sarfaesi act 2002

TRANSCRIPT

• Securitisation & Reconstruction of Financial Assets &

Enforcement of Security Interest Act 2002 – Promulgation on

23.08.2002

• Amended during 2004 on Supreme Court suggestion in case

of Mardia Chemicals Vs Union of India.

• Major step in Financial Sector Reforms.

• For Movables – The Indian Contract Act 1872

For Movables & Immovables etc – SARFAESI Act 2002

• Prior to Act, help of legal system was a must for selling

immovable property which used to take unduly long time.

2

• This Act allows to lay hand on the securities. Not applicable in

respect of clean loans.

• The Act extends to the whole of India including the states of

Jammu & Kashmir.

• The Act has retrospective application i.e. it applies for loans and

securities created prior to the Act coming into operation.

• The a/c has to be classified as NPA as per RBI norms before

taking action under SARFAESI Act.

• After possession, the aggrieved party may go to DRT by paying

only court fees & in case of verdict in favour of the Bank,

aggrieved party may appeal to DRAT by paying 50% of dues

(may be reduced to 25% but not less than that).

3

• BIFR Cases – Cases already referred to BIFR can be called back

if 75% of lenders agree for that. Even if matter is pending with

BIFR, the lender can take possession of security.

• Consortium Accounts or Multiple Lending Arrangement

If 75% of the secured creditors in value agree to initiate

recovery action, the same shall be binding on all secured

creditors.

• DRT pending Cases

Action as regards possession & subsequent can be initiated

under SARFAESI Act in DRT pending cases as per Supreme

Court judgement in Transcore Vs Union of India.

4

Provisions of SARFAESI Act 2002

In the event of default by a borrower, a secured creditor

(bank/FI) will have the following powers

1. Take possession, sell or lease the secured assets.

2. Take over the management of the business of the borrower.

3. Appoint a manager (powers vested with scale IV officers in

banks).

4. Recover any money payable by 3rd parties to the borrowers.

5

Loans not eligible under SARFAESI Act

1. Loans with outstanding upto Rs.1 Lac.

2. Agriculture land cannot be sold.

3. Where the amt. due is less than 20% of the principal and

interest.

4. Loans secured by pledge, lien & security of bank deposits.

5. Where limitation has expired.

6. Where security is not charged to bank.

6

Sale of Charged Securities

Under Securities Interest (Enforcement) Rules 2002, Ministry

of Finance notified rules for taking possession and subsequent

sale of assets of defaulters.

Possession

An authorised officer of lender (scale IV officer in bank) would

have to take possession of the same by service of a 60 days

possession notice (Sec.13(2))

7

Receipt of notice by Borrower

If after receiving possession notice, the borrower makes any

representation or raises any objection, the secured creditor shall

consider such representation or objection. If secured creditor –

objection / representation not tenable, shall communicate within

one week of receipt, the reasons for non – acceptance of objection

/ representation to the borrower.

Application by borrower to DRT

Borrower may make an application (with fees) to DRT, without

deposit of any amount within a period of 45 days (sec. 17)

8

Action by DRT

If measures taken by secured creditor – not in accordance with

provisions of Act – DRT may declare measures taken by

secured creditor as invalid & restore possession of secured

assets to borrower. If measures in accordance with provisions

– secured creditor entitled to take steps to recover debt – DRT

to dispose off the application within – 60 – days (Max.– 4 –

months)

9

Appeal to DRAT – Deposit of Amt. before appeal

Appeal to Appellate Tribunal within 30 days – borrower to

deposit with Tribunal 50% of the amount of debt due – as

claimed by secured creditor or determined by DRT whichever

is less. ( The Tribunal may reduce the amt. to not less than

25% of debt) (Sec.18)

Sale of Assets

• Sale by way of public tenders or through public auction has

to be backed by public notices in two newspapers one of

which in local vernacular language.

10

• Minimum notice period

30 days, notice to be given to owner by designated officer

after taking possession by authorised officer and eventual

sale of property.

• Reserve Price

Proper valuation by approved valuer prior to sale of

property.

• Offer Price

If price higher than reserve price cannot be obtained, assets

can be disposed off at lower price with consent of both the

borrower & the lender.

11

• Sale will be confirmed after deposit of 25% by the highest

bidder. Balance within 15 days of confirmation of sale.

• When secured creditor is required to take possession or

control of the secured asset or for sale, help of Chief

Metropolitan Magistrate or District Magistrate be taken by

request in writing. (Sec. 14)

12

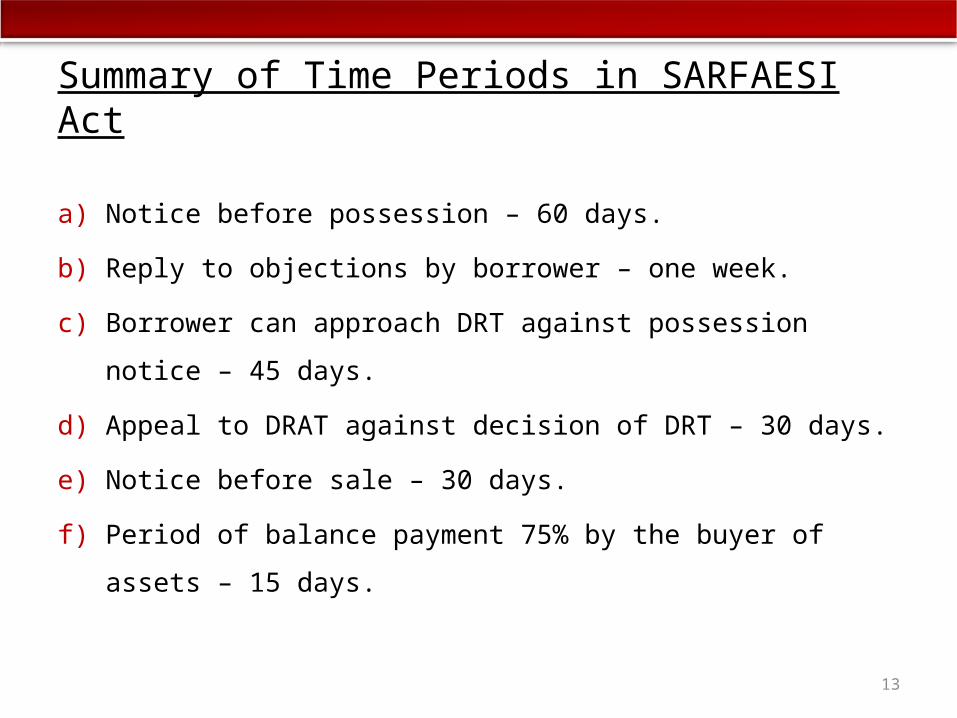

Summary of Time Periods in SARFAESI Act

a) Notice before possession – 60 days.

b) Reply to objections by borrower – one week.

c) Borrower can approach DRT against possession notice – 45

days.

d) Appeal to DRAT against decision of DRT – 30 days.

e) Notice before sale – 30 days.

f) Period of balance payment 75% by the buyer of assets –

15 days.

13

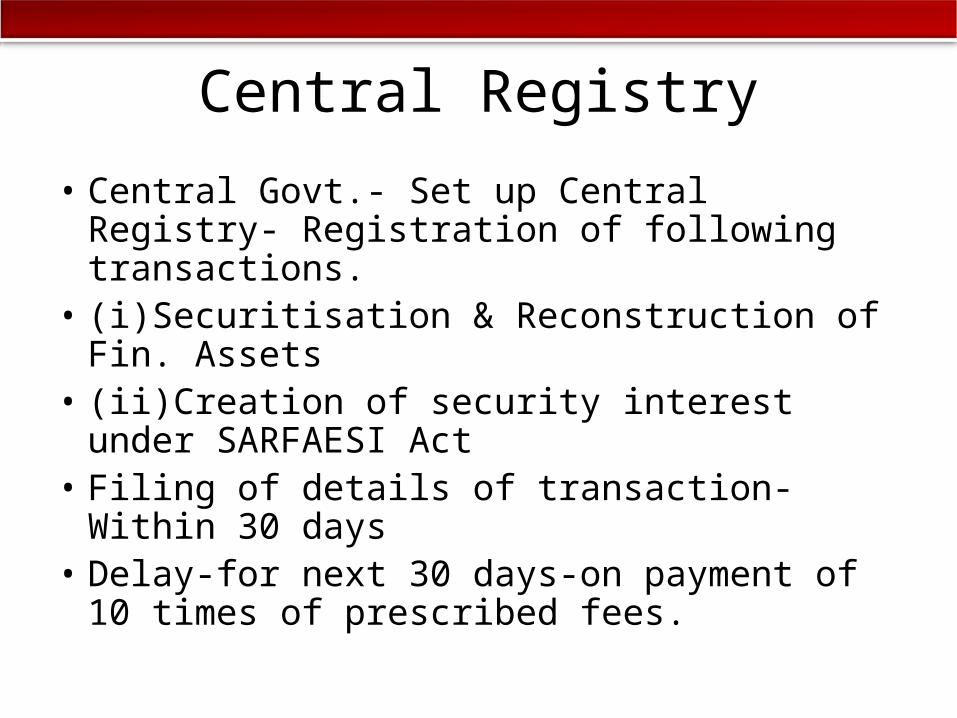

Central Registry

• Central Govt.- Set up Central Registry- Registration of following transactions.

• (i)Securitisation & Reconstruction of Fin. Assets

• (ii)Creation of security interest under SARFAESI Act

• Filing of details of transaction- Within 30 days• Delay-for next 30 days-on payment of 10 times

of prescribed fees.

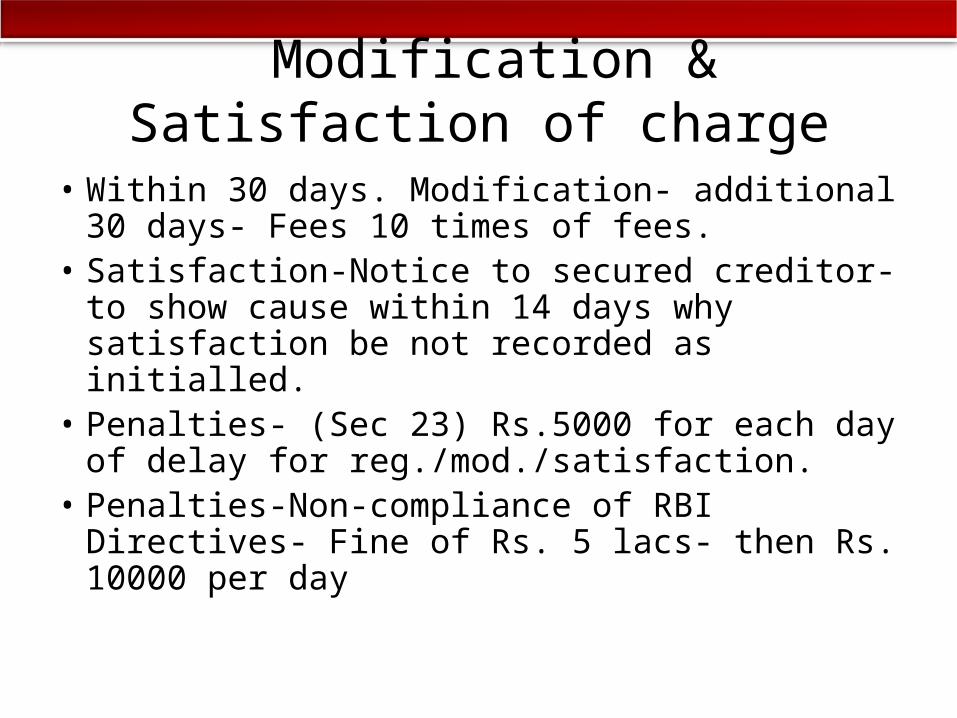

Modification & Satisfaction of charge

• Within 30 days. Modification- additional 30 days- Fees 10 times of fees.

• Satisfaction-Notice to secured creditor- to show cause within 14 days why satisfaction be not recorded as initialled.

• Penalties- (Sec 23) Rs.5000 for each day of delay for reg./mod./satisfaction.

• Penalties-Non-compliance of RBI Directives- Fine of Rs. 5 lacs- then Rs. 10000 per day

16