small business and nonprofit training, consulting and technical assistance solutions to business...

TRANSCRIPT

Small Business and Nonprofit Training, Consulting and Technical Assistance

Solutions to Business Problems and Strategies for SuccessASharpe Consulting

Small Business and Nonprofit Training, Consulting and Technical Assistance

Solutions to Business Problems and Strategies for SuccessASharpe Consulting

Welcome to A-133 Audit

www.asharpeconsulting.com 2

PresenterAngela D. Sharpe

www.asharpeconsulting.com 3

Preparing for the Audit

The A-133 audit is the method of testing that internal controls are effective. Internal controls consists of all measures taken by the organization for the purpose of protecting its resources against waste, fraud, and inefficiencies; thus ensuring accuracy and reliability in accounting and operating data; securing compliance with the policies of the organization; and evaluating the level of performance in all units of the organization

Simply put, internal controls are good business practices.

www.asharpeconsulting.com 5

OMB

• Office of Management & Budget– Oversees and coordinates the Administration's

procurement, financial management, information and regulatory policies

– Coordinates mechanisms to reduce waste.…– Assures that grants are managed properly and

that Federal dollars are spent in accordance with applicable laws and regulations.

www.asharpeconsulting.com 6

OMB Circulars

• OMB A-110– Administrative Requirements for (Federal) Grants

• OMB A-133– Audits of…Non-Profit Organizations or recipients

of Federal Funds exceeding $500,000

www.asharpeconsulting.com 7

A-133 Audit Requirements

• Who?– Organizations that expend more than $500,000 of Federal

assistance during the year as Prime, sub-recipient or both– Must be completed and submitted within 9 months of the

close of the fiscal year– Written response to any audit findings, including corrective

action plan, if not submitted, must be done within 30 days after the audit is issued – failure can result in withholding, suspending and/or termination of Federal award

www.asharpeconsulting.com 8

A-133 Audit Requirements

• Independent auditor– Audit must be performed by independent auditor– Audit includes the Operational Audit – Auditors tests receipts for compliance with award

restrictions– Auditors test internal controls for regulatory compliance – Auditor attests to compliance with laws, regulations, rules,

award conditions– Zero tolerance for errors

www.asharpeconsulting.com 9

A-133 Audit Requirements

• Independent auditor– Reviews organization’s processes– Reaffirms that oversight exist and is appropriate– Recommends improvements to institutional

procedures– Confirms benefits of procedures to recipient and

sponsor

www.asharpeconsulting.com 10

A-133 Audit Requirements

• Independent auditor– Establish there is compliance with laws,

regulations and award conditions– Ensure organization can adequately demonstrate

compliance with applicable laws– Assess organizations internal controls and

determine if sufficient to ensure assets are safeguarded and financial reporting is accurate

www.asharpeconsulting.com 11

A-133 Audit Requirements

• Independent auditor– Make certain financial statements are presented

fairly in accordance with GAAP

– Confirm the SEFA (Schedule of Expenditures and Federal Awards) is fairly presented in all material aspects

www.asharpeconsulting.com 12

A-133 Audit Requirements

• What?– All federal grants received and still open in the current

year• Direct and indirect funds that are federal are included

– A report of all revenues and expenses incurred in the current year are reviewed

– Tracking system is validated for accuracy of cost allocations– Expenses reviewed for rates and compliance

www.asharpeconsulting.com 13

A-133 Audit Requirements

• When should you prepare?– Begin preparation as soon as you receive the award and

continue until closeout of the award– Identify and prepare resources that will be needed by the

auditor and make available– Notify any agents that have been recipients of the award

www.asharpeconsulting.com 14

A-133 Audit Requirements

• Prepare an Audit Book– New Award notifications– Subcontract payment schedule– List of all organizations with contact names that are

required to give A-133 notification– Copy of facilities and Administrative Rate proposal and

approval • if indirect cost method• Monthly rate analysis which verifies rate is applied correctly• Monthly fringe benefit rate analysis

www.asharpeconsulting.com 15

A-133 Audit Requirements

Question and Answer Time

www.asharpeconsulting.com

OMB A-133

• OMB A-133 Supplement Issued 2014

16

Bonding Insurance

1. Basic rules the government will not require additional insurance of bonding, but will follow agency’s practice.

2. For construction grants of $100,000a. If federal oversight agency determines that the

government interest is protected then the agency policies and procedures are acceptable

b. If determination is made that government’s interests are not protected the government will require bonding

Retention and Custodial

1. In general – financial records, supporting documentation, statistical records and any other pertinent records must be retained for 3 years from date of final expense report.

2. Authorization needed to use microfilm, fiche, scans or other storage mechanisms

3. Gov’t duly authorized representative may audit, examine, excerpt or transcribe any of this information

Program Income

1. Agencies are required to account for program income.2. Program income is gross income earned by the agency from federally supported activities, and includes, but is not limited to, rental fees, service fees and sales of equipment.3. Program income can be retained by the agency, with

approval, and:a. Added to the project to be used to further the program

objectives,b. Used to finance the non-federal share of the project (requires

approval), andc. Deducted from the total project costs when determining the

federal share of the project.

Cost Sharing and Matching

1. Cost sharing and matching represents that portion of the project or program not borne by the Agency.

2. Cost sharing or matching may consist of:a. Project costs incurred by the agency.b. Costs financed from non-federal sources such as

contributions and donations.c. Project costs represented by services, and real or personal

property or use thereof from non-federal sources (a.k.a. “In Kind” contributions).

Cost Sharing and Matching

4. Valuation of in-kind contributions should be based on applicable cost principles. a. Value of services should be consistent with those paid for

similar work.b. Value of property must be at fair market value.c. Volunteer services must be documented.d. Basis for determining the value of personal services,

material, equipment, land and buildings must be documented.

Financial Management Systems

Agency’s financial management system must provide for: a. Accurate, current, and complete disclosure of each project or program.b. Documentation of source and applicability of funds for federally sponsored

activities.c. Control and accountability for all funds including safeguards to assure they are

used only for authorized purpose.d. Comparison of actual outlays with budget amounts for each grant or

agreement. e. Procedures to minimize elapsed time between receipts of funds and outlay.f. Procedures to determine reasonableness, allowable and allocation method of

costs in accordance with federal cost principles and terms of grant agreement.g. Accounting records supported by source documents. h. Examination by independent audit.

Monitoring and Reporting

1. Agencies must monitor and report on technical performance (programmatic) through a report which presents:

a. Comparison of actual accomplishments to goals. b. Findings of investigator if appropriate.c. Reasons why goals were not met. d. Other pertinent data.

2. Problems or unfavorable developments should be

reported promptly. This includes changes in budgetary needs.

Revision of Financial Plans

1. Agencies are required to immediately report deviations from financial plans and to request approval for financial plan revisions involving:

a. A change in scope or objective.b. The need for additional federal funds. c. Other budget modifications or changes that exceed

$100,000.

2. None of the substantive programmatic work under the grant or other agreement may be subcontracted or transferred without prior approval of the federal sponsoring agency.

Suspension and Termination

1. Definitions:a. Termination – Cancellationb. Suspension - Temporary removal of support until corrective action

or termination.

2. Each federal sponsoring agency must have procedures for suspension or termination when agency has not complied with conditions of a program.

3. Termination may be:a. For cause - failure to comply.b. For convenience - mutual agreement.

Property Management StandardsAdequate

Property Management System

a. Unique identification numberb. Descriptionc. Funding sourced. Acquisition coste. Federal participation

percentage f. Title Assignmentg. Location, use and conditionh. Disposition datai. Other data to support cost

allocation

Property Management Process1. Federal property must be marked as

such.2. Physical inventory to be taken every two

years.3. Property must be made available for

shared usage with other federal projects.4. Control system to be in effect to

safeguard against loss, damage or theft of property.

5. Adequate maintenance procedures to be implemented.

6. Disposal procedures require authorization, competitive sales, and highest possible return.

Procurement Standards

Agency may follow their own procedures but must include:1. Code of conduct for Officers, employees or agents engaged in awarding or administering;

a. Officer, employee or agent may not engage an organization in which he has a financial interest or is negotiating employment.

b. May not accept gratuities.c. Disciplinary measures should be provided for violations.

2. Open and free competition.3. Procedures to avoid purchasing unnecessary or duplicate items-lease purchase analysis.4. Solicitation based on accurate description of technical requirements. e. Positive efforts to use small and

minority businesses. 5. Type of contract shall be determined by agency but not cost plus or percentage of cost contracts.6. Use of responsible contractors.7. Prior approval of sole source over $5,000. 8. Some sort of price or cost analysis should be made on every procurement. 9. Records for purchases of $10,000 must include:

a. Basis of contractor selection.b. Justification for lack of competition. c. Basis for award.

10. Assurance of contractor compliance with contract.

INTERNAL CONTROLSOMB CIRCULAR

A-133

COSO frameworkCommittee of Sponsoring Organizations

• CHARACTERISTICS OF INTERNAL CONTROLS

COSO Framework

• Control Environment• Risk Assessment• Control Activities• Information and Communication• Monitoring

Control Environment

• Sets the tone of an organization influencing the control consciousness of its people.

• It is the foundation for all other components of internal control, providing discipline and structure

Control Environment

• Ethical Conduct – evidenced by code of conduct or other verbal or written directive

• Governing Board – audit committee or equivalent to receive and review reports, communicate with auditor and ensure audit findings and recommendations are addressed

• Management response to prior questioned costs & control recommendations• Management adherence to program compliance requirements• Key manager responsibilities clearly defined• Key managers have adequate knowledge and experience to perform duties• Staff knowledgeable of compliance requirements and directive to discuss all

instances of noncompliance with management• Management commitment to competence and staff receive adequate training

to perform duties• Management support of adequate information system

Risk Assessment

• Entity’s identification and analysis of risks relevant to achievement of its goals and objectives

• Forming a basis for determining how the risks should be mitigated, managed and eliminated

• Monitoring on a regular basis

Risk Assessment

• Program managers and staff understand and have identified key compliance objectives

• Process established to implement changes in program objectives and procedures

• Organization structure provides identification of noncompliance:– Key managers have been given responsibility to identify and

communicate changes– Employees who require close supervision (e.g. inexperienced) are

identified– Management has identified and assessed complex operations,

programs or projects– Management is aware of results of monitoring, audits, reviews and

related risks of noncompliance

Control Activities

• Policies and procedures that help ensure that management objectives are met and manager directives are fulfilled

Control Activities

• Operating policies and procedures clearly written and communicated• Procedures in place to implement changes in laws, regulations, guidance and funding

agreements affecting Federal Awards• Management prohibits intervention or overriding established controls• Adequate segregation of duties between performance, review and recordkeeping tasks• Supervision of employee compensation with level of competence • Personnel with adequate knowledge and experience perform responsibilities• Equipment, inventory, cash and other assets are secured physically and periodically counted

and compared to recorded amounts• Governing Board conducts regular meetings, financial matters reviewed, program activities

discussed and written documentation of meeting is maintained• Computer and program controls should include:

– Data entry controls, e.g. edit checks– Exception Reporting– Access controls– Reviews of input and output data– Computer general controls and security

Information and Communication

• The identification, capture and exchange of information in a form and time frame that enable people to perform their duties and responsibilities

Information and Communication

• Accounting system provides for separate identification of Federal and non-federal transactions and allocation of transactions applicable to both

• Adequate source documentation exists to support amounts reported• Recordkeeping system is established to ensure that records and

documentation retained for the time period required• Reports provided timely to managers for review and appropriate action• Accurate information is accessible to those who need it• Reconciliations and reviews done to ensure accuracy of reports• Established internal and external communication channels:

– Staff Meetings– Bulletin Boards– Memos, circulation files, email– Surveys, suggestion box

Information and Communication

• Employee duties and control responsibilities effectively communicated

• Channels of communication for people to report suspected improprieties established (Whistleblower Policy)

• Actions taken as a result of communications received

• Established channels of communication between pass-thru entity and sub-recipients

Monitoring

• Process that assesses the quality for internal control performance over a period of time

Monitoring

• Ongoing monitoring built-in through independent reconciliations, staff meeting feedback, rotating staff, supervisory review and management review of reports

• Periodic site visits performed at decentralized locations (including sub-recipients) and checks performed to determine whether procedures are being followed as intended

• Follow-up on irregularities and deficiencies to determine cause• Internal quality control reviews performed• Management meets with program monitors, auditors and reviewers

to evaluate the condition of the program and controls• Internal audit routinely tests for compliance with Federal

requirements• Board reviews results of all monitoring or audit reports and

periodically assesses the adequacy of corrective action

www.asharpeconsulting.com 42

AUDIT REPORTS

• Audit Responsibilities: Audit Requirements Opinion Financial Statements Footnotes Supplementary Information Finding and Recommendations

Auditor’s Opinions

• Unqualified• Qualified• Adverse• Disclaimer (no)• Internal Controls• Going Concern

www.asharpeconsulting.com 43

Auditor’s Opinion

• Unqualified Opinion– Auditor's judgment that he or she has no reservation as to the fairness

of presentation of a company's financial statements and their conformity with Generally Accepted Accounting Principles (GAAP) also termed clean opinion. In the auditor's opinion, the company has presented fairly its financial position, results of operations, and changes in cash flows.

– In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Company as of December 31, 20XX, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in (the country where the report is issued).

www.asharpeconsulting.com 44

Auditor’s Opinion

• Qualified Opinion– Auditor's Qualified Opinion is issued when the auditor encounters one of two

types of situations which do not comply with generally accepted accounting principles, however the rest of the financial statements are fairly presented. The two types of situations which would cause an auditor to issue this opinion over the Unqualified opinion are:• Single deviation from GAAP – this type of qualification occurs when one or more areas of

the financial statements do not conform with GAAP• Limitation of scope - this type of qualification occurs when the auditor could not audit

one or more areas of the financial statements, and although they could not be verified, the rest of the financial statements were audited and they conform GAAP

– “In our opinion, except for the effects of such adjustments, if any, as might have been determined to be necessary had we been able to perform proper tests and procedures on the Company’s inventory, the financial statement referred to in the first paragraph presents fairly, in all material respects, the financial position of…”

www.asharpeconsulting.com 45

PAUSE

Auditor’s Opinion

• Adverse Opinion– Auditor's Adverse Opinion is issued when the auditor determines that the

financial statements are materially misstated and, when considered as a whole, do not conform with GAAP. It is considered the opposite of an unqualified or clean opinion, essentially stating that the information contained is materially incorrect, unreliable, and inaccurate in order to assess the company’s financial position and results of operations.

– Investors, lending institutions, and governments very rarely accept an company’s financial statements if the auditor issued an adverse opinion, and usually request the company to correct the financial statements and obtain another audit report.

– “In our opinion, because of the situations mentioned above (in the explanatory paragraph), the financial statements referred to in the first paragraph do not present fairly, in all material respects, the financial position of…”

www.asharpeconsulting.com 46

STOP

Auditor’s Opinion

• Disclaimer Opinion– A Disclaimer, is issued when the auditor could not form, and consequently refuses to present,

an opinion on the financial statements. This type of report is issued when the auditor tried to audit an entity but could not complete the work due to various reasons and does not issue an opinion

– (SAS) provide certain situations where a disclaimer of opinion may be appropriate:• A lack of independence, or material conflict(s) of interest, exist between the auditor and

the auditee (SAS No. 26) • There are significant scope limitations, whether intentional or not, which hinder the

auditor’s work in obtaining evidence and performing procedures (SAS No. 58); • There is a substantial doubt about the auditee’s ability to continue as a going concern or,

in other words, continue operating (SAS No. 59) • There are significant uncertainties within the auditee (SAS No. 79).

– The Company does not maintain adequate accounting records to provide sufficient information for the preparation of the basic financial statements. The Company’s accounting records do not constitute a double-entry system which can produce financial statements. Because of the significance of the matters discussed in the preceding paragraphs, the scope of our work was not sufficient to enable us to express, and we do not express, an opinion of the financial statements referred to in the first paragraph.

www.asharpeconsulting.com 47

STOP

Auditor’s Opinion

• Internal Controls– Included in the accompanying Management’s Annual Report on Internal Control Over Financial Reporting, that

the Company maintained effective internal control over financial reporting as of December 31, 20XX, based on criteria established in Internal Control—Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”).

– A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures :• (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the

transactions and dispositions of the assets of the company• (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of

financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company

• (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

– In our opinion, management’s assessment the Company maintained effective internal control over financial reporting as of December 31, 20XX, is fairly stated, in all material respects, based on criteria established in Internal Control—Integrated Framework issued by COSO. Furthermore, in our opinion, ABC Company maintained, in all material respects, effective internal control over financial reporting as of December 31, 20XX, based on criteria established in Internal Control—Integrated Framework issued by COSO.

www.asharpeconsulting.com 48

Auditor’s Opinion

• Going Concern Disclosure– This is a term which means that an entity will continue to operate in the near future, which is

generally more than next 12 months, so long as it generates or obtains enough resources to operate. If the auditor considers that the auditee is not a going concern, or will not be a going concern in the near future, then the auditor is required to include an explanatory paragraph before the opinion paragraph or following the opinion paragraph, in the audit report explaining the situation. • As for the actual wording of the auditor’s report, when a lack of going concern is determined by the auditor,

the disclosure paragraph should state the situation, state the auditor’s determination, and state the auditee’s plan to correct the situation. The disclosure paragraph should immediately follow the opinion paragraph.

• The following is the most widely used format of the paragraph which, in this case, deals with a company that has recurring losses:

– Company will continue as a going concern. As discussed in Note (X) to the financial statements, the Company has suffered recurring losses and has a net capital deficiency. These conditions raise substantial doubt about its ability to continue as a going concern. Management's plans in regard to these matters are also described in Note (X). The financial statements do not include any adjustments relating to the recoverability and classification of asset carrying amounts or the amount and classification of liabilities that might result should the Company be unable to continue as a going concern.

www.asharpeconsulting.com 49

STOP

Definitions

Caution– ask questions to be sure there’s no issue that cannot be easily resolved

Upon review, a yellow flag may be a mild recommendation to the process

Changes will prevent future problems or more serious issues

Significant deficiencies

Stop – ask very sharp, probing questions before going any further

Get clarity on the issues Red flags often mean a serious problem that could affect funding

Material weaknesseswww.asharpeconsulting.com 50

Yellow Flag Red Flag

www.asharpeconsulting.com

OMB Circular A-133

TYPE OF REPORT REQUIRED BY

Report on the Financial Statements Statement of Financial Position Statement of Activities Statement of Cash Flows Statement of Functional Expenses

Generally Accepted Accounting Principles (GAAP) FAS 117

Schedule of Expenditures of Federal Awards (SEFA) OMB Circular A-133

Internal Controls over Federal Awards OMB Circular A-133

Compliance with Laws and Regulations OMB Circular A-133

Findings and Recommendations OMB Circular A-133

Managements Comments and Corrective Actions OMB Circular A-133

Status of Prior Findings OMB Circular A-133

Data Collection Form (SF-SAC) OMB Circular A-133

51

The Major Financial Statements

www.asharpeconsulting.com 52

www.asharpeconsulting.com

Financial Statements

53

CATEGORY STATEMENT OF INCREASE DECREASE TYPICAL BALANCE

Assets Financial Position Debit Credit Debit

Liabilities Financial Position Credit Debit Credit

Revenues Activities Credit Debit Credit

Expenses Activities Debit Credit Debit

www.asharpeconsulting.com

The Balance Sheet

ASSETSUsually positiveWhat you own

LIABILTIESUsually negativeWhat you owe

54

NET WORTHAssets less Liabilities

Assets

• Assets are property owned by an individual or a business

• Assets have monetary exchange value• Assets may consist of specific goods or claims

against others• Assets appear on a Balance Sheet– Also called Statement of Financial Position

Liabilities

• A Liability is a legal claim on the property of an entity that requires payment or some monetary exchange of equal value

• Liabilities are debts and other financial obligations

• Liabilities are found on the Balance Sheet

Net Assets

• Net Assets is total assets less total liabilities sometimes described as Net Worth

• Net Assets are found on the Balance Sheet– Net Assets are also known as Fund Balance– Consists of Unrestricted, Temporarily Restricted

and Permanently Restricted– Change in Net Asset is the current year earnings

or (loss)

Cash vs. Accrual

Cash StatementsRevenue is recorded when cash is receivedBased on the money trailSmall Business - cash accounting

www.asharpeconsulting.com 58

Accrual StatementsRevenue is recorded

when earned, regardless whether cash was received

Based on the paper trail

Medium to larger businesses use accrual based system

Short term vs. Long Term

ASSETS – includes cash and assets that will convert to cash within 12 months

LIABILITIES – will be paid within 12 months

www.asharpeconsulting.com 59

ASSETS – will last more than one year (“mortgages, notes, FF&E, less LLR and depreciation”)

LIABILITIES – time to pay exceeds 12 months

Revenue & Expenses

• Revenue is income that a company receives from its normal business activities

• Expense or expenditure is an outflow of money to another person or company to pay for an item or service, costs

• Revenue & Expenses are found on a Report– Sometimes called Revenue and Expense– Sometimes called Operating Statement– Sometimes called Statement of Activities– Sometimes called Revenue, Expenditures and changes

in Net Assets

Statement of Financial Position

• Assets are property owned that has monetary exchange value

• Liabilities are debts or legal claims on the property of an entity that requires payment or some monetary exchange of equal value

• Net Assets is total assets less total liabilities sometimes described as Net Worth. It is the cumulative effect of all transactions in the organization.– Change in Net Asset is the current year earnings or (loss)– Unrestricted, Temp Restricted and Perm Restricted

www.asharpeconsulting.com 61

Statement of Activities

• Revenue is income that a company receives from its normal business activities. These earnings are generated from the delivery of a service or contributions.– Consists of Unrestricted, Temporarily Restricted and

Permanently Restricted

• Expense is an outflow of money to another person or company to pay for an item or services - costs as a result of service delivery or administrative overhead

www.asharpeconsulting.com 62

Statement of Cash Flow

• Definition– A Cash Flow Statement identifies the sources and uses of

cash – It is measured during a specified or finite period of time

• Components – Traditional– Operating Cash Flow– Investing Cash Flow– Financing Cash Flow

www.asharpeconsulting.com 63

www.asharpeconsulting.com

Current Assets

64

Current AssetsCash - Operating $21,489

Cash – Temp Restricted 13,165

Grant/Contract Rec. $78,660

Less Reserve Bad Debt (10,000) 68,660

Due From 9,000

Prepaid Expenses 9,310

Notes Receivable (CP) 20,000

Other 5,000

$146,624

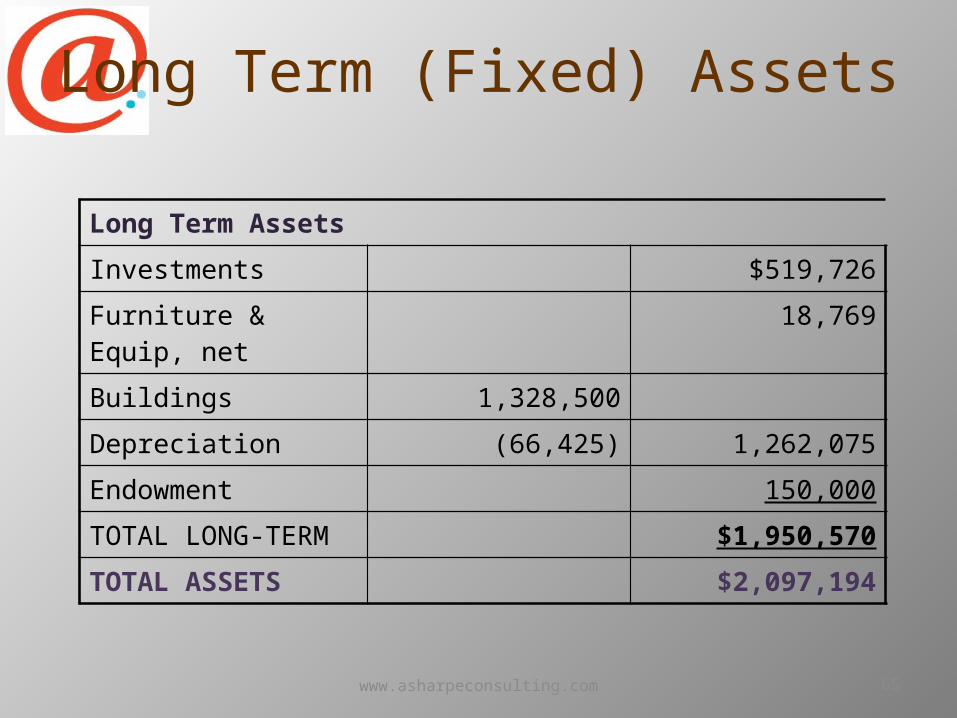

Long Term (Fixed) Assets

www.asharpeconsulting.com 65

Long Term AssetsInvestments $519,726

Furniture & Equip, net 18,769

Buildings 1,328,500

Depreciation (66,425) 1,262,075

Endowment 150,000

TOTAL LONG-TERM $1,950,570

TOTAL ASSETS $2,097,194

Current Liabilities

www.asharpeconsulting.com 66

Current LiabilitiesAccounts Payable $14,046

Payroll Taxes Payable 12,084

Interest Payable 2,042

Line of Credit 25,000

CP of Notes Payable 75,000

$128,172

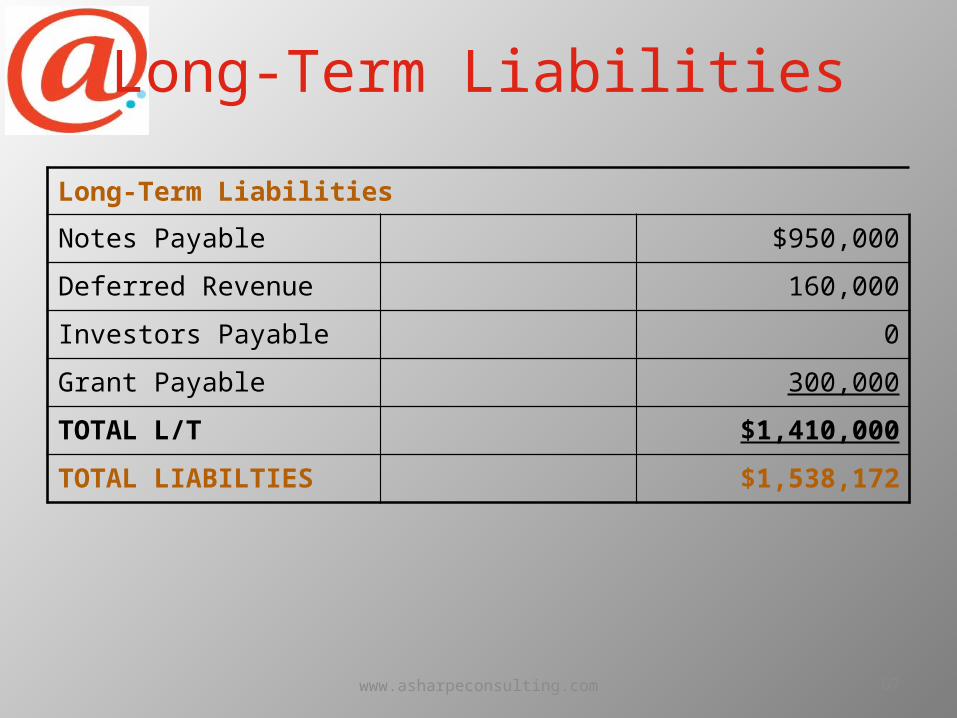

Long-Term Liabilities

Long-Term Liabilities

Notes Payable $950,000

Deferred Revenue 160,000

Investors Payable 0

Grant Payable 300,000

TOTAL L/T $1,410,000

TOTAL LIABILTIES $1,538,172

www.asharpeconsulting.com 67

Revenue/Expense

Revenue

Federal Grants 2,300,000

Non-Federal Grants 160,000

Contracts 1,040,000

Program Fees 140,000

TOTAL REVENUE $3,640,000

Expense

Salaries 2,200,000

Operating Expense 1,030,978

TOTAL EXPENSE $3,230,978

Earnings/Carry Forward $409,022www.asharpeconsulting.com 68

Net Worth

Total Assets $2,097,194Total Liabilities $1,538,172Net Worth $ 559,022

Unrestricted $ 273,344Temp Restricted $ 135,678Perm Restricted $ 150,000

www.asharpeconsulting.com 69

A-133 Audit

• Areas of Testing and Review

OMB Circular A-133

www.asharpeconsulting.com 71

Effective for audits of fiscal years - begin June 30, 2008

Transaction Testing Allowed/Disallowed

Should not exceed market for similar costs or goods Prudent Consistent treatment of expenses Significant deviation is documented Costs are in alignment with contract specifications Supporting documentation available

OMB Circular A-133

www.asharpeconsulting.com 72

Additional Audit Testing Davis-Bacon Act Procurement, Suspension and Debarment Reporting Sub-recipient Monitoring Special Test and Provisions

OMB CIRCULAR A-133

www.asharpeconsulting.com 73

Compliance Requirements cont’d Davis – Bacon Act and compliance Contracts and agreements over $2000

contain language regarding Davis-Bacon Act

Evidence sub-recipients notified of requirements Evidence of prevailing wages on projects Documentation of compliance

Weekly submission of payroll with statement of compliance (alternative - Form WH-347)

www.dol.gov/esa/programs/dbra/index.htm

OMB CIRCULAR A-133

www.asharpeconsulting.com 74

Compliance Requirements cont’d Reporting Form completed when required

SF-425 if electronic submission and funds request

Interest earned remitted to Dept. of Health and Human Services thru PMS (Payment Management System)

After September 2009 SF-425 supersedes 269, 272

www.whitehouse.gov.omb/grants/grants_forms.html

OMB Circular A-133

www.asharpeconsulting.com 75

Reporting Requirements FFR’s will be submitted on a quarterly,

semi-annual and annual basis Final FFR submitted on completion of

award agreement Semi-annual report due 30 days after end of

reporting period Annual submitted 90 days after end of

reporting period Final submitted 90 days after project or

grant period end date

OMB Circular A-133

www.asharpeconsulting.com 76

Compliance Requirements cont’d Reporting Submitted timely and in compliance with

requirements Performance Reporting

Annually and not more than quarterly

A-133 Final Thoughts

– Be Prepared• Schedule an exit interview–Discuss preliminary findings–Clear up misconceptions or erroneous

information–Have a procedure for audit review–Prepare written response with new

processes to eliminate weakness or deficiency–Follow-up Action Plan Meeting

www.asharpeconsulting.com 77

Helpful Links

• Catalog of Federal Domestic Assistance http://www.cfda.gov/• Data Collection Form http://harvester.census.gov.sac• Frequently asked questions http://harvester.census.gov.sac.faq.htm• Office of Management and Budget Circulars

http://www.whitehouse.gov/omb/circulars/• Single Audit Database

http://harvester.census.gov/sac/dissem/discalim.html• Single Audit reference information

http://harvester.census.gov/sac/sainfo.html

www.asharpeconsulting.com 78