sas credit scoring in-house scorecard … formação sas oferta para 2003 author jos van der velden...

TRANSCRIPT

Copyright © 2003, SAS Institute Inc. All rights reserved.

SAS Credit ScoringIn-House Scorecard Development Project

Helena Junqueiro PM CRM Solutions & Data Mining, SAS PortugalHendrik Wagner, PM Data Mining Solutions, SAS EMEA

Copyright © 2003, SAS Institute Inc. All rights reserved.

SAS Credit ScoringHendrik Wagner, PM Data Mining Solutions, SAS EMEA

Copyright © 2003, SAS Institute Inc. All rights reserved. 3

SAS Credit Scoring

! Credit Risk Data Mart

! In-house Scorecard Development Environment

! Scorecard Monitoring Reports

! Interfaces to Operational Systems

! Efficient Knowledge Transfer

Copyright © 2003, SAS Institute Inc. All rights reserved. 4

Benefits of in-housescorecard development! Faster

! Cheaper

! More flexible

! More accurate

! More secure

! Basel compliant

! Reusable skills

! Better monitoring

Copyright © 2003, SAS Institute Inc. All rights reserved. 5

Capabilities for Basel

! Development of rating models

! Individual PD from statistical models

! Definition of rating grades and pools

! LGD and EAD estimation

! Proof of risk differentiation

! Recognition of all factors

! Representative samples

Copyright © 2003, SAS Institute Inc. All rights reserved. 6

Capabilities for Basel

! Documentation through process flow diagrams

! Transparent / Robust

! Data management processes� Data Access and Collection� Reporting Data Mart � Scorecard Development Data Mart

! Scorecard development processes

Copyright © 2003, SAS Institute Inc. All rights reserved. 7

SAS Risk Management Solutions

Copyright © 2003, SAS Institute Inc. All rights reserved.

In-House Scorecard Development Project

Helena JunqueiroCRM Solutions & Data Mining Product ManagerSAS Portugal

Copyright © 2003, SAS Institute Inc. All rights reserved. 9

Company Details

� It�s a finance company established in 1991

� Specialized in credit card management

� SAS customer since 1998 with Statistical Package

� Belongs to one of largest Portuguese financial group

� Average Market Share 17%

� SAS customer since April 1996

� Is established since XIX century (1880)

� Major activities: Banking, Leasing, Consumer Credit, Insurance, Brokerage, Asset Management, e-business, Factoring, Venture Capital

Copyright © 2003, SAS Institute Inc. All rights reserved. 10

Business Pain� Keep growing the market penetration rates� Internal costs� Lack of knowledge on their data� Unable to have behaviour scoring framework� Dependence of a credit scoring company�s outsource

(implementation / developing)

Copyright © 2003, SAS Institute Inc. All rights reserved. 11

Project Methodology:

! Phase 1: Defining the scope

! Phase 2: Making data available (data mart)

! Phase 3: Evaluating the environment for modeling

! Phase 4: Model development

! Phase 5: Model deployment

! Phase 6: Performance monitoring

Copyright © 2003, SAS Institute Inc. All rights reserved. 12

Project Methodology:

! Phase 1: Defining the scope! Phase 2: Making data available (data mart)

! Phase 3: Evaluating the environment for modeling

! Phase 4: Model development

! Phase 5: Model deployment

! Phase 6: Performance monitoring

Copyright © 2003, SAS Institute Inc. All rights reserved. 13

Phase 1: Defining the Scope

� Build a behaviour credit card model to assign a credit card limit

� Automating the decision process on accepting or rejecting credit cards on giving credit card limits

Copyright © 2003, SAS Institute Inc. All rights reserved. 14

Project Methodology:

! Phase 1: Defining the scope

! Phase 2: Making data available (data mart)! Phase 3: Evaluating the environment for modeling

! Phase 4: Model development

! Phase 5: Model deployment

! Phase 6: Performance monitoring

Copyright © 2003, SAS Institute Inc. All rights reserved. 15

Phase 2: Data Mart! Developing the Data Mart using

SAS/Warehouse Administrator

! Duration 4 months : November 2002 - February 2003

! Advantages of using SAS/WA tool:� Process integration &

documentation � Process Automation� Flexible and adaptable for

incorporating business rules� � Cornerstone for every

successful Credit Scoring projects.

Copyright © 2003, SAS Institute Inc. All rights reserved. 16

Phase 2: Variables� Account Information (id, opening/cancellation date,�)

� Credit card Information ( type/brand, credit limit, number of credit cards, number of active/inactive,�)

� Payment behaviour information (number of times with 1,2,3,4 delays, total number of delays,�)

� Behaviour information:last purchase or cash advance date,

number/amount of transactions (national and foreign),number/amount of purchases (national and foreign),number/amount of cash advances (national and foreign)% of credit limit usage (Transactions amount/Credit limit)% of purchase usage ( Purchase Amount /Transactions amount)% of cash advance usage (Cash Advance Amount /Transactions amount)Monthly average Debt amount Average amount of Revolving ,�

Copyright © 2003, SAS Institute Inc. All rights reserved. 17

Phase 2: Variables

Customer Demographic information

� District code � Nationality � Customer type (emigrant, resident,�)� Marital status� Sex� Number of dependents� Residence status� Job situation� Age��

Relationship with the bank information

� Tenure at the bank� Default indicator on any other credit � Number of other products on bank � Average Balance � Net Indicator� Call Center Indicator

� Assets Amount� Liabilities Amount� Portfolio of equities (stocks) Amount��

Copyright © 2003, SAS Institute Inc. All rights reserved. 18

Project Methodology:

! Phase 1: Defining the scope

! Phase 2: Making data available (data mart)

! Phase 3: Evaluating the environment for modeling! Phase 4: Model development

! Phase 5: Model deployment

! Phase 6: Performance monitoring

Copyright © 2003, SAS Institute Inc. All rights reserved. 19

Phase 3: Evaluating the Environment for Modeling

Definitions:− Good/Bad Account definition

− Time Window

− Exclusions

− Countings

Copyright © 2003, SAS Institute Inc. All rights reserved. 20

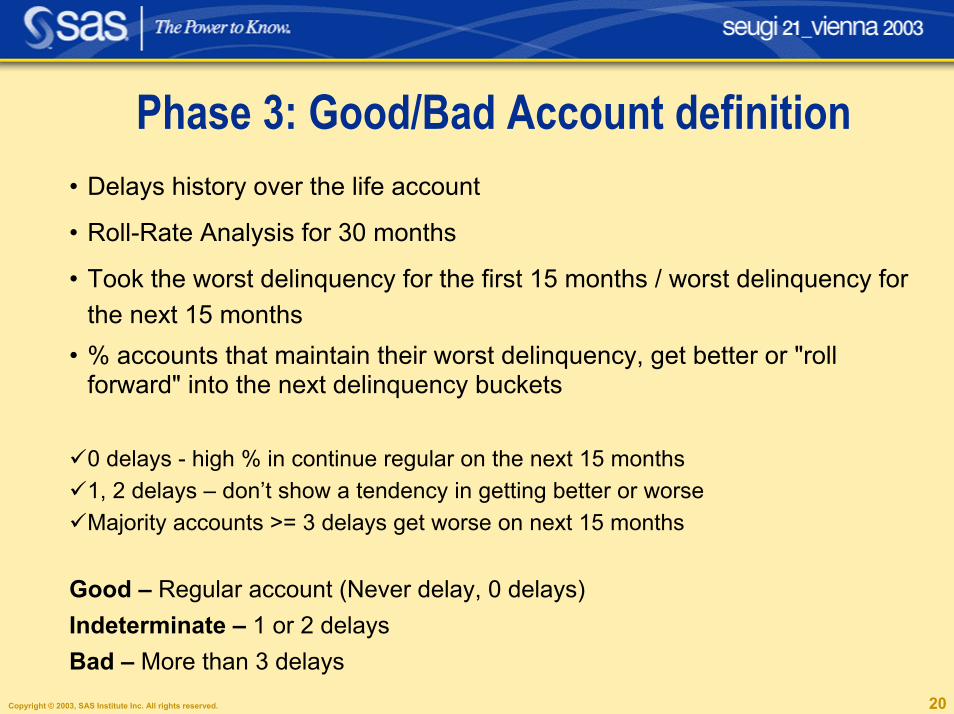

Phase 3: Good/Bad Account definition� Delays history over the life account

� Roll-Rate Analysis for 30 months

� Took the worst delinquency for the first 15 months / worst delinquency for the next 15 months

� % accounts that maintain their worst delinquency, get better or "roll forward" into the next delinquency buckets

"0 delays - high % in continue regular on the next 15 months"1, 2 delays � don�t show a tendency in getting better or worse"Majority accounts >= 3 delays get worse on next 15 months

Good � Regular account (Never delay, 0 delays)Indeterminate � 1 or 2 delays Bad � More than 3 delays

Copyright © 2003, SAS Institute Inc. All rights reserved. 21

Phase 3: Time Window

Observation Point

12 months

Behaviour Period

Jan 2001 � Dec 2001

Result Point

12 months

Results Period

Jan 2002 � Dec 2002

Copyright © 2003, SAS Institute Inc. All rights reserved. 22

Phase 3: ExclusionsSecure that� Only have individual credit cards

−not include corporate credit cards, non customers credit cards, internet credit cards, student university credit cards

� Life accounts on the considered time window

� Account cancellations on the behaviour period not included

� Write-offs not included

Result PointObservation Point

12 months

12 months

Behaviour Period

Jan 2001 � Dec 2001

Results Period

Jan 2002 � Dec 2002

Copyright © 2003, SAS Institute Inc. All rights reserved. 23

Phase 3: Countings

Good73%

Bad4%

Indeterminate13%

Inactive (1)10%

Candidates40%

TOTALACCOUNTS

100%

60%Exclusions

Bad Rate 5 %(1) Inactive � Accounts without transactions on the behaviour period (12 months)

Copyright © 2003, SAS Institute Inc. All rights reserved. 24

Project Methodology:

! Phase 1: Defining the scope

! Phase 2: Making data available (data mart)

! Phase 3: Evaluating the environment for modeling

! Phase 4: Model development! Phase 5: Model deployment

! Phase 6: Performance monitoring

Copyright © 2003, SAS Institute Inc. All rights reserved. 25

Phase 4: Modeling

� Finally using SAS/Enterprise Miner� Have a proportion of 5% bad and 95% good credit

accounts� Stratified (on target) Sampling of 30 000 accounts− Classing using Interactive Grouping Node (IGN) on this 30 000 accounts

Copyright © 2003, SAS Institute Inc. All rights reserved. 26

Phase 4: Classing using IGNThe process of automatically and/or interactively binning and grouping interval, nominal or ordinal input variables in order to

� manage the number of attributes per characteristic (variable)� improve the predictive power of the characteristic� select predictive characteristics� make the Weights Of Evidence vary smoothly or even linearly across the

attributes

WeightOfEvidence attribute= log(p_good attribute / p_bad attribute),where p_good attribute= #good attribute/ # good

p_bad attribute= # bad attribute/ # bad

The Information Value is a measure of the predictive power of a characteristic. It is used to

� judge the appropriateness of the classing � select predictive characteristics

The IV is similar to an entropy:IV= Σ ( (p_good attribute - p_bad attribute )*woe attribute )

Copyright © 2003, SAS Institute Inc. All rights reserved. 27

Phase 4: Example: Age

High RiskLow Risk

Copyright © 2003, SAS Institute Inc. All rights reserved. 28

Phase 4: Modeling � Used some variable selection:

� Variable selection node� Tree node� PROC VARCLUS

� Running some Logistic Regressions with the WoEvariables− Used Stepwise / Backward− Used only the greater IV variables− Used variables chosen by the results of the Variable Selection Node− Used variables chosen by the results of the Tree Node− Used variables chosen by the results of Proc Varclus− Used variables chosen between business considerations and statistical issues

log(p_bad/ p_good) =-log(p_good/p_bad) =-log(odds) = age_woe * b age +status_woe * b car +�+a

Copyright © 2003, SAS Institute Inc. All rights reserved. 29

Phase 4: Modeling � Have to choose the model

− Compare them on Assessment node, ROC curve

20% Worst

ponctuation, 70%

bad accounts

ROC Curve

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%1-specificity

sens

itivi

ty

Modelo 2 - ROC=0.790 Modelo 1 - ROC=0.788

Copyright © 2003, SAS Institute Inc. All rights reserved. 30

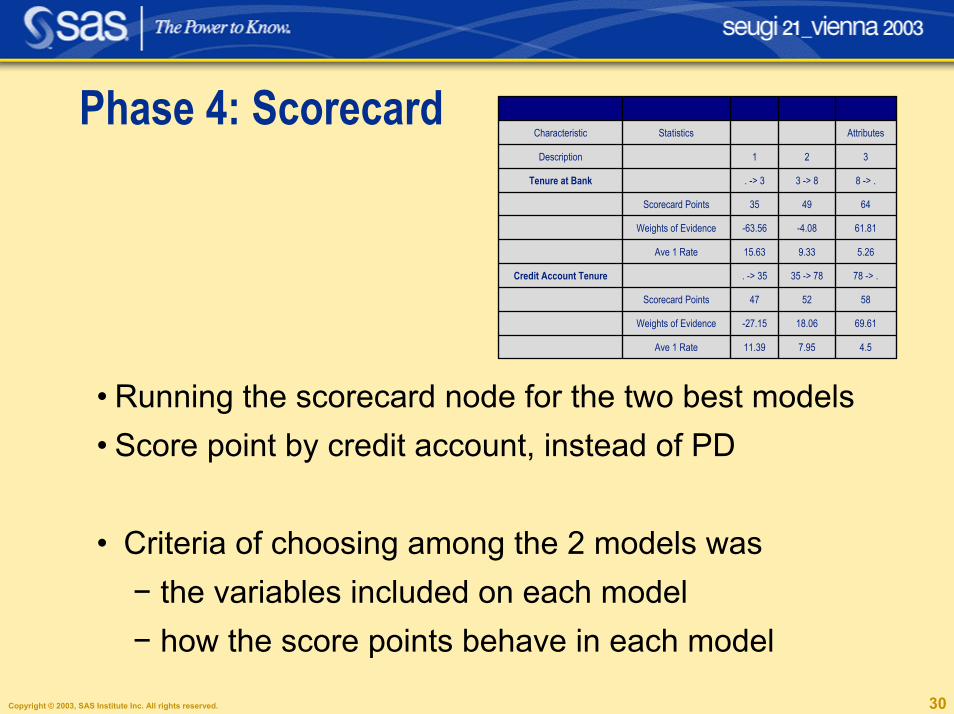

Phase 4: Scorecard

4.57.9511.39Ave 1 Rate

69.6118.06-27.15Weights of Evidence

585247Scorecard Points

78 -> .35 -> 78. -> 35Credit Account Tenure

5.269.3315.63Ave 1 Rate

61.81-4.08-63.56Weights of Evidence

644935Scorecard Points

8 -> .3 -> 8. -> 3Tenure at Bank

321Description

AttributesStatisticsCharacteristic

var3var2var1CB

� Running the scorecard node for the two best models� Score point by credit account, instead of PD

� Criteria of choosing among the 2 models was− the variables included on each model− how the score points behave in each model

Copyright © 2003, SAS Institute Inc. All rights reserved. 31

Phase 4: Results Tenure at the bank Average Balance<= 2 years .............................................. 35 <= 250 � .......................................... 353 - 7 years .............................................. 49 251 � - 500 � ................................... 538 - 10 years ............................................ 55 501 � - 1100 � ................................. 64>= 11 years ............................................ 64 1001 � - 2000 � ............................... 71

>= 2001 � ........................................ 75

Tenure Credit Account % of Cashadvance<= 24 months ......................................... 44 <= 10 .............................................. 6325 - 36 months ....................................... 49 11 - 20 ............................................ 5437 - 75 months ....................................... 53 21 - 66 ............................................ 49>= 76 months ......................................... 65 >= 67 .............................................. 38

........................ .............................

Copyright © 2003, SAS Institute Inc. All rights reserved. 32

Phase 4: Score points

An attribute�s points reflect� the risk of an attribute relative to the other attributes of the

same characteristic� the relative contribution of each characteristic to the

overall score

The relative risk of an attribute is determined by its �Weight of Evidence�.

The contribution of a characteristic is determined by its co-efficient in a logistic regression.

Copyright © 2003, SAS Institute Inc. All rights reserved. 33

Phase 4: Segmentation

Bad Poor Medium Good Excellent

Tenure at the bank < 2 years 2 - 5 years 5 - 7 years 7 - 10 years > 10 years

Tenure Credit Account < 24 months 24 - 40 months 40 - 43 months 43 - 50 months > 50 months

Delays Have Have Don't Have Don't Have Don't Have

Average Balance < 100 � 100 � - 200 � 200 � - 500 � 500 � - 1000 � > 1000 �

Nº Products on bank 1 2 - 3 4 - 5 6 - 7 > 7

% Credit limit usage > 83% 83% - 75% 74% - 40% 39% - 10% < 10%

Default Indicator on any other credit Have Have Have Don't Have Don't HaveAge < 20 years 20 - 25 years 25 - 30 years 30 - 38 years >38 years

Copyright © 2003, SAS Institute Inc. All rights reserved. 34

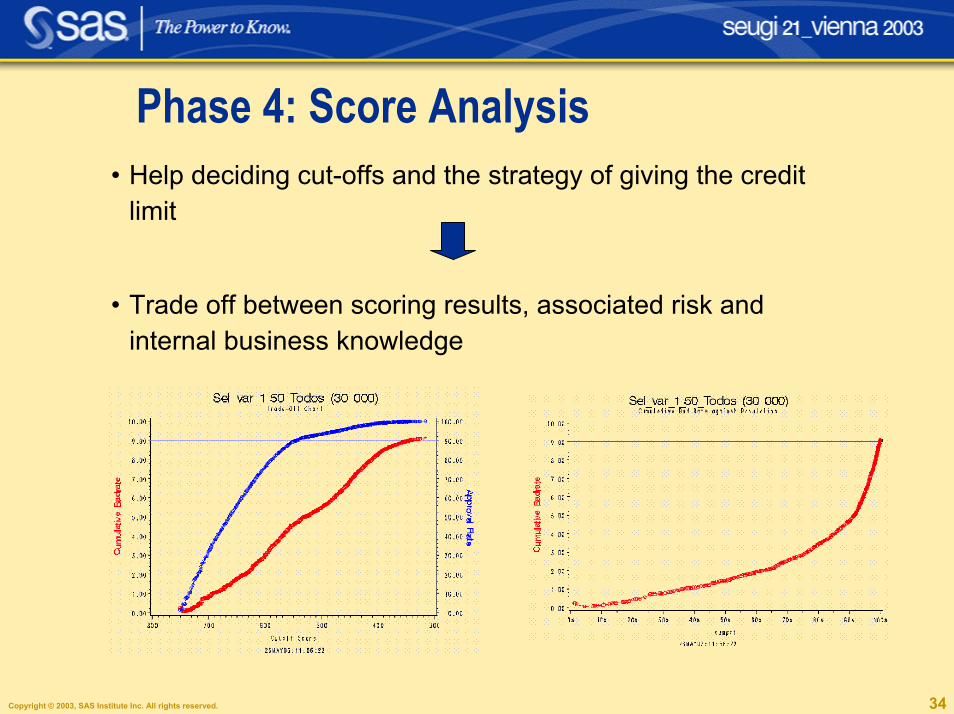

Phase 4: Score Analysis� Help deciding cut-offs and the strategy of giving the credit

limit

� Trade off between scoring results, associated risk and internal business knowledge

Copyright © 2003, SAS Institute Inc. All rights reserved. 35

Phase 4: ResultsScore Points < 100 100 - 200 200 - 400 400 - 500 >500

% Accounts 5% 10% 20% 20% 45%

Bad Rate 78% 45% 15% 4% 1%

� If accepted the credit accounts with a score points >= 400 we have an automatic decision of around 65% credit card accounts

� If we rejected the credit accounts with a score points <= 100 we have an automatic decision of around 5%

This leads to a 70% of automatic decision making coming out from the model on assigning a credit limit!

Copyright © 2003, SAS Institute Inc. All rights reserved. 36

Project Methodology:

! Phase 1: Defining the scope

! Phase 2: Making data available (data mart)

! Phase 3: Evaluating the environment for modeling

! Phase 4: Model development

! Phase 5: Model deployment! Phase 6: Performance monitoring

Copyright © 2003, SAS Institute Inc. All rights reserved. 37

Project Duration & Next Steps

! Project Duration:� Started November 2002

� Ended May 2003

! Next Steps � To develop an Web (AppDev) application for:� Phase 5: Model deployment − Scoring credit card accounts, give the appropriate

strategy/actions (Back Office)� Phase 6: Performance monitoring− Reporting for monitoring the model (Risk Department)

Copyright © 2003, SAS Institute Inc. All rights reserved. 38

Benefits� Be able to build scorecards faster, more accurately and for a

greater variety of purposes and segments

� Independence of outsourcing

� Full control of core activities

− Documented processes

− Ability to monitor scorecard performance

− Decision execution through a variety of web enable reports

� Full internal control (required condition for Basel II)� Improve credit decisions� Reduce credit loss� Increase company profits

�It�s an innovative project with excellent quality, the project time was fulfilled, we�ve got a great

model!�

Copyright © 2003, SAS Institute Inc. All rights reserved. 39

Contacts

� Project Manager � M. Helena Antunes ([email protected])

� CRM Analytics Specialist (Scorecard Implementation) �Helena Junqueiro ([email protected])

� Warehouse Consultant � Rui Martins ([email protected])

� Account Manager � Raquel Quaresma ([email protected])

Copyright © 2003, SAS Institute Inc. All rights reserved. 40Copyright © 2003, SAS Institute Inc. All rights reserved. 40