selangor becomes data centre hotspot - ssic.com.my · msc malaysia: ... others followed this...

TRANSCRIPT

2012

The market for data centres in Southeast Asia is currently estimated at USD 10.9 billion and projections show strong growth potentials for the coming years. In this context, Malaysia aspires to become the region’s leading data centre hub. Headed by the Minister of Human Resources under the initiative “Outsourcing Malaysia”, data centres are about to become the next pillar of the country’s booming service industry. With more than 60 % of the current data centres being located in Selangor, the state will be a major contributor and facilitator for interested investors and the data centre business community. This report is providing insights into this expanding market, its players and trends. Furthermore, the specific advantages of Selangor as an investment destination and in comparison to other states of Malaysia are highlighted.

Outsourcing Malaysia – Selangor becomes Data Centre Hotspot

Selangor – Data Centre Industry Report 2012/13

2

Malaysia Selangor (Klang Valley) Rank in Malaysia

Doing Business Ranking – World Bank (2012)

12 AT Kearney Global Services Location Index 2011

3 Population 27m 5.1m 1 GDP (2010) 559,554m

(100%) 128,815m (23.03%)

1

GDP Growth (2010) 7.2% 10.8% 1

Number of Investment Projects (2010)

910 (100%) 325 (35.71%) 1

Data Centre Distribution (%)

100% 64% (80%) 1

Cybercities/ Centres

26 19 1

Data Centre - Market Value in RM billion

3.4 2.176 (estimated) 1

Supportive Infrastructure

Outsourcing Malaysia: www.outsourcingmalaysia.org.my MSC Malaysia: www.mscmalaysia.my Multimedia Development Corporation: www.mdec.my

Data Centre Industry Report – Summary 2012

Picture 1 Geographic Distribution of Data Centres in Malaysia, Source: SSIC 2012

Selangor – Data Centre Industry Report 2012/13

3

Table of Contents

1. Shared Services and Outsourcing in Malaysia .......................................... 4

1.1 Malaysia and Selangor – Prime Business Locations .......................... 4

1.2 Skilled Workforce ................................................................................ 5

1.3 Industrial Property ............................................................................... 6

1.4 Free from Natural Disaster ................................................................. 7

2. Why to invest in Selangor? ........................................................................ 7

2.1 Selangor – At a Glance ....................................................................... 8

2.2 IT Outsourcing in Selangor ................................................................. 9

2.3 Data Centres – Market Structure ...................................................... 10

2.4 Selangor – Who is Who in the Data Centre Industry ........................ 12

2.5 Trends and Developments ................................................................ 13

3. Investment Incentives for ICT Companies ............................................... 14

3.1 MSC Malaysia Status Company ....................................................... 14

3.2 Incentives for ICT .............................................................................. 15

4. Main Sources .......................................................................................... 16

Selangor – Data Centre Industry Report 2012/13

4

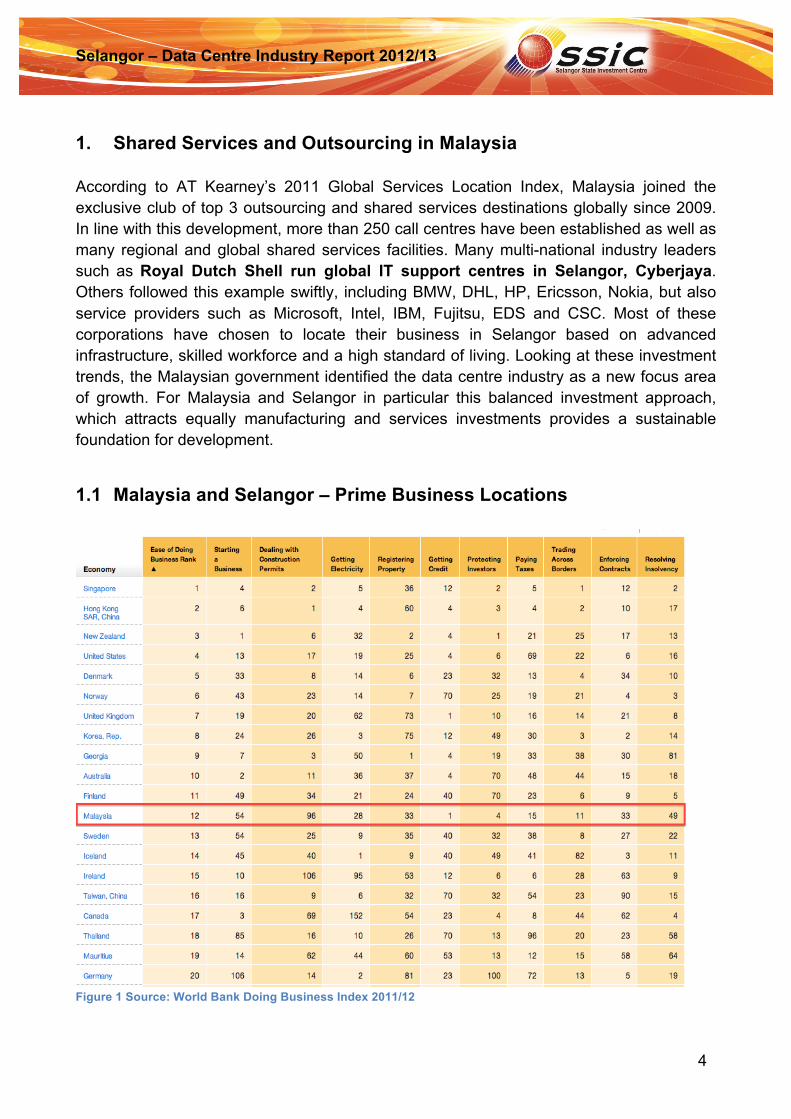

1. Shared Services and Outsourcing in Malaysia According to AT Kearney’s 2011 Global Services Location Index, Malaysia joined the exclusive club of top 3 outsourcing and shared services destinations globally since 2009. In line with this development, more than 250 call centres have been established as well as many regional and global shared services facilities. Many multi-national industry leaders such as Royal Dutch Shell run global IT support centres in Selangor, Cyberjaya. Others followed this example swiftly, including BMW, DHL, HP, Ericsson, Nokia, but also service providers such as Microsoft, Intel, IBM, Fujitsu, EDS and CSC. Most of these corporations have chosen to locate their business in Selangor based on advanced infrastructure, skilled workforce and a high standard of living. Looking at these investment trends, the Malaysian government identified the data centre industry as a new focus area of growth. For Malaysia and Selangor in particular this balanced investment approach, which attracts equally manufacturing and services investments provides a sustainable foundation for development.

1.1 Malaysia and Selangor – Prime Business Locations

Figure 1 Source: World Bank Doing Business Index 2011/12

Selangor – Data Centre Industry Report 2012/13

5

Malaysia has become a preferred investment destination, which is supported by a business friendly investment environment, the availability of a skilled workforce and relative low initial investment costs. It does not come as a big surprise that the recent Doing Business ranking by the World Bank indicated remarkable improvements and ranked Malaysia at position 12 as of now before nations such as Sweden, Germany, Ireland and Canada. Independent research has highlighted the competitiveness of Malaysia, in which Selangor has become the role model of development and successful investment promotion.

Figure 2 Source: AT Kearney 2011/12

AT Kearney’s 2011 Global Services Location Index offers a glimpse of Malaysia’s exceptional competitiveness. Only beaten by two giants, China and India, Malaysia ranked 3rd in the index. Especially in regard to the business environment Malaysia was able to score and received higher ratings than both of its larger competitors. However, there is more to it, as the following chapter reveals.

1.2 Skilled Workforce

Table 1 Salary Range for IT Professionals, Source: Outsourcing Malaysia 2012 (Conversion Rate RM 3.2=1 USD)

Year Fresh Graduates (Entry Level)

Jun. Executives (1 - 4 years experience)

Sen. Executives (> 5 years experience)

Middle Management (Manager)

Sen. Management (Senior Manager)

2011 RM 2.238 (USD 699)

RM 3,151 (USD 985)

RM 5,039 (USD 1,575)

RM 7,005 (USD 2,449)

RM 10,795 (USD 3,802)

Percentage Change (%) to 2010

n/a

7,3

11,6

11,9

12,7

Selangor – Data Centre Industry Report 2012/13

6

Malaysia, even though it only commands a workforce of 12-16 million, is equipped with unique features. Many employees are effectively trilingual (Bahasa Malaysia, English, Mandarin or Tamil) and highly skilled. The country spends about 8.1 % of its gross domestic product on education. Only in Selangor, every year more than 10,000 students graduate from about 130 institutions of higher learning, while there are approximately 160,000 graduates in the whole country. Moreover, Selangor is the state with the most universities and colleges as well as graduates in comparison. Besides, many graduates from other states finally settle in the Klang Valley due to better job opportunities, infrastructure and a high standard of living. In regard to the salary range, the average in table 1 reflects Selangor’s labour situation most appropriately. In Kuala Lumpur the salary usually rises higher as does the Iskandar region in Johor, while other states either have reached similar levels or mark lower because of the lack of workforce, infrastructure and further development.

1.3 Industrial Property

Industrial property and land have experienced a steady growth trend in recent years. In this context, Selangor has the highest supply of industrial property with 34,515 units as per 2011 followed by Johor and Penang. Therefore investors are able to access a wide variety of locations, prices and different facilities. A good selection and quality usually come with a certain price tag, but the truth is far more complex. Selangor offers prime property, but does not always demand prime prices. The chart above is comparing Selangor with Johor

Diagram 1 Industrial Property Prices, Source: CBRE 2011/12

Selangor – Data Centre Industry Report 2012/13

7

and Penang, which are two other established and upcoming investment destinations respectively. While Penang is experiencing one price hike after another due to limited space, the property prices in Johor are also starting to catch-up due to demand from Singapore. Unconfirmed statistics tend to mark Johor already as high as Selangor. Both regions do not offer the same infrastructure, large amount of property and availability of skilled workforce. In addition, Johor cannot compare to the living standard in Selangor. Especially in regard to the property question, investors can rely on the support of the Selangor State Investment Centre, which is identifying and proposing property and land to potential investors.

1.4 Free from Natural Disaster

Besides the supportive business environment, industry experts have highlighted the fact that Malaysia and especially Selangor never experienced any serious natural disaster. Even tsunamis cannot reach Selangor, since the long-stretching Indonesian island of Sumatra protects the whole coastline. This relative safety at the Straits of Malacca also refers to the power grid and possible blackouts. Since Selangor is home to major infrastructures such as sea- and airports, the national energy company Tenaga Nasional has installed the best equipment available to avoid any downtime. For data centres, these facilities and conditions are the perfect environment to establish their business.

2. Why to invest in Selangor?

Figure 3 Selangor is free from natural disaster

Picture 2 Key Benefits to Invest in Selangor Source: SSIC 2013

Selangor – Data Centre Industry Report 2012/13

8

2.1 Selangor – At a Glance

Comparing Selangor to other investment destinations in Malaysia, there are some advantages unique to this state. Selangor provides with 2.82 million people the largest workforce in Malaysia. More than 100 institutions of higher learning, some 30 international schools and several international colleges and universities offer the broadest and most diverse education available in Malaysia. Besides, Selangor’s advanced infrastructure includes the largest port (Port Klang), the largest international airport (Kuala Lumpur International Airport), other international airports (e.g. Subang Airport) and the most extensive network of highways, railroad and related public transportation systems. In addition, investors find with Cyberjaya the national ICT-capital of Malaysia in Selangor, including the best IT infrastructure available in the country. Connectivity is key in this industry and Malaysia acknowledges the requirement for fast and reliable internet connections. The picture below is providing a good understanding of what Malaysia’s government accomplished in regard to connectivity.

Picture 3 Malaysia's International Connectivity, Source: MSC Malaysia 2013

Evaluating some of the relevant statistics, Selangor presents itself as the nations economic powerhouse with a contribution of 22-23 % to the national GDP, top investment projects and a vibrant business community. Most manufacturing projects in Malaysia are located in Selangor, which also creates the biggest contribution to the national gross domestic product. The demand for business services has been rising ever since. Furthermore, most employment opportunities are created in the region. Consequently, companies benefit from a continuous flow of ambitious graduates and workers as well as potential clients into Selangor.

Selangor – Data Centre Industry Report 2012/13

9

Sources: Malaysian Department of Statistics 2011, MIDA 2011/12

Table 2 Economic Statistics Selangor

Certainly, the advanced infrastructure of the state has supported economic and investment trends positively. The same can be said about the rising star of the data centre industry. In the following chapter, some of the IT specific infrastructures will be introduced, which are able to provide a better understanding of the available resources and facilities.

2.2 IT Outsourcing in Selangor AT Kearney’s Global Services Location Index 2011 ranked Malaysia in third place behind China and India. The diagram below reflects the booming IT outsourcing (ITO) industry in the country. Building on this strength, the Malaysian government announced that data centres are meant to become the next key industry in Malaysia’s aspirations to grow knowledge- and high-technology industries over labour-intensive operations.

Figure 4 Industry activity in top 10 countries, Source: AT Kearney 2011

Selangor Rank Malaysia

Population 5.1m (18.88%) 1 27 m (100%)

GDP at constant prices in RM million (2010)

128,815m (23.03%)

1 559,554m (100%)

GDP Growth (2010) Year-to-year

10.8% 1 7.2%

Labor Force 2.169m (18.68%) 1 11.611m (100%)

Unemployment 2.3% - 3%

Total Capital Investment for 2012 (RM)

11,734,817,935 (28.58%)

1 41,052,392,045 (100%)

Number of Investment Projects (2012)

252 (31.34%) 1 804 (100%)

Potential Employment from Investment Projects (2012)

22,719 (29.64%) 2 76,631(100%)

Selangor – Data Centre Industry Report 2012/13

10

While business process outsourcing and voice are growing slowly, the skilled workforce and strength in ITO are becoming a driving force of the whole economy. Out of this observation, the government intends to achieve a contribution of RM 2.1 billion to the gross national income by data centres.

2.3 Data Centres – Market Structure The regional market for data centres is currently estimated at USD 10.9 billion for Southeast Asia. Malaysia intends to challenge data centre strongholds such as Singapore with new concepts, green technology and also a different pricing strategy. In Malaysia, the market is expected to reach a value of RM 3.4 billion by 2014 (approx. USD 1 billion) and is expected to grow at a healthy rate of 17.3 % annually. Global projections only expect growth rates of 12%, which Malaysia is likely to outpace. In order to achieve the government’s target of 5 million sqm in data centre space 2020 higher growth rates are imperative, since so far only 0.5 million sqm are available in the whole country. The recent investment trends show figures up to RM 4.1 billion and a growing determination of existing providers to expand their services, upgrade certification and security measures. In line with these developments, the industry has also created about 13,290 jobs in Malaysia.

Diagram 2 Source: Data Centre Map 2012

The Malaysian market is driven by a small group of 16 established services providers in this sector, which are part of the “Outsourcing Malaysia” Initiative. Besides, there are also an increasing number of international and domestic investments introducing new

64%

36%

Geographical Distribution of Data Centers in Malaysia

Selangor

Other States

Source: Data Center Map 2012

Selangor – Data Centre Industry Report 2012/13

11

companies into the market. Almost 2/3 or 10 companies of the “Outsourcing Malaysia” Initiative installed their headquarters in Selangor, while the other 6 companies are located in Kuala Lumpur. In other words, the industry is concentrated in the Klang Valley including the majority of data centres and technical facilities. Basically, the market share of the Klang Valley almost covers 80 % of the whole industry. In this context, Cyberjaya, the national ICT capital in Selangor plays a major role in attracting investments. This cyber-city has been entirely planned and developed to become the regional epicentre of ICT and high technology. Consequently, investors will find here the most advanced IT infrastructure in the country and most likely the whole region. Following this statement, the Klang Valley hosts 19 of 26 cybercities and cybercentres in Malaysia. These areas are meant to be prime business locations for ICT companies and offer the state-of-the-art infrastructure. Many of these locations have already attracted international industry leaders and continue to provide the highest quality of services and infrastructure. The following table offers an overview on the available infrastructure in form of cybercities and data centres in Selangor, which are dedicated areas of ICT excellence. Respective investments in these specific areas will receive additional support such as investment incentives and programs, including grants, specific infrastructure and skilled labour.

Name Area Brands Contact

Cyberjaya (ICT Capital)

6,960.69 acres • Basis Bay

• Dell • Ericsson

• Fujitsu • HP Global

Centre • IBM • Mahindra

Satyam

Contact person: Md Nazri Tumin Tel. +60 (0)3 8315 6001 Email. [email protected] Web. www.cyberview.com.my

I-City 72 acres Contact person: Y.Bhg. Dato’ Eu Hong Chew Tel. +60 (0) 3 5521 8800 Fax. +60 (0) 3 5521 8808 Web. www.i-city.my

Bandar Utama 124.75 acres Contact person: Gary Yau Tel. +60 (0) 3 7728 8878 Fax. +60 (3) 7728 9978

UPM-MTDC 39 acres

Contact person: Abdul Rahman Yasir Tel. +60 (0) 3 8941 4100

Selangor – Data Centre Industry Report 2012/13

12

• Measat

• Shell

Fax. +60 (0) 3 8941 4200 Web. www.mtdc.com.my

Jaya 33 6.2 acres Contact person: Mike Kan Tel. +60 (0) 3 7954 9888 Email. [email protected] Web. www.jaya33.com

Table 3 Source: Multimedia Development Corporation 2011/2012

2.4 Selangor – Who is Who in the Data Centre Industry Company Location Data Centre Space/

Building Contact

AIMS Data Centre Sdn Bhd

• Kuala Lumpur • Cyberjaya, Selangor • Johor Bahru

Cyberjaya: 34,500 ft2

www.aims.com.my

Basis Bay • Cyberjaya, Selangor • Shah Alam, Selangor • Glenmarie, Selangor • Kulim, Kedah

Cyberjaya: 30,000 ft2

www.basisbay.com

Computer Recovery Facility Sdn Bhd

• Petaling Jaya, Selangor

Petaling Jaya: 60,000 ft2

www.crf.my

CST Group plc • Petaling Jaya, Selangor

More than 530,000 ft2 in SEA

www.csf-group.com

Free Net Business Solutions Sdn Bhd

• Cyberjaya, Selangor Cyberjaya: 155,000 ft2

www.fnbs.net

HDC Data Centre • Shah Alam, Selangor Shah Alam: 50,000 ft2

www.hdc.net.my

HeiTech Padu Berhad

• Subang Jaya, Selangor n/a www.hms.heitech.com.my

Jaring Communications Sdn Bhd

• 8 locations in Malaysia Nationwide 32,500 ft2

www.jaring.my

Maxis Bhd • Shah Alam, Selangor Shah Alam: 3,500 ft2

www.maxis.com.my/business

MYTelehaus Sdn Bhd

• Cyberjaya, Selangor 36,000 ft2 www.mytelehaus.com

Selangor – Data Centre Industry Report 2012/13

13

NTT MSC Sdn Bhd • Cyberjaya, Selangor

50,000++ ft2 www.my.ntt.com

i-Tech Network Solutions Sdn Bhd

• Kuala Lumpur 1,000 ft2 www.safehouse.com.my/

SKALI Group • Cyberjaya and Serdang, Selangor

Cyberjaya: 70,000 ft2

www.skali.net

Strateq Data Centre Sdn Bhd

• Petaling Jaya, Selangor

Petaling Jaya: 100,000 ft2

www.strateqgrp.com

Teliti Datacentres Sdn Bhd

• Negeri Sembilan 120,000 ft2 www.teliti.com

VADS Berhad • Kuala Lumpur 14 Data Centres: 150,000 ft2

www.vads.com

Table 4 Source: Outsourcing Malaysia 2012

2.5 Trends and Developments

The data centre industry in Malaysia is determined to achieve the governmental target of 5 million sqm centre space until 2020 and thereby creating the perfect environment for a healthy industry meeting customer demand. While established initiatives such as Outsourcing Malaysia, cybercities as well as the MSC Malaysia ICT initiative are providing platforms, incentives and support for investors, the industry adopted innovative strategies to optimise the existing facilities and create new

services. For Malaysia and Selangor in particular, two major trends have emerged out of this sector. On the one hand, data centres become greener and on the other, the race for advanced technology standards and new services requires continuous innovation and upgrades. What is the impact of both trends? In regard to green technology, investments have been focused on reducing the demand for electricity and thereby improving the environmental track record of data centres. Furthermore, many client companies are evaluating new ways of decreasing their carbon footprint globally, which will also include their suppliers and service providers. In this

Picture 4 Selangor's Data Centre "GO GREEN"

Selangor – Data Centre Industry Report 2012/13

14

context, new investments in Malaysia will offer the opportunity to utilise the most up-to-date technology as well as lower carbon emissions. With up to RM 400 million of investments in new green data centres, new technologies and better standards, Malaysia is well prepared for the carbon-conscience customer. Approximately 1/3 of the amount is again invested in Selangor and includes several upgrades and expansions of companies such as the homegrown Malaysian AIMS Group. The company has just recently completed two projects valued RM 80 million and recorded double-digit growth figures in recent years. One of the main projects has been located in Cyberjaya, Selangor, where in 2012 another expansion has been completed. Also located in Cyberjaya, a competitor of AIMS, Basis Bay, introduced one of the first green data centres and continues to expand with the same model in other regions. What might be surprising, industry experts estimate that green data centres are able to save 20% to 30% of costs compared to existing business models. Looking at the innovation-driven environment of this industry, all data centres in Selangor at least fulfill the tier-3 standard, which offers better energy security and multiple distribution paths among other features. On top, several providers, including the local telecommunication giant Telekom Malaysia, prepared their data centres to be tier-4 ready. The Malaysian industry has taken all measures to meet highest international standards based on the US ANSI/TIA-942 standard, the German datacentre star audit as well as the Uptime Institute’s standards. Apart from these technology-changes, new topics surfaced in the light of international trends and opportunities. Cloud computing has become the new buzzword of a thriving industry. Many data centres already introduced additional services in this context and will offer client companies to manage their contents in the cloud. This outsourcing service reduces IT-related investments and maintenance costs in the client company, while high standards of data security are applied. Evaluating these developments, Selangor presents itself as a leading business location for ICT companies, outsourcing services and data centres here in Malaysia. Excellent facilities, infrastructure and a well-educated workforce were key for this success and offer further potentials to invest.

3. Investment Incentives for ICT Companies The Malaysian Investment Development Authority (MIDA) in collaboration with the Multimedia Development Corporation (MDeC) is providing the following investment incentives for ICT Companies:

3.1 MSC Malaysia Status Company MSC Malaysia status multimedia companies operating in MSC Malaysia Cybercities or Cybercentres are eligible for the following incentives/facilities:

Selangor – Data Centre Industry Report 2012/13

15

I. Pioneer Status with income tax exemption of 100% of the statutory income for a period of 10 years or Investment Tax Allowance of 100% on the qualifying capital expenditure incurred within a period of five years to be offset against 100% of statutory income for each year of assessment.

II. Eligibility for R&D grants (for majority Malaysian-owned MSC Malaysia Status companies)

Other benefits also include: • Duty-free import of multimedia equipment • Intellectual property protection and a comprehensive framework of cyberlaws • No censorship of the Internet • World-class physical and IT infrastructure • Globally competitive telecommunication tariffs and services • Consultancy and assistance by the Multimedia Development Corporation to companies

within the MSC Malaysia • High quality, planned urban development • Excellent R&D facilities • Green and protected environment • Import duty, excise duty and sales tax exemption on machinery, equipment and

materials. Applications for MSC Malaysia Status should be submitted to MDeC.

3.2 Incentives for ICT (i) Accelerated Capital Allowance Companies are eligible for Accelerated Capital Allowance (ACA) that provides an initial allowance of 20% and an annual allowance of 40% for expenditure incurred in acquiring computers and information technology assets, including software. Effective for the Year of Assessment 2009 to the Year of Assessment 2013, the period to claim ACA on expenses incurred on ICT equipment including computer and software is accelerated from two years to one year. The cost of developing websites is allowed as an annual deduction of 20% for a period of five years. Claims should be submitted to the IRB. (ii) Deduction of Operating Expenditure Companies enjoy a single deduction of operating expenditure including payments to consultants related to IT usage for improving management and production processes. Claims should be submitted to IRB.

Selangor – Data Centre Industry Report 2012/13

16

(iii) Tax Exemption on the Value of Increased Exports Companies in the ICT sector can apply for a tax exemption on their statutory income equivalent to 50% of the value of increased exports. Claims should be submitted to IRB.

4. Main Sources: • AT Kearney (2011): Global Services Location Index,

http://www.atkearney.com/gbpc/global-services-location-index • CB Richard Ellis Malaysia (2012): http://www.cbre.com.my • Data Centre Map – Malaysia (2012): http://www.datacentermap.com/malaysia/ • Data Centre Malaysia (2012): http://www.datacentre.my • Malaysian Department of Statistics (2011/12): http://www.statistics.gov.my/ • MSC Malaysia – National ICT Initiative (2012): http://www.mscmalaysia.my • Multimedia Development Corporation (2012): http://www.mdec.my • Outsourcing Malaysia (2012): http://www.outsourcingmalaysia.org.my • World Bank Group (2012): Doing Business Index, http://www.doingbusiness.org • Malaysian Investment Development Authority (MIDA): http://www.mida.gov.my