sas group 3rd quarter presentation 2007 · newco bmi air greenland. 9 sas group q3 presentation ......

TRANSCRIPT

SAS Group 3rd Quarter Presentation 2007Analyst PresentationLondon, November 9

2SAS Group Q3 presentation

A challenging Quarter, but record passenger numbers

EBT bef. non rec. Q3: MSEK 632, Jan-Sep 2007: MSEK 982

– Record number of passengers

– Group airlines perform strongly

– Negative effect from Q400, ECA agreement

S11 implementation as planned

Despite setbacks SAS has full focus ahead

– Still favorable market conditions

– S11 will secure strong and profitable SAS

3SAS Group Q3 presentation

Quarter overshadowed by Q400 problems

Two accidents in September

– Aalborg, Vilnius

Three weeks grounding

Third accident in October

– Unique and strong decision to permanently stop operations

– Customers

– Employees

– SAS brand

Ongoing dialogue with Bombardier

4SAS Group Q3 presentation

Continued good growth in most SAS Group markets

Estonia:

Latvia:

Lithuania:

Sweden:

3.5%2%

Norway:

3.3%

7%

Denmark:

2.0% 3.7%

7.4%10%

10.1%

27%

8.2%

>25%

Expected GDP growth (2007)Passenger growth (Jan-Sep vs. last year)

Finland:

3.8%

6%

Spain (domestic):

3.6%11%

Eurozone:

2.5%4.9%

Continued favorable economic cycleGood growth on all marketsIncreased growth rate in Q3

SAS Group passenger growth (Jan-Sep vs. last year)

2.7%

4%

0.4%

6%

0.7%

15%

>27%

>5%

44%

5SAS Group Q3 presentation

Record number of passengers for the 31st

consecutive month

31 000 00032 000 00033 000 00034 000 00035 000 00036 000 00037 000 00038 000 00039 000 00040 000 00041 000 00042 000 000

jan-05

may-05

sep-0

5

jan-06

may-06

sep-0

6

jan-07

may 20

07

sep-0

7

62,0%63,0%64,0%65,0%66,0%67,0%68,0%69,0%70,0%71,0%72,0%73,0%

Number of passengers (12 months rolling) Passenger load factor (12 months rolling)

Record number of passengers since April 2005

6SAS Group Q3 presentation

Overall reflection: Complex company and thereby difficult to manage

S11 strategy will ensure SAS’s future

Cultural Turnaround

Focus and concentration

Harmonization and development of

customer offer

Competitiveness

Profitable growth

7SAS Group Q3 presentation

Cultural Turnaround

Customer orientation

Increased participation and

commitment

Improved management

Common target and new

cooperation model

Profit sharing system and part-

ownership program

Ongoing tight dialogue with the

unions

Employee incentive scheme to be

presented on AGM in April 2008

8SAS Group Q3 presentation

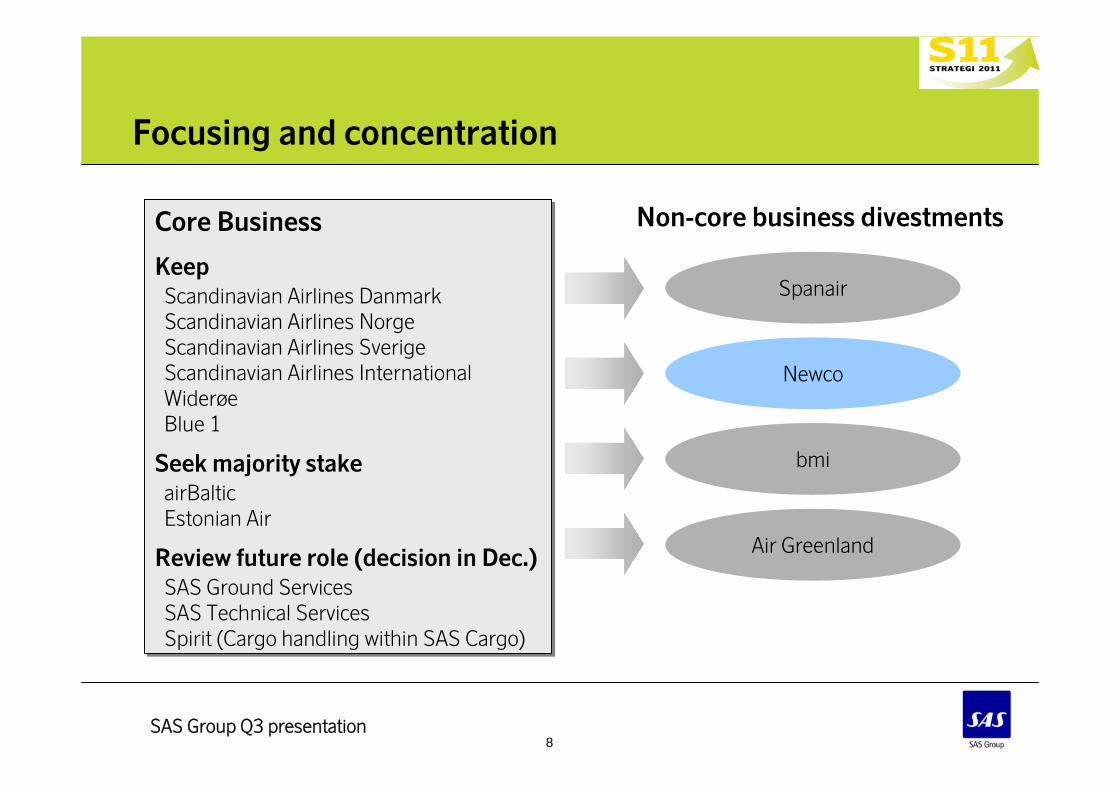

Focusing and concentration

Core Business

KeepScandinavian Airlines DanmarkScandinavian Airlines NorgeScandinavian Airlines SverigeScandinavian Airlines InternationalWiderøeBlue 1

Seek majority stakeairBalticEstonian Air

Review future role (decision in Dec.)SAS Ground ServicesSAS Technical ServicesSpirit (Cargo handling within SAS Cargo)

Core Business

KeepScandinavian Airlines DanmarkScandinavian Airlines NorgeScandinavian Airlines SverigeScandinavian Airlines InternationalWiderøeBlue 1

Seek majority stakeairBalticEstonian Air

Review future role (decision in Dec.)SAS Ground ServicesSAS Technical ServicesSpirit (Cargo handling within SAS Cargo)

Non-core business divestments

Spanair

Newco

bmi

Air Greenland

9SAS Group Q3 presentation

Harmonization and development of customer offerPositive effects from New Commercial initiatives

Customer improvements:New fast track in StockholmBiometric solutionsSMS serviceMore distinct product conceptsLower prices in Economy ExtraSeamless flow at the airportIncreased award recognitionNew offers to corporate market

Positive Customer feedbackSAS takes market shares in premium segmentsEconomy Extra well receivedIncreased Business traffic– London f.ex.

World class electronic travel solutions

• “ h u m a n ” h o m e o r a

• In g a k ö e rFast track

• “ h u m a n ” h o m e o r a

• In g a k ö e rFast track

SMS check in service launched

WLAN service launched

New fast track at Stockholm-Arlanda

Fast track to be introduced at Oslo-

Gardermoen

10SAS Group Q3 presentation

Competitiveness:Status of the cost reductions of SEK 2.8 bn

0,0

0,5

1,0

1,5

2,0

2,5

3,0

Implemented To be implemented

2.8

Cost programSep 30 2007

Group administrative functions 300-400 MSEK– Administration, to be completed by year end

– Shared services, ongoing effects in 2008

Group coordination of procurement 400 MSEK– Centralized purchasing function with a clear mandate

– Many activities in process

SAS Group subsidiaries SEK 2.1bn

– Operational flight costs SEK 1000m

– Administrative and sales cost SEK 600m

– Ground/Technical SEK 500m

18% implemented

11SAS Group Q3 presentation

Profitable growthNew routes and commercial initiatives – Fall 2007

Decision to add one new long haul aircraft– Copenhagen – San Francisco (2008)

– Copenhagen – New Delhi (2008)

Long haul routes– Copenhagen-Dubai (October)

– Stockholm-Bangkok (October)

18 new routes in Europe introduced

New aircraft– 2 B737-800 and 2 A319 (2007)

– 3 B737-800 (2008)

– 2 B737-800 (2009)

SAS Norway focus on leisure segment– Reallocation of aircraft

– 12 new destinations

S11 Target to grow 20% until 2011

15-20 new aircraft

Gunilla BergCFO

13SAS Group Q3 presentation

Underlying 3rd Quarter Result improved

+423147570+17782259Joint Venture Lufthansa/ECA

+2000200+2000200Q400 effects

300

982

2007

January-September

350

239

2006

+1 316

-50

+743

Change

+158

0

-219

Change

July-SeptemberUnderlying result development

0

851

20062007MSEK

0

632

Underlying result improvement

Strike effects

Income before nonrecurring items in

continuing operations

3rd Quarter

14SAS Group Q3 presentation

Full year Q400 direct result effect estimated to MSEK 600-700

0

100

200

300

400

500

sep oct nov-dec

Q400 first groundingEstimated result impact = appr. 300MSEK

Q400 second groundingEstimated result impact = appr. 300-400MSEK

500 MSEK first grounding estimate:• 300 MSEK direct effect

• 200 MSEK indirect goodwill effect

Q3 effect Q4 effectSAS Group Q400 incidents direct result effect 2007

15SAS Group Q3 presentation

Actions taken to mitigate negative passenger consequences from the grounding of Q400

Q400 permanently grounded on Oct 28– 27 of the Group’s 303 aircraft accounting for 5% of the

capacity

Measures to mitigate negative passenger consequences

– Review of network and reallocation of aircraft capacity within the SAS group

– External wet lease capacity– External dry lease capacity

Long term replacement is expected to start implementation in the 2nd Half 2008

As of early November, 8 wet leases secured – Estimated to be 11-14 by end of November

– Almost 80% of capacity covered

0%10%20%30%40%50%60%70%80%90%

100%

29 Oct 12-nov 26-nov 10-dec 24-dec

Q400 replacement in production

Due to wet lease, internal group changes, usage of reserves and minor timetable changes. SAS is able to recover quickly.

16SAS Group Q3 presentation

SAS Norge and SAS Sverige close or above profitability targets

ChangeQ3 2007ChangeQ3 2007ChangeQ3 2007ChangeQ3 2007Results

-0.4 p.u.10.5%+3.5 p.u.5.3%+6.1 p.u.8.6%+1.4 p.u.6.0%EBIT margin

228

SAS International

+78207

SAS Norge

283

SAS Danmark SAS SverigeScandinavian Airlines

+213 108 -22+60EBT before nonrec. (MSEK)

SAS International

SAS Sverige

SAS Danmark

SAS Norge

EBIT-margins, 12 months rolling

1.4%

9.7%

6.3%

8.3%

17SAS Group Q3 presentation

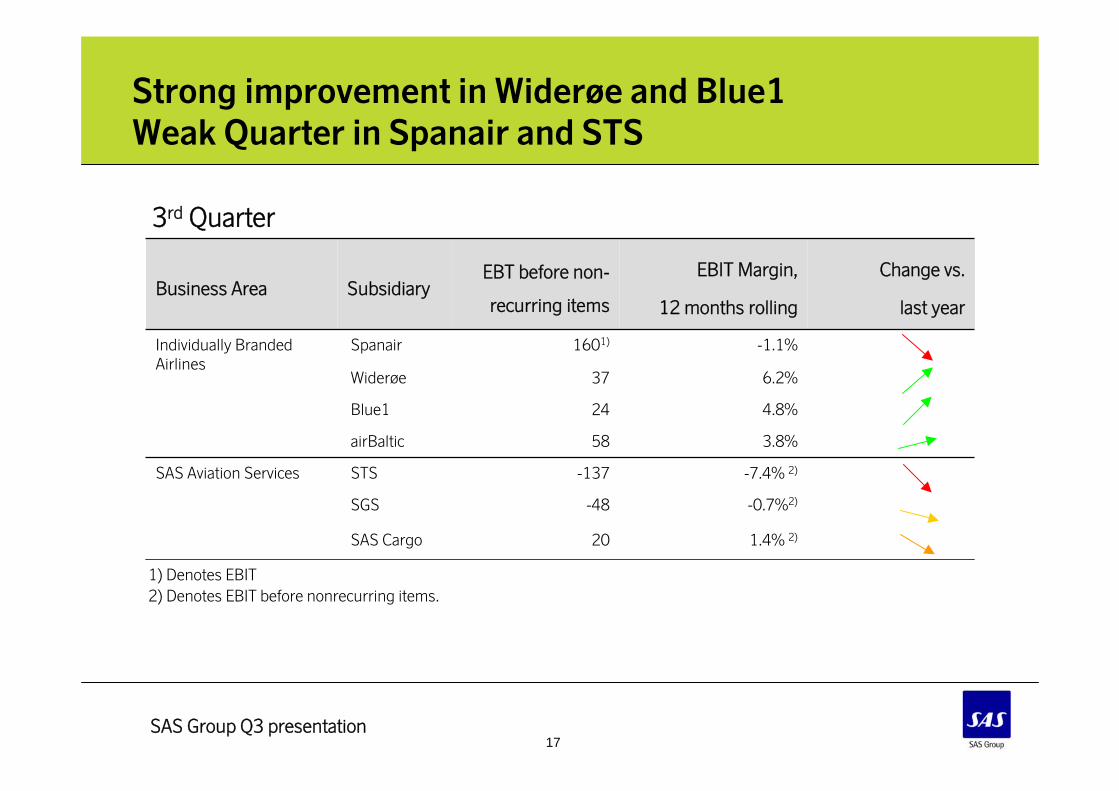

Strong improvement in Widerøe and Blue1Weak Quarter in Spanair and STS

-0.7%2)-48SGS

1.4% 2)

-7.4% 2)

3.8%

4.8%

6.2%

-1.1%

EBIT Margin,

12 months rolling

Change vs.

last year

EBT before non-

recurring itemsSubsidiaryBusiness Area

20

-137

58

24

37

1601)

SAS Cargo

STSSAS Aviation Services

Individually Branded Airlines

airBaltic

Blue1

Widerøe

Spanair

3rd Quarter

1) Denotes EBIT2) Denotes EBIT before nonrecurring items.

18SAS Group Q3 presentation

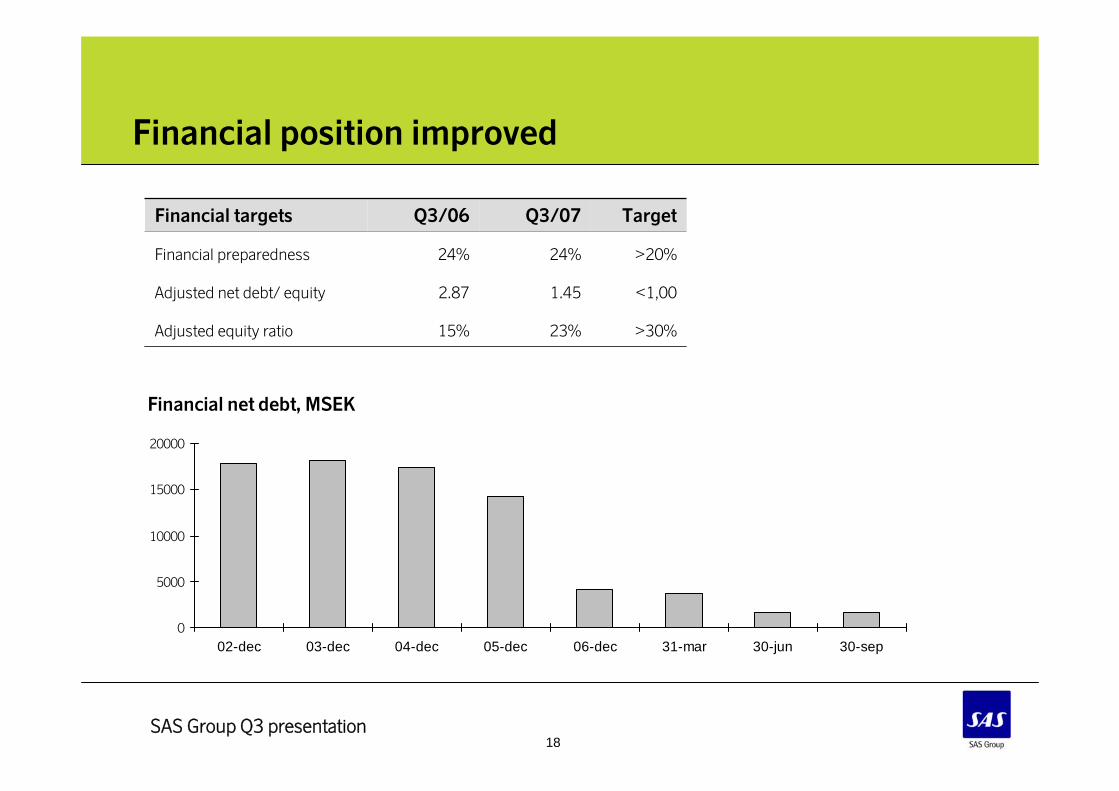

Financial position improved

Financial net debt, MSEK

0

5000

10000

15000

20000

02-dec 03-dec 04-dec 05-dec 06-dec 31-mar 30-jun 30-sep

15%

2.87

24%

Q3/06

23%

1.45

24%

Q3/07

Adjusted equity ratio

Adjusted net debt/ equity

Financial preparedness

Financial targets

>30%

<1,00

>20%

Target

19SAS Group Q3 presentation

Fuel cost expected to be SEK 10.5 billion in 2007- Ambition to offset even 2008 cost increase

Fuel prices at all time high in October 2007

Strategy to offset jet fuel priceHedging 40-60% of expected consumption (12 months rolling)Yield management Cost initiatives

Current hedges44% Oct 07 – Sep 08 CAP at 722 USD/MT

– Of which appr. 10 p.u. with swaps at 700 USD/MT

49% hedged during 4th Quarter 2007 at 708 USD/MT

0

100

200

300

400

500

600

700

800

900

jan-99

maj-9

9se

p-99

jan-00

maj-0

0se

p-00

jan-01

maj-0

1se

p-01

jan-02

maj-0

2se

p-02

jan-03

maj-0

3se

p-03

jan-04

maj-0

4se

p-04

jan-05

maj-0

5se

p-05

jan-06

maj-0

6se

p-06

jan-07

maj-0

7se

p-07

20SAS Group Q3 presentation

Sum up 3rd Quarter

Ongoing activitiesOngoing activities Strategy 2011 under implementationCost measures of SEK 2.8bn in process

Strategy 2011 under implementationCost measures of SEK 2.8bn in process

Key DriversKey Drivers

Strong market growthStable loadPositive yieldCost & capacity control

Strong market growthStable loadPositive yieldCost & capacity control

20072007Currently no clear signs of weaker marketQ400 to affect full year negative by 600-700 MSEK

Currently no clear signs of weaker marketQ400 to affect full year negative by 600-700 MSEK

22SAS Group Q3 presentation

Appendices

23SAS Group Q3 presentation

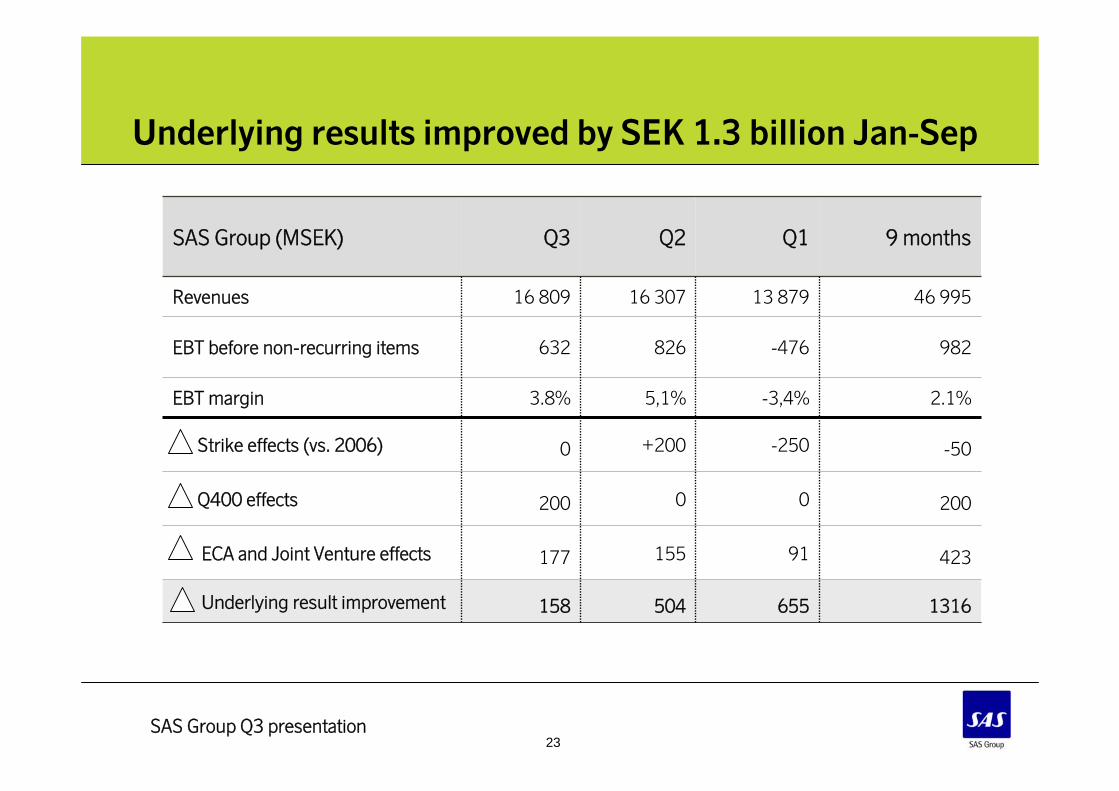

Underlying results improved by SEK 1.3 billion Jan-Sep

-50-250+2000Strike effects (vs. 2006)

42391155177ECA and Joint Venture effects

2.1%-3,4%5,1%3.8%EBT margin

1316655504158Underlying result improvement

20000200Q400 effects

632

16 809

Q3

-476

13 879

Q1

982

46 995

9 months

826

16 307

Q2

EBT before non-recurring items

Revenues

SAS Group (MSEK)

24SAS Group Q3 presentation

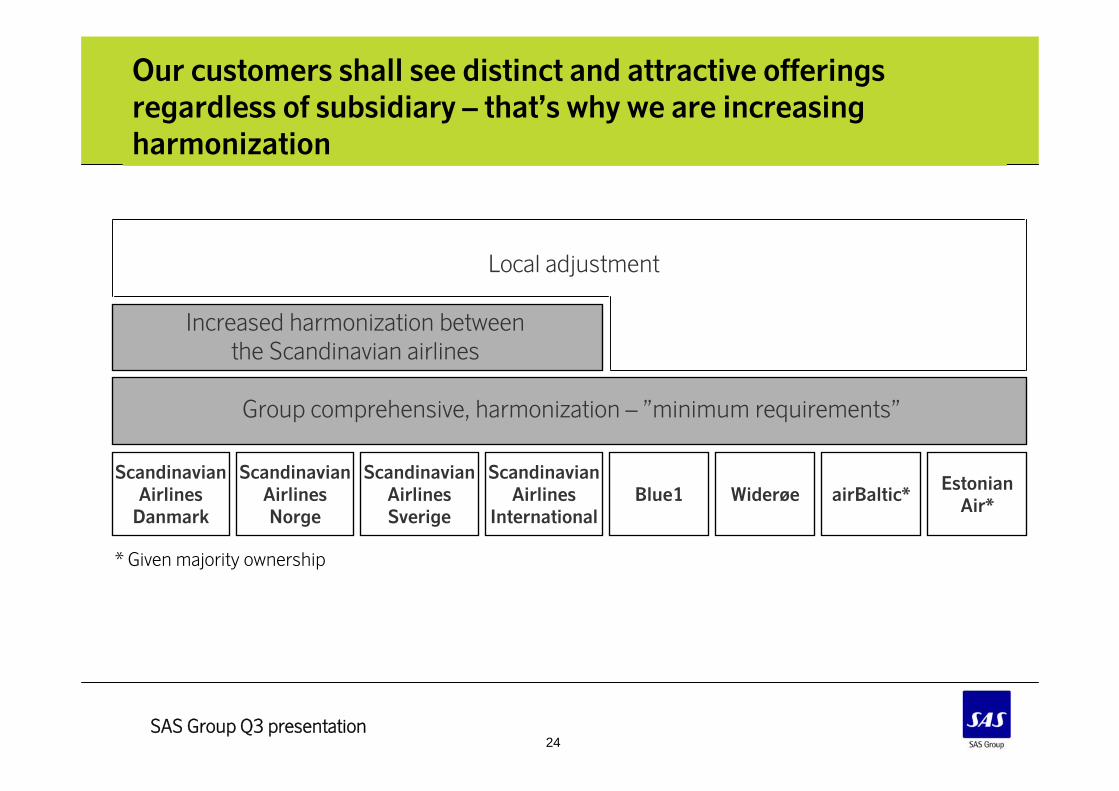

Our customers shall see distinct and attractive offerings regardless of subsidiary – that’s why we are increasing harmonization

Scandinavian Airlines

Danmark

Scandinavian AirlinesNorge

Scandinavian AirlinesSverige

Scandinavian Airlines

InternationalBlue1 Widerøe airBaltic*

Estonian Air*

Increased harmonization between the Scandinavian airlines

Local adjustment

Group comprehensive, harmonization – ”minimum requirements”

* Given majority ownership

25SAS Group Q3 presentation

More streamlined group structure after sale of Flight Academy and Newco

Scandinavian Airlines Norge

Scandinavian Airlines Danmark

Scandinavian Airlines Sverige

Scandinavian Airlines International

Spanair

Widerøe

Blue1

airBaltic

SAS Ground Services

SAS Technical Services

SAS Cargo

Strategic affiliated company: Estonian Air

26SAS Group Q3 presentation

SAS Aviation Services

SAS Scandinavian Airlines

SAS Individually Branded Airlines

Revenues (SEK bn)

28,8 29,8

05

101520253035

Jan-Sep 06 Jan-Sep 07

Revenues (SEK bn)

13,4 14

0

5

10

15

Jan-Sep 06 Jan-Sep 07

Revenues (SEK bn)

10,6 10,5

0

5

10

15

Jan-Sep 06 Jan-Sep 07

Group Revenue distribution

Revenues growing the airline business areasRevenues growing in the airline business areas

27SAS Group Q3 presentation

SAS Group’s seasonal pattern

SAS Group Revenues (per month)

jan feb mar apr maj jun jul aug sep okt nov dec

2004

2005

2006

2007

28SAS Group Q3 presentation

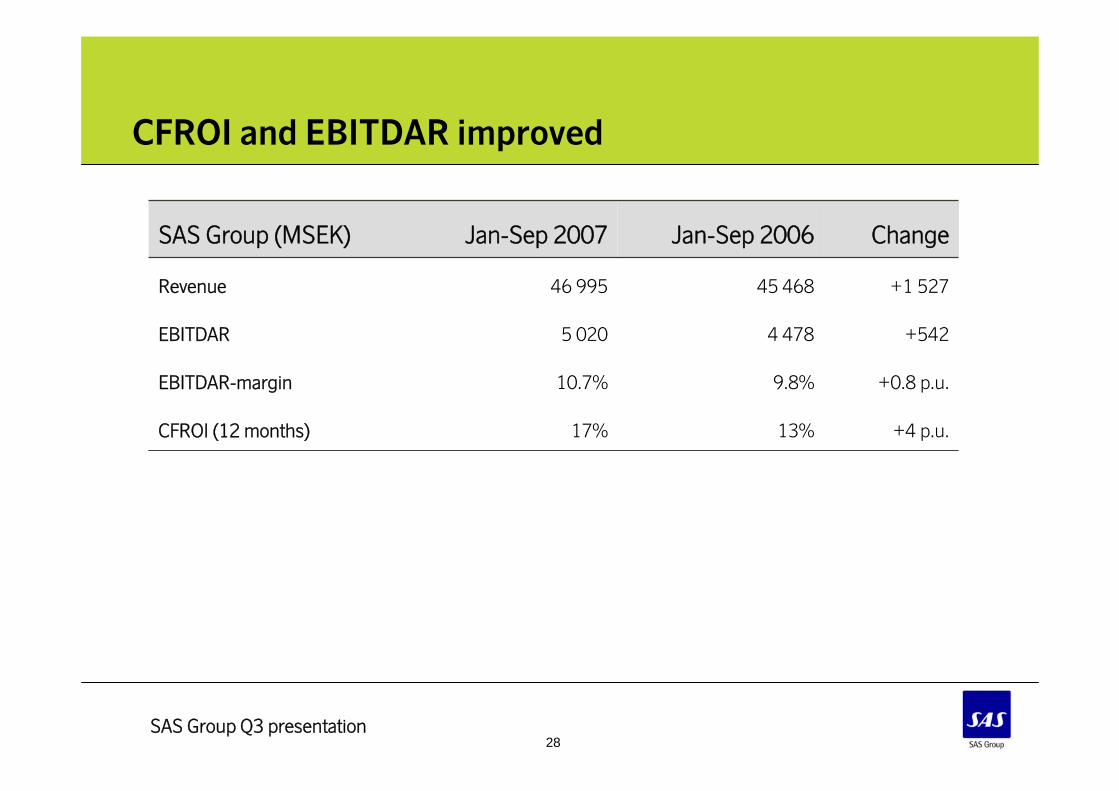

CFROI and EBITDAR improved

13%

9.8%

4 478

45 468

Jan-Sep 2006

+4 p.u.17%CFROI (12 months)

+0.8 p.u.10.7%EBITDAR-margin

+5425 020EBITDAR

+1 52746 995Revenue

ChangeJan-Sep 2007SAS Group (MSEK)

29SAS Group Q3 presentation

After two strong quarters the third quarter is slightly weaker than previous years – due to Q400 incidents and ECA agreement

-1909

-13

11638

184

579 543

-1

677

852

558

826

632

-415

-1603

-320

-1312

-1290

-476

-2 500

-2 000

-1 500

-1 000

-500

0

500

1 000

Q1 Q2 Q3 Q4

2003 2004 2005 2006 2007

MSEK, EBT before gains and nonrecurring items

30SAS Group Q3 presentation

Positive trend in EBIT-margin and revenues

10 000

11 000

12 000

13 000

14 000

15 000

16 000

17 000

18 000

19 000

1Q 20

032Q

2003

3Q 20

034Q

2003

1Q 20

042Q

2004

3Q 20

044Q

2004

Q1 200

5Q2 2

005

Q3 200

5Q4 2

005

Q1 200

6Q2 2

006

Q3 200

6Q4 2

006

Q1 200

7Q2 2

007

Q3 200

7

-15,00%

-10,00%

-5,00%

0,00%

5,00%

10,00%

Revenues EBIT-margin

31SAS Group Q3 presentation

Growth in most group airlines

-10

0

10

20

30

40

50

airBalt

ic

Spana

irSAS Swed

en

SAS Grou

p

Widerøe

SAS Norw

ay

Blue1SAS D

enmark

SAS Inter

nationa

l

Passenger growth in Jan-Sep 2007 vs Jan-Sep 2006

31,2 million passengers in Jan-Sep

2007- new record

(%)

32SAS Group Q3 presentation

Jet fuel prices

433593Q1 2007

503510

674718

Q2 2007Q3 2007

651

568

399

282

233

245

297

USD/MT

1 988

1 980

Consumption (mMT)Year

2002

2003

2005

2004

2006

2001

2000

Average market prices on high jet fuel (2000-2007)

33SAS Group Q3 presentation

Overview of the SAS Group’s fuel hedging and expected cost 2008

0%0%0%7%3-Way

825Price, USD/MT

10%8%7%13%Swaps

718

20%

708

663

20%

Q1 2008

Price, USD/MT

0 Cost

Price, USD/MT

Strike price, USD/MT

Options

781

17%

705

713

15%

Q2 2008

702684

Q3 2008Q4 2007

800700

8%7%

751685

22%21%

SEK 13.5 bnSEK 13.0 bnSEK 12.5 bn1000 USD/MT

SEK 11.1 bn

SEK 8.9 bn

6.75 SEK/USD

800 USD/MT

600 USD/MT

Market price

SEK 11.5 bn

SEK 9.3 bn

7.00 SEK/USD6.50 SEK/USD

SEK 10.7 bn

SEK 8.6 bn

SAS Group’s jet fuel costs in 2008 (annual average values)

SAS Group’s jet fuel hedging portfolio

34SAS Group Q3 presentation

Business areas

SAS Scandinavian Airlines

36SAS Group Q3 presentation

Underlying improvement in Scandinavian Airlines despite Q400 incidents and ECA agreement

658

638

663

0

- 249

912

- 546

1 459

- 8 863

10 322

Jul-Sep2007

(MSEK)

564

579

719

1

- 295

982

- 522

1 504

- 8 551

10 055

Jul-Sep2006

(MSEK)

+94

+59

-56

-1

+46

-70

-24

-45

-312

+267

Change

+902

+917

+660

-24

+158

+582

-67

+650

-377

+1 027

Change

509

463

971

16

-902

1 801

- 1 566

3 367

- 25 433

28 799

Jan-Sep 2006

(MSEK)

1 411

1 380

1 631

-8

- 744

2 383

- 1 633

4 017

- 25 810

29 826

Jan-Sep 2007

(MSEK)

EBITDA

EBITDAR

SAS Scandinavian Airlines

EBT before nonrecurring items

EBIT

Income from sales/affiliated

Depreciation

EBT

Lease

Operating expenses

Revenues

37SAS Group Q3 presentation

EBITDAR in 3rd Quarter 1 459 MSEK

EBITDAR, SAS Scandinavian Airlines (MSEK)

-500

0

500

1 000

1 500

2 000

Q1 Q2 Q3 Q4

2002 2003 2004 2005 2006 2007

38SAS Group Q3 presentation

Positive result development in SAS Scandinavian Airlines

-600-400-200

0200400600800

Q42005

Q12006

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

SAS Danmark

0

200

400

600

800

1 000

1 200

Q42005

Q12006

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

SAS Norge

-200-100

0100200300400

Q42005

Q12006

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

SAS International

-400-200

0200400600800

1 000

Q42005

Q12006

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

SAS Sverige

EBT before nonrecurring items (12 months rolling)

39SAS Group Q3 presentation

Sweden above and Norway close to return targets

561

1 055

8 826

Jan-Sep

SAS Danmark

+572

+472

+732

Change

+336

+209

+455

Change

512

920

6 414

Jan-Sep

SAS Sweden

-55

-113

-223

Change

50

550

5 711

Jan-Sep

SAS International

857

1 616

9 966

Jan-Sep

SAS Norge

+694

+709

+600

Change

SK Results

EBT before nonrecurring items

(MSEK)

EBITDAR

Total Revenues

SAS Norge Jan-Sep 2007Strong yield and stable traffic development

– No of pass up 1.8%– Cabin factor up 0.5 p.u. to 70.4%– Yield up 9.6%– Unit cost up 1.8%

SAS Norge Jan-Sep 2007Strong yield and stable traffic development

– No of pass up 1.8%– Cabin factor up 0.5 p.u. to 70.4%– Yield up 9.6%– Unit cost up 1.8%

SAS Danmark Jan-Sep 2007Strong yield and unit cost perform.

– No of pass down 0.9%– Cabin factor down 1.2 p.u. to 71.7%– Yield up 5.8%– Unit cost down 6.2%

SAS Danmark Jan-Sep 2007Strong yield and unit cost perform.

– No of pass down 0.9%– Cabin factor down 1.2 p.u. to 71.7%– Yield up 5.8%– Unit cost down 6.2%

SAS Sverige Jan-Sep 2007Continued improved load

– No of pass up 6.7%– Cabin factor up 2.5 p.u. to 72.6%– Yield down 0.7%– Unit cost up 3.6%

SAS Sverige Jan-Sep 2007Continued improved load

– No of pass up 6.7%– Cabin factor up 2.5 p.u. to 72.6%– Yield down 0.7%– Unit cost up 3.6%

SAS International Jan-Sep 2007Challenging development

– Cabin factor at 82.9%– Yield up 5.0%– Unit cost up 2.1%

SAS Business Sleeper installed

SAS International Jan-Sep 2007Challenging development

– Cabin factor at 82.9%– Yield up 5.0%– Unit cost up 2.1%

SAS Business Sleeper installed

40SAS Group Q3 presentation

Most key airline profitability drivers improving

Traffic (RPK)Traffic (RPK)

Cabin FactorCabin Factor

Yields (RPK)Yields (RPK)

RASKRASK

2007 vs 2006 Jul-Sep

+1.0 p.u.

+7.5%

+2.7%

+3.5%

+1.5%

SAS Group

Scandinavian Airlines

Fuel adj. unit costFuel adj. unit cost

41SAS Group Q3 presentation

Yield up 8.5% in Jan-Sep 2007 in Scandinavian Airlines

1

1,1

1,2

1,3

1,4

dec-0

3mar-

04jun

-04se

p-04

dec-0

4mar-

05jun

-05se

p-05

dec-0

5mar-

06jun

-06se

p-06

dec-0

6mar-

07jun

-07se

p-07

42SAS Group Q3 presentation

North Atlantic cabin factor above AEA

Daily departures from Copenhagen

to New York, Washington DC,

Chicago, Seattle

Daily departures from Stockholm to

New York and Chicago

SK traffic up 6% in Q3 vs last year

-40

-30

-20

-10

0

10

20

30

1 5 9 13 17 21 25 29 33 37 41 45 49 1 5 9 13 17 21 25 29 33 37 41

%, RPK vs. Last year

%, Cabin factor

Week

65707580859095

Janu

aryMarc

hMay Ju

lySep

tembe

rNov

embe

rJa

nuary

March

May July

Septem

ber

Novem

ber

Janu

aryMarc

hMay Ju

lySep

tembe

r

SAS AEA

43SAS Group Q3 presentation

Solid performance on European routes

New Business Models a success– Cabin factor above AEA average since

September 2005

Strong performance on UK, Finland and

Switzerland

New non stop routes from Stockholm,

Copenhagen and Gothenburg during

2007– 12 new routes from Oslo in 2008

Traffic Jan-Sep 2007:– AEA traffic up 7.0%

– SAS traffic up 1.1%

-40-30-20-10

010203040

1 6

11

16

21

26

31

36

41

46

51 4 9

14

19

24

29

34

39

%, RPK vs. Last year

%, Cabin factor

45

55

65

75

Janu

aryMarc

hMay Ju

lySep

tembe

rNov

embe

rJa

nuary

March

May July

Septem

ber

Novem

ber

Janu

aryMarc

hMay Ju

lySep

tembe

r

SAS AEA

44SAS Group Q3 presentation

60

65

70

75

80

85

90

95

Januar

yM

arch May

July

Septem

berNove

mber

JanuaryM

arch

May

July

Septem

berNovem

berJa

nuaryM

arch

May

July

Septem

ber

SAS AEA

Copenhagen-Dubai and Stockholm-Bangkok introduced in October 2007

Scandinavian Airlines serving Bangkok, Beijing, Tokyo and Dubai

Stockholm-Beijing as from March 2007

Stockholm-Bangkok and Copenhagen-Dubai as from October 2007

New strategy on China successful – traffic up 49% vs last year on Beijing in Q3 with increased load factor

SK passenger load factor above AEA

Traffic in Jan-Sep 2007:– AEA traffic up 2,8%

– SAS traffic down 15% due to reduced capacity during

the summer program

-50

-40

-30

-20

-10

0

10

20

30

40

1 5 9

13

17

21

25

29

33

37

41

45

49 1 5 9

13

17

21

25

29

33

37

%, RPK vs. Last year

%, Cabin factor

Week

SAS Individually Branded Airlines

46SAS Group Q3 presentation

Weak quarter in SAS Individually Branded Airlines –mainly due to Spanair result

269

312

357

68

-76

365

-388

752

-4 623

5 375

Jul-Sep2007

(MSEK)

349

349

392

29

-71

434

-375

809

- 4 396

5 204

Jul-Sep2006

(MSEK)

-80

-37

-35

+39

-5

-69

-13

-57

-227

+171

Change

-46

-4

17

59

-3

-39

19

-59

-658

599

Change

212

212

326

54

-218

490

-1 128

1 619

- 11 776

13 395

Jan-Sep 2006 (MSEK)

166

208

343

113

-221

451

-1 109

1 560

- 12 434

13 994

Jan-Sep 2007

(MSEK)

EBITDA

EBITDAR

SAS Individually Branded AirlinesResult

EBT before nonrecurring items

EBIT

Income from sales/affiliated

Depreciation

EBT

Lease

Operating expenses

Revenues

47SAS Group Q3 presentation

Spanair result weaker due to phasing out aircraft, strong improvement for Widerøe and Blue1

150

349

2 252

Jan-Sep

Widerøe

+146

+140

+49

Change

+116

+97

+19

Change

80

190

1 492

Jan-Sep

Blue1

+24

+85

+439

Change

68

250

1591

Jan-Sep

airBaltic

-91 (EBIT)

762

8 645

Jan-Sep

Spanair

-363

-416

+82

Change

SAS Individually Branded Airlines

EBT before nonrecurring items

Results (MSEK)

EBITDAR

Total Revenues

Spanair Jan-Sep 2007Strong growth, but tough market

– No of pass up 16.1%– Cabin factor up 0.5 p.u. to 69.0%– Yield down 8% due to labor conflicts and increased

competition

Spanair Jan-Sep 2007Strong growth, but tough market

– No of pass up 16.1%– Cabin factor up 0.5 p.u. to 69.0%– Yield down 8% due to labor conflicts and increased

competition

Widerøe Jan-Sep 2007Best Jan-Sep ever

No of pass up 2.7%– Cabin factor up 3.0 p.u. to 59.9%– Yield up 2.0%

Widerøe Jan-Sep 2007Best Jan-Sep ever

No of pass up 2.7%– Cabin factor up 3.0 p.u. to 59.9%– Yield up 2.0%

Blue1 Jan-Sep 2007Strongly improved result

– No of pass on same level as last year– Cabin factor up 1.3 p.u. to 68.3%– Yield down 5.2%– Unit cost down

Blue1 Jan-Sep 2007Strongly improved result

– No of pass on same level as last year– Cabin factor up 1.3 p.u. to 68.3%– Yield down 5.2%– Unit cost down

airBaltic Jan-Sep 2007Strong growth

– No of pass up 39%– Cabin factor up 1.5 p.u. to 64.5%– Yield down 11% mainly due to longer routes

airBaltic Jan-Sep 2007Strong growth

– No of pass up 39%– Cabin factor up 1.5 p.u. to 64.5%– Yield down 11% mainly due to longer routes

48SAS Group Q3 presentation

Estonian Air’s growth increasing

The SAS Group holds 49% in Estonian Air

Estonian Air number of passengers up 4% in 2007 and 11% in Q3 – Growth has increased due to increased fleet

Competitive cost position

Increased charter operation

Number of passengers Estonian Air

010 00020 00030 00040 00050 00060 00070 00080 00090 000

Dec Mar Jun

Sep Dec Mar Jun

Sep Dec Mar Jun

Sep Dec Mar Jun

Sep Dec Mar Jun

12 month rolling Monthly figures

SAS Aviation Services

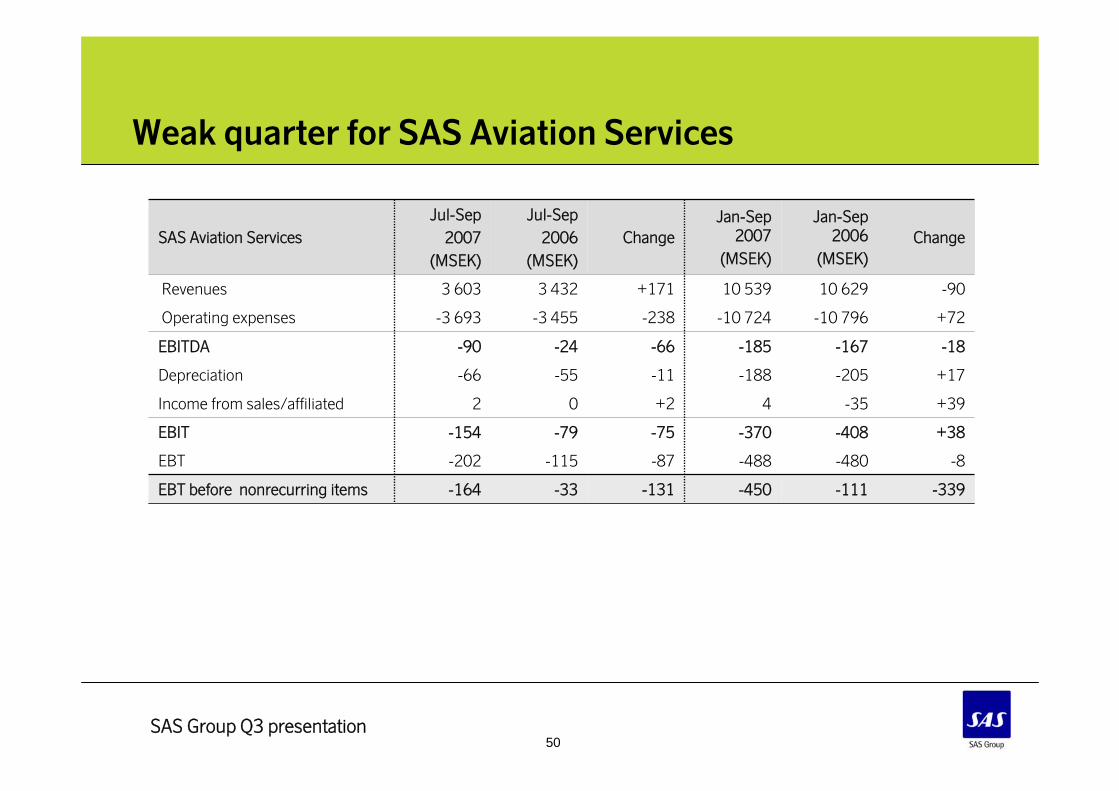

50SAS Group Q3 presentation

Weak quarter for SAS Aviation Services

-164

-202

-154

2

-66

-90

-3 693

3 603

Jul-Sep2007

(MSEK)

-33

-115

-79

0

-55

-24

-3 455

3 432

Jul-Sep2006

(MSEK)

-131

-87

-75

+2

-11

-66

-238

+171

Change

-339

-8

+38

+39

+17

-18

+72

-90

Change

-111

-480

-408

-35

-205

-167

-10 796

10 629

Jan-Sep 2006

(MSEK)

-450

-488

-370

4

-188

-185

-10 724

10 539

Jan-Sep 2007

(MSEK)

EBITDA

SAS Aviation Services

EBT before nonrecurring items

EBIT

Income from sales/affiliated

Depreciation

EBT

Operating expenses

Revenues

51SAS Group Q3 presentation

Breakdown SAS Aviation Services

-82-69664 464SAS Ground Services

-177

4

Change

-12

-369

Jan-Sep 2007

EBT before nonrec. itemsRevenues

ChangeJan-Sep 2007SAS Aviation Services

-58

-234

2 483

3 649

SAS Cargo

SAS Technical Services

Financial update

53SAS Group Q3 presentation

SAS Group Balance Sheet

4 134

51 164

16 338

3 473

16 528

14 825

51 164

27 648

12 713

10 803

Dec 31, 2006

17 211Equity

3 789Deferred tax

29 403Other assets

1 618

50 737

12 301

17 436

50 737

12 420

8 914

Sep 30, 2007

Total assets

SAS Group Balance Sheet

Financial net debt

Total liabilities and equity

Interest-bearing liabilities

Operating liabilities

Aircraft, spare parts

Liquid funds

54SAS Group Q3 presentation

CAPEX

Other investments approximately MSEK 1 500 /year

Above orders, planned to be financed through sale and leaseback

26

2008

66

2

2

2009

24

1

1

2007

( remaining part)

116CAPEX

3

2

1

Total

Boeing 737-800 (NG)

Number of aircraft

Firm Aircraft Orders

Airbus A319

55SAS Group Q3 presentation

The Revolving Credit Facility of MEUR 366 with maturity in June 2010 – Improved terms and conditions

New Revolving Credit Facility of MUSD 156 agreed in Q1 2007

SAS Group has more than SEK 15 bn in available funds

+5878 3278 914Liquid Funds

+1 01301 013Revolving Credit Facility (MUSD 156)

Available Credit Facilites:

Others

Bi-lateral Facilities

Revolving Credit Facility (MEUR 366)

14 208

5 881

674

1 500

3 707

Sep 06

+1476 028Total Available Facilities

+73414 942Total Available Funds

644

1 000

3 371

Sep 07

-500

- 30

-336

ChangeAvailable Funds MSEK

6 946

1 065

5 881

- 836229Utilized facilities

-6896 257Total facilities

6 028 +147Available facilities:

56SAS Group Q3 presentation

SAS Group CAPEX holiday continues

SAS Group total CAPEX

0

2000

4000

6000

8000

10000

12000

14000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

F20

08F

2009

FMSEK

57SAS Group Q3 presentation

Strong improvement in all key ratios in 2007

>30%15%23%Adjusted equity/assets ratio*

<100%168%145%Adjusted gearing**

Financial net debt/ equity

Equity/assets ratio (solidity)

Key figures

9%

34%

Sep 07

<50%

Target

25%

19%

Dec 06

Consolidation coming years

Low investments

Improved cash flow from operations

*Defined as:

**Defined as:

lease operating7assets totalequity∗+

equity

lease operating *7debtnet financial +

58SAS Group Q3 presentation

Amortization profile of interest bearing liabilities- Reduced level in 2008

2 881

104

1 086

115130403

953856

4 625

528

-

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

2007 2008 2009 2010 2011 2012 2013 2014 2015 >2015

Oct-Dec

59SAS Group Q3 presentation

Development of Financial Net Debt January – September 2007

-77Deconsolidation, currency & other

-1 618Financial Net Debt Sep 07

+475Sale of subsidiaries, net

+2 618Cash flow from operating activities

-4 134Financial net debt Dec 06

Investments

Sale of aircraft and properties

Financial Net Debt

-1 879

+1 379

Sep 2007

60SAS Group Q3 presentation

SAS Group Financial Net

-859

+12

-871

Oct 2005-Sep 2006

+284

-19

+303

Difference

-575

-7

-568

Oct 2006-Sep 2007

Financial net

Exchange rate differences

Interest net and others

MSEK

Oct 2006-Sep 2007 vs. Oct 2005-Sep 2006

-704

+13

-717

Jan-Sep 30, 2006

+348

-7

+355

Difference

-356

+6

-362

Jan-Sep, 2007

Financial net

Exchange rate differences

Interest net and others

MSEK

Jan-Sep 2007 vs. Jan-Sep 2006

-256

+14

-270

Q3, 2006

+179

-20

+199

Difference

-77

-6

-71

Q3, 2007

Financial net

Exchange rate differences

Interest net and others

MSEK

Q3 2007 vs. Q3 2006

61SAS Group Q3 presentation

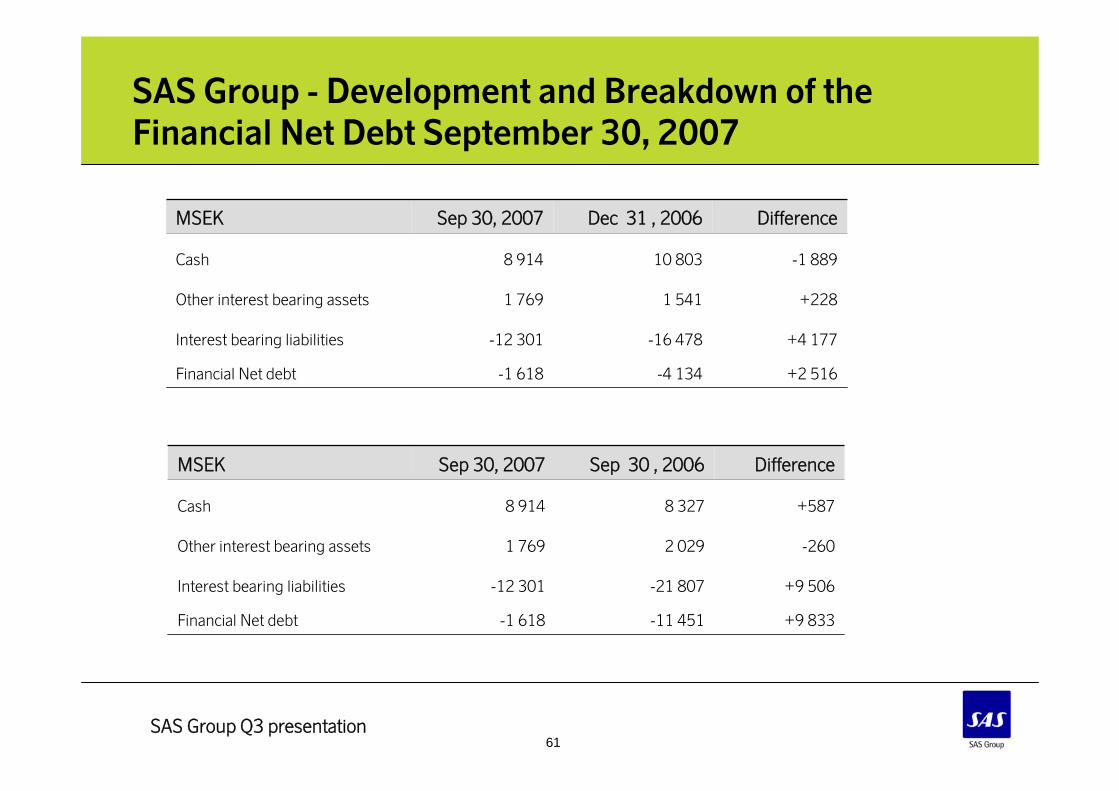

SAS Group - Development and Breakdown of the Financial Net Debt September 30, 2007

+4 177-16 478-12 301Interest bearing liabilities

+2281 5411 769Other interest bearing assets

-4 134

10 803

Dec 31 , 2006

-1 618

8 914

Sep 30, 2007

+2 516Financial Net debt

-1 889Cash

MSEK Difference

+9 506-21 807-12 301Interest bearing liabilities

-2602 0291 769Other interest bearing assets

-11 451

8 327

Sep 30 , 2006

-1 618

8 914

Sep 30, 2007

+9 833Financial Net debt

+587Cash

MSEK Difference

62SAS Group Q3 presentation

Development of the Financial Net Debt, reduced by more than SEK 15bn since peak levels

0

5 000

10 000

15 000

20 000

25 000

92-12 93-12 94-12 95-12 96-12 97-12 98-12 99-12 00-12 01-12 02-12 03-12 04-12 05-12 06-12

MS

EK

Average 93 15.900

Average 94 9.700

Average 95 4.950

Average 96 2.350

Average 97 2.150

Average 98 2.900

Average 99 6.750

Average 00 5.450

Average 01 9.150

Average 02 17.950

Average 03 19.100

Average 0418.600

Average 05 16.100

Average 0611.600

63SAS Group Q3 presentation

Development of the Equity/Asset ratio

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

199219931994199519961997199819992000200120022003200420052006

64SAS Group Q3 presentation

Financial Net Debt/Equity ratio development

0,0

0,3

0,5

0,8

1,0

1,3

1,5

1,8

2,0

2,3

2,5

199219931994199519961997199819992000200120022003200420052006

65SAS Group Q3 presentation

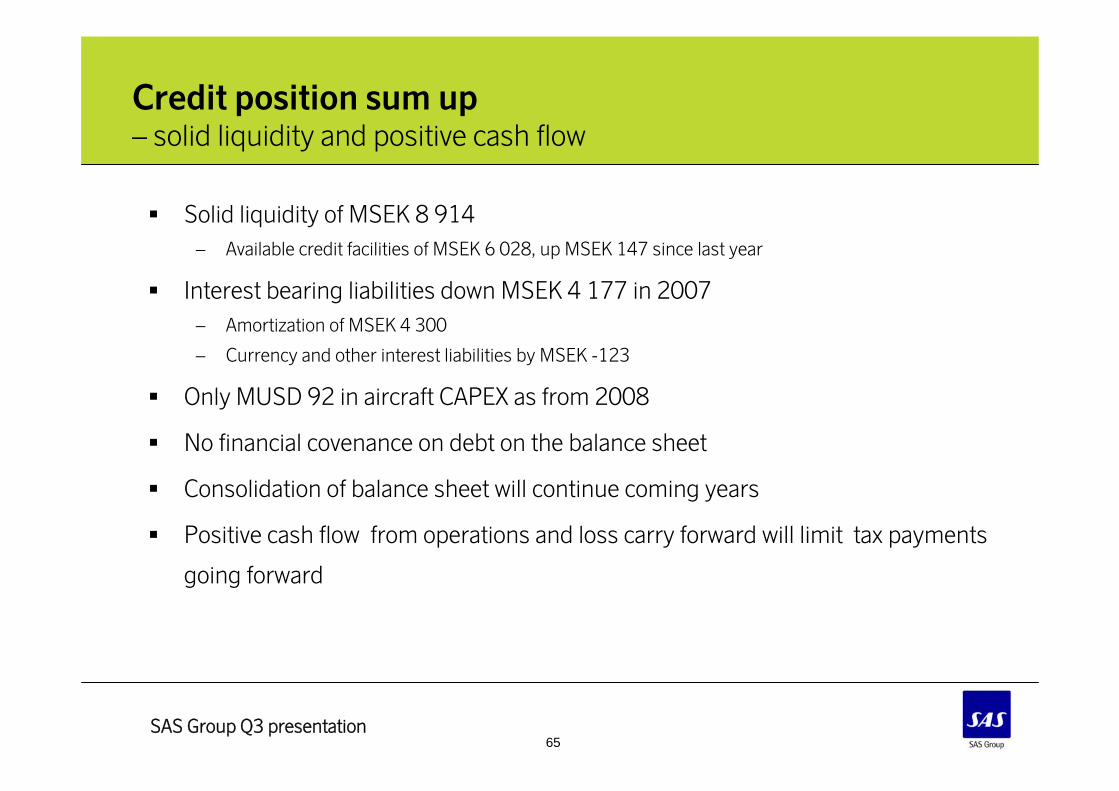

Credit position sum up – solid liquidity and positive cash flow

Solid liquidity of MSEK 8 914– Available credit facilities of MSEK 6 028, up MSEK 147 since last year

Interest bearing liabilities down MSEK 4 177 in 2007– Amortization of MSEK 4 300

– Currency and other interest liabilities by MSEK -123

Only MUSD 92 in aircraft CAPEX as from 2008

No financial covenance on debt on the balance sheet

Consolidation of balance sheet will continue coming years

Positive cash flow from operations and loss carry forward will limit tax payments

going forward

66SAS Group Q3 presentation

APPENDICES

Capacity, fuel, and yield 2007

Traffic Data

Yield

Unit cost

Fleet

Financial key figures

67SAS Group Q3 presentation

2007 vs. 2006SAS Group

2007 vs. 2006SAS Scandinavian Airlines

2007 estimatesSAS Group

+2%Blue 1

+15%Spanair

- (4-5)%Widerøe

+40%airBaltic

+7 – 8%Scandinavian Airlines Sverige

-1%Scandinavian Airlines Norge

+1%Scandinavian Airlines Danmark

-6%Scandinavian Airlines International

Flat/slightly positiveLoad factor

-1%ASK

Positive 1st Half, Stable 2nd Half Yield

Flat/slightly positiveLoad factor

up 4-6%ASK

Capacity, fuel, yield and load factor

The grounding of Q400 is expected to be offset by leased in capacity

68SAS Group Q3 presentation

Yield development

2.7%105.1108.0Currency adj. yield

105.4

Jul-Sep 2006

108.0

Jul-Sep 2007

2.5%Yield (öre/RPK)

MSEK Change

Yield, SAS Scandinavian Airlines

-0.9%

-12.0%

-11.3%

-3.1%

Jul-Sep 2007Yield, local currency

Yield, SAS Individually Branded Airlines

8.5%109.4118.7Currency adj. yield

111.6

Jan-Sep 2006

118.7

Jan-Sep 2007

6.4%Yield (öre/RPK)

MSEK Change

+2.0%

-8.2%

-11.2%

-5.2%

Jan-Sep 2007Yield, local currency

69SAS Group Q3 presentation

Improved yield and load factor

40%

50%

60%

70%

80%

03-no

v04

-feb

04-m

aj04

-aug

04-no

v05

-feb

05-m

ay05

-aug

05-no

v06

-feb

may-06

06-au

go6

-nov

07-fe

b07

-maj

07-au

g

1,00

1,05

1,10

1,15

1,20

1,25

1,30

Load factor Yield (12 months rolling)

SAS Scandinavian Airlines

70SAS Group Q3 presentation

Yield development – SAS Scandinavian Airlines

-20

-15

-10

-5

0

5

10

15

20

Q1vs

2003

Q2 Q3 Q4 Q1vs

2004

Q2 Q3 Q4 Q1vs

2005

Q2 Q3 Q4 Q1vs

2006

Q2 Q3

Yields down 9.1% in 2004

Yields down 0.3 in 2005

Yield up 1.2% in Q1 2006

Yield up 1.9% in Q2 2006

Yield up 9.2% in Q3 2006

Yield up 15.4% in Q4 2006

Yield up 16.0% in Q1 2007

Yield up 8.3% in Q2 2007

Yield up 2.7 in Q3 2007

71SAS Group Q3 presentation

Break down of SAS Scandinavian Airlines Unit Cost Jul-Sep 2007

-8 392

-467

-7 925

-703

-990

-1 232

-134

-959

-1 871

-2 036

Jul-Sep 07

-0,4%-6,4%-499Aircraft costs

1,5%14,5%-864Technical

-0,1%-0,4%-1 237Ground Services

2,0%

2,6%

-16,1%

-1,9%

3,7%

2,4%

7,3%

Var %

2,0%

2,4%

-1,6%

0,0%

0,4%

0,5%

1,7%

Share of total var%

-7 725TOTAL OPERATING EXPENSES

-1 828Fuel

-1 897Personnel

-137Selling cost

-924Gov. Charges

-8 225ADJUSTED EBIT

-837

Jul-Sep 06

Other operating costs

Cost break down

Cost break down, volume, currency and method adjusted SAS Scandinavian Airlines

72SAS Group Q3 presentation

Break down of SAS Scandinavian Airlines Unit Cost Jan-Sep 2007

-24 924

-1 397

-23 527

-2 516

-2 930

-3 706

-390

-2 716

-5 092

-6 177

Jan-Sep 07

-0,3%-5,7%-1 481Aircraft costs

0,4%3,3%-2 837Technical

0,0%0,0%-3 705Ground Services

2,3%

2,9%

-9,5%

-2,1%

3,0%

7,2%

7,1%

Var %

2,3%

2,7%

-1,1%

0,0%

0,3%

1,4%

1,7%

Share of total var%

-22 874TOTAL OPERATING EXPENSES

-4 752Fuel

-5 766Personnel

-398Selling cost

-2 636Gov. Charges

-24 356ADJUSTED EBIT

-2 779

Jan-Sep 06

Other operating costs

Cost break down

Cost break down, volume, currency and method adjusted SAS Scandinavian Airlines

73SAS Group Q3 presentation

Unit cost slightly up in Q3 2007

-22%

-17%

-12%

-7%

-2%

3%

8%

1st

Q 2

00

3

2n

d Q

20

03

3rd

Q 2

00

3

4th

Q 2

00

3

1st

Q 2

00

4

2n

d Q

20

04

3rd

Q 2

00

4

4th

Q 2

00

4

1st

Q 2

00

5

2n

d Q

20

05

3rd

Q 2

00

5

4th

Q 2

00

5

1st

Q 2

00

6

2n

d Q

20

06

3rd

Q 2

00

6

4th

Q 2

00

6

1st

Q 2

00

7

2n

d Q

20

07

3rd

Q 2

00

7

SAS Scandinavian Airlines unit cost change

Unit cost down 10.9% in 2004Unit cost down 1.7% in 2005Unit cost up 5.2% in 2006Unit cost up 2.1% in Q1 2007

– Adjusted for fuel, unit cost was down 0.2%

Unit cost up 2.9% in Q2 2007– Adjusted for fuel, unit cost was up 1.5%

Unit cost up 2.0% in Q3 2007– Adjusted for fuel, unit cost was up 1.5%

74SAS Group Q3 presentation

Productivity

7828098,25airBaltic

699

417

615

Cabin

hours/year

5748,07SAS Scandinavian Airlines

6618,58Blue1

4326,62Widerøe

Pilots

hours/year

Aircraft

hours/day

12 months rolling

Block hours, 12 months rolling, Oct 06 - Sep 07

75SAS Group Q3 presentation

Key productivity ratios – SAS Scandinavian Airlines

Aircraft utilization (12 months roling)

5

5,5

6

6,5

7

7,5

8

8,5

DecApr Aug DecApr Aug DecApr Aug DecApr Aug

Cabin, pilot utilization (12 month roling)

420

470

520

570

620

670

Dec Mar Jun

Sep Dec Mar Jun

Sep Dec Mar Jun

Sep Dec Mar Jun

Sep

Pilots Cabin crew

76SAS Group Q3 presentation

Self Service check in above 50% Internet check in over 5%

20%

25%

30%

35%

40%

45%

50%

55%

200211200303200307200311200403200407200411200503200507200511200603200607200611200703200707

Automat Automat+internet

77SAS Group Q3 presentation

Long term passenger cabin factor trend positive

50%

55%

60%

65%

70%

75%

80%

DEC94 DEC95 DEC96 DEC97 DEC98 DEC99 DEC00 DEC01 DEC02 DEC03 DEC04 DEC05 DEC06 DEC07

78SAS Group Q3 presentation

Continued weak USD in 2007

6

7

8

9

10

11

12

20032002200120002004200520062007

79SAS Group Q3 presentation

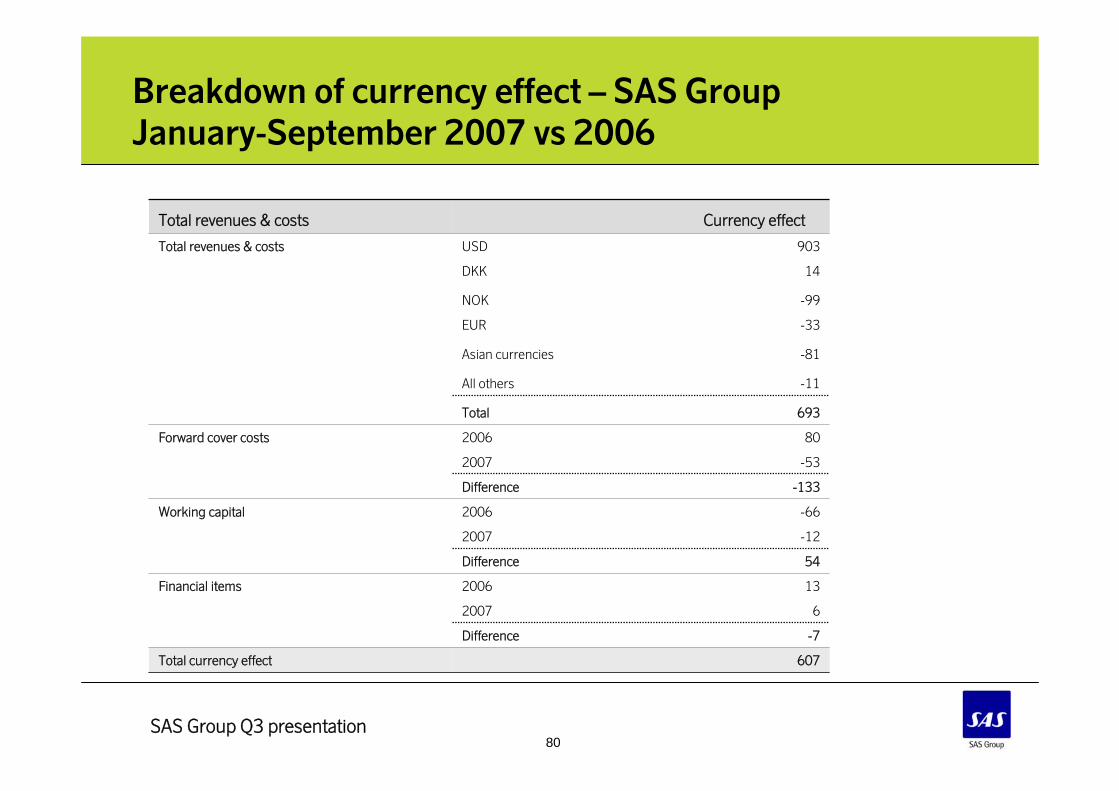

Currency effect – SAS GroupJanuary-September 2007 vs 2006

607Income before tax

-7Financial items

614

-79

1 500

-807

Jan-Sep 2007

Total costs

Total revenues

Income before depreciation

Forward cover costs & working cap

MSEK

80SAS Group Q3 presentation

Breakdown of currency effect – SAS GroupJanuary-September 2007 vs 2006

-7Difference

132006Financial items

-662006Working capital

-122007

802006Forward cover costs

-532007

-11All others

-81Asian currencies

693Total

Total currency effect

Total revenues & costs

Total revenues & costs

-99NOK

-33EUR

607

62007

54

-133

14

903

Currency effect

DKK

USD

Difference

Difference

81SAS Group Q3 presentation

Breakdown of currency effect – SAS GroupJuly-September 2007 vs 2006

-20Difference

142006Financial items

-632006Working capital

172007

342006Forward cover costs

-852007

2All others

-16Asian currencies

243Total

Total currency effect

Total revenues & costs

Total revenues & costs

13NOK

6EUR

184

-62007

80

-119

0

238

Currency effect

DKK

USD

Difference

Difference

82SAS Group Q3 presentation

Currency distribution in the SAS Group 2006

Expenses

DKK13%

EUR18%

GBP3%

NOK19%

SEK15%

USD30%

Others2%

Revenues

DKK11%

EUR26%

GBP5%

NOK29%

SEK18%

USD6%

Others5%

83SAS Group Q3 presentation

SAS Group fleet – September 2007

2812.7Wideroe

995.9Blue1

212115.2airBaltic

3930311.5Total

9

9

0

0

0

3

2

0

4

0

0

Leased out

47

198

303

52

14

9

8

79

7

90

33

11

Total

68

18

0

0

8

13

0

20

4

5

Owned

47

235

34

14

9

0

66

7

70

29

6

Leased

010.7Douglas MD-90-series

05.9Avro RJ-85/100

09.7deHavilland Q-series

017.9Fokker F50

018.2Douglas MD-80-series

311.2SAS Scandinavian Airlines

11.3Spanair

311.5Totalt

Boeing 717 (MD-95)

Boeing 737-series

Airbus A321/A320/A319

Airbus A330/A340

SAS Group fleet

29.7

07.1

1

0

On order

4.7

5.3

Average age

84SAS Group Q3 presentation

SAS share

85SAS Group Q3 presentation

Development of the SAS Group’s Market Capitalization

0

5 000

10 000

15 000

20 000

25 000

30 000

jan-05

maj-05

sep-05

jan-06

maj-06

sep-06

jan-07

maj-07

sep-07

86SAS Group Q3 presentation

SAS Share vs Peers Index

80,0

120,0

160,0

200,0

240,0

280,0

320,0

dec-04

mar-05

jun-05se

p-05

dec-05

mar-06

jun-06se

p-06dec

-06mar-

07

jun-07

Peers SAS

SAS Market Capitalization vs. European Peers measured in SEK(December 31, 2004 - September 30, 2007)

192.5

167.3

87SAS Group Q3 presentation

Volume of traded shares in balance after very active summer

Number of traded shares, SAS Group Jan 2005 – Sep 2007

0

5 000 000

10 000 000

15 000 000

20 000 000

25 000 000

30 000 000

Jan

Feb Mar Apr

May Jun Jul

Aug

Sep Oct

Nov

Dec

2005 2006 2007