slide 13-1 statement of cash flows financial accounting, seventh edition chapter 13

TRANSCRIPT

Slide 13-1

Statement Statement of Cash of Cash FlowsFlows

Financial Accounting,

Seventh Edition

Chapter 13

Slide 13-2

Provides information to help assess:

1. Entity’s ability to generate future cash flows.

2. Entity’s ability to pay dividends and obligations.

3. Reasons for difference between net income and

net cash provided (used) by operating activities.

4. Cash investing and financing transactions during

the period.

Usefulness and FormatUsefulness and FormatUsefulness and FormatUsefulness and Format

Usefulness of the Statement of Cash Flows

Slide 13-3

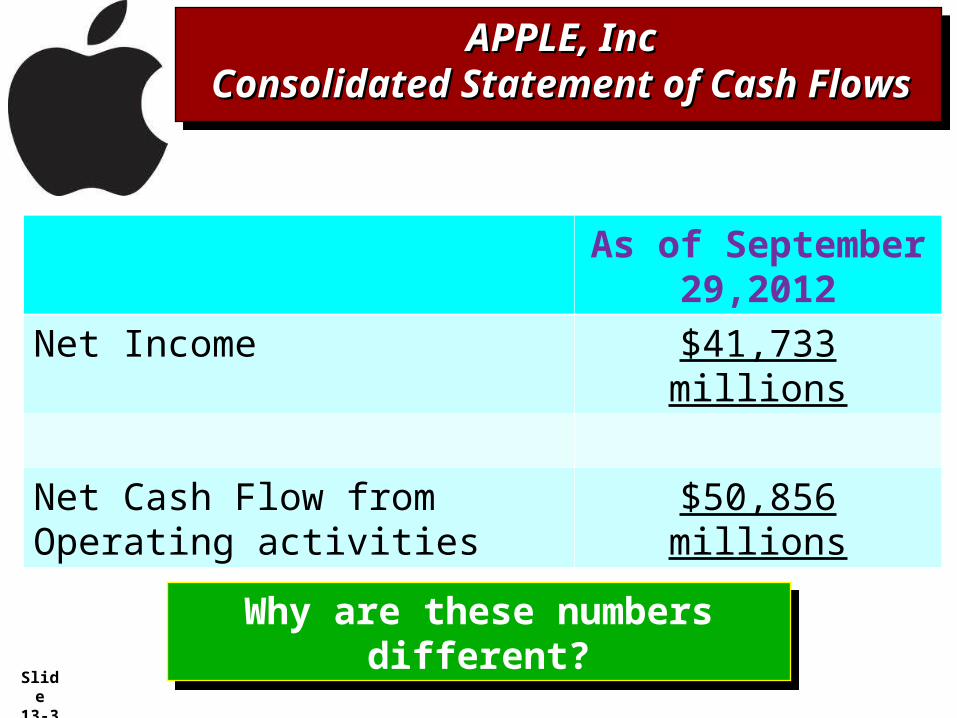

APPLE, IncAPPLE, IncConsolidated Statement of Cash Consolidated Statement of Cash

FlowsFlows

APPLE, IncAPPLE, IncConsolidated Statement of Cash Consolidated Statement of Cash

FlowsFlows

As of September 29,2012

Net Income $41,733 millions

Net Cash Flow from Operating activities

$50,856 millions

Why are these numbers different?Why are these numbers different?

Slide 13-4

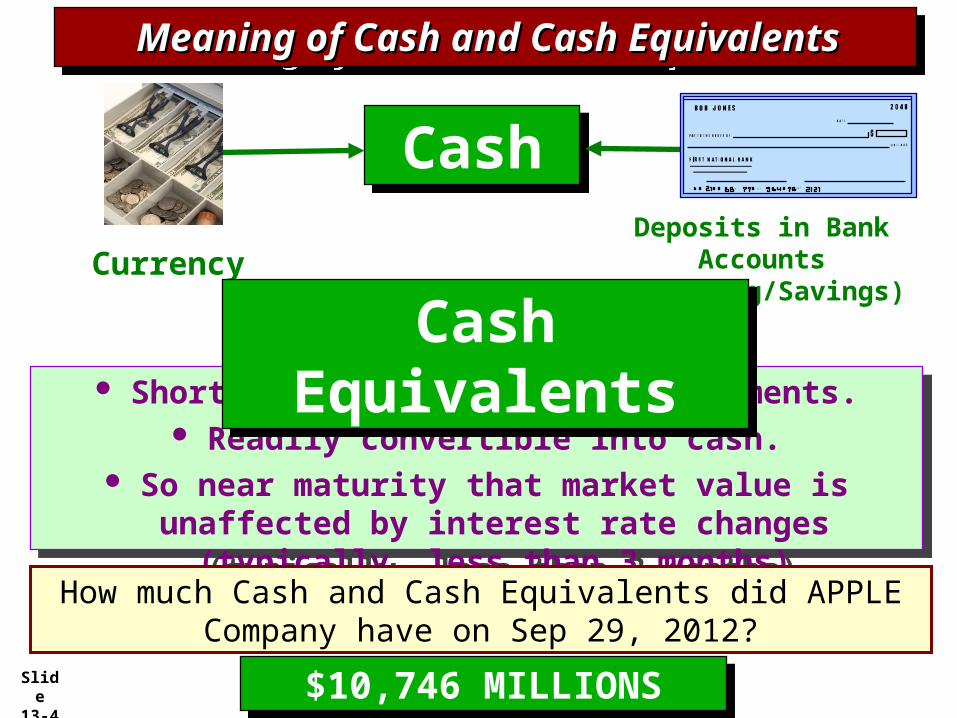

CashCashDeposits in Bank Accounts

(Checking/Savings)

Short-term, highly liquid investments. Readily convertible into cash.

So near maturity that market value is unaffected by interest rate changes (typically, less than 3 months)

Short-term, highly liquid investments. Readily convertible into cash.

So near maturity that market value is unaffected by interest rate changes (typically, less than 3 months)

Meaning of Cash and Cash Meaning of Cash and Cash EquivalentsEquivalents

Meaning of Cash and Cash Meaning of Cash and Cash EquivalentsEquivalents

Currency

Cash EquivalentsCash Equivalents

How much Cash and Cash Equivalents did APPLE Company have on Sep 29, 2012?

$10,746 MILLIONS$10,746 MILLIONS

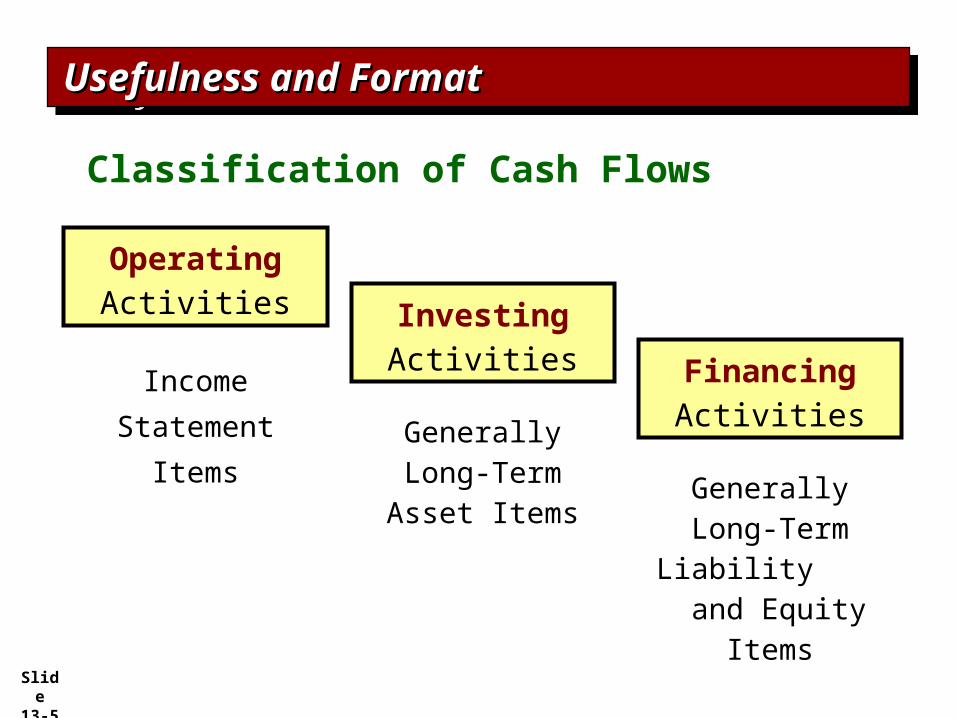

Slide 13-5

Income

Statement

Items

Operating Activities

Generally Long-Term Asset Items

Investing Activities

Generally Long-Term

Liability and Equity Items

Financing Activities

Classification of Cash Flows

Usefulness and FormatUsefulness and FormatUsefulness and FormatUsefulness and Format

Slide 13-6

6

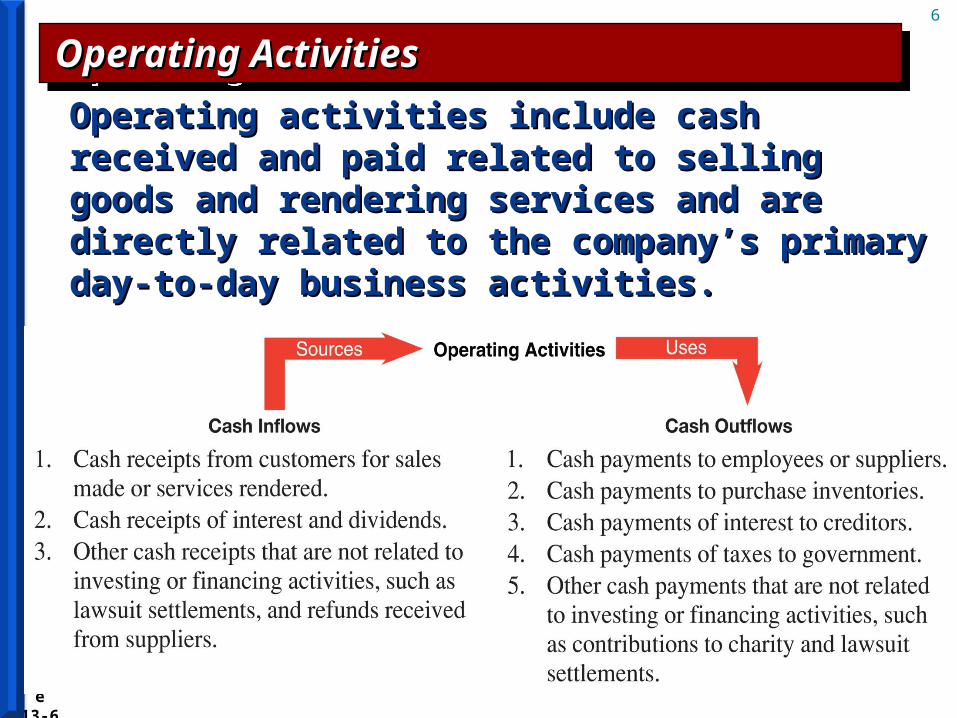

Operating activities include cash received and Operating activities include cash received and paid related to selling goods and rendering paid related to selling goods and rendering services and are directly related to the company’s services and are directly related to the company’s primary day-to-day business activities.primary day-to-day business activities.

Operating ActivitiesOperating ActivitiesOperating ActivitiesOperating Activities

Slide 13-7

7

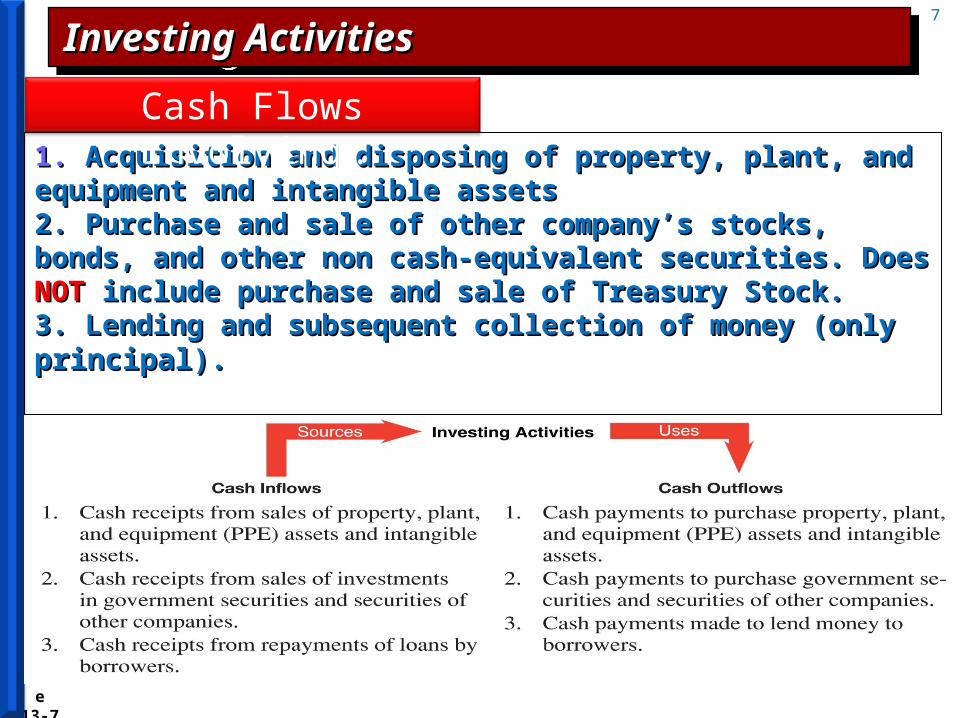

1. 1. Acquisition and disposing of property, plant, and Acquisition and disposing of property, plant, and equipment and intangible assetsequipment and intangible assets2. Purchase and sale of other company’s stocks, bonds, 2. Purchase and sale of other company’s stocks, bonds, and other non cash-equivalent securities. Does and other non cash-equivalent securities. Does NOTNOT include purchase and sale of Treasury Stock.include purchase and sale of Treasury Stock.3. Lending and subsequent collection of money (only 3. Lending and subsequent collection of money (only principal).principal).

Cash Flows Involving…

Investing ActivitiesInvesting ActivitiesInvesting ActivitiesInvesting Activities

Slide 13-8

8

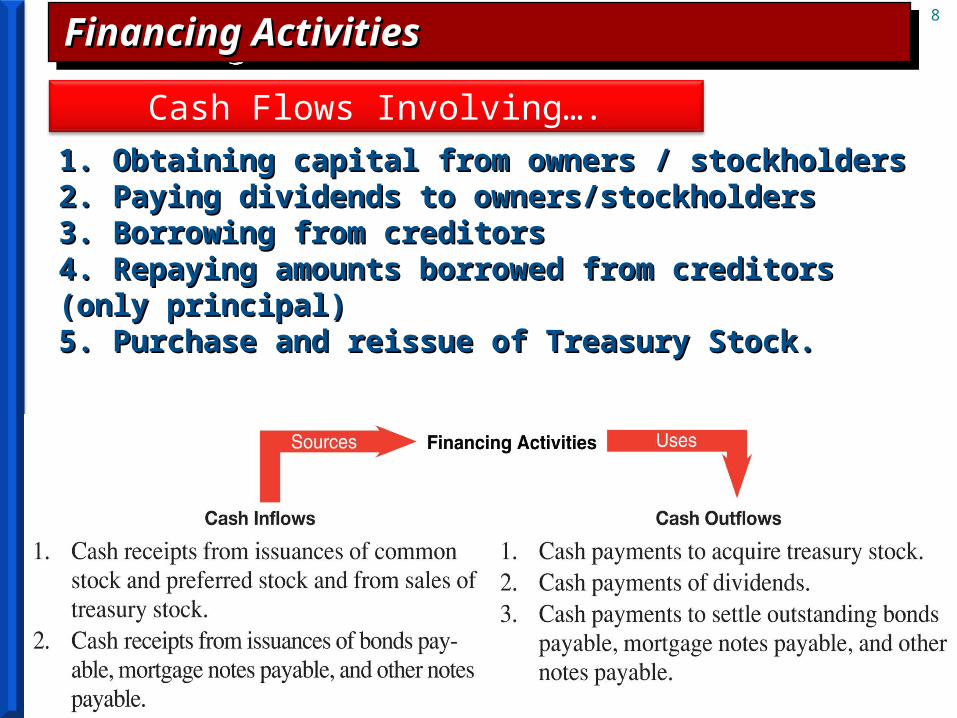

1. Obtaining capital from owners / stockholders1. Obtaining capital from owners / stockholders2. Paying dividends to owners/stockholders2. Paying dividends to owners/stockholders3. Borrowing from creditors3. Borrowing from creditors4. Repaying amounts borrowed from creditors 4. Repaying amounts borrowed from creditors (only principal)(only principal)5. Purchase and reissue of Treasury Stock.5. Purchase and reissue of Treasury Stock.

Cash Flows Involving….

Financing ActivitiesFinancing ActivitiesFinancing ActivitiesFinancing Activities

Slide 13-9

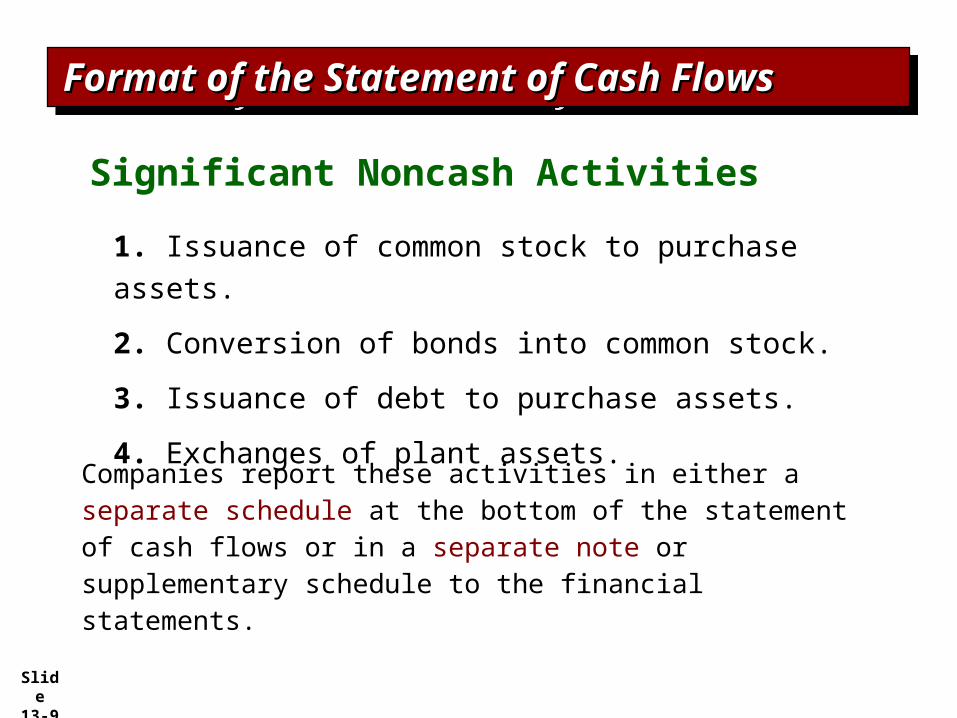

Significant Noncash Activities

1. Issuance of common stock to purchase assets.

2. Conversion of bonds into common stock.

3. Issuance of debt to purchase assets.

4. Exchanges of plant assets.

Companies report these activities in either a separate schedule at the bottom of the statement of cash flows or in a separate note or supplementary schedule to the financial statements.

Format of the Statement of Cash Format of the Statement of Cash FlowsFlowsFormat of the Statement of Cash Format of the Statement of Cash FlowsFlows

Slide 13-10

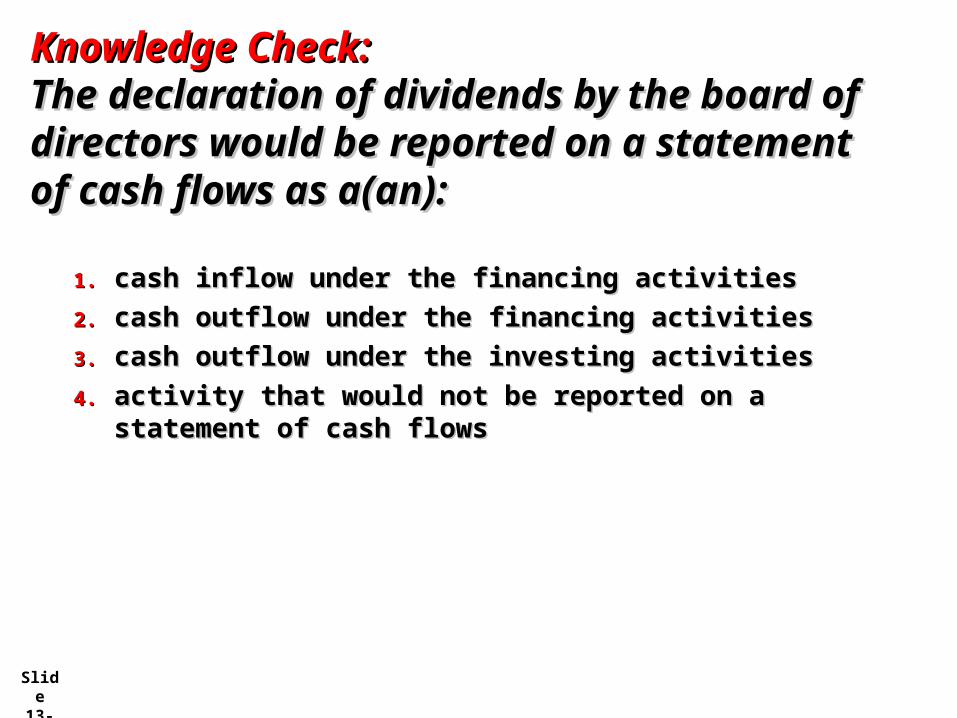

Knowledge Check:Knowledge Check:The declaration of dividends by the The declaration of dividends by the board of directors would be reported board of directors would be reported on a statement of cash flows as a(an):on a statement of cash flows as a(an):

1.1. cash inflow under the financing activitiescash inflow under the financing activities

2.2. cash outflow under the financing activitiescash outflow under the financing activities

3.3. cash outflow under the investing activitiescash outflow under the investing activities

4.4. activity that would not be reported on a activity that would not be reported on a statement of cash flowsstatement of cash flows

Slide 13-11

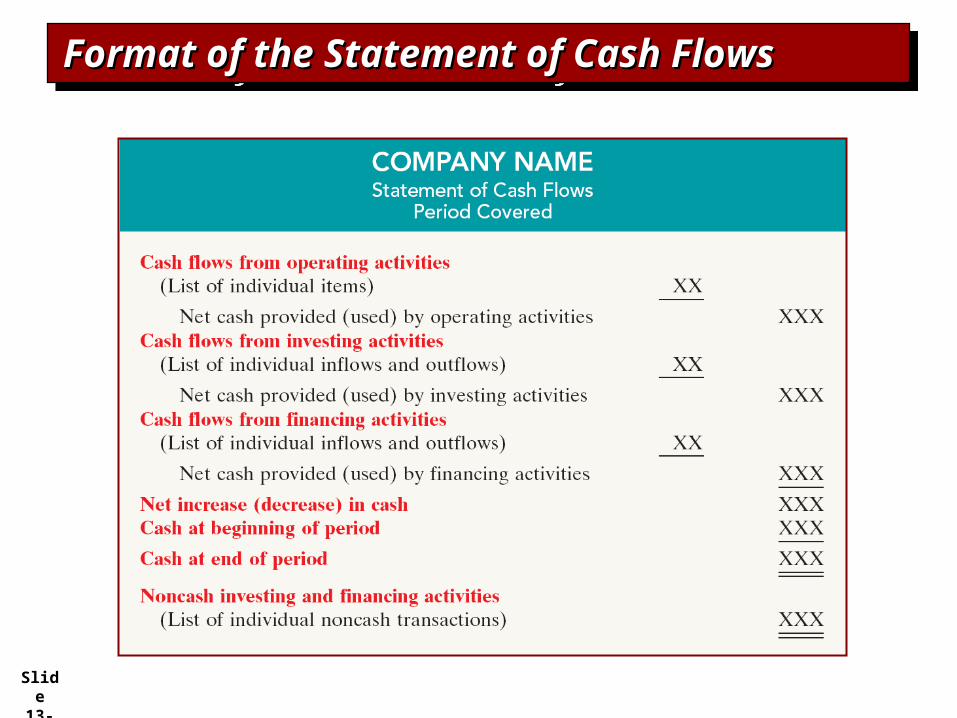

Order of Presentation:

1. Operating activities.

2. Investing activities.

3. Financing activities.

The cash flows from operating activities section always appears first, followed by the investing and financing sections.

Direct Method

Indirect Method

Format of the Statement of Cash Flows

Usefulness and FormatUsefulness and FormatUsefulness and FormatUsefulness and Format

Slide 13-12

Format of the Statement of Cash Format of the Statement of Cash FlowsFlowsFormat of the Statement of Cash Format of the Statement of Cash FlowsFlows

Slide 13-13

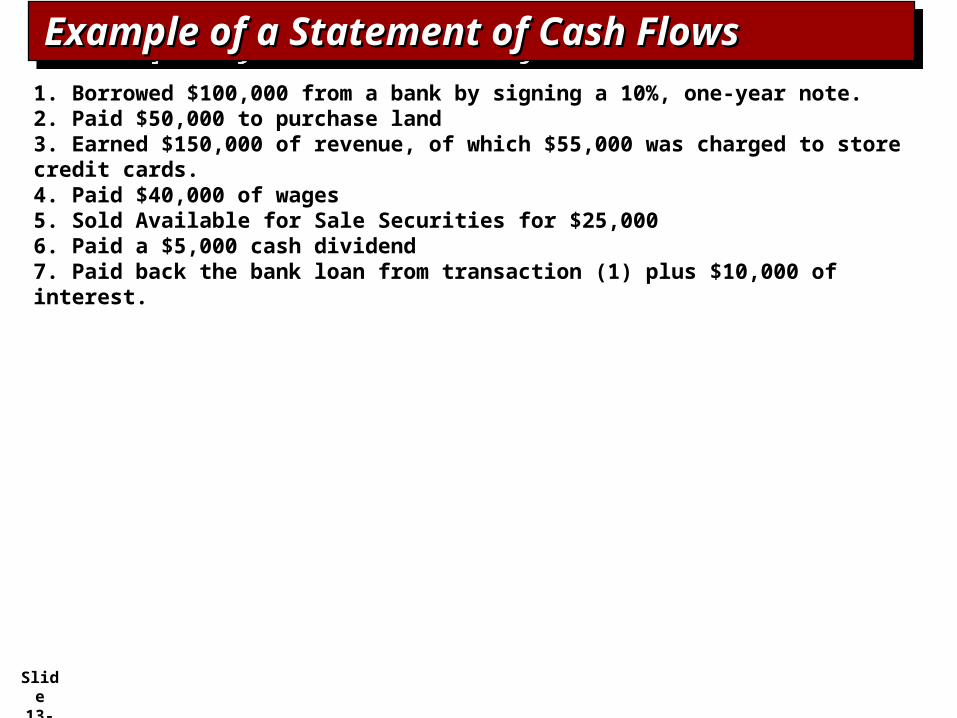

1. Borrowed $100,000 from a bank by signing a 10%, one-year note.2. Paid $50,000 to purchase land3. Earned $150,000 of revenue, of which $55,000 was charged to store credit cards.4. Paid $40,000 of wages5. Sold Available for Sale Securities for $25,0006. Paid a $5,000 cash dividend7. Paid back the bank loan from transaction (1) plus $10,000 of interest.

Example of a Statement of Cash FlowsExample of a Statement of Cash FlowsExample of a Statement of Cash FlowsExample of a Statement of Cash Flows

Slide 13-14

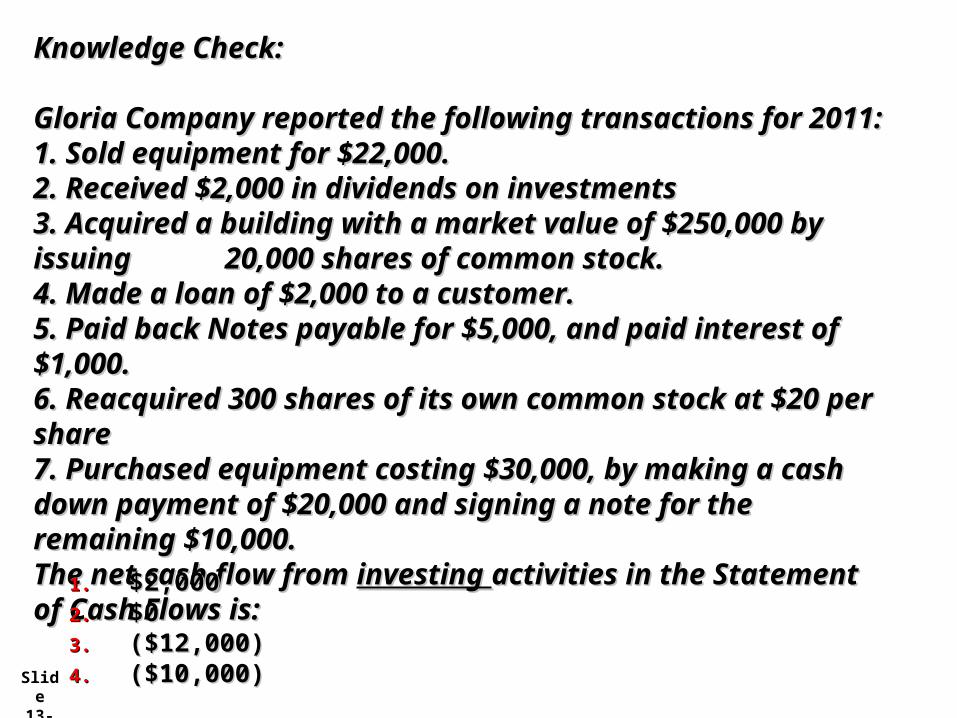

Knowledge Check:Knowledge Check:

Gloria Company reported the following transactions for 2011:Gloria Company reported the following transactions for 2011:1. Sold equipment for $22,000.1. Sold equipment for $22,000.2. Received $2,000 in dividends on investments2. Received $2,000 in dividends on investments3. Acquired a building with a market value of $250,000 by issuing 3. Acquired a building with a market value of $250,000 by issuing 20,000 shares of common stock.20,000 shares of common stock.4. Made a loan of $2,000 to a customer.4. Made a loan of $2,000 to a customer.5. Paid back Notes payable for $5,000, and paid interest of $1,000.5. Paid back Notes payable for $5,000, and paid interest of $1,000.6. Reacquired 300 shares of its own common stock at $20 per share6. Reacquired 300 shares of its own common stock at $20 per share7. Purchased equipment costing $30,000, by making a cash down 7. Purchased equipment costing $30,000, by making a cash down payment of $20,000 and signing a note for the remaining $10,000.payment of $20,000 and signing a note for the remaining $10,000.The net cash flow from The net cash flow from investing investing activities in the Statement of Cash activities in the Statement of Cash Flows is:Flows is:

1.1. $2,000$2,0002.2. $0$03.3. ($12,000)($12,000)4.4. ($10,000) ($10,000)

Slide 13-15

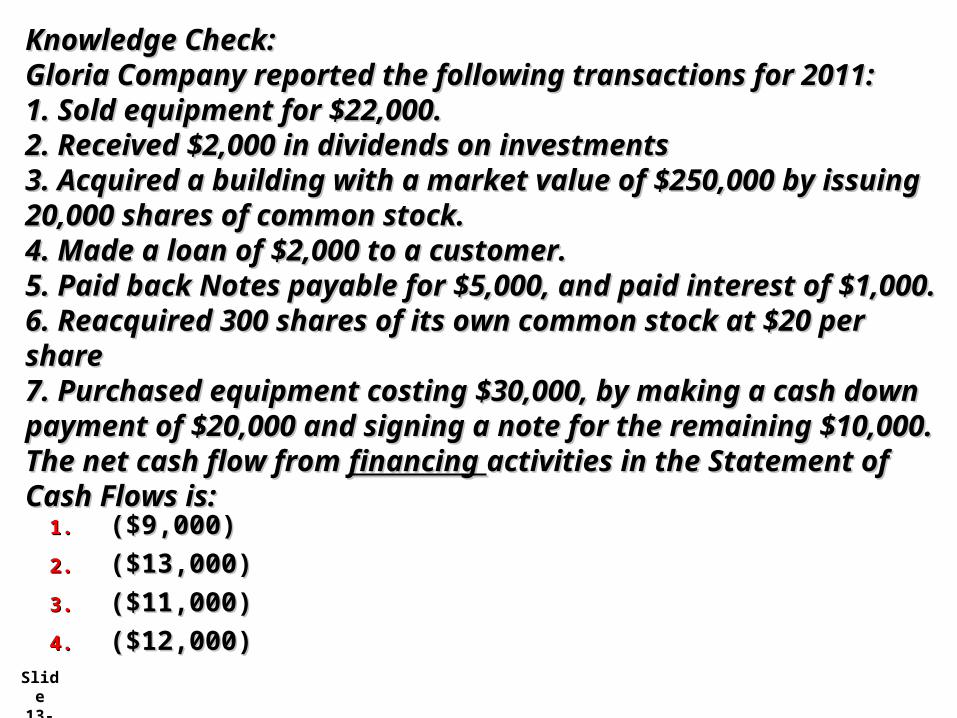

Knowledge Check:Knowledge Check:Gloria Company reported the following transactions for 2011:Gloria Company reported the following transactions for 2011:1. Sold equipment for $22,000.1. Sold equipment for $22,000.2. Received $2,000 in dividends on investments2. Received $2,000 in dividends on investments3. Acquired a building with a market value of $250,000 by issuing 20,000 3. Acquired a building with a market value of $250,000 by issuing 20,000 shares of common stock.shares of common stock.4. Made a loan of $2,000 to a customer.4. Made a loan of $2,000 to a customer.5. Paid back Notes payable for $5,000, and paid interest of $1,000.5. Paid back Notes payable for $5,000, and paid interest of $1,000.6. Reacquired 300 shares of its own common stock at $20 per share6. Reacquired 300 shares of its own common stock at $20 per share7. Purchased equipment costing $30,000, by making a cash down payment 7. Purchased equipment costing $30,000, by making a cash down payment of $20,000 and signing a note for the remaining $10,000.of $20,000 and signing a note for the remaining $10,000.The net cash flow from The net cash flow from financing financing activities in the Statement of Cash Flows activities in the Statement of Cash Flows is:is:

1.1. ($9,000)($9,000)

2.2. ($13,000)($13,000)

3.3. ($11,000)($11,000)

4.4. ($12,000)($12,000)

Slide 13-16

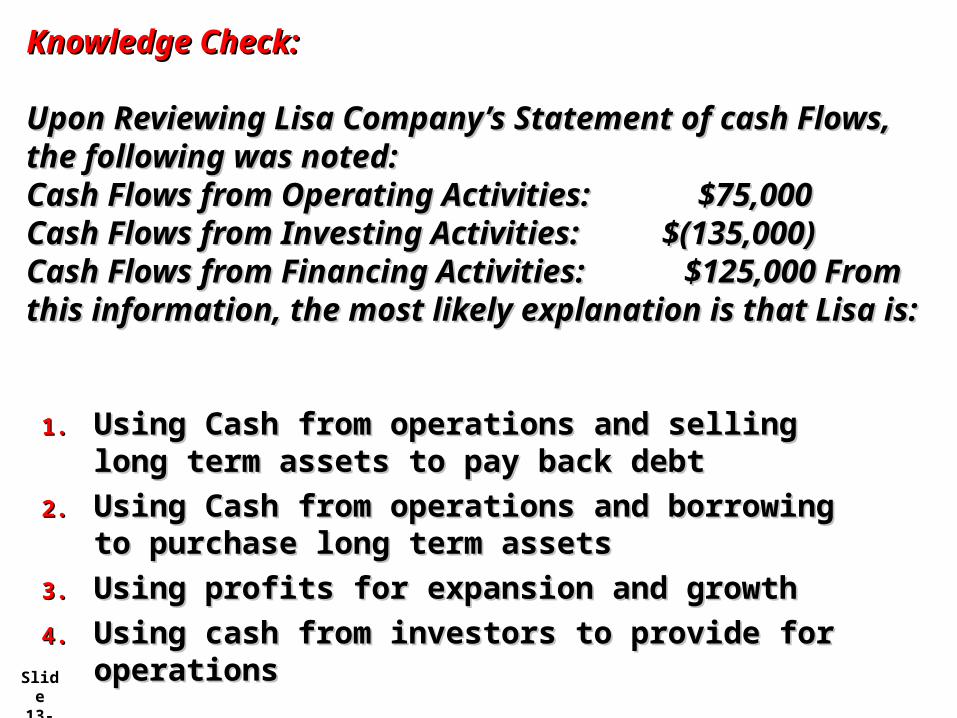

Knowledge Check:Knowledge Check:

Upon Reviewing Lisa Company’s Statement of Upon Reviewing Lisa Company’s Statement of cash Flows, the following was noted:cash Flows, the following was noted:Cash Flows from Operating Activities: Cash Flows from Operating Activities: $75,000$75,000Cash Flows from Investing Activities: Cash Flows from Investing Activities: $(135,000)$(135,000)Cash Flows from Financing Activities: Cash Flows from Financing Activities: $125,000 From this information, the most likely $125,000 From this information, the most likely explanation is that Lisa is:explanation is that Lisa is:1.1. Using Cash from operations and selling long Using Cash from operations and selling long

term assets to pay back debtterm assets to pay back debt

2.2. Using Cash from operations and borrowing to Using Cash from operations and borrowing to purchase long term assetspurchase long term assets

3.3. Using profits for expansion and growthUsing profits for expansion and growth

4.4. Using cash from investors to provide for Using cash from investors to provide for operationsoperations

Slide 13-17

Three Sources of Information:

1. Comparative balance sheets

2. Current income statement

3. Additional information

Usefulness and FormatUsefulness and FormatUsefulness and FormatUsefulness and Format

Preparing the Statement of Cash Flows

Slide 13-18

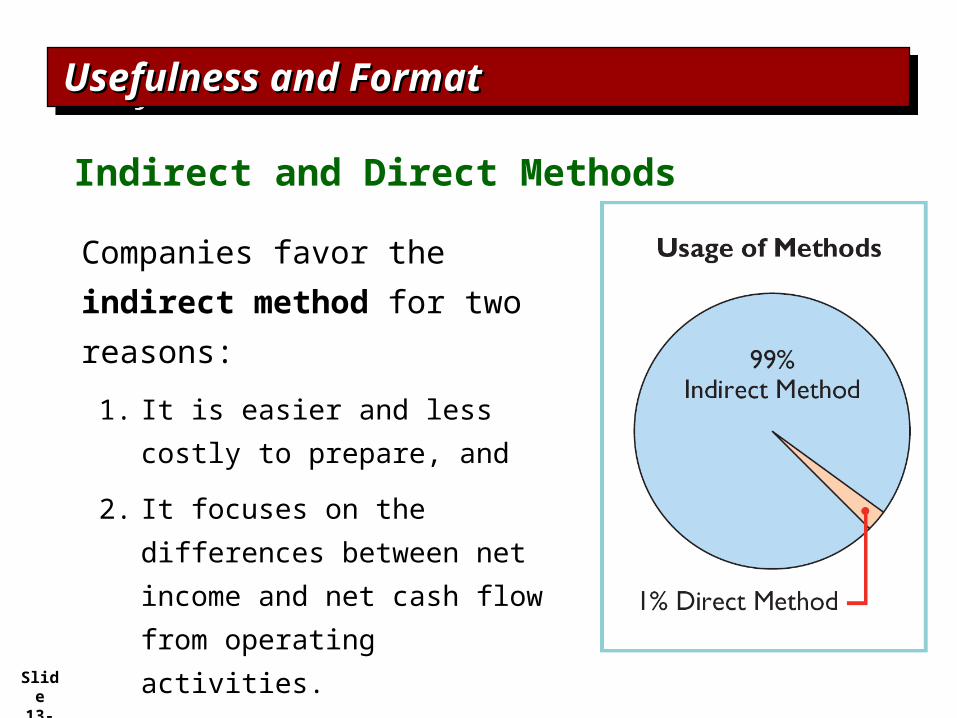

Indirect and Direct Methods

Companies favor the

indirect method for two

reasons:

1. It is easier and less costly to

prepare, and

2. It focuses on the differences

between net income and net

cash flow from operating

activities.

Usefulness and FormatUsefulness and FormatUsefulness and FormatUsefulness and Format

Slide 13-19

Operating Activities

Determine net cash provided/used by operating activities by converting net income from an accrual basis to a cash basis.

Common adjustments to Net Income (Loss):

Add back non-cash expenses.

Deduct gains and add losses.

Changes in noncash current assets and current liabilities.

Preparing the Statement of Cash Preparing the Statement of Cash FlowsFlowsPreparing the Statement of Cash Preparing the Statement of Cash FlowsFlows

Indirect Method

Slide 13-20

Non Cash Expenses (such as Depreciation, Depletion, Amortization Expense, Bad Debts Expense) reduces Net Income, but does NOT reduce Cash. So these expenses must be added back to Net Income to determine Cash Flow from Operating Activities.

Adjustments to Net IncomeAdjustments to Net IncomeAdjustments to Net IncomeAdjustments to Net Income

Step 1: Add back noncash expenses

Slide 13-21

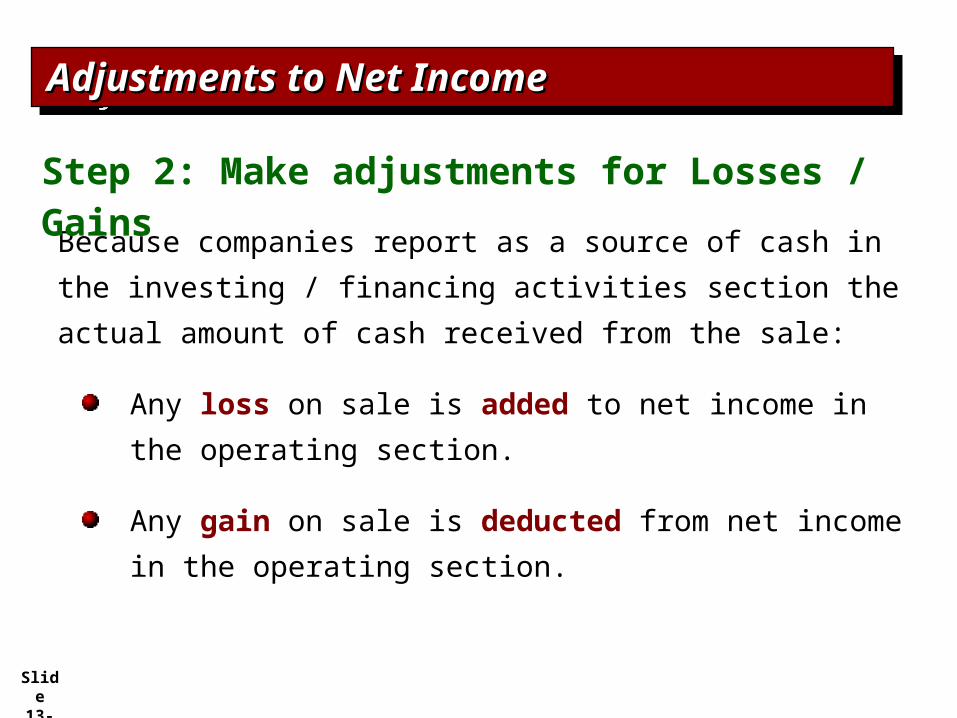

Because companies report as a source of cash in the

investing / financing activities section the actual amount

of cash received from the sale:

Any loss on sale is added to net income in the

operating section.

Any gain on sale is deducted from net income in the

operating section.

Step 2: Make adjustments for Losses / Gains

Adjustments to Net IncomeAdjustments to Net IncomeAdjustments to Net IncomeAdjustments to Net Income

Slide 13-22

Adjustments to Net IncomeAdjustments to Net IncomeAdjustments to Net IncomeAdjustments to Net Income

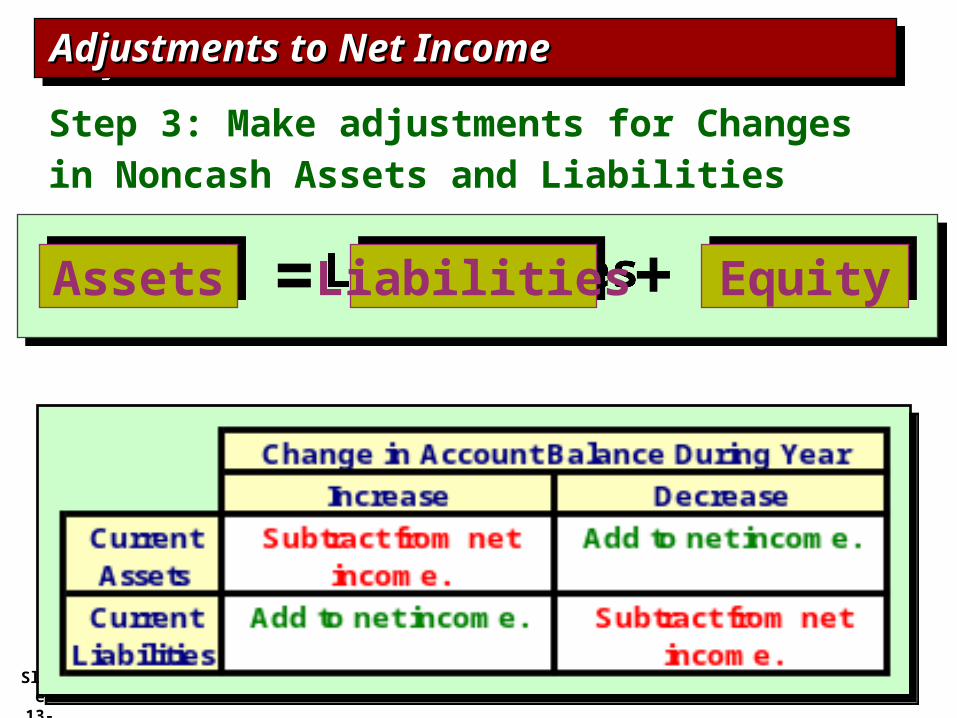

Step 3: Make adjustments for Changes in Noncash Assets and Liabilities

LiabilitiesLiabilities EquityEquityAssetsAssets = +

Slide 13-23

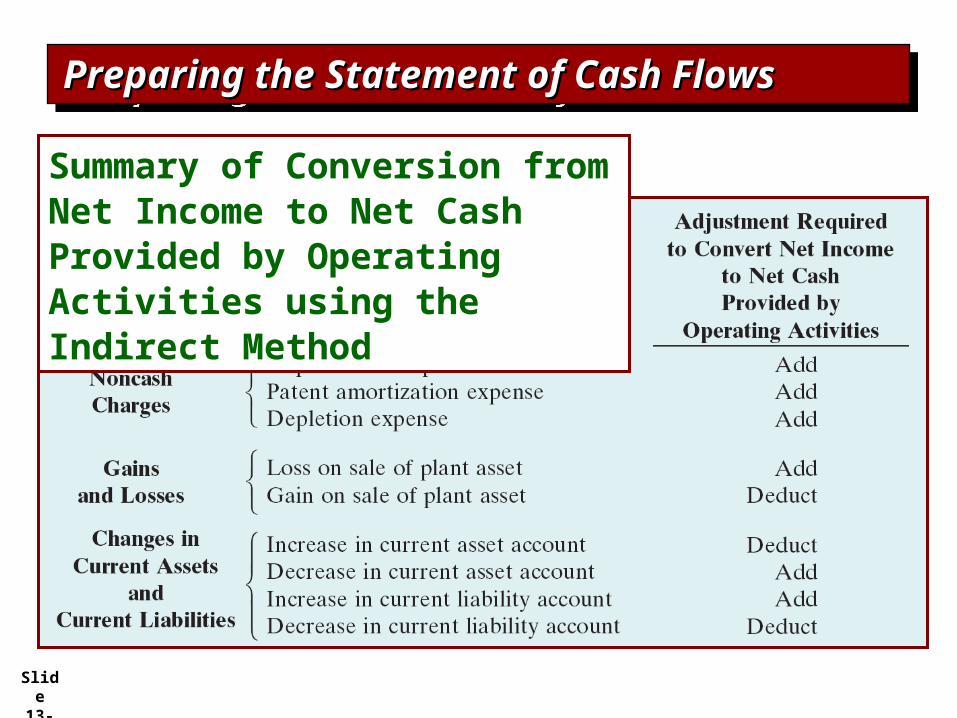

Summary of Conversion from Net Income to Net Cash Provided by Operating Activities using the Indirect Method

Preparing the Statement of Cash Preparing the Statement of Cash FlowsFlowsPreparing the Statement of Cash Preparing the Statement of Cash FlowsFlows

Slide 13-24

24

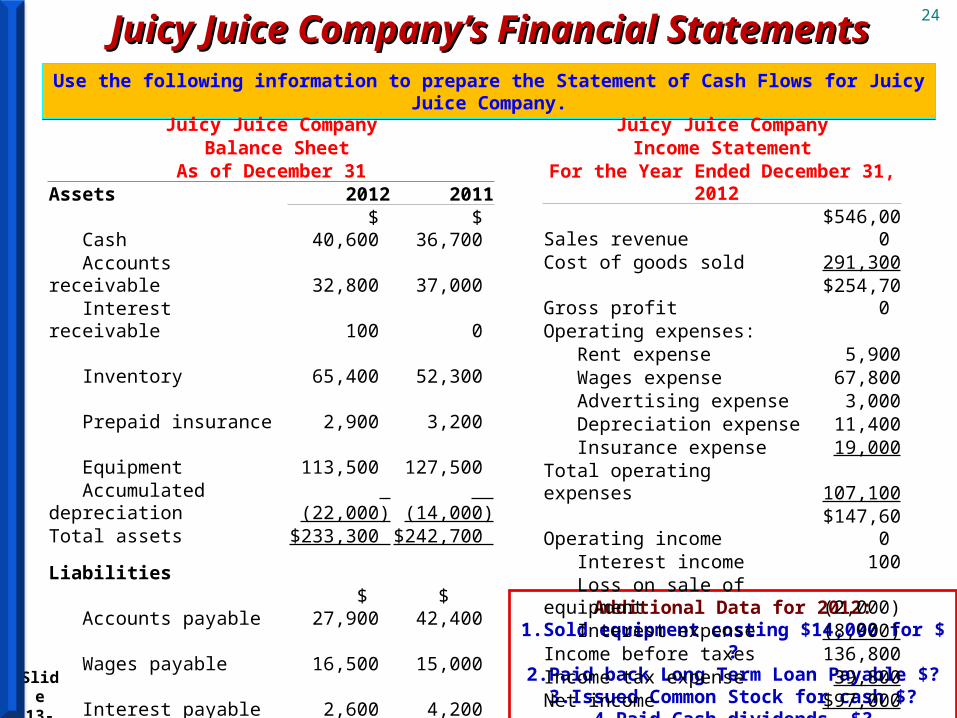

Juicy Juice Company’s Financial Juicy Juice Company’s Financial StatementsStatementsUse the following information to prepare the Statement of Cash Flows for Juicy Juice Company.Use the following information to prepare the Statement of Cash Flows for Juicy Juice Company.

Juicy Juice Company Balance Sheet

As of December 31Assets 2012 2011 Cash $ 40,600 $ 36,700 Accounts receivable 32,800 37,000 Interest receivable 100 0 Inventory 65,400 52,300 Prepaid insurance 2,900 3,200 Equipment 113,500 127,500 Accumulated depreciation (22,000) (14,000)Total assets $233,300 $242,700

Liabilities Accounts payable $ 27,900 $ 42,400 Wages payable 16,500 15,000 Interest payable 2,600 4,200 Income tax payable 8,100 5,400 Unearned revenue 15,100 18,300 Long-term loan payable 60,000 73,000 Equities Common stock 59,100 47,000 Retained earnings 44,000 37,400 Total liabilities and equity $233,300 $242,700

Additional Data for 2012:1.Sold equipment costing $14,000 for $ ?2.Paid back Long Term Loan Payable $?

3.Issued Common Stock for cash $?4.Paid Cash dividends, $?

Juicy Juice CompanyIncome Statement

For the Year Ended December 31, 2012 Sales revenue $546,000 Cost of goods sold 291,300Gross profit $254,700 Operating expenses: Rent expense 5,900 Wages expense 67,800 Advertising expense 3,000 Depreciation expense 11,400 Insurance expense 19,000Total operating expenses 107,100Operating income $147,600 Interest income 100 Loss on sale of equipment (2,000) Interest expense (8,900)Income before taxes 136,800Income tax expense 39,800Net income $97,000

Slide 13-25

25Operating Activities Section of Juicy Juice Company’s Statement of Operating Activities Section of Juicy Juice Company’s Statement of Cash FlowsCash Flows

Slide 13-26

Knowledge Check Question:Knowledge Check Question:A company's income statement showed the A company's income statement showed the following: net income, $124,000; depreciation following: net income, $124,000; depreciation expense, $30,000; and gain on sale of plant expense, $30,000; and gain on sale of plant assets, $14,000. An examination of the assets, $14,000. An examination of the company's current assets and current liabilities company's current assets and current liabilities showed the following changes as a result of showed the following changes as a result of operating activities: accounts receivable operating activities: accounts receivable decreased $9,400; merchandise inventory decreased $9,400; merchandise inventory increased $18,000; prepaid expenses decreased increased $18,000; prepaid expenses decreased $6,200; accounts payable increased $3,400. $6,200; accounts payable increased $3,400. Calculate the net cash provided by operating Calculate the net cash provided by operating

activities.activities. 1.1. $139,000. $139,000. 2.2. $141,000. $141,000. 3.3. $145,800. $145,800. 4.4. $155,000. $155,000.

Slide 13-27

Investing Activities for Juicy Juice Investing Activities for Juicy Juice CompanyCompanyInvesting Activities for Juicy Juice Investing Activities for Juicy Juice CompanyCompany

The Additional Data section notes that Juicy Juice Company

sold some equipment. Determine the cash proceeds from the

sale.

Slide 13-28

Financing Activities for Juicy Juice Financing Activities for Juicy Juice CompanyCompanyFinancing Activities for Juicy Juice Financing Activities for Juicy Juice CompanyCompanyThe Additional Data section notes that the company paid

back some of its Long Term Loan Payable. Determine the

cash payment.

Slide 13-29

Financing Activities for Juicy Juice Financing Activities for Juicy Juice CompanyCompanyFinancing Activities for Juicy Juice Financing Activities for Juicy Juice CompanyCompanyThe additional data section notes that the company

issued some new shares for cash. Determine the cash

proceeds.

Slide 13-30

Financing Activities for Juicy Juice Financing Activities for Juicy Juice CompanyCompanyFinancing Activities for Juicy Juice Financing Activities for Juicy Juice CompanyCompany

The Additional Data section reported that the company paid cash dividends. Determine the cash paid for dividends.

Slide 13-31

Knowledge Check:Knowledge Check:Equipment costing $100,000 with Equipment costing $100,000 with accumulated depreciation of accumulated depreciation of $40,000 is sold at a loss of $40,000 is sold at a loss of $10,000. What amount would be $10,000. What amount would be reported under “Cash Flows from reported under “Cash Flows from Investing Activities?Investing Activities?1.1. $40,000$40,000

2.2. $50,000$50,000

3.3. $60,000$60,000

4.4. $70,000$70,000

Slide 13-32

Knowledge Check:Knowledge Check:Lance Company’s financial statements Lance Company’s financial statements showed that the Retained Earnings showed that the Retained Earnings account had a balance of $30,100 on account had a balance of $30,100 on December 31, 2010, and a balance of December 31, 2010, and a balance of $41,500 on December 31, 2011. The net $41,500 on December 31, 2011. The net income for the year 2011 was $25,800. If income for the year 2011 was $25,800. If the only change affecting retained the only change affecting retained earnings are net income and cash earnings are net income and cash dividends paid, calculate the cash dividends paid, calculate the cash dividends paid during 2011.dividends paid during 2011.1.1. $10,100$10,100

2.2. $45,800$45,800

3.3. $14,400$14,400

4.4. $15,700$15,700

Slide 13-33

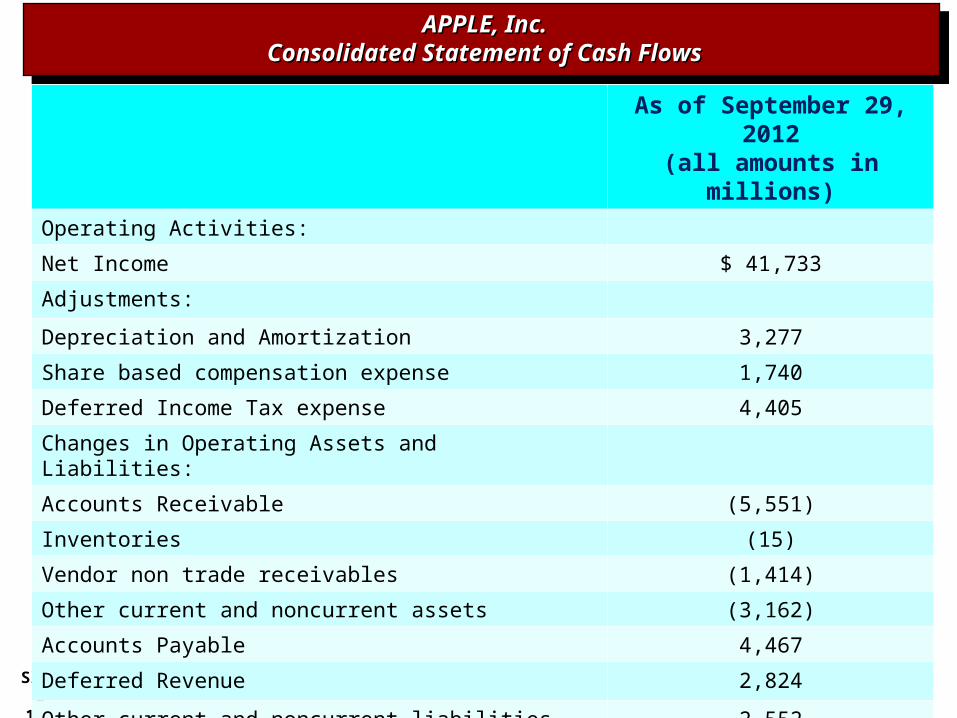

As of September 29, 2012(all amounts in millions)

Operating Activities:

Net Income $ 41,733

Adjustments:

Depreciation and Amortization 3,277

Share based compensation expense 1,740

Deferred Income Tax expense 4,405

Changes in Operating Assets and Liabilities:

Accounts Receivable (5,551)

Inventories (15)

Vendor non trade receivables (1,414)

Other current and noncurrent assets (3,162)

Accounts Payable 4,467

Deferred Revenue 2,824

Other current and noncurrent liabilities 2,552

Cash generated by operating activities $ 50,856

APPLE, Inc.APPLE, Inc.Consolidated Statement of Cash FlowsConsolidated Statement of Cash Flows

APPLE, Inc.APPLE, Inc.Consolidated Statement of Cash FlowsConsolidated Statement of Cash Flows

Slide 13-34

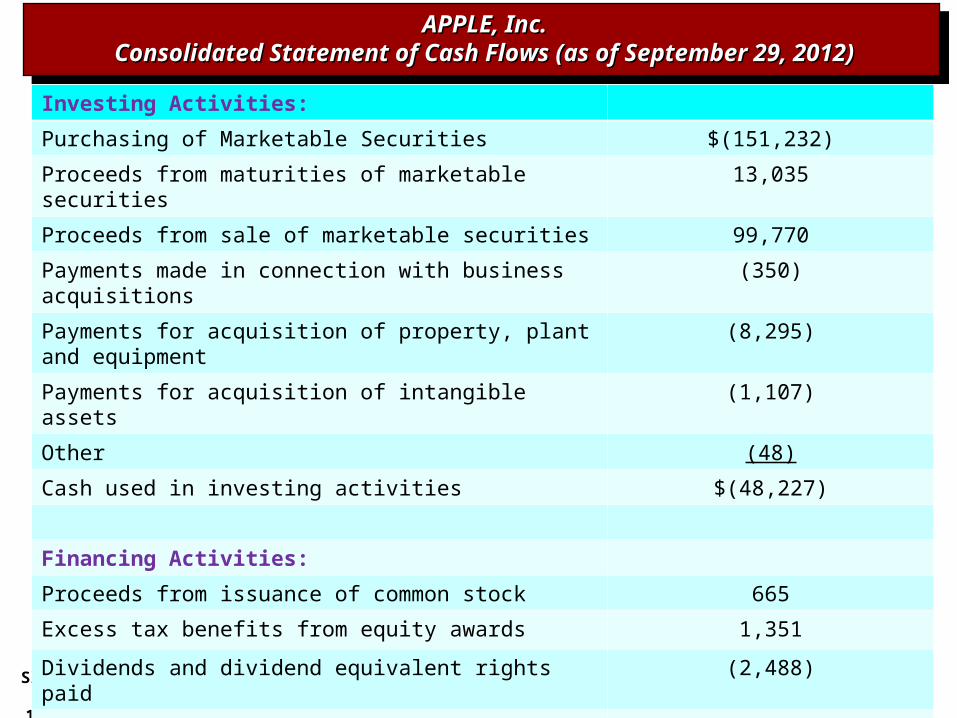

Investing Activities:

Purchasing of Marketable Securities $(151,232)

Proceeds from maturities of marketable securities 13,035

Proceeds from sale of marketable securities 99,770

Payments made in connection with business acquisitions (350)

Payments for acquisition of property, plant and equipment (8,295)

Payments for acquisition of intangible assets (1,107)

Other (48)

Cash used in investing activities $(48,227)

Financing Activities:

Proceeds from issuance of common stock 665

Excess tax benefits from equity awards 1,351

Dividends and dividend equivalent rights paid (2,488)

Taxes paid related to net share settlement of equity awards

(1,226)

Cash used in financing activities $(1,698)

Increase in Cash and Cash Equivalents $ 931

APPLE, Inc.APPLE, Inc.Consolidated Statement of Cash Flows (as of September 29, Consolidated Statement of Cash Flows (as of September 29,

2012)2012)

APPLE, Inc.APPLE, Inc.Consolidated Statement of Cash Flows (as of September 29, Consolidated Statement of Cash Flows (as of September 29,

2012)2012)

Slide 13-35

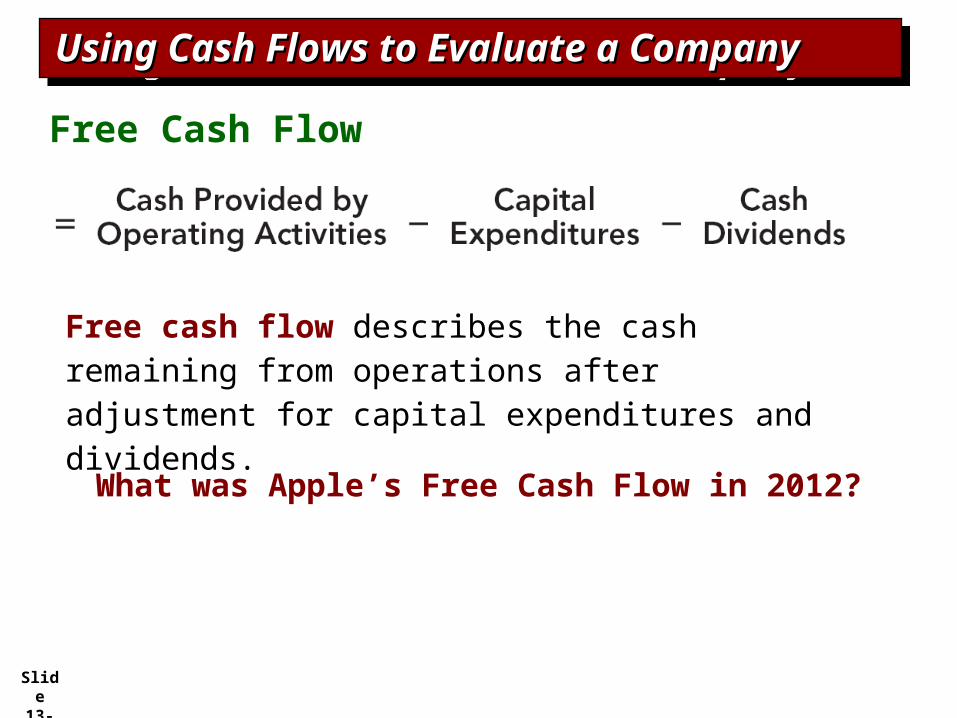

Free Cash Flow

Free cash flow describes the cash remaining from operations after adjustment for capital expenditures and dividends.

Using Cash Flows to Evaluate a Using Cash Flows to Evaluate a CompanyCompanyUsing Cash Flows to Evaluate a Using Cash Flows to Evaluate a CompanyCompany

What was Apple’s Free Cash Flow in 2012?

Slide 13-36

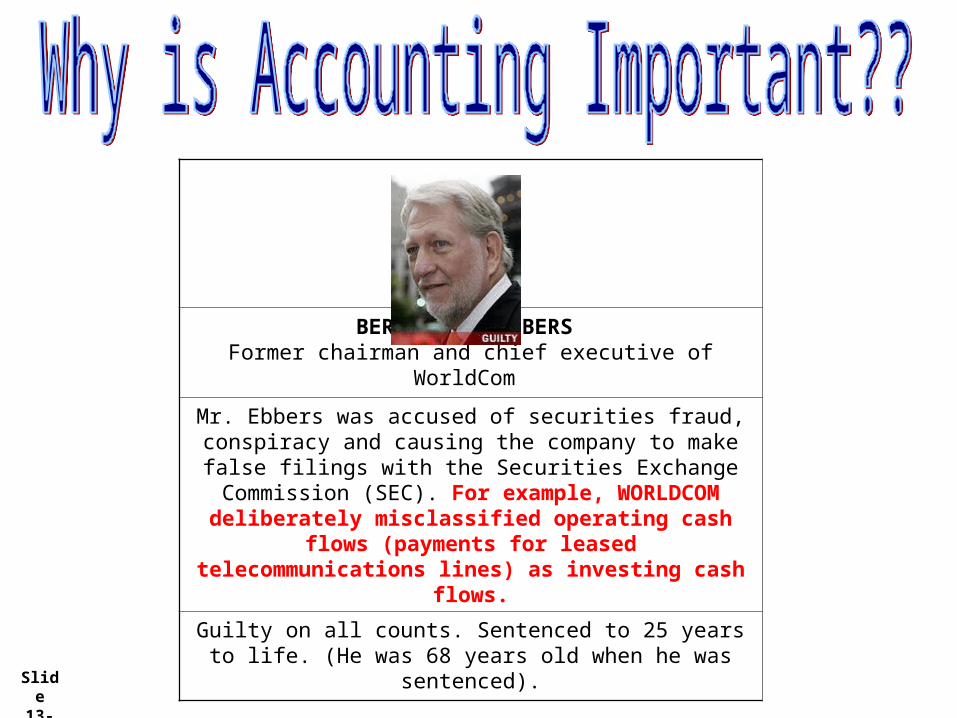

BERNARD J. EBBERS Former chairman and chief executive of WorldCom

Mr. Ebbers was accused of securities fraud, conspiracy and causing the company to make false filings with the

Securities Exchange Commission (SEC). For example, WORLDCOM deliberately misclassified operating cash flows (payments for leased telecommunications lines)

as investing cash flows.

Guilty on all counts. Sentenced to 25 years to life. (He was 68 years old when he was sentenced).

Slide 13-37

End of Chapter 13End of Chapter 13