

2001 2002 2003 2004 2005

Inventory Turnover Ratio

0.00

10.00

20.00

30.00

40.00

COP 5.59 9.85 17.05 24.60 33.55

Industry 16.54 15.21 18.04 20.66 22.06

BP 15.15 11.41 12.81 13.21 12.39

Chevron 20.54 20.72 26.93 31.65 31.05

ExxonMobil 13.92 13.48 14.39 17.12 22.75

2001 2002 2003 2004 2005

ConocoPhillips’ ability to pay off there debt differs from what is going on in the

industry. The industry

average of current assets over

current liabilities over the past five

years has been steadily

increasing; however,

ConocoPhillips proportion of

current assets over current

liabilities took a major

decrease during the merger in

2001, but they have started to turn it around with what the industry is doing.

ConocoPhillips’ relationship of the amount of cash or other easily converted assets to its

current liabilities is increasing as is the industry, but it is just at a much smaller rate

than its competitors. Overall, ConocoPhillips ability to payoff its debt is not preferable

in many industries, but in this large industry the amount of assets on hand is often

times not enough to cover its liabilities.

In the integrated oil and gas

industry, companies’ ability to

collect on receivables over

the past five years has been

around thirty six days to

collect, where as

ConocoPhillips’ has been

able to keep there accounts

receivable turnover well

below the industry average, at an average of around twenty two days. ConocoPhillips’ is

starting to decrease its efficiency with accounts receivable as its accounts receivable

turnover has started to move towards the average of the industry. Since the merger of

Conoco with Phillip’s, the company has been able to drastically decrease the amount of

days that inventory is on hand, in 2001 the company was the worst in the industry in

34

terms of inventory turnover. However, during the last five years the company has been

able to not only catch up with the industry, but has surpassed its competitors and is

now the leader. ConocoPhillips’ working capital turnover is a major cause for concern

for the company due to the greater amount of liabilities than assets. ConocoPhillips has

a negative working capital turnover since the merger; however, the company’s

competitors also maintain negative working capital turnover ratios, but not near as

severe as ConocoPhillips. In the integrated oil and gas industry, ConocoPhillips has

become the most efficient of the companies in both its inventories and accounts

receivables; nevertheless, the company does need to work on its working capital by

either decreasing its liabilities or increasing sales to get back to a positive number.

ConocoPhillips gross profit margin has been around thirty percent of its sales over the

last five years, where as the industry averages just above that by averaging around

thirty-five percent. Operating costs in the integrated oil and gas industry are a very

miniscule part of a company’s total sales; therefore, the ratio between the two is very

low. ConocoPhillips maintains a lesser ratio than the other companies at an average of

around .03 to the industry average of .07. This shows how the company is minimizing

its operating costs as it is increasing its sales. ConocoPhillips net income margin took a

decline whenever the merger took place, but has been steadily increasing ever since.

However, ConocoPhillips is still trailing its Competitors in terms of net income margin.

ConocoPhillips was not the only company that showed losses in 2002, both Chevron and

Exxon had a decrease from the year before. ConocoPhillips return on assets and return

on equity has constantly remained below the industry average throughout the past five

35

Debt to Equity

0.60

0.80

1.00

1.20

1.40

1.60

1.80

COP 1.41 1.57 1.37 1.15 1.01

Industry 1.13 1.30 1.24 1.14 1.12

BP 1.16 1.41 1.54 1.45 1.49

Chevron 1.28 1.45 1.24 1.06 1.01

Exxon 0.96 1.05 0.94 0.92 0.87

2001 2002 2003 2004 2005

years. This shows how the company is struggling to capitalize on its assets and equity

to generate income. Recently the company has shown considerable improvement in

both categories and is starting to gain ground on its competitors in these areas. As a

whole, ConocoPhillips went through a decline in profits during 2002, but is slowly

rebounding back and has been able to catch up with its competitors in terms of

profitability.

The capital structure of ConocoPhillips’ consists of a great amount of outstanding

liabilities. Over the past five years the company has primarily used debt to finance its

assets, which is shown in the debt to equity ratio. However, ConocoPhillips’

competitors also primarily use debt to finance there operations, but not to the same

extent that ConocoPhillips’ does. In more recent years the company has decreased the

amount of debt used and is now at below what the industry average is. The industry

average for times interest earned over the past five years is 52.63 times, where as

ConocoPhillips average for that same time frame was 20.06 times. This shows that

ConocoPhillips is not near as successful with its income from operations in relation to its

interest expense. However, the company is starting to gain ground and become more

like its competitors in recent years. ConocoPhillips’ is very successful in terms of its

ability to provide cash from operations to pay off its annual principal payments.

ConocoPhillips has maintained its debt service margin above the industry mean for the

last five years. In terms

of the company’s capital

structure, ConocoPhillips

had a substantial amount

of debt five years ago,

but they have been able

to decrease that amount

and become more

efficient with their use of

debt. Taken as a whole,

36

the company was struggling in all areas five years ago, but has made steady

improvement since to now become a leader in the integrated oil and gas industry.

Financial Statement Forecast Analysis

After compiling all the data for the financial statements and ratios, trends,

growth, and averages were looked for to forecast into the future. Using growth

analysis we could look at the balance sheet and see that total assets had grown at a

reasonable rate in 2005, and according to Value Line analyst estimates, a rate that

should be maintained over the next 2 years. Based on analyst estimates that

ConocoPhillips and the Oil and Gas Industry would see less growth in the 5 to 10 year

time period, we reduced the growth rate for total assets to eight percent. Noticing that

inventory averaged a sustainable 4.4% of total assets over the last 3 years, inventory

growth could be forecasted for the next 10 years. Using other liquidity, leverage, and

capital structure ratios most of the remaining balance sheet data could be forecasted.

Using the average Inventory Turnover ratio, Cost of Goods Sold could be

forecasted by multiplying the average inventory turnover by the forecasted inventory

for the year being estimated. The average Total Asset Turnover ratio could be used to

forecast Sales. According to Value Line analyst estimates, Sales are expected to dip in

the year. The dip in sales makes sense, considering the recent drop in oil prices. With

Sales and Cost of Goods Sold forecasted Gross Profit could be found for the entire ten

year time period. Continuing to use averages and financial ratios the remainder of the

income statement could be forecasted.

37

Because the Oil and Gas industry is so volatile and profitability is partially

determined by such factors as the weather and foreign politics, developing a reliable

growth rate for extended time periods is difficult. The large degree of uncontrollable

volatility makes using averages to forecast data a weakness to our forecasting method.

The skyrocketing oil prices over the last five years have created growth rates that can

not possibly be continued for the next 10 years. Using a technical analysis of charts it

appears as though that prices have reached a plateau and using recent growth rates

should be more reliable than rates from earlier years. Since Total Assets are the

foundation for the Common Sized Balance Sheet, using adjusted growth rates for Total

Assets will allow for reasonable growth rates to be used over the ten year time period.

A major weakness to this method is that Sales have been so volatile over the past 5

years, that forecasting further out than two years becomes a guessing game. The

tremendous growth in the industry makes forecasting using recent growth unreliable.

Using averages over the last five years and reducing growth rates to more reasonably

sustainable amounts helps to take out some of the inherent risks associated with

forecasting a company in such a volatile industry.

38

Valuation Analysis

To value ConocoPhillips, a variety of valuation models were used to determine if

ConocoPhillips is overvalued, undervalued, or fairly valued. The first method used to

value ConocoPhillips was the Method of Comparables model. Next, the cost of debt and

equity was determined to estimate a weighted average cost of capital. After, finding

the cost of capital, the dividend discount, free cash flow, residual income, abnormal

earnings growth, and long-run ROE/RI perpetuity models were used to determine the

intrinsic value of ConocoPhillips.

Method of Comparables

The first and easiest valuation model used was the Method of Comparables

model. This model is easy

to use because the model

does not require the use of

forecasting, estimating cost

of capital, or finding present

values. We used the earnings per share, book value per share, and dividends per share

for the years 2004 and 2005. We compared competitors BP, and Chevron to find the

value of ConocoPhillips.

We used the 2004

price per share divided

by the 2004 earnings per

share to determine the

2004 P/E trailing. We

then used the 2004 price and 2005 estimated earnings to determine the P/E forward.

The average was taken of both competitors to determine the industry average. After

finding the industry average ConocoPhillips’ corresponding multiple was used to

determine the price of ConocoPhillips.

2004 EPS BPS DPS PPS

ConocoPhillips 4.93 25.92 0.75 43.42

BP 4.14 23.71 1.66 57.93

Chevron 6.28 21.47 1.54 52.51

2005 EPS BPS DPS PPS

ConocoPhillips 8.21 32.00 0.99 58.18

BP 5.48 24.82 2.09 64.22

Chevron 6.54 28.07 1.75 56.77

39

After computing the average price-to-earnings per share trailing and forward for

the industry and multiplying the average by the earnings per share, the price for

ConocoPhillips was found to be overvalued. The industry average price-to-book was

found and multiplied by ConocoPhillips’ book value to determine that the price per share

was overvalued. The industry average dividend per share was used to determine that

the price per share for ConocoPhillips is undervalued. The overall reliability for the

Method of Comparables model was found to be less than desirable and inconsistent.

Comparables (COP)

P/E Trailing

P/E Forecast P/B D/P P/S

2004 Avg. 11.18 10.20 2.44 0.03 0.72 2005 Avg. 10.20 8.66 2.30 0.03 0.76 COP Price

(2004) $55.13 $50.31 $63.37 $25.79 $67.72 COP Price

(2005) $83.73 $71.13 $73.75 $31.39 $94.03

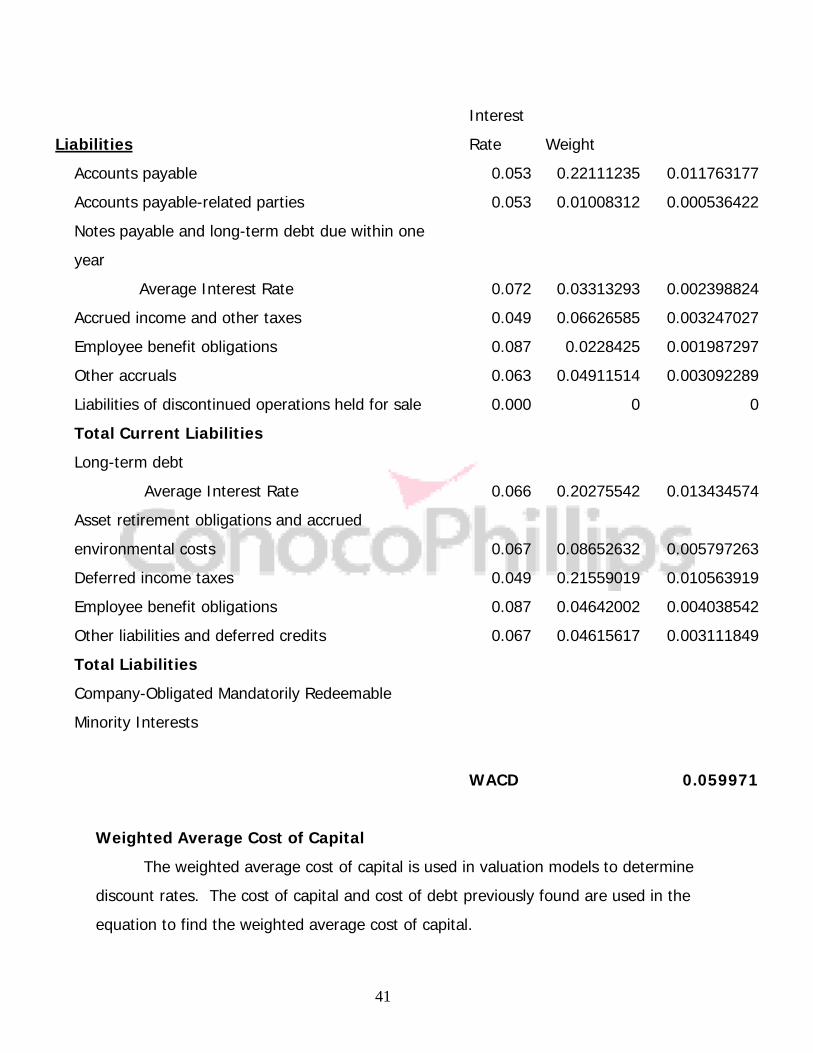

Cost of Capital

The cost of capital and the factors that make it up are some of the most

important calculations because they are the discount rates used to find present values

on some of the most important models. The cost of equity is found by using the CAPM

model. Beta is estimated by running a regression of ConocoPhillips returns and S&P

500 returns. The cost of debt is found by using a weighted formula. Finally, the

weighted average cost of capital is found by using an equation and both costs of equity

and debt.

Cost of Equity

The cost of equity is found using the capital asset pricing model. The CAPM

model uses market risk premium, risk free rate, and beta to determine the cost of