shale gas: analyzing risks and opportunities - boston university

TRANSCRIPT

Shale Gas: Analyzing Risks and Opportunities

Sue Tierney – Analysis Group

Society for Risk Assessment Boston University – April 9, 2012

Society for Risk Assessment / Boston University

O i N t l G Ri k d O t itiOverview – Natural Gas Risks and Opportunities:

Shale Gas: Game Changer or Something Else?Context for my comments

What’s happening with shale gas

Some implications

Page 2April 9, 2012

Society for Risk Assessment / Boston University

CONTEXT FOR MY COMMENTS:Natural Gas: Shale Gas

CONTEXT FOR MY COMMENTS:Recent Involvement in NPC and SEAB Studies

Page 3April 9, 2012

Society for Risk Assessment / Boston University

O i d b k dOverview and background:

Who: SEAB Board Natural Gas SubcommitteeDeutch, Holditch, McGinty, Krupp, Yergin, Tierney, Zoback

Wh t P id ti l t t S t ChWhat: Presidential request to Secretary Chu (Blueprint for Secure Energy Future Charge):

examine steps to improve the safety and environmental performance of shale gas developmentnot regulation, per se

When: Initial report: mid-August 2011Final report: mid-November 2011

Page 4April 9, 2012

Society for Risk Assessment / Boston University

O i d b k dOverview and background:

Who: National Petroleum Council

What: Energy Secretary Request to NPCAssessment of the size of the oil and natural gas resource base in North Americabase in North AmericaAssessment of the role of natural gas in GHG reductions

When: Start – early 2010When: Start early 2010

Report: September 15, 2011“Prudent Development: Realizing thePrudent Development: Realizing the Potential of North America’s Abundant Natural Gas and Oil Resources”

Page 5April 9, 2012

Society for Risk Assessment / Boston University

WHAT’S HAPPENINGNatural Gas: Shale Gas

WHAT S HAPPENING

Page 6April 9, 2012

Society for Risk Assessment / Boston University

What does shale gas look like? ROCK

Shale Gas Outcropping

Page 7April 9, 2012

Shale Gas Outcropping –Marcellus

Society for Risk Assessment / Boston University

Wh d h l l k lik ? REGIONSWhat does shale gas look like? REGIONS

Page 8April 9, 2012

Society for Risk Assessment / Boston University Drill site

Stored water

Drinking waterSteel casing and cement

BoreholeWhat does shale gas look like? TECHNOLOGY

Hydraulic fracturing

Page 9April 9, 2012

http://news.nationalgeographic.com/news/energy/2010/10/101022-energy-marcellus-shale-gas-rush/

Horizontal drilling

Society for Risk Assessment / Boston University

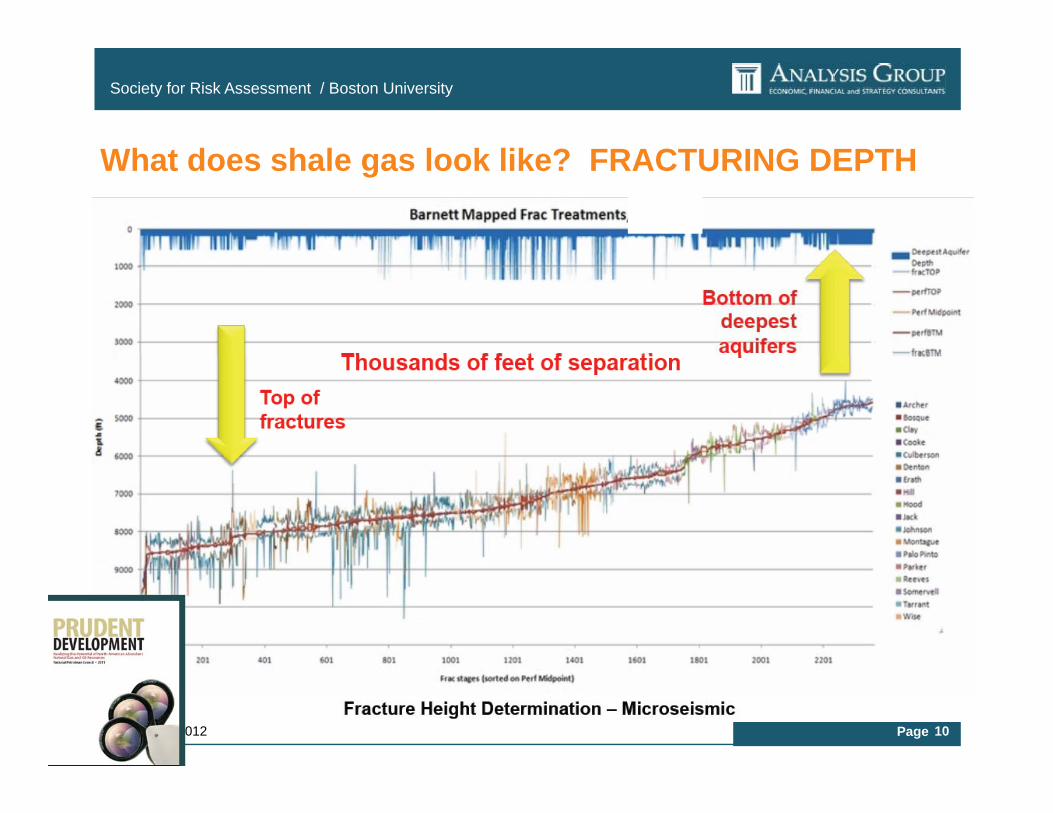

Wh t d h l l k lik ? FRACTURING DEPTHWhat does shale gas look like? FRACTURING DEPTH

Page 10April 9, 2012

Society for Risk Assessment / Boston University

What does shale gas look like? SURFACE ACTIVITIES

Page 11April 9, 2012

http://news.nationalgeographic.com/news/2010/10/photogalleries/101022-energy-shale-gas-drilling-pictures/#/energy-marcellus-shale-environment03-hallowich-dinner_27065_600x450.jpg

Society for Risk Assessment / Boston University

What does shale gas look like? ENVIRONMENTAL RISKSWhat does shale gas look like? ENVIRONMENTAL RISKS

Risks from past ti d

Page 12April 9, 2012

Phil Nguyen, Regulatory Options and Challenges in Hydraulic Fracturing, WISE, 2010

practices and events

Society for Risk Assessment / Boston University

What does shale gas look like? PRODUCTION GROWTHgPast decade…..

Marcellus

Shale plays

Marcellus

Page 13April 9, 2012 NPC, Prudent Development, 2011

Society for Risk Assessment / Boston University

What does shale gas look like? PRODUCTION GROWTHgPast decade ………… versus past two years

Page 14April 9, 2012 NPC, Prudent Development, 2011

Society for Risk Assessment / Boston University

What does shale gas look like?

3500

gPACE OF DEVELOPMENT

Marcellus shale gas permits issued and wells

2500

3000 drilled in Pennsylvania 2007 – 2011 (Dec)

1500

2000

500

1000

0

500

Permitted Drilled

Page 15April 9, 2012

Marcellus Shale Gas Commission, July 2011, Figures 22 and 23; http://www.dep.state.pa.us/dep/deputate/minres/oilgas/Marcellus%20Wells%20permitted-drilled%20NOVEMBER%202011.gif

Society for Risk Assessment / Boston University

What does shale gas look like? ATTENTION (+ and -)

Page 16April 9, 2012

Society for Risk Assessment / Boston University

Wh t d h l l k lik ? SUPPLY ESTIMATESWhat does shale gas look like? SUPPLY ESTIMATES 3500

ANGAChanging estimates of the U.S. natural gas resources* 1999-2011

2500

3000

ICF, PGC

EIA

TCF

2000

NPC EIA EIA EIANPC

PGC, MIT

1000

1500

PGC

PGC/ NPC

NPC

PGC

EIA

500

Page 17April 9, 2012

01999 2000 2003 2004 2005 2006 2007 2008 2009 2010 2011

* Technically recoverable The effect of a reduction in EIA’s Marcellus estimate from 410 Tcf to 84 Tcf (the new USGS estimate, up from 2 in 2002)

Society for Risk Assessment / Boston University

What does shale gas look like? LOWER GAS PRICES1.4

coal

1.0

1.2

0.6

0.8

Average delivered price of coal to electric utilities

gas

0.2

0.4

Average delivered price of coal to electric utilities

Average delivered price of coal to IPPs

Average price of natural gas to electric generators

0.02006 2007 2008 2009 2010

g p g g

S N t l i EIA htt // i /d / / i d ht

Page 18April 9, 2012

Source: Natural gas prices: EIA, http://www.eia.gov/dnav/ng/ng_pri_sum_dcu_nus_a.htm; Coal prices: William Watson, Nicholas Paduano, Tejasvi Raghuveer and Sundar Thapa, EIA, “U.S. Coal Supply and Demand: 2010 Year in Review,” June 1, 2011 (available at http://www.eia.gov/coal/review/pdf/feature10.pdf)

Society for Risk Assessment / Boston University

Natural gas prices – before shale gas……$14

U.S. Natural Gas Price History, 1976 to 2008

$10

$12

y,(Nominal Dollars)

$6

$8

$4

$6

$0

$2

Jan-1976 Jan-1981 Jan-1986 Jan-1991 Jan-1996 Jan-2001 Jan-2006 Jan-2011

Page 19April 9, 2012

Source: EIA, Wellhead prices through 1994. Henry Hub prices from 1995 – 2011

Society for Risk Assessment / Boston University

Natural gas prices – before shale gas……$14

U.S. Natural Gas Price History, 1976 to 2010

$10

$12

y,(Nominal Dollars)

$6

$8

$4

$6

$0

$2

Jan-1976 Jan-1981 Jan-1986 Jan-1991 Jan-1996 Jan-2001 Jan-2006 Jan-2011

Page 20April 9, 2012

Source: EIA, Wellhead prices through 1994. Henry Hub prices from 1995 – 2011

Society for Risk Assessment / Boston University

What does shale gas look like? LOWER GAS PRICES

201120122012

S N t l i EIA htt // i /d / / i d ht

Page 21April 9, 2012

Source: Natural gas prices: EIA, http://www.eia.gov/dnav/ng/ng_pri_sum_dcu_nus_a.htm; Coal prices: William Watson, Nicholas Paduano, Tejasvi Raghuveer and Sundar Thapa, EIA, “U.S. Coal Supply and Demand: 2010 Year in Review,” June 1, 2011 (available at http://www.eia.gov/coal/review/pdf/feature10.pdf)

Society for Risk Assessment / Boston University

What does shale gas look like? LOWER GAS PRICES

9

10 $/mcf 3-2008

3 20103-2009

What does shale gas look like? LOWER GAS PRICES

7

8

3-2011

3-20103-2007

5

6

3-2012

3-2011

2

3

4

0

1

2

Natural Gas Futures – Henry Hub

Page 22April 9, 2012

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

Society for Risk Assessment / Boston University Shale Gas: New Opportunities, New Challenges

Bipartisan Policy Center Energy Project

What does shale gas look like? MEETING DEMAND

40U.S. Energy Consumption by Sector - 2010

30

35 NuclearRenewableCoal

20

25

adril

lion

Btu

Natural GasOil

10

15

Qua

Feedstock

0

5 Feedstock

Page 23April 9, 2012

0

Residential Commercial Industrial Transportation ElectricSource: Bipartisan Policy Center Energy Project; U.S. Energy Information Administration, Annual Energy Outlook 2011.

Society for Risk Assessment / Boston University

What does shale gas look like? LOWER INPUT PRICESMeeting industrial demand (directly, indirectly)

Aluminum manufacturing cost structureTotal power production cost structure

Announcements by Dow Chemical, Shell, Williams Companies: new chemical facility investments

Aluminum manufacturing cost structure Total power production cost structure

Page 24April 9, 2012

Society for Risk Assessment / Boston University

What does shale gas look like? BOOST TO OUTPUT

Industrial d ddemand

Aluminum cost structure

Page 25April 9, 2012

Society for Risk Assessment / Boston University

What does shale gas look like? PRESSURE ON COAL PLANTS

U.S. Major Coal-Fired Power Plants

Page 26April 9, 2012Source: National Public Radio – http://www.npr.org/templates/story/story.php?storyId=110997398, based on information from: American Electric Power, American Wind Energy Association, Center for American Progress, Department of Energy, Edison Electric Institute, Energy Information Administration, Electric Power Research Institute, Federal Energy Regulatory Commission, National Renewable Energy Laboratory, Environmental Protection Agency, Western Resource Advocates

Society for Risk Assessment / Boston University

Impacts from electricity produced at coal power plantsImpacts from electricity produced at coal power plants

National Mortality Effects from Existing National Mortality Effects from Existing Power Plants (Annual Persons/100 000)Power Plants (Annual Persons/100 000)Power Plants (Annual Persons/100,000)Power Plants (Annual Persons/100,000)

< 3< 333--77

77--10101010--1414> 14> 14 14 14

Annual Mortality Due to Individual Annual Mortality Due to Individual Power Plants (Persons)Power Plants (Persons)

<25<252525--7575> 75> 75

Page 27April 9, 2012Clean Air Task Force, “Toll from Coal,” 2010 (Google Maps programs)

Society for Risk Assessment / Boston University

What does shale gas look like? ALTERNATIVES TO COALWhat does shale gas look like? ALTERNATIVES TO COALPower plants affected by EPA MATS Rule

Page 28April 9, 2012

Society for Risk Assessment / Boston University

Coal plant capacity –All coal plantsWithout emission controls, by state

12

All coal plants

8

10

6GW

4

Coal Units Without Emissions Controls(Total GW – 2009)

0

2

(Total GW 2009)

Page 29April 9, 2012

0

IL MI

OH

MO TX IN IA OK

TN AL KY PA NC

NE

WV SC GA VA WI

AR FL LA MS

MD NY

MN KS DE

CO MA

UT

MT CT ND NJ

CA WY

NV AZ ME

NH SD ID NM

Notes:[1] Totals do not include Alaska or Hawaii.[2] Units without emissions are those units without SCR or FGD systems.

Source: SNL data.

Society for Risk Assessment / Boston University 200810GW load 20GW load 25GW load

Coal: $31 7

Gas:$95 1ISO-NE

Oil$157.9

$31.7 $95.1

@20 GW load, gas price is3x coal @10GW load3 coa @ 0G oad

2010What it means for NE electricity consumers

Coal: Gas:Gas:$94.5

What it means for NE electricity consumers…..

$39.0Gas:$43.4

@20 GW load gas price is

Page 30April 9, 2012

@20 GW load, gas price is1.1x coal @10GW load

SNL Financial Data, accessed 3-1-2012

Society for Risk Assessment / Boston University

Page 31April 9, 2012

Society for Risk Assessment / Boston University

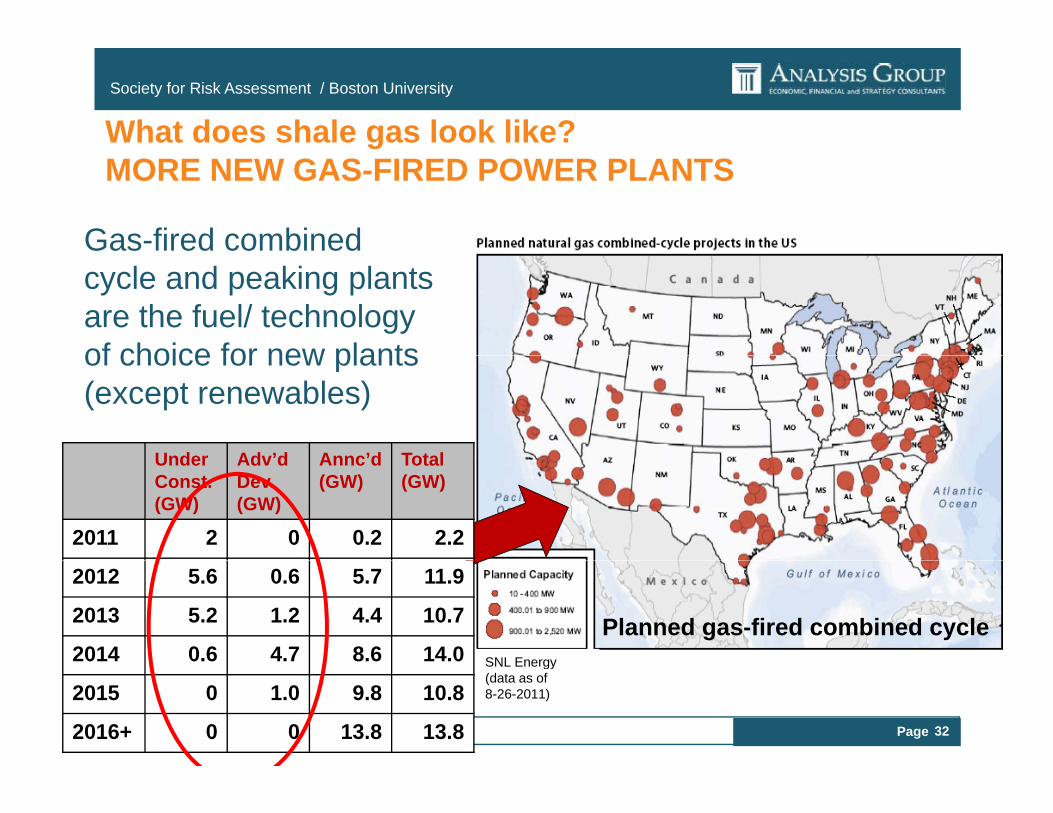

What does shale gas look like?MORE NEW GAS-FIRED POWER PLANTS

Gas-fired combined cycle and peaking plants are the fuel/ technology of choice for new plantsof choice for new plants (except renewables)

Under Adv’d Annc’d TotalUnder Const. (GW)

Adv dDev. (GW)

Annc d(GW)

Total (GW)

2011 2 0 0.2 2.2

SNL Energy

Planned gas-fired combined cycle

2012 5.6 0.6 5.7 11.9

2013 5.2 1.2 4.4 10.7

2014 0.6 4.7 8.6 14.0

Page 32April 9, 2012

SNL Energy (data as of 8-26-2011)2015 0 1.0 9.8 10.8

2016+ 0 0 13.8 13.8

Society for Risk Assessment / Boston University

Markets: Gas-fired plants are now the fuel/technology of choice

140.00

Natural gas prices:

100.00

120.00Natural gas prices:

Already putting pressure on many coal plants

Possible to sign long-term fuel contracts

60 00

80.00

40.00

60.00

0.00

20.00

Hydro Nuclear Coal Wind Solar Natural gas

Page 33April 9, 2012

Hydro Nuclear Coal Wind, Solar, Biomass

Natural gas

EIA, Annual Energy Outlook, 2011

Society for Risk Assessment / Boston University

More gas-powered generation aheadMore gas powered generation aheadISO-NE Interconnection Queue* (new generation projects)

60%

5 931 MWNatural gas prices:

40%

50%

5,931 MWAlready putting pressure on many coal plants, but also other technologies (renewables, nuclear)

Increasingly able to sign long-term fuel contracts,but may require alignment between capacity

30%

40% but may require alignment between capacity markets, firm transportation service, and other market rules

10%

20% 2,430 MW

10%

0%Gas Wind Hydro Solar Oil Biomass

1,163 MW

345 MW

Page 34April 9, 2012

-10%

* ISO-NE, “Active FERC” Queue, as of 2-1-2012 (does not include transmission projects or equipment replacement)

Society for Risk Assessment / Boston University

Gas will be needed even more as renewables ramp upGas will be needed even more as renewables ramp up

Significant increases in renewable energy needed in upcoming years

Colorado

energy needed in upcoming years to meet RPS requirements – with push and pull from gas market

conditions and operations Maryland

Pennsylvania

N Y k

New Jersey

Texas

2011

California

New York

Page 35April 9, 2012

http://www.emerging-energy.com/content/press-details/State-RPS-Policies-Will-Drive-250-Increase-in-Renewable-Energy-Generation-by-2025/32.aspx

2x 3x

Society for Risk Assessment / Boston University

OPPORTUNITIES ANDImplications for Massachusetts and the Region

OPPORTUNITIES AND CHALLENGES

Page 36April 9, 2012

Society for Risk Assessment / Boston University

A huge opportunity for U.S. energy markets

NPC report: “N. America’s natural gas resource base is enormous – with potential benefits to the economy, environment and energy security”y, gy y

Secretary of Energy Advisory Board report:

“extremely important for U.S. energy security, with potentially large economic impact on local communities and states” and well aslocal communities and states and well as benefits for customers of natural gas and electricity

Page 37April 9, 2012

Society for Risk Assessment / Boston University

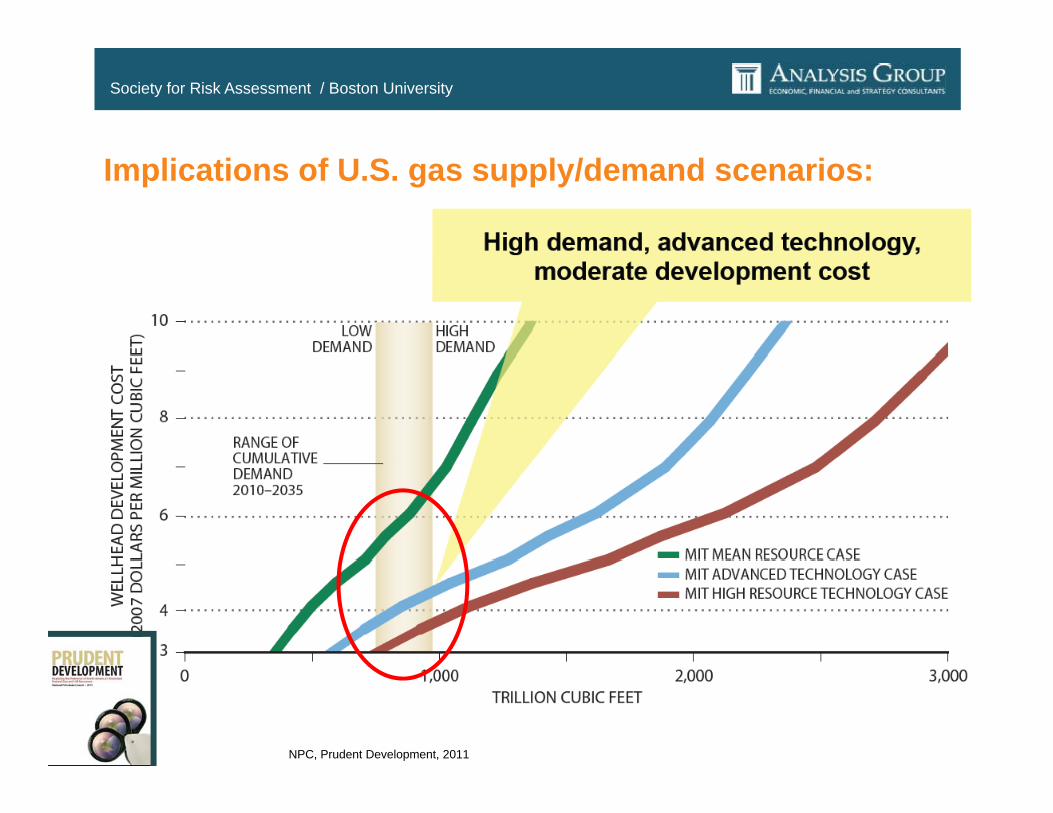

Implications of U.S. gas supply/demand scenarios:

Page 38April 9, 2012

NPC, Prudent Development, 2011

Society for Risk Assessment / Boston University

U S G d d tl k d i b tU.S. Gas demand outlooks – driven by power sector

Page 39April 9, 2012 NPC, Prudent Development, 2011

Society for Risk Assessment / Boston University

But this depends upon doing it right …..NPC report: ‘benefits depend on prudent development’

Everywhere, responsible practices are needed.

Regulators must evolve their requirements.

Such steps are necessary for public trust, protection of health, safety and the environment – and for maintaining access to the natural gas resources.maintaining access to the natural gas resources.

Page 40April 9, 2012

Society for Risk Assessment / Boston University

But this depends upon doing it right …..SEAB report: ‘genuine environmental urgency’

There are potentially serious environmental impacts.

These impacts need to be prevented, reduced and, h ibl li i t d iblwhere possible, eliminated as soon as possible.

Absent effective control, public opposition will grow, thus putting continued production at risk.thus putting continued production at risk.

Page 41April 9, 2012

Society for Risk Assessment / Boston University

SEAB’s “environmental urgency” related to shale gas:

Areas of concern:

Water – possible pollution of drinking water (methane, chemicals), water consumption, disposition/management of flow back waterdisposition/management of flow back water

Air pollution – GHG (methane), ozone precursors

Community disruption during shale gas production

Preservation of unique and/or sensitive areas

Cumulative adverse impacts (traffic, noise, visual, odors, intensity) on communities and ecosystems, wildlife

Page 42April 9, 2012

wildlife

Society for Risk Assessment / Boston University

Natural gas can help lower GHG emissions

Deep reductions require CCS or other zero-

Page 43April 9, 2012 NPC, Prudent Development, 2011

CCS or other zerocarbon technologies

Society for Risk Assessment / Boston University

GHG reductions …Depend on addressing methane emissions from gas….

120 0120

Comparison of NG and Coal Burnertip GHG Emissions in Recent LCAs

94.2

79.9

104.899.2 99.7 100.2 96.3

106.4101.9

107.4

80 0

100.0

120.0

80

100

120

u

MethaneUpstream CO2Fuel CO2

Natural Gas Coal

65.172.3

63.167.7 64.5

70.2

40 0

60.0

80.0

40

60

80

kg CO2e/M

MBtu

Variation in total footprint is largely due to

uncertainty

0 0

20.0

40.0

0

20

40k

in methane

0.00

DB 20

10

DB 20

11

Jaramillo

Barnett

Dom

estic

Conv Low

Conv High

Shale Low

Shale High

DB

Jaramillo

Dom

estic

PRB

Illinois #6

Surface

Und

ergrou

nd

DBCCA/WWINETL Howarth NETL Howarth

Page 44April 9, 2012

Source: Armond Cohen, Clean Air Task Force, “Natural Gas and Climate Bridge, Highway, or Destination?” EUEC presentation, 1-30-2012

Howarth Howarth

Society for Risk Assessment / Boston University

Shale gas – and energy marketsShale gas development provides opportunities for:

lower building heating costs than previously expected

lower power prices than previously expected – and less differential than in traditional coal regionsdifferential than in traditional coal regions

lower emissions profile of power plants in upwind regions

B tBut ….greater challenges with meeting renewables’ targets

greater need for integration of gas/electric market operations

increased attention by many players to the GHG from gas

Page 45April 9, 2012

increased attention by many players to the GHG from gas

Society for Risk Assessment / Boston University

Sue TierneyManaging PrincipalManaging PrincipalAnalysis Group111 Huntington Avenue, 10th Floor Boston, MA [email protected]

Page 46April 9, 2012