shining streak - by sanjiv chainani

TRANSCRIPT

u 112 u

Sep tember 30, 2012

buSi n e SS i n di a u the m aga zi n e of the cor por ate wor ldColumn

Shining streakWhen real interest rates are low, the yellow metal glitters

“When paper money systems begin to crack at the seams, the run to gold could be explosive”

– Harry Browne

what is real interest rate (rir)? “real interest rate is the lending interest rate adjusted for inflation as mea-

sured by the gdp deflator” – world bank. from this definition, it is very clear that rir is a factor of interest rates prevailing in the economy and the rate of inflation.

it is a known fact that india is struggling with the problem of persistently high infla-tion despite the tight monetary policy stance adopted by the reserve bank of india (rbi). this has resulted in a lower-to-negative rir in india in past few years.

on the other hand, western economies are facing the problem of a liberal monetary policy with all-time low interest rates and constant infusion of money by way of quanti-tative easing to boost their economies. this has resulted in the lower or negative rir in western economies.

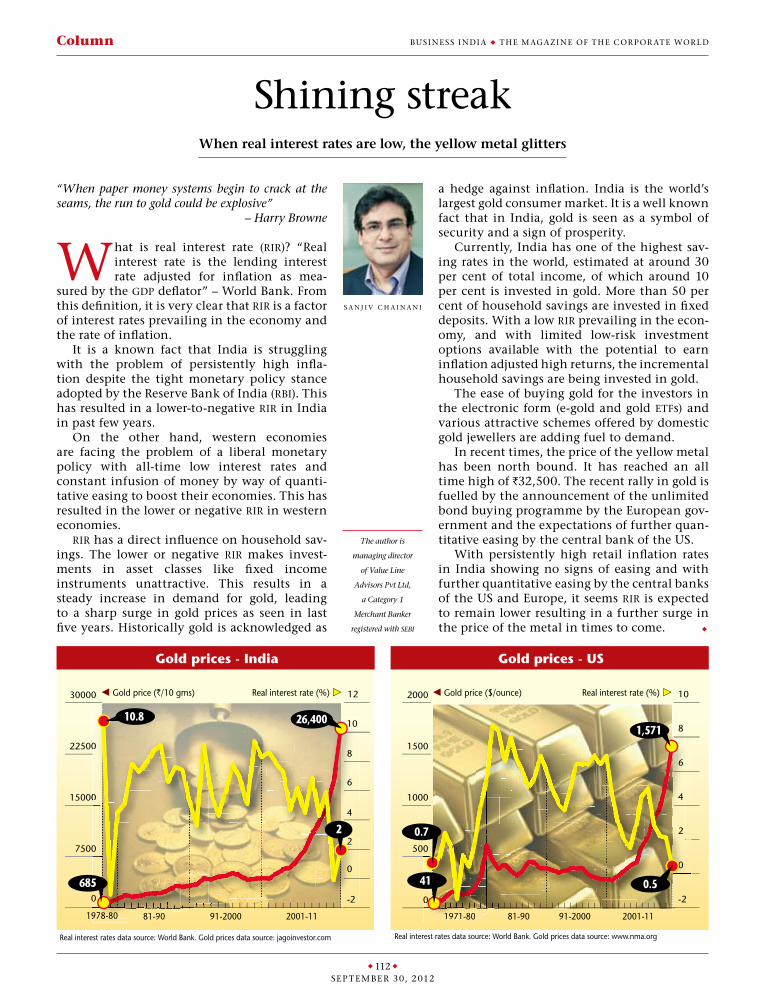

rir has a direct influence on household sav-ings. the lower or negative rir makes invest-ments in asset classes like fixed income instruments unattractive. this results in a steady increase in demand for gold, leading to a sharp surge in gold prices as seen in last five years. historically gold is acknowledged as

a hedge against inflation. india is the world’s largest gold consumer market. it is a well known fact that in india, gold is seen as a symbol of security and a sign of prosperity.

currently, india has one of the highest sav-ing rates in the world, estimated at around 30 per cent of total income, of which around 10 per cent is invested in gold. more than 50 per cent of household savings are invested in fixed deposits. with a low rir prevailing in the econ-omy, and with limited low-risk investment options available with the potential to earn inflation adjusted high returns, the incremental household savings are being invested in gold.

the ease of buying gold for the investors in the electronic form (e-gold and gold etfs) and various attractive schemes offered by domestic gold jewellers are adding fuel to demand.

in recent times, the price of the yellow metal has been north bound. it has reached an all time high of `32,500. the recent rally in gold is fuelled by the announcement of the unlimited bond buying programme by the european gov-ernment and the expectations of further quan-titative easing by the central bank of the uS.

with persistently high retail inflation rates in india showing no signs of easing and with further quantitative easing by the central banks of the uS and europe, it seems rir is expected to remain lower resulting in a further surge in the price of the metal in times to come. u

The author is

managing director

of Value Line

Advisors Pvt Ltd,

a Category 1

Merchant Banker

registered with sebi

S a n j i v c h a i n a n i

Gold prices - US

1971-80 81-90 91-2000 2001-11

0

500

1000

1500

2000

0

1197

-2

0

2

4

6

8

10

0

11 -801-97 -81-979 808197

22

0

22

Gold price ($/ounce) Real interest rate (%)

Real interest rates data source: World Bank. Gold prices data source: www.nma.org

1,571

0.7

41 0.5

Gold prices - India

1978-80 81-90 91-2000 2001-11

0

7500

15000

22500

30000

978-80 8-800 81 9818 909818 909818

0

0

0

97

0

8 800

-2

0

2

4

6

8

10

12 Gold price (`/10 gms) Real interest rate (%)

Real interest rates data source: World Bank. Gold prices data source: jagoinvestor.com

10.8

685

26,400

2