rr results q1_2016_en_final2

TRANSCRIPT

4 MAY 2016

MAGNUS ROSÉN, PRESIDENT AND CEO PIERRE BRORSSON, CFO

Improvement in sales and profitability

Interim report Q1/2016

• Group performance

• Segment review

• Market outlook

• Key figures

• Financial position

• Appendices

Agenda

2 4/5/2016 Interim report Q1/2016

3

• Net sales 146.0 (140.6) MEUR up by 3.9% or by 5.5% at comparable exchange rates

• EBITA 7.2 (4.1) MEUR up by 75.5%

• EBITA margin 5.0% (2.9%)

• ROCE 10.7% (10.3%)

• ROE 14.6% (9.7%)

• Gross capex 40.4 (18.1) MEUR

• Net debt 287.9 (226.2) MEUR

• Net debt to EBITDA 1.7x (1.4x)

Highlights Q1 2016 – Improvement in sales and profitability

4/5/2016 Interim report Q1/2016

4/5/2016 Interim report Q1/2016 4

• Ramirent signed a cooperation agreement with NCC Roads in Finland

• To serve the customer Ramirent invested in new fleet especially needed in the asphalt business

• The agreement strengthens Ramirent’s position within Finland’s infrastructure construction sector

• Ramirent signed its first frame agreement with JM AB in Sweden

• Three-year agreement for equipment rental and related services includes option for prolongation

• The agreement covers most of Ramirent’s product groups

Important new customer agreements with NCC Roads in Finland and JM in Sweden

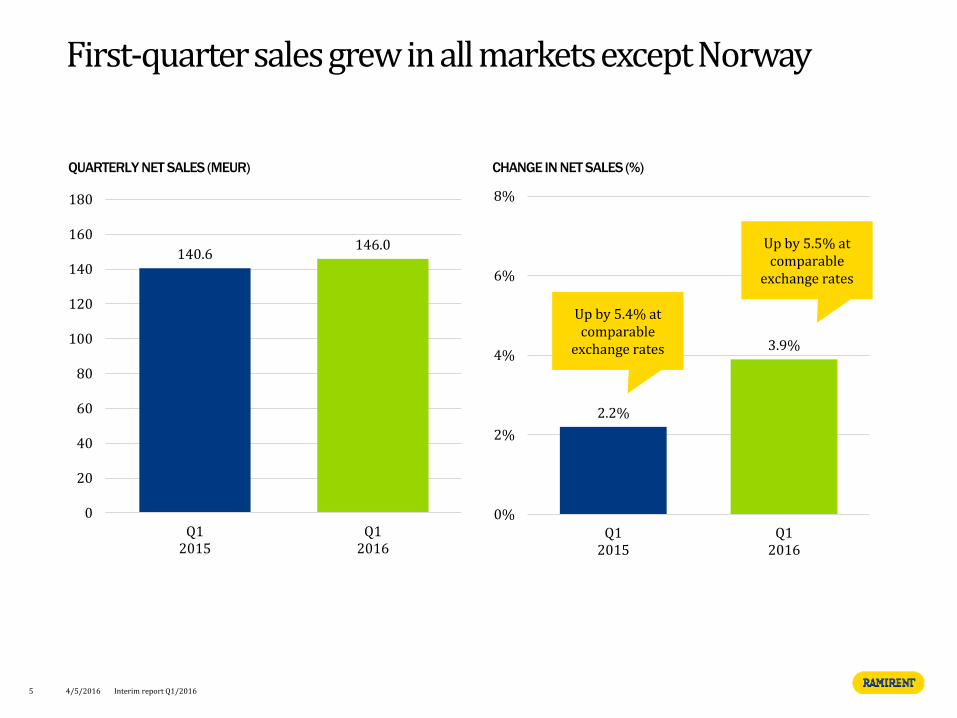

First-quarter sales grew in all markets except Norway

QUARTERLY NET SALES (MEUR) CHANGE IN NET SALES (%)

5 4/5/2016 Interim report Q1/2016

140.6 146.0

0

20

40

60

80

100

120

140

160

180

Q12015

Q12016

2.2%

3.9%

0%

2%

4%

6%

8%

Q12015

Q12016

Up by 5.5% at comparable

exchange rates

Up by 5.4% at comparable

exchange rates

First-quarter EBITA improved based on higher sales and good control of material and services costs

QUARTERLY EBITA (MEUR) QUARTERLY EBITA MARGIN

6 4/5/2016 Interim report Q1/2016

2.9%

5.0%

0%

2%

4%

6%

8%

10%

12%

Q12015

Q12016

4.1

7.2

0

2

4

6

8

10

12

14

Q12015

Q12016

• Sales growth was driven by higher service sales and deliveries to ongoing Total Solutions projects

• Projects mainly in the Nordic countries and in Poland

7

• Sales growth driven mainly by improving market conditions in the Nordic construction and industrial sector

• Demand was weaker in Europe Central and the Baltics due to slow start to the year in construction of new buildings

• Favourable demand in all Nordic countries except Norway, where demand was sluggish mainly due to a weak business climate in the oil & gas sector

• In Sweden demand was strong especially in the public sector

Q1 2016 overview by business area

4/5/2016 Interim report Q1/2016

Share of Group sales

63% 32% 5%

All long-term financial targets were met in Q1 2016

8 4/5/2016 Interim report Q1/2016

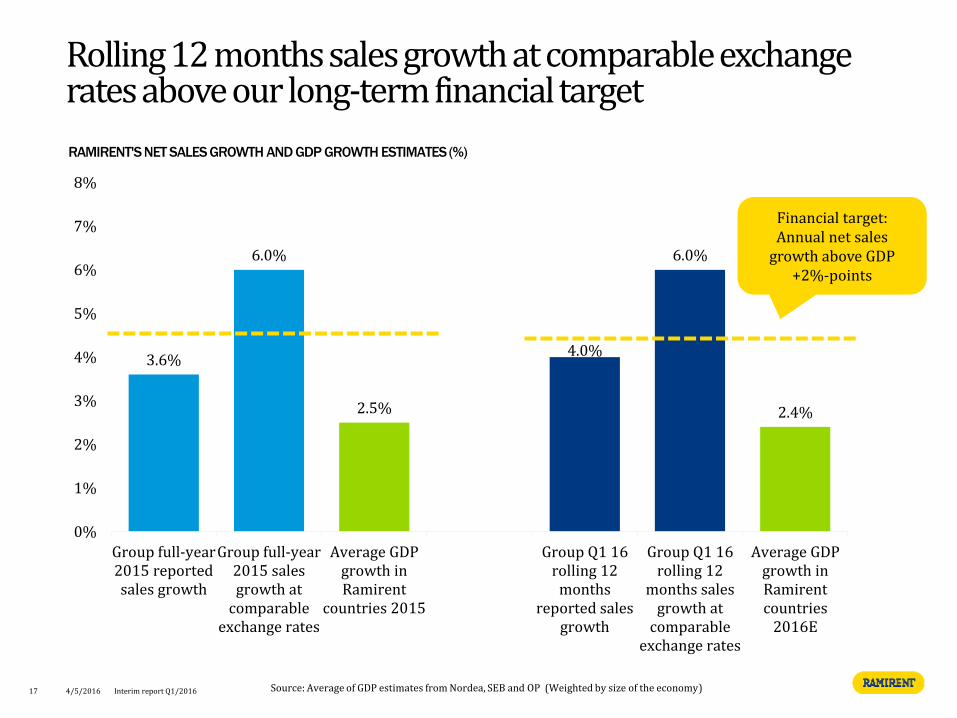

*Rolling 12 months net sales growth at comparable exchange rates which was above FY2016 growth target of 4.4% (2.0%-points + 2.4% estimated GDP growth for 2016)

Source: Average of GDP estimates from Nordea, SEB and OP (Weighted by size of the economy)

4/5/2016 Interim report Q1/2016 9

Segment review

HIGHLIGHTS Q1 16

Finland: Strong execution in the first quarter

NET SALES

KEY FIGURES PROFITABILITY

• Sales grew in all Business Areas based on strong execution from our Finnish team supported by improved underlying demand in the market

• In Solutions, especially large construction projects and activity in the industry sector supported growth in the first quarter

• EBITA improvement was mainly driven by higher sales 0

10

20

30

40

50

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

Finland 1–3/16 1–3/15 Change 1–12/15

Net sales 38.1 32.0 19.0% 160.2

EBITA 2.9 0.8 262.6% 21.11)

% of net sales 7.7% 2.5% 13.2%1)

Capital employed 120.6 113.0 6.7% 120.6

ROCE (%)2) 18.8% 14.7% 17.5%

Personnel (FTE) 471 487 -3.3% 455

Customer centres

53 62 -14.5% 56

Net sales up by 19.0%

10

0%

5%

10%

15%

20%

25%

30%

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

EBITA-margin (%) ROCE (%) R12

1) Comparable EBITA was EUR 20.3 million or 12.7% of net sales in January–December 2015. The items affecting comparability included derecognition of a contingent liability and the amount, EUR 0.8 million was recognised in other operating income. 2) Rolling 12 months

4/5/2016 Interim report Q1/2016

HIGHLIGHTS Q1 16

Sweden: Sales grew, EBITA impacted by project write-downs

NET SALES

KEY FIGURES PROFITABILITY

• In General Rental, high sales growth achieved especially among building construction customers and in Solutions, strong service sales and deliveries to Total Solutions projects contributed to growth

• In Temporary Space strong demand continued in the public sector

• Write-downs in solutions projects of 1.1 MEUR hampered the first quarter EBITA

0%

5%

10%

15%

20%

25%

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

EBITA-margin (%) ROCE (%) R12

0

10

20

30

40

50

60

70

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

11

1) Comparable EBITA was EUR 29.4 million or 13.1% in January–December 2015. The items affecting comparability included derecognition of a contingent consideration liability. The amount, EUR 3.8 million, was recognised in other operating income in the second quarter of 2015. A restructuring provision of EUR 0.3 million was recognised in the fourth quarter of 2015. 2) Rolling 12 months 4/5/2016 Interim report Q1/2016

Sweden 1–3/16 1–3/15 Change 1–12/15

Net sales 53.7 51.0 5.3% 225.4

EBITA 4.4 5.1 -13.8% 33.01)

% of net sales 8.2% 10.0% 14.6%1)

Capital employed 199.4 157.4 26.6% 199.0

ROCE (%)2) 15.5% 16.9% 16.1%

Personnel (FTE) 751 760 -1.2% 779

Customer centres

78 80 -2.5% 78

Net sales up by 5.3% or by 4.6% at

comparable exchange rates

HIGHLIGHTS Q1 16 NET SALES

KEY FIGURES PROFITABILITY

• In General Rental and Solutions sales grew slightly in the first quarter

• Improved organisational structures supported performance in General Rental and Solutions

• Temporary space with exposure to oil & gas sector remains a challenge

0%

5%

10%

15%

20%

25%

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

EBITA-margin (%) ROCE (%) R12

05

1015202530354045

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

Net sales down by 10.2% or by 2.0% at

comparable exchange rates

12

1) Comparable EBITA was EUR 7.0 million or 5.8% of net sales in January–December 2015. The items affecting comparability included EUR 0.5 million of restructuring costs recognised in the fourth quarter of 2015. 2) Rolling 12 months

4/5/2016 Interim report Q1/2016

Norway: Improved profitability despite challenges in Temporary space

Norway 1–3/16 1–3/15 Change 1–12/15

Net sales 27.8 31.0 -10.2% 120.7

EBITA 1.3 1.0 33.0% 6.51)

% of net sales 4.8% 3.3% 5.4%1)

Capital employed 125.3 126.1 -0.6% 120.9

ROCE (%)2) 4.0% 7.8% 3.8%

Personnel (FTE) 406 405 0.3% 401

Customer centres

41 43 -4.7% 42

HIGHLIGHTS Q1 16

Denmark: Improved demand and lower cost base improved EBITA

NET SALES

KEY FIGURES PROFITABILITY

• Strong performance by the Danish organisation drove sales growth; In General Rental, volumes grew based on high activity especially in the construction sector and in Solutions, strong service sales contributed to growth

• Sales growth was also supported by higher sales of used equipment in the quarter

• EBITA improvement was driven by strong sales growth and successfully implemented cost reduction measures in 2015 that have resulted in a lower fixed cost base

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

EBITA-margin (%) ROCE (%) R12

0

2

4

6

8

10

12

14

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

Net sales increased by 10.7% or by

10.9% at comparable exchange rates

13

1) Comparable EBITA was EUR 0.8 million or 1.8% of net sales in January–December 2015. The items affecting comparability included a EUR 0.5 million of restructuring provision recognised in the third quarter of 2015 2) Rolling 12 months

4/5/2016 Interim report Q1/2016

Denmark 1–3/16 1–3/15 Change 1–12/15

Net sales 10.4 9.4 10.7% 42.3

EBITA 0.4 -1.4 130.3% 0.31)

% of net sales 4.0% -14.8% 0.7%1)

Capital employed 30.5 25.0 22.4% 26.0

ROCE (%)2) 6.1% -16.7% -0.5%

Personnel (FTE) 139 142 -2.3% 139

Customer centres

13 15 -13.3% 13

HIGHLIGHTS Q1 16

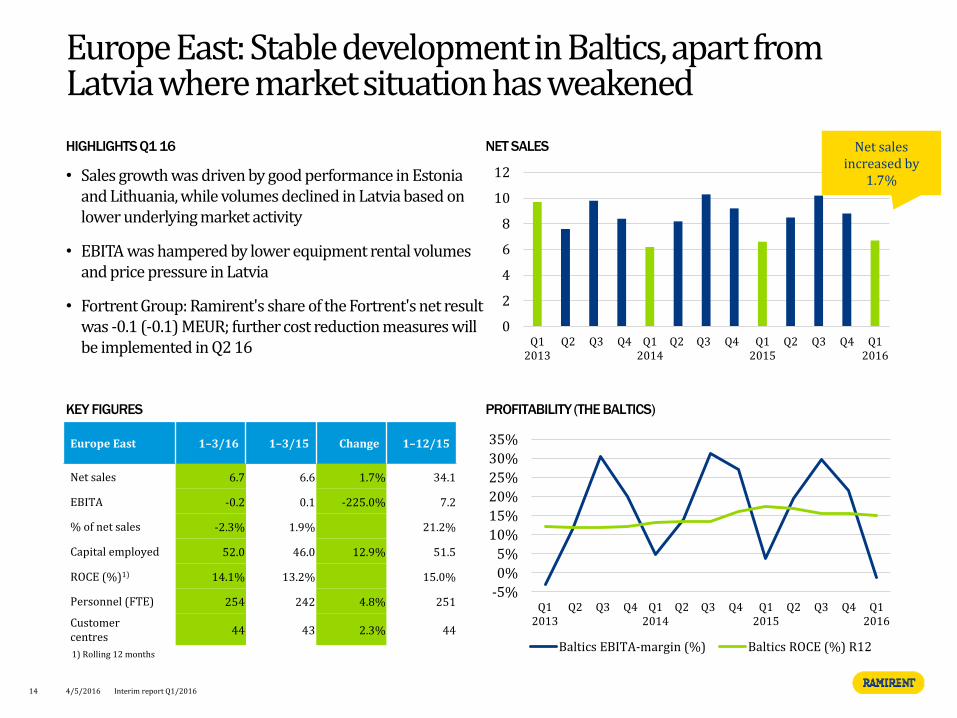

Europe East: Stable development in Baltics, apart from Latvia where market situation has weakened

NET SALES

KEY FIGURES PROFITABILITY (THE BALTICS)

• Sales growth was driven by good performance in Estonia and Lithuania, while volumes declined in Latvia based on lower underlying market activity

• EBITA was hampered by lower equipment rental volumes and price pressure in Latvia

• Fortrent Group: Ramirent's share of the Fortrent's net result was -0.1 (-0.1) MEUR; further cost reduction measures will be implemented in Q2 16

0

2

4

6

8

10

12

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

Net sales increased by

1.7%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

Baltics EBITA-margin (%) Baltics ROCE (%) R12

14 4/5/2016 Interim report Q1/2016

Europe East 1–3/16 1–3/15 Change 1–12/15

Net sales 6.7 6.6 1.7% 34.1

EBITA -0.2 0.1 -225.0% 7.2

% of net sales -2.3% 1.9% 21.2%

Capital employed 52.0 46.0 12.9% 51.5

ROCE (%)1) 14.1% 13.2% 15.0%

Personnel (FTE) 254 242 4.8% 251

Customer centres

44 43 2.3% 44

1) Rolling 12 months

HIGHLIGHTS Q1 16

Europe Central: Demand supported by industry projects, slower start to the year in construction activity

NET SALES

KEY FIGURES PROFITABILITY

• Sales growth was supported by good progress in large power plant projects in Poland, whereas activity in the construction sector was slower than expected

• Performance remained good in Slovakia, but was weaker in the Czech Republic due to postponements of construction projects

• EBITA was negatively impacted by a higher share of service sales in the business mix and tough competition in the Polish market

-25%-20%-15%-10%

-5%0%5%

10%15%20%

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

EBITA-margin (%) ROCE (%) R12

15

02468

1012141618

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

4/5/2016 Interim report Q1/2016

Europe Central 1–3/16 1–3/15 Change 1–12/15

Net sales 11.3 11.0 2.5% 55.4

EBITA -0.8 -0.6 -34.8% 3.3

% of net sales -6.7% -5.1% 5.9%

Capital employed 53.6 59.0 -9.1% 54.7

ROCE (%)1) 5.3% 3.7% 5.6%

Personnel (FTE) 510 481 6.1% 493

Customer centres

55 58 -5.2% 55

Net sales up by 2.5% or by 5.4% at comparable

exchange rates

1) Rolling 12 months

16

Market outlook

4/5/2016 Interim report Q1/2016

17

Rolling 12 months sales growth at comparable exchange rates above our long-term financial target

RAMIRENT'S NET SALES GROWTH AND GDP GROWTH ESTIMATES (%)

3.6%

6.0%

2.5%

4.0%

6.0%

2.4%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Group full-year2015 reportedsales growth

Group full-year2015 salesgrowth at

comparableexchange rates

Average GDPgrowth inRamirent

countries 2015

Group Q1 16rolling 12

monthsreported sales

growth

Group Q1 16rolling 12

months salesgrowth at

comparableexchange rates

Average GDPgrowth inRamirentcountries

2016E

Source: Average of GDP estimates from Nordea, SEB and OP (Weighted by size of the economy) 4/5/2016 Interim report Q1/2016

Financial target: Annual net sales

growth above GDP +2%-points

Ramirent expects to see stable and fair overall market conditions in 2016

GDP GROWTH ESTIMATES BY SEGMENT FOR 2016 RAMIRENT'S EXPECTATIONS ON OVERALL DEMAND BY EQUIPMENT RENTAL MARKET

18

Favourable

Stable

Challenging

4/5/2016 Interim report Q1/2016

Sources: Confederation of Finnish Construction Industries (RT) 4/2016, Swedish Construction Federation (BI) 3/2016, Prognosesenteret 3/2016, Danish Construction Industry (DB) 2/2016 and Euroconstruct 12/2015

0.6%

3.7%

1.4% 1.6%

2.6% 3.2%

0%

1%

2%

3%

4%

5%

6%

Finland Sweden Norway Denmark TheBaltics

EuropeCentral

3.5% 4.0% 4.2%

2.7%

1.5%

5.8%

0%

1%

2%

3%

4%

5%

6%

Finland Sweden Norway Denmark TheBaltics

EuropeCentral

CONSTRUCTION VOLUME GROWTH BY SEGMENT FOR 2016

Ramirent outlook for 2016 unchanged

In 2016, Ramirent’s net sales in local currencies and EBITA margin are expected to increase from the level in 2015.

19 4/5/2016 Interim report Q1/2016

4/5/2016 Interim report Q1/2016 20

Key figures

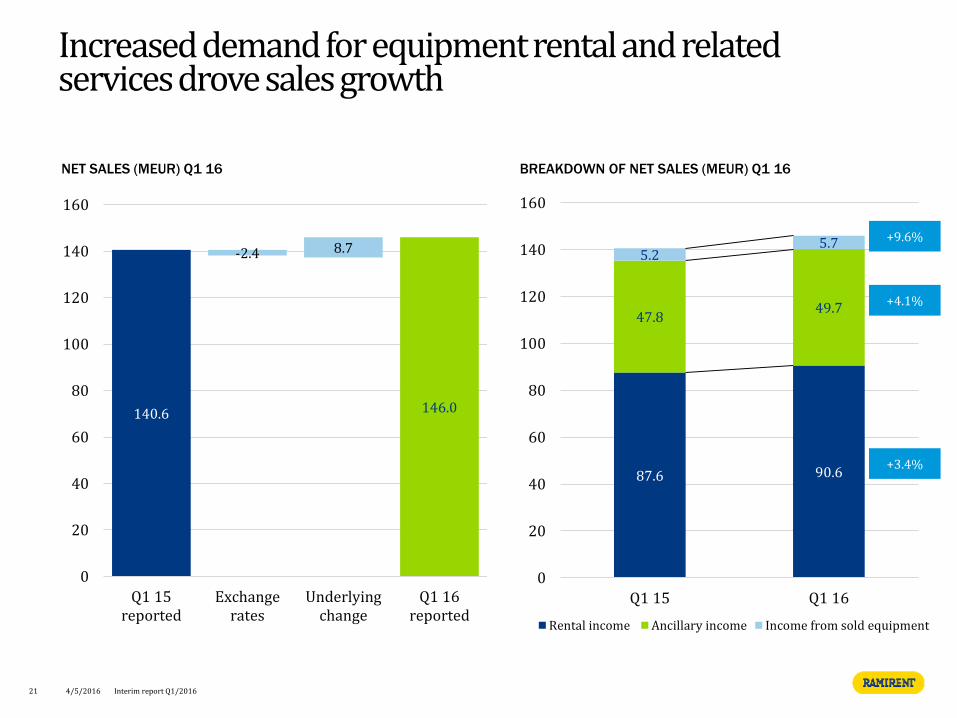

87.6 90.6

47.8 49.7

5.2 5.7

0

20

40

60

80

100

120

140

160

Q1 15 Q1 16

Rental income Ancillary income Income from sold equipment

+3.4%

+4.1%

+9.6%

140.6

-2.4 8.7

146.0

0

20

40

60

80

100

120

140

160

Q1 15reported

Exchangerates

Underlyingchange

Q1 16reported

Increased demand for equipment rental and related services drove sales growth

NET SALES (MEUR) Q1 16 BREAKDOWN OF NET SALES (MEUR) Q1 16

21 4/5/2016 Interim report Q1/2016

2.5%

10.0%

3.3% 3.8%

-5.1%

7.7% 8.2%

4.8% 4.0%

-1.1%

-6.7% -10%

-5%

0%

5%

10%

15%

Finland Sweden Norway Denmark The Baltics Europe Central

First-quarter sales growth at comparable exchange rates, GDP growth and margins by segment

Q1 15 Q1 16

FIRST-QUARTER 2016 SALES GROWTH AT COMPARABLE FX. AND GDP GROWTH ESTIMATES*

FIRST-QUARTER 2016 EBITA MARGIN (%)

22 4/5/2016 Interim report Q1/2016

4.6%

-2.0%

10.9%

1.7%

5.4%

0.6%

3.7%

1.4% 1.6% 2.6%

3.2%

-2%

2%

6%

10%

Finland Sweden Norway Denmark The Baltics Europe Central

At comparable fx. Q1 2016

GDP growth FY2016E

*Source: Average of GDP estimates from Nordea, SEB and OP

-14.8%

19.0%

Sales growth and cost reductions implemented in the previous year driving EBITA

EBITA BRIDGE (MEUR) Q1 15 – Q1 16

4.1

2.1

−0.7 0.3

1.8

−0.3 −0.2 0.0

7.2

0

2

4

6

8

10

EBITA Q12015

Finland Sweden Norway Denmark Europe East EuropeCentral

Items notallocated to

segments

EBITA Q12016

EBITA impacted by write-downs of 1.1 MEUR in Solutions

projects

Improvement driven by higher sales in all

Business Areas

2.5% 10.0% 3.3% −14.8% 1.9% −5.1%

7.7% 8.2% 4.8% 4.0% −2.3% −6.7%

EBITA margin Q1/2015

EBITA margin Q1/2016

23 4/5/2016 Interim report Q1/2016

Strong sales growth and cost reduction measures driving

EBITA

20.3% 21.8%

0%

5%

10%

15%

20%

25%

30%

Q1 15 Q1 16

EBITDA (MEUR)

First-quarter EBITDA margin improved to 21.8% (20.3%)

EBITDA MARGIN

• First-quarter EBITDA margin improved to 21.8% (20.3%) of net sales

• First-quarter EBITDA increased by 11.5% and amounted to 31.9 (28.6) MEUR

24 4/5/2016 Interim report Q1/2016

28.6

31.9

0

5

10

15

20

25

30

35

40

Q1 15 Q1 16

GROSS PROFIT (MEUR) Q1 16

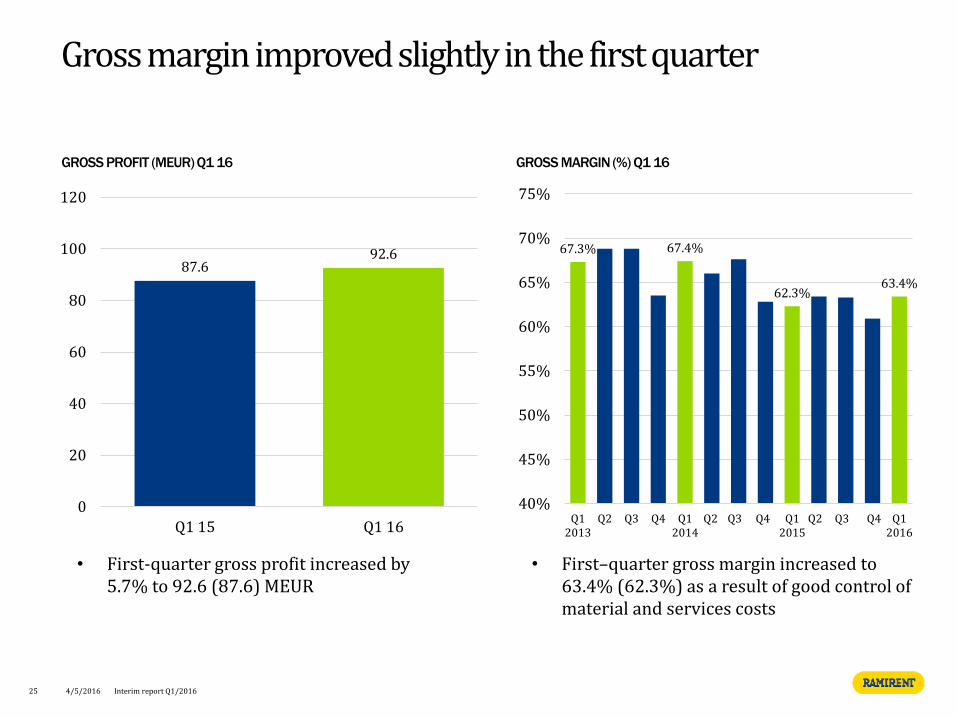

67.3% 67.4%

62.3% 63.4%

40%

45%

50%

55%

60%

65%

70%

75%

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

87.6 92.6

0

20

40

60

80

100

120

Q1 15 Q1 16

GROSS MARGIN (%) Q1 16

• First–quarter gross margin increased to 63.4% (62.3%) as a result of good control of material and services costs

• First-quarter gross profit increased by 5.7% to 92.6 (87.6) MEUR

25

Gross margin improved slightly in the first quarter

4/5/2016 Interim report Q1/2016

FIXED COSTS (MEUR) AND % OF GROUP NET SALES

Good control of fixed costs in the first quarter

• First-quarter fixed costs 61.0 (59.6) MEUR or 41.8% (42.4%) of net sales

• Employee benefit expenses 39.5 (37.8) MEUR

• Other operating expenses 21.5 (21.9) MEUR

• Rolling 12 months fixed costs amounted to 238.2 (237.0) MEUR or 37.2% (38.4%) of net sales

• Rolling 12 months fixed costs excluding items affecting comparability amounted to 237.0 (232.8) MEUR or 37.0% (37.8%) of net sales

65.9

60.9 59.6 61.0

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

10

20

30

40

50

60

70

80

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

26 4/5/2016 Interim report Q1/2016

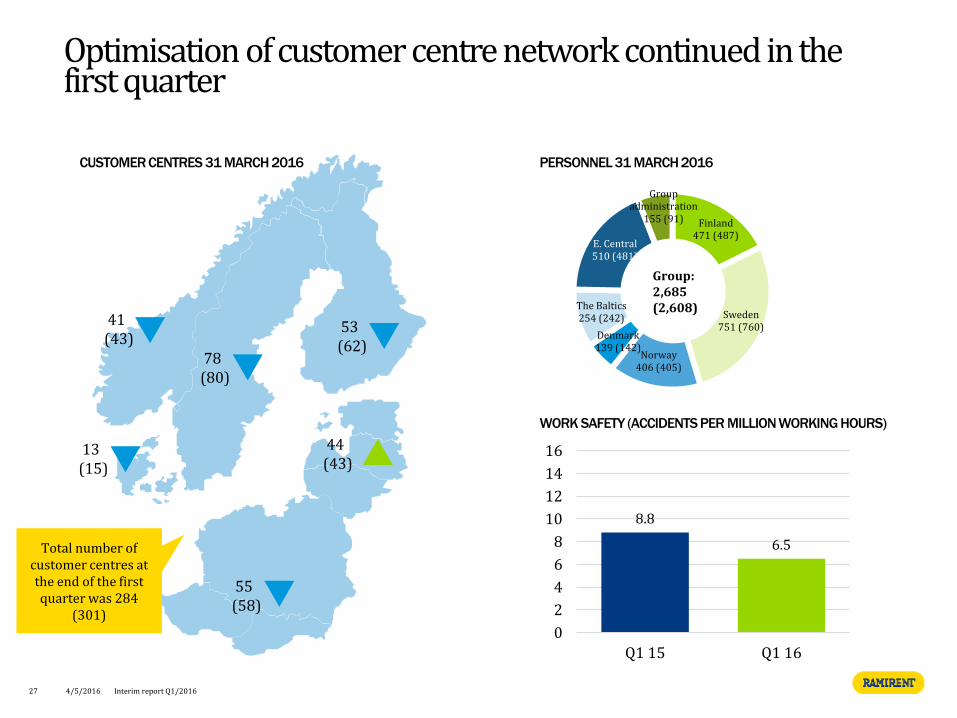

Finland 471 (487)

Sweden 751 (760)

Norway 406 (405)

Denmark 139 (142)

The Baltics 254 (242)

E. Central 510 (481)

Group administration

155 (91)

CUSTOMER CENTRES 31 MARCH 2016 PERSONNEL 31 MARCH 2016

Optimisation of customer centre network continued in the first quarter

Group: 2,685 (2,608)

53 (62)

44 (43)

55 (58)

78 (80)

13 (15)

41 (43)

27 4/5/2016 Interim report Q1/2016

8.8

6.5

0

2

4

6

8

10

12

14

16

Q1 15 Q1 16

WORK SAFETY (ACCIDENTS PER MILLION WORKING HOURS)

Total number of customer centres at the end of the first quarter was 284

(301)

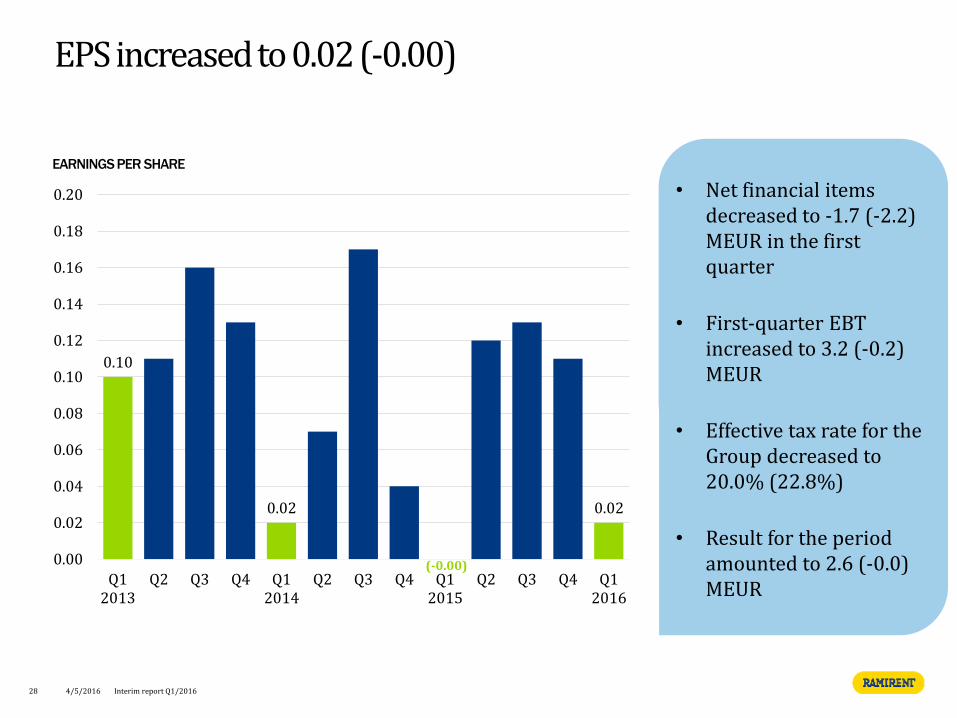

EARNINGS PER SHARE

EPS increased to 0.02 (-0.00)

• Net financial items decreased to -1.7 (-2.2) MEUR in the first quarter

• First-quarter EBT increased to 3.2 (-0.2) MEUR

• Effective tax rate for the Group decreased to 20.0% (22.8%)

• Result for the period amounted to 2.6 (-0.0) MEUR

28

0.10

0.02 0.02

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0.20

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

4/5/2016 Interim report Q1/2016

(-0.00)

CAPITAL EXPENDITURE EXCL. ACQUISITIONS (MEUR) AND % OF NET SALES

Investments in machinery and equipment increased to support growth in all business areas

• Q1 16 Gross capex 40.4 (18.1) MEUR or 27.7% (12.9%) of net sales

• Q1 16 investments in machinery and equipment 35.1 (15.9) MEUR. No acquisitions in the first quarter 2016 nor in 2015.

• Sales of used equipment amounted to 5.7 (5.2) MEUR

• Committed investments in rental machinery 57.0 (42.7) MEUR at the end of the first quarter

29 4/5/2016 Interim report Q1/2016

29.0

22.0

15.9

35.1

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

10

20

30

40

50

60

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

Capex excl. acquisitions Share of net sales-%

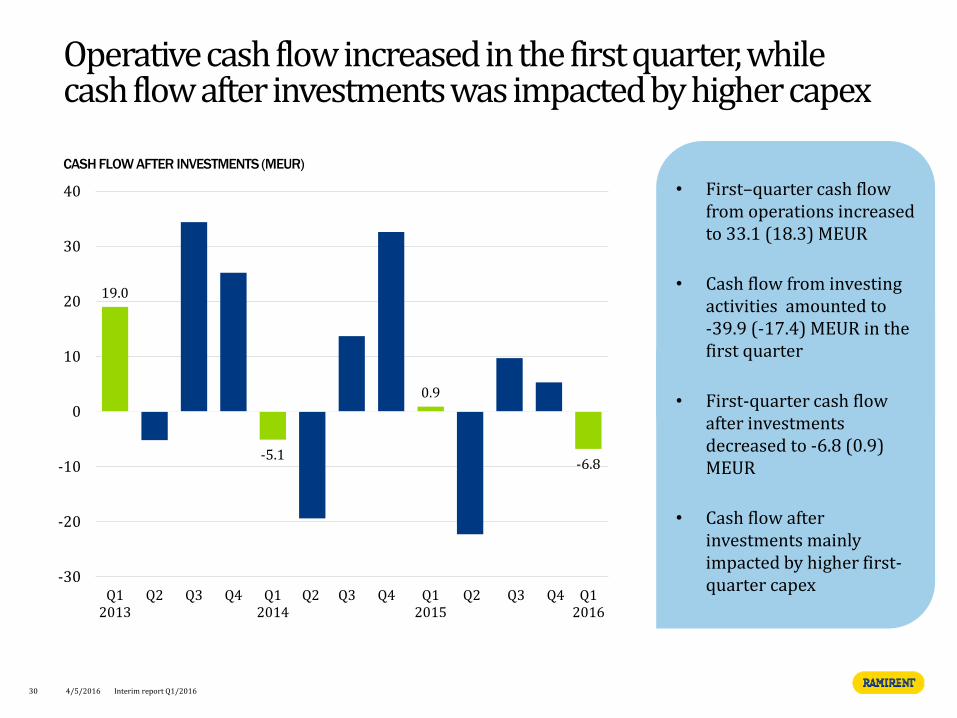

CASH FLOW AFTER INVESTMENTS (MEUR)

Operative cash flow increased in the first quarter, while cash flow after investments was impacted by higher capex

• First–quarter cash flow from operations increased to 33.1 (18.3) MEUR

• Cash flow from investing activities amounted to -39.9 (-17.4) MEUR in the first quarter

• First-quarter cash flow after investments decreased to -6.8 (0.9) MEUR

• Cash flow after investments mainly impacted by higher first-quarter capex

19.0

-5.1

0.9

-6.8

-30

-20

-10

0

10

20

30

40

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

30 4/5/2016 Interim report Q1/2016

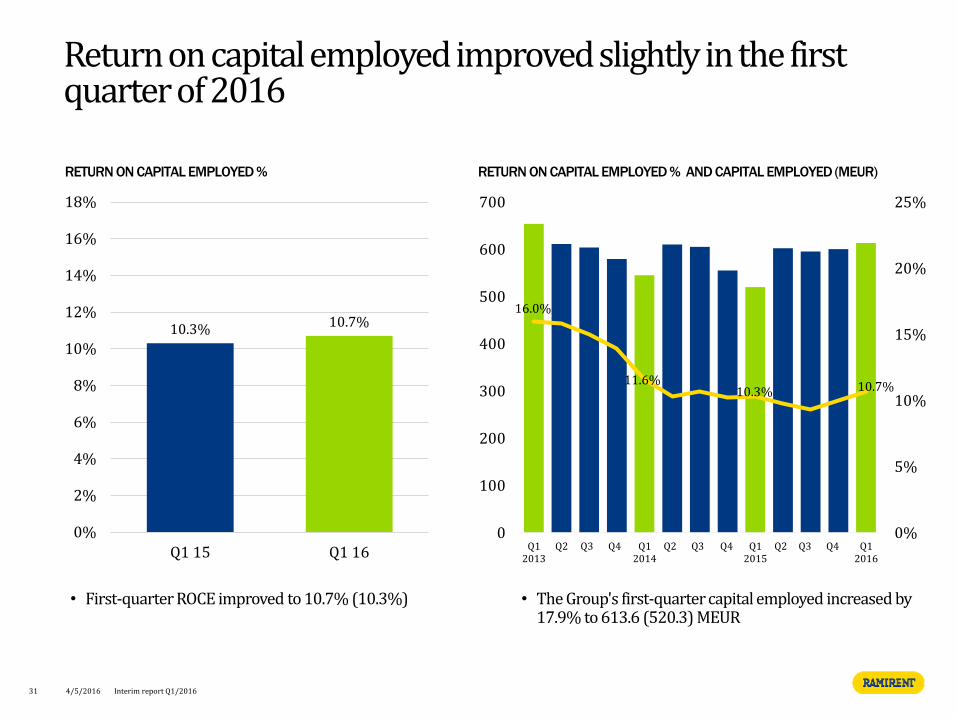

Return on capital employed improved slightly in the first quarter of 2016

RETURN ON CAPITAL EMPLOYED %

10.3% 10.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q1 15 Q1 16

• The Group's first-quarter capital employed increased by 17.9% to 613.6 (520.3) MEUR

RETURN ON CAPITAL EMPLOYED % AND CAPITAL EMPLOYED (MEUR)

31 4/5/2016 Interim report Q1/2016

• First-quarter ROCE improved to 10.7% (10.3%)

16.0%

11.6% 10.3% 10.7%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

700

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

18.8%

15.5%

4.0% 6.1%

15.0%

5.3%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Finland Sweden Norway Denmark The Baltics Central

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

RETURN ON CAPITAL EMPLOYED % (ROLLING 12 MONTHS)

ROCE continued to improve in Finland and Denmark

32 4/5/2016 Interim report Q1/2016

Return on equity above our long-term financial target

RETURN ON EQUITY %

9.7%

14.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q1 15 Q1 16

• The Group's total equity amounted to MEUR 280.4 (291.1) at the end of March 2016

• Equity per share was 2.60 (2.70) at the of end of the first quarter

• On a rolling 12 months basis Return on equity was 14.6% (9.7%), which was slightly above long-term financial target of 12% per fiscal year

ROE % AND TOTAL EQUITY (MEUR)

20.7%

13.6%

9.7%

14.6%

0%

5%

10%

15%

20%

25%

0

50

100

150

200

250

300

350

400

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

33

Financial target: Return on Equity of 12% per fiscal

year

4/5/2016 Interim report Q1/2016

34

Financial position

4/5/2016 Interim report Q1/2016

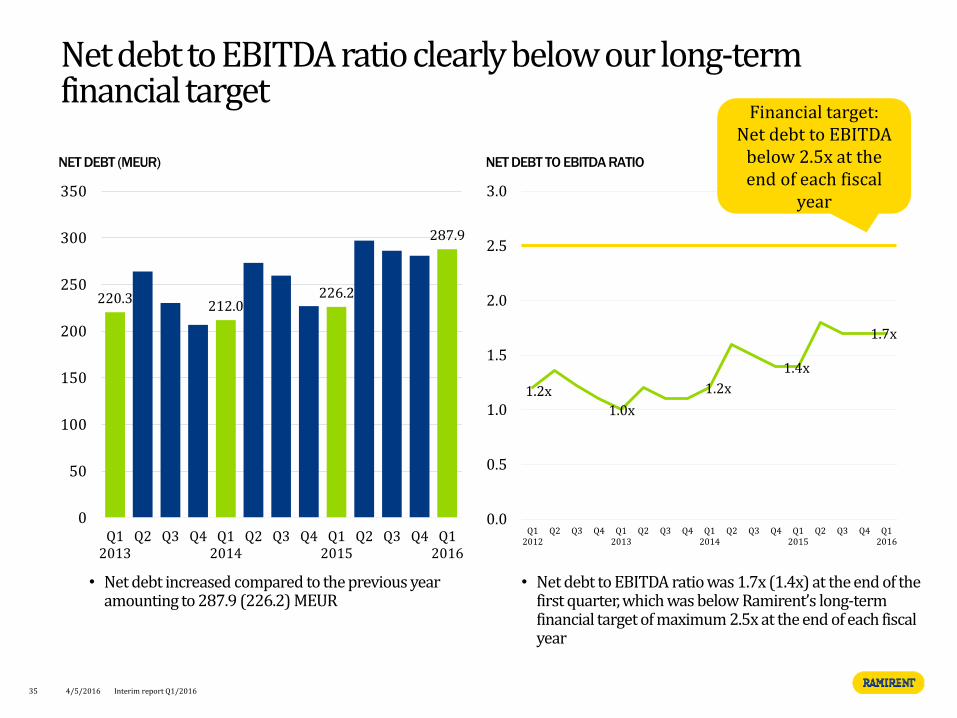

Net debt to EBITDA ratio clearly below our long-term financial target

NET DEBT (MEUR)

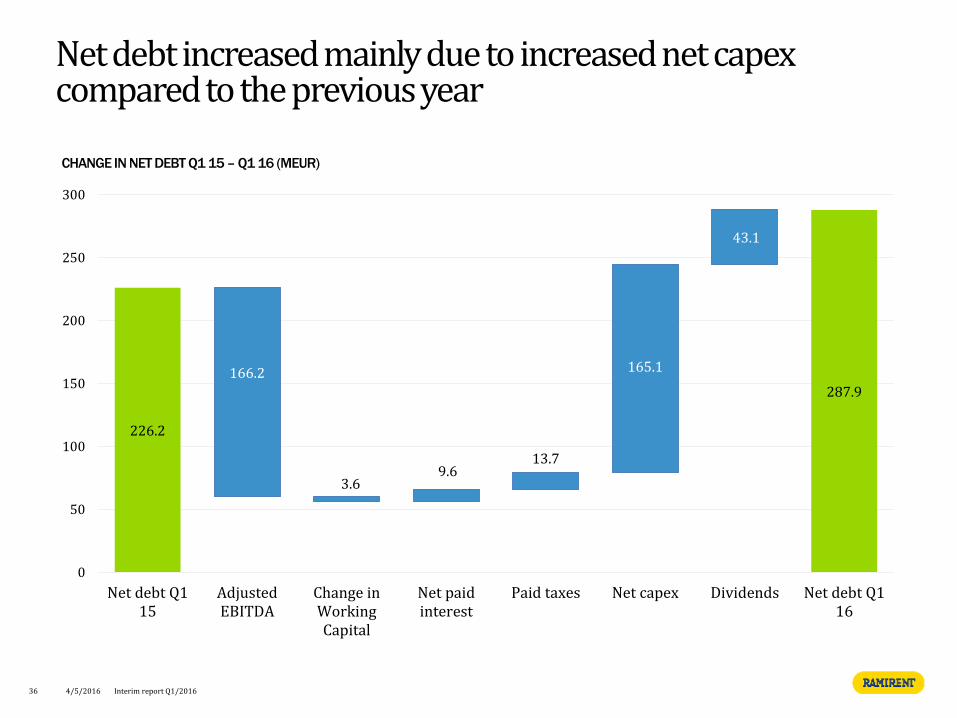

• Net debt to EBITDA ratio was 1.7x (1.4x) at the end of the first quarter, which was below Ramirent’s long-term financial target of maximum 2.5x at the end of each fiscal year

• Net debt increased compared to the previous year amounting to 287.9 (226.2) MEUR

NET DEBT TO EBITDA RATIO

1.2x

1.0x

1.2x

1.4x

1.7x

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

35

Financial target: Net debt to EBITDA

below 2.5x at the end of each fiscal

year

4/5/2016 Interim report Q1/2016

220.3 212.0

226.2

287.9

0

50

100

150

200

250

300

350

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

Net debt increased mainly due to increased net capex compared to the previous year

CHANGE IN NET DEBT Q1 15 – Q1 16 (MEUR)

36 4/5/2016 Interim report Q1/2016

226.2

287.9

166.2

3.6 9.6

13.7

165.1

43.1

0

50

100

150

200

250

300

Net debt Q115

AdjustedEBITDA

Change inWorkingCapital

Net paidinterest

Paid taxes Net capex Dividends Net debt Q116

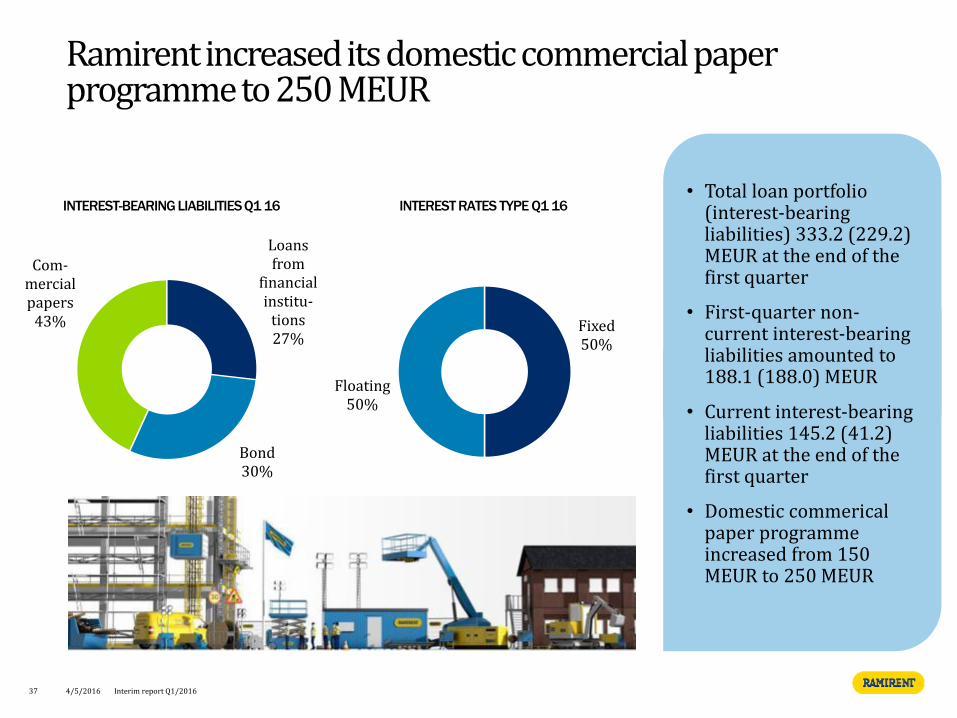

Fixed 50%

Floating 50%

• Total loan portfolio (interest-bearing liabilities) 333.2 (229.2) MEUR at the end of the first quarter

• First-quarter non-current interest-bearing liabilities amounted to 188.1 (188.0) MEUR

• Current interest-bearing liabilities 145.2 (41.2) MEUR at the end of the first quarter

• Domestic commerical paper programme increased from 150 MEUR to 250 MEUR

Ramirent increased its domestic commercial paper programme to 250 MEUR

Loans from

financial institu-

tions 27%

Bond 30%

Com-mercial papers

43%

INTEREST-BEARING LIABILITIES Q1 16 INTEREST RATES TYPE Q1 16

37 4/5/2016 Interim report Q1/2016

REPAYMENT SCHEDULE OF INTEREST-BEARING LIABILITES (MEUR)

At the end of the first quarter, Ramirent had unused committed back–up loan facilities of EUR 127.3

• Ramirent had unused committed back-up loan facilities of 127.3 (189.0) MEUR available at the end of the first quarter

• First-quarter average interest rate of the loan portfolio including interest rate hedges was 2.2% (3.0%)

• In addition to bank facilities, Ramirent is utilising a domestic commercial paper programme of up to 250 MEUR

75

95

100

145

2016 2017 2018 2019 2020

Net debt EUR 287.9 million

EUR 415.0 million in committed credit facilities

38 4/5/2016 Interim report Q1/2016

For further information

4/5/2016 Interim report Q1/2016 39

4/5/2016 Interim report Q1/2016 40

Appendix

• Ramirent is a leading equipment rental solutions group operating in 10 countries with 2015 net sales of EUR 636 million

• Ramirent’s mission is to combine the best equipment, services and know-how into rental solutions that simplify customer’s business

• Ramirent serves a broad range of customer sectors including construction, industry, services, the public sector and households

• Ramirent has 2,685 employees operating from 284 customer centres

• Ramirent was founded in 1955 and is listed on the NASDAQ Helsinki (RMR1V)

Ramirent is a leading equipment rental solutions group serving a large customer base

Russia and Ukraine presence through JV Fortrent

JV Fehmarnbelt Solutions Services A/S, with Zeppelin Rental

NET SALES PER SEGMENT Q1 16

NET SALES BY CUSTOMER SECTOR Q1 16

NET SALES BY BUSINESS AREA Q1 16

Finland 26%

Sweden 36%

Norway 19%

Denmark 7%

Europe East –Baltics 4%

Europe Central 8%

Construction 51%

Industrial 19%

Services & Retail 23%

Public 3%

Other 4%

Private 1%

General Rental 63%

Solutions 32%

Temporary Space 5%

41 4/5/2016 Interim report Q1/2016

42

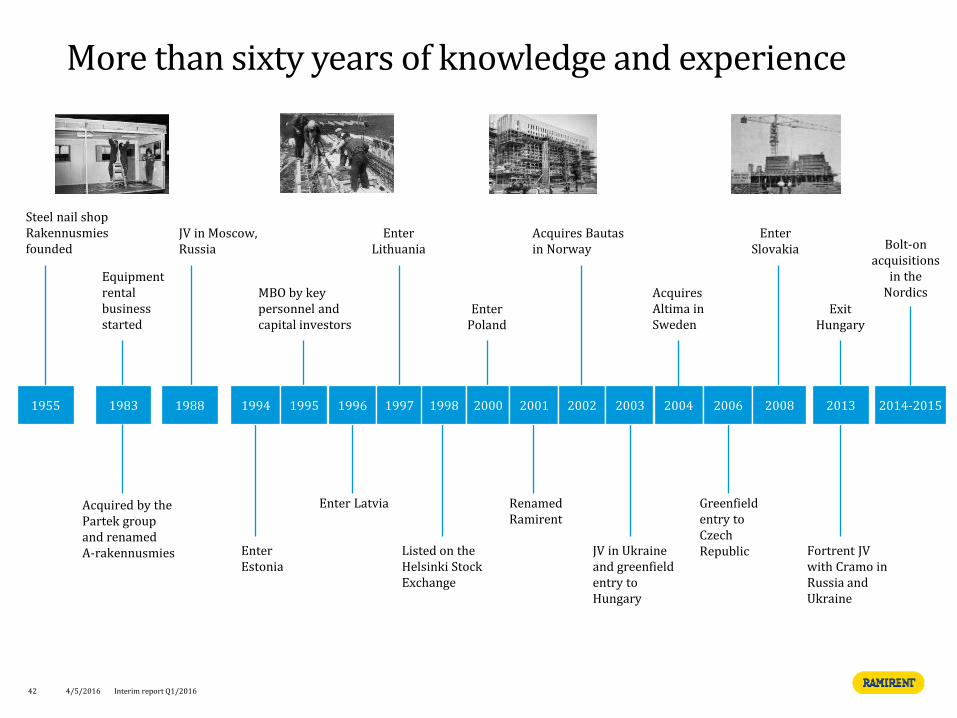

Steel nail shop Rakennusmies founded

Equipment rental business started

JV in Moscow, Russia

Enter Estonia

MBO by key personnel and capital investors

Enter Lithuania

Listed on the Helsinki Stock Exchange

Enter Poland

Enter Slovakia

1983 1955 1988 1994 1995 1996 1997 1998 2000 2001 2002 2003 2004 2006 2013 2008

Acquires Bautas in Norway

Acquires Altima in Sweden

Fortrent JV with Cramo in Russia and Ukraine

Acquired by the Partek group and renamed A-rakennusmies

Enter Latvia Renamed Ramirent

Greenfield entry to Czech Republic JV in Ukraine

and greenfield entry to Hungary

Exit Hungary

2014-2015

Bolt-on acquisitions

in the Nordics

More than sixty years of knowledge and experience

4/5/2016 Interim report Q1/2016

Benefits More uptime in core operations due to less downtime in equipment, less maintenance costs, right choice of equipment improves efficiency, less product liability risk

Planning

On-site services

Logistics

Merchandise sale

Rental insurance

Training

Benefits Lighter balance sheets, less investments

43

Benefits Understanding client requirements helps to customise product and service selection and further improve productivity

Heavy Equipment

Access Equipment Lifts, Hoists,

Scaffolding, Tower cranes

Modules and site equipment

Light Equipment Tools, power and heating

equipment

Integrated rental Solutions

Benefits Easy to buy, reduced number of subcontractors, increased focus on the core business

Ramirent's offering stretches from single equipment rental to solutions

4/5/2016 Interim report Q1/2016

We continue to pursue sustainable profitable growth through five strategic focus themes

Customer facing

Internal

44 4/5/2016 Interim report Q1/2016

CHARACTERISTICS

• Local business, where Ramirent provides equipment and services

• Higher gross margin, but must carry fixed costs of the customer centre network

• Higher share of equipment rental

• Focus on service level and efficiency

Interim report Q1/2016

CHARACTERISTICS

• Larger projects, where Ramirent is involved early in the process

• Lower gross margin, with more subcontracted services

• More service intense and less employed capital

• Focus on turn-key solutions and know-how

CHARACTERISTICS

• Long rental contracts

• Ramirent provides modules for accommodation, offices, schools & health care

• High margins but capital intense

• Stable cash flow profile

Ramirent targets sustainable profitable growth by developing the business mix

45 4/5/2016

Business areas with different characteristics and risk profiles

Share of Group sales

Ramirent targets a business mix that balances growth opportunities, profitability and risk

GROUP NET SALES SPLIT BY BUSINESS AREA Q1 16

46 Interim report Q1/2016 4/5/2016

Temporary Space

5%

General Rental 63%

Solutions 32%

Ramirent can generate growth in multiple ways

Ramirent seeks growth from five different sources

New customer segments

New geographies

Bolt-on acquisitions

Capturing outsourcing opportunities in construction sector

Increasing services, customer project coordination and solutions

Grow with new customers

Increased share-of-wallet with current customers

Strategic transactions

47

Capturing outsourcing opportunities in other sectors

4/5/2016 Interim report Q1/2016

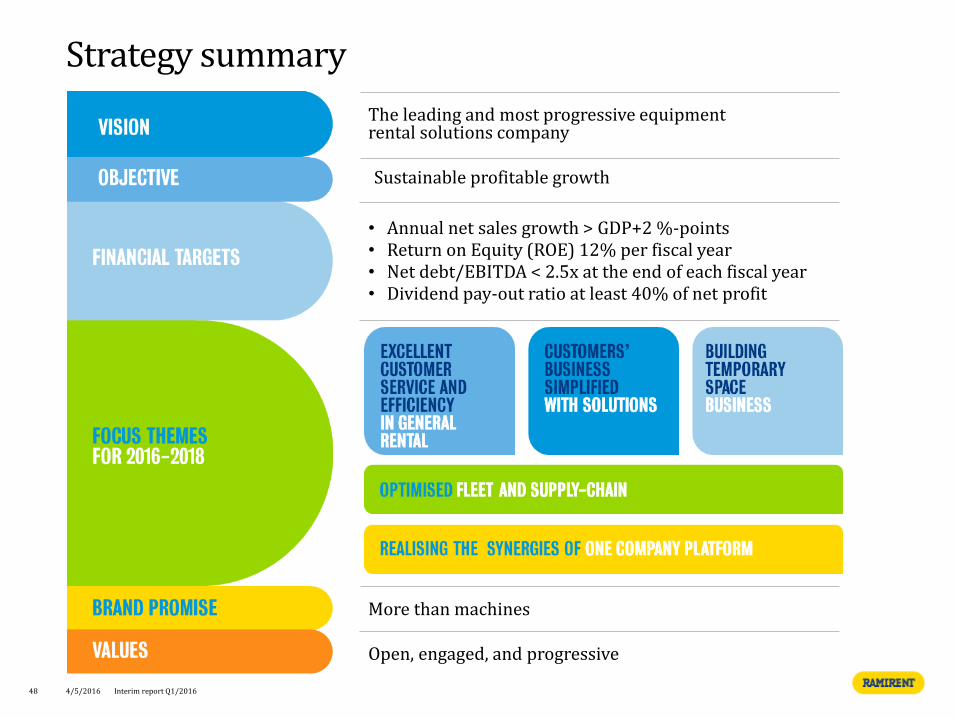

Strategy summary

The leading and most progressive equipment rental solutions company

• Annual net sales growth > GDP+2 %-points • Return on Equity (ROE) 12% per fiscal year • Net debt/EBITDA < 2.5x at the end of each fiscal year • Dividend pay-out ratio at least 40% of net profit

More than machines

Open, engaged, and progressive

Sustainable profitable growth

48 4/5/2016 Interim report Q1/2016

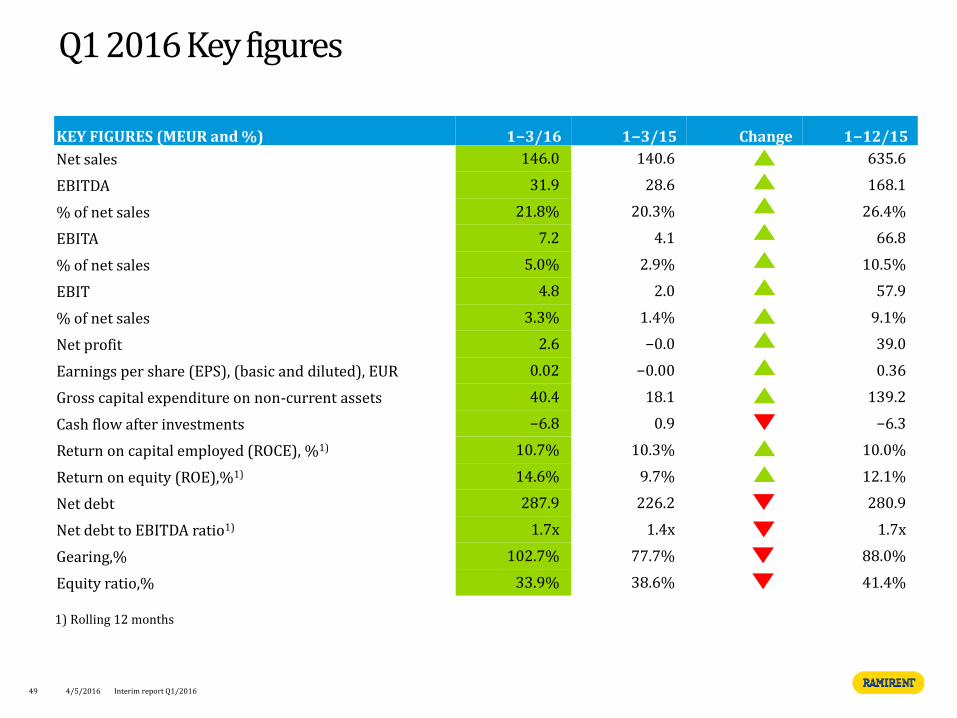

Q1 2016 Key figures

49 4/5/2016

KEY FIGURES (MEUR and %) 1−3/16 1−3/15 Change 1−12/15

Net sales 146.0 140.6 635.6

EBITDA 31.9 28.6 168.1

% of net sales 21.8% 20.3% 26.4%

EBITA 7.2 4.1 66.8

% of net sales 5.0% 2.9% 10.5%

EBIT 4.8 2.0 57.9

% of net sales 3.3% 1.4% 9.1%

Net profit 2.6 −0.0 39.0

Earnings per share (EPS), (basic and diluted), EUR 0.02 −0.00 0.36

Gross capital expenditure on non-current assets 40.4 18.1 139.2

Cash flow after investments −6.8 0.9 −6.3

Return on capital employed (ROCE), %1) 10.7% 10.3% 10.0%

Return on equity (ROE),%1) 14.6% 9.7% 12.1%

Net debt 287.9 226.2 280.9

Net debt to EBITDA ratio1) 1.7x 1.4x 1.7x

Gearing,% 102.7% 77.7% 88.0%

Equity ratio,% 33.9% 38.6% 41.4%

1) Rolling 12 months

Interim report Q1/2016

Return on investment improved slightly in the first quarter

RETURN ON INVESTMENT %

9.7%

10.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q1 15 Q1 16

• The Group's invested capital increased by 17.9% to 613.6 (520.3) MEUR due to investments in the rental fleet to capture growth opportunities in growing business areas

• Comparison figures adjusted accordingly

RETURN ON INVESTMENT % AND INVESTED CAPITAL (MEUR)

16.6%

11.2% 9.7%

10.8%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

700

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4 Q12016

50 4/5/2016 Interim report Q1/2016

• With the new formula, first-quarter ROI was 10.8% (9.7%)

Calculation of Return on investments (ROI %) has been changed from the beginning of 2016

51 4/5/2016 Interim report Q1/2016

12.9%

-249 basis points 40

basis points

10.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

ROI Q1 15 (old) Change incalculation

Profitabilityimprovement

ROI Q1 16 (new)

• In the new Return on investment (ROI) calculation, exchange rates are excluded from the nominator in the formula

• The comparative information is adjusted accordingly in the first quarter report

• First-quarter 2016 ROI % with the new formula was 10.8% (9.7%)

• Change in calculation decreased ROI by 249 bps, while improved profitability had a positive impact of 40 bps to the ROI

RETURN ON INVESTMENT (ROI %) BRIDGE Q1 15 – Q1 16

New ROI =

𝑅𝑒𝑠𝑢𝑙𝑡 𝑏𝑒𝑓𝑜𝑟𝑒 𝑡𝑎𝑥𝑒𝑠+𝑖𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑎𝑛𝑑 𝑜𝑡ℎ𝑒𝑟 𝑓𝑖𝑛𝑎𝑛𝑐𝑖𝑎𝑙 𝑒𝑥𝑝𝑒𝑛𝑠𝑒𝑠𝑒𝑥𝑐𝑙𝑢𝑑𝑖𝑛𝑔 𝑓𝑥. 𝑑𝑖𝑓𝑓𝑒𝑟𝑒𝑛𝑐𝑒𝑠

𝑇𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑠𝑡 −𝑖𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑏𝑒𝑎𝑟𝑖𝑛𝑔 𝑙𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠 (𝑎𝑣𝑒𝑟𝑎𝑔𝑒 𝑜𝑣𝑒𝑟 𝑡ℎ𝑒 𝑓𝑖𝑛𝑎𝑛𝑐𝑖𝑎𝑙 𝑝𝑒𝑟𝑟𝑖𝑜𝑑)

∗ 100%

Old ROI =

𝑅𝑒𝑠𝑢𝑙𝑡 𝑏𝑒𝑓𝑜𝑟𝑒 𝑡𝑎𝑥𝑒𝑠+𝑖𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑎𝑛𝑑 𝑜𝑡ℎ𝑒𝑟 𝑓𝑖𝑛𝑎𝑛𝑐𝑖𝑎𝑙 𝑒𝑥𝑝𝑒𝑛𝑠𝑒𝑠

𝑇𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑠𝑡 −𝑖𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑏𝑒𝑎𝑟𝑖𝑛𝑔 𝑙𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠 (𝑎𝑣𝑒𝑟𝑎𝑔𝑒 𝑜𝑣𝑒𝑟 𝑡ℎ𝑒 𝑓𝑖𝑛𝑎𝑛𝑐𝑖𝑎𝑙 𝑝𝑒𝑟𝑟𝑖𝑜𝑑)

∗ 100%

Ramirent‘s largest shareholders at the end of March 2016

TRADING INFORMATION Listing: NASDAQ HELSINKI Segment: Mid Cap Sector: Industrials Trading code: RMR1V SHARE INFORMATION Q1 16 Closing price 5.75 (6.61) Highest 6.41 (7.45) Lowest 5.05 (6.35) VWAP* 5.86 (6.99)

At the end of March 2016 a total of 52.1% (51.2%) of the company’s shares were owned by nominee-registered and non-Finnish investors

52

LARGEST SHAREHOLDERS 31 MARCH 2016

Largest shareholders Number of

shares % of share

capital

1. Nordstjernan AB 27,513,716 25.31%

2. Oy Julius Tallberg Ab 12,207,229 11.23%

3. Nordea funds 5,384,915 4.95%

4. Varma Mutual Pension Insurance Company 3,640,865 3.35%

5. Ilmarinen Mutual Pension Insurance Company 3,445,154 3.17%

6. Aktia funds 2,055,558 1.89%

7. Ramirent Plc 948,014 0.87%

8. Pensionsförsäkringsaktiebolaget Veritas 708,353 0.65%

9. Föreningen Konstsamfundet R.f 593,500 0.55%

10. The State Pension Fund 532,000 0.49%

Subtotal 10 largest shareholders 57,029,304 52.47%

Other shareholders 51,668,024 47.53%

Total number of shares 108,697,328 100.00%

*VWAP = Volume weighted average trading price

4/5/2016 Interim report Q1/2016

Ramirent's share price development in 2016

53

INDEX

4/5/2016 Interim report Q1/2016

70

80

90

100

110Ramirent

OMX Helsinki

OMX Helsinki Mid Cap