shale gas exploration: why should india be cautious to … · shale gas – a new mantra •shale...

TRANSCRIPT

Block: Natural Gas Processing, Transportation and MarketingForum: Impact of growing unconventional gas supply

Shale gas exploration: Why should India be cautious to commit?Why should India be cautious to commit?

Saurabh AgarwalaS E i E i I di Li it d I diSr. Engineer, Engineers India Limited, IndiaA Deshpande, G Prasad, R K Gupta, Engineers India Limited, India

Moscow, Russia | 15-19 June, 2014

Abstract

Block: Natural Gas Processing, Transportation and MarketingForum: Impact of growing unconventional gas supply

AbstractIndia’s growth story has resulted in increased energy consumption and thus need for uninterrupted, economicalviable & clean fuel supplies. Due to lack of sufficient indigenous supply options to mitigate the growing demand-supply gap, India is bound to consider unconventional resources. Unconventional resources encompass tight oil andgas formations, shale gas, coalbed methane, heavy oil, oil shale, deep and ultra deep water plays, and gas hydrates.

Shale-gas being projected as new mantra, a game-changer, has thus called for attention and serious considerationby Indian policy makers. The most significant contribution, from Indian side towards shale gas exploration, yet, hasbeen the supply of guar or cluster beans which is used to increase the viscosity of proppants materials which arebeen the supply of guar or cluster beans which is used to increase the viscosity of proppants, materials which areforced into shale fractures to enlarge them so that the oil and gas can be extracted.

In India, shale deposits are found across the Gangetic plain, Assam, Rajasthan and many coastal areas butestimation of reserves have not been carried out thoroughly. There are various factors that policy makers will need to

ti i b f i h d ith i l d ti f h l E ti f l l d d iscrutinize before going ahead with commercial production of shale gas. Expertise of local producers and servicesector, land use, availability of infrastructure, availability of data and its analysis, treatment of water and containmentare few such issues. SWOT analysis has been done to establish the status of system and thus study internal andexternal development environment. A development strategy is formulated to address the issues and suggest a wayforward.

Keywords: Indian gas scenario, Shale gas, Energy demand, SWOT, Regulatory framework

Moscow, Russia | 15-19 June, 2014

Shale Gas – a new Mantra

•Shale gas is naturalgas producedgas producedfrom shale, a type ofsedimentary rock.Shale gas is trappedShale gas is trappedin rock formationsand carbon-richorganic matter(called kerogen).•Methane is thelargest constituent ofshale gas (~95% inshale gas (~95% incomposition)

Moscow, Russia | 15-19 June, 2014

Developed on the basis of Rogers’ Five Factors Model

CHINATechnically Recoverable Shale Gas

Shale Gas – Why is everyone talking about it? Global energy demand increases byone-third from 2010 to 2035, with

INDIAUSA

1161 Tcf

CHINA1115 Tcf

one third from 2010 to 2035, withChina & India accounting for 50% ofthe growth.US Shale gas production is projected

96 Tcf

AUSTRALIAS. AFRICA

390 Tcf

to increase from 23% of total US gasproduction in 2010 to 49% by 2035.

Growth in primary energy demand

Data Source: EIA Report 2013AUSTRALIA

437 TcfCountries seeking energy independence areexcited about shale gas. China, Australia and3000

4000ChinaIndiaRest of AsiaRussiaMiddle East excited about shale gas. China, Australia and

Canada are leaders in shale gas exploration asthe unconventional resources have promisedenergy security. World over the contribution of1000

2000

mto

e

Middle East

crude oil towards energy mix will decrease & thatof natural (including shale gas) will increase.

Moscow, Russia | 15-19 June, 2014

0

2010 2015 2020 2025 2030

• Conventional gas has high capitalintensity but also offers predefined

Shale Gas – What’s different?

intensity but also offers predefineddevelopment plan. Shale gas, on the otherhand, has higherhigher lifecyclelifecycle capexcapex whereconstant re-investment is required in newqwells. The methodology is of ongoingongoing fieldfielddevelopmentdevelopment optimizationoptimization. Shale gasrequires largerlarger acreageacreage (about 67% moreb ti t ) d ll liliby an estimate) and longerlonger licenselicensedurationduration compared to conventional source.

Conventional asset life cycle

ExplorationExploration ProductionProductionDevelopmentDevelopmentAppraisalAppraisal

Unconventional asset life cycle

Moscow, Russia | 15-19 June, 2014

Concept Pilot Ramp-up Manufacture Exploit y

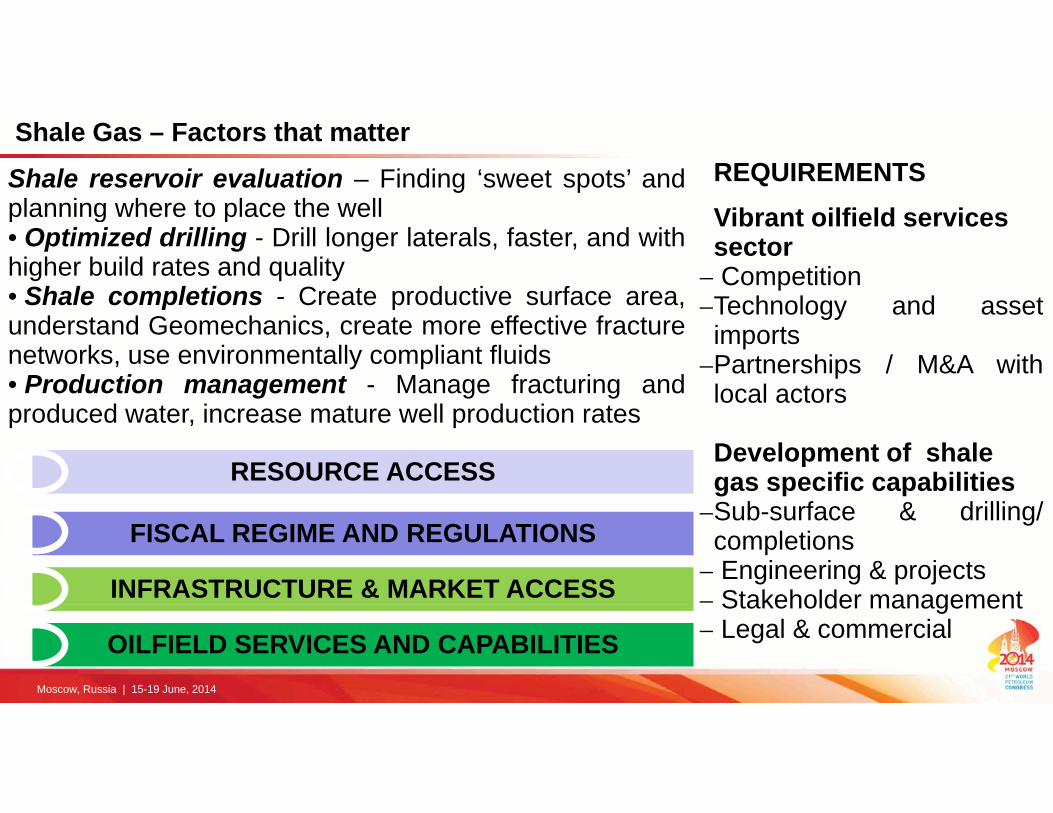

Shale Gas – Factors that matterREQUIREMENTSVib t ilfi ld i

Shale reservoir evaluation – Finding ‘sweet spots’ andplanning where to place the well Vibrant oilfield services

sectorCompetition

Technology and asset

planning where to place the well• Optimized drilling - Drill longer laterals, faster, and withhigher build rates and quality• Shale completions - Create productive surface area, Technology and asset

importsPartnerships / M&A withlocal actors

p p ,understand Geomechanics, create more effective fracturenetworks, use environmentally compliant fluids• Production management - Manage fracturing and

d d t i t ll d ti tDevelopment of shale gas specific capabilitiesS b f & d illi /

produced water, increase mature well production rates

RESOURCE ACCESSRESOURCE ACCESSSub-surface & drilling/completionsEngineering & projectsStakeholder management

FISCAL REGIME AND REGULATIONSFISCAL REGIME AND REGULATIONS

INFRASTRUCTURE & MARKET ACCESSINFRASTRUCTURE & MARKET ACCESS

Moscow, Russia | 15-19 June, 2014

Stakeholder managementLegal & commercialOILFIELD SERVICES AND CAPABILITIESOILFIELD SERVICES AND CAPABILITIES

Factoring upChallenges in monetizingshale gas assets:

If resource access indicates size and duration of license thenfiscal regime stresses on regulations on issues like water g

•Shale gas E&P is anarrow margin business.Sh l ti ti

Resource ServicesInfra-Fiscal

g gmanagement. Availability of pipeline distribution is majorinfrastructure requirement as is mature services sector.

•Shale gas monetizationare long term plays andworks best on economiesof scale

Australia

Access structureRegime

of scale.•Well stimulation design& execution requirestechnical and

Argentina

Chinaengineering excellence ofa high order• It requires lager tractsof inhabited land

India

Poland

Moscow, Russia | 15-19 June, 2014

of inhabited land.Algeria

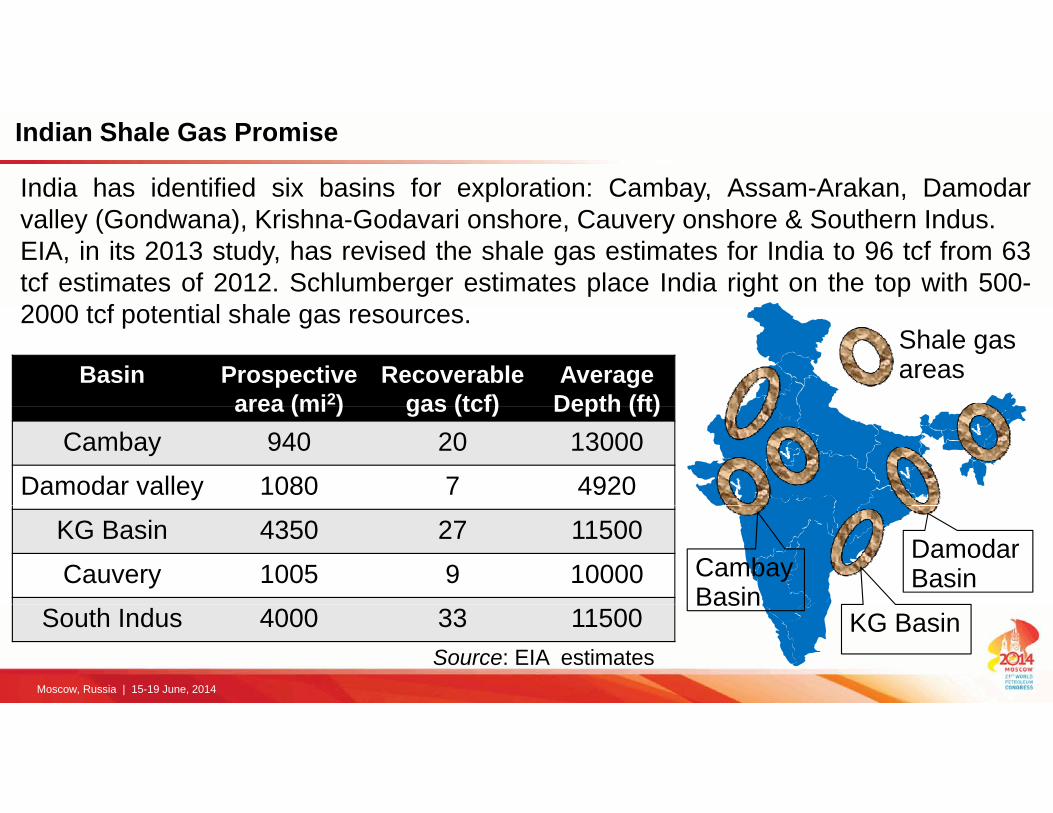

Indian Shale Gas Promise

India has identified six basins for exploration: Cambay, Assam-Arakan, Damodarll (G d ) K i h G d i h C h & S h I dvalley (Gondwana), Krishna-Godavari onshore, Cauvery onshore & Southern Indus.

EIA, in its 2013 study, has revised the shale gas estimates for India to 96 tcf from 63tcf estimates of 2012. Schlumberger estimates place India right on the top with 500-2000 t f t ti l h l2000 tcf potential shale gas resources.

Shale gas areasBasin Prospective

area (mi2)Recoverable

gas (tcf)Average Depth (ft)area (mi ) gas (tcf) Depth (ft)

Cambay 940 20 13000

Damodar valley 1080 7 4920

Damodar BasinCambay

Basin

KG Basin 4350 27 11500

Cauvery 1005 9 10000

Moscow, Russia | 15-19 June, 2014

BasinKG BasinSouth Indus 4000 33 11500

Source: EIA estimates

Indian Gas Scenario – Crossing the chasm

India’s natural gas market continues to be in a stateof deficit In FY12 around 38% of the gas demandof deficit. In FY12, around 38% of the gas demandwas unmet. Energy consumption in India is to growat 3% per annum out with natural gas growing at4 5% By 2015 the demand for gas in India is

???

4.5%. By 2015, the demand for gas in India isprojected to rise by approximately 40% whileaggregate domestic output will only rise 8.7%.

India needs to decide if shalegas technologies should be

???

g gadopted in early stages or tocross the chasm. Bulgaria,Denmark, France are facing

i t f itiresistance from citizens onshale gas ventures.

Moscow, Russia | 15-19 June, 2014

Innovators Early Adopters

Early Majority

Late Majority

Laggards

Why can’t India just replicate US model?WATER SOURCE GAS TRANSPORT WASTE DISPOSALISSUES US SHALE INDIAN SHALE

Industry Structure Competition between E&P’s andintegrated oil companies for

Only National players(ONGC OIL) have beenintegrated oil companies for

acreage(ONGC, OIL) have beenallocated resources yet

Industry age & size 1400 to 1500 rigs were deployedin US to achieve close to 35 000

Fewer than 100 land rigsdrilled less than 650 wellsin US to achieve close to 35,000

natural gas wells in a 20 yearsold industry

drilled less than 650 wellsin an infant industry of 2-3years

Sub surface substantial sub surface legacy sub surface dataSub-surfaceunderstanding

substantial sub-surface legacydata available

sub surface dataavailability is limited

Technology Advanced in drilling rigs, multi-t f i t fl id

Foreign exposure will beiti l t l

Moscow, Russia | 15-19 June, 2014

stage fraccing, proppant fluids critical to learn

Challenges for Indian Shale industry

Very limited subsurface data on shale gas resource potentialy g p Cost of production is such high that market would not haveabsorbed shale gasLand access/ road access potentially an issue Government

ki t d fi h l d l t f k i l di

Infrastructure varies across basins and is not integrated

working to define shale gas development framework, includingenvironmental/water legislation and well approval process

Infrastructure varies across basins and is not integrated Gas demand varies by basin (powergen, industry, LNG)Acreage overlapping with conventional oil & gas licenses

Limited fraccing/ horizontal drilling capabilityHigh operating cost due to topography, land accessProcurement model/system may not enable efficient

Moscow, Russia | 15-19 June, 2014

Procurement model/system may not enable efficientdevelopment through adoption of the right technology

More ChallengesWATER SOURCE GAS TRANSPORT WASTE DISPOSAL

CHALLENGES •8-20 million litres water per well• Shallow aquifers, surface water and municipal water

• Multiple truck trips for frac and flow-back• Pipeline network for di t ib ti

•Water reuse,surface disposal,wastewater treatment

POLICY ISSUES

water and municipal water distribution treatment

• Water access rights & enforcement

• Land access• Road management

• Effluent disposal, setting t t t li itISSUES

OPERATIONAL

• Impact on local municipalities

gand safety statutory limits

•Optimization of frac • Optimizing transport operations

•Max water reuse•Min chemical use

Moscow, Russia | 15-19 June, 2014

OPERATIONALISSUES

psizes & water usage operations

• Training personnelMin chemical use

•Water treatment companies

The average size of a multi-well pad for the drilling and fracturing phase of operations is3 5 ( 0 014 k ²) L b f ll i d t l it h l l

The weakest link

3.5 acres (=0.014 km²). Large numbers of wells are required to exploit a shale gas play.An average well density of 1.15 wells per km² was calculated for the overall BarnettShale play but regionally there may be up to ~6 wells per km². Total capex investment of>US$ 1 9 trillion over next 25 years whereas Indian and China are not investing that big>US$ 1.9 trillion over next 25 years whereas Indian and China are not investing that big.Current capex of US$33bn equals total China upstream expenditure. Transparentlicensing arrangements and clear established fiscal structure exist in US unlike India.

Population density (per sq Km)

The percentage of arable land is almost 49% inf

Population density (per sq. Km)India - 370 > China - 139.6 > USA - 33.7

India, meaning disruption of communities andagriculture activities can result in severe resistanceto shale gas operations from locals. It also meansthe water resources will not be generously

Moscow, Russia | 15-19 June, 2014

the water resources will not be generouslyavailable.

Environmental ConcernsIndia’s nascent shale-gas industry faces major challengesto its growth in the form of environmental concerns which

Freshwater availability (per capita)(in m3)to its growth in the form of environmental concerns which

have surrounded the shale-gas drilling process globally. InEurope, environmental considerations have led manynations in the EU to place a moratorium on domestic

(in m )

nations in the EU to place a moratorium on domesticdrilling for shale-gas, even as they continue to importnatural gas from other sources. The global debate centerson a host of issues that include the contamination of wateraquifers, disposal of hazardous drilling fluids, theinstigation of earthquakes and strain on water supplies.

The vast majority of the country’s unconventional gasAverage Indian’s entitlement toSource: World Bank

j y y gpotential lies in inland basins in the subcontinent’shinterland. It is evident that potential shale gasbearing areas, such as Cambay, Gondwana, and theI d G ti l i l th t ill

gfresh water has reduced by60% in last 50 years.Groundwater abstraction forI di t d t 251 k 3/

Moscow, Russia | 15-19 June, 2014

Indo-Gangetic plains are also areas that willexperience severe water stress by 2025.

India stands at 251 km3/year,highest in the world.

SWOT Analysis – Indian shale gas: summary

SS WWSTRENGTHSSTRENGTHS WEAKNESSES

• Lack of key technologies• High capital expenditure

• Cleaner fuel• Great development potential

SS WW WEAKNESSES

High capital expenditure• Serious environmental risks• Water treatment problems

• Great development potential• Abundant resource reserves• Long life for exploitation

H d ti d d I f t li t

TTOO OPPORTUNITIESOPPORTUNITIES THREATSTHREATS

• Huge domestic demand• Policy support• International support• Foreign forays by Indian companies

• Imperfect policy system• Unconfirmed resource potential• Under-developed infrastructure

like pipeline network

Moscow, Russia | 15-19 June, 2014

• Foreign forays by Indian companies like pipeline network• Land and water availablity for use

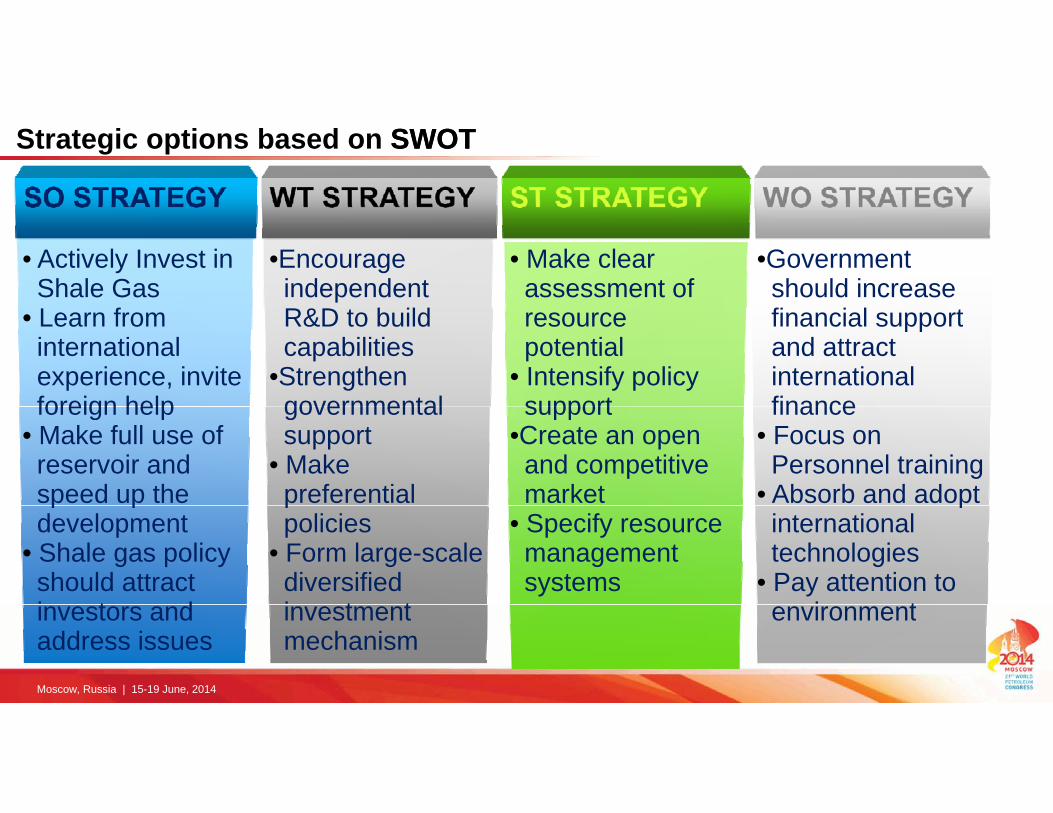

Strategic options based on SWOTSWOT

•Governmentshould increasefi i l t

• Actively Invest in Shale GasL f

• Make clear assessment of

•EncourageindependentR&D t b ild financial support

and attractinternationalfinance

• Learn frominternationalexperience, inviteforeign help

resource potential

• Intensify policysupport

R&D to buildcapabilities

•Strengthengovernmental finance

• Focus onPersonnel training

• Absorb and adopt

foreign help• Make full use ofreservoir andspeed up the

support•Create an openand competitivemarket

governmentalsupport

• Makepreferential p

internationaltechnologies

• Pay attention toi t

p pdevelopment

• Shale gas policyshould attracti t d

• Specify resourcemanagementsystems

ppolicies

• Form large-scalediversifiedi t t environmentinvestors and

address issuesinvestmentmechanism

Moscow, Russia | 15-19 June, 2014

Policy frameworkIn line with the policy of the Government of India attracting private investment to movetowards self reliance in the indigenous production of oil and gas sector it is important totowards self reliance in the indigenous production of oil and gas sector, it is important tohave a framework to facilitate and regulate Shale Oil and Gas Exploration andExploitation. Following are the important features mentioned in proposed policy:The offer of acreages under this policy would be made through an open InternationalThe offer of acreages under this policy would be made through an open InternationalCompetitive Bidding (ICB) process.All data gathered during the course of operation shall be the property of the GOI.Safety aspects will be regulated as per existing regulations / OISD guidelines andpracticesMinistry of Environment and Forest (MOEF) will prescribed a panel of agencies,competent to carry out the Environment Impact Assessment for the blocks allotted.Govt of India will ensure all statutory regulatory and security clearances are obtainedGovt. of India will ensure all statutory, regulatory and security clearances are obtainedbefore bidding.Exploration of Shale oil / gas will be accordance with the law of the land, including theWater (prevention and control of pollution) act, 1974, Air (prevention and control of

Moscow, Russia | 15-19 June, 2014

Water (prevention and control of pollution) act, 1974, Air (prevention and control ofpollution) act, 1981 and the overall ambit of environment protection measures.

Policy and regulatory reforms• Allocation of Resources: The process will be complicated by the fact that shale-

gas often occurs in the same surface environments as coal-bed methane (CBM)gas often occurs in the same surface environments as coal bed methane (CBM)resources, which are auctioned per the block system by the Directorate General ofHydrocarbons (DGH). The government will have to reconcile regulations on tworesources, and streamline access to each block with the minimum room for conflict.D l i ti f P i A lti l t h t d d l i ti f• De-regularization of Prices: As multiple experts have noted, de-regularization ofprices will also be a critical step in unfettering the growth potential of India’sdomestic gas industry. Currently India has over 27 pricing regimes for gas,organized on the basis of industry, and in nearly all cases, heavily subsidized.

• Land Acquisition: As drilling operations eventually move onshore, the acquisitionis likely to become a contentious issue and pose a major challenge to developmentof inland shale gas resources. The central government will need to devisetransparent regulations that assure adequate and fair compensation at market

• Acquisition of technology: The acquisition of advanced exploration as wellextractive technologies should be the foremost priority. Exploration is key forid tif i dditi l tl l ll f ti f I di ’ t ti l

transparent regulations that assure adequate and fair compensation at marketprices and resettlement of any displaced persons.

Moscow, Russia | 15-19 June, 2014

identifying additional resources, as currently only a small fraction of India’s potentialresource base has been explored.

1 Strengthen the support for technology R&D in shale gas

The road ahead

R&D support policy

1. Strengthen the support for technology R&D in shale gasexploration and development

2. Establish a national R&D (experimental) center of ShaleGaspolicy Gas

3. Encourage domestic enterprises and institutions to carry outjoint research of key technologies of exploration

International Enterprises can cooperate with foreign experiencedInternational Cooperation policy

Enterprises can cooperate with foreign experiencedcorporations and introduce relevant technologies

Land policy Shale gas will receive priority of land examination and approval.

Fiscal Policy1. Financial subsidies2. Tax exemption3 For the imported equipment which cannot be produced at3. For the imported equipment which cannot be produced at

home can be exempted from tariffs.

Moscow, Russia | 15-19 June, 2014

In the end…..Immense challenges lie ahead for India on energy security. These include theimmediate need to bridge the energy deficit and the longer term issue of securingimmediate need to bridge the energy deficit and the longer-term issue of securingthe country’s energy future in the light of a growing population and economy.

India will need to fast track several initiatives, both at home and abroad. Thesei l d i i i f l i d d illi h l f d iinclude: acquisition of exploration and drilling technology for domestic resources,development of gas transportation infrastructure, negotiation of access to additionalU.S. shale gas resources and export terminals, deregulation of domestic gas pricingand environmental regulations for the shale gas industryand environmental regulations for the shale gas industry

The unlocking of domestic shale gas can help India meet its growing energydemand, besides reducing its dependence on expensive energy imports and theenergy import bill Taking a note from the impact of shale gas development in theenergy import bill. Taking a note from the impact of shale gas development in theUS, the development of the sector can help increase economic activity in thecountry, thereby boosting government revenues and creating new jobs. Additionalgas supplies can also spur investments in associated downstream segments, which

Moscow, Russia | 15-19 June, 2014

gas supplies can also spur investments in associated downstream segments, whichcater to significant latent gas demand in the country.

Saurabh AgarwalaSenior EngineerEngineers India Limited IndiaEngineers India Limited, India

Author BiographyPhoto

Saurabh Agarwala is a Chemical Engineer, graduated from Meerut Universityand completed M.S. in Chemical Engineering from Washington University in St.Louis, US. He joined Research and Development division of Engineers IndiaLimited, New Delhi in 2007 and is presently serving as Sr. Engineer.

Presently involved in technology development and implementation of LPGtreatment units Exploring sun rise areas in energy sector is also a field oftreatment units. Exploring sun-rise areas in energy sector is also a field ofinterest. Previous work experience as Operation engineer in a gas crackerplant.

Moscow, Russia | 15-19 June, 2014