study on automobile market of india

TRANSCRIPT

Page | 1

Study on Automobile Market in India,

Car loan and finance

SUBMITTED BY: Priyank Thada

ENROLLMENT NO.: A30806414018

COURSE: BBA

BATCH: 2014-2017

AN INTERNSHIP PROJECT SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE

INTERNAL EVALUATION.

SUBMITTED TO

GUIDE NAME: Dr. NILESH PANDYA

INDUSTRY GUIDE NAME: Mrs. DARSHINI SHETH

& Miss HELI SHAH

COLLEGE NAME: AMITY GLOBAL BUSINESS SCHOOL

Page | 2

CERTIFICATE FROM FACULTY GUIDE

This is to certify that work entitled project “STUDY ON AUTOMOBILE MARKET IN

INDIA, CAR LOAN AND FINANCE” is done by the PRIYANK THADA student name

under my guidance and supervision for the partial fulfilment of degree of BBA 2014-17,

AMITY GLOBAL BUSINESS SCHOOL, AHMEDABAD.

To the best of my knowledge and belief the thesis:

Embodies the work of the student itself.

Has duly been completed.

Fulfils the requirements of the rules and regulations relating to the summer internship

of the institute.

Dr. Nilesh Pandya

Faculty Guide

Amity Global Business School, Ahmedabad

DATE FACULTY GUIDE SIGNATURE

Page | 3

DECLARATION

I Priyank Thada hereby declare that the project entitled “Dissertation” on “STUDY ON

AUTOMOBILE MARKET IN INDIA, CAR LOAN AND FINANCE”, is a genuine work

of BBA semester 5

To the best of my knowledge any part of this context has not been submitted earlier for any

degree diploma or certificate examination. I also declare that all the data, charts, diagram and

tables all are facts and genuine and best of my work. All data are genuine and collected by

me only and this project is not copy or theft from any other source of information.

Priyank Thada

A30806414018

BBA semester 5th

AGBS Ahmedabad

Page | 4

ACKNOWLEDGEMENT

I express my sincere thanks to Dr. Prashant Saxena, Dean, Amity global business school,

my project guide Dr. Nilesh Pandya, professor and my industry guide Mrs. Darshini Sheth

& Miss Heli Shah, back office coordinator, Pioneer Finmart for guiding me right from the

inception till the successful completion of the project. I sincerely acknowledge her for

extending their valuable guidance, support for literature, critical reviews of project and the

report and above all the moral support.

Without their cooperation and support, this study would never have been possible.

Page | 5

PREFACE

In this development and dynamic world, I feel proud for being a student of BBA programmed

at Amity global Business School Ahmedabad. The summer training in the BBA course is

the major event that gives you an insight into the expectations that a company has from the

BBAs. It provides a pre working experience for a student and gives enough exposure so that

one can give his/her best in the organization which he/she joins in the future. Due to ever

increasing competitiveness in the market today the specific skills of management are always

called for.

For this project my training place was PIONEER FINMART. During my study I got enough

information. This report is purely based on what I worked and analysed during me training.

This project is a summary of the information gathered during the study. I am confident that

my sincere effort and special attention will justify the subject in the report.

Page | 6

Executive summary

Demographically and economically, India’s automotive industry is well-positioned

for growth, servicing both domestic demand and, increasingly, export opportunities. A

predicted increase in India’s working-age population is likely to help stimulate the

burgeoning market for private vehicles. Rising prosperity, easier access to finance and

increasing affordability is expected to see four-wheelers gaining volumes, although two

wheelers will remain the primary choice for the majority of purchasers, buoyed by greater

appetite from rural areas, the youth market and women.

Domestically, some consolidation or alliances might be expected, driven by the need

for access to better technology, manufacturing facilities, service and distribution networks.

The components sector is in a strong position to cash-in on India’s cost-effectiveness,

profitability and globally-recognized engineering capabilities. As the benefits of

collaborations become more apparent, super-specialists may emerge in which the automobile

is treated as a system, with each specialist focusing on a sub-system, akin to the IT industry.

Though this approach is radical, it could prove an important step in reducing complexity and

investment requirements, while promoting standardization and meeting customer demands.

Could prove an important step in reducing complexity and investment requirements, while

promoting standardization and meeting customer demand.

Manufacturers are already planning for the future: early advocates of technological

and distribution alliances have yielded generally positive results, enabling domestic OEMs to

access global technology and experience, and permitting them to grow their ranges with

fewer financial risks.

This exciting outlook for the industry is set against a backdrop of two potentially

game-changing transportation trends – the gradual legislative move towards greener, gas-

based public transport vehicles, and a greater requirement for urban mass mobility schemes to

service rapidly-expanding cities.

Green revolution: In a price-conscious economy such as India’s, the shift towards

green vehicles will be slow unless spurred by government mandates. Although the

major players are already equipped with the necessary capabilities to develop cleaner

Page | 7

vehicles, they do not see much merit in commercializing these technologies until the

green revolution gains momentum – most likely through changes in political

legislation – and it achieves the market scale required for commercial viability.

Mobility revolution: Use of public transport in India has waned as private vehicle

ownership has boomed, but increasing strain on the road infrastructure in major cities

means public investment is likely in Urban Mass Mobility Schemes such as metro

systems and buses. The automotive industry is unlikely to lose much of its customer

base in the near-term, even as these schemes become more prevalent, because the

socio-economic statement of car ownership will continue to make private vehicles

desirable. At present there is a lack of clarity in the automotive industry over the role

it will play in any mobility revolution. Although some industry experts believe the

impact of the mobility revolution will be minimal in the short-term, there may be

opportunities for manufacturers to become involved with the public sector in areas

such as improving links between different modes of transport.

Page | 8

Sno. Contents Page no.

Acknowledgment 4

Preface 5

Executive Summary 6-7

1. Introduction 9

1.1 Background of study 9

1.2 Objectives of study 31

1.3 Scope of study 31

1.4 Hypotheses & Limitations of study 32

2. Research Methodology 33-38

3. Analysis 39-43

4. Findings 44

5. Suggestions 45

6. Conclusion 46

Bibliography 47

Page | 9

Chapter 1

Introduction

Automobile Market in India:

The automotive industry in India is one of the largest in the world with an annual production

of 23.37 million vehicles in FY 2014-15, following a growth of 8.68 per cent over the last

year. The automobile industry accounts for 7.1 per cent of the country’s gross domestic

product (GDP). The Two Wheelers segment, with 81 per cent market share, is the leader of

the Indian Automobile market, owing to a growing middle class and a young population.

Moreover, the growing interest of companies in exploring the rural markets further aided the

growth of the sector. The overall Passenger Vehicle (PV) segment has 13 per cent market

share. India is also a prominent auto exporter and has strong export growth expectations for

the near future. In FY 2014-15, automobile exports grew by 15 per cent over the last year. In

addition, several initiatives by the Government of India and the major automobile players in

the Indian market are expected to make India a leader in the Two Wheeler (2W) and Four

Wheeler (4W) market in the world by 2020.

History:

In 1897, the first car ran on an Indian road. Through the 1930s, cars were imports only, and in

small numbers. An embryonic automotive industry emerged in India in the 1940s. Hindustan

Motors was launched in 1942, Long-time competitor Premier in 1944, building Chrysler,

Dodge, and Fiat products respectively. Mahindra & Mahindra was established by two

brothers in 1945, and began assembly of Jeep CJ-3A utility vehicles. Following independence

in 1947, the Government of India and the private sector launched efforts to create an

automotive component manufacturing industry to supply to the automobile industry. In 1953,

an import substitution programme was launched, and the import of fully built-up Cars began

to be restricted.

Page | 10

The Indian automobile industry has seen interesting dynamics in recent times with the effect

of the global downturn, followed by recovery in domestic demand. The future of the industry

in the medium term based on current trends is analysed here along two broad themes in the

global automobile industry:

Growth

Consolidation

Growth: India’s automobile market has grown steadily over the last seven to eight years,

with the exception of the previous two years where the effects of the global downturn were

felt, primarily in sales of commercial vehicles. However, even during the downturn, the two

wheeler and three-wheeler segments, which were until then experiencing low growth or

losing volumes, bucked the trend.

While quite a few new vehicles launched in the Indian market have been developed

locally, vehicle affordability remains a significant concern as seen in Figure 6. Although the

price of an average motorcycle in India (about USD 900) is comparable to the average per

capita income, the prices of passenger cars have a long way to go. Although the entry level

car (Nano) is priced at around USD 2,500, the passenger car market could grow multi-fold if

there is a break-through of another price level in the years to come.

Vehicles based on alternative fuels remain another area of interest for both consumers

and companies. Reva4, a pioneer in electric cars, remains an exception in the area of electric

vehicles in India, although in two-wheelers there are multiple offerings, none of which have

as yet taken off in terms of volume. Although both commercial vehicles and passenger

vehicles running on CNG are gaining popularity among transport service providers and

consumers due to their lower cost of operation, much more needs to be done to improve the

fuelling infrastructure before CNG vehicles become more mainstream. This report explores

this theme in detail in the section on Green Revolution.

While India remains predominantly a cost-conscious market, profitable niches are

available for the products which address specific needs. One example is the growth in the

sales of gearless scooters, as seen in Figure 7. Of these, most of the scooters are in the 75-

Page | 11

125cc sub-segment5, often targeted at young people and women in particular. The growing

population, a significant proportion of which will be of working age over the next decade, is

another source of demand to most automobile companies.

Consolidation: As India seeks to become one of the world’s largest automobile markets, it is

interesting to look at its evolution over the years. India’s attraction as a destination for

automobile manufacturers has been underscored by the number of new manufacturers

entering the country over the last two decades. Unlike in several markets, the number of

manufacturers has continued to grow in India over the years across vehicle segments. “Global

consolidation is a natural process of business alignments based on technologies and market

opportunities,” says Daimler’s Marc Llistosella. “The Indian market is evolving as the next

big opportunity and players from across the world see it as a natural extension of their

business domain. And Indian players in the automotive component sector are now viewing

the entire global market as an opportunity. With high skill levels and a competitive

environment, they are no longer restricted to viewing India alone.”

Manufacturing Facilities:

The majority of India’s car manufacturing industry is evenly divided into three clusters.

Around Chennai is the southernmost and largest, with a 35% revenue share, accounting for

60% of the country’s automotive exports, and home of the India operations of Ford, Hyundai,

Renault, Mitsubishi, Nissan, BMW, Hindustan Motors, Daimler, Caparo, Mini, and Datsun.

Near Mumbai, Maharashtra, along the Chakan corridor near Pune, is the western cluster, with

a 33% share of the market. Audi, Volkswagen, and Skoda are located in Aurangabad.

Mahindra and Mahindra have an SUV and engine assembly plant at Nashik. General Motors,

Tata Motors, Mercedes Benz, Land Rover, Jaguar Cars, Fiat, and Force Motors have

assembly plants in the area. The northern cluster is around the National Capital Region, and

contributes 32%. Gurgaon and Manesar, in Haryana, are where the country’s largest car

manufacturer, Maruti Suzuki, is based. An emerging cluster is the state of Gujarat, with a

manufacturing facility of General Motors in Halol, and a facility for Tata Nano at their plant

in Sanand. Ford, Maruti Suzuki, and Peugeot-Citroen plants are also planned for Gujarat.

Kolkata with Hindustan Motors, Noida with Honda, and Bengaluru with Toyota are other

automotive manufacturing regions around the country.

Page | 12

Exports:

India’s automobile exports have grown consistently and reached $4.5 billion in 2009, with

the United Kingdom being India’s largest export market, followed by Italy, Germany,

Netherlands, and South Africa.

According to the New York Times, India’s strong engineering base and expertise in

the manufacturing of low-cost, fuel-efficient cars has resulted in the expansion of

manufacturing facilities of several automobile companies like Hyundai, Nissan, Toyota,

Volkswagen, and Maruti Suzuki. In 2008, South Korean multinational Hyundai Motors alone

exported 240,000 cars made in India. Nissan Motors plans to export 250,000 vehicles

manufactured in its India plant by 2011. Similarly, US automobile company, General Motors

announced its plans to export about 50,000 cars manufactured in India by 2011.

In September 2009, Ford Motors announced its plans to set up a plant in India with an

annual capacity of 250,000 cars, for US$500 million. The cars will be manufactured both for

the Indian market and for export. The company said that the plant was a part of its plan to

make India the hub for its global production business. Fiat Motors announced that it would

source more than US$1 billion worth auto components from India. In 2009 India surpassed

China as Asia’s fourth largest exporter of cars after Japan, Korea and Thailand by allowing

foreign carmakers 100% ownership of factories in India, which China does not allow. In July

2010, The Economic Times reported that PSA Peugeot Citroën was planning to re-enter the

Indian market and open a production plant in Andhra Pradesh that would have an annual

capacity of 100,000 vehicles, investing € 700M in the operation. PSA’s intention to utilise

this production facility for export purposes however remains unclear as of December 2010.

SWOT analysis of Indian automobile industry: (3 Companies)

Strength:

1. Evolving Industry: Automobiles represent freedom and economic growth. Automobiles

allow people to live, work and travel in ways that were unimaginable a century ago.

Automobiles provide access to markets, to doctors, to jobs. Nearly every automobile trip ends

with either an economic transaction or some other benefit to the quality of life.

Page | 13

2. Continuous product innovation & technological advancement: With the advent of E-

vehicles & alternative fuel such as Shell gas, CNG and others, Automobile Companies are

increasing R & D expenditure to drive the next phase of growth through use of renewable

sources of energy which may be solar, wind etc.

3. Growth shifting towards Asian market: Although American & European market is the

pulse of this Industry, but the focus is shifting to developing markets like China, India &

other Asian nations because of the rise in disposable income, changing lifestyle & stable

economic conditions.

4. Increasing demand for VFM vehicles: Intense competition in the matured/developed

markets has forced automobile manufacturers to target developing economies. But these

developing economies have high demand for VFM products (value for money). In the

automobile industry, VFM products would be fuel efficient, high mileage vehicles because

majority of customers in these nations prefer vehicles for commuting. On the other hand,

developed nations need is of vehicles for interstate travelling and high speed vehicles suitable

for long route with high engine power.

5. Increase in demand of luxury commercial vehicles: Companies like VOLVO,

Daimler/Chrysler, and Bharat Benz are betting high & are targeting the developing nations

due to increase in demand of Luxury public transportation system.

Weaknesses:

1. Cars recalled: Controversies relating to recalling vehicles on account of some technical dis-

functionality or non-abidance to govt. led rules are becoming very common.

2. Bargaining power of customers: Over the last 3-4 decades the automobile market has

shifted from demand to supply market. Availability of large number of variants, Stiff

competition between them, and long list of alternatives to choose from has given power to

customers to choose whatever they like.

3. Growth rate of Automobile industry is the in the hands of the government due to

regulations like excise duty, no entry of outside vehicles in the state, decreasing number of

validity of registration period & volatility in the fuel prices. These factors always affect the

growth of the industry.

Page | 14

Opportunities:

1. Introducing fuel efficient vehicles: Optimization of fuel-driven combustion engines and

cost efficiency programs are good opportunities for the automobile market. Emerging

markets will be the main growth drivers for a long time to come, and hence fuel efficient cars

are the need of the hour.

2. Strategic alliances: Making strategic alliances can be a smart strategy for Automobile

companies. By using specialized capabilities & partnering with other companies, they

can differentiate their offerings.

3. Changing lifestyles and consumer groups: Three powerful forces are rolling the auto

industry. Shift in consumer demand, expanded regulatory requirements for safety and fuel

economy, and the increased availability of data and information. Also with the increase in

nuclear families there has been increase in demand of two-wheelers & compact cars and this

will grow further.

4. OEM priorities: Given the increase in electronic content, OEMs need to collaborate with

suppliers and experts outside the traditional auto industry. Accomplishing this will require

changes in the way OEMs function. OEMs will be looking to their top suppliers to co-invest

in new global platforms & this will be the driving force in the future.

Threats:

1. Intense competition: Presence of such a large number of players in the Automobile

industry results into extensive competition, every company eating into others share leaving

little scope for new players.

2. Volatility in fuel prices: At least for the passenger segment fluctuations in the fuel prices

remains the determining factor for its growth. Also government regulations relating the use of

alternative fuels like CNG. Shell gas is also affecting the inventories.

3. Sluggish economy: Macroeconomic uncertainty, Recession, un-employment etc. are the

economic factors which will daunt the automobile industry for a long period of time.

Page | 15

4. High fixed cost and investments in R & D: Due to the fact that mature markets are already

overcrowded, industry is shifting towards emerging markets by building facilities, R & D

centres in these markets. But the ROI out of these decisions is yet to be capitalized.

SWOT analysis of Maruti Suzuki:

Strength:

Maruti Udyog limited (MUL) is in a leadership position in the market with a market

share of 48.74

Major strength of MUL is having largest network of dealers and after sales service

centres in the country.

Good promotional strategy is adopted by MUL to transfer its thoughts to the people

about its products.

Strong brand value and loyal customer base are big strengths of MUL.

MUL is the first automobile company to start second hand vehicle sales through its

True-value utility.

Weaknesses:

Low interior quality inside the cars when compared to quality players like Hyundai

and other foreign players.

Government intervention due to having share in MUL.

Younger generations started getting a great affinity towards new foreign brands.

Maruti hasn’t proved itself in SUV segment like other players.

Opportunities:

MUL has launched its LPG version of wagon R and it was a good move

simultaneously.

MUL can start R & D on electric cars for a much better substitute of the fuel.

Exports capacity of the company is giving new hopes in American and UK markets.

Economic growth of the country is constantly increasing and the government is

working hard to increase the GDP to double digit.

Threats:

Major players like Maruti Suzuki, Hyundai, Tata has lost its market share due to many

small players like Volkswagen- polo. Ford has shown a considerable increase in

market share due to its Figo

Page | 16

China may give a good competition as they are also planning to enter into Indian car

segment.

SWOT analysis of Hyundai:

Strength:

Hyundai India has such a brand equity that it is almost assumed to be an Indian brand,

with lot of good accolades for being India’s second most selling brand next to MUL

in market share

HMIL is known for its quality products which has better performance and it has

constantly been ahead in the race with Maruti Udyog limited in many parameters

The product length includes around 8 cars, starting from new Eon in small car

segment to SUV segment Santa Fe.

Hyundai products never fail to win laurels in each segment from various automobile

ratings ever since its operations in India.

Hyundai has the largest network of showrooms and service station next to Maruti in

India.

Weaknesses:

HMIL took a long time to gain the market share as it’s not the first mover in India

In terms of most reliable and trusted brand; Maruti is more strong in Indian

subcontinent

Spare parts of Hyundai vehicles are comparatively priced higher and spare parts do

not have PAN India presence

Increase in commodity prices such as steel, aluminium and ancillary parts has affected

margins

Since HMIL concentrates on both domestic and International sales there are higher

risks of exchange rate fluctuations

Opportunities:

The saving consumption pattern of India is an added advantage for any segment doing

business in India. This was one of the major reason for Indian market to survive

amidst global recession

Page | 17

There is more scope of HMIL to enter into small car segment as it has dedicated R&D

plant in Hyderabad, India. Hyundai is one of the very few companies that has widest

R&D network across the world located in Korea, Europe, India, US, Japan

Hyundai has very good opportunity in entering into commercial vehicles and

Recreational vehicles as they are already doing well outside India. Currently HMIL

has its focus only on Passenger car segment.

Threats:

Though Hyundai claims itself to have no direct competitors other than MUL, there are

Indian players like Tata, Mahindra imposing a strong threat for Hyundai Motors India

to expand its product category

Foreign Direct Investments flowing in Indian automobile space are not good signs for

already existing Giants like MUL and Hyundai.

Many manufacturers have started to concentrate on small car segment as an

alternative to Nano. These will slow down the expected sales of Eon.

SWOT Analysis of Honda:

Strength:

There are many feathers in the cap of Honda motors but one of its biggest advantages

is that it is world’s largest motorcycle manufacturer. It has a lion’s share of the market

of motorcycles.

Like motorcycles, Honda motors also has a large presence in combustion engine

market which is used for aeroplanes, jet skis, yachts or any heavy engine usage.

Besides being the world’s number 1 automobile manufacturer, Honda motors are also

the eight largest manufacturers of Automobiles. It has a strong and localised product

portfolio.

One of the reasons that Honda has been able to achieve these heights is because of its

focus on R&D and its manpower employed in R&D. Hence Honda is always coming

up with elegant and efficient designs which are a hit in the market.

Page | 18

Weaknesses:

Naturally, with a high investment in R&D and into the latest technology, the cost of

the product goes high and the pricing to end customer is high as well. This might be a

weakness of Honda but it needs to have this weakness, because it cannot reduce its

brand equity by lowering the prices.

One common complaint for Honda cars is that the cars are only for the upper middle

class and Honda needs more automobile portfolio for the lower middle class, which

already other automobile manufacturers like Hyundai and Maruti are targeting.

At least in India, Honda motors suffered badly when Hero and Honda were separated.

As a result, Honda has had to replan its presence in India.

Opportunities:

This division is targeted towards the future of automobile market wherein people will

be demanding usage of clean energy because fuel like Petrol and Diesel as well as

CNG has its limitations.

The number of automobiles across the world is increasing. One of the reasons is the

increase in buying power of individuals; another is that it is a social norm now to have

a motorcycle or a car. Thus, consumption is at an all-time high.

Adding more products in the portfolio and making more variants to increase the

product line are two tactics commonly used by Automobile manufacturers. There are

many considerations to be undertaken before launching a new model. However,

product expansion is the key to grow in a competitive market.

Threats:

Competition from local and regional or national players in each of the countries it is

present in is denting the revenues of Honda.

Although people have more funds now for buying cars, the rising cost of fuel is

troubling everyone and is one of the reasons that many people are still hesitant to buy

cars, because later on the fuel cost paid is more than the car.

One of the aspects plaguing all automobile manufacturers is the transportation as well

as manufacturing and labour costs. With inflation, these costs are always on the rise

and hence are a point of concern.

Page | 19

Future technological demand:

Now from Today, there are some future technological demands which should be fulfil in

future, those demands are listed below:

• Fuel Efficiency

• Emission Reduction

• Safety and Durability

• Cost Effectiveness

• Innovative Features

Some of the innovative features are Key Less Entry, Electrically controlled mechanisms,

enhanced driving control, Composites, Long life Components, Soft feel interiors.

Various challenges:

In Indian Automotive Market, there are some challenges by virtue of which automobile

industry faces lot of problems. These challenges should be overcome and the challenges are

listed below:

• Growth in input costs

• Fuel price volatility

• Slowdown in demand

• Slowdown in USA

• Production cuts

• Growing competition

• Changing consumer preferences

• Chinese competition

• Environmental issues

• Low R&D orientation

Current Market Scenario:

Domestic vehicle sales of Indian Automobile industry has been growing at of 9.6% over the

period of FY05-FY15 while exports have grown at of 18.9%. However, post the three

consecutive years of strong double digit growth during FY10-FY12, the industry is struggling

to reach even a low double digit growth rate. During FY13-FY15, domestic sales grew at of

just 4.4% which was mainly driven by 7.2% growth in FY15. This weakness in demand for

Page | 20

automobile vehicle in domestic market was mainly due to sluggish economic growth with

subdued consumer sentiment due to rising interest rate and fuel prices.

Source: Times of India (2016).

On the above image growth in sales of passenger cars in India has been highlighted. In this image

comparison has been done in between April 2015 and April 2016. 6 companies have been taken in

this research.

Page | 21

Source: Indian automobile manufactures.

2012-13 is the worst year for India car sales as because the sales in India fell 6.7 percent for the fifth

consecutive month in March.

The above image shows the growth rate of all car companies in India. This comparison has

been done between 2 years i.e. 2014-15 and 2013-14. In this report Maruti Suzuki and

Hyundai have equal percentage of growth rate and consider as tough competitor for each

other in Indian automobile industry. In 2014-15 total number of car sales is 2534882, and

total number of car sales in 2013-14 is 2398264, the growth rate is 5.4%.

Page | 22

Page | 23

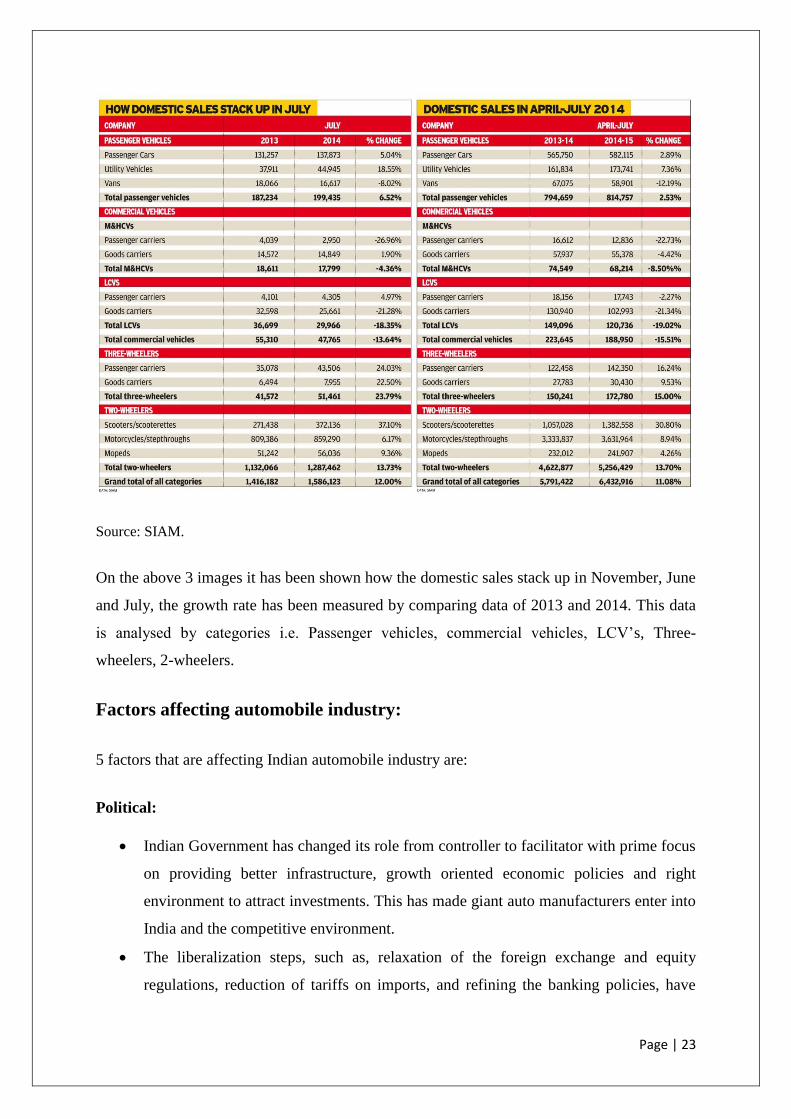

Source: SIAM.

On the above 3 images it has been shown how the domestic sales stack up in November, June

and July, the growth rate has been measured by comparing data of 2013 and 2014. This data

is analysed by categories i.e. Passenger vehicles, commercial vehicles, LCV’s, Three-

wheelers, 2-wheelers.

Factors affecting automobile industry:

5 factors that are affecting Indian automobile industry are:

Political:

Indian Government has changed its role from controller to facilitator with prime focus

on providing better infrastructure, growth oriented economic policies and right

environment to attract investments. This has made giant auto manufacturers enter into

India and the competitive environment.

The liberalization steps, such as, relaxation of the foreign exchange and equity

regulations, reduction of tariffs on imports, and refining the banking policies, have

Page | 24

played an equally important role in bringing the Indian Auto- motive industry to great

heights.

Institutionalization of automobile finance has further paved the way to sustain a long-

term high growth of industry.

Economical:

Rising GDP consecutively for the last 5 years has led to increased purchasing power

and hence the automobiles.

Per capita income is rising, which is affecting the segments of automobile being

ventured into.

There is cut throat competition among many players in the market.

Increasing urbanization of rural India also has given rise to increase in sales.

The concept of service in auto industry has changed into customer care now, thus

encompassing the greater value into it.

Social environment:

Indian families are becoming increasingly nuclear.

Increasing propensity to spend.

Increasing distances between work-places and residence.

Technology:

Increasing use of CNG and LPG instead of conventional fuel has made entry of new

kinds of vehicle in market.

The customer can now use the internet to place the order and expect the manufacturer

to fulfil his customized demand in the minimum time.

With technological advancement electrical car may emerged as a preferred option.

Page | 25

Car Loan Market in India:

Indian auto market has more than 35 financers that offer auto financing solutions to the

intended car buyers. Being one of the fastest growing automobile markets in the world, the

Indian automobile market has got so much of potential and hence a number of auto finance

companies have come up to tap the booming market. It can be added here that the passenger

vehicle market constitutes almost 80% of automobile sales. In 2008, the stock passenger car

was about 11 per 1,000 people. The production of passenger vehicle is further expected to go

up at a CAGR of about 10% from 2009-10 to 2012-13. So, sensing this market potential,

many financial companies in India have given special attention on auto financing.

During the 2000s, the auto finance in India was dominated by private banks, when Citibank

was the market leader. But its market share dropped from 27 per cent during 90s to less than

8 percent during early 2000. ICICI Bank became the new leader with almost 29.2 per cent

market share during 2003-04. The journey continued till 2008 when HDFC bank took the

lead. However, the current trend shows that the PSU banks like SBI, PNB, Bank of Baroda,

Bank of India, Canara Bank, Syndicate Bank and Union Bank etc. are leaving behind their

private sector counterparts in the ` 22,000 crore passenger car and 2-wheeler loan market.

The reason behind this is the fact that, private banks have been compelled to reduce their

exposure to the sector owing to increased delinquencies.

List of top auto finance companies in India:

1. State bank of India: State Bank of India (SBI) is one of the leaders in the auto finance

segments in India. Recently it has slashed down its rate of interest for the new cars, which, in

turn, has attracted a number of customers. Its long repayment option and extensive network

of more than 12,150 branches have also made it quite popular among the customers. Recently

SBI has inked a deal with General Motors for car finance. In 2008-09, SBI registered a net

profit of 9,121 crore, which was 35.55% bigger than the last financial year's profit of 6,729

crore.

2. ICICI Bank: ICICI Bank was the market leader in auto finance in India till 2008. Though

currently not on the top, it still remains amongst the top 10 auto finance companies in India.

However, to regain its lost reign, ICICI Bank is putting car loans on fast track. In the current

Page | 26

financial year, ICICI Bank has doubled auto loan disbursement amount to more than 1,500

crore, comparing to the last financial year. ICICI Bank registered a net income of ` 35,769.5

million in the last financial year.

3. HDFC Bank: HDFC Bank is a market leader in auto finance in India. In order to stay in

the race of dominating Indian auto finance market, HDFC Bank also cut down the rate of

interest for its car loan. In the financial year 2008-09, HDFC Bank registered a profit

of 244,493 lacs, comparing to 159,018 in the previous financial year.

3. Bajaj auto finance limited: Bajaj Auto Finance Ltd is one of the leading auto finance

companies in India. Offering a diverse array of financial products to its clients ranging from

two wheeler loans to other loans like consumer durable loans, business loans and many more,

BAFL also offers free personal accident insurance to its clients. It has an extensive network

of 50 branch offices and more than 6000 consumer durable dealerships. In the financially

year 2008-09, BAFL registered a profit (after taxation) of ` 339.1 million, comparing to

previous year's profit of ` 201.2 billion.

4. Citibank: Once a market leader in auto financing in India, Citibank offers automobile

financing to its clients through its extensive dealership network across the country. One of the

leading players in the market, Citibank offers a range of auto financing options for the

customers. For the year ended March 31, 2009, Citibank registered a net profit (after tax) of

2,173 crore, which was 20% higher than its previous year's profit of 1,804 crore.

5. Bank of Baroda: Bank of Baroda offers specially-designed car loans for the customers so

that it meets their demands, status and taste. Loans are offered for new as well as used cars.

Bank of Baroda also offers a unique facility for installation of CNG/LPG Gas-kit in the cars.

Unique features and low interest rates are USPs of Bank of Baroda car loans. In 2008-09,

Bank of Baroda registered a net profit of 2,227.20 crore, comparing to the net profit of

1,435.52 crore in the previous financial year.

6. Punjab national bank: Punjab National Bank, a renowned leader in the field of auto

finance market in India, offers auto loan for new as well as old vehicles of not older than 3

years. Loans are also offered for purchase of vehicles of foreign/indigenous makes. In

September 2009, PNB tied up with Mahindra and Mahindra for financing their vehicles

Page | 27

across the nation. PNB registered a net profit of 309,088 lacs in the year ended March 31,

2009.

7. Kotak Mahindra prime limited: Kotak Car Finance has crafted a niche in the Indian auto

finance market through its flexible schemes, hassle-free documentation and quick processing.

KMPL finances new as well as used cars. In 2008-09, KMPL registered a net profit of 1,570

million.

8. Sundaram Finance: Sundaram Finance is one of the market leaders in the auto finance

market in India. Founded in 1998, this company extends finance in all models of cars.

Customers can choose from a range of vehicle and finance packages offered by the company.

It also has an extensive network of more than 400 branches across the nation.

9. United Bank of India: United Bank of India is one of the leading auto finance companies

in India offering range of car financing options to the customers. It offers car loan for new

cars as well as for used cars. In 2008-09, UBI registered a net profit of 18470.96 lakhs.

10. Canara bank: Canara Bank offers attractive interest in the auto loans for its customers.

From August 2009, Canara Bank further reduced its auto loan rates to woo customers. Canara

Bank registered a net profit of 2072 crore in 2008-09, which saw a 32.4% rise from previous

year's net profit of 1565 crore.

Page | 28

Source: www.jagoinvester.com

On the above image research is conducted among 1504 people and find out number of

people’s preference for car loan. The results are 42.42% people prefer SBI for car loan which

is the highest; PNB is lowest at 1.60%. The reason of fluctuation is because of services

provided by SBI bank is different from other banks.

Categories of auto financiers:

Entry in the auto financing segment has been relatively easy and hence the gap between

existing players and new entrants is not much. Auto financing market typically remains

competitive. Some of the players in the market are:

Banks: Banks, both public and private, cover a huge portion of the auto finance market since

they are among the most established lending institutions around. They are in a position to

offer competitive rates as compared to other financers with better access to credit histories.

Customers are used to working with their local bank for a variety of day-to-day needs.

Turning to them for car financing seems like the natural next step. The CASA advantage that

banks have given them an edge over other financiers.

Page | 29

Non-banking Finance companies (NBFCs): Acting as an aide-de-camp to banks, NBFCs

occupy a significant position in financial intermediation. NBFCs cover a signification portion

of the total auto finance market in India. Though banks have low cost of funds, NBFCs have

certain advantages and lesser stringent regulatory requirements as compared to banks. NBFCs

are not bound by priority sector lending requirements, not required to maintain CRR, can

customize products, and have wider reach to customers. These differences have resulted in

NBFCs having a significant role playing with banks on the lending front. Also, banks have

concentrated more on the car loan segment whereas NBFCs are more focussed on providing

finance to the commercial vehicle segment.

Commercial vehicle loan in India: Commercial vehicle loans are usually taken by

individual, partnership firms, proprietorship firms, HUF (Hindu Undivided Family), trusts,

societies, self-employed, businessmen and private and public limited companies for their

financing needs for owning and running commercial vehicles. Commercial vehicle loan

options are available for buses, tippers, transit mixers or any other heavy, light or small

commercial vehicle. A commercial vehicle loan can be taken for a variety of commercial

vehicles, which may be used at different locations. While loans are sanctioned for the

purchase of a new commercial vehicle, banks also offer loans for pre-owned vehicles.

Borrowers can also avail of a top up on existing loans subject to conditions. The interest rates

range from 10% to 15% depending on the customer and vehicle segment. The rate depends

on a lot of factors such as the number of vehicles owned by the borrower, his business

turnover, repayment track record from other financiers (if any), etc. The financial institutions

are able to confirm the rate of interest once they have studied the documents. The interest rate

may be fixed or variable. Processing charges include processing fee, stamp duty and vehicle

valuation charges. The processing fee depends on the loan amount. It usually ranges from

2%-4%.

Commercial Vehicles Leasing in India: Globally there is a clear domination of lease over

loan. In auto financing segment over 60% of US market and 40% of European market follows

the lease route for an auto purchase. The auto-leasing sector in India has recently picked up

pace, although the market is still in its nascent stage.

The scope of growth of leases in this sector is very high owing to the large number of

infrastructural projects in the pipeline which will result in the demand for commercial

Page | 30

vehicles to grow combined with the rising cost of manufacturing these vehicles, users are

forced to look at lease options more actively than ever before.

On the flip side, the deterrents to growth of leasing as a financial product, which may

be more generic to the product than specific to the sector, are multiplicity of taxes. For

instance, in a chassis, the combination of the chassis and the body is treated as a new asset for

indirect tax purposes and accordingly, the chassis suffers local taxes whereas the body of the

vehicle is subject to works contract. From leasing point of view sales tax in form of VAT/

CST are applicable on lease rentals. Then, at the end of the lease if there is any transfer of

ownership, sale tax is applicable on the sale consideration. Further there may be issues of

input tax credit being disallowed, adding to the costs of the transaction, making it completely

unviable.

Though leasing is becoming attractive as a more popular product, the add-on costs in

the form of taxes are acting as a deterrent and add to the complexities. Nevertheless this

untapped sector provides huge opportunities to financial institutions due to its inherent

benefits pertaining to risk removal and cash flow restructuring.

Leasing has been a widely accepted product in the passenger vehicle segment owing

to the tax free perquisite benefit availed by the employees. In the current market scenario the

penetration rate of leasing in passenger vehicle segment is 25% vis-à-vis the penetration rate

of leasing being 3%-4%. CV financing and CV industry in particular is posed to several

challenges in the recent times than opportunities clearly explaining the traction in volumes

and numbers.

According to a report by Ernst and Young, Indian commercial vehicle (CV) sales

were expected to grow at a CAGR of 15% in the next five years - from 0.8 million in 2011-12

to reach 1.6 million units by 2016-17.8 the improving road infrastructure in rural and semi-

urban areas will be one of the main drivers of this development.

The growth of commercial vehicle industry has been linked to the country’s industrial

activities and the overall GDP. In the short term the CV volumes and financing has got

impacted due to the macro factors, but considering the huge infrastructural demand in the

country and the strong fundamentals, we are bullish on the long term prospects of the CV

industry in general and higher penetration for CV financing in particular.

Page | 31

Objectives of the Project

The objective behind the research of this project is to understand the two main topics

of my study i.e. automobile market of India and car loan & finance. In these two topics I will

study related to history of automobile market of India, current market scenario, segments of

cars, companies work in this field, market share of companies, manufacturing units in India,

exports and import scheme in India.

Second topic of my project is car loan and finance. In this topic I will study related to

car loan market of India, categories of auto financiers, procedure of getting a car loan,

documents required for getting a car loan.

Primary Objective:

Understanding the growth of automobile market of India

Understanding factor affecting automobile sector.

To learn procedure of getting car loan.

Link between car loan and sales of the car.

Secondary Objective:

Changes in income level in las 10 years.

Relation between changes in population and car sales.

Relation between change of interest rate and car sales.

Scope of the Project

As the study is to analyse the automobile market of India and study related to car loan

and finance market of India this study will be useful for the people who are willing to

study related to automobile market and to get information related to car loan and

finance its procedures and documents require getting the car loan. This report will

also give information related to current market scenario of automobile sector. Since

the report is related to automobile sector it will show the growth of the company year

by year and factors affecting gross domestic product (GDP) of country. This report

will also help for making future predictions.

Page | 32

Limitation of the Study

The study is based on secondary data collection methodology so the information may

not be totally liable.

Only limited number of companies is taken into consideration in this study.

Hypotheses

Find out the relationship between sales of automobile and growth rate of income of

individual.

There is a link between growth rate of commercial vehicles and total sale of a

vehicles.

Page | 33

Chapter 2

Research Methodology

Introduction

The purpose behind the research of this project is to understand the two main topics of my

study i.e. automobile market of India and car loan & finance. In these two topics I will study

related to history of automobile market of India, current market scenario, segments of cars,

companies work in this field, market share of companies, manufacturing units in India,

exports and import scheme in India.

Objectives

Understanding the growth of automobile market of India

Understanding factor affecting automobile sector.

To learn procedure of getting car loan.

Link between car loan and sales of the car.

Page | 34

Literature Review

PTI, June (2016): Analyses done by Press trust of India that hiring momentum picked up pace

again in May with recruitment activity growing by a moderate 2 per cent led by the

automobile sector, says a report. According to the latest Times Jobs RecruiteX report,

automobile sector was the top employment generator in May, followed by consumer durables

and FMCG.

PTI, April (2013): Analyses done by press trust of India that the auto companies and ancillary

makers are confident of posting 10 per cent rise in business, provided barriers to free

movement of goods are removed, a survey said on Thursday. Over 80 per cent of the players

in the automobile industry, having units in north India, said business activities could grow by

10 per cent while 20 per cent of the respondents said business was likely to go beyond 10 per

cent, a survey conducted by the PHD Chamber of Commerce and Industry said.

Economic Times, April (2003): Analyses done by Economic times that the auto companies

and ancillary makers are confident of posting 10 per cent rise in business, provided barriers to

free movement of goods are removed, a survey said on Thursday. Over 80 per cent of the

players in the automobile industry, having units in north India, said business activities could

grow by 10 per cent while 20 per cent of the respondents said business was likely to go

beyond 10 per cent, a survey conducted by the PHD Chamber of Commerce and Industry

said.

ET, bureau May(2016): The automotive business is confused over a rule that industry

executives say will make tax collection at source (TCS) compulsory even when someone

sells a vehicle costing Rs 10 lakh or more in the second-hand market. Unlike what was

originally expected, the rule that is approved as part of the Finance Bill and will come into

effect on June 1covers all types of vehicles

PTI, May(2016): Press trust of India analyses that European rival Daimler Chrysler, US-

based automaker General Motors will test its advanced automobile engines on bio-diesel

being developed by an Indian research institute. "As part of a two-year project, General

Motors will be testing and evaluating the performance of their most advanced and futuristic

Page | 35

automobile engines on the bio-diesel developed by our institute," said Central Salt and

Marine Chemicals Research Institute (CSMCRI)

ET bureau, June (2002): It was analyses that at first sight are not the right place for an article

trashing auto technology. But then again, it's the only place for a common-sense look at that

highly-strung hunk of steel. The disclaimer first: I'm not in love with automobiles, but I don't

really dislike them. I just think they're basically inefficient. I also have nothing against men.

ET bureau, May (2016): The capital will witness the country's first automobile carnival 'Auto

jumble' next week, on the lines of the Beaulieu International Auto jumble held in the UK.

Items ranging from spare car parts of old automobiles, accessories, books and manuals will

displayed for sale at the Auto jumble in the capital on February 24, said Vintage car owners'

association Heritage Motoring Club of India (HMCI) president K T S Tulsi.

ET intelligence group, February (2016): The government's decision to increase minimum

import price (MIP) of steel for the next six months will reduce the benefit of lower

commodity prices for automobile companies. Steel prices may rise in the range of 30 to 70%

depending upon the grade. However, not all of the rise will be reflected in the performance of

auto players.

Times News Network, October (2010): Bangalore and Punjab have overtaken Mumbai as the

fastest growing car finance markets in the country. They now share the top slot with Delhi

(including Gurgaon). Earlier it used to be a close contest between Mumbai and Delhi.

Occupying the second rung are Kerala and Gujarat followed closely by Mumbai and Chennai.

Trade experts say that the market had stagnated for three to four years, and may finally see a

boom this year (April to August), growing at around 25-26%.

PTI, January (2016): Domestic brokerage Kotak Institutional Equities today launched a tool

to forecast auto sales and said it is keen to introduce a broader consumer sentiment index in

next one year. 'Consumer Querimetrix', a tool focussed on the four-wheeler industry, has

been unveiled in association with Indian arm of Internet search giant Google, the brokerage

said.

Page | 36

Times News Network, April (2010): The new car finance market has grown to 6.1 lakh units

worth anything between Rs 18,000 crore to Rs 23,000 crore in 03-04, according to industry

estimates. That's up from the 02-03 range of Rs 15,000-17,000 crore. Add to that another Rs

2000 crore in used car finance and the finance pie in the million year touches anywhere

between Rs 20,000-25,000 crore.

PTI, March (2010): Stepping up efforts to penetrate deeper into the semi urban and rural

India, country's largest car maker Maruti Suzuki India on Monday inked a pact with Shriram

City Union Finance with an initial allocation of Rs 1,000 crore. The tie-up would focus on

financing of entry level cars from Maruti portfolio, which include the M800, Omni and Alto

models, the company said in a statement.

PTI, March (2014): Auto major Tata Motors today said it has tied up with Bharatiya Mahila

Bank to provide retail finance to its passenger vehicle customers. "With this association,

Bharatiya Mahila Bank will be one of the preferred retail financiers of Tata Motors'

passenger car business and will be able to help reach out to the growing women customer

base of the bank," Tata Motors said in a statement. Bharatiya Mahila Bank will facilitate

eligible customers of Tata Cars.

Times News Network, September (2010): Interest rates on car finance have dropped to an

effective rate of 7% and are expected to drop further with direct selling agents, financiers and

manufacturers doling out huge discounts to entice car buyers. In a desperate bid to increase

volumes, commissions on registration and insurance are being passed onto the customer.

While official rack rates offered by financiers have dropped from 12-13% to 10-11%, huge

cash discounts by manufacturers like Hyundai and Maruti etc.

The Investment Information and Credit Rating Agency of India (ICRA, 2003) studies the

competitiveness of the Indian auto industry, by global comparisons of microenvironment,

policies and cost structure. This has a detailed account on the evolution of the global auto

industry. The United States was the first major player from 1900 to 1960, after which Japan

took its place as the cost-efficient leader. Cost efficiency being the only real means in as

mature an industry as automobiles to retain or improve market share, global auto

manufacturers have been sourcing from the developing countries. India and China have

emerged as favourite destinations for the first-tier OEMs since late 1980s. There are only a

Page | 37

few dominant Indian OEMs, while the number of OEMs is very large in China (122 car

manufacturers and 120 motorcycle manufacturers).

PTI, May (2008): Global IT major IBM today said it has identified Pune and Chennai as key

delivery hubs to serve its domestic and global clients in the automotive sector. The company

which has six Global Business Service Centres (GBSCs) in India at Bangalore, Chennai,

Kolkata, Pune, Hyderabad, Noida, Gurgaon, Pune and Chennai, would focus on serving

domestic and global clients in the automotive industry, primarily from the two identified

sites. "Pune and Chennai will be the core centres for automotive industry.

ET bureau, June (2013): Armtek Auto, India's leading forging and integrated auto component

manufacturer, on Thursday announced that it has acquired a 51.27% stake in JMT Auto for

about Rs 110 crore. Headquartered in Jamshedpur, JMT has revenues of around Rs 307 crore

for the March ended fiscal and is one of the leading auto component manufacturers in the

Eastern Indian region. It has seven manufacturing facilities spread across locations such as

Jamshedpur, Dharwad and Lucknow. Arvind Dham's $2-billion Armtek Auto would acquire

shares of JMT at Rs 148.70 a share, a 28% premium over the current market price.

Scope

As the study is to analyse the automobile market of India and study related to car loan and

finance market of India this study will be useful for the people who are willing to study

related to automobile market and to get information related to car loan and finance its

procedures and documents require getting the car loan. This report will also give information

related to current market scenario of automobile sector. Since the report is related to

automobile sector it will show the growth of the company year by year and factors affecting

gross domestic product (GDP) of country. This report will also help for making future

predictions.

Sources of Data

In this project Secondary data is used for research

Secondary sources as mentioned below are used

1. Internet

Page | 38

2. Newspaper

3. Magazine

Limitation of the research

The study is based on secondary data collection methodology so the information may

not be totally liable.

Only limited number of companies is taken into consideration in this study.

Page | 39

Chapter 3

Analysis

For the analysis of my research topic i.e. Automobile market of India I have taken

manufacturing and sales data of passenger vehicles and commercial vehicles in India. The

data of manufacturing and sales is collected I time period of 2005-2015.

The method that is used for analysis is correlation and regression matrix, in this the

data of manufacturing and sales is linked with per capita income of India.

Factor analysis is a statistical method used to describe variability among observed,

correlated variables in terms of a potentially lower number of unobserved variables called

factors. Factor analysis searches for such joint variations in response to unobserved latent

variables. The observed variables are modelled as linear combinations of the potential factors,

plus "error" terms. The information gained about the interdependencies between observed

variables can be used later to reduce the set of variables in a dataset. Factor analysis

originated in psychometrics and is used in behavioural sciences, social sciences, marketing,

product management, operations research, and other fields that deal with data sets where

there are large numbers of observed variables that are thought to reflect a smaller number of

underlying/latent variables.

Factor analysis is a technique that requires a large sample size. Factor analysis is

based on the correlation matrix of the variables involved, and correlations usually need a

large sample size before they stabilize. The determination of the number of factors to extract

should be guided by theory, but also informed by running the analysis extracting different

numbers of factors and seeing which number of factors yields the most interpretable results.

In this study we have included many options, including the original and reproduced

correlation matrix, the scree plot and the plot of the rotated factors.

Page | 40

Descriptive Statistics

Mean Std.

Deviation

N

Growth

Rate 10.1545 11.38590 11

Sales 2655571.455 772198.6012 11

Production 3128573.812 954041.7470 11

Income 4382.0000 834.52477 11

A. Mean - These are the means of the variables used in the factor analysis.

B. Std. Deviation - These are the standard deviations of the variables used in the factor

analysis.

C. Analysis N - This is the number of cases used in the factor analysis.

On the above table mean and standard deviation is calculated. The arithmetic mean or

average of a set of values is the ratio of the sum of these values to the number of elements in

the set, here N is number of variables.

Standard deviation means set of dispersion of a set of data from its mean. Use of standard

deviation is to determine how spread out the data is from mean. A higher standard deviation

value indicates greater spread in data.

Correlations

GrowthRate Sales Production Income

Pearson Correlation

GrowthRate 1.000 -.231 -.256 -.393

Sales -.231 1.000 .998 .917

Production -.256 .998 1.000 .932

Income -.393 .917 .932 1.000

Sig. (1-tailed)

GrowthRate . .247 .224 .116

Sales .247 . .000 .000

Production .224 .000 . .000

Income .116 .000 .000 .

N

GrowthRate 11 11 11 11

Sales 11 11 11 11

Production 11 11 11 11

Income 11 11 11 11

Page | 41

On the above table correlations has been measured. These numbers measure the strengths and

direction of the linear relationship between the two variables. The correlation coefficient can

range from -1 to +1, with -1 indicating perfect negative correlation, +1 indicating a perfect

positive correlation, and 0 indicating no correlation at all.

Variables Entered/Removeda

Model Variables

Entered

Variables

Removed

Method

1 Income, Sales,

Productionb

. Enter

a. Dependent Variable: GrowthRate

b. All requested variables entered.

Model Summaryb

Model R R

Square

Adjusted R

Square

Std. Error of

the Estimate

Change Statistics

Durbin-Watson

R Square Change

F Change

df1 df2 Sig. F

Change

1 .527a 0.278 -0.031 11.56251 0.278 0.899 3 7 0.488 1.762

a. Predictors: (Constant), Income, Sales, Production

b. Dependent Variable: Growth Rate

On the above table in model summary the main thing on that we have to focus is R square

because R square tells about the goodness of fit of the model in this table R square is 0.031

which means that the one variable can explain about 3.1% change in other variable. In this

table predictors are Income, Sales, Production and dependent variable is Growth rate.

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1

Regression 360.546 3 120.182 .899 .488b

Residual 935.841 7 133.692

Total 1296.387 10

a. Dependent Variable: GrowthRate

b. Predictors: (Constant), Income, Sales, Production

Page | 42

On the above table the main focus is on Significance, Significance will decide whether we

should whether we should reject Null hypotheses or not. In this case the Significance is .488

which means the null hypotheses can’t be rejected “The model has some predictive value”.

Coefficientsa

Model

Unstandardized Coefficients

Standardized Coefficients

t Sig.

95.0% Confidence Interval for B

Collinearity Statistics

B

Std. Error

Beta Lower Bound

Upper Bound

Tolerance VIF

1

(Constant) 31.162 42.031 0.741 0.483 -68.227 130.55

Sales 5.82E-05 0 3.946 0.54 0.606 0 0 0.002 518.079

Production

-4.17E-05

0 -3.491 -0.432 0.679 0 0 0.002 633.175

Income -0.01 0.016 -0.756 -0.637 0.545 -0.049 0.028 0.073 13.673

a. Dependent Variable: GrowthRate

On the above table the main thing that we have to focus is Significance of variables i.e. Sales,

Production, Income. If the Significance of the variables are .000 then the null hypotheses is

rejected but in this case Significance is 0.483, 0.606, 0.679, and 0.545 respectively.

Coefficient Correlationsa

Model Income Sales Production

1

Correlations

Income 1.000 .664 -.736

Sales .664 1.000 -.994

Production -.736 -.994 1.000

Covariances

Income .000 1.159E-006 -1.151E-006

Sales 1.159E-006 1.162E-008 -1.033E-008

Production -1.151E-006 -1.033E-008 9.300E-009

a. Dependent Variable: Growth Rate

On the above table covariance’s is measured it means how changes in one variable are

associated with changes in a second variable.

Page | 43

Collinearity Diagnosticsa

Model Dimension Eigenvalue Condition

Index

Variance Proportions

(Constant) Sales Production Income

1

1 3.946 1 0 0 0 0

2 0.051 8.802 0.09 0 0 0

3 0.003 33.619 0.23 0.01 0 0.49

4 6.39E-05 248.476 0.68 0.99 1 0.51

a. Dependent Variable: Growth Rate

On the above table collinearity diagnostics is calculated with the help of variance proportions

i.e. constant, sales, production, Income. These 4 variables effect collinearity diagnostics

results.

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value -.4989 16.6161 10.1545 6.00455 11

Residual -11.47417 20.23069 .00000 9.67389 11

Std. Predicted Value -1.774 1.076 .000 1.000 11

Std. Residual -.992 1.750 .000 .837 11

a. Dependent Variable: GrowthRate

Page | 44

Chapter 4

Findings

There is link between income level and cars sales as income level increases cars sales

increases.

In our research we have found that there are many factors which are affecting

automobile sector or may affect in future.

There is vast competition in passenger vehicle market as there are more than 20

companies are providing car sales and services.

Maximum number of companies has already started manufacturing plant in India,

some other companies has there assembly line.

Indian government is also helping automobile sector to grow in India.

Commercial vehicles market is not much vast as compared to passenger vehicles.

There are lot companies who used to produce commercial vehicle and export the

vehicles in other countries.

Page | 45

Chapter 5

Suggestions

Since automobile market is growing vast in India there are some rules and regulation

must be implemented regarding the manufacturing of commercial vehicles and

passenger vehicles.

There will be more foreign industry interaction from 2020 regarding the sales of

passenger cars in India.

Prices of cars must be adjusted to income level so that average income people can buy

car.

Page | 46

Chapter 6

Conclusion

India is becoming one of the fastest growing automobile markets in the word and many

reports suggesting that India will surpass china in the average automobile (Passenger Vehicle

Segment) by 2025 there is tremendous potential in automobile industry and the recent growth

figures by all the automobile majors prove this point that Indian automobile industry is back

on track. Now the competition will not be limited to just the existing players in the market i.e.

Maruti, Hyundai, TATA, GM, Honda and Skoda. Competition will now be much higher with

all the auto majors lining up for entry into India either to market their cars here or to

manufacture, but all the auto majors seem to be coming to India.

India’s automobile industry is poised at the start of an exciting phase of growth, not all of

which may derive from manufacturing conventional fuel-based vehicles. Various possibilities

ranging from developing vehicles based on alternate fuels to collaborating with some-time

rivals, have the potential to open fresh avenues for growth.

Page | 47

Bibliography

http://www.oica.net/category/sales-statistics/

https://www.sbi.co.in/portal/web/interest-rates/base-rate-historical-data

http://www.autocarpro.in/analysis-sales/india-sales-analysis-march-2016-

11039/page/3?id=11039

http://articles.economictimes.indiatimes.com/keyword/automobile

http://www.statista.com/statistics/200002/international-car-sales-since-1990/

http://www.tradingeconomics.com/india/interest-rate

https://en.wikipedia.org/wiki/Automotive_industry_in_India

http://articles.economictimes.indiatimes.com/keyword/car-finance

http://business.mapsofindia.com/finance/top-auto-finance-companies-in-india.html