restart the carbon market - ieta 23/side-event-presentations/restart the... · restart the carbon...

TRANSCRIPT

RestarttheCarbonMarketWednesday8th November2017 | 15:30– 17:00

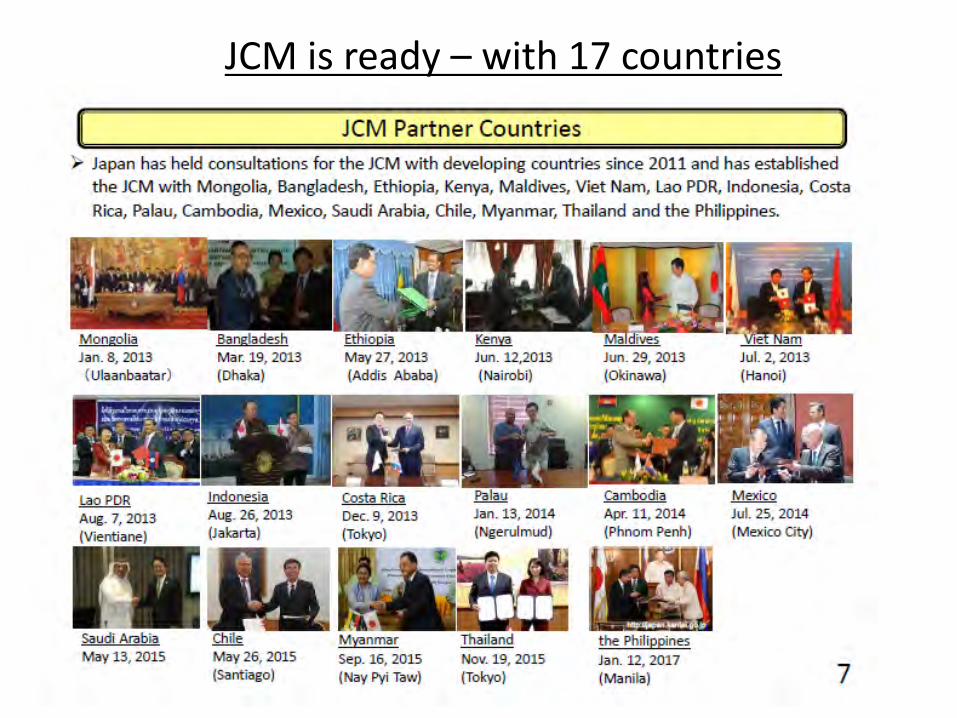

JCMisready– with17countries

CanJCMbetakeoff?- ProgressandtheFuture

TakashiHongoSeniorFellow

Mitsui&Co.GlobalStrategicStudiesInstitute

3

RestartthecarbonmarketIETABusinessHub3:30pm-5:00pm,on8Nov.2017

TrendofGHGemissionandreductiontargets

20203.8%reductionfrom2005

205080%reduction

203026%reductionfrom2013

100milliontonCO2e

Source,RewriteofMinistryofEnvironmentPP4

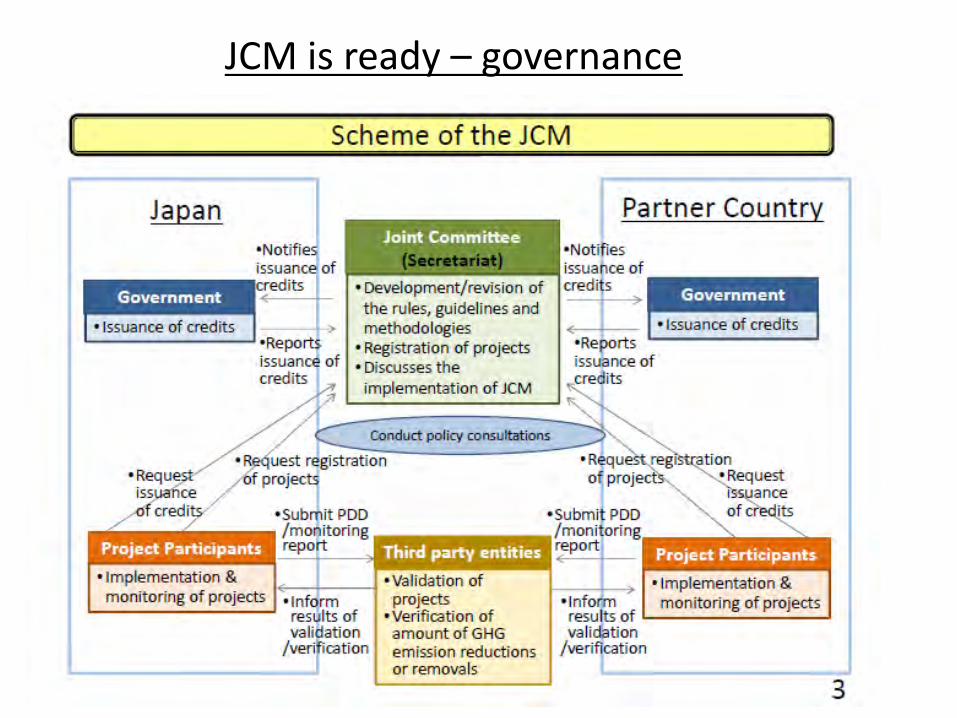

JCMisready– governance

JCMisready– registryasakeyinfrastructure

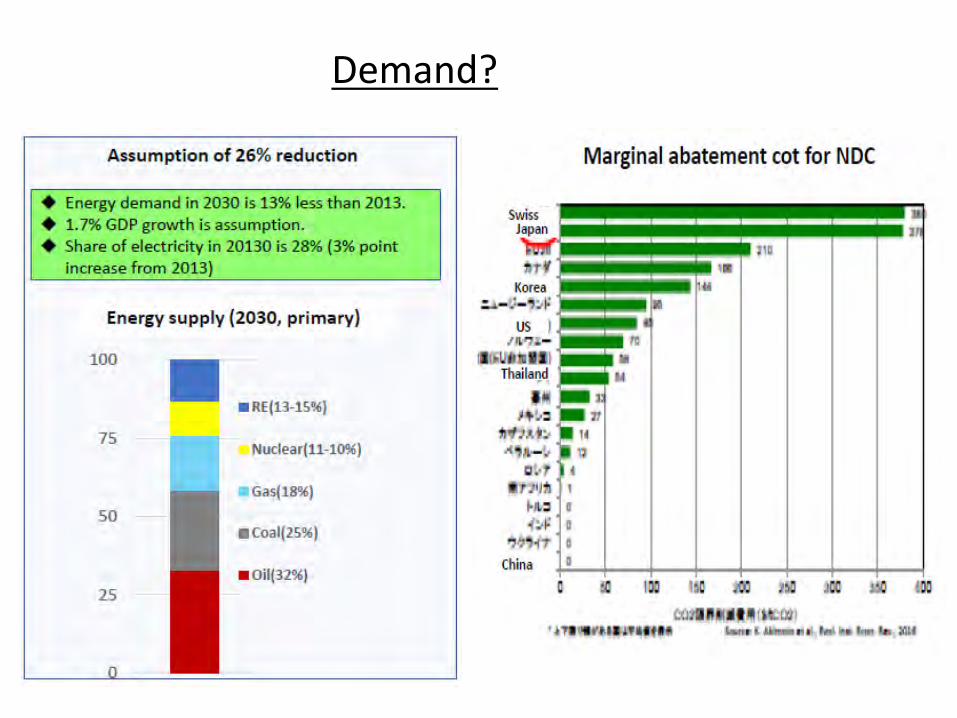

Demand?

JCM– future

Legal base – Colombian carbon taxArt. 221 Tax Reform of 2016; and decree 926* of 1 June 2017

South Pole Group

● 15.000 Pesos / tCO2e from liquid fossil fuels● Carbon Credits eligibility criteria:➞ Colombian credits➞ For 2017, any credit➞ Vintage 2010 and later➞ DOE / VVB verified➞ Retired in Markit / APX / ICONTEC’s own registry

Pág. 9

*Por el cual se adiciona el epígrafe de la Parte 5 y el Título 5 a la Parte 5 del Libro 1 del Decreto Único Reglamentario en Materia Tributaria, 1625 de 2016 y el Título 11 de la Parte 2 de Libro 2 al Decreto Único Reglamentario del Sector Ambiente y Desarrollo Sostenible, 1076 de 2015, para reglamentar el parágrafo 3 del artículo 221 y el parágrafo 2 del artículo 222 de la Ley 1819 de 2016

Some considerations:- No Carbon tax on biofuels- Natural gas is only taxed in the petrochemical sector- International flights are exempted- The offsetting has to be one the name of the fuel retailer.

AboutCarbon Market Institute

• Australia’s peak industry body for climate change, business & markets.

• Provide market intelligence to help business seize opportunities in rapidly evolving carbon markets.

• Facilitating connections between business, policy makers and thought leaders.

• Engaging leaders, shaping policy in the transition to a zero-carbon economy.

• Building capacity to optimise commercial opportunities in the transition.

• Harness our membership base to have influence and impact.

MembersCarbon Market Institute

2017 Australian Climate Policy Review

• Process not confirmed but expected outcome/recommendations by December 2017

• Key conclusions from Submissions:

o Need to frame policy around a long term target – i.e. zero net emissions by 2050

o Treat energy/electricity emission separately but integrated

o Safeguard mechanism must evolve and baselines lowered over time

o Emission Reduction Fund (ERF) – has a key role in future domestic credit supply

o International units should be available to be used for compliance

o Must protect competitiveness of trade exposed entities

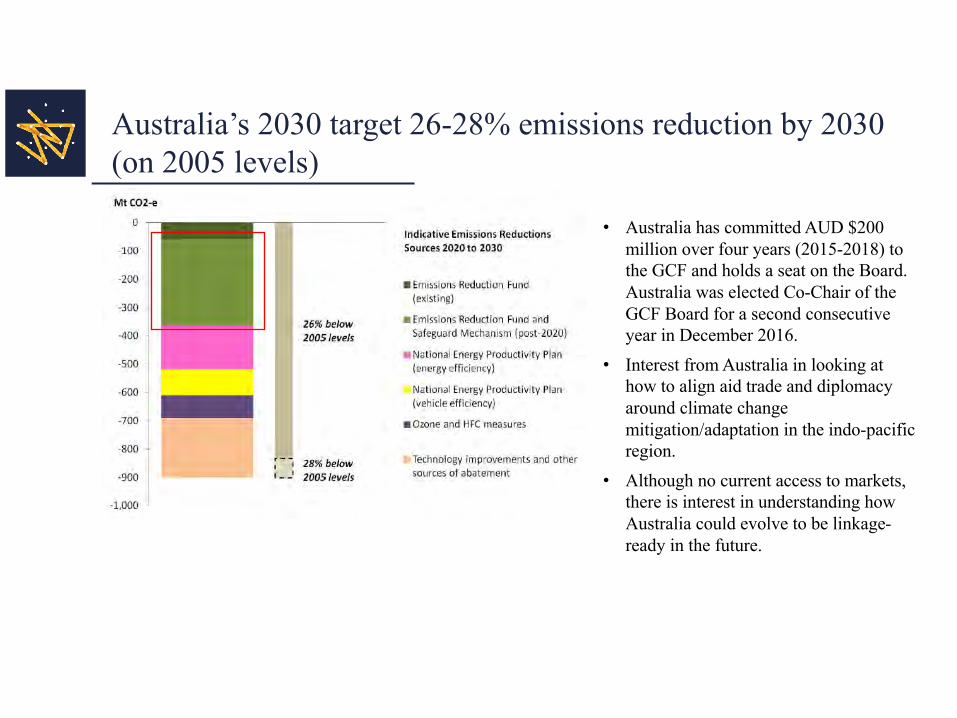

Australia’s 2030 target 26-28% emissions reduction by 2030 (on 2005 levels)

• Australia has committed AUD $200 million over four years (2015-2018) to the GCF and holds a seat on the Board. Australia was elected Co-Chair of the GCF Board for a second consecutive year in December 2016.

• Interest from Australia in looking at how to align aid trade and diplomacy around climate change mitigation/adaptation in the indo-pacific region.

• Although no current access to markets, there is interest in understanding how Australia could evolve to be linkage-ready in the future.

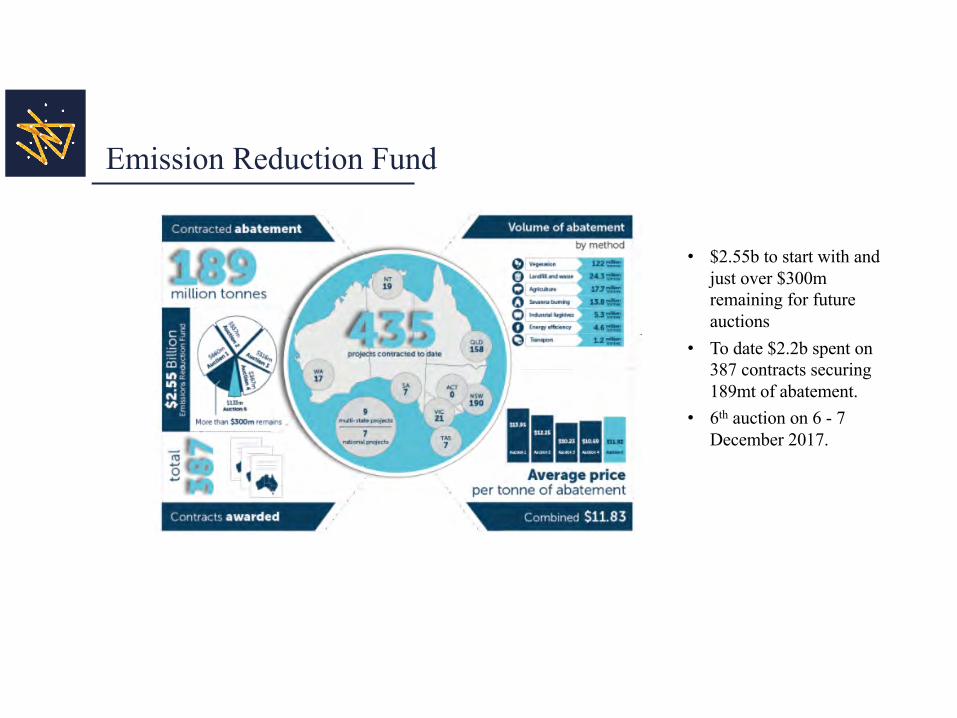

Emission Reduction Fund

• $2.55b to start with and just over $300m remaining for future auctions

• To date $2.2b spent on 387 contracts securing 189mt of abatement.

• 6th auction on 6 - 7 December 2017.

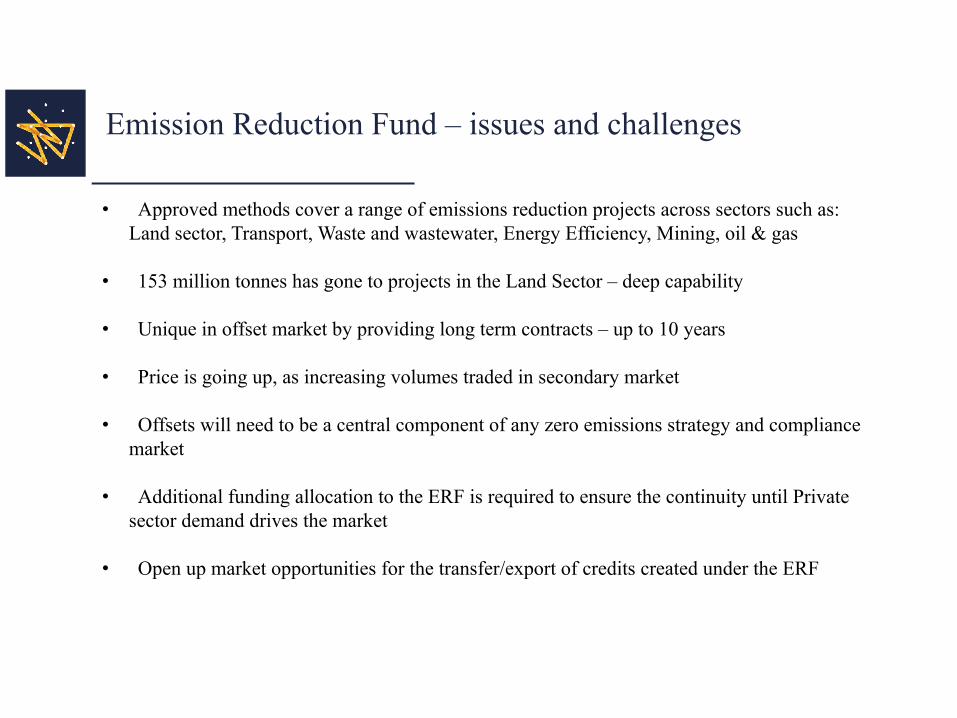

Emission Reduction Fund – issues and challenges

• Approved methods cover a range of emissions reduction projects across sectors such as: Land sector, Transport, Waste and wastewater, Energy Efficiency, Mining, oil & gas

• 153 million tonnes has gone to projects in the Land Sector – deep capability

• Unique in offset market by providing long term contracts – up to 10 years

• Price is going up, as increasing volumes traded in secondary market

• Offsets will need to be a central component of any zero emissions strategy and compliance market

• Additional funding allocation to the ERF is required to ensure the continuity until Private sector demand drives the market

• Open up market opportunities for the transfer/export of credits created under the ERF

Safeguard Mechanism– issues and challenges

• Baselines cover 350 facilities that exceed 100K t/co2e

• Must purchase ACCUs if there is an emissions exceedance

• First reporting period in Oct 2017, compliance 1 Mar 2018

• Likely to be some emissions exceedance/compliance requirements in this first period

• Need clarity on:o The contribution of the SGM to the target - the trajectory of the baselineso The conditions, criteria and process for how baselines will be adjusted to decline in the

post-2020 periodo If electricity is in or out

• The Safeguard Mechanism can evolve into an effective trading system and drive below BAU emissions

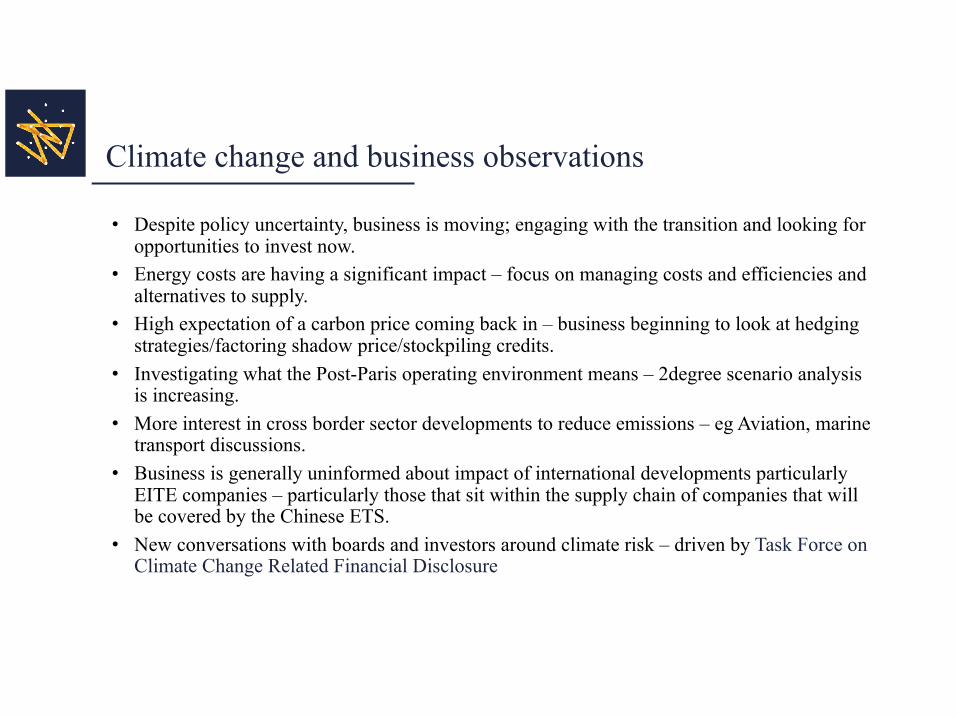

Climate change and business observations

• Despite policy uncertainty, business is moving; engaging with the transition and looking for opportunities to invest now.

• Energy costs are having a significant impact – focus on managing costs and efficiencies and alternatives to supply.

• High expectation of a carbon price coming back in – business beginning to look at hedging strategies/factoring shadow price/stockpiling credits.

• Investigating what the Post-Paris operating environment means – 2degree scenario analysis is increasing.

• More interest in cross border sector developments to reduce emissions – eg Aviation, marine transport discussions.

• Business is generally uninformed about impact of international developments particularly EITE companies – particularly those that sit within the supply chain of companies that will be covered by the Chinese ETS.

• New conversations with boards and investors around climate risk – driven by Task Force on Climate Change Related Financial Disclosure

What’s coming…

• Delayed decisions on National Energy Guarantee and policy review

• Business understand that a carbon price will come back – more explicit if there is a change of Federal Government

• Action at the State level – net-zero emissions targets will drive new markets

• Demand for low carbon goods, services and financing will lead to export market opportunity –government have a role in aligning aid, trade and diplomacy

• Innovation in public/private financing models to fund low carbon dev & Paris commitments