reg. no. gr/rnp/goa/32 rni no....

TRANSCRIPT

Panaji, 22nd March, 2007 (Chaitra 1, 1929) SERIES I No. 51

GOVERNMENT OF GOA

Department of Finance

Revenue & Control Division___

Notification

3/2/2006-Fin(R&C)(2)

In exercise of the powers conferred bysub-section (1) of section 14 of the GoaEntertainment Tax Act, 1964 (Act 2 of 1964), andall other powers enabling it in this behalf, theGovernment of Goa hereby makes the followingrules, namely:-

1. Short title and commencement.� (1) Theserules may be called the Goa Entertainment TaxRules, 2007.

(2) They shall come into force from the dateof their publication in the Official Gazette.

2. Definitions.� In these rules, unless thecontext otherwise requires:

(a) �Act� means the Goa EntertainmentTax Act, 1964 (Act 2 of 1964).

(b) �Advisory Committee� means aCommittee comprising of not more than fiveeminent persons of national stature in the fieldof audiovisual entertainment and other artisticand literary activities, constituted by theGovernment for a period of five years;

RNI No. GOAENG/2002/6410Reg. No. GR/RNP/GOA/32

EXTRAORDINARY

(c) �Assistant Entertainment Tax Officer�means a person appointed as AssistantEntertainment Tax Officer by the Commissionerunder sub-section (3) of section 2A of the Act;

(d) �Appellate Authority� means theAssisstant Commissioner of Entertainment Taxor such other Officer not lower than theCommissioner of Entertainment Tax appointedby the Government as Appellate Authority incase order appealed against is passed by theAssistant Commissioner of Entertainment Tax;

(e) �Appropriate Assessing Authority�means,�

(i) in relation to any proprietor or person,the Assistant Commissioner of EntertainmentTax or the Entertainment Tax Officer orAssistant Entertainment Tax Officer withinwhose jurisdiction, his place of entertainmentis situated; or

(ii) in relation to any proprietor or personwho has more than one place ofentertainment in the State of Goa, theAssistant Commissioner of Entertainment Taxor the Entertainment Tax Officer or theAssistant Entertainment Tax Officer, withinwhose jurisdiction the Head Office of suchproprietor or person responsible for conductof activity of providing entertainment issituated in the State of Goa, or as specifiedby the Commissioner by way of special orgeneral order;

(iii) the Commissioner/Additional Com-missioner of Entertainment Tax, wherever

1300 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

the powers are conferred on him by or underthe provisions of the Act;

(f) �Appropriate Government Treasury�means any treasury of Taluka, sub-treasury orthe Reserve Bank of India, or a branch of theState Bank of India or its subsidiary or anybank so notified by the Government, situatedin the area in which the proprietor or personconcerned has his place of entertainment orits head office, if the activity providingentertainment is carried on at more than oneplace in the State of Goa;

(g) �Assistant Commissioner of EntertainmentTax� means a person appointed as AssistantCommissioner of Entertainment Tax by theGovernment under sub-section (2) of section2A of the Act;

(h) �casino� means a place whereentertainment is provided to any individual orgroups of persons by way of electronic andtable games, betting, gambling or any otherkind of activity of similar nature besides otherhospitality and entertainment related functions;

(i) �drama� with it�s grammatical variationsmeans a composition in prose or versearranged for enactment by actors on a stageand intended to portray life or character orto tell a story by means of dialogue and actionsof the enactors and include opera, ballet anddance-drama;

(j) �Entertainment Tax Inspector� means aperson appointed as Entertainment TaxInspector by the Commissioner undersub-section (3) of section 2A of the Act;

(k) �Entertainment Tax Officer� means aperson appointed as Entertainment Tax Officerby the Government under sub-section (2) ofsection 2A of the Act;

(l) �form� means a form appended to theseRules;

(m) �Government� means the Governmentof Goa;

(n) �quarter� means the period of threemonths ending on the 30th June, 30th September,31st December or 31st March;

(o) �registered proprietor or person� meansa proprietor or person registered under the Act;

(p) �return period� means the period forwhich the returns of tax due and paid are tobe furnished by proprietor or person underthese Rules;

(q) �rules� means rules made under the Act;

(r) �section� means section of the Act;

(s) �tax period� means such period as maybe specified by the Commissioner for paymentof tax;

(t) �theatrical performance� with it�sgrammatical variations means any performanceon a stage or relating to theatre or to theacting or presentation of plays and includemusic and dance;

(u) �ticket or season ticket� means a ticketissued by a proprietor or person for admissionof a person or persons to an entertainmentperformance;

(v) �turnover means��

(i) total amount of charges for admissionto a place of entertainment received orreceivable by a proprietor or person duringa given period;

(ii) amount charged for boat cruise//rides, water sports, parasailing, etc.;

(c) charges/income received by proprietoror person towards casino games includingincome from tickets issued for admission toa casino;

(d) income from number of connectionsof cable through TV antennae, headendcontrol and distributor, DTH disc service etc.;

(iii) any other receipts that are chargesfor admission .

3. Registration of proprietor or person.�(1) An application for registration shall be madeby a proprietor or person as stated insub-sections (1) and (2) of section 3G of the Act,in Form ENT � I appended hereto, within theperiod specified in the said sub-sections. Theregistration fees as specified in Schedule �E� tothe Act shall be paid by challan in FormENT�III appended hereto in the appropriateGovernment treasury. Receipted copy of thechallan thereof shall be submitted alongwith theapplication:

OFFICIAL GAZETTE � GOVT. OF GOA 1301SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

Provided that, no proprietor or person, whois registered as hotelier under the Goa Tax onLuxuries Act, 1988 (Act No. 17 of 1988) andholding a valid registration certificate under thesaid Act, shall be required to pay registrationfees under the Act.

(2) Provisions of sub-rule (1) above, shall alsobe applicable to any proprietor or person makingapplication for registration after succession of theactivity of providing entertainment registeredunder the Act and the fees for registration shallbe payable alongwith such application.

(3) An application for registration shall be made,signed and verified in the case of:-

(a) A proprietorship, by the proprietor or bya person;

(b) a firm, by partner thereof;

(c) a Hindu Undivided Family, by the Kartaor an adult member thereof;

(d) a Body Corporate (including a company,co-operative society or a corporation or localauthority), by a Director, Manager, Secretaryor Principal Officer thereof or by a person dulyauthorized to act on it�s behalf;

(e) an association of individuals to whichclause (b), (c) and (d) does not apply, by thePrincipal Officer or the person managing theactivity of providing entertainment;

(f) the Government, by a person dulyauthorized to act on it�s behalf

(4) The registration fee once paid shall not berefunded under any circumstances.

4. Issue of Certificate of Registration.�(1) The Appropriate Assessing Authority, onmaking such enquiries as it may think necessaryand on being satisfied of the genuineness of theinformation furnished and on ascertaining thatregistration fee as specified in Schedule �E�appended to the Act has been paid, shall registerthe proprietor or person and shall issue acertificate of registration in Form ENT�IIappended hereto.

The certificate of registration issued to theproprietor or person,�

(a) shall take effect or be valid from thedate of accruing of liability to pay tax, if

application for registration is made within aperiod specified in sub-section (1) and (2) ofsection 3G of the Act;

(b) shall take effect or be valid from the dateon which the application has been filed withthe Appropriate Assessing Authority, if suchapplication is made after the expiry of theperiod specified in sub-sections (1) and (2) ofsection 3G of the Act;

(c) shall take effect, in case of an applicationunder sub-section (1) of section 3H of the Act,from the date of application or from such furtherdate as the Appropriate Assessing Authoritymay, by order, fix:

Provided that the proprietor or person filingsuch application within 30 days from the dateof coming into force of these Rules, shallbe issued registration certificate valid from1-9-2006.

(2) The certificate of registration initially issuedshall be valid for a period of one year or for anyother period as the Commissioner may prescribeexcept for provisional registration certificatewhich shall be issued to the proprietor or personmaking an application under sub-section (1) ofsection 3H which shall be valid for the year forwhich, it is issued or for such shorter period forwhich it is sought. The provisional registrationcertificate so issued shall lapse upon expiry ofits validity.

(3) Any registered proprietor or person mayobtain from Appropriate Assessing Authority onpayment of fee as specified in rule 29 of theserules in a Government treasury and on productionof receipt thereof, a duplicate copy of registrationcertificate issued to him.

5. Renewal of certificate of registration.�(1) An application for renewal of certificate ofregistration other than provisional registrationcertificate shall be made in Form ENT�I within30 days from the commencement of the financialyear.

(2) Every application for renewal shall beaccompanied with a receipted copy of the challanin proof of payment of renewal fees as specifiedin Schedule �E� to the Act, which shall not berefunded in any circumstances.

(3) The Appropriate Assessing Authority, onbeing satisfied that the information furnished in

1302 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

the application is in order, shall renew thecertificate of registration issued in FormENT�II by making necessary endorsement theretoor issuing a letter stating that the certificate ofregistration stands renewed for a periodspecified therein which shall form part ofthe certificate of registration originallyissued.

6. Cancellation of Registration Certificate.�(1) When any certificate of registration other thanprovisional registration certificate issued undersection 3H is required to be cancelled undersub-section (7) of section 3G of the Act, theproprietor or person shall make an applicationin Form ENT�IV to the Appropriate AssessingAuthority within 30 days from the date ofoccurrence of the event necessitatingcancellation and the Appropriate AssessingAuthority, on being satisfied about the correctnessof the facts, shall issue the order for cancellationof registration certificate effective from the dateof occurrence of such event.

(2)(a) When the Appropriate AssessingAuthority is satisfied at any time and for anyreasons other than that referred to in sub-rule(1) above, that the certificate of registration ofany proprietor or person requires cancellation,he shall, for reasons to be recorded in writing,and after giving the proprietor or person anopportunity of being heard, cancel thecertificate of registration with effect from suchdate as may be specified in the order to beissued and the liability of the proprietor or personto pay tax shall cease with effect from the saiddate.

(b) (i) Every proprietor or person whoseregistration certificate is cancelled otherwisethan on the basis of application in FormENT�IV, shall surrender the certificate ofregistration to the Appropriate AssessingAuthority upon service of such order ofcancellation.

(ii) The order of cancellation of certificateof registration shall be entered in theregister maintained in the office of theAppropriate Assessing Authority.

7. Amendment of certificate of registration.�(1) When any registered proprietor or personinforms the Appropriate Assessing Authority asregards to,�

(a) change in the name of his businessor nature of his activity of providingentertainment; or

(b) change in the place of business oropening of a new or on additional place ofproviding entertainment; or

(c) is a firm, and there is a change in theconstitution of the firm without dissolutionthereof, for the reason of demise of any partnerin the firm or otherwise; or

(d) is a trust and there is change in the trusteethereof; or

(e) is a guardian of a ward and there ischange in guardianship; or

(f) for any other reasons where the certificateof registration requires amendment.

The Appropriate Assessing Authority, afterconsidering such information, make suchenquiries or obtain such evidence as it may deemfit and thereafter on being satisfied shall amendthe certificate of registration.

(2) An amendment under the foregoingsub-rule shall be effective from the date of thecontingencies which necessitate the amendment.

(3) In case of a company, where two or morecompanies are to be merged or amalgamated byorder of the Court, Tribunal or order of the CentralGovernment, the Appropriate AssessingAuthority shall amend the certificate ofregistration effective from the date of such orders.

(4) If the registered proprietor or person failsto furnish the information as required undersection 3M of the Act, the Appropriate AssessingAuthority, on the basis of information which mayhave come to his notice otherwise, and if he issatisfied that there has been any of the changescovered under said section 3M or under clauses(a) to (f) of sub-rule (1) and/or sub-rule (3) above,and the certificate or other records of theproprietor or person maintained in his officerequired amendment, he may, after giving theproprietor or person an opportunity of beingheard, by order, amend the certificateaccordingly. For this purpose, the proprietor orperson shall submit the certificate of registrationand copies thereof to the Appropriate AssessingAuthority within the time specified in the order.

(5) If the proprietor or person to whomcertificate of registration in Form ENT�II heretohas been issued, reports that any one or moreadditional places of entertainment has or have

OFFICIAL GAZETTE � GOVT. OF GOA 1303SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

been opened or closed, his certificate ofregistration shall be so amended by the respectiveAppropriate Assessing Authority and he shall befurnished a copy of registration certificate for eachplace of entertainment.

(6) If the information referred to in section 3Mof the Act, relates to a branch of place ofentertainment, located outside the jurisdiction ofany Appropriate Assessing Authority, a copy ofthe information and of any order passed thereon,shall be forwarded to the Appropriate AssessingAuthority within whose jurisdiction the branchis situated.

(7) All the amendments in the certificate ofregistration shall be entered in the registermaintained in the office of the AppropriateAssessing Authority which shall be in FormENT�V.

8. Information to be furnished regardingchanges in business, etc.� The informationrequired to be submitted under section 3M ofthe Act, shall be furnished by the registeredproprietor or person to the Appropriate AssessingAuthority within 30 days of the occurrence ofevent as specified in said section 3M.

9. Payment of tax and filing of returns.�(1) A return to be filed by a registered personor proprietor under sub-section (2) of section4 of the Act, shall be in Form ENT�VI and shallbe filed within 20 days from the end of monthto the Appropriate Assessing Authority havingjurisdiction over the person or proprietor.

(2) A return to be filed as specified insub-rule (1) above shall be accompanied by areceipted copy of challan in Form ENT�III inproof of payment of the tax into appropriateGovernment treasury in respect of each of themonths to which it is payable.

In case of a registered proprietor or personhaving more than one place of entertainment,a consolidated return shall be submitted by theHead Office of the proprietor or person, to theAppropriate Assessing Authority and the sameshall include total payments due under the Actin respect of all the places of entertainment ofthe person or proprietor in the State of Goa.

(3) Where a registered person or proprietoreffects closure of his activity of providingentertainment and applies for cancellation ofregistration certificate in the middle of the month,

he shall file return for the period commencingfrom the first day of the month, till the date ofclosure of business within 15 days from the dateof closure.

(4) If any person or proprietor, having furnishedreturns under sub-section (2) of section 4,discovers any omission or incorrect statement,he may furnish a revised return as provided insub-section (4) of section 4 of the Act, before theexpiry of three months following the last dateprescribed for furnishing the original return andif the revised return shows a greater amount oftax to be due than was shown in the originalreturn, it shall be accompanied by a receiptedcopy of the challan for the payment of differentialamount of tax.

(5) Every registered proprietor or person shallpay the tax payable under the Act for every monthwithin 20 days from the expiry of each month.

(6) In respect of person or proprietor registeredunder section 3H of the Act, the payment of taxshall be made within 10 days from the expiryof each month.

10. Composition of tax under section 3D.�(1) Any registered proprietor or person coveredunder section 3D of the Act, may apply to theAppropriate Assessing Authority in FormENT�VII to compound the tax in accordance withsection 3D of the Act, 10 days before the dateof commencement of the month.

(2) The Appropriate Assessing Authority uponscrutiny of application received from theproprietor or person under sub-rule (1) shall grantpermission for payment of entertainment tax byway of composition. The lumpsum amount shallbe deposited in the Government Treasury within3 days from the date of grant of said permissionand furnish the receipted copy of the challan tothe respective Appropriate Assessing Authorityin proof of payment.

11. Exemption from payment of tax.� Anyproprietor or person in order to claim exemptionfrom payment of entertainment tax, under section5 of the Act, may make an application to theCommissioner in Form ENT�VIII. An applicationalongwith a receipted copy of challan in proofof payment of fee of Rs.100/- into a GovernmentTreasury shall be submitted at least 10 daysbefore the date of entertainment. An applicationfor exemption may, after the period so specified,be entertained if the applicant satisfies to the

1304 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

Commissioner that he had sufficient cause for notpresenting the application within such period.The Commissioner on being satisfied, shall issuethe exemption certificate with such conditionsas may be specified therein.

12. Concessions for members of the armedforces.� (1) In the case of entertainment givenby military , air, and naval wings of the armedforces of the Union, the price of tickets soldto the Indian armymen (including airmen andsailors) shall be the price of admission only,exclusive of entertainment tax.

(2) Such tickets shall be special tickets markedwith the price of admission only and shall beissued through a service authority not below therank of a commissioned officer, and proprietoror person shall maintain record of such ticketsin Form ENT�IX.

13. Complimentary tickets.� (1) Everycomplimentary ticket issued by proprietor orperson responsible for an entertainmentperformance, shall show on the complimentaryticket the price for admission and theentertainment to which the holder of such ticketis to be admitted, the date and show for whichit is available and the provisions of rule 15 shallapply to such ticket.

(2) Not more than one person shall be admittedagainst each complimentary ticket issued by theproprietor of an entertainment

14. Record for issue of tickets.� Everyproprietor or person who is required to pay taxunder the provisions of section 3 and section 3Eof the Act, shall maintain records of tickets issuedin Form ENT - IX which shall also be accessibleto the Commissioner for inspection or otherwise.

15. Tickets issued for admission to anyentertainment.� (1) Every ticket including acomplimentary ticket issued either in the formof physical mode or electronic mode by aproprietor or person who is required to pay thetax under the provisions of section 3 andsection 3E of the Act, shall consist of three partsof which one shall be the counterfoil.

(2) At the time of issue of ticket for admissionthe counterfoils shall be retained in the ticketbook and the remaining two parts shall bedetached therefrom and issued to the purchaserand shall bear on each part of such ticket theprice for admission, the amount of tax payable,

if any, and the total amount recoverable fromthe purchaser, the book number and the serialnumber of the ticket, the date on which and theshow for which it is issued. Similar procedureshall be observed, while issuing of tickets eitherthrough electronic or any mechanical device.

(3) On admission of the holder of the ticket,the proprietor or person shall cause to becollected one of the two parts of the tickets andthe other part shall be returned to the purchaser.

16. Production of ticket.� A person who hasbeen admitted to an entertainment shall, upondemand made during the course of, orimmediately before or after, the entertainment,produce to any officer appointed under section2A of the Act, the ticket, badge, card ofmembership, voucher or documents by meansof which he was admitted, or a portion of theticket by means of which he was admitted.

17. Inspection of books of accounts, etc.� TheCommissioner or any other Officer appointedunder section 2A of the Act and duly authorizedby the Commissioner or the AppropriateAssessing Authority may require the proprietoror person providing an entertainment to produceor cause to be produced for inspection all hisbooks of accounts and records and all tickets orportion of tickets in his possession relating to theentertainment. This will also include the recordsof tickets issued through computer or throughany mechanical or electronic device.

18. Assessment of tax and imposition ofpenalty.� (1) The Appropriate AssessingAuthority or the Officers appointed undersection 2A of the Act may, when he deems itnecessary to make an assessment of tax duefrom the registered proprietor or person undersub-sections (2) or (3) of section 6A of the Act,shall cause to serve upon such proprietor orperson a notice in Form ENT�X hereto.

(2) The Appropriate Assessing Authority orthe officers appointed under section 2A of theAct may for any good and sufficient reason tobe recorded in writing assess a registeredproprietor or person, whether permanent orprovisional, in respect of the part of a year.

(3) The Appropriate Assessing Authority, whenit considers it desirable to make an assessmentof tax, for a proprietor or person under provisionsof sub-section (7) of section 6A of the Act, shall

OFFICIAL GAZETTE � GOVT. OF GOA 1305SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

cause to serve upon the proprietor or person anotice in Form ENT�X hereto.

(4) After giving the proprietor or person areasonable opportunity of being heard, theAppropriate Assessing Authority shall pass anorder of assessment which shall be recorded inwriting in Form ENT�XI hereto and where theAppropriate Assessing Authority determines theturnover of a proprietor or person at a figuredifferent from that shown in the returns submittedby the proprietor or person under the provisionsof the Act and these Rules, the order shall statebriefly the reasons thereof. The provision of thissub-section shall also apply mutatis mutandis tothe proprietor or person registered under section3H of the Act.

(5) The order imposing penalty and/or theinterest in respect of any period shall beincorporated in the order of assessment relatingto that period or a separate order may be issuedfor levy of such penalty and/or interest wherethe assessment has been completed on a differentoccasion.

(6) If the assessment made under these Rulesresults in tax payable in excess of the amountdeclared and paid alongwith the returns, thenthe Appropriate Assessing Authority shall serveupon the proprietor or person a notice in theForm ENT�XII �A� hereto directing the proprietoror person to pay the excess amount demandedwithin the specified time which may not exceed60 days from the date of service of such notice.

(7) When the copy of challan acknowledgingreceipt of tax is furnished by the proprietor orperson from whom any amount is demandedunder these Rules, the Appropriate AssessingAuthority shall cause to make necessary entriesin the office record wherever necessary and shallplace such copy of the challan in the respectivecase record of the proprietor or person or otheroffice records.

(8) Any assessment in respect of proprietor orperson registered under section 3H of the Actshall be completed immediately upon expiry ofthe validity of the registration certificate.

(9) Where the Appropriate Assessing Authorityis not satisfied about the correctness orcompleteness of the accounts of a proprietor orperson or where no method of accounting hasbeen regularly employed by a proprietor orperson, the Appropriate Assessing Authority shall,

after giving the proprietor or person a reasonableopportunity of being heard, assess to the bestof his judgment, the amount of tax due from himby observing the procedure laid down insub-rule (1) above.

(10) Any assessment made under this rule shallbe without prejudice to any penalty orprosecution for an offence, under the Act.

19. Re-assessment of turnover escapingassessment, under assessed, etc.� (1) If theAppropriate Assessing Authority has reasons tobelieve that any turnover or receipts of chargesfor admission of entertainment, in respect of anyperiod/year, has escaped assessment or has beenunder assessed or assessed at a lower rate orthat any deductions have been made wronglyin an order of assessment made undersection 6A of the Act, the Appropriate AssessingAuthority shall cause to serve upon the concernedproprietor or person, within the time specifiedin sub-section (1) of section 6C, a notice in FormENT�X appended hereto and after giving himreasonable opportunity of being heard andmaking such enquiries as it considers necessary,may proceed to assess or re-assess the amountof tax due from such proprietor or person.

(2) The order of assessment or re-assessmentreferred to in sub-rule (1) shall be made in writingin Form ENT�XI appended hereto.

(3) A notice for demand of tax levied, interestand penalty imposed, if any, arising out of saidorders, shall be served upon the concernedproprietor or person in Form ENT�XII appendedhereto.

20. To whom appeal should be made.� Anappeal against an order of assessment orre-assessment or any order raising demand,passed by an Appropriate Assessing Authority,shall be made to the Assistant Commissioner ofEntertainment Tax (hereinafter referred to as�Appellate Authority�), except appeal against anorder passed by the Assistant Commissioner ofEntertainment Tax or against order with disputedamount exceeding Rs. 15 lakh, in which case,the appeal shall lie to the Additional Commissionerof Entertainment Tax and a second appealagainst an order passed in appeal shall lie to theTribunal.

21. How the memorandum of appeal shall bepresented.� The memorandum of appeal shallbe drawn up in duplicate in Form ENT�XIII and

1306 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

after being signed by the proprietor or personbe filed before or sent by a registered post tothe Appellate Authority or to the Tribunal, as thecase may be.

22. What should accompany the memorandumof appeal.� The memorandum of appeal whenpresented to the Appellate Authority shall beaccompanied with a receipted copy of thechallan in proof of payment of fees as specifiedin rule 29 and a certified copy of the orderappealed against. It shall be endorsed by theappellant or by the person duly authorized, asfollows:�

(a) that the amount of tax assessed orre-assessed and the penalty, if any, imposedor the tax or penalty admitted to be due, hasbeen paid; and

(b) that to the best of his knowledge andbelief the facts set out in the memorandum ofappeal are true; and

(c) the memorandum of appeal whenpresented to the Tribunal shall be accompaniedby a receipted copy of the challan in proof ofpayment of fees as prescribed in rule 29, anda certified copy of the order appealed against.It should also be accompanied by necessarydocuments in proof of payment of undisputedamount of tax or penalty or both that may bedue as per order passed in appeal by theAppellate Authority. It shall further be endorsedby the appellant or person duly authorized thatto the best of his knowledge and belief factsset out in the memorandum of appeal aretrue; and

(d) the memorandum of appeal may beaccompanied by an application for stay ofdisputed amount till disposal of the appeal.

23. Stay of disputed amount of tax or penalty.�(1) Pending the final decision of an appeal filedunder sub-section (1) of section 6D of the Act,on an application from the appellant, the recoveryof any tax assessed or re-assessed or penaltyimposed under the Act and not admitted by theappellant to be due from him, shall be stayed,if so directed by the Appellate Authority andotherwise, on such terms and conditions as maybe specified in the direction.

(2) The Appellate Authority shall dispose of anystay application not later than 30 days from

receipt of such application by giving the applicantan opportunity of being heard in the matter.

(3) The appeal may be summarily rejected ifthe appellant after being given an opportunityto comply with any of the requirements underrule 21 and rule 22 of these rules fails to complywith the requirements of the said Rules or failsto furnish security or for any other good andsufficient reasons to be recorded in writing.

24. Hearing and recording of evidence.� If theAppellate Authority does not reject the appealsummarily, it shall fix a date for hearing and notifythe same to the parties. It may call for evidenceas may be necessary to decide the appeal.

25. Application for revision or review.�(1) The provisions of rules 21 and 22 shallapply mutatis mutandis to every applicationfor revision:

Provided that the provisions of clause (a) ofrule 23 shall not apply to an application forrevision of any order other than an order ofassessment or re-assessment made under section6A or section 6C and the appeal order madeunder section 6D of the Act, as the case maybe.

(2) No application for review or revision filedbefore the authority competent to hear it shallbe entertained, unless it is presented within 30days from the date of such order:

Provided that an application for review orrevision may, after the period so specified butnot beyond 45 days be entertained if theapplicant satisfies the authority to which suchapplication is made that he had sufficient causefor not presenting the application within suchperiod.

Explanation:� In computing the period oflimitation prescribed in this rule for revision ofan order, the time requisite for obtaining acertified copy of the order sought to be revisedshall be excluded.

(3) The Tribunal upon receipt of application forreview shall issue a notice to be served on theapplicant specifying the date and time forhearing and upon hearing shall make necessaryorder.

(4) When the Commissioner proposes to reviewor revise any order, upon application or on his

OFFICIAL GAZETTE � GOVT. OF GOA 1307SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

own motion, he shall give the proprietor orperson as well as Appropriate AssessingAuthority and Appellate Authority, as the casemay be, an opportunity of being heard.

(5) When any order passed as a consequenceof review or revision creates additional tax liabilitypayable by the proprietor or person, then, he shallbe called upon to pay the difference in tax withina period of sixty days.

(6) When any person appointed under section2A or the Tribunal constituted under section 2Breviews any order under sub-section (10) ofsection 6D, such person or Tribunal, as the casemay be, shall record reasons thereof.

(7) When any Appropriate Assessing Authorityreviews any order it shall send a copy of theorder and of the statement of reasons to theCommissioner of Entertainment Tax.

26. Order of higher authorities shall be bindingon subordinate authorities.� (1) The order passedby the appellate or revisional Authorities shallsupersede the orders of any subordinateauthorities and shall be binding on them.Similarly, the reviewing or rectification orderpassed by an authority shall supersede or modify,as the case may be, the original order passedby the same authority.

(2) A copy of any order passed upon anyappeal or application for revision shall be sentto the Officer whose order forms the subjectmatter of the appeal or revision proceedings.

27. Rectification of clerical or arithmeticalmistakes.� (1) Appropriate Assessing Authority,appellate authority or revisional authority may,at any time within one year from the date of anyorder passed by it, upon an application from theproprietor or person or on his own motion, rectifyany clerical or arithmetical mistake apparent onthe face of record or otherwise brought to hisnotice:

Provided that, no such rectification shall bemade if it has the effect of enhancing the taxunless the authority concerned has given noticein writing to the proprietor or person of hisintention to do so and has allowed him areasonable opportunity of being heard.

(2) Where such rectification has the effect ofreducing the amount of tax or penalty or interest,the authority concerned shall order refund of the

amount which may be due to the proprietor orperson.

(3) Where such rectification has the effect ofenhancing the amount of tax or penalty or interestthe authority concerned shall recover the amountdue from such proprietor or person in the mannerprovided for in section 4 of the Act.

28. Recovery of Arrears.� (1) When a proprietoror person from whom any amount of tax or penaltyor interest has been demanded by issue of anotice or order, fails to pay the demanded amountwithin the time specified in the notice or order,or within the extended time, if any, granted formaking such payments, the AppropriateAssessing Authority shall issue for the purposeof recovery of the arrears from the defaulter orother person responsible for the payment, acertificate for the recovery of amount due in FormENT�XIV.

(2) The certificate referred to in sub-rule (1)above shall be the basis to proceed to recoverthe amount due as arrears of land revenue. Incase such recovery is to be effected by the Officerauthorized by the Government under provisionsof sub-section (8) of section 4 of the Act, andfor the same purpose of recovery, the relevantprovisions contained in the Goa Land RevenueCode, 1968 (Act No.9 of 1969), and Rules madethereunder shall be applicable.

(3) The certificate referred to in sub-rule (1)above shall serve as requisition for the authoritycompetent to make the recovery of the amountdue as arrears of land revenue under theprovisions contained in the Goa Land RevenueCode, 1968 and Rules made thereunder, in allcases wherein no Officer is authorized by theGovernment under the Act to exercise the powersof a Collector under the said Goa Land RevenueCode, 1968, for the purpose of recovering the duesas arrears of land revenue.

(4) In all cases wherein the defaulter or otherperson responsible for the payment of amountdue is residing or is having property outside thedistrict, the Appropriate Assessing Authorityshall send the certificate referred to insub-rule (1) to the Officer authorized by theGovernment under sub-section (8) of section 4of the Act, or to the Collector of the District ifno Officer is authorized under the said sub-section(8) of section 4 of the Act, soliciting that the samemay be sent to the Collector of other districtwherein the defaulter or person responsible for

1308 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

the payment of the dues is residing or is havingproperty. Such certificate shall be sent by theAppropriate Assessing Authority himself, if he isthe Officer authorized by the Government underthe said sub-section (8) of section 4 of the Act.

Whenever the amount of arrears recoveredby the Collector of other district are remitted tothe Appropriate Assessing Authority, the saidauthority shall take immediate step to enter sameamount into the Government Treasury.

(5) Certificate referred to in sub-rule (1) shallbe issued in respect of each defaulter or personresponsible for payment of arrears.

(6) The officer referred to in sub-rule (2) andthe authorities referred to in sub-rules (3) and(4), as the case may be, shall keep informed theAppropriate Assessing Authority about the stepstaken in the matter of recovery of arrears, whensuch information is called for by the saidAppropriate Assessing Authority and shallreport to him as soon as the recovery is made,the amount recovered giving the particulars ofthe recovery, mainly, the date on which therecovery is made, the name of the treasurywherein the amount is entered and the date ofchallan under which the amount is paid into thetreasury.

(7) On the basis of the report of paymentreferred to in sub-rule (6) received fromconcerned authorities, the Appropriate AssessingAuthority shall cause to make the necessaryentries in the assessment case record of theproprietor or person and other office recordsmaintained.

29. Payment of Fees on appeal.� (1) Everymemorandum of appeal to the Tribunal shall beaccompanied by challan in Form ENT-IIIappended hereto showing payment of fees ofRs. 250/- into the Government Treasury .

(2) Fee of Rs. 200/- shall be payable intoGovernment Treasury by challan in FormENT�III hereto in following cases:�

(i) on memorandum of appeal against orderof assessment/re-assessment or any otherorder raising demand with or withoutpenalty/interest;

(ii) for obtaining duplicate copy of registrationcertificate.

(3) Fee of Rs. 50/- shall be payable in courtfees stamps in the following cases:�

(i) on application for remission of interest;

(ii) on a letter of authority for representinga case before any authority under the Act andthen Rules framed thereunder;

(iii) on any application or petition for reliefto any authority under the Act and Rulesframed thereunder;

(iv) on application for grant of certified copyof any document or order issued by anyauthority;

(v) on application for determination ofdisputed question to the Commissioner ofEntertainment Tax, under section 3A of the Act;

(vi) on application for making anyamendment to the registration certificate.

30. Refund.� (1) When any refund arises froman order of assessment or re-assessment madeunder section 6A or section 6C or from an orderpassed in appeal, revision or review under section6D, or from an order of rectification passed undersection 6G and the amount to be refunded doesnot exceed Rs. 10,000/-, the AppropriateAssessing Authority shall forthwith proceed torefund such amount by cash to the proprietoror person concerned by issue of refund voucherin Form ENT�XV hereto. However, beforeproceeding to refund such amount, theAppropriate Assessing Authority shall firstlyverify that any amount being due by theproprietor or person is left unpaid by him, in suchcase, shall adjust the amount to be refunded byissue of an order towards the amount due fromthe proprietor or person on the date of adjustmentand thereafter shall refund the balance, if any.

(2) When the amount of refund arising fromany of the contingencies referred to in sub-rule(1) exceeds rupees ten thousand but does notexceeds rupees fifty thousand, the AppropriateAssessing Authority shall obtain the sanction ofthe Assistant Commissioner of Entertainment Taxin charge of or having the jurisdiction over,the ward before proceeding to refund suchamount after submitting full facts to him.

(3) When the amount of refund arisingfrom any of the contingencies referred to insub-rule (1) above exceeds rupees fifty thousand,

OFFICIAL GAZETTE � GOVT. OF GOA 1309SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

the Appropriate Assessing Authority shallobtain the sanction from the AdditionalCommissioner of Entertainment Tax beforeproceeding for refund.

31. Maintenance of records under section 8F.�(1) Every registered proprietor or person shallkeep and maintain a true and correct accountof the Entertainment Tax receipts.

(2) The following records in particular shall bemaintained:

(a) A monthly account specifying totalreceipts of charges for admission separatelyfor each class of entertainment and taxpayable thereon as per Form ENT�IXappended hereto.

(b) Monthly account of purchase and issueof Casino entry tickets (wherever applicable).

(c) A monthly account showing compli-mentary tickets issued.

(d) Monthly account showing receipts ofcharges for admission for each entertain-ment to which exemption is granted undersection 5.

(e) Counterfoils of tickets issued in physicalmode for each class of entertainment includingentertainment to which exemption is grantedunder the Act, in numerical order.

(f) All forms, tax challans, etc.

(g) Cash records, viz., Cash Book, Vouchersand other accounting records including cashregisters, machine rolls details in daily takings.

(h) The registers, accounts and documentsmaintained shall be sequentially numbered andwhere the registers and other documents aremaintained by means of a computer or anyother similar mechanical device, the proprietoror person shall maintain copies in paper of suchregisters and other documents printed on amonthly basis.

(i) Annual accounts including profit and lossaccount and Balance Sheet with Schedules.

(j) Records of the bank transactions.

(3) A proprietor or person opting for compositionof tax under section 3D of the Act, shall maintaina daily record of his gross receipts of chargesfor admission.

(4) All records maintained in course of carryingactivity of providing entertainment (except forcounterfoils of tickets issued which are to beretained for 30 days only) shall be retained fora period of five years from the expiry ofthe year to which they relate.

(5) Wherever the Commissioner deems it es-sential he may direct a person or proprietor tomaintain Accounts of above nature by issuingdirections in Form ENT�XII-B.

32. Superintendence and control.� (1) TheGovernment shall superintend the administrationand collection of tax leviable under the Act.

(2) Subject to the general control andsuperintendence of the Government, theCommissioner shall control all officers empoweredunder the Act, who shall in turn have controlover respective subordinates as per delegationof powers under the Act and Rules.

33. The activity of providing entertainmentforming part of estate under the control of theCourt.� The administrator general, the officialtrustee and the executor or administrator or anyreceiver carrying on any activity of providingentertainment forming part of an estate placedunder his control by an order of the Court, shallbe liable to perform all obligations imposed bythe Act and these Rules in respect of such activityof providing entertainment to the same extentas if he was the proprietor or person and alsoshall be liable to pay any tax assessed or penaltyimposed thereon for the period during which heremains in control thereof.

34. Notice under section 8A(2).� TheAppropriate Assessing Authority shall cause toserve upon the concerned proprietor or persona notice for imposition of penalty or for forfeitureof any sum under section 8A of the Act fixing

1310 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

the date for compliance therewith not earlier thanfifteen days from the date of service thereof.

35. Compounding of offences.� (1) Subject tothe limitations provided in the Act, theCommissioner may decide on an application fromany proprietor or person a sum by way ofcomposition of an offence committed by himunder the Act or these Rules either before orafter the commencement of any proceedingagainst such proprietor or person in respect ofsuch offence.

(2) On taking a decision under sub-rule (1),the Commissioner, shall, if there are no reasonsto the contrary make an order in writingspecifying therein.�

(a) the sum determined by way ofcomposition;

(b) the date on or before which the sum shallbe paid into the Government Treasury;

(c) the authority before whom and the dateon or before which a challan shall be producedin proof of such payment; and

(d) the date on or before which the proprietoror person shall report the fact to theCommissioner.

(3) On receipt of the challan for payment ofthe composition fee as required under sub-rule(2), the Commissioner shall pass an ordercompounding the offence and shall send a copyof such order to the proprietor or personconcerned and also to the authority referred toin clause (c) of sub-rule (2).

36. Printing of tickets, etc.� (1) The entrytickets for charges for admission in respect ofclass of entertainment covered underSchedule �D� appended to the Act shall be printedby the Office of the Commissioner, and the personor proprietor operating such entertainmentperformance shall purchase the said tickets onmaking necessary remittances into theGovernment Treasury upon valid authorizationby the Office of the Commissioner ofEntertainment Tax.

(2) The counterfoils of the tickets sold to bereturned by the proprietor or person operatingthe entertainment to the Office of theCommissioner of Entertainment Tax for record by10th of every month.

37. Supply of copies of records anddocuments.� (1) Any records pertaining to theproceedings under the Act and Rules can beinspected after making a request to AdditionalCommissioner and deposit of an advance fee ofRs.50/- in Court Fees Stamp. For every subsequenthour of inspections, a fee of Rs. 50/- shall bepayable.

(2) Copies of any records may be furnished onpayment of copying charges @ Rs. 10/- per pageagainst advance payment made by way of CourtFee Stamp through an application made to theAdditional Commissioner of Entertainment Taxwho shall ensure supply of copy of record in twoweeks time.

38. Furnishing of security for controlling theuse of mechanical/electric contrivances.�(1) The Commissioner or Appropriate AssessingAuthority may for good and sufficient reasondemand from the proprietor or person who usesthe mechanical/electrical contrivances, andcomputers, a reasonable security for properpayment of tax payable by him under the Act.

(2) The Commissioner or Appropriate AssessingAuthority may for good and sufficient cause forfeitthe whole or any part of the security obtainedunder sub-rule (1), if after due verification andhaving given an opportunity of explanation tothe proprietor or person it is found that suchdevice is being manipulated to conceal or reducethe tax liability due from the proprietor or personunder this Act and such forfeiture of security shallbear a reasonable nexus to the estimatedconcealment of tax liability.

39. Nomination of Head Office in the case ofthe proprietor or person having more than oneplace of entertainment.� (1) Where a proprietoror person has within the State of Goa more thanone place of entertainment (hereinafter referredto as �branches�) he shall nominate one such

OFFICIAL GAZETTE � GOVT. OF GOA 1311SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

branch as the Head Office of the activity ofproviding entertainment for the purpose of theseRules under intimation to all the AppropriateAssessing Authorities within whose jurisdictionsuch branches are situated, failing which, theCommissioner may nominate one of suchbranches to be the Head Office for the purposeof this rule.

(2) All applications, returns or statementsspecified under the Act or these Rules shall besubmitted in respect of all branches jointly bythe Head Office to the Appropriate AssessingAuthority.

(3) All notices and orders required or permittedby the Act or these Rules, to be served on anyproprietor or person, shall be issued to and servedon the person in charge of the head office referredto in these Rules and shall thus be deemed tohave been issued to and served on all branchesof the proprietor or person concerned.

40. Jurisdiction.� For implementing theprovisions of the Act and these rules, the Stateof Goa shall be divided into the following twoWards comprising of the areas noted againsteach.�

(I) Panaji Ward (North)� Talukas of Tiswadi,Ponda, Pernem, Bardez, Bicholim and Satari.

(II) Margao Ward (South)� Talukas of Salcete,Quepem, Canacona, Sanguem and Mormugao.

41. Qualifications of members of Tribunal andtheir period of office.� (1) One of the membersof the Tribunal shall always be a person havingthe qualifications as specified in sub-section (1)of section 2B of the Act.

(2) Other members of the Tribunal shall bepersons of eminence having professionalbackground and expertise in legal or financialmatters for not less than 15 years.

(3) The members of the Tribunal shall hold officefor a period of one year from the date of theirappointment:

Provided that the Government may, for reasonsto be recorded in writing, extend the said periodby such further period not exceeding one year,as may be deemed fit by the Government.

42. Determination of disputed questions.�(1) If any proprietor or person desiring that aquestion referred to in sub-section (1) of section3A, may be determined by the Commissioner, heshall make an application on plain paper drawnin duplicate setting out a concise statement ofhis case, stating therein precisely the questionto be determined, and indicating clearly the basisfor dispute. The fees payable on such applicationshall be as provided under rule 29.

(2) The statement of the case referred insub-rule (1), shall contain a declaration that thequestion submitted for determination of theCommissioner does not arise from any orderpassed under the Act, and the said statementof the case shall be signed and verified by theproprietor or person.

(3) The Commissioner after considering all therelevant material produced before him in thisbehalf shall pass appropriate order, determiningthe question within a period of six months fromthe date of receipt of such application.

43. Repeal and savings.� (1) The GoaEntertainment Tax Rules, 1965, are herebyrepealed.

(2) Notwithstanding such repeal, anything doneor any action taken, including any order made,direction given or notice issued under the GoaEntertainment Tax Rules, 1965, shall in so far asit is not inconsistent with the provisions of theserules, be deemed to have been done, taken, made,given or issued, as the case may be, within thecorresponding provisions of these rules.

By order and in the name of the Governorof Goa.

Vasanti H. Parvatkar, Under Secretary, Fin.(Budget-I.)

Porvorim, 21st March, 2007.

1312 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

FORM ENT - ISee rule 3(1) and 5(1)

Application for grant of Certificate of Registration//Renewal of Certificate of RegistrationTo,The Commercial Tax Officer,Ward,Department of Commercial Taxes, Goa.

Sir,

I hereby apply for Registration/Renewal of theCertificate of Registration as per details given below:

(1)Name and Style of activityof providing entertainment:

(2)Address of the Place Main Officeof entertainment: Additional place 1

Additional place 2Additional place 3

(3)Constitution of the Natureentity providing Names and Address ofentertainment Partners/Proprietors/(Attach Documents): Managing Director/Of-

fice bearers/Key persons1.2.3.4.5.

(4) Nature of Entertainment:

(5)(1) Registration No. under the GoaValue Added Tax Act, 2005(if granted)

(5)(2) Registration No. under the GoaTax on Luxuries Act, 1988(if granted)

(5)(3) Registration No. under the GoaEntertainment Tax Act, 1964 (ifgranted) (For renewal cases)

(5)(4) Bank Account No.

(5)(5) PAN Details

(6) Details of registration fees Challan Amountpaid as per Schedule E No./Date

(7) Details of renewal fees Challan Amountpaid as per Schedule E No./Date

(8) Details of lump sum paid Challan Amountas charges for admission No./Dateas per Schedule D (ForHotels having Casinos)

.......................................................Signature of the applicant Date PlaceStatus

Full address for correspondence

FORM ENT - IISee rule 4(1)

Certificate of Registration/Renewal

WARD OFFICE

REGISTRATION CERTIFICATE NUMBER:

(1) Name and Style ofactivity of providingentertainment:

(2) Address of the Place Main Officeof entertainment and Additional place 1area of operation: Additional place 2

Additional place 3

(3) Area of operation:

(4) Nature of Entertainment:

(5) Date of liability:

(6) Date of validity: From To

(1) Return is to be furnished in Form ENT-VI byregistered entity along with proof of payment of taxon monthly/quarterly/annual basis.

(2) a copy of this certificate is to be displayed promptly bythe assessee at the place(s) of business.

(3) Any change in particulars recorded above is to be re-ported in 30 days time.

...............................................................................Signature of the Registering Authoritywith seal and date

Ward Address

RENEWAL DETAILS

Date of Period up to Signature of therenewal which renewed Appropriate

Assessing Authority

OFFICIAL GAZETTE � GOVT. OF GOA 1313SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

Duplicate(To be furnished to the ETO)

0045-Other Taxes & Duties on Com-modities & Services

Challan of tax, license and Registra-tion fees and other receipts paid intothe�������

(Branch) of SBI/Treasury/ ��Bank

Period: From��.��..to����..

Regn. No�����������...

Name & Address of Assessee for whompayment is being made

Name of Person making the deposit

Payments made on account of(amount in figures) Rs.

101 Entertainment Tax

01-Tax Collection Rs. .................

02-Regisration & Renewal feesRs. .................

03-Composition Fees Rs. ............

04- Other Receipts Rs. ...............

90. Deduct Refunds Rs. .............

Total Rs. (in words)

...............................................Signature of Depositor/Assessee

with date

FOR USE IN TREASURY/BANK

Received payment of Rs. /-(....................................................)

Date:

Challan No.

.........................................Signature of Acctt:

.........................................Signature of Manager/TO

Triplicate(To be retained by the Treasury)

0045-Other Taxes & Duties on Com-modities & Services

Challan of tax, license and Registra-tion fees and other receipts paid intothe�������

(Branch) of SBI/Treasury/ ��Bank

Period: From��.��..to����..

Regn. No�����������...

Name & Address of Assessee for whompayment is being made

Name of Person making the deposit

Payments made on account of(amount in figures) Rs.

101 Entertainment Tax

01-Tax Collection Rs. .................

02-Regisration & Renewal feesRs. .................

03-Composition Fees Rs. ............

04- Other Receipts Rs. ...............

90. Deduct Refunds Rs. .............

Total Rs. (in words)

...............................................Signature of Depositor/Assessee

with date

FOR USE IN TREASURY/BANK

Received payment of Rs. /-(....................................................)

Date:

Challan No.

.........................................Signature of Acctt:

.........................................Signature of Manager/TO

Quadriplicate(To be sent by the Treasury to ETO)

0045-Other Taxes & Duties on Com-modities & Services

Challan of tax, license and Registra-tion fees and other receipts paid intothe�������

(Branch) of SBI/Treasury/ ��Bank

Period: From��.��..to����..

Regn. No�����������...

Name & Address of Assessee for whompayment is being made

Name of Person making the deposit

Payments made on account of(amount in figures) Rs.

101 Entertainment Tax

01-Tax Collection Rs. .................

02-Regisration & Renewal feesRs. .................

03-Composition Fees Rs. ............

04- Other Receipts Rs. ...............

90. Deduct Refunds Rs. .............

Total Rs. (in words)

...............................................Signature of Depositor/Assessee

with date

FOR USE IN TREASURY/BANK

Received payment of Rs. /-(....................................................)

Date:

Challan No.

.........................................Signature of Acctt:

.........................................Signature of Manager/TO

Original(To be retained by the payee)

0045-Other Taxes & Duties on Com-modities & Services

Challan of tax, license and Registra-tion fees and other receipts paid intothe�������

(Branch) of SBI/Treasury/ ��Bank

Period: From��.��..to����..

Regn. No�����������...

Name & Address of Assessee for whompayment is being made

Name of Person making the deposit

Payments made on account of(amount in figures) Rs.

101 Entertainment Tax

01-Tax Collection Rs. .................

02-Regisration & Renewal feesRs. ..................

03-Composition Fees Rs. ............

04- Other Receipts Rs. ...............

90. Deduct Refunds Rs. .............

Total Rs. (in words)

...............................................Signature of Depositor/Assessee

with date

FOR USE IN TREASURY/BANK

Received payment of Rs. /-(....................................................)

Date:

Challan No.

.........................................Signature of Acctt:

.........................................Signature of Manager/TO

FORM ENT - III[See rule 3 (1) and 9(2)]

CHALLAN

1314 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

FORM ENT - IVSee rule 6(1)

Application for cancellation of Certificate ofRegistration under section 3G (7) of the Goa Enter-tainment Tax Act, 1964 (To be filed in Duplicate)

To,The Commercial Tax Officer,Ward,Department of Commercial Taxes, Goa.

Sir,

I hereby apply for cancellation of Certificate ofRegistration under the Goa Entertainment Tax Act,1964 as per details given below:

(1a) Name and Style ofactivity of providingentertainment:

(1b)Registration No.:

(2) Address of the place Main Office

of entertainment: Additional place 1

Additional place 2

Additional place 3

(3) Reasons for seekingcancellation of Re-gistration:

Signature of the applicant �����.� Status: ���

Full address for future correspondence:

Encl: Original Certificate of Registration:

The above application was considered by the under-signed in accordance with the duly laid down proce-dure and having considered all the facts, I, in exerciseof powers delegated under the Goa Entertainment TaxAct, 1964 hereby accept the application and cancelthe Registration Certificate with effect from........ /rejectthe same for grounds given below.

Grounds for rejection if application not accepted.

A copy of this order is given to the applicant. Theoriginal papers are retained for records.

.......................................................(Signature and Name of

Assessing AuthorityPlace: with seal)

Date:

_____

FORM ENT - V

[See rule 7(7)]

Register for Registration/Amendment/Cancellation

S. RC. Name of Address of the place of Entertainment Nature of Authorised Validity of Date/De- Date/De- Date/De- Date/De- Date ofNo. No. applicant business Entertain- Person Registra- tails of tails of tails of tails of cancella-

Head Other Other Other ment busi- tion amend- amend- amend- amend- tion ofOffice place place place ness ments ments ments ments registration

of of of effected effected effected effectedbusiness business business

_____

FORM ENT - VI[See rule 9 (1)]

Return of Tax payable by Assessee under the Goa Entertainment Tax Act, 1964Return Period: From���.. To ���..

1. Registration Certificate No. Under:(a) Goa Entertainment Tax Act, 1964(b) Goa Value Added Tax Act, 2005 (TIN)(c) Goa Tax on Luxuries Act, 1988

2. Name and Address of the Assessee:

3. Compilation of turnover liable for taxation:(a) Total turnover for admission charges

OFFICIAL GAZETTE � GOVT. OF GOA 1315SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

(b) Deductions

(i) Total turnover for admission charges not exigible to tax

(ii) Total turnover for admission charges exempt from taxu/s 5 of the Goa Entertainment Tax Act, 1964

(iii) Others (give details)

TOTAL DEDUCTIONS (i) to (iii)

(c) TAXABLE TURNOVER (a) � (b)

4. Tax payable under Schedule A (For Cinema Halls and Theatres):

Item TTO Rate of Tax payable Item TTO Rate of Tax payable(Rs.) tax % (Rs.) (Rs.) tax % (Rs.)

1 (b) 30 3 (d)(ii) 151 (c) 40 4 (a) (i) 102 30 4 (a) (ii) 152 10 4 b(ii) 103 (b) 10 4 (b)(iii) 153 (c) 20 TOTAL

5. Tax payable under Schedule B (For Cruise Operators):

Item TTO Rate of Tax payable Item TTO Rate of Tax payable(Rs.) tax % (Rs.) (Rs.) tax % (Rs.)

1 15 2 10

TOTAL

6. Tax payable under Schedule C (For Cable Operators):

Item TTO (No. of Tax Rs. per Tax payable Item Item Rate of Tax payableconnections) connection (Rs.) tax % (Rs.)

(i) 10 (iv) 5 %(ii) 15(iii) 10 TOTAL (i)+(ii)+(iii)+(v)+(iv)

(v) 20

7. Tax payable under Schedule D (For Casinos):

Item No. of Rate of Tax payable Item TTO Rate of Tax payablePAX Tax/PAX (Rs.) (Rs.) tax % (Rs.)

1 (a) (i) 10/PAX

1 (a) (ii) 200/PAX 1(c) 10%1 (b) 200/PAX Lumpsum charges for Casino Entry as per

proviso to Schedule D @ Rs. 10/-/room/month

TOTAL Rs.

8. TOTAL( 4+5+6+7) Rs. /- (Rs�����������������.................................................�..)

9. Challan No. Date Period

The signatory certifies that the returns are true and correct.

......................................................Signature and name

1316 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

FORM ENT - VIISee rule 10(1)

Application for composition of tax under section 3D of the Goa Entertainment Tax Act, 1964 (to be filed induplicate)

To,The Commissioner,Department of Commercial Tax, Goa,

Sir,

I hereby apply for composition of Tax payable under section 3 D of the Goa Entertainment Tax Act, 1964 forthe period���.to���..for entertainment provided by conducting boat/river cruise. I agree to comply with anyconditions imposed including furnishing of appropriate security as directed by the Assessing Authority.

In case of any information furnished being found false or incorrect by the Assessing Authority on basis of firmevidence, the undersigned, hereby undertakes to clear the default along with penalty/interest as may be determinedby the Assessing Authority.

(1) Name and Style of activity of providingentertainment.

(2) Address of the Main Office and place Main Officeof entertainment:

Name of Boat/ Seating No. of trips Rate charged/Cruise and capacity per month per person for

Regn. details admission

(3) Constitution of the entity providing Natureentertainment (Attach Documents):

Names and Address of Partners/Proprietors/ManagingDirector/Office bearers/Key persons1.2.3.

(4) Nature of Entertainment:

(5) Registration No. under Goa EntertainmentTax Act, 1964 (if granted):

Signature of the applicant and status ...............................................................................Full address for correspondence:

The above application having been considered and the permission is hereby granted to applicant for paymentof composition amount of Rs������ (������.........�...................................���������.) for the monthof �������������. subject to the condition that:

(i) The applicant shall deposit the aforesaid amount in the appropriate treasury/Bank within three days of issueof this order.

(ii) He shall not carry passengers in excess of the sanctioned capacity as given above and shall intimate theCommercial Tax Department, Goa, regarding any augmentation of passenger capacity of vessel(s) promptly.

(iii) Failure to comply with the conditions by the applicant shall invite penal action as provided under the GoaEntertainment Tax Act, 1964, and Rules framed thereunder.

..................................................Dated (Commissioner)

Seal

OFFICIAL GAZETTE � GOVT. OF GOA 1317SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

FORM ENT - VIII(See rule 11)

Application for exemption from payment of Tax under section 5(1) and 5(3) of the Goa Entertainment Tax Act,1964 (to be filed in duplicate)

To,The Commissioner,Department of Commercial Tax, Goa.

Sir,

I, hereby apply for exemption from payment of tax under section 5(1) and 5(3) of the Goa Entertainment TaxAct, 1964 for entertainment proposed to be provided for social/charitable purposes.

I have attached documents referred in column (3) and (5), below.

In case of any information furnished being found false or incorrect by the Assessing Authority on basis of firmevidence, the undersigned, hereby undertakes to clear the default along with penalty/interest as may be determinedby the Assessing Authority.

(1) Name and Style of activity of providing entertainment:

(2) Address of the Main Office and place of entertainment: Main Office

Place of Entertainment

Details of show (attach details separately if space is Nature of en- Seating Frequency Rate to beinsufficient in this column): tertainment Capacity of the show charged

per person

(3) Constitution of the entity providing entertainment Nature(Attach Documents including Annual Report/Articlesof Association and audited balance sheet): Names and Address of Partners/Proprietors/Manag-

ing Director/Office bearers/Key persons1.2.3.

(4) (a) Regn. No. under Societies Act, 1860 and annualturnover as per audited balance sheet:

(4) (b) PAN No. of beneficiary:

(5) Details of any previous exemptions granted andwhether accounts thereof have been rendered:

(6) Detailed write up explaining the reasons for seekingexemption showing as to how the income generatedshall be utilized:

Signature of the applicant, with date and status:Full address for correspondence:

The above application having been considered and exemption has been granted by the Government frompayment of tax in respect of event mentioned above subject to the condition that:

(i) The entire sales proceeds shall be utilized as per details given in the application.

(ii) The applicant shall render detailed accounts of the income generated and charitable/socially beneficial usethereof made by the applicant within 30 days of the issue of this exemption.

(iii) This exemption shall not be used for any other show and shall be surrendered to the Commercial TaxDepartment if the show is cancelled or postponed.

(iv) Failure by the applicant to comply with the conditions shall render him liable to pay tax due alongwithpenalty as may be considered desirable under the Goa Entertainment Tax Act, 1964 and Rules framed thereunder.

Dated .......................................................(Commissioner)

1318 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

FORM ENT - IX(See rule 12 and 14)

Record of tickets under Goa Entertainment Tax Act, 1964Date

1a. Name and Style address of the place of entertainment.

1b. Registration No.

Class Time Film Admin. Ent. Tax Surcharge Total Opn. No. Closing No. Total Gross Ent. Tax Surchargeof show name rates of tickets of tickets tickets

sold sold sold

1 2 3 4 5 6 7 8 9 10 11 12 13

_____

FORM ENT - X [See rule 18(i), 18(3) and 19(1)]

No. Office of the ������

To,�����������.��������..

RC No���������������..

Whereas the undersigned on basis of material infor-mation has grounds to prima facie believe that the amountof tax due under the Goa Entertainment Tax Act, 1964recoverable from you has not been assessed/paidproperly/under assessed for the period�....� to ���.;

And whereas the returns for the period as prescribedunder the Goa Entertainment Tax Act, 1964 have not beenproperly filed by you;

And whereas you being liable to pay tax under GoaEntertainment Tax Act, 1964 for the period ����..havenot applied for registration under the said Act within theprescribed time;

And whereas default under the Goa EntertainmentTax Act, 1964 have been committed by you, renderingyou liable for imposition of penalty/forfeiture or both.

Now, therefore, in exercise of the powers conferredupon me under section 6A of the Goa Entertainment TaxAct, 1964, I, hereby direct you to put in appearance inperson or through your attorney/authorized person atthe address stated above at��. a.m./p.m. on���alongwith all records maintained by you inrespect of activities covered under the Goa Entertain-ment Tax Act, 1964 for facilitating appropriateassessment of your liabilities under the aforesaid Act.

You may kindly note that in case of your failure toappear before the undersigned on the date and time givenabove, the undersigned shall have no other optionexcept to proceed on ex-parte basis and decide thematter to his best judgment.

Issued under my hand and seal on this ���...� dayof ����. 2007.

.....................................................................(Appropriate Assessing Authority)

OFFICIAL GAZETTE � GOVT. OF GOA 1319SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

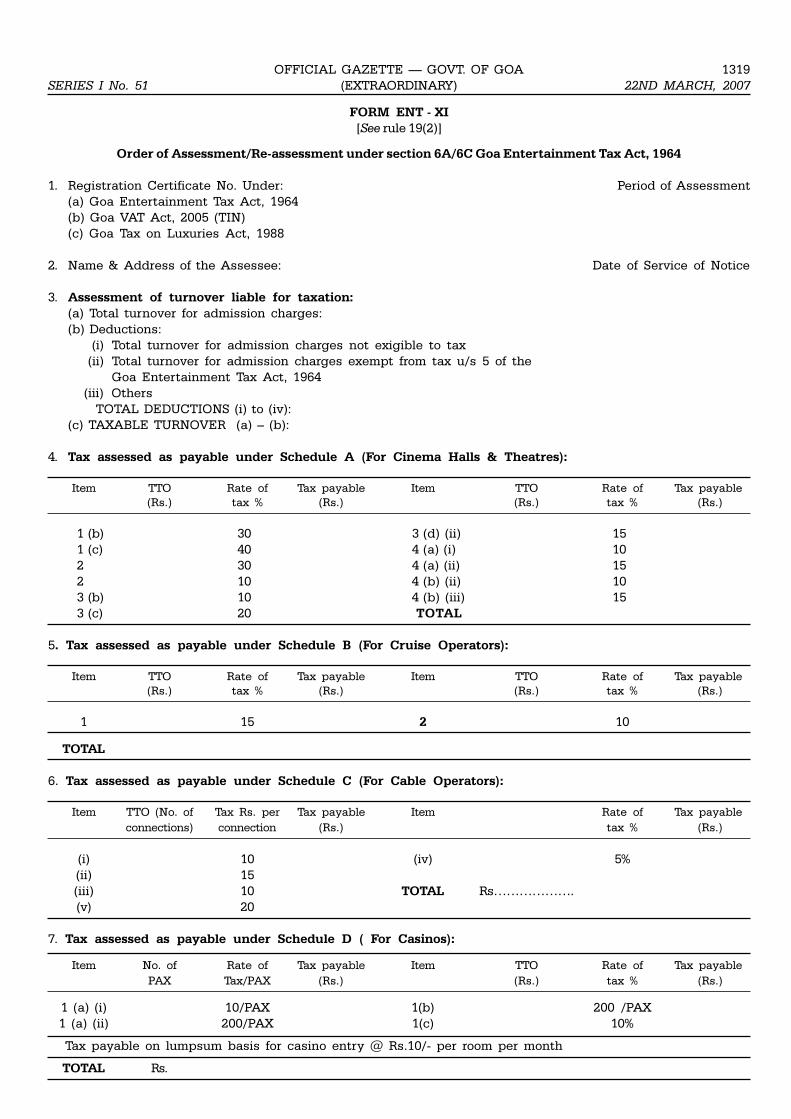

FORM ENT - XI[See rule 19(2)]

Order of Assessment/Re-assessment under section 6A/6C Goa Entertainment Tax Act, 1964

1. Registration Certificate No. Under: Period of Assessment(a) Goa Entertainment Tax Act, 1964(b) Goa VAT Act, 2005 (TIN)(c) Goa Tax on Luxuries Act, 1988

2. Name & Address of the Assessee: Date of Service of Notice

3. Assessment of turnover liable for taxation:(a) Total turnover for admission charges:(b) Deductions:

(i) Total turnover for admission charges not exigible to tax(ii) Total turnover for admission charges exempt from tax u/s 5 of the

Goa Entertainment Tax Act, 1964(iii) Others

TOTAL DEDUCTIONS (i) to (iv):(c) TAXABLE TURNOVER (a) � (b):

4. Tax assessed as payable under Schedule A (For Cinema Halls & Theatres):

Item TTO Rate of Tax payable Item TTO Rate of Tax payable(Rs.) tax % (Rs.) (Rs.) tax % (Rs.)

1 (b) 30 3 (d) (ii) 151 (c) 40 4 (a) (i) 102 30 4 (a) (ii) 152 10 4 (b) (ii) 103 (b) 10 4 (b) (iii) 153 (c) 20 TOTAL

5. Tax assessed as payable under Schedule B (For Cruise Operators):

Item TTO Rate of Tax payable Item TTO Rate of Tax payable(Rs.) tax % (Rs.) (Rs.) tax % (Rs.)

1 15 2 10

TOTAL

6. Tax assessed as payable under Schedule C (For Cable Operators):

Item TTO (No. of Tax Rs. per Tax payable Item Rate of Tax payableconnections) connection (Rs.) tax % (Rs.)

(i) 10 (iv) 5%(ii) 15(iii) 10 TOTAL Rs������.(v) 20

7. Tax assessed as payable under Schedule D ( For Casinos):

Item No. of Rate of Tax payable Item TTO Rate of Tax payablePAX Tax/PAX (Rs.) (Rs.) tax % (Rs.)

1 (a) (i) 10/PAX 1(b) 200 /PAX1 (a) (ii) 200/PAX 1(c) 10%

Tax payable on lumpsum basis for casino entry @ Rs.10/- per room per month

TOTAL Rs.

1320 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

8. TOTAL Tax Assessed (4+5+6+7) Rs. /- ( Rs�����������������.�..)

9. Tax Paid Challan No. Date

10. Balance to be paid

11. Interest Due

12. Penalty

13. Total liability assessed

14. Demand payable/Refund due

...........................................Seal Place: Signature and date

_______

FORM ENT - XII - A [See rule 18(6) and 19(3)]

Office of the Commercial Tax Officer

No.

To,�����������.��������..

RC No���������������..

Whereas the undersigned on basis of materialinformation has grounds to prima facie believe that thetax/penalty amounting to Rs. �����������(�����.............................................��.) has become ofdue under the Goa Entertainment Tax Act, 1964 from youfor the period���� to ����.as per assessmentorder enclosed.

Therefore, the undersigned in exercise of powersconferred under section 6A /6C of the Goa EntertainmentTax Act, 1964 hereby directs you to pay the aforesaiddemand in Government Treasury or notified bankwithin �..�days of issue of this notice and furnish proofthereof to the undersigned by���.. failing which, theundersigned shall have no other option except toproceed to order the recovery of this amount as arrears ofland revenue.

Issued under my hand and seal on this����dayof����.2007.

......................................................................(Appropriate Assessing Authority)

Date :

Place :

Seal

FORM ENT - XII - B(See rule 35)

Office of the Entertainment Tax Officer

No.

To,�����������.��������..

RC No���������������..

Whereas, the undersigned on the basis of materialinformation has grounds to prima facie believe that youare required to maintain true and correct returns forreceipt of the Entertainment Tax collected by you.

Therefore, I, in exercise of powers conferred undersection 8F of the Goa Entertainment Tax Act, 1964 herebydirect you to maintain the accounts with effectfrom���. in the format for returns prescribed underthe aforesaid Act and Rules framed thereunder.

You are directed to report compliance within twoweeks of receipt of this notice or penal action as prescribedunder the aforesaid Act shall be initiated against you.

Issued under my hand and seal on this����dayof����. 2007.

......................................................................(Appropriate Assessing Authority)

Date :

Place :

Seal

OFFICIAL GAZETTE � GOVT. OF GOA 1321SERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

FORM ENT - XIII (See rule 21)

Memorandum of Appeal to the Appellate Authority//Tribunal under section 6D(1)/6D(3) of the Goa

Entertainment Tax Act, 1964

Before the Appellate Authority/Tribunal

No������..of 200....

M/s. Appellant���������������������������������..

Name of Assessing Date of Period to Date of Demand crea-Authority/Appellate order which appeal service of ted in disputedAuthority which has pertains order order

passed the order under (Rs.)appeal/review

Demand Demand Balance Admitted Tax/Feescreated in admitted Demand Payment Proof

disputed order (Challan No.(Rs.) (Rs.) (Rs.) and date)

TaxPenaltyInterest

Total

Grounds of Appeal:

.............................................................................(Signature of Appellant/Representative)

RC No. of the Dealer

Status:

List of annexures:

VERIFICATION

I/We���������������.do herebydeclare that the facts set out in the memorandum ofappeal are true to the best of my/our knowledge andbelief and that nothing has been concealed ormisrepresented therein. Further the tax admitted as duehas been paid in the appropriate treasury/bank as perproof enclosed.

Verified on this���.day of���.200....... at.����

...................................................................(Signature of applicant or his

authorized representative)

Acknowledgement

Received from������������memorandumof appeal with enclosures mentioned thereinand ��������

Seal of Office Date:

______

FORM ENT - XIVSee rule 28(1)

Certificate of Recovery under Section 7 of GoaEntertainment Tax Act, 1964

WARD NAME

REGN. CERTIFICATE No.

1. Name & Style ofactivity of defaulter

2. Address of the Place Main Officeof entertainment

Additional place 1Additional place 2Additional place 3

3. Constitution of the Naturedefaulter entity

Names & Address of Partners// P r o p r i e t o r s / M a n a g i n gDirector/Office bearers/Keypersons

1.

2.

3.

4.

5.

4A. Amount to berecovered

4B. Period to whichdues pertain

5. Details of Assets of defaulter

6. Head of account to which theamount is to be credited

Date of Issue of RC ...................................Signature of AA

Seal

1322 OFFICIAL GAZETTE � GOVT. OF GOASERIES I No. 51 (EXTRAORDINARY) 22ND MARCH, 2007

FORM ENT - XV[See rule 30 (1)]

Refund Voucher

WARD No.

REGN. CERTIFICATE No.

1. Name and Style of Payee

2. Address of the Main Office//place of entertainment

3. Details of Amount Date of Sl. No. in Amountto be refunded Order Collection

Register

Date of Issue of RO.................................Signature of AA

Seal

FORM ENT - XV Counterfoil[See Rule 30 (1)]

Refund Order

WARD No.

REGN. CERTIFICATE No.

1. Name and Style of Payee

2. Address of the Main Office//Place of entertainment

3. Details of Amount Date of Sl. No. in Amountto be refunded Order Collection

Register

Date of Issue of RO....................................Signature of AA

Seal

_____________________________GOVERNMENT PRINTING PRESS,

PANAJI-GOAPRICE: Rs. 24.00

www.goagovt.nic.in/gazette.htm