4q11 disclosure and results

TRANSCRIPT

1

Earnings Release | Conference Call – 4Q11 March 13th, 2012

2

Agenda

Ricardo Ribeiro

COO

Roberto Senna

CEO

Carlos Wollenweber

CFO | IR

4Q11 and 2011 Highlights

Operational Highlights

Financial Highlights

4Q11 2011

Launched PSV% Direcional

R$ million 428 1,447

Contracted PSV% Direcional

R$ million 367 1,230

Sales Over Supply (VSO) % PSV 31.8% 58.8%

Net Revenues R$ million 296 1,072

Adjusted Net Income² R$ million 48 199

Adjusted Net Margin² % 16.2% 18.5%

Main Figures

3

1

1

1. Considering the acquisition of 60% of the residential towers of Parque Ponta Negra project in 2Q11;

2. Adjusted by non-cash expenses (Stock-Options Program).

4

Significant growth with cash burn reduction

+37%

2011

1,072

2010

782

Net Operating Revenue

(R$ million)

Cash Burn¹

(R$ million)

2011

-38%

176

2010

283

1. Cash Burn: measured by the variation of the net debt, less capital increases, dividends and stock repurchase plan.

2011 2010 D %

Net Revenues R$ million 1,072 782 37%

Cash Burn¹ R$ million 176 283 -38%

5

“Residencial Macapaba” “Aterrado do Leme” “Residencial Meu Orgulho” – 2nd Phase

# Units

Segment

Housing PSV

Infrastructure PSV

5,384

MCMV – 1st Layer

R$ 272.6 MM

R$ 40.7 MM

Total PSV R$ 313.4 MM

Location Manaus - AM

Launch 3Q11

1,340

MCMV – 1st Layer

R$ 79.1 MM

R$ 79.1 MM

Rio de Janeiro - RJ

4Q11

2,148

MCMV – 1st Layer

R$ 117.8 MM

R$ 12.2 MM

R$ 130.0 MM

Macapá - AP

4Q11

Minha Casa, Minha Vida 1st Layer

2011: Total PSV of R$ 522.5 million, consisting of 8,872 units

# Units

Segment

Housing PSV

Infrastructure PSV

Total PSV

Location

Launch

# Units

Segment

Housing PSV

Total PSV

Location

Launch

6

Operational Highlights

Launches

Sales

Land Bank

Inventory

Ricardo Ribeiro

Operational Highlights

7

Launches

Launched PSV

(R$ million)

1.447

+36%

428

+3%

2011

793

522

131

2010

1.067

686

380

4Q11

218

209

4Q10

415

225

190

Development

MCMV 1st Layer

Project Acquisition

Launched PSV – Track Record

(R$ million)

783710

176

CAGR +69%

2011

1.447

1.316

131

2010

1.067

2009 2008 2007

Launched PSV

Project Acquisition

Total

(R$'000)

% Direcional

(R$'000)

1 Aterrado do Leme October Rio de Janeiro - RJ 79,060 79,060 1,340 1,340 MCMV 1st Layer

2 Parque Ponta Negra - 4th Phase October Manaus - AM 53,915 53,910 138 820 Upper-Middle

3 Condomínio Parque Silvestre - 2nd Phase October Rio de Janeiro - RJ 13,152 10,785 140 488 RET1

4 Bem Viver Residencial Clube November Ceilândia - DF 62,912 62,849 220 220 Medium

5 Verano Residencial - 2nd Phase November Belém - PA 19,064 19,045 92 539 Medium

6 Residencial Macapaba December Amapá - AP 130,037 130,037 2,148 4,148 MCMV 1st Layer

7 Grand Ville December São Bernardo - SP 53,038 41,104 264 528 Medium

8 Monte Rey December Belo Horizonte - MG 30,766 30,735 128 128 Medium

Total 441,944 427,525 4,470 8,211

# of Units

Launched

Total Units

(All Phases)Segment4Q11 Projects Date City - State

PSV

AM PA

AP

MG

SP RJ

Launches Breakdown

8

DF

13%

36%

40%

16%

29%

2%

49%

5%

30%

28%

1% 2% 8%

44%

46%

8% 7%

36%

4Q11 4Q10 2010 2011

Launches by Segment

(% PSV) 2

7

6

5

4

3

8

1 Launches by Region

(% PSV)

49%

21%

30% 30%

9%

61%

2010 4Q10 2011 4Q11

38%

33%

67%

47%

15%

Southeast North Midwest

Upper-Middle

Commercial MCMV 1st Layer

Low-Income

Medium

9

Sales

Sales by Segment

(% PSV)

2010

1,037

657

380

4Q11

158

209

4Q10

406

217

190

1,230

+19%

367

-10%

2011

619

522

89 Development

MCMV 1st Layer

Project Acquisition

Sales by Region

(% PSV)

661

441

127

CAGR +76%

2011

1,230

1,141

89

2010

1,037

2009 2008 2007

Development

Project Acquisition

13%11%

46%

18%

26%

6% 4%

2010

37%

30%

20%

4Q11

57%

2011

15%

22%

5% 1%

4Q10

47%

16%

25%

1%

MCMV 1st Layer

Low-Income

Medium

Upper-Middle

Commercial

Sales by Segment

(% PSV)

Sales by Region

(% PSV)

4%

37%

4Q10

19%

15%

66%

2011

65%

9%

26%

2010

47%

19%

34%

4Q11

59% Midwest

Southeast

North

10

Sales Speed

4Q11

31.8%

18.5%

3Q11

36.7%

16.0%

2Q11

18.5%

1Q11

22.1%

4Q10

38.3%

27.6%

With MCMV 1st Layer projects

Without MCMV 1st Layer projects

Sales-Over-Supply Ratio (VSO)

(In Total PSV - %)

4Q10 93% 87% 4%

1% 1Q11 81% 48% 21% 9% 3%

2Q11 58% 20% 20% 18%

3Q11 92% 90%

2%

4Q11 85%

3M 6M 9M 12M 15M

10%

17%

4Q11 33%

3Q11

11%

2Q11

25% 1Q11

3% 2010

<2010

Sales by Period of Launching – 4Q11

(% PSV – Ex MCMV 1st Layer)

Sales Speed

(% Units)

67% of sales in 4Q11 refers to sales of inventory;

17% of PSV sold refers to projects launched before 2010.

11

Land Bank

60.7% large scale projects (more than 1,000 units);

53.3% in the North and Midwest regions;

53.0% projects in the low-income segment;

46.6% are eligible for the MCMV program.

R$ 6,9 Billion

66.906 units ES 2%

AM 14%

MG 38%

RO 5%

SP 6%

PA 13%

DF 21%

RJ 1%

Land Bank by Segment

(% PSV)

Low-Income 53%

Upper-Middle

7%

Medium 35%

Commercial 5%

Landbank Changes 2011

(PSV R$ million)

6,948 +191

2011 Launches

805

Review of

Assumptions

416

Acquired

Land Bank

581

2010

6,757

Land Bank by Region

(% PSV)

In 2011, Direcional

acquired six lots with

PSV of R$ 581 million;

Type of Payment

(2011 – % PSV)

Swap

99.76% Cash 0.24%

12

Inventory

7% of PSV are finished units;

89,1% of units under construction have already been sold.

12.2% 2009

<2009 7.3%

7.9%

22.8%

Finished Units

2011

49.7%

2010

64% North

11%

Southeast 25%

Midwest

Inventory by Region

(% PSV)

Inventory by Period of Launching

(% PSV)

Under Construction 668,461 92.7% 3,704 93.7%

Finished Units 52,536 7.3% 247 6.3%

Total Inventory 720,997 100.0% 3,951 100.0%

% Total Units in Inventory % TotalInventoryPSV in Inventory

% Direcional (R$'000)

13

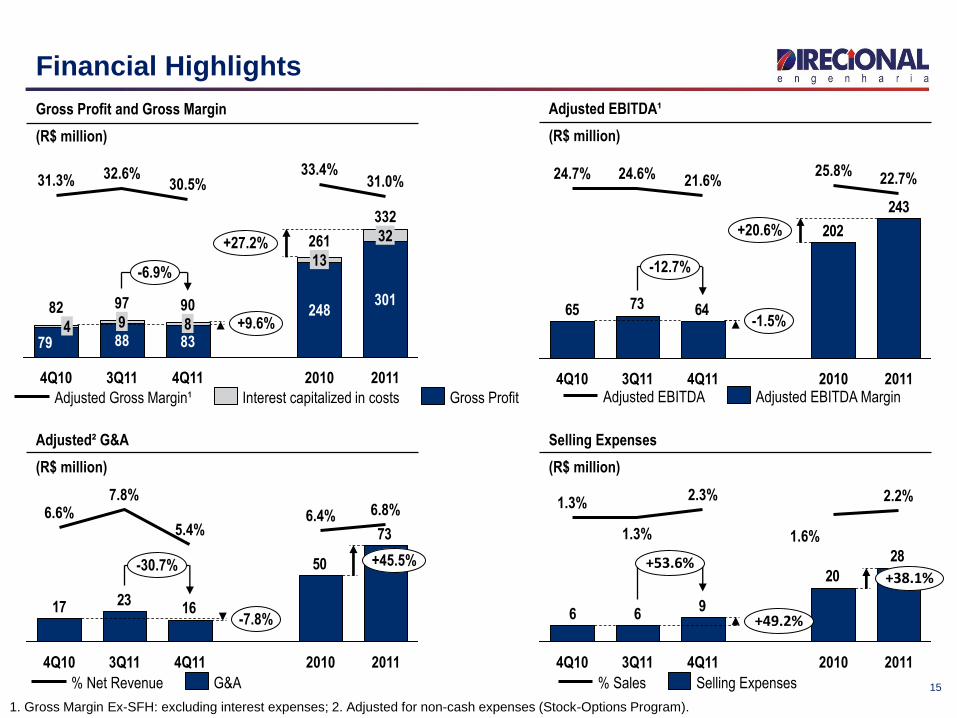

Financial Highlights

Financial Performance

Liquidity Ratios

Cash Burn

Deferred Results

DIRR3 Stock Analysis

Carlos Wollenweber

Financial Highlights

14

Financial Highlights

782

296298263

-0.6%

+12.4%

1,072

37.1%

2011 2010 4Q11 3Q11 4Q10

CAGR +80%

2011

1,072.3

2010

781.9

2009

377.6

2008

263.2

2007

102.3

Net Revenue

(R$ million)

Net Revenues - Track Record

(R$ million)

2115

130%

450%

2011

269

25%

2010

117

14%

4Q11

82

27%

3Q11

72

24%

2Q11

58

23%

1Q11

57

24%

4Q10

48

18%

3Q10

33

15%

2Q10

12%

1Q10

10%

Revenue from Services - Track Record

(R$ million)

MCMV 1st Layer

96.0% Brokerage Fee

1.8%

Management

2.3%

Breakdown of Revenue from Services

(in 2011 - %)

Revenue from Services % Net Revenue

15

Financial Highlights

1. Gross Margin Ex-SFH: excluding interest expenses; 2. Adjusted for non-cash expenses (Stock-Options Program).

-6.9%

+9.6%

+27.2%

2011

332

301

32

31.0%

2010

261

248

13

33.4%

4Q11

90

83 8

30.5%

3Q11

97

88 9

32.6%

4Q10

82

79 4

31.3%

Gross Profit Interest capitalized in costs Adjusted Gross Margin¹

Gross Profit and Gross Margin

(R$ million)

73

50

162317

-30.7%

-7.8%

+45.5%

2011

6.8%

2010

6.4%

4Q11

5.4%

3Q11

7.8%

4Q10

6.6%

G&A % Net Revenue

28

20

966

+53.6%

+49.2%

+38.1%

2011

2.2%

2010

1.6%

4Q11

2.3%

3Q11

1.3%

4Q10

1.3%

Selling Expenses % Sales

Adjusted² G&A

(R$ million)

Selling Expenses

(R$ million)

243

202

647365

-12.7%

-1.5%

+20.6%

2011

22.7%

2010

25.8%

4Q11

21.6%

3Q11

24.6%

4Q10

24.7%

Adjusted EBITDA Adjusted EBITDA Margin

Adjusted EBITDA¹

(R$ million)

16

Financial Highlights

1. Adjusted by non-cash expenses (Stock-Options Program).

199176

485951

-19.4%

-5.7%

+12.6%

2011

18.5%

2010

22.6%

4Q11

16.2%

3Q11

20.0%

4Q10

19.3%

2011

199

18.5%

2010

176

22.6%

2009

85

22.5%

2008

64

24.5%

2007

22

21.1%

CAGR +74%

Adjusted Net Income¹

(R$ million)

Net Income - Track Record

(R$ million)

Adjusted Net Income Adjusted Net Margin Adjusted Net Income Adjusted Net Margin

17

Cash, Debt and Cash Burn

Net Debt

Without SFH

-285.5

Net Debt

122.0

Cash and Cash

Equivalent

351.1

Gross Debt

473.2

SFH

407.6

65.6

Debt

(R$ million)

SFH 92.6%

FINAME and others

3.0%

Working Capital

4.7%

Loans and Financing Ex-Securitization

(%)

Cash and Debt 4Q11 3Q11 4Q10 D % D %

(R$'000) (a) (b) (c) (a/b) (a/c)

Loans and Financing 473,152 437,708 302,374 8.1% 56.5%

SFH 407,563 372,640 226,056 9.4% 80.3%

Receivables Securitization 31,847 35,273 46,843 -9.7% -32.0%

FINAME and others 13,076 9,480 8,882 37.9% 47.2%

Working Capital 20,666 20,315 20,593 1.7% n/a

Cash and Cash Equivalents 351,112 343,618 190,852 2.2% 84.0%

Net debt 122,040 94,090 111,522 29.7% 9.4%

Net debt / Equity 9.9% 7.9% 13.5% 0.0% 0.0%

18

Cash Burn

2Q11

34.0

1Q11

62.6

4Q10

100.9

3Q10

86.3

2Q10

-46.3%

1Q10

41.2

4Q09

32.7

3Q09

22.5

2Q09

25.3

1Q09

14.5

-72.5%

4Q11

27.7

3Q11

51.6 54.9

-37.9%

2011

175.9

2010

283.3

2011

122.0

Cash

4.9

155.4

Gross Debt

170.8

2010

111.5

351.1

+84%

2011 Operational

4.9

Stock

repurchase

plan

15.8

Dividends

40.3

Net

Follow-on

221.3

2010

190.9

Cash Burn¹

(R$ million)

Net Debt – Track Record

(R$ million)

Change in Cash

(R$ million)

1. Cash Burn: measured by the variation of the net debt, less capital increases, dividends and stock repurchase plan.

19

Deferred Results

Deferred Results Estimated Schedule

(%)

2014

1%

2013

22%

2012

77%

Deferred Results

(R$ million)

+12.1%

560 +34.7%

4Q11

334

226

3Q11

500

329

171

4Q10

416

327

89

Development

MCMV 1st Layer projects

Deferred Results Consolidated (R$'000) 4Q11 3Q11 4Q10 D % D %

(a) (b) (c) (a/b) (a/c)

Deferred results Consolidated (1+2) 560,382 499,703 415,909 12.1% 34.7%

Deferred revenues 1,482,460 1,325,614 1,022,801 11.8% 44.9%

Deferred results - Margin 37.8% 37.7% 40.7% 0.1 p.p. -2.9 p.p.

Deferred results Development (1) 334,100 328,803 326,813 1.6% 2.2%

Deferred revenues 775,531 773,964 751,614 0.2% 3.2%

Deferred results - Margin 43.1% 42.5% 43.5% 0.6 p.p. -0.4 p.p.

Deferred results MCMV 1st Layer projects (2) 226,282 170,899 89,096 32.4% 154.0%

Deferred revenues 706,928 551,651 271,186 28.1% 160.7%

Deferred results - Margin 32.0% 31.0% 32.9% 1.0 p.p. -0.8 p.p.

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

19

-no

v-0

9

8-d

ez-0

9

28

-dez

-09

15

-jan

-10

3-f

ev-

10

23

-fe

v-1

0

11

-mar

-10

29

-mar

-10

15

-ab

r-1

0

4-m

ai-1

02

0-m

ai-1

0

9-j

un

-10

28

-ju

n-1

0

15

-ju

l-1

0

4-a

go-1

0

24

-ago

-10

20

-set

-10

8-o

ut-

10

27

-ou

t-1

0

18

-no

v-1

0

6-d

ez-1

0

27

-dez

-10

13

-jan

-11

1-f

ev-

11

17

-fe

v-1

1

9-m

ar-1

1

25

-mar

-11

12

-ab

r-1

1

2-m

ai-1

1

18

-mai

-11

3-j

un

-11

21

-ju

n-1

1

8-j

ul-

11

26

-ju

l-1

1

11

-ago

-11

29

-ago

-11

15

-set

-11

3-o

ut-

11

20

-ou

t-1

18

-no

v-1

1

25

-no

v-1

1

13

-dez

-11

29

-dez

-11

17

-jan

-12

3-f

ev-

12

23

-fe

v-1

2

Pre

ço d

a A

ção

Vo

lum

e (

R$

mil)

Volume (R$ '000)

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

18

-No

v-0

9

7-D

ec-0

9

23

-De

c-0

9

14

-Jan

-10

2-F

eb

-10

22

-Fe

b-1

0

10

-Mar

-10

26

-Mar

-10

14

-Ap

r-1

03

-May

-10

19

-May

-10

8-J

un

-10

25

-Ju

n-1

0

14

-Ju

l-1

0

3-A

ug-

10

23

-Au

g-1

0

15

-Se

p-1

0

7-O

ct-1

02

6-O

ct-1

0

12

-No

v-1

0

3-D

ec-1

0

23

-De

c-1

0

12

-Jan

-11

31

-Jan

-11

16

-Fe

b-1

1

4-M

ar-1

1

24

-Mar

-11

11

-Ap

r-1

1

29

-Ap

r-1

1

17

-May

-11

2-J

un

-11

20

-Ju

n-1

1

7-J

ul-

11

25

-Ju

l-1

1

10

-Au

g-1

1

26

-Au

g-1

11

4-S

ep

-11

30

-Se

p-1

1

19

-Oct

-11

7-N

ov-

11

24

-No

v-1

1

12

-De

c-1

1

28

-De

c-1

1

16

-Jan

-12

2-F

eb

-12

22

-Fe

b-1

2

9-M

ar-1

2

Sto

ck P

erf

orm

ance

Vo

lum

e (

R$

'00

0)

Average Volume (21 days) Ibovespa IMOB Direcional

20

Shares Performance Since IPO

21

Disclosure

This presentation contains certain forward-looking statements concerning the business prospects,

projections of operating and financial results and growth potential of the Company, which are based on

management’s current expectations and estimates of the future performance of the Company. Although the

Company believes such forward-looking statements are based on reasonable assumptions, it can give no

assurance that its expectations will be achieved. Expectations and estimates that are based on the future

prospects of the Company are highly dependent upon market behavior, Brazil’s political and economic

situation, existing and future regulations of the industry and international markets and, therefore, are

subject to changes outside the Company’s and management’s control. The Company undertakes no

obligation to update any information contained herein or to revise any forward-looking statement as a result

of new information, future events or other information.

22

Contacts

Carlos Wollenweber CFO | IR Officer

Lucas Bousas IR Analyst

Paulo Sousa IR Analyst

www.direcional.com.b/ri

(55 31) 3214-6200

(55 31) 3214-6450