sgp presentation 4q11 -...

TRANSCRIPT

Siamgas and Petrochemicals PLC

“Toward a New Horizon”

Presentationfor investor & analyst4Q’11 and 2011

2Disclaimer

• The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in Siamgasand Petrochemicals Public Company Limited (“SGP” and shares in SGP, “shares”) in any jurisdiction or should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever.

• This presentation may include information which is forward‐looking in nature. Forward‐looking information involve known and unknown risks, uncertainties and other factors which may impact on the actual outcomes, including economic conditions in the markets in which SGP operates and general achievement of SGP business forecasts, which will cause the actual results, performance or achievements of SGP to differ, perhaps materially, from the results, performance or achievements expressed or implied in this presentation.

• This presentation has been prepared by the SGP. The information in this presentation has not been independently verified. No presentation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the SGP or any of its agents or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of the presentation or its contents or otherwise arising in connection with this presentation.

• This presentation is made, furnished and distributed for information purposes only. No part of this presentation shall be relied upon directly or indirectly for any investment decision‐making or for any other purposes.

• This presentation and all other information, materials or documents provided in connection therewith, shall not, either in whole or in part, be reproduced, redistributed or made available to any other person, save in strict compliance with all applicable laws.

3Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

4Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

5New perspective on SGP for 2011 onward

• Previously, relied only on stable Thailand domestic business– Controlled price (U$ 333/ton), moderate competition, stable but limited growth

• Changing perspectives on SGP after expansion to oversea markets:– Opportunities for unlimited growth

– Trading with LPG world price (CP Saudi Aramco U$700‐900/ton) • Changing price on monthly basis

• Seasonal pricing trend is normally in line with climate condition

• Annual cycle of business operation gives a clearer picture of SGP’s oversea operation performance

• Significant price movement may imply change in financial figures

• Profit margin relies on price moving trend, and inventory balance

– Financial cost is probably high at the beginning of expansion projects

– Foreign exchange has some effect on booking transaction in financial statement.

6Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

7Current areas of SGP’s operations

THAILAND

VIETNAM

SINGAPORE

ZHUHAI

SHANTOU

SUPER GAS

SINGGAS

SGP, UNIQUE GAS, LOGISTICS, ETC

SINO SIAM GAS AND PETROCHEMICALS

SIAM OCEAN GAS AND ENERGY

BATAM

8

Siamgas and Petrochemicals PCLThailandLPG Offshore Trading BusinessUtilizing mega size storage and facilities of subsidiaries in China i.e. SINO SIAM, and SOGEL in importingand re‐exporting LPG to other traders and subsidiaries in the regionSGP currently utilizes VLGC as floating terminal in Batam (Indonesia) to enhance competitive advantage in SEA

LPG Business

Acquired from Chevron (Jun’11)

LPG Terminal (Bulk‐Breaking)

Storage. Cap 100,000 tons

(Underground Storage Caverns)

LPG Business

Acquired from BP (Dec’10)

LPG Terminal (Bulk‐Breaking)

LPG Filling Plant

LPG Retail Outlets

Storage. Cap 200,000 tons

(Underground Storage Caverns)

LPG Business

Acquired from Shell Gas (LPG), Jul’10

LPG Filling Plant

Storage. Cap 75 tons

LPG Business

(Acquired from Chinese owner), Mar’10

LPG Terminal & Filling Plant

Storage. Cap 2,000 tons

Siam Ocean Gas& EnergyLtdShantou, China

Sino Siam Gas &PetrochemicalsCo LtdZhuhai, China

SingGas (LPG)Pte Ltd

Singapore

Super GasCo Ltd

Vietnam

Oversea Business Operations

9South East Asia Re-Export Markets

Zhuhai Terminal

ShantouTerminal

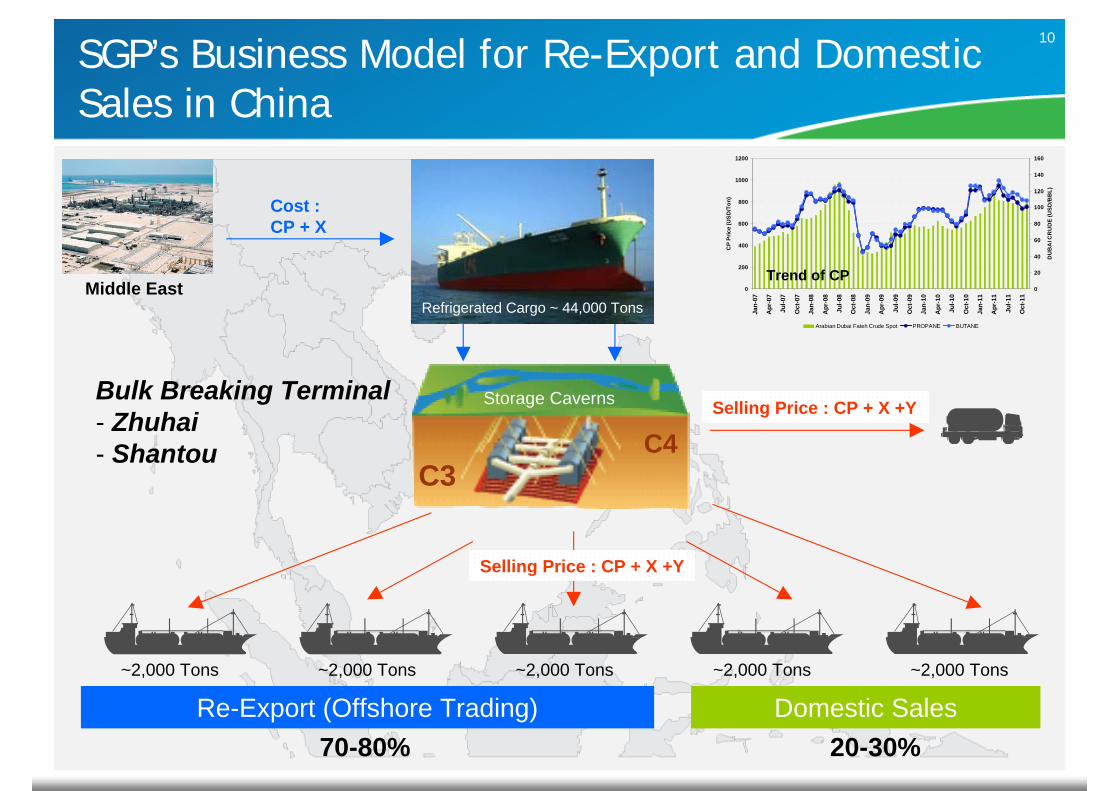

10SGP’s Business Model for Re-Export and Domestic Sales in China

Bulk Breaking Terminal- Zhuhai- Shantou

C3C4

~2,000 Tons ~2,000 Tons ~2,000 Tons ~2,000 Tons~2,000 Tons

Re-Export (Offshore Trading) Domestic Sales

Cost :CP + X

Selling Price : CP + X +Y

Selling Price : CP + X +Y

70-80% 20-30%

Storage Caverns

Middle EastRefrigerated Cargo ~ 44,000 Tons

0

200

400

600

800

1000

1200

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

CP

Pric

e (U

SD

/Ton

)

0

20

40

60

80

100

120

140

160

DU

BA

I CR

UD

E (U

SD/B

BL)

Arabian Dubai Fateh Crude Spot PROPANE BUTANE

Trend of CP

11

z

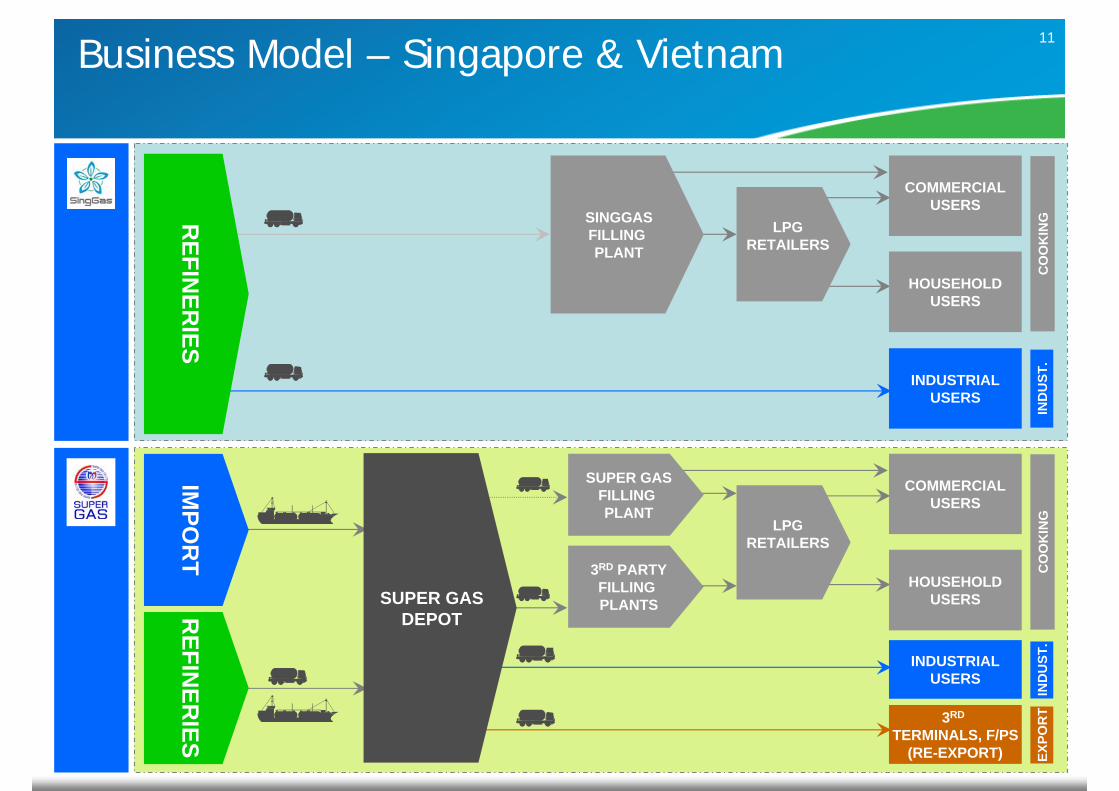

Business Model – Singapore & Vietnam

SINGGASFILLING PLANT

LPGRETAILERS

HOUSEHOLDUSERS

COMMERCIALUSERS

INDUSTRIALUSERS

CO

OK

ING

IND

UST

.

REFIN

ERIES

SUPER GASFILLING PLANT

LPGRETAILERS

HOUSEHOLDUSERS

COMMERCIALUSERS

INDUSTRIALUSERS

CO

OK

ING

IND

UST

.

IMPO

RT

3RD PARTYFILLING PLANTS

3RD

TERMINALS, F/PS(RE-EXPORT) EX

POR

T

REFIN

ERIES

SUPER GASDEPOT

12

RESIDENTIAL

COMMERCIAL

INDUSTRIAL

AUTOMOTIVE

3RD PARTYFILLINGPLANTS

COMPANYFILLING PLANT

SHOPS

3RD PARTYTERMINALS

S.CHINA

DOMESTIC

SGP’sOVERSEA

SUBSIDIARIES

SINGAPOREVIETNAM…………

SOUTHEASTASIA

RE-EXPORT

MID

DLE EA

ST

SGP’s

BU

LK B

REA

KIN

G TER

MIN

AL

IN

SOU

TH C

HIN

A

VLGCRefrigerated LPG(Propane, Butane)

CavernStorage

LOC

AL

REFIN

ERIES Sphere Tanks

Pressurized

Pressurized LPG(Mixed)

Business Model – Zhuhai, South China

TRADERS/3RD PARTY

TERMINALS INTHE REGION

SSGPSSGP

13

MID

DLE EA

ST

VLGCRefrigerated

Business Model – Shantou, South China

TRADERS/3rd PARTY TERMINALS

IN THE REGION

RE-EXPORT

INDUSTRIAL

COMMERCIAL

RESIDENTIAL3RD PARTY

FILLINGPLANTS

3RD PARTYTERMINALS

S.CHINA

SOGEL

DOMESTIC

SGP’s

BU

LK B

REA

KIN

G TER

MIN

AL

IN

SOU

TH C

HIN

A

CavernStorage

Refrigerated

14Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

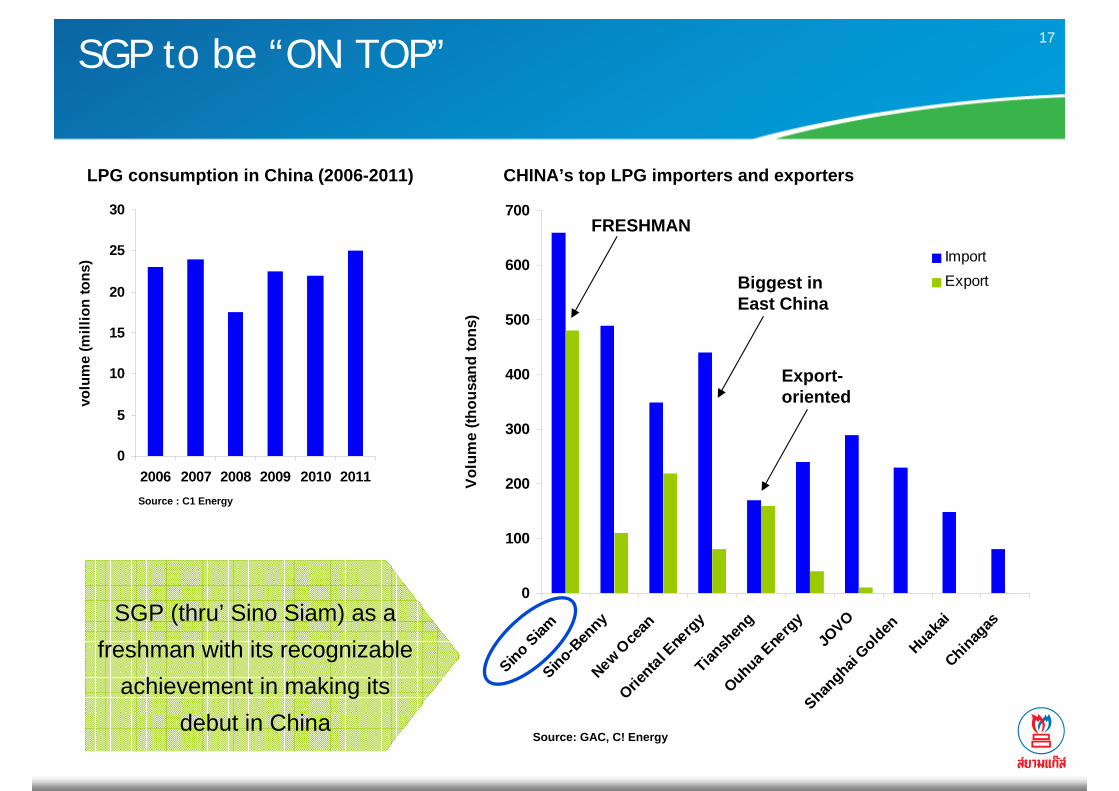

15Oversea LPG Market Highlights

• Global LPG consumption growth tends to continue – Petchem plays a key role driving growth

• LPG world price volatility

– March 2011 Libya turmoil cast shadow : triggered LPG price hike with 2011 historical high in May.

– Declining trend after hike up in May 2011

– Tended to climb up from July going on August 2011, but shifted downward due to concern on European

debt Around mid August 2011

– Colder climate in 4Q’11 gradually drove up LPG price

• SGP’s minor stock loss from Offshore Trading due to QoQ LPG price decrease

• Business operations of SOGEL commercially started in quarter December 2011

• Increasing offshore trading sales volume in 4Q’11 with higher demand and additional

customers/channels

• SGP, thru’ SINO SIAM was recognized as top importer in China

16

Grow

th indications from traders &

major exporters

Room to grow in the growing global market

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012 2013 2014 2015

Mill

ion

Tons

0

5

10

15

20

25

30

35

40

2010 2011 2012 2015

Mill

ion

Tons

World Propane & Butane Trade Outlook

Source : Poten & Partner

Middle East Export O/L (2010-2015)

Source : Poten & Partner

LPG consumption in the world (2010)

Source: Compiled by the Agency for Natural ResourcesFrom data released by the World LP Gas Association (WLPG)

* Total 2010 consumption : 246 million tons* LPG consumption including Petchem

71.56

4.31

5.44

5.99

7.01

9.06

9.16

10.20

12.91

13.25

16.27

25.12

55.92

- 20 40 60 80

Others

Egypt

Thailand

Canada

Brazil

Mexico

South Korea

Russia

Saudi Arabia

India

Japan

China

USA

volume (million tons)

17

0

100

200

300

400

500

600

700

Sino Siam

Sino-Ben

nyNew O

cean

Oriental E

nerg

yTian

shen

gOuhua E

nerg

y

JOVO

Shanghai

GoldenHuaka

iChinag

as

Volu

me

(thou

sand

tons

)

ImportExport

SGP to be “ON TOP”

0

5

10

15

20

25

30

2006 2007 2008 2009 2010 2011

volu

me

(mill

ion

tons

)

Source: GAC, C! Energy

LPG consumption in China (2006-2011)

Source : C1 Energy

CHINA’s top LPG importers and exporters

SGP (thru’ Sino Siam) as a freshman with its recognizable

achievement in making its debut in China

FRESHMAN

Biggest inEast China

Export-oriented

18

-

200

400

600

800

1,000

1,200

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

2007 2008 2009 2010 2011 2012

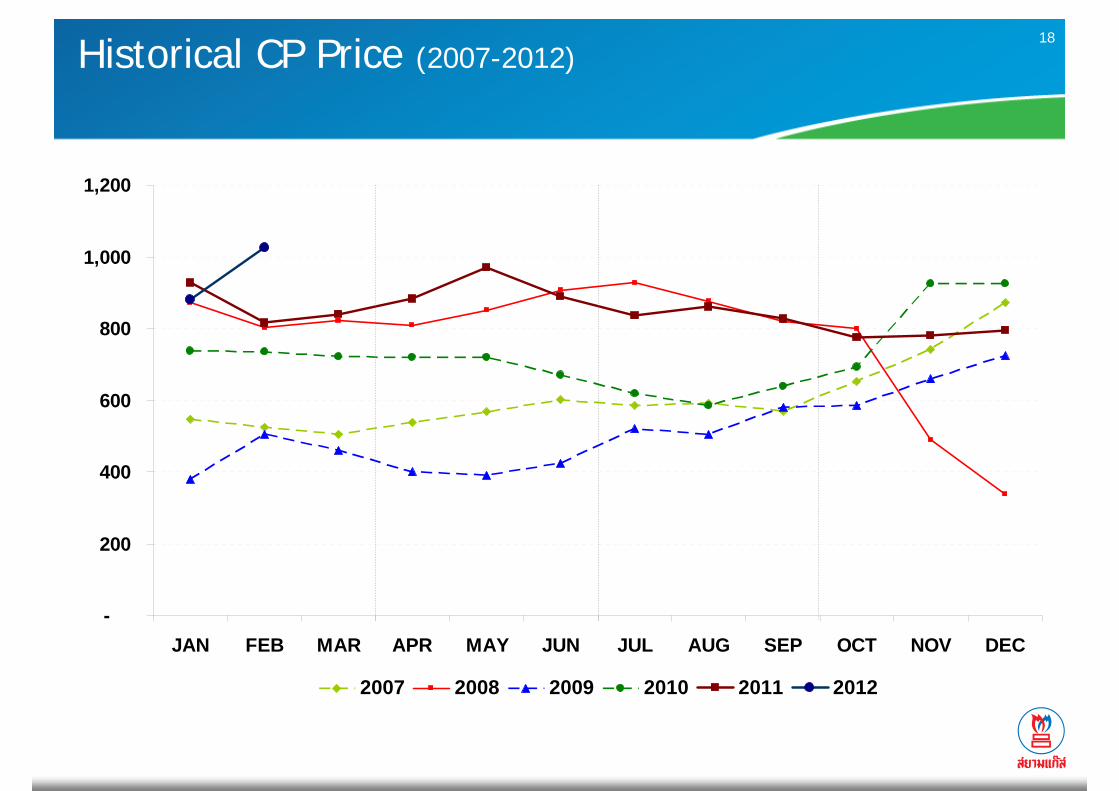

Historical CP Price (2007-2012)

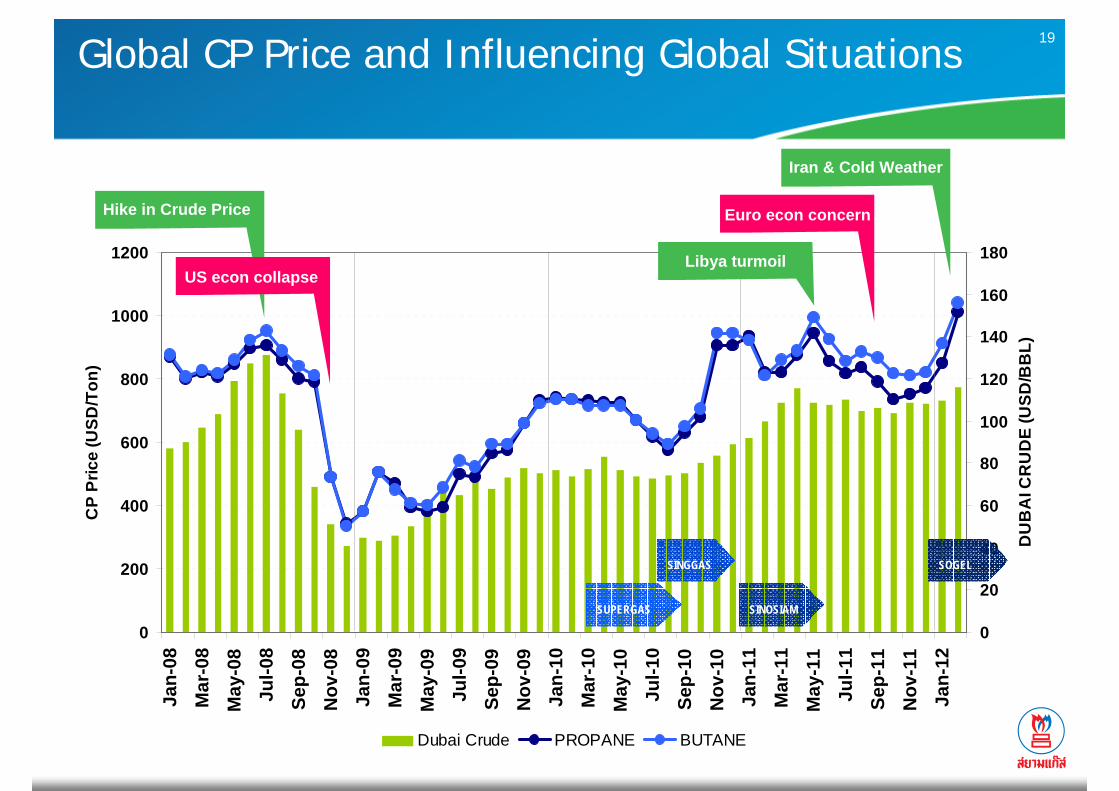

19Global CP Price and Influencing Global Situations

0

200

400

600

800

1000

1200

Jan-

08M

ar-0

8M

ay-0

8Ju

l-08

Sep-

08N

ov-0

8Ja

n-09

Mar

-09

May

-09

Jul-0

9Se

p-09

Nov

-09

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep-

10N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1Se

p-11

Nov

-11

Jan-

12

CP

Pric

e (U

SD/T

on)

0

20

40

60

80

100

120

140

160

180

DU

BA

I CR

UD

E (U

SD/B

BL)

Dubai Crude PROPANE BUTANE

Libya turmoil

Euro econ concern

Iran & Cold Weather

Hike in Crude Price

US econ collapse

SUPERGAS

SINGGAS

SINOSIAM

SOGEL

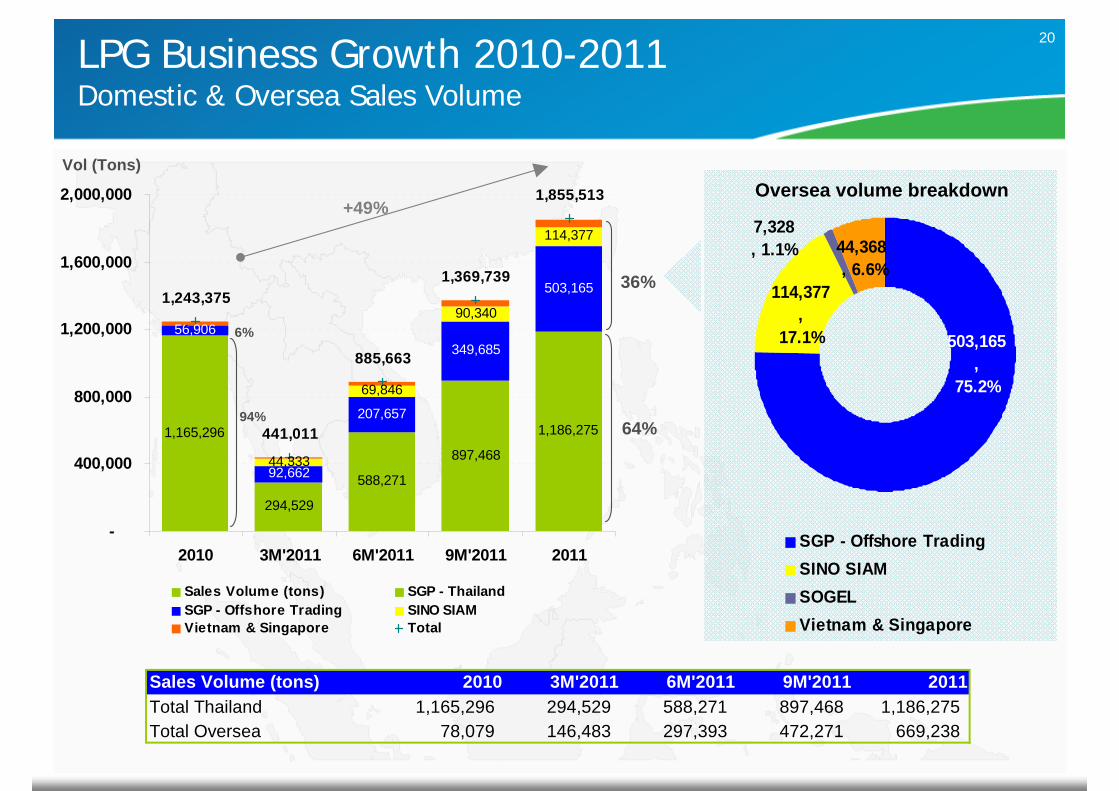

20

1,165,296

294,529

588,271

897,468

1,186,275

56,906

92,662

207,657

349,685

503,165

-

44,333

69,846

90,340

114,377

1,243,375

441,011

885,663

1,369,739

1,855,513

-

400,000

800,000

1,200,000

1,600,000

2,000,000

2010 3M'2011 6M'2011 9M'2011 2011

Sales Volume (tons) SGP - ThailandSGP - Offshore Trading SINO SIAMVietnam & Singapore Total

503,165

, 75.2%

114,377

, 17.1%

44,368 , 6.6%

7,328 , 1.1%

SGP - Offshore TradingSINO SIAMSOGELVietnam & Singapore

LPG Business Growth 2010-2011Domestic & Oversea Sales Volume

+49%

Vol (Tons)Oversea volume breakdown

36%

64%

6%

94%

Sales Volume (tons) 2010 3M'2011 6M'2011 9M'2011 2011Total Thailand 1,165,296 294,529 588,271 897,468 1,186,275 Total Oversea 78,079 146,483 297,393 472,271 669,238

21Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

22Business Model - Thailand

REFIN

ERIES

&

GA

S SEPAR

ATIO

N PLA

NTS

SGP TERMINALS

&DEPOTS

SGP FILLING PLANTS

AGENT FILLING PLANTS

LPGRETAILERS

SGP AUTO-LPGSTATIONS

AGENT AUTO-LPGSTATIONS

MOTORISTS

HOUSEHOLDUSERS

COMMERCIALUSERS

INDUSTRIALUSERS

CO

OK

ING

AU

TOM

OTI

VEIN

DU

ST.

23Thailand LPG Market Highlights

• Economic slow down due to flood which had impact on LPG demand in inundated

areas started in late quarter 3 till quarter 4

• Competition in automotive segment was still intense

• Continuous trend of gasoline price increase (THB 1/lt on average QoQ) and tend to go

on in the following quarter

• Government’s policy in lifting prices of certain energy sources

– Price adjustment for cooking was still on hold

– Government still gave signal of LPG auto‐gas and NGV price increase

• LPG price lifted (monthly) – THB 0.41/lt in Jan’12 and THB 0.41/kg in Feb’12

• NGV price lifted (monthly) – THB 0.50/kg in Jan’12 and THB 0.50/kg in Feb’12

– The government has quarterly raised LPG price for industrial usage by THB 3/kg in Jul’11 and

THB 3/kg in Oct’11, and THB 3/kg in Jan’12 – and final THB 3/kg to go in Apr’12

– LPG price for Petrochemical Feed Stock was also lifted in Jan’12

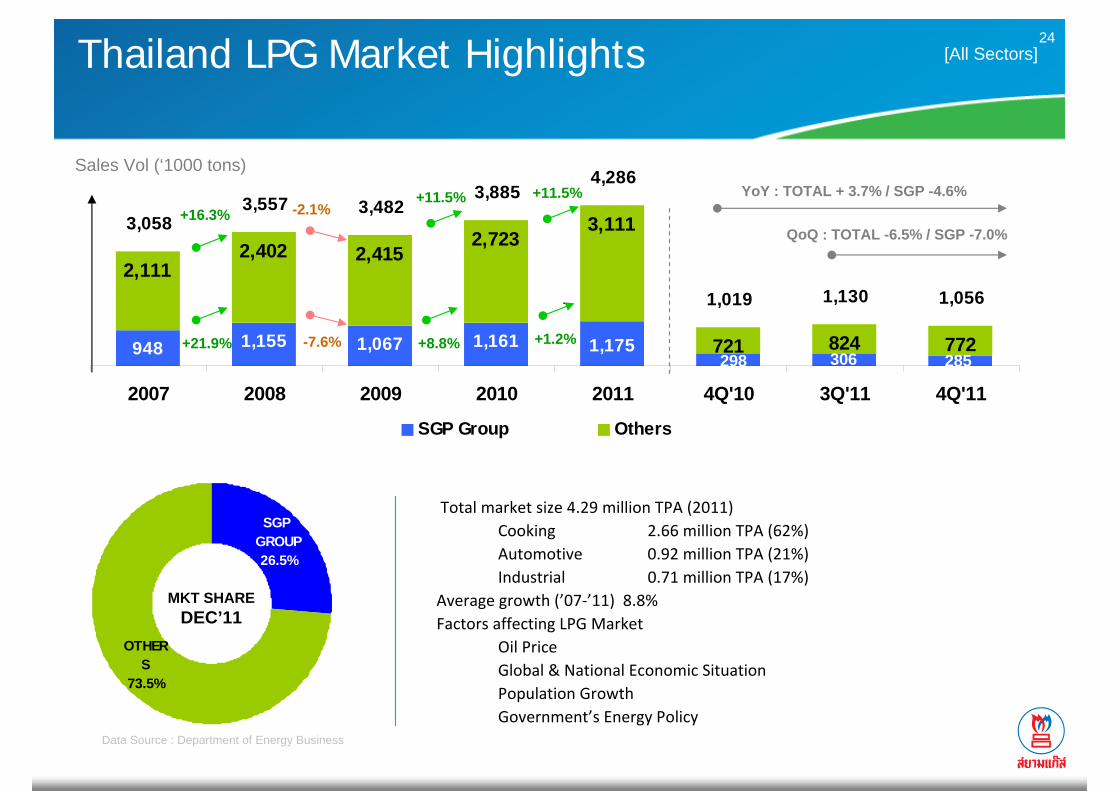

24

OTHERS

73.5%

SGP GROUP26.5%

Total market size 4.29 million TPA (2011)Cooking 2.66 million TPA (62%)Automotive 0.92 million TPA (21%)Industrial 0.71 million TPA (17%)

Average growth (’07‐’11) 8.8%Factors affecting LPG Market

Oil PriceGlobal & National Economic SituationPopulation GrowthGovernment’s Energy Policy

Thailand LPG Market Highlights

948 1,155 1,067 1,161

2,1112,402 2,415

2,7233,111

721 824 772285306298

1,175

1,019 1,130 1,056

3,0583,557 3,482

3,8854,286

2007 2008 2009 2010 2011 4Q'10 3Q'11 4Q'11

SGP Group Others

z

[All Sectors]

MKT SHAREDEC’11

Data Source : Department of Energy Business

Sales Vol (‘1000 tons)YoY : TOTAL + 3.7% / SGP -4.6%

QoQ : TOTAL -6.5% / SGP -7.0%

+8.8%-7.6%+21.9%

+11.5%-2.1%+16.3%

+1.2%

+11.5%

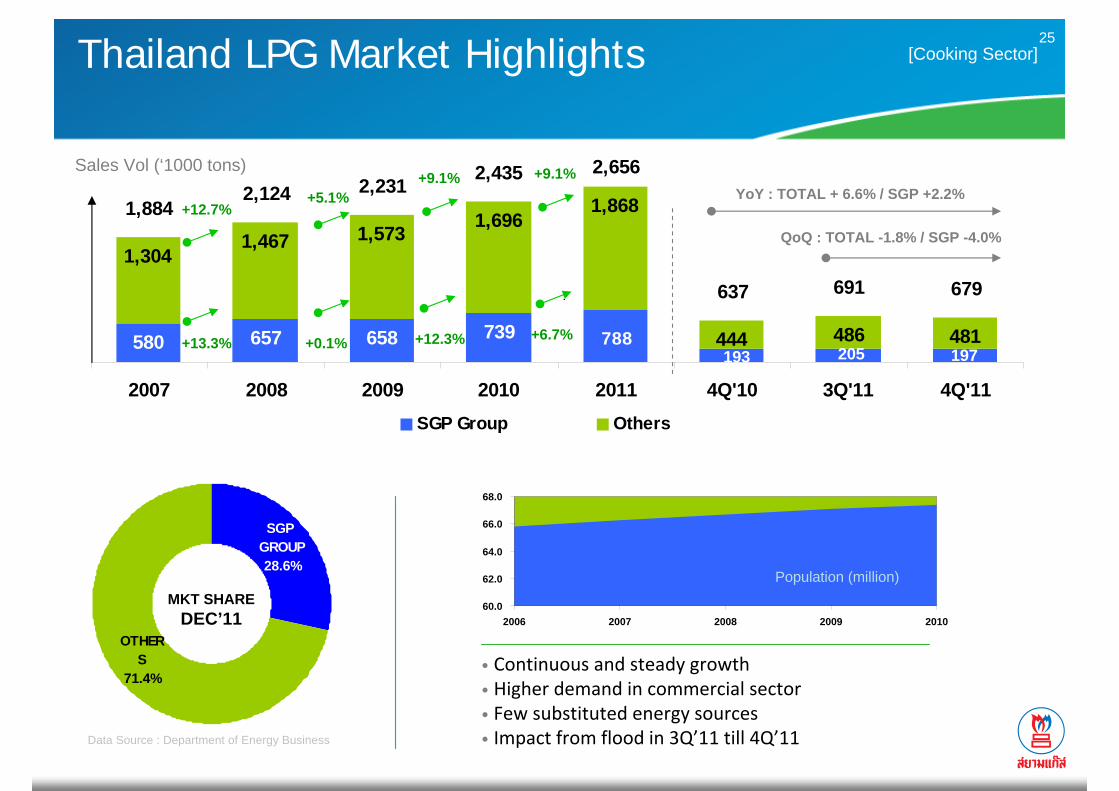

25

OTHERS

71.4%

SGP GROUP28.6%

580 657 658 739

1,3041,467 1,573 1,696

1,868

444 486 481197193 205

788

637 691 679

2,6562,4352,2312,1241,884

2007 2008 2009 2010 2011 4Q'10 3Q'11 4Q'11SGP Group Others

z

Thailand LPG Market Highlights [Cooking Sector]

MKT SHAREDEC’11

• Continuous and steady growth • Higher demand in commercial sector• Few substituted energy sources• Impact from flood in 3Q’11 till 4Q’11

60.0

62.0

64.0

66.0

68.0

2006 2007 2008 2009 2010

Population (million)

Sales Vol (‘1000 tons)

Data Source : Department of Energy Business

+12.3%+0.1%+13.3%

+9.1%+5.1%

+12.7%YoY : TOTAL + 6.6% / SGP +2.2%

QoQ : TOTAL -1.8% / SGP -4.0%

+6.7%

+9.1%

26

ENERGY UNIT RETAIL PRICE

CONS. KM/LT

COST THB/KM

NGV (Lifted THB 1.0/kg) THB/KG 9.50 10.69 0.89 LPG (Lifted THB 0.82/lt) THB/LT 12.12 7.41 1.64 LPG WORLD PRICE THB/LT 23.41 7.41 3.16 E85 THB/LT 23.68 6.13 3.86 GASOHOL 91 (E10) THB/LT 37.88 7.91 4.79 GASOHOL 95 (E10) THB/LT 39.63 7.91 5.01 UGR 91 THB/LT 40.91 8.76 4.67 ULG 95 THB/LT 45.26 8.76 5.17 NGV (After adj THB +6 /kg) THB/KG 14.50 10.69 1.36 LPG (After adj THB +5.75 /lt) THB/LT 17.05 7.41 2.30 LPG WORLD PRICE USD/TON 1,205.00 Mar-12FX THB/USD 30.50 Mar-12

266389

320 306

306

386346 374

193 170627275

277

644

110

185265 232

572

776666 680

920

2007 2008 2009 2010 2011 4Q'10 3Q'11 4Q'11

SGP Group Others

z

OTHERS

74.6%

SGP GROUP25.4%

Thailand LPG Market Highlights [Automotive Sector]

MKT SHAREDEC’11

Sales Vol (‘1000 tons)

• Rising oil price – growing LPG consumption• Competition was still intense.Data Source : Department of Energy Business

-4.4%-17.8%

+46.2%

+2.1%-14.1%+35.6%

-9.5%

+35.3%YoY : TOTAL + 25.3% / SGP -17.5%

QoQ : TOTAL -12.4% / SGP -13.6%

27

101 109 90 117 110

501 548 496

652 599

167 1452930 25121

198 174 146

602 658 585

769 709

2007 2008 2009 2010 2011 4Q'10 3Q'11 4Q'11

SGP Group Others

z

OTHERS

82.0%

SGP GROUP18.0%

Thailand LPG Market Highlights [Industrial Sector]

MKT SHAREDEC’11

Sales Vol (‘1000 tons)

• Price for indust’ usage has been lifted by THB 9/kg as of Mar’11 •Advantages of LPG (e.g.cleaner, lower R&M maintenance) are stillmajor factors affecting growth in spite of price shifted

• Expected continual growth of manufacturing sector • Minor impact on company’s sales from flood in 4Q’11Data Source : Department of Energy Business

+30.4%-18.1%+7.8%

+31.5%

-11.0%+9.3%

-5.5%

-7.8%YoY : TOTAL -26.1% / SGP -16.0%

QoQ : TOTAL -16.0% / SGP -12.7%

ENERGY UNIT PRICE (Exc.VAT)

HEATING VALUE (BTU)

PRICE/ Mil BTU

COAL THB/KG 2.70 23,003 117.38 NG THB/Mil BTU 340.00 1,000,000 340.00 LPG (Lifted by THB 9/kg) THB/KG 26.12 47,300 552.22 FUELOIL THB/LT 24.00 39,600 606.06 LPG WORLD PRICE THB/KG 40.18 47,300 849.52 DIESEL OIL THB/LT 31.73 36,700 864.58 LPG (After THB 12/kg lifted) THB/KG 29.12 47,300 615.64 LPG WORLD PRICE USD/TON 1,205.00 Mar-12FX THB/USD 30.50 Mar-12

28Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

29

20,163 19,445 22,000

38,096

5,6589,973 9,598

653

498

653

20,163 19,44522,653

38,594

6,312

9,973 9,598

2008 2009 2010 2011 4Q10 3Q11 4Q11

Core Revenue Gain on Business Acquisition

Financial Highlights - Revenue

REVENUEMillion Baht

-3.6%+16.5%

+70.4%

Core: YoY +69.6%

QoQ – 3.8%

YoY +52.1%

Core:+13.1%

Core:+70.4%

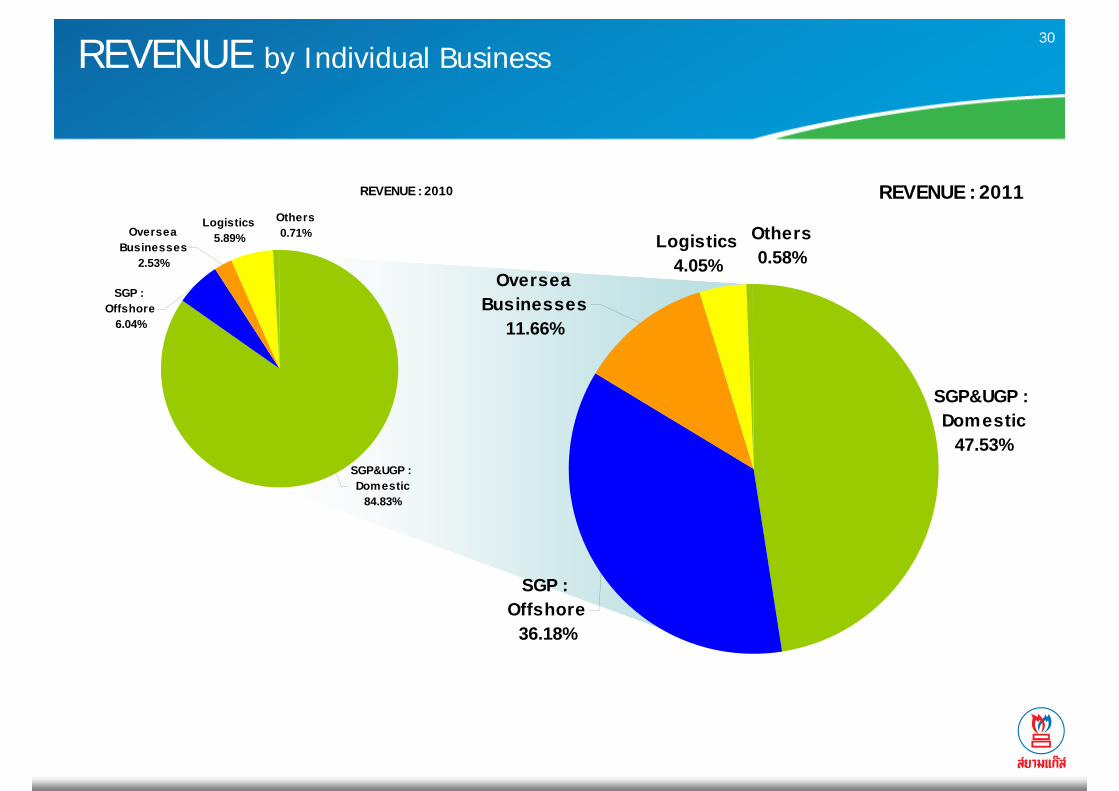

30REVENUE by Individual Business

REVENUE : 2010

SGP&UGP : Domestic

84.83%

Oversea Businesses

2.53%

Logistics5.89%

Others0.71%

SGP : Offshore

6.04%

REVENUE : 2011

SGP : Offshore

36.18%

Others0.58%

Logistics4.05%

Oversea Businesses

11.66%

SGP&UGP : Domestic

47.53%

31

1,9872,229 2,213

1,892

570297 378

653

498

653

1,9872,229

2,866

2,391

1,224

297 378

2008 2009 2010 2011 4Q10 3Q11 4Q11

Core EBITDA Gain on Business Acquisition

Financial Highlights - EBITDA

EBITDAMillion Baht

+12.2%

+28.6%-16.6%

YoY – 69.1%

QoQ +27.2%

Core: YoY – 33.7%-0.7%

-14.5%

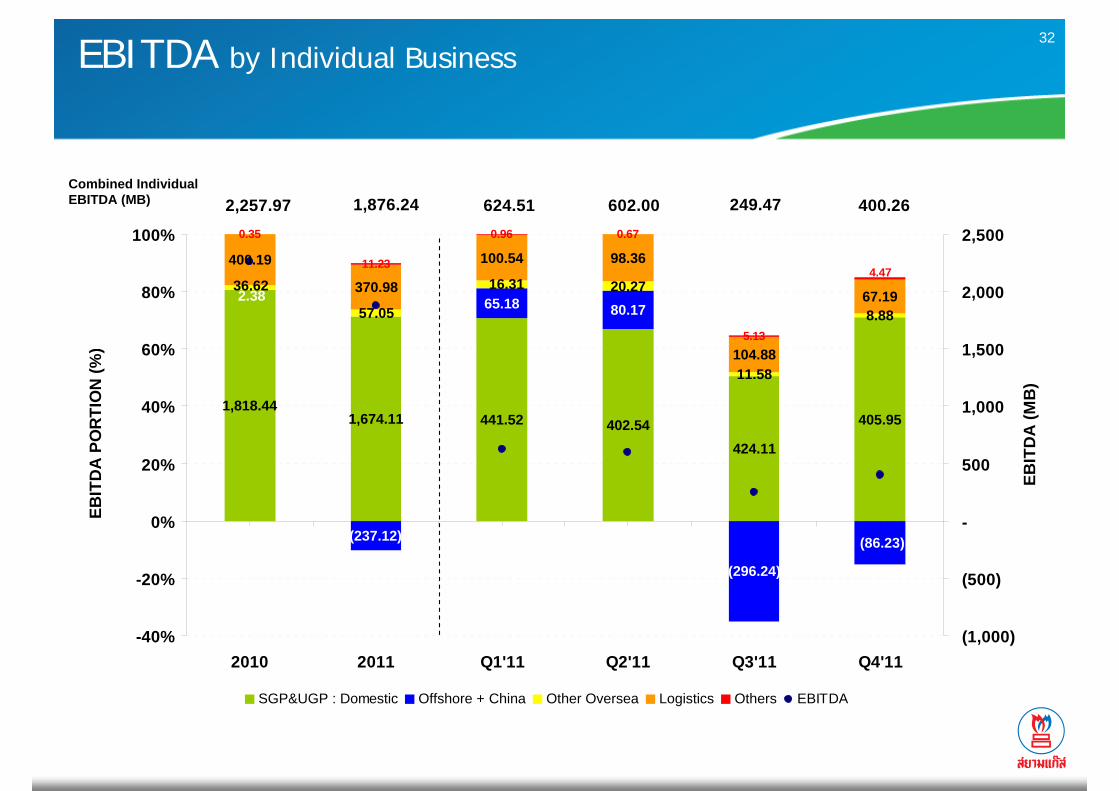

32

1,818.441,674.11 441.52 402.54

424.11

405.95

65.18 80.17

(86.23)

57.05

20.27

11.58

8.88

400.19

370.98

100.54 98.36

104.88

67.19

0.35

11.23

0.96 0.67

5.13

(296.24)

(237.12)

2.3816.3136.62

4.47

2,257.97 1,876.24 624.51 602.00 249.47 400.26

-40%

-20%

0%

20%

40%

60%

80%

100%

2010 2011 Q1'11 Q2'11 Q3'11 Q4'11

EBIT

DA

PO

RTI

ON

(%)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

EBIT

DA

(MB

)

SGP&UGP : Domestic Offshore + China Other Oversea Logistics Others EBITDA

EBITDA by Individual Business

Combined IndividualEBITDA (MB)

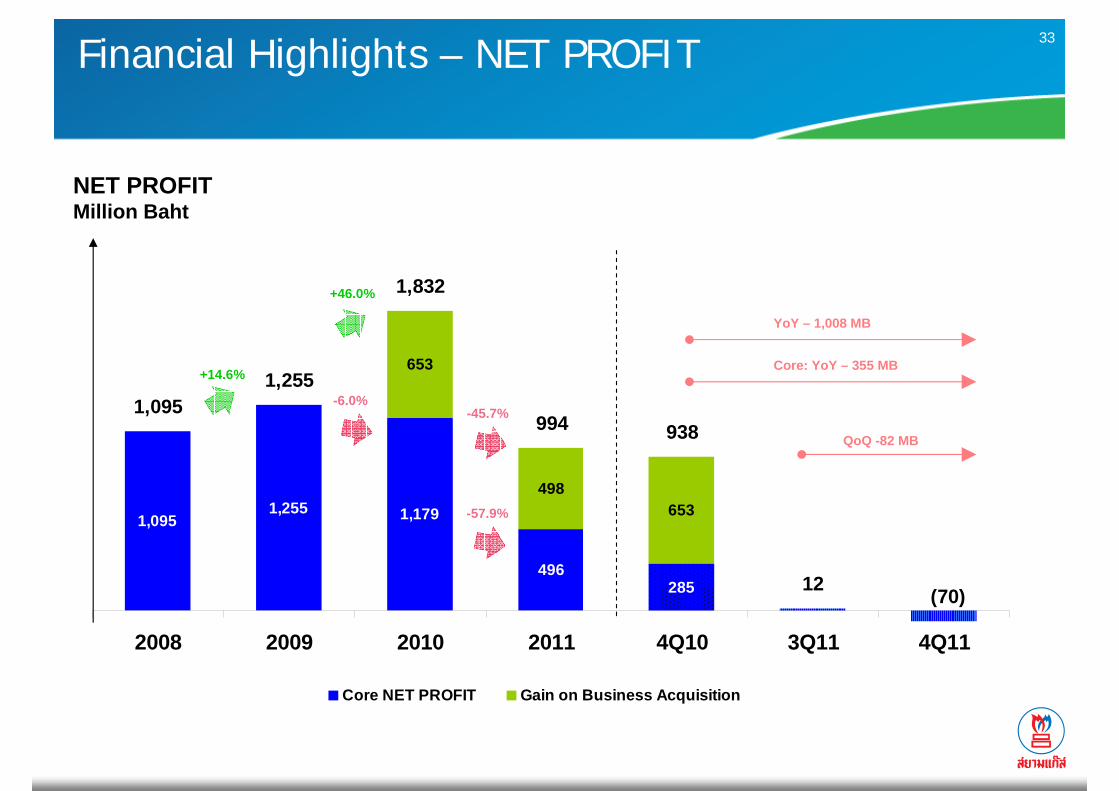

33

1,0951,255 1,179

496285

653

498653

1,0951,255

1,832

994 938

12 (70)

2008 2009 2010 2011 4Q10 3Q11 4Q11

Core NET PROFIT Gain on Business Acquisition

Financial Highlights – NET PROFIT

NET PROFITMillion Baht

+14.6%

+46.0%

-45.7%

YoY – 1,008 MB

QoQ -82 MB

Core: YoY – 355 MB

-6.0%

-57.9%

34

Changes in Depreciation

369.17 415.90 451.22

671.610.77

0.979.08

51.83

369.94416.87

460.30

723.44

-

300

600

900

2008 2009 2010 2011

Depreciation Amortization

+46.93

MB

+43.43

+263.14

Mar’10 : +Super Gas

Dec’10 : +Sino Siam

Jun’11 : +SOGEL

Nov’10 : +Vessel & VLGC

Feb’09 : +Vessel

Oct’09 : +Vessel

Jun’10 : +Vessel

Jul’10 : +SingGasMajo

r bus

iness

expa

nsion

inve

stmen

t

35

62.20 43.63 66.59

424.93

-

150

300

450

2008 2009 2010 2011

Financial Cost

Changes in Financial Costs

MB

+22.96

+358.34Mar’10 : +Super Gas

Dec’10 : +Sino Siam

Jun’11 : +SOGEL

Nov’10 : +Vessel & VLGC

Feb’09 : +Vessel

Oct’09 : +Vessel

Dec’08 : +Land

Jun’10 : +Vessel

Jul’10 : +SingGas

-18.57

Major busin

ess exp

ansion in

vestm

ent

36

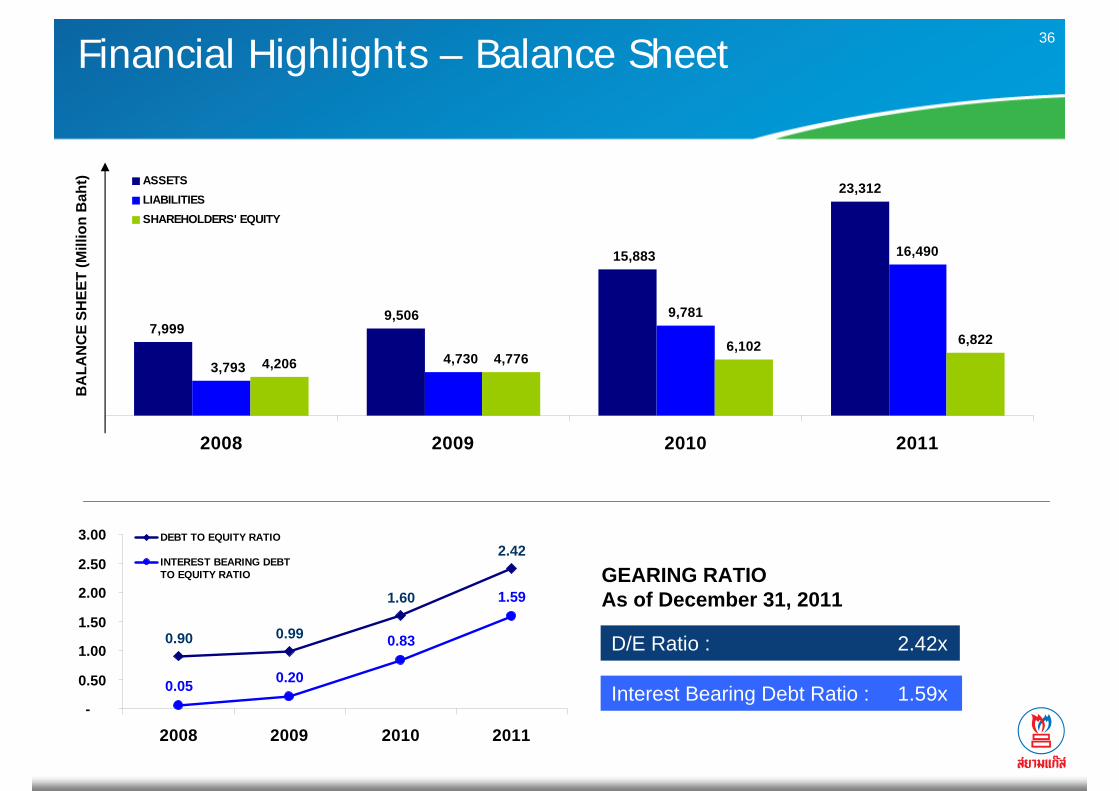

23,312

9,781

16,490

4,206 4,7766,102 6,822

15,883

9,5067,999

3,793 4,730

2008 2009 2010 2011

ASSETSLIABILITIESSHAREHOLDERS' EQUITY

Financial Highlights – Balance SheetB

ALA

NC

E SH

EET

(Mill

ion

Bah

t)

GEARING RATIOAs of December 31, 2011

D/E Ratio : 2.42x

Interest Bearing Debt Ratio : 1.59x

0.90 0.99

1.60

2.42

0.05 0.20

0.83

1.59

-

0.50

1.00

1.50

2.00

2.50

3.00

2008 2009 2010 2011

DEBT TO EQUITY RATIO

INTEREST BEARING DEBTTO EQUITY RATIO

37

• Dividend Policy– Not less than 40% of net profit after corporate income tax of the company’s

financial statement and after deduction of statutory reserve.

• Historical Dividend Payments

Dividend Payment

Interim, 0.15 Interim, 0.20 Interim, 0.20

Interim, 0.15

Final, 0.25

Final, 0.30 Final, 0.30 Final, 0.30

-

0.10

0.20

0.30

0.40

0.50

0.60

2008 2009 2010 2011

Div

iden

d (T

HB

)

38Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

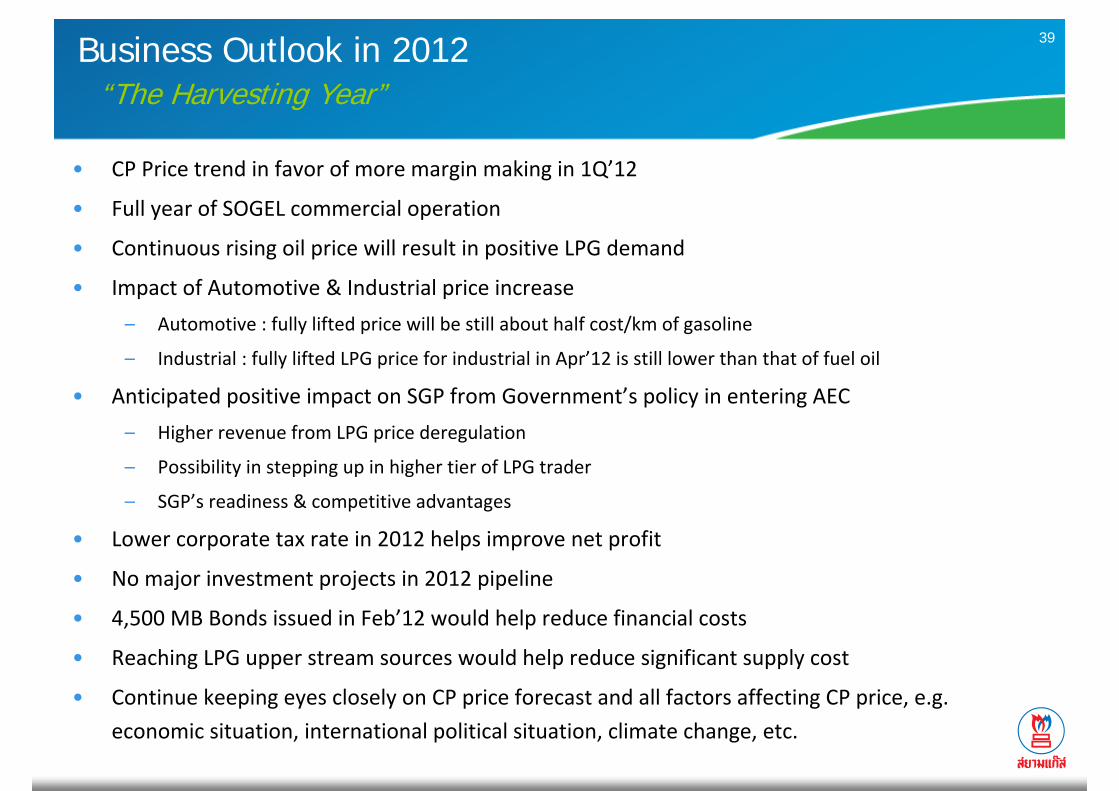

39Business Outlook in 2012“The Harvesting Year”

• CP Price trend in favor of more margin making in 1Q’12

• Full year of SOGEL commercial operation

• Continuous rising oil price will result in positive LPG demand

• Impact of Automotive & Industrial price increase

– Automotive : fully lifted price will be still about half cost/km of gasoline

– Industrial : fully lifted LPG price for industrial in Apr’12 is still lower than that of fuel oil

• Anticipated positive impact on SGP from Government’s policy in entering AEC

– Higher revenue from LPG price deregulation

– Possibility in stepping up in higher tier of LPG trader

– SGP’s readiness & competitive advantages

• Lower corporate tax rate in 2012 helps improve net profit

• No major investment projects in 2012 pipeline

• 4,500 MB Bonds issued in Feb’12 would help reduce financial costs

• Reaching LPG upper stream sources would help reduce significant supply cost

• Continue keeping eyes closely on CP price forecast and all factors affecting CP price, e.g.

economic situation, international political situation, climate change, etc.

40

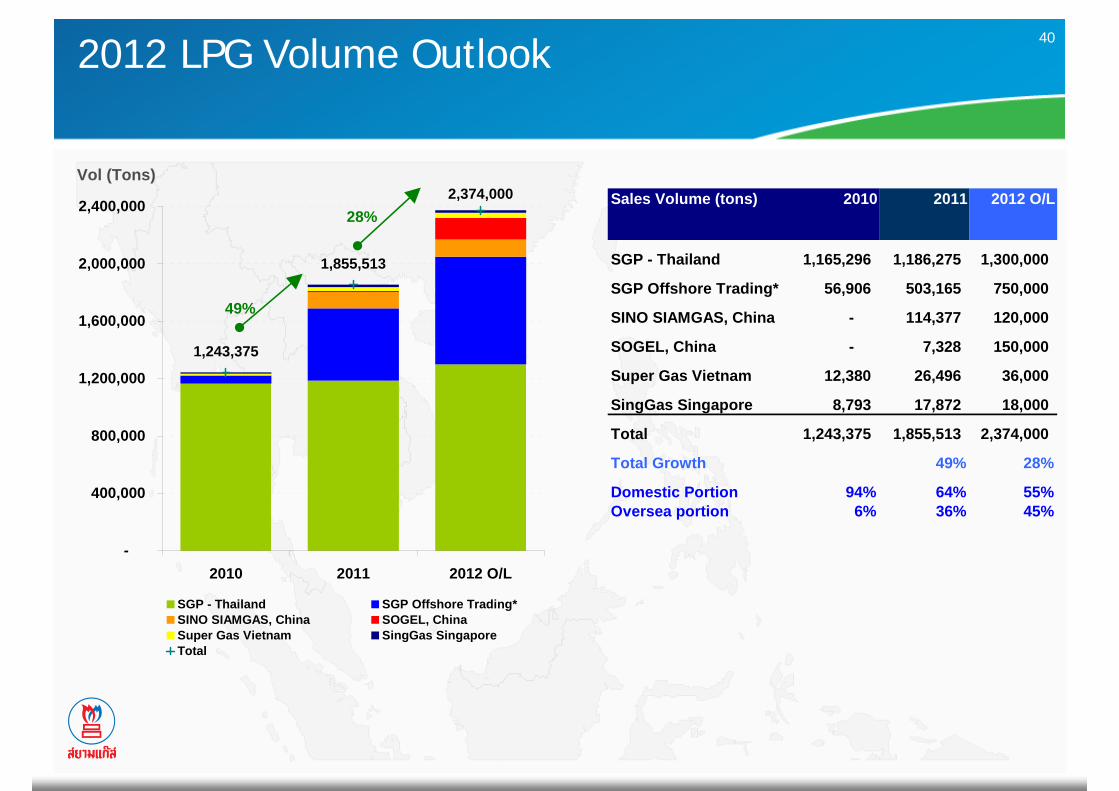

Sales Volume (tons) 2010 2011 2012 O/L

SGP - Thailand 1,165,296 1,186,275 1,300,000

SGP Offshore Trading* 56,906 503,165 750,000

SINO SIAMGAS, China - 114,377 120,000

SOGEL, China - 7,328 150,000

Super Gas Vietnam 12,380 26,496 36,000

SingGas Singapore 8,793 17,872 18,000

Total 1,243,375 1,855,513 2,374,000

Total Growth 49% 28%

Domestic Portion 94% 64% 55%Oversea portion 6% 36% 45%

1,243,375

1,855,513

2,374,000

-

400,000

800,000

1,200,000

1,600,000

2,000,000

2,400,000

2010 2011 2012 O/L

SGP - Thailand SGP Offshore Trading*SINO SIAMGAS, China SOGEL, ChinaSuper Gas Vietnam SingGas SingaporeTotal

28%

49%

2012 LPG Volume Outlook

Vol (Tons)

41Agenda

• New perspective on SGP

• Current SGP’s major businesses

• Oversea LPG Market Highlights

• Thailand LPG Market Highlights

• Financial Results

• 2012 Business Outlook

• Recent events

• Q & A

42SOGEL MOU Signing Ceremony Feb 18’12(SOGEL & Shantou Chenghai Hongsheng Petroleum Gas Co.,Ltd)

43SOGEL Grand Opening Ceremony – Mar 9’12

44

Questions are welcomedQuestions are welcomed !!

45

Investor Relations Contact

Siamgas and Petrochemicals Public Company Limited

498/997-999 Bobae Tower, Dumrongrak Road,

Klong-Mahanak, Pomprab-Satrupai, Bangkok

THAILAND 10100

Telephone : +662 628 1700-10 Ext 1589

Email : [email protected]

Website : www.siamgas.com

: www.facebook.com/siamgas