strategy and vision

TRANSCRIPT

Strategy and Vision

Dwayne Gunter, CEO

Brendan Rokke, SVP Strategy

2

Back to March 2020

Introduction of

QHR Health brand

and mission

Introduction of

QHR Health’s

shared services

Introduction of

QHR Health’s vision

for the future

3

Since Leaving the Wigwam…

4

5

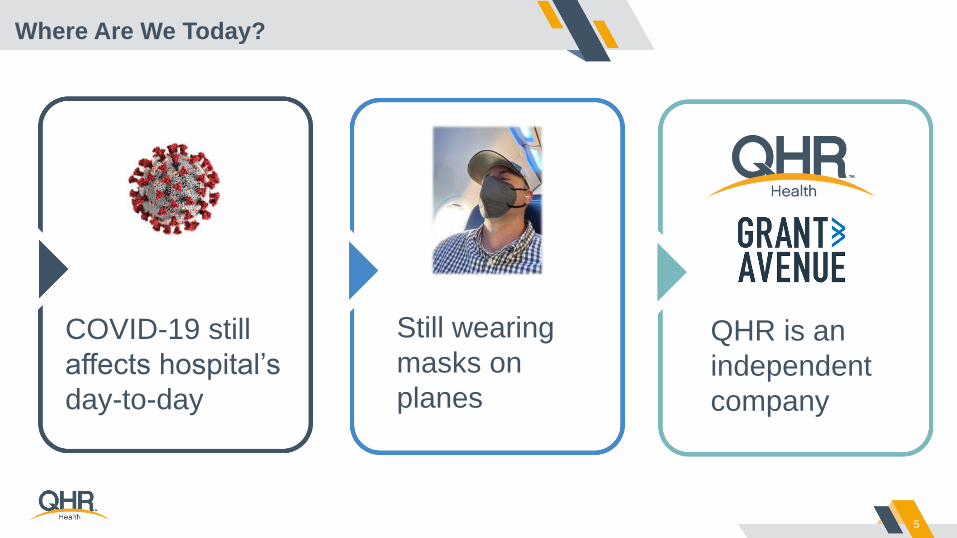

Where Are We Today?

COVID-19 still

affects hospital’s

day-to-day

QHR is an

independent

company

Still wearing

masks on

planes

6

Add Strategy Screenshot

7

Grant Avenue Capital Partnership

Grant Avenue Capital Acquires QHR HealthInvesting in Independent Community Healthcare

Overview• Healthcare-focused private equity firm with deep healthcare network, long-term partner-focused approach,

and forward-thinking strategic mindset

Why Grant Avenue?• Commitment to QHR Health’s mission of strengthening independent community healthcare

• Experience with supporting technology-enabled shared services

• Meaningfully investing to bring real differentiated value to QHR Health clients

8

QHR’s Brand and Mission Remain Strong

9

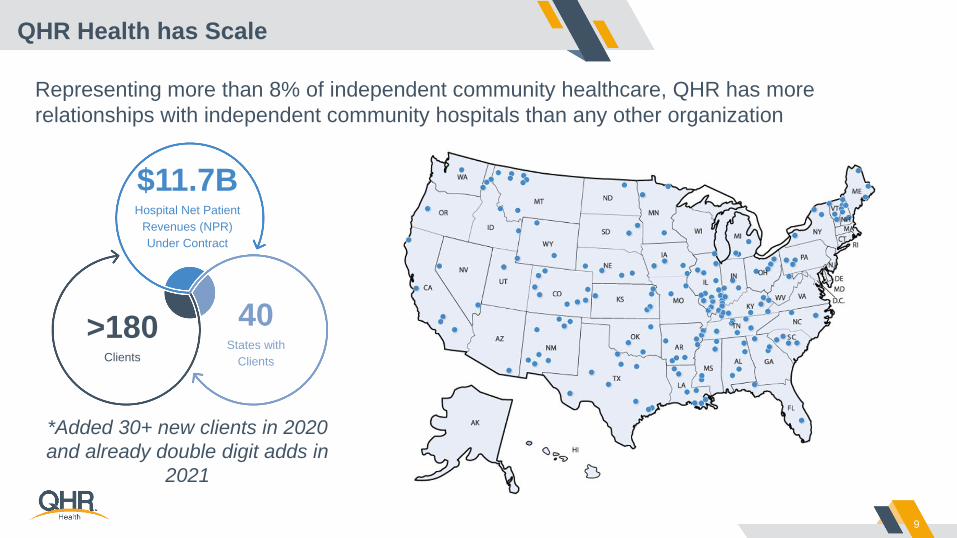

Representing more than 8% of independent community healthcare, QHR has more

relationships with independent community hospitals than any other organization

$11.7BHospital Net Patient

Revenues (NPR)

Under Contract

>180Clients

40States with

Clients

QHR Health has Scale

*Added 30+ new clients in 2020

and already double digit adds in

2021

10

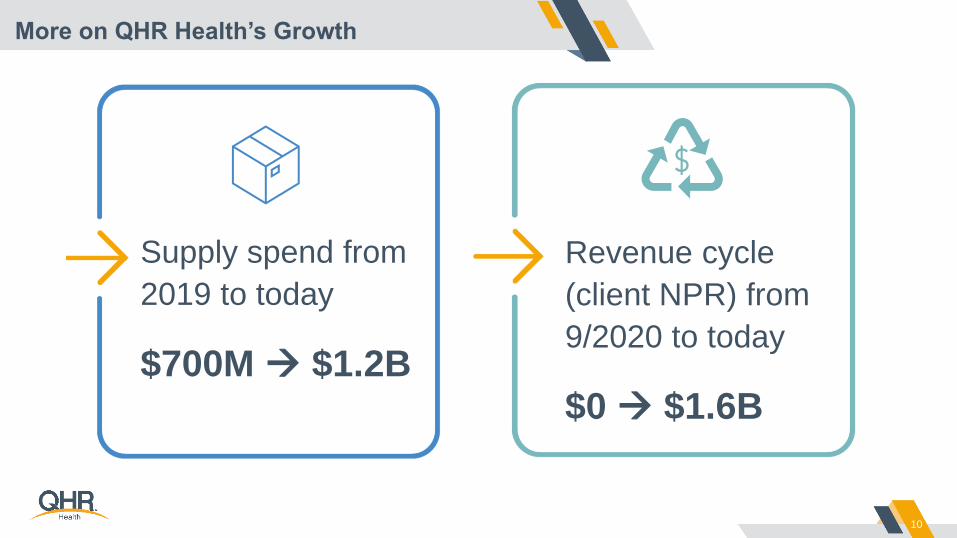

More on QHR Health’s Growth

Supply spend from

2019 to today

$700M → $1.2B

Revenue cycle

(client NPR) from

9/2020 to today

$0 → $1.6B

11

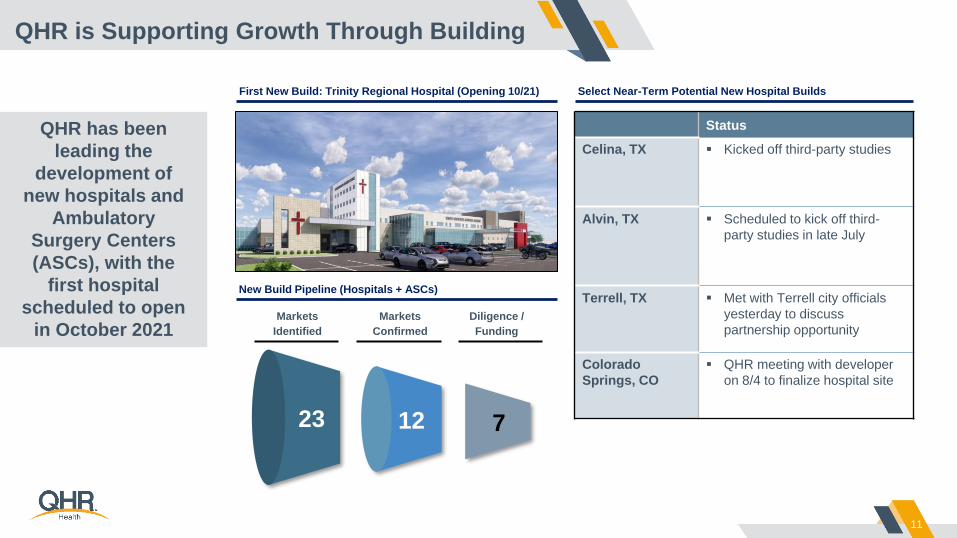

QHR is Supporting Growth Through Building

First New Build: Trinity Regional Hospital (Opening 10/21) Select Near-Term Potential New Hospital Builds

New Build Pipeline (Hospitals + ASCs)

Status

Celina, TX ▪ Kicked off third-party studies

Alvin, TX ▪ Scheduled to kick off third-

party studies in late July

Terrell, TX ▪ Met with Terrell city officials

yesterday to discuss

partnership opportunity

Colorado

Springs, CO

▪ QHR meeting with developer

on 8/4 to finalize hospital site

23 12 7

Diligence /

Funding

Markets

Confirmed

Markets

Identified

QHR has been

leading the

development of

new hospitals and

Ambulatory

Surgery Centers

(ASCs), with the

first hospital

scheduled to open

in October 2021

12

The “QHR Health Way”

QHR Health Councils More to come!

Operating Practices Diligence

Technology Vantage

Education QLI & Leadership U

13

Support

Independence

through QHR

Shared

Services

(Power Plants)

Invest in

Creating

Revenue for

our Hospitals

Prepare for

Technology

beyond EHR

Influence

Policy in

Rural

Communities

Develop Next

Generation of

Hospital

Leadership

QHR Health Continues its Committed Vision

14

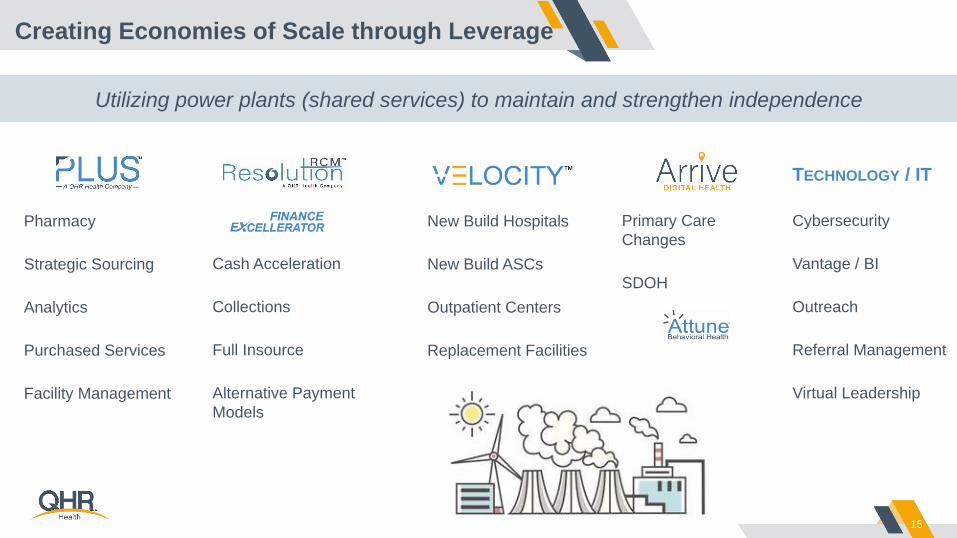

Delivering Our Vision to You Requires Power

15

Creating Economies of Scale through Leverage

Utilizing power plants (shared services) to maintain and strengthen independence

Pharmacy

Strategic Sourcing

Analytics

Purchased Services

Facility Management

Cash Acceleration

Collections

Full Insource

Alternative Payment

Models

New Build Hospitals

New Build ASCs

Outpatient Centers

Replacement Facilities

Primary Care

Changes

SDOH

Cybersecurity

Vantage / BI

Outreach

Referral Management

Virtual Leadership

TECHNOLOGY / IT

16

The Power Plants in Motion

17

Driving Forces in Healthcare

18

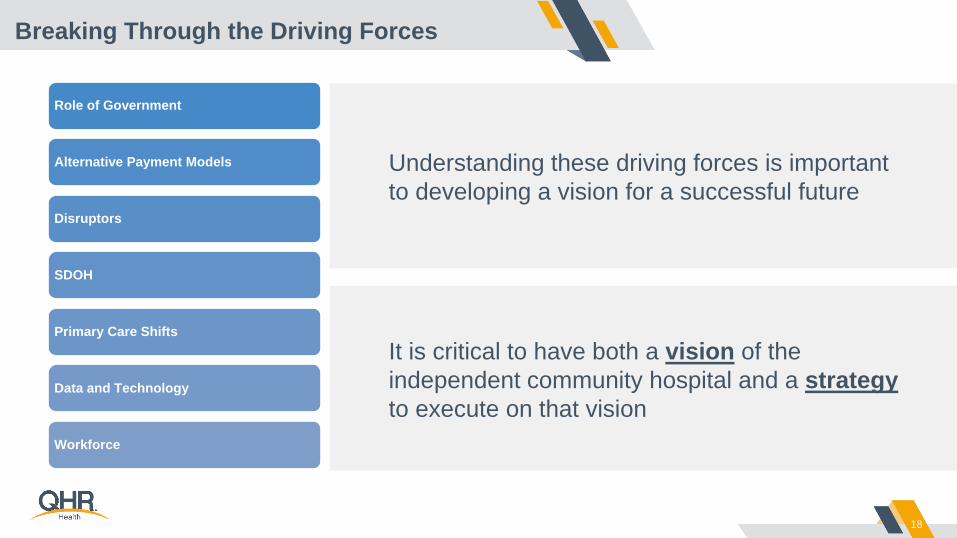

Breaking Through the Driving Forces

Understanding these driving forces is important

to developing a vision for a successful future

It is critical to have both a vision of the

independent community hospital and a strategy

to execute on that vision

Role of Government

Alternative Payment Models

Disruptors

SDOH

Primary Care Shifts

Data and Technology

Workforce

19

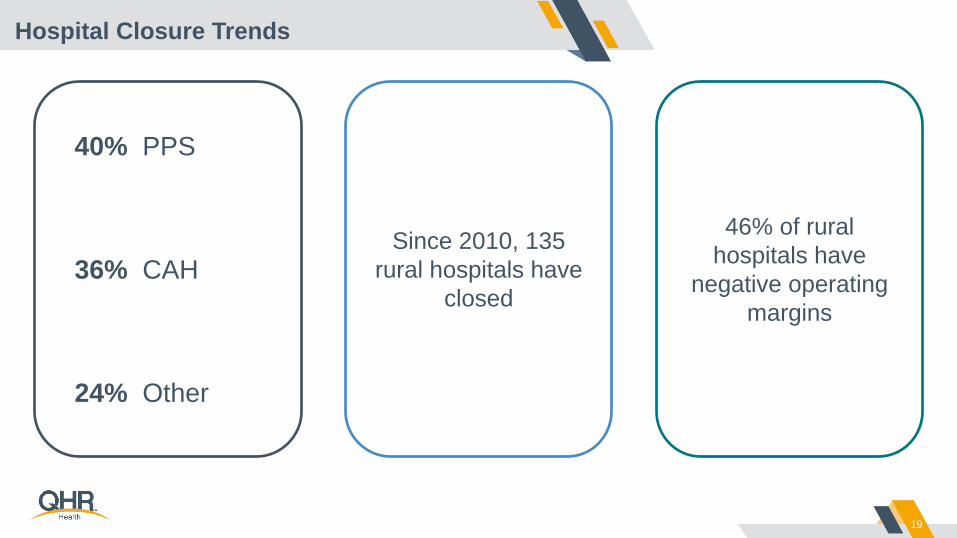

Hospital Closure Trends

Since 2010, 135

rural hospitals have

closed

46% of rural

hospitals have

negative operating

margins

40% PPS

36% CAH

24% Other

20

Rural versus Urban

Source: NRHA

21

United States Population Shifts

Source: US Dep’t of Commerce, Bureau of the Census

Change +1.9% +2.7% +44.3% +31.6%

22

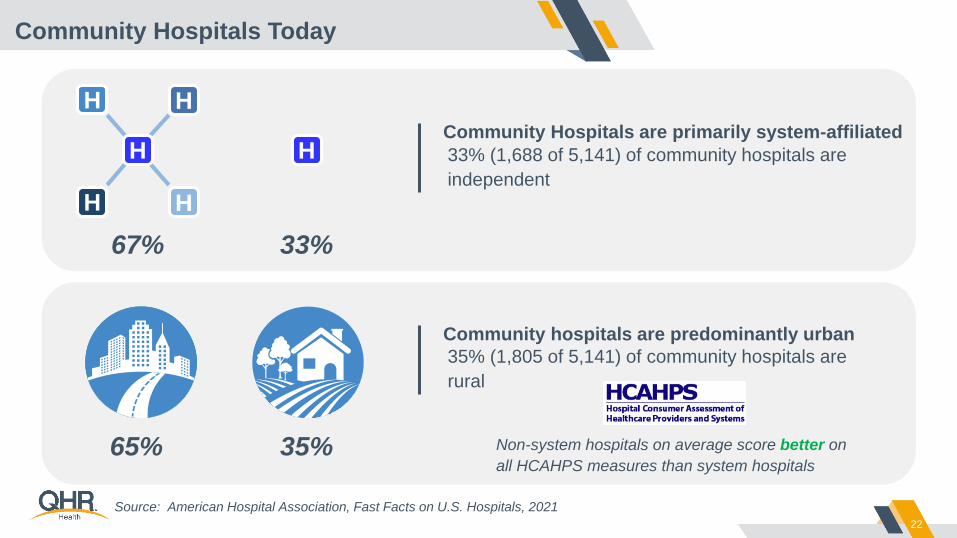

Community Hospitals Today

33% (1,688 of 5,141) of community hospitals are

independent

Community Hospitals are primarily system-affiliatedHH

H H

H H

67% 33%

Source: American Hospital Association, Fast Facts on U.S. Hospitals, 2021

35% (1,805 of 5,141) of community hospitals are

rural

Community hospitals are predominantly urban

65% 35% Non-system hospitals on average score better on

all HCAHPS measures than system hospitals

23

Newly-formed to support effective non-profits working in

communities QHR serves

State Hospital Associations

QHR Engages for Community Healthcare

Formed a policy team to stay current on

key policy changes, legislative updates,

and other factors affecting independent

community hospitals—including sharing

with our clients directly and through QLI.

Constantly exploring new opportunities

for independent community hospitals,

including demonstration projects and

novel site designations:• Rural Emergency Hospital (REH)

designation

• Community Health Access and Rural

Transformation (CHART) model

24

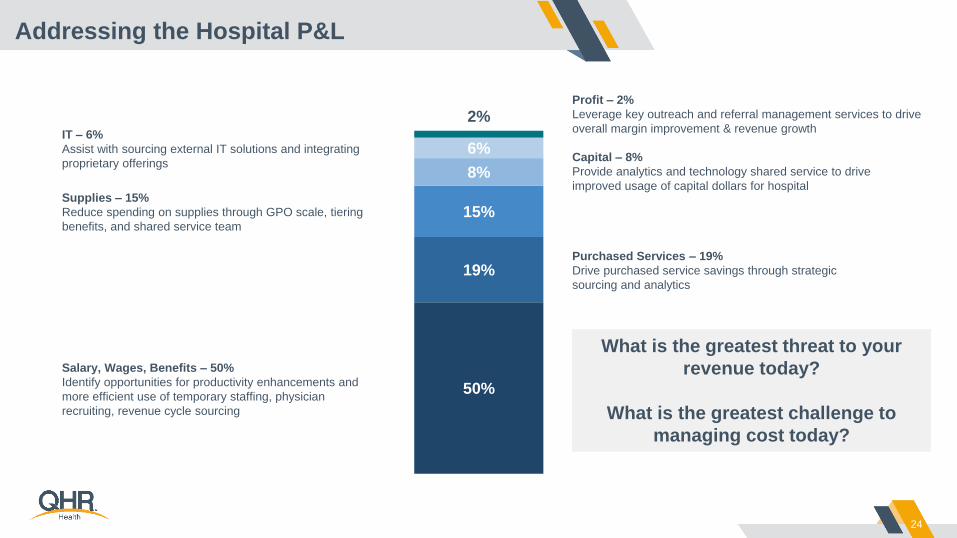

50%

19%

15%

8%

6%

2%Profit – 2%

Leverage key outreach and referral management services to drive

overall margin improvement & revenue growthIT – 6%

Assist with sourcing external IT solutions and integrating

proprietary offeringsCapital – 8%

Provide analytics and technology shared service to drive

improved usage of capital dollars for hospital

Purchased Services – 19%

Drive purchased service savings through strategic

sourcing and analytics

Supplies – 15%

Reduce spending on supplies through GPO scale, tiering

benefits, and shared service team

Salary, Wages, Benefits – 50%

Identify opportunities for productivity enhancements and

more efficient use of temporary staffing, physician

recruiting, revenue cycle sourcing

Addressing the Hospital P&L

What is the greatest threat to your

revenue today?

What is the greatest challenge to

managing cost today?

25

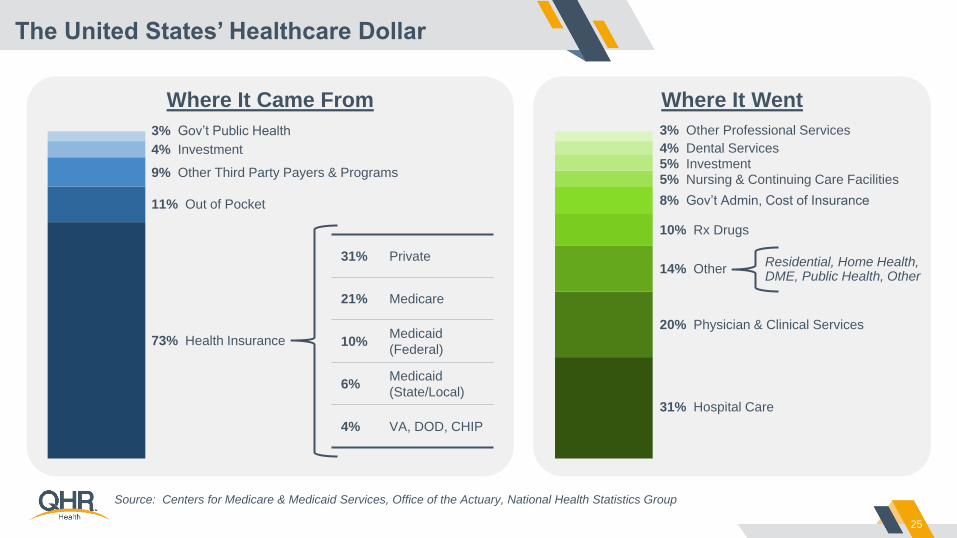

The United States’ Healthcare Dollar

Source: Centers for Medicare & Medicaid Services, Office of the Actuary, National Health Statistics Group

Where It Came From

73% Health Insurance

4% Investment

9% Other Third Party Payers & Programs

11% Out of Pocket

3% Gov’t Public Health

31% Private

21% Medicare

10%Medicaid

(Federal)

6%Medicaid

(State/Local)

4% VA, DOD, CHIP

Where It Went

31% Hospital Care

10% Rx Drugs

14% Other

20% Physician & Clinical Services

8% Gov’t Admin, Cost of Insurance

5% Nursing & Continuing Care Facilities

5% Investment

4% Dental Services

3% Other Professional Services

Residential, Home Health, DME, Public Health, Other

26

Inpatient to Outpatient Shifts

60%

30%

40%

70%

2020

1995

Inpatient vs. Outpatient Revenue

% IP Revenue % OP Revenue

Source: American Hospital Association

36.4

%

36.6

%

37.0

%

36.5

%

36.5

%

36.1

%

35.5

%

35.1

%

34.0

%

33.8

%

33.2

%

32.6

%

32.4

%

32.0

%

31.6

%

63.6

%

63.4

%

63.0

%

63.5

%

63.5

%

63.9

%

64.5

%

64.9

%

66.0

%

66.2

%

66.8

%

67.4

%

67.6

%

68.0

%

68.4

%

2005 2007 2009 2011 2013 2015 2017 2019

Inpatient vs. Outpatient Surgeries

Inpatient Outpatient

27

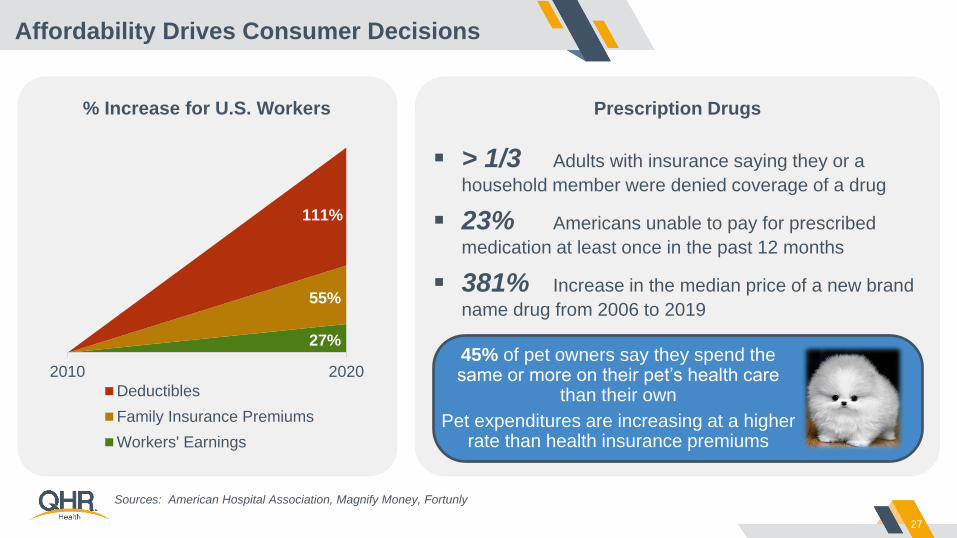

Affordability Drives Consumer Decisions

27%

55%

111%

2010 2020

% Increase for U.S. Workers

Deductibles

Family Insurance Premiums

Workers' Earnings

Prescription Drugs

▪ > 1/3 Adults with insurance saying they or a

household member were denied coverage of a drug

▪ 23% Americans unable to pay for prescribed

medication at least once in the past 12 months

▪ 381% Increase in the median price of a new brand

name drug from 2006 to 2019

45% of pet owners say they spend the same or more on their pet’s health care

than their own

Pet expenditures are increasing at a higher rate than health insurance premiums

Sources: American Hospital Association, Magnify Money, Fortunly

28

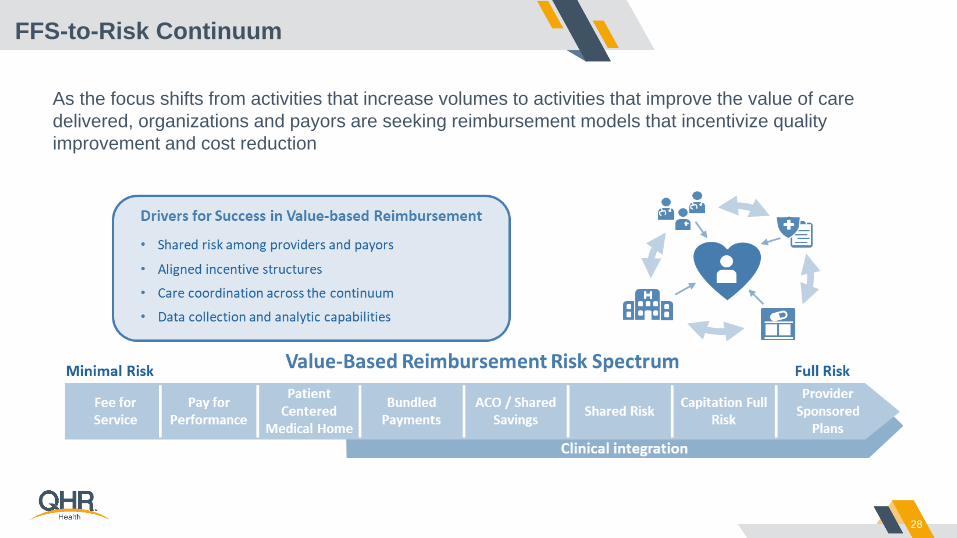

FFS-to-Risk Continuum

As the focus shifts from activities that increase volumes to activities that improve the value of care

delivered, organizations and payors are seeking reimbursement models that incentivize quality

improvement and cost reduction

29

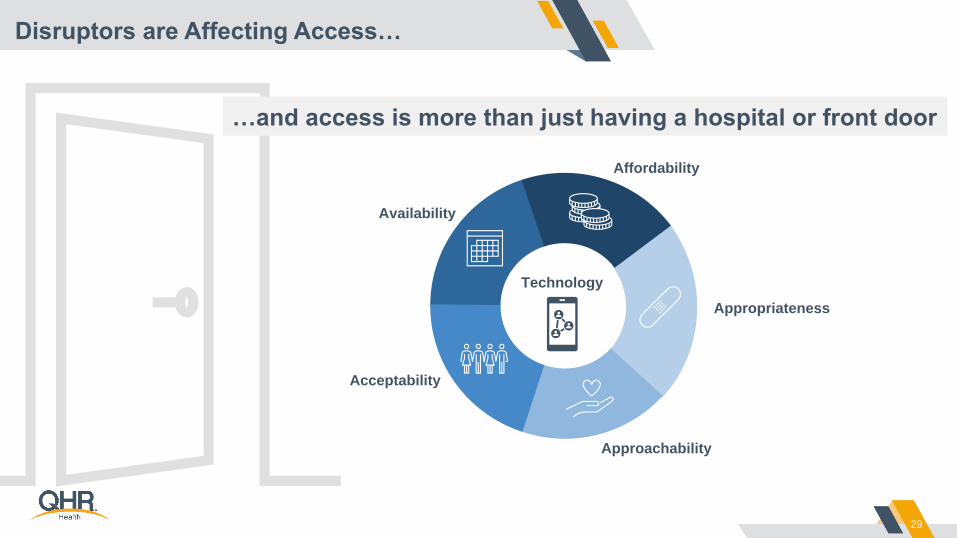

Disruptors are Affecting Access…

…and access is more than just having a hospital or front door

Approachability

Acceptability

Availability

Affordability

Appropriateness

Technology

30

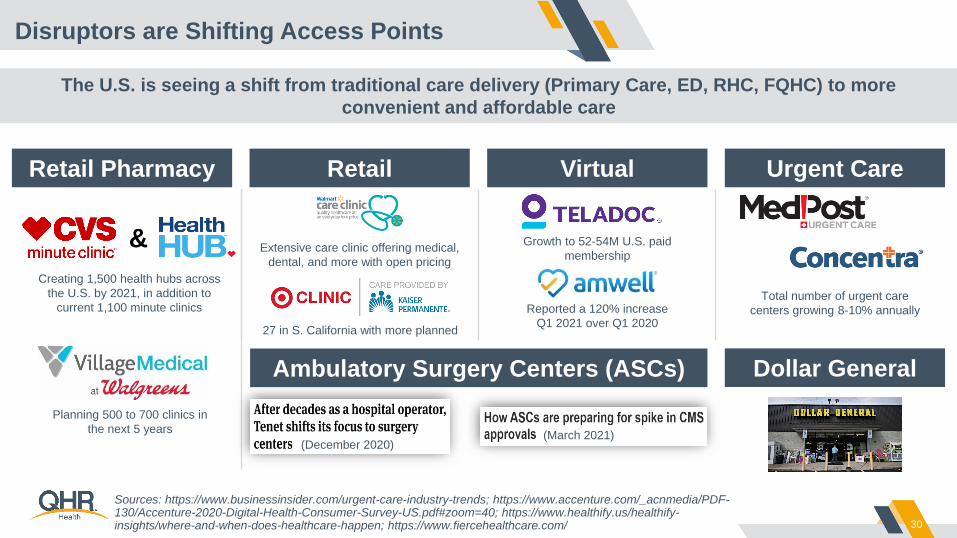

Disruptors are Shifting Access Points

The U.S. is seeing a shift from traditional care delivery (Primary Care, ED, RHC, FQHC) to more

convenient and affordable care

RetailRetail Pharmacy Urgent CareVirtual

&

Total number of urgent care

centers growing 8-10% annuallyReported a 120% increase

Q1 2021 over Q1 2020

Growth to 52-54M U.S. paid

membership

Creating 1,500 health hubs across

the U.S. by 2021, in addition to

current 1,100 minute clinics

Planning 500 to 700 clinics in

the next 5 years

27 in S. California with more planned

Extensive care clinic offering medical,

dental, and more with open pricing

Ambulatory Surgery Centers (ASCs)

(December 2020)(March 2021)

Sources: https://www.businessinsider.com/urgent-care-industry-trends; https://www.accenture.com/_acnmedia/PDF-130/Accenture-2020-Digital-Health-Consumer-Survey-US.pdf#zoom=40; https://www.healthify.us/healthify-insights/where-and-when-does-healthcare-happen; https://www.fiercehealthcare.com/

Dollar General

31

Dollar General?

32

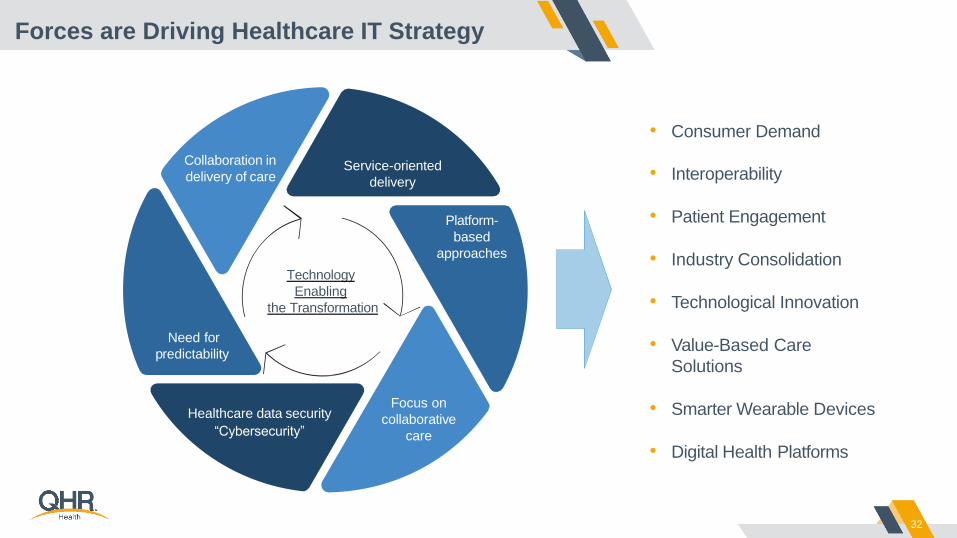

Forces are Driving Healthcare IT Strategy

Collaboration in

delivery of care

Healthcare data security

“Cybersecurity”

Platform-

based

approaches

Focus on

collaborative

care

Service-oriented

delivery

Need for

predictability

Technology

Enabling

the Transformation

• Consumer Demand

• Interoperability

• Patient Engagement

• Industry Consolidation

• Technological Innovation

• Value-Based Care

Solutions

• Smarter Wearable Devices

• Digital Health Platforms

33

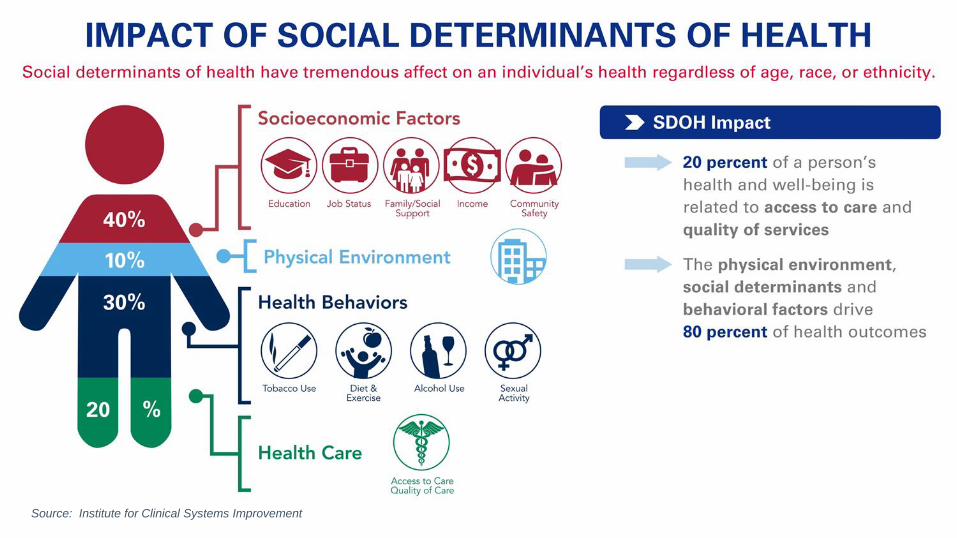

More on SDOH

Source: American Hospital Association

34

More on SDOH

Source: Institute for Clinical Systems Improvement

35

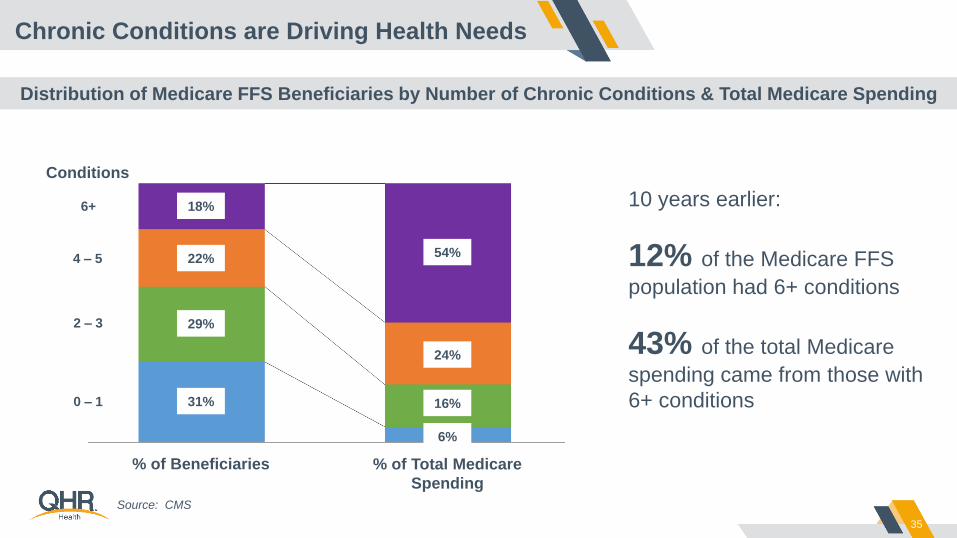

Chronic Conditions are Driving Health Needs

Distribution of Medicare FFS Beneficiaries by Number of Chronic Conditions & Total Medicare Spending

% of Beneficiaries % of Total Medicare

Spending

Source: CMS

18%

22%

29%

31%

54%

24%

16%

6%

Conditions

0 – 1

2 – 3

4 – 5

6+ 10 years earlier:

12% of the Medicare FFS

population had 6+ conditions

43% of the total Medicare

spending came from those with

6+ conditions

36

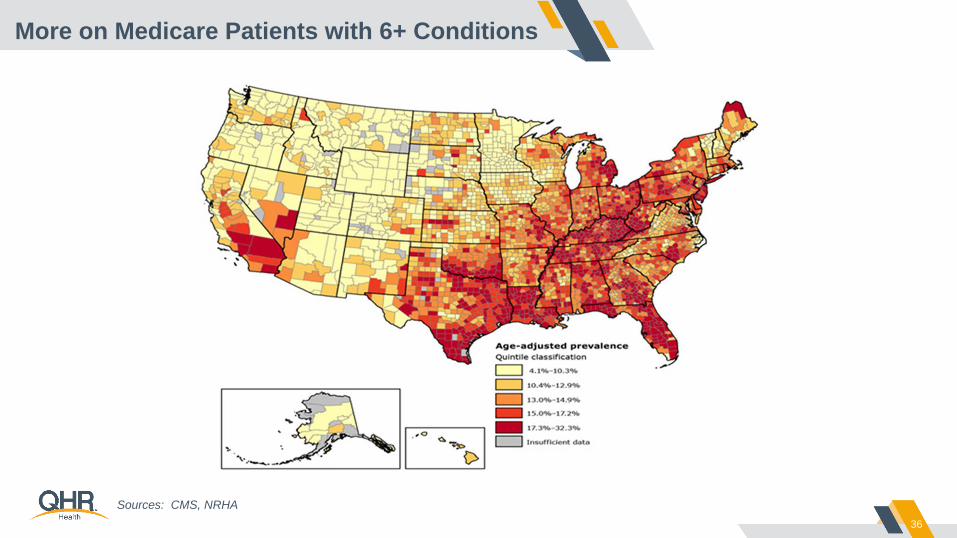

More on Medicare Patients with 6+ Conditions

Sources: CMS, NRHA

37

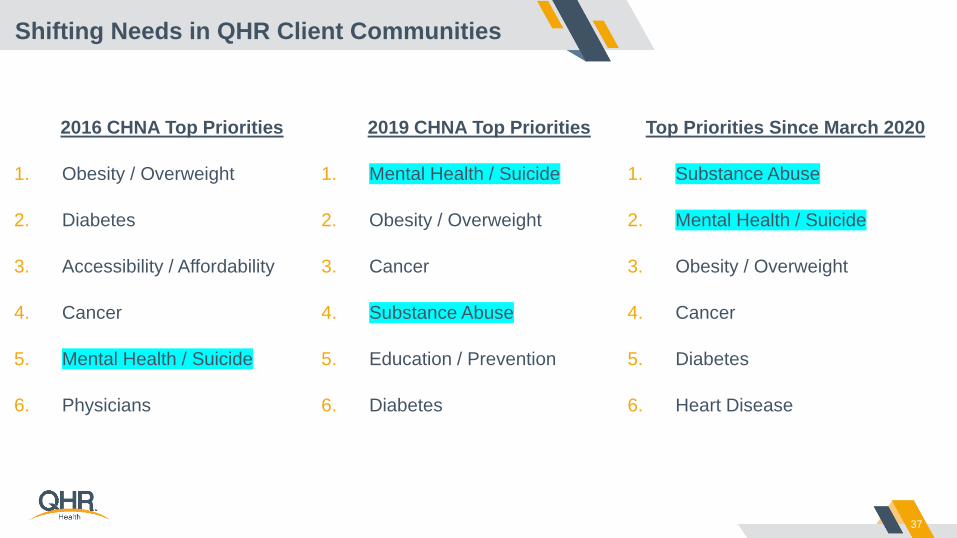

Shifting Needs in QHR Client Communities

2016 CHNA Top Priorities

1. Obesity / Overweight

2. Diabetes

3. Accessibility / Affordability

4. Cancer

5. Mental Health / Suicide

6. Physicians

2019 CHNA Top Priorities

1. Mental Health / Suicide

2. Obesity / Overweight

3. Cancer

4. Substance Abuse

5. Education / Prevention

6. Diabetes

Top Priorities Since March 2020

1. Substance Abuse

2. Mental Health / Suicide

3. Obesity / Overweight

4. Cancer

5. Diabetes

6. Heart Disease

38

Sample QHR Health Client Market Share

1

2

31

2

3

Primary Service Area Secondary Service Area

Securing and growing market share is critical to supplying needed care locally to the community and to

provide funding for investments and additional growth

56%44% 35%

Hosp 1 Hosp 2 Hosp 3

12% 6% 3%

Hosp 1 Hosp 2 Hosp 3

45% 44%32%

Hosp 1 Hosp 2 Hosp 3

3% 7% 7%

Hosp 1 Hosp 2 Hosp 3

57%38%

26%

Hosp 1 Hosp 2 Hosp 3

12% 10% 9%

Hosp 1 Hosp 2 Hosp 3

39

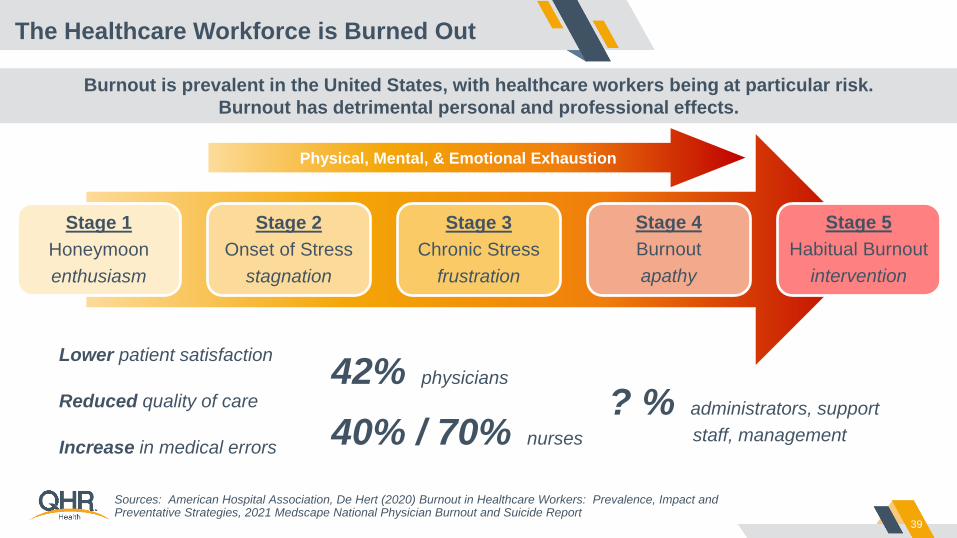

The Healthcare Workforce is Burned Out

Burnout is prevalent in the United States, with healthcare workers being at particular risk.

Burnout has detrimental personal and professional effects.

Stage 1

Honeymoon

enthusiasm

Stage 2

Onset of Stress

stagnation

Stage 3

Chronic Stress

frustration

Stage 4

Burnout

apathy

Stage 5

Habitual Burnout

intervention

Physical, Mental, & Emotional Exhaustion

Sources: American Hospital Association, De Hert (2020) Burnout in Healthcare Workers: Prevalence, Impact and Preventative Strategies, 2021 Medscape National Physician Burnout and Suicide Report

Lower patient satisfaction

Reduced quality of care

Increase in medical errors

42% physicians

40% / 70% nurses

? % administrators, support

staff, management

40

Vision and Strategy

41

Vision and Strategy Must Intersect

QHR Health believes that independent

community healthcare must:

Imagine what it will take to…

…grow a healthier community by

engaging each person at the right

time, in the right place, and using the

right data and technology

42

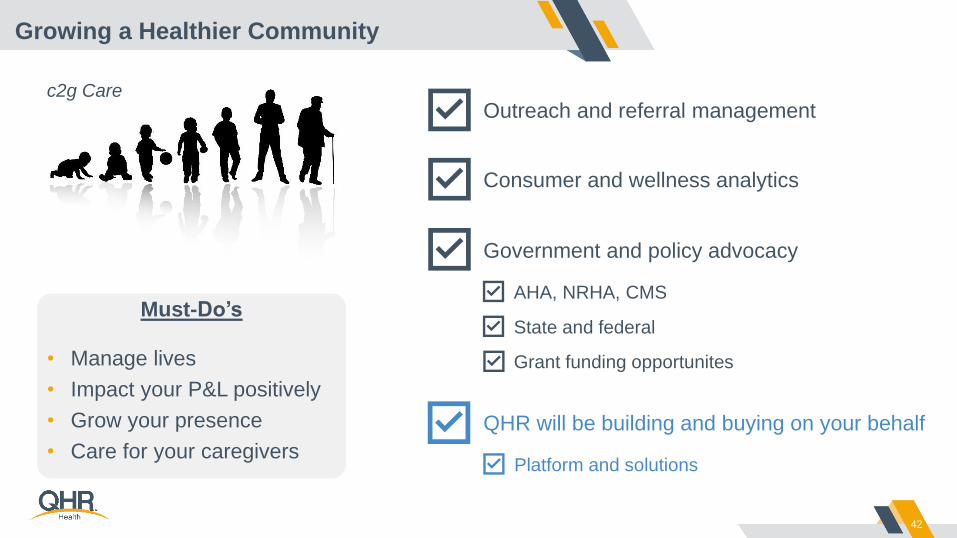

Growing a Healthier Community

Outreach and referral management

Consumer and wellness analytics

Government and policy advocacy

AHA, NRHA, CMS

State and federal

Grant funding opportunites

Must-Do’s

• Manage lives

• Impact your P&L positively

• Grow your presence

• Care for your caregivers

QHR will be building and buying on your behalf

Platform and solutions

c2g Care

43

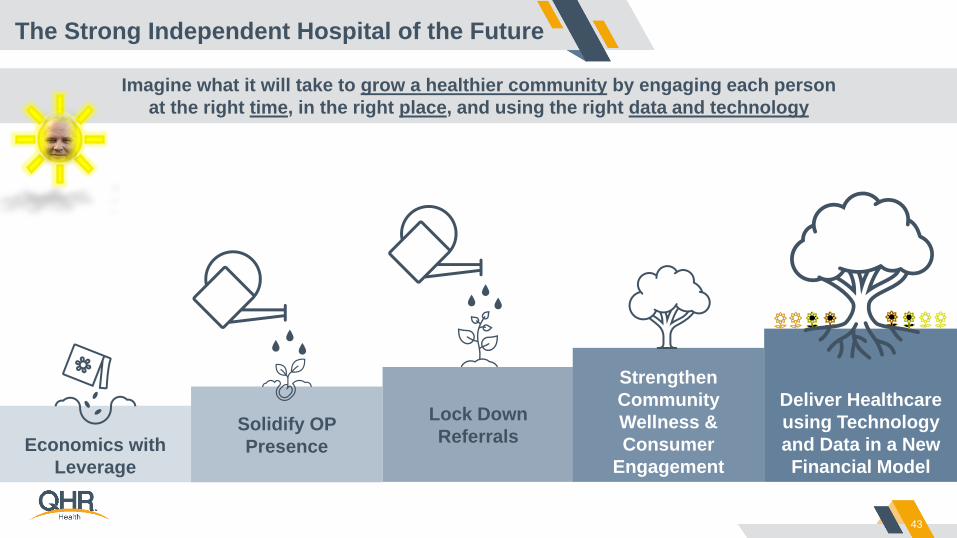

The Strong Independent Hospital of the Future

Imagine what it will take to grow a healthier community by engaging each person

at the right time, in the right place, and using the right data and technology

Economics with

Leverage

Solidify OP

Presence

Lock Down

Referrals

Strengthen

Community

Wellness &

Consumer

Engagement

Deliver Healthcare

using Technology

and Data in a New

Financial Model

44

At the Intersection of Vision and Strategy

QHR in 2021

Growing, Investing, Building

QHR 3-Year Vision

Tech-enabled “power plant”

provider for healthcare facilities

Human CapitalDevelop team, help hospitals with resource

needs, invest in QHR Learning Institute

Service ExpansionNew service lines to focus on the following: Other shared

services (i.e. IT solutions, telehealth, behavioral health) and

managing new developments / ASCs / medical office buildings

Core Operational EfficiencyOpportunities for enhanced efficiency include

RCM tech investment, “QHR Health Way”

Methodology, RPA, Business Intelligence

Tech EnablementInvest in QHR’s technology roadmap

(“Vantage”), which will collect sharable data

across facilities and identify specific areas

with operational improvement potential

Hospital StrategyProactively partner in local

communities to drive market

share & operational strategies

Strengthening Independent Community Healthcare

45

Introducing the QHR Advisory Councils

To advance the ongoing discussion of Vision & Strategy, and to help you continue to

grow healthier communities, QHR is establishing Advisory Councils

For more information

contact your QHR

representative or

Chip Holmes, SVP

802.377.0676

• Board Advisory Council

• Executive Advisory Council

– Listening

– Learning

– Leading

– Together

• First Meeting: Virtual Fall 2021

• First Face to Face Meeting: Phoenix 2022

46

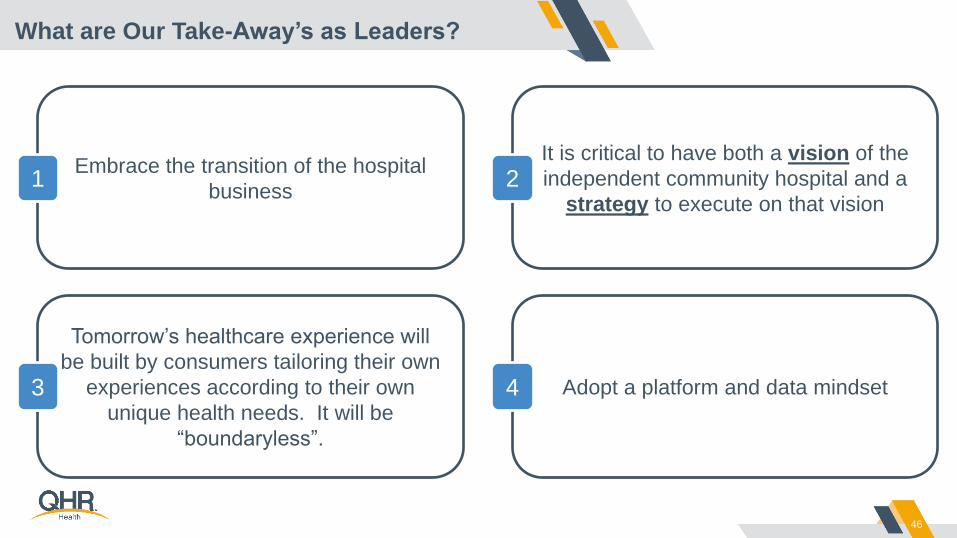

What are Our Take-Away’s as Leaders?

Embrace the transition of the hospital

business

It is critical to have both a vision of the

independent community hospital and a

strategy to execute on that vision

Tomorrow’s healthcare experience will

be built by consumers tailoring their own

experiences according to their own

unique health needs. It will be

“boundaryless”.

Adopt a platform and data mindset

1

3

2

4

47

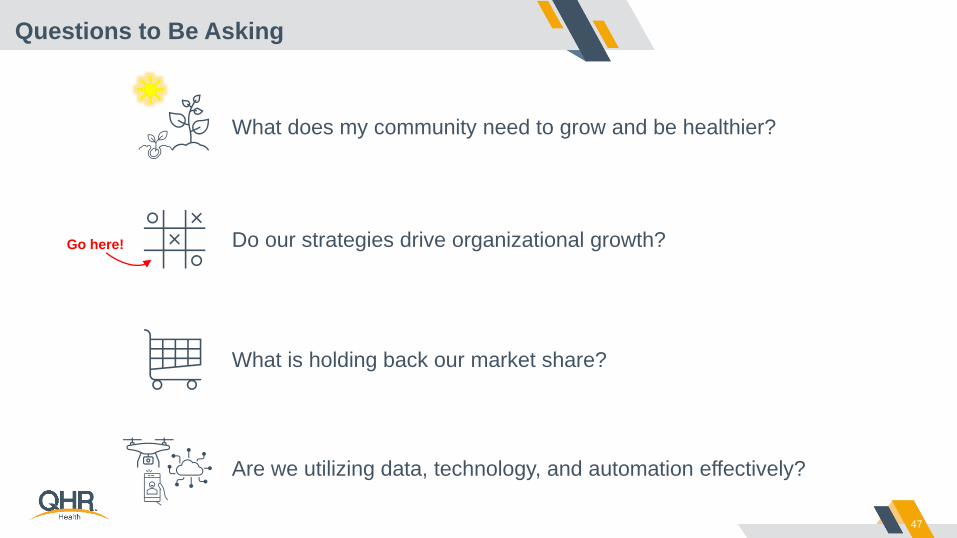

Questions to Be Asking

What does my community need to grow and be healthier?

Do our strategies drive organizational growth?Go here!

What is holding back our market share?

Are we utilizing data, technology, and automation effectively?

48

And a Final Take-Away…

We need radical interdependence.

We need each other.

Thank You

This presentation may contain information that is

Proprietary, Confidential, or legally privileged or

protected. Do not deliver, distribute or copy this

message and do not disclose its contents or take any

action in reliance on the information it contains.

This presentation may contain information that is

Proprietary, Confidential, or legally privileged or

protected. Do not deliver, distribute or copy this

message and do not disclose its contents or take any

action in reliance on the information it contains.