speculation, returns, volumes and volatility in commodities

TRANSCRIPT

Speculation, Returns, Volumes and Volatility in Commodities Futures MarketsMatteo ManeraUniversity of Milano-Bicocca and FEEMjoint with Andrea Bastianin – University of Milano-Bicocca and FEEMMarcella Nicolini – University of Pavia and FEEMIlaria Vignati – FEEM

Financial Speculation in the Oil Market and the Determinants of the Oil Price

FEEM, 12-13 January

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets1

1. Investigate the relationship between returns on futures prices of energy and non-energy commodities and financial speculation:−

Does speculation help to explain commodities returns?

−

Does speculation influence price volatility?−

Which macroeconomic factors are relevant in modeling returns?

2. Measure the “vulnerability”

of commodities futures markets to financial speculation:−

Volume-volatility relations

−

How much liquidity is needed to alter futures prices?−

Excess speculation and position limits

1. Motivation

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets2

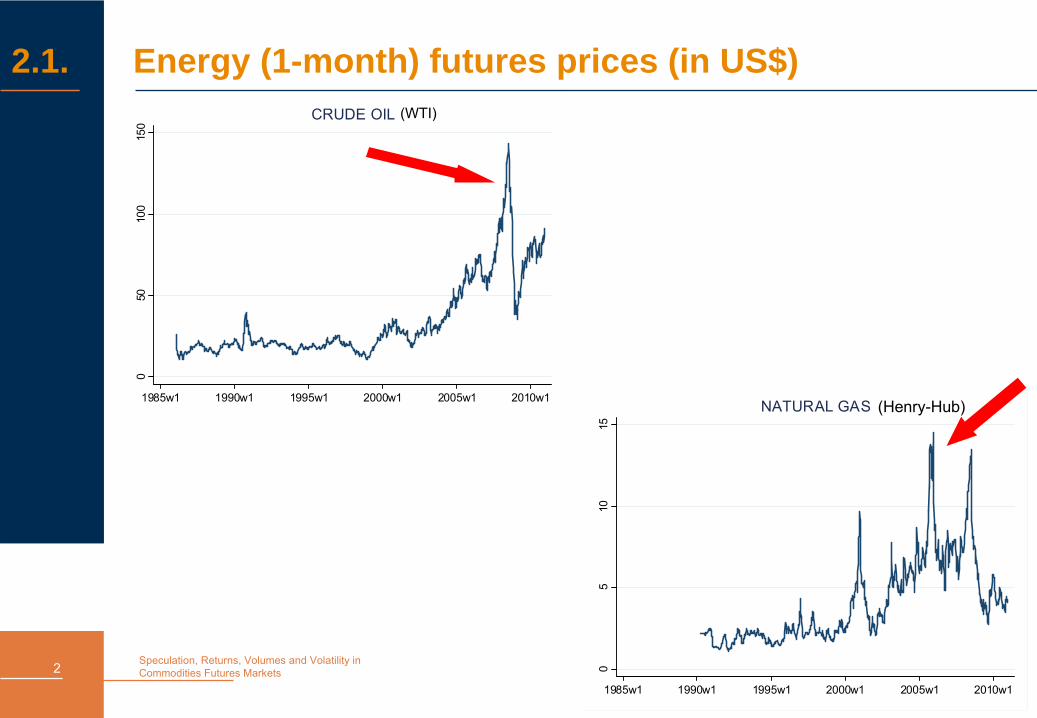

2.1. Energy (1-month) futures prices (in US$)

Sezione 2

Sezione 3

Sezione 2.1

050

100

150

1985w1 1990w1 1995w1 2000w1 2005w1 2010w1

CRUDE OIL

05

1015

1985w1 1990w1 1995w1 2000w1 2005w1 2010w1

NATURAL GAS

(WTI)

(Henry-Hub)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets3

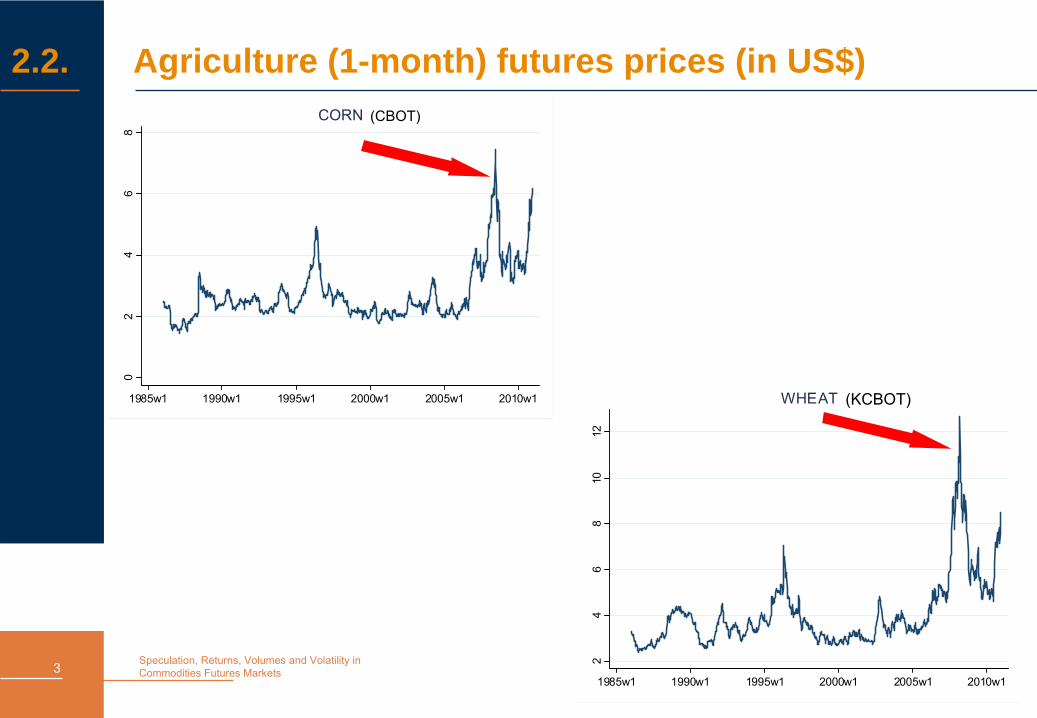

2.2. Agriculture (1-month) futures prices (in US$)

Sezione 2

Sezione 3

Sezione 2.1

02

46

8

1985w1 1990w1 1995w1 2000w1 2005w1 2010w1

CORN

24

68

1012

1985w1 1990w1 1995w1 2000w1 2005w1 2010w1

WHEAT (KCBOT)

(CBOT)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets4

2.3. Stylized facts on commodity prices

•

From 2000 to 2008 a sharp increase is observed in:Energy pricesFood pricesNumber of participants (both hedgers and speculators) in commodities futures markets

•

These stylized facts have led to claim that:oil/energy prices are responsible for food price increasesspeculators drive energy and food prices speculators affect commodities price volatility

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets5

3.1. Literature review: oil prices and macroeconomic factors

•

Main macroeconomic factors which affect commodities futures returns:

Treasury bill yieldsEquity dividend yieldsJunk bond premiaExchange rates

(e.g. Sadorsky

2002; Chevallier

2009; Chen, Rogoff

and Rossi 2009)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets6

3.2. Literature review: oil prices and speculation

•

Several papers suggest that the increasing presence of speculators in the oil futures markets could explain the oil price spikes in 2007-2008 (e.g. Masters 2008; Medlock III and Jaffe, 2009)

•

However, other papers show that the two phenomena are not related (e.g. Irwin and Sanders 2010; Büyükşahin

and Harris, 2011)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets7

4.1. Data description: dependent variable

•

Dependent variable: returns on futures prices for4 energy commodities [crude oil, gasoline, heating oil, natural gas (NYMEX)]5 non-energy commodities [corn, oats, soybean oil, soybeans (CBOT) and wheat (KCBOT)]

•

Time period: 1986-2010

•

Frequency: weekly

•

Source: Datastream, CFTC (US Commodity Futures Trading Commission), FRED (Federal Reserve Economic Data)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets8

4.2.a Data description: explanatory variables

•

Macroeconomic factors:

Returns on the annual yield on the 90-day T-bill

Returns of S&P 500 Index

Junk bond yield = (returns on the annual yield on Moody’s long-term-BAA-rated corporate bonds) –(returns on the annual yield on Moody’s long-term-AAA-rated corporate bonds)

Weighted exchange rate index (of the US dollar against a subset of broad index of currencies outside US)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets9

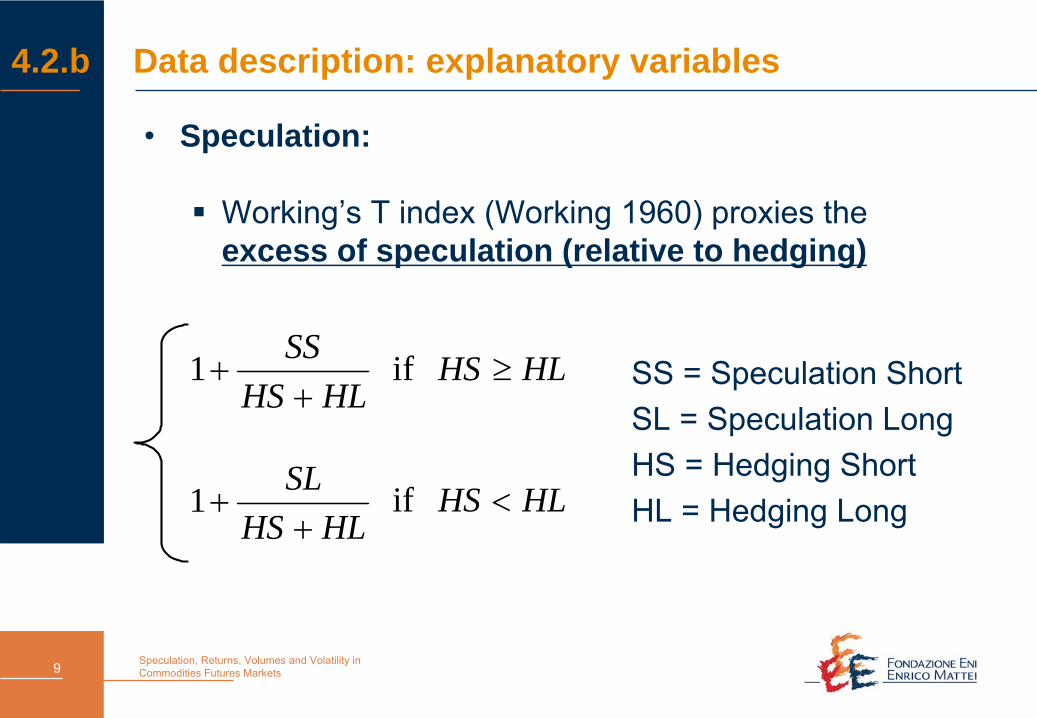

4.2.b Data description: explanatory variables

•

Speculation:

Working’s T index (Working 1960) proxies the excess of speculation (relative to hedging)

SS = Speculation ShortSL = Speculation LongHS = Hedging ShortHL = Hedging Long

HLHSSS+

+1 if HLHS ≥

HLHSSL+

+1 if HLHS <

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets10

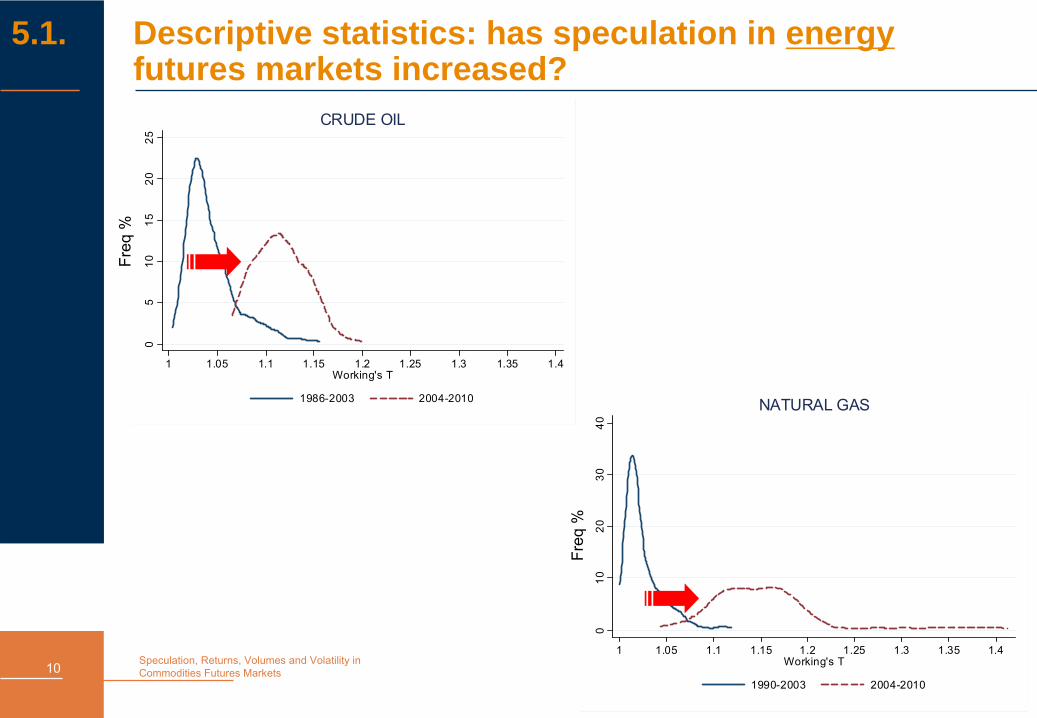

5.1. Descriptive statistics: has speculation in energy futures markets increased?

05

1015

2025

1 1.05 1.1 1.15 1.2 1.25 1.3 1.35 1.4Working's T

1986-2003 2004-2010

CRUDE OIL

010

2030

40

1 1.05 1.1 1.15 1.2 1.25 1.3 1.35 1.4Working's T

1990-2003 2004-2010

NATURAL GAS

Freq

%

Freq

%

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets11

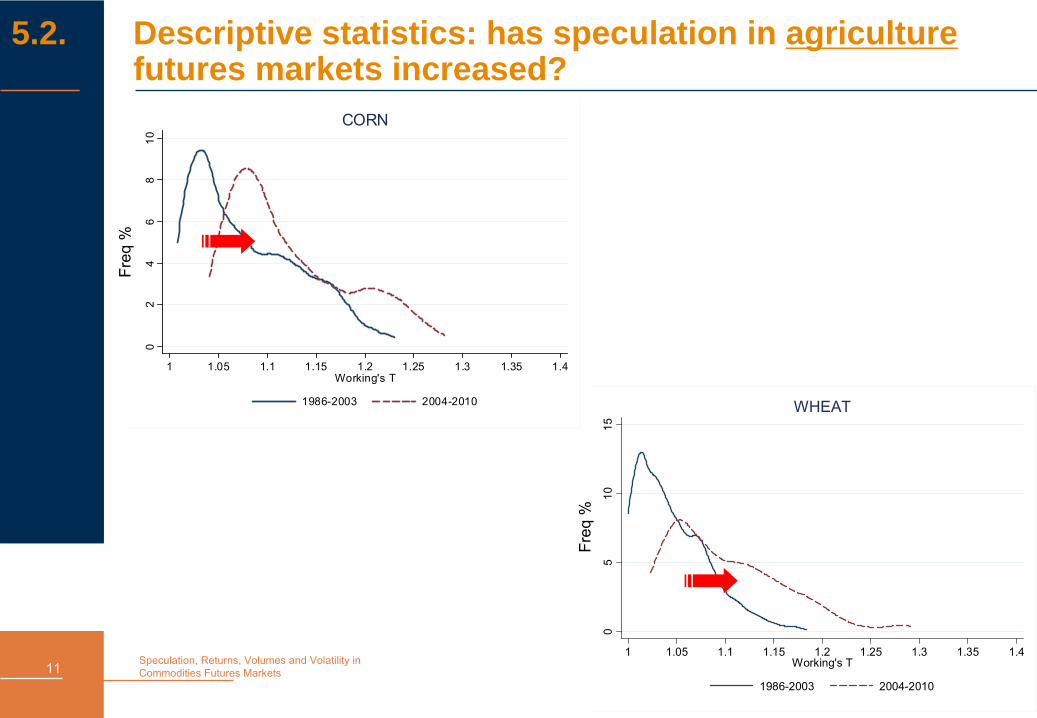

5.2. Descriptive statistics: has speculation in agriculture futures markets increased?

02

46

810

1 1.05 1.1 1.15 1.2 1.25 1.3 1.35 1.4Working's T

1986-2003 2004-2010

CORN

05

1015

1 1.05 1.1 1.15 1.2 1.25 1.3 1.35 1.4Working's T

1986-2003 2004-2010

WHEAT

Freq

%

Freq

%

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets12

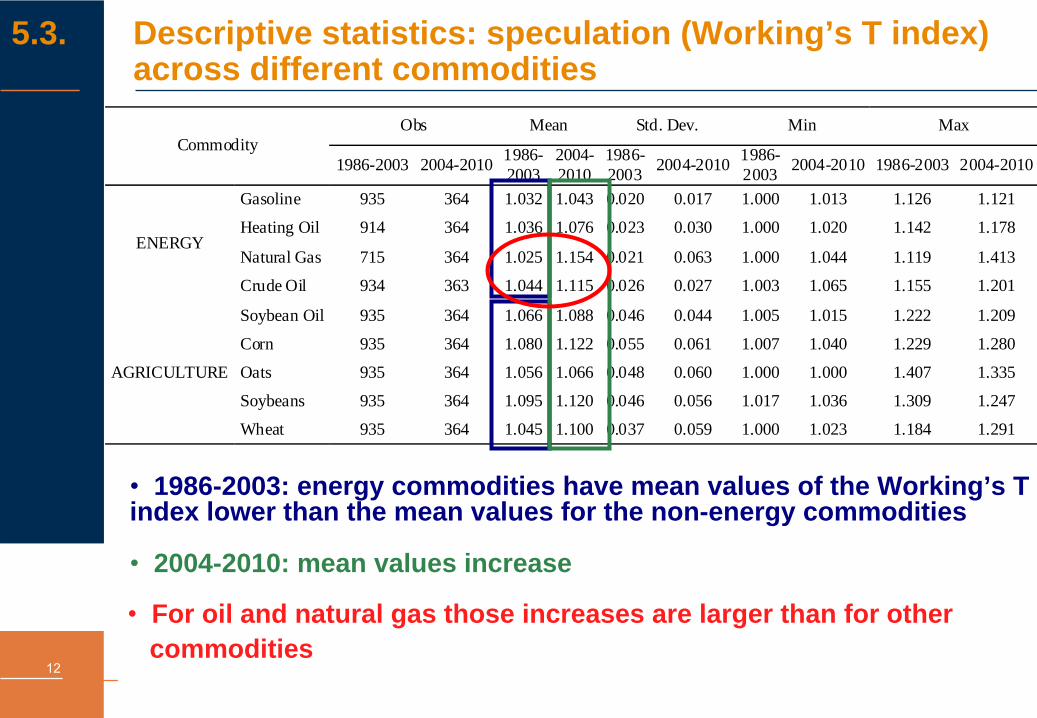

5.3. Descriptive statistics: speculation (Working’s T index) across different commodities

Obs Mean Std. Dev. Min Max Commodity

1986-2003 2004-2010 1986-2003

2004-2010

1986-2003 2004-2010 1986-

2003 2004-2010 1986-2003 2004-2010

Gasoline 935 364 1.032 1.043 0.020 0.017 1.000 1.013 1.126 1.121

Heating Oil 914 364 1.036 1.076 0.023 0.030 1.000 1.020 1.142 1.178

Natural Gas 715 364 1.025 1.154 0.021 0.063 1.000 1.044 1.119 1.413 ENERGY

Crude Oil 934 363 1.044 1.115 0.026 0.027 1.003 1.065 1.155 1.201

Soybean Oil 935 364 1.066 1.088 0.046 0.044 1.005 1.015 1.222 1.209

Corn 935 364 1.080 1.122 0.055 0.061 1.007 1.040 1.229 1.280

Oats 935 364 1.056 1.066 0.048 0.060 1.000 1.000 1.407 1.335

Soybeans 935 364 1.095 1.120 0.046 0.056 1.017 1.036 1.309 1.247

AGRICULTURE

Wheat 935 364 1.045 1.100 0.037 0.059 1.000 1.023 1.184 1.291

•

1986-2003: energy commodities have mean values of the Working’s T index lower than the mean values for the non-energy commodities

• For oil and natural gas those increases are larger than for othercommodities

• 2004-2010: mean values increase

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets13

6.1. Univariate ARMA-GARCH

•

Returns on futures prices for each commodity are explained by:

Treasury bill yieldsJunk bond premiaEquity dividend yieldsExchange ratesMeasures of speculation (i.e. Working’s T index)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets14

6.2. Results: Univariate ARMA-GARCH

Gasoline Heating Oil Natural Gas Crude Oil Soybean Oil Corn Oats Soybeans Wheat

Constant 0 .157 (0.066)

** 0.050(0.037)

0.051(0.029)

* -0.052(0.029)

* 0.035(0.018)

* 0.044(0.015)

*** -0.037(0.023)

0.026(0.014)

* 0.025 (0.017)

Tbill 0 .037 (0.015)

** 0.028(0.012)

** 0.016(0.017)

0.022(0.014)

0.012(0.009)

0.018(0.011)

* -0.001(0.012)

0.009(0.010)

0.011 (0.012)

Junk Bond Yield -0 .049 (0.032)

-0.023(0.027)

0.055(0.050)

-0.032(0.027)

-0.012(0.019)

-0.012(0.021)

-0.018(0.028)

-0.019(0.018)

-0.003 (0.019)

S&P 500 0 .065 (0.054)

0.096(0.050)

* 0.149(0.082)

* 0.133(0.051)

*** 0.101(0.035)

*** 0.070(0.036)

* 0.065(0.049)

0.090(0.033)

*** 0.039 (0.036)

Exchange Rate -0 .355 (0.134)

*** -0.566(0.115)

*** -0.133(0.190)

-0.383(0.122)

*** -0.277(0.089)

*** -0.145(0.087)

* -0.257(0.119)

** -0.195(0.073)

*** -0.119 (0.084)

Working’s T -0 .150 (0.064)

** -0.046(0.035)

-0.047(0.027)

* 0.050(0.028)

* -0.032(0.017)

* -0.040(0.014)

*** 0.035(0.021)

-0.022(0.013)

* -0.024 (0.016)

Mea

n E

quat

ion

AR(1) 0 .183 (0.029)

*** 0.170(0.030)

*** 0.202(0.033)

*** 0.152(0.029)

*** 0.220(0.027)

*** 0.195(0.028)

*** 0.173(0.028)

*** 0.204(0.030)

*** 0.210 (0.028)

***

Constant 0 .000 (0.000)

*** 0.000(0.000)

*** 0.000(0.000)

*** 0.000(0.000)

*** 0.000(0.000)

** 0.000(0.000)

*** 0.000(0.000)

*** 0.000(0.000)

*** 0.000 (0.000)

**

ARCH(1) 0 .114 (0.025)

*** 0.159(0.028)

*** 0.153(0.037)

*** 0.130(0.026)

*** 0.065(0.018)

*** 0.152(0.030)

*** 0.114(0.032)

*** 0.172(0.029)

*** 0.087 (0.018)

***

Var

ianc

e E

quat

ion

GARCH(1) 0 .830 (0.037)

*** 0.750(0.045)

*** 0.765(0.053)

*** 0.825(0.034)

*** 0.888(0.033)

*** 0.795(0.037)

*** 0.768(0.062)

*** 0.796(0.030)

*** 0.892 (0.022)

***

LM test for ARCH 63.549 *** 162.984 *** 8.492 *** 56.581 *** 27.570 *** 22.515 *** 88.271 *** 28.085 *** 32.637 *** Ljung-Box Q test (lag 1) 2 .301 0.150 0.618 0.387 0.209 0.001 0.516 0.064 0.404 Log Likelihood 2284 2398 1559 2401 2914 2820 2443 2995 2888 AIC -4546 -4773 -3096 -4781 -5807 -5617 -4864 -5968 -5755 BIC -4490 -4717 -3041 -4724 -5750 -5560 -4808 -5912 -5698 N. of Obs. 1298 1277 1078 1296 1298 1298 1298 1298 1298

Notes : error distribution is a Student’s T. Standard errors in parentheses. * significant at 10% level, ** significant at 5% level, *** significant at 1% level.

• Apart

from

crude oil, Working’s T index

is

negative or not

significant

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets15

6.3.a Multivariate GARCH

•

It is more informative to estimate a system where returns for different commodities are jointly estimated, allowing spillover

effects in the mean, variance and covariance

equations

•

With a multivariate GARCH model is possible to indentify

if and how returns on oil/energy futures prices

are related to food/non-energy commodities futures prices

•

Models: Constant Conditional Correlations (CCC) and Dynamic (i.e. time-varying) Conditional Correlations (DCC)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets16

6.3.b Multivariate GARCH

•

We form two subgroups of commodities:

1.

Group “Fuels”: it includes the four energy commodities and soybean oil (spillovers between energy markets and bio-fuels)

2.

Group “Agriculture”: it includes the five agricultural commodities (spillovers between food markets and bio- fuels)

•

We consider a third group:

3.

Group “Agriculture + factor of energy commodities”: it includes the five agricultural commodities and a factor of the energy commodities (spillovers between energy and food markets and bio-fuels)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets17

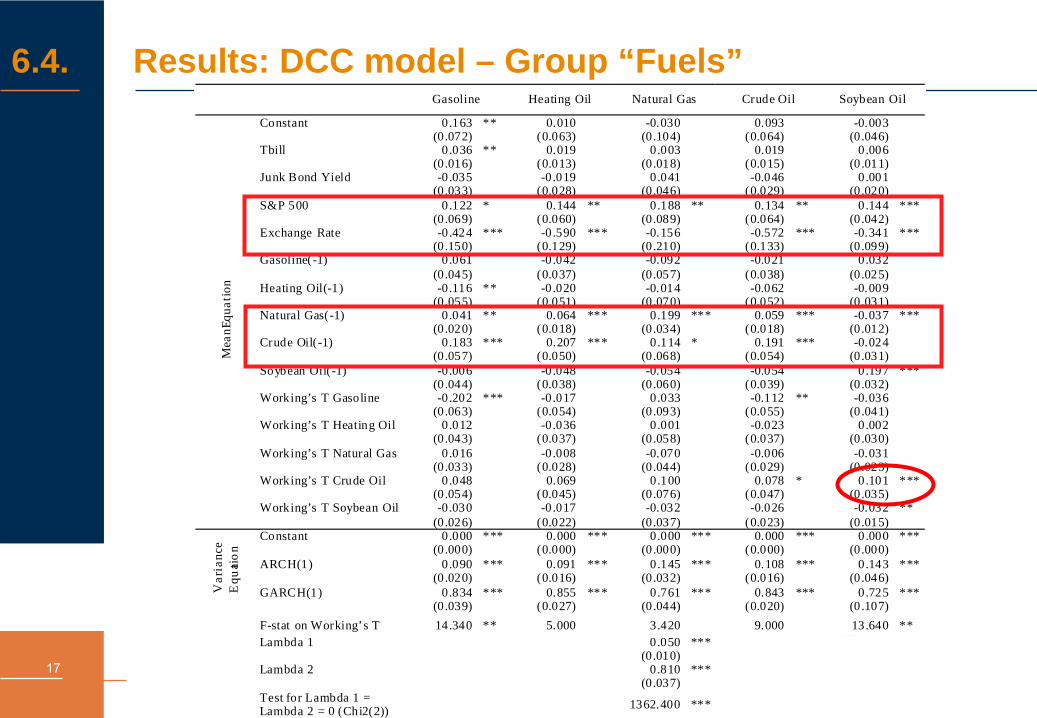

6.4. Results: DCC model – Group “Fuels”

Gasoline Heating Oil Natural Gas Crude Oil Soybean Oil

Constant 0.163(0.072)

** 0.010 (0.063)

-0.030(0.104)

0.093(0.064)

-0.003(0.046)

Tbill 0 .036(0.016)

** 0.019 (0.013)

0.003(0.018)

0.019(0.015)

0.006(0.011)

Junk Bond Yield -0.035(0.033)

-0.019 (0.028)

0.041(0.046)

-0.046(0.029)

0.001(0.020)

S&P 500 0.122(0.069)

* 0.144 (0.060)

** 0.188(0.089)

** 0.134(0.064)

** 0.144(0.042)

***

Exchange Rate -0.424(0.150)

*** -0.590 (0.129)

*** -0.156(0.210)

-0.572(0.133)

*** -0.341(0.099)

***

Gasoline(-1) 0.061(0.045)

-0.042 (0.037)

-0.092(0.057)

-0.021(0.038)

0.032(0.025)

Heating Oil(-1) -0.116(0.055)

** -0.020 (0.051)

-0.014(0.070)

-0.062(0.052)

-0.009(0.031)

Natural Gas(-1) 0.041(0.020)

** 0.064 (0.018)

*** 0.199(0.034)

*** 0.059(0.018)

*** -0.037(0.012)

***

Crude Oil(-1) 0.183(0.057)

*** 0.207 (0.050)

*** 0.114(0.068)

* 0.191(0.054)

*** -0.024(0.031)

Soybean Oil(-1) -0.006(0.044)

-0.048 (0.038)

-0.054(0.060)

-0.054(0.039)

0.197(0.032)

***

Working’s T Gasoline -0.202(0.063)

*** -0.017 (0.054)

0.033(0.093)

-0.112(0.055)

** -0.036(0.041)

Working’s T Heating Oil 0.012(0.043)

-0.036 (0.037)

0.001(0.058)

-0.023(0.037)

0.002(0.030)

Working’s T Natural Gas 0.016(0.033)

-0.008 (0.028)

-0.070(0.044)

-0.006(0.029)

-0.031(0.023)

Working’s T Crude Oil 0.048(0.054)

0.069 (0.045)

0.100(0.076)

0.078(0.047)

* 0.101(0.035)

***

Mea

n Equ

atio

n

Working’s T Soybean Oil -0.030(0.026)

-0.017 (0.022)

-0.032(0.037)

-0.026(0.023)

-0.032(0.015)

**

Constant 0.000(0.000)

*** 0.000 (0.000)

*** 0.000(0.000)

*** 0.000(0.000)

*** 0.000(0.000)

***

ARCH(1) 0.090(0.020)

*** 0.091 (0.016)

*** 0.145(0.032)

*** 0.108(0.016)

*** 0.143(0.046)

***

Var

ianc

e E

quati

on

GARCH(1) 0.834(0.039)

*** 0.855 (0.027)

*** 0.761(0.044)

*** 0.843(0.020)

*** 0.725(0.107)

***

F-stat on Working’s T 14.340 ** 5.000 3.420 9.000 13.640 **

Lambda 1 0.050(0.010)

***

Lambda 2 0.810(0.037)

***

Test for Lambda 1 = Lambda 2 = 0 (Chi2(2)) 1362.400 ***

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets18

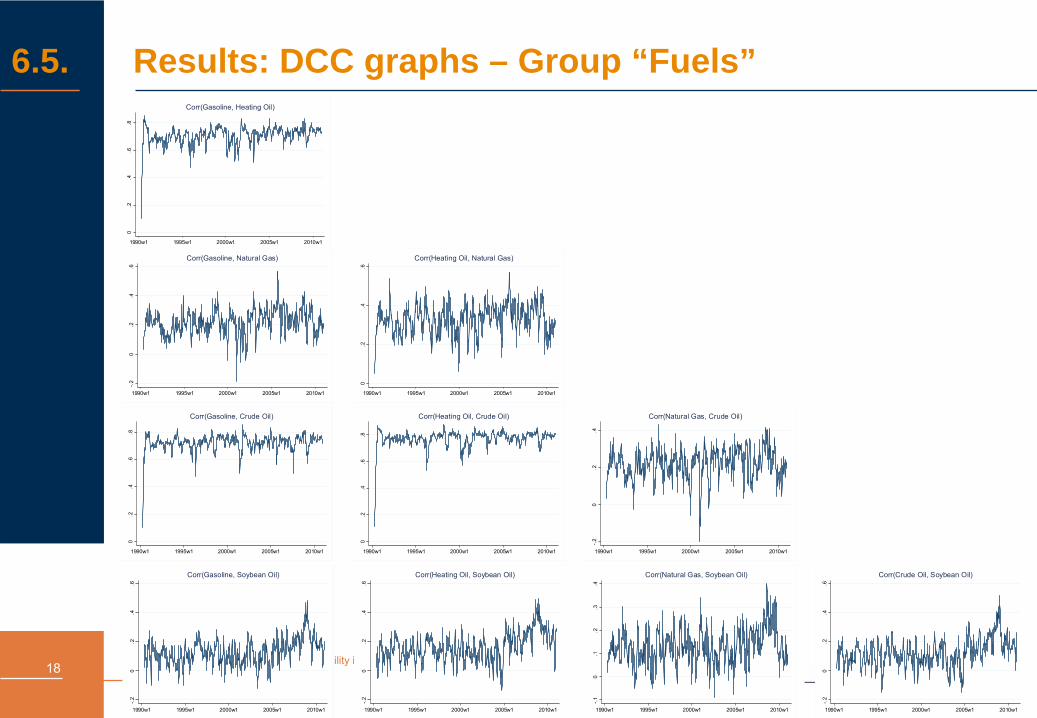

6.5. Results: DCC graphs – Group “Fuels”0

.2.4

.6.8

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Gasoline, Heating Oil)

-.2

0.2

.4.6

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Gasoline, Natural Gas)

0.2

.4.6

.8

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Gasoline, Crude Oil)

-.2

0.2

.4.6

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Gasoline, Soybean Oil)

0.2

.4.6

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Heating Oil, Natural Gas)

0.2

.4.6

.8

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Heating Oil, Crude Oil)

-.2

0.2

.4.6

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Heating Oil, Soybean Oil)

-.2

0.2

.4

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Natural Gas, Crude Oil)

-.1

0.1

.2.3

.4

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Natural Gas, Soybean Oil)

-.2

0.2

.4.6

1990w1 1995w1 2000w1 2005w1 2010w1

Corr(Crude Oil, Soybean Oil)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets19

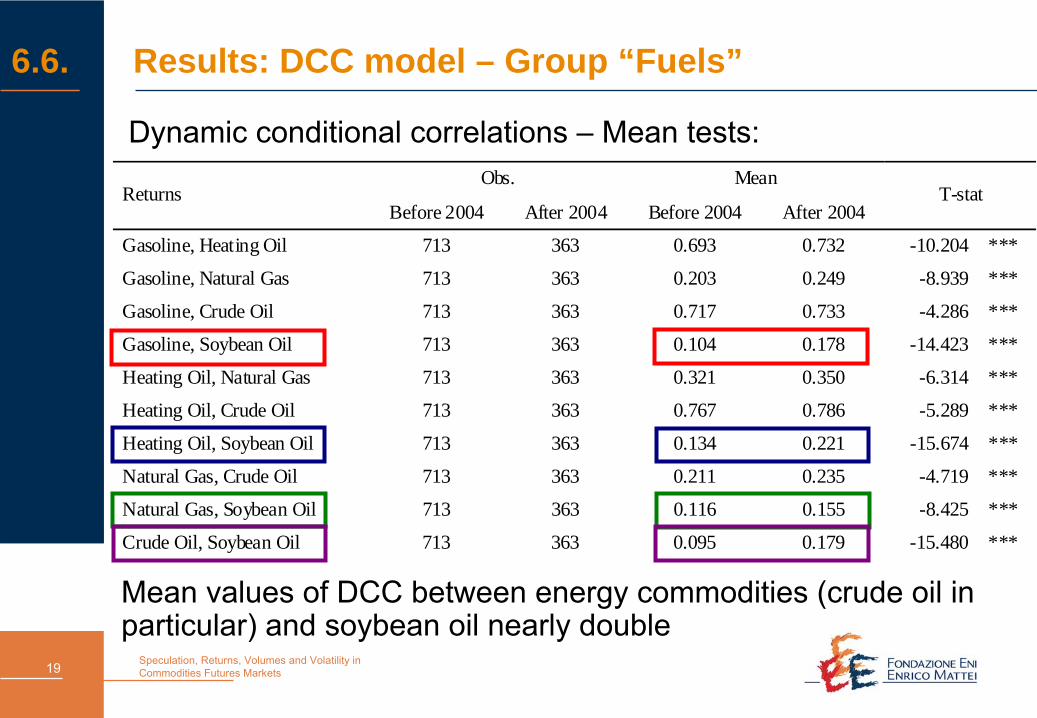

6.6. Results: DCC model – Group “Fuels”

Dynamic conditional correlations –

Mean tests:Obs. Mean

Returns Before 2004 After 2004 Before 2004 After 2004

T-stat

Gasoline, Heating Oil 713 363 0.693 0.732 -10.204 ***

Gasoline, Natural Gas 713 363 0.203 0.249 -8.939 ***

Gasoline, Crude Oil 713 363 0.717 0.733 -4.286 ***

Gasoline, Soybean Oil 713 363 0.104 0.178 -14.423 ***

Heating Oil, Natural Gas 713 363 0.321 0.350 -6.314 ***

Heating Oil, Crude Oil 713 363 0.767 0.786 -5.289 ***

Heating Oil, Soybean Oil 713 363 0.134 0.221 -15.674 ***

Natural Gas, Crude Oil 713 363 0.211 0.235 -4.719 ***

Natural Gas, Soybean Oil 713 363 0.116 0.155 -8.425 ***

Crude Oil, Soybean Oil 713 363 0.095 0.179 -15.480 ***

Mean values of DCC between energy commodities (crude oil in particular) and soybean oil nearly double

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets20

7. Conclusions I

•

Speculation−

Working’s T index is poorly significant in both univariate

and multivariate models, suggesting that speculation is not relevant in explaining commodities’

returns

•

Macroeconomic factors−

Equity returns are generally positive and significant

−

Exchange rate is generally negative and significant

•

Spillovers−

Within

the two groups of commodities (“fuels”

and

“agriculture”)−

Between

the two groups of commodities (i.e. Working’s T

index of crude oil significant in the soybean oil equation; increased co-volatilities after 2004)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets21

8.1. “Market depth”

•

“Market depth” (e.g. Kyle 1985; Bessembinder

and Seguin 1993): “approximate unexpected dollar trading volume which is necessary to alter futures prices by ‘one unit’”

(“vulnerability” of a market to speculation)

•

Estimate a modified ARCH model for returns and volatility, augmented with (expected and unexpected) volume and open interest, where:

Expected volume (open interest): fitted values of ARIMA models applied to volume (open interest)Unexpected volume (open interest): residuals of ARIMA models applied to volume (open interest)

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets22

8.2. “Market depth”

•

Markets: crude oil, natural gas, heating oil and gasoline (NYMEX)

•

Sizes of futures contracts:Crude oil: 1,000 barrelsNatural gas: 10,000 mmbtuHeating oil: 42,000 gallonsGasoline: 42,000 gallons

•

Time period: 1986-2010 (1990-2010 for natural gas)

•

Frequency: daily

•

Source: Datastream, CFTC

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets23

8.3. “Market depth”

•

From the coefficient associated to unexpected volume in the volatility equation we obtain an estimate of the “market depth”:

MD = (1 × size of contract × avg. price)/ β̂

where: is the coefficient on the unexpected volume1 is the “one unit”

defined as 1% variation in prices

β̂

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets24

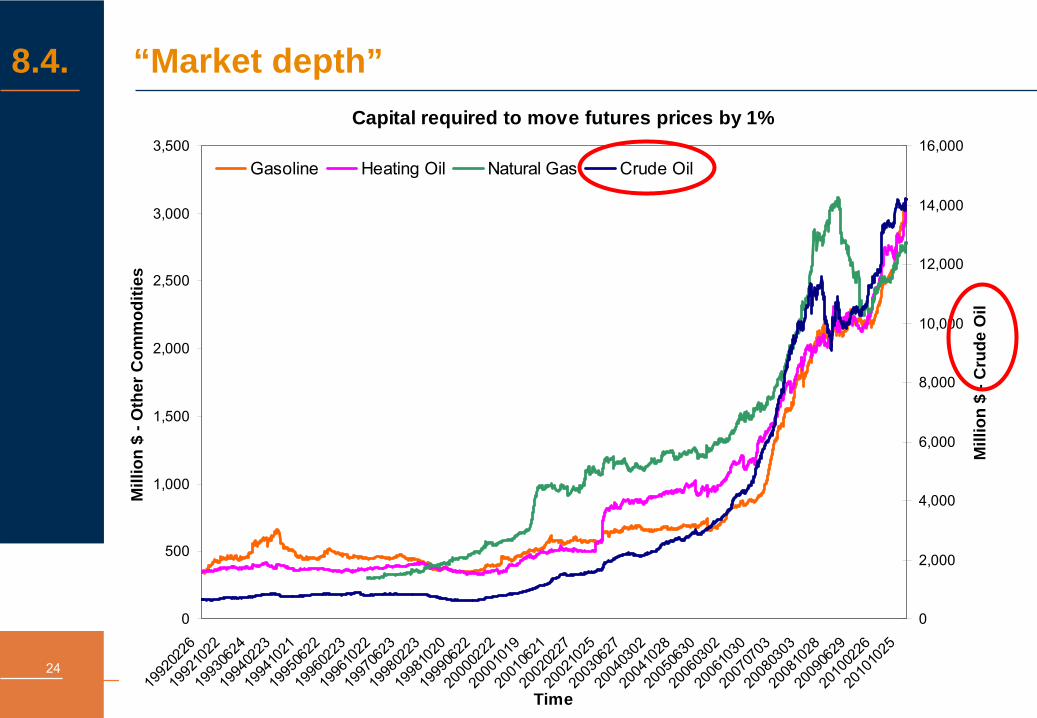

8.4. “Market depth”Capital required to move futures prices by 1%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1992

0226

1992

1022

1993

0624

1994

0223

1994

1021

1995

0622

1996

0223

1996

1022

1997

0623

1998

0223

1998

1020

1999

0622

2000

0222

2000

1019

2001

0621

2002

0227

2002

1025

2003

0627

2004

0302

2004

1028

2005

0630

2006

0302

2006

1030

2007

0703

2008

0303

2008

1028

2009

0629

2010

0226

2010

1025

Time

Mill

ion

$ - O

ther

Com

mod

ities

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Mill

ion

$ - C

rude

Oil

Gasoline Heating Oil Natural Gas Crude Oil

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets25

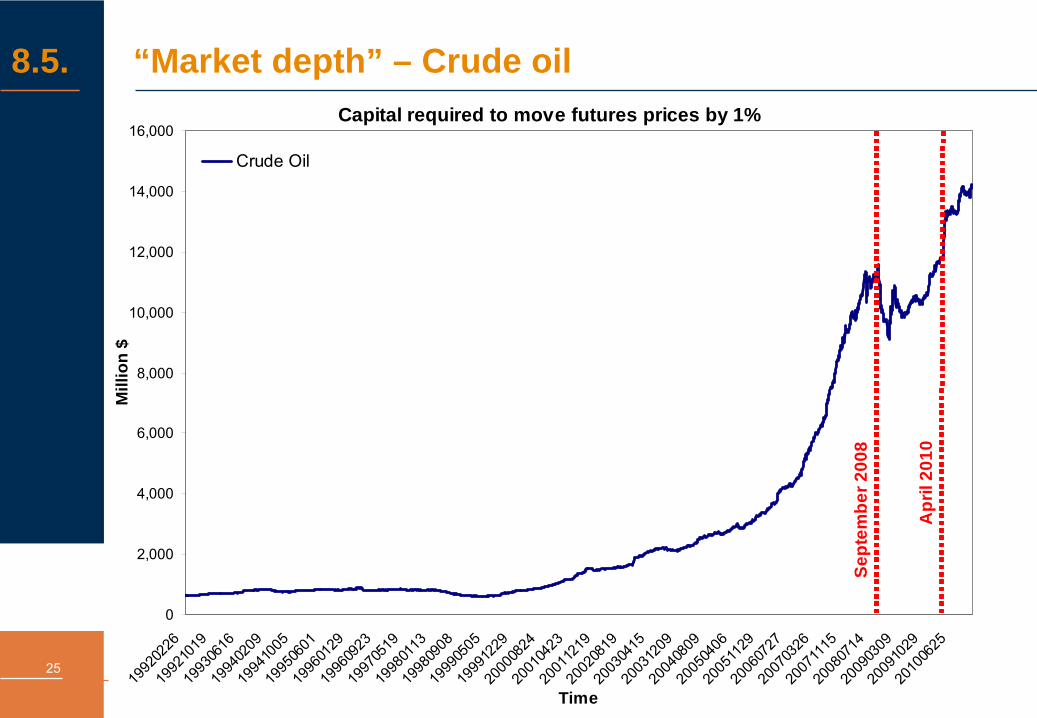

8.5. “Market depth” – Crude oilCapital required to move futures prices by 1%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1992

0226

1992

1019

1993

0616

1994

0209

1994

1005

1995

0601

1996

0129

1996

0923

1997

0519

1998

0113

1998

0908

1999

0505

1999

1229

2000

0824

2001

0423

2001

1219

2002

0819

2003

0415

2003

1209

2004

0809

2005

0406

2005

1129

2006

0727

2007

0326

2007

1115

2008

0714

2009

0309

2009

1029

2010

0625

Time

Mill

ion

$

Crude Oil

Sept

embe

r 200

8

Apr

il 20

10

Speculation, Returns, Volumes and Volatility in Commodities Futures Markets26

9. Conclusions II

•

Our empirical evidence suggests that:

“Market depth” has increased after 2000

In the financial crisis period (after 2008), “market depth” in the market of oil futures has dropped, i.e. this market is more vulnerable to speculation

•

Estimates of “market depth”

have to be interpreted with care

Corso Magenta 63, 20123 Milano - Italia - Tel +39 02.520.36934 - Fax +39 02.520.36946 - www.feem.it