red bank charter school of monmouth county red bank

TRANSCRIPT

Red Bank Charter School

of Monmouth County

Red Bank Charter School

Red Bank, New Jersey

COMPREHENSIVE ANNUAL FINANCIAL REPORT

Fiscal Year Ended June 30, 2020

COMPREHENSIVE ANNUALFINANCIAL REPORT

Of the

Red Bank Charter Schoolof Monmouth County

Red Bank, New Jersey

For the Fiscal Year Ended June 30, 2020

Prepared by

David P. BlockSchool Business Administrator

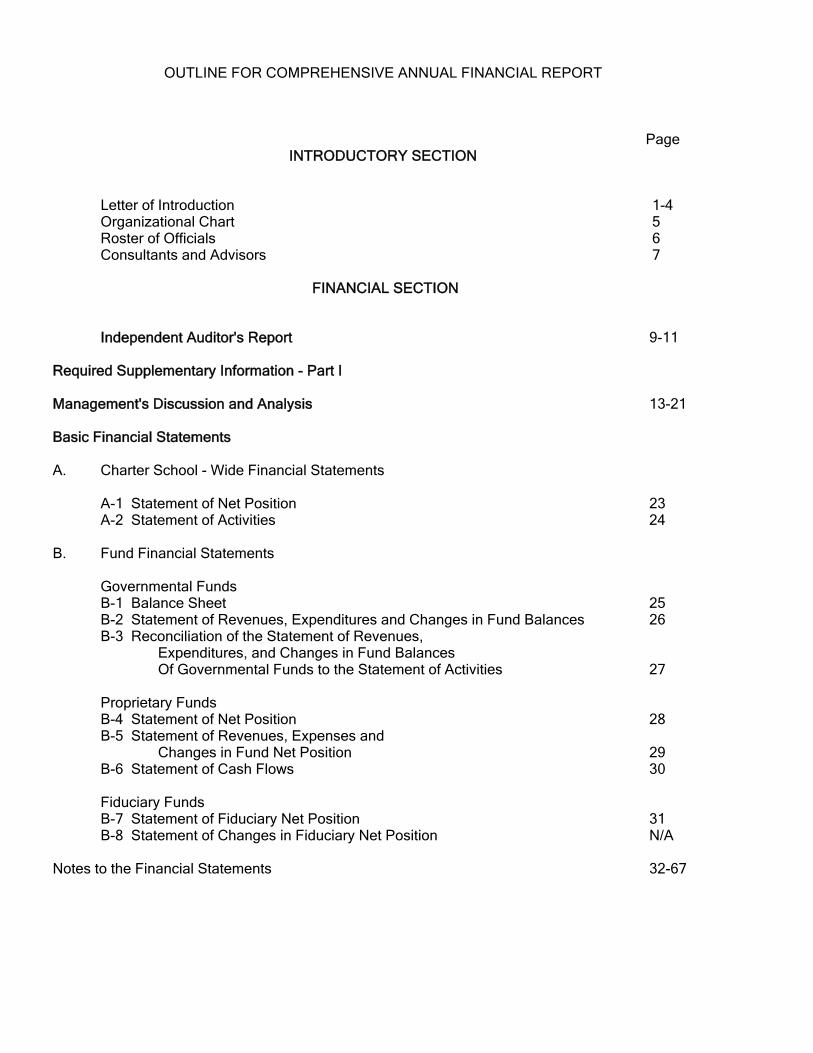

OUTLINE FOR COMPREHENSIVE ANNUAL FINANCIAL REPORT

PageINTRODUCTORY SECTION

Letter of Introduction 1-4Organizational Chart 5Roster of Officials 6Consultants and Advisors 7

FINANCIAL SECTION

Independent Auditor's Report 9-11

Required Supplementary Information - Part I

Management's Discussion and Analysis 13-21

Basic Financial Statements

A. Charter School - Wide Financial Statements

A-1 Statement of Net Position 23A-2 Statement of Activities 24

B. Fund Financial Statements

Governmental FundsB-1 Balance Sheet 25B-2 Statement of Revenues, Expenditures and Changes in Fund Balances 26B-3 Reconciliation of the Statement of Revenues,

Expenditures, and Changes in Fund BalancesOf Governmental Funds to the Statement of Activities 27

Proprietary FundsB-4 Statement of Net Position 28B-5 Statement of Revenues, Expenses and

Changes in Fund Net Position 29B-6 Statement of Cash Flows 30

Fiduciary FundsB-7 Statement of Fiduciary Net Position 31B-8 Statement of Changes in Fiduciary Net Position N/A

Notes to the Financial Statements 32-67

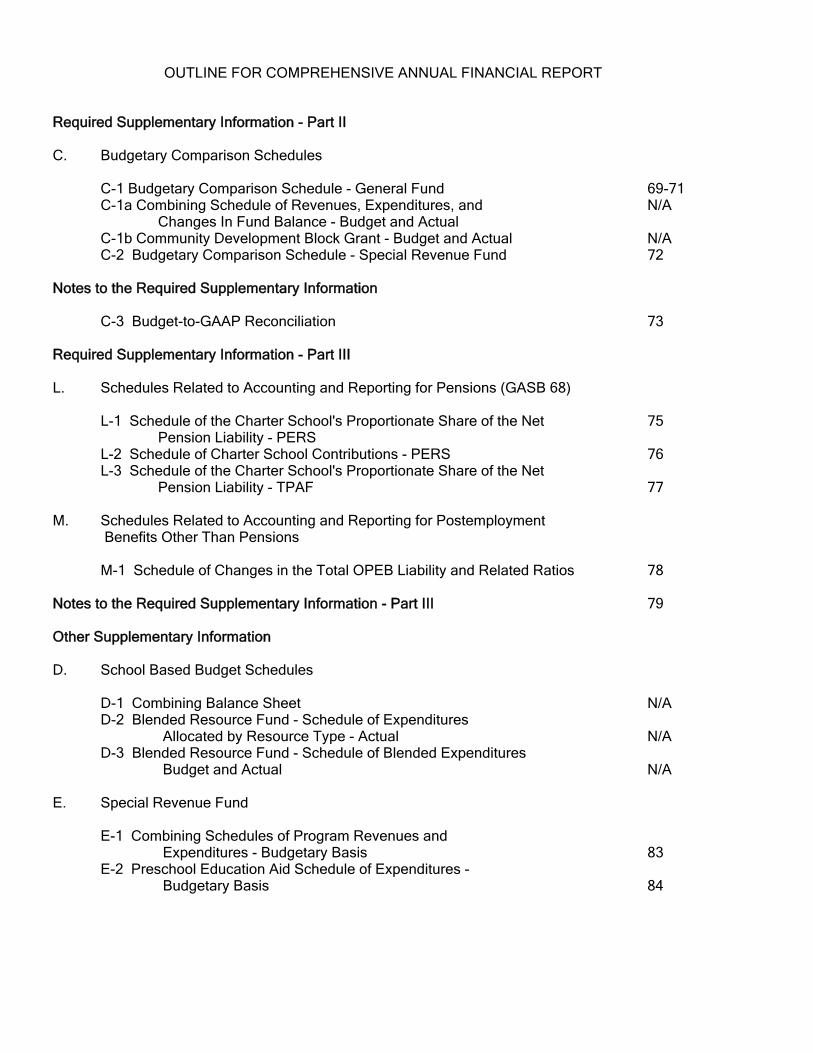

OUTLINE FOR COMPREHENSIVE ANNUAL FINANCIAL REPORT

Required Supplementary Information - Part II

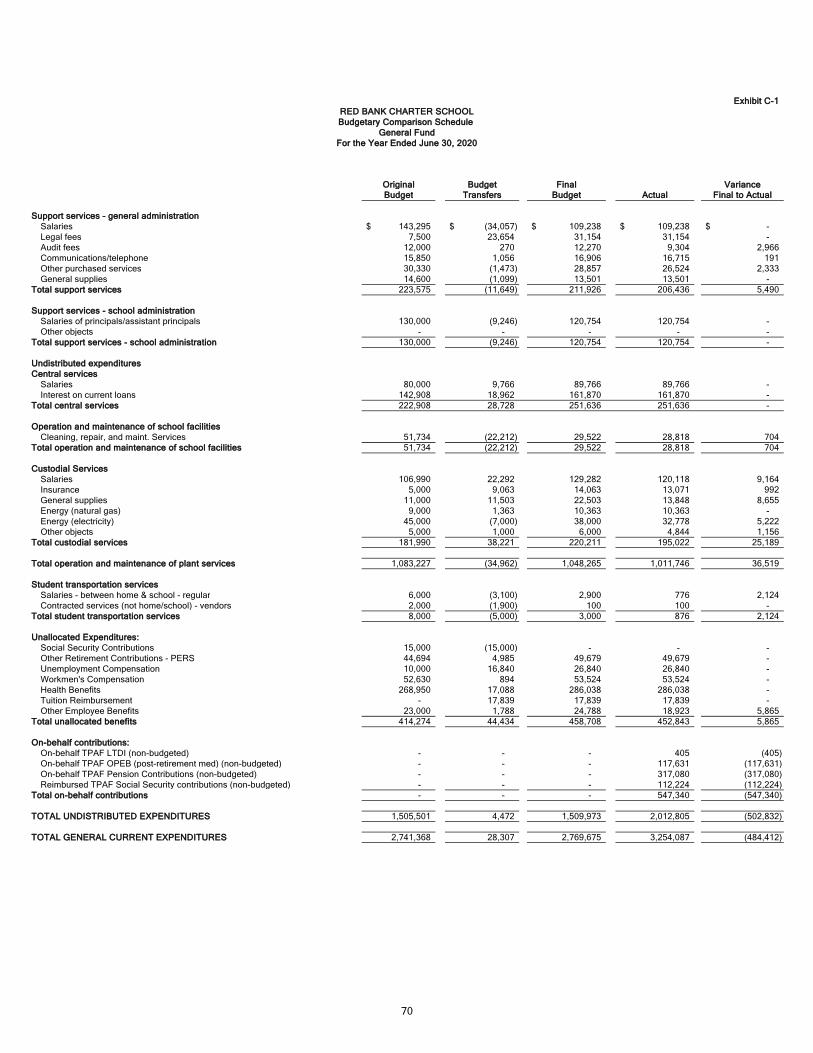

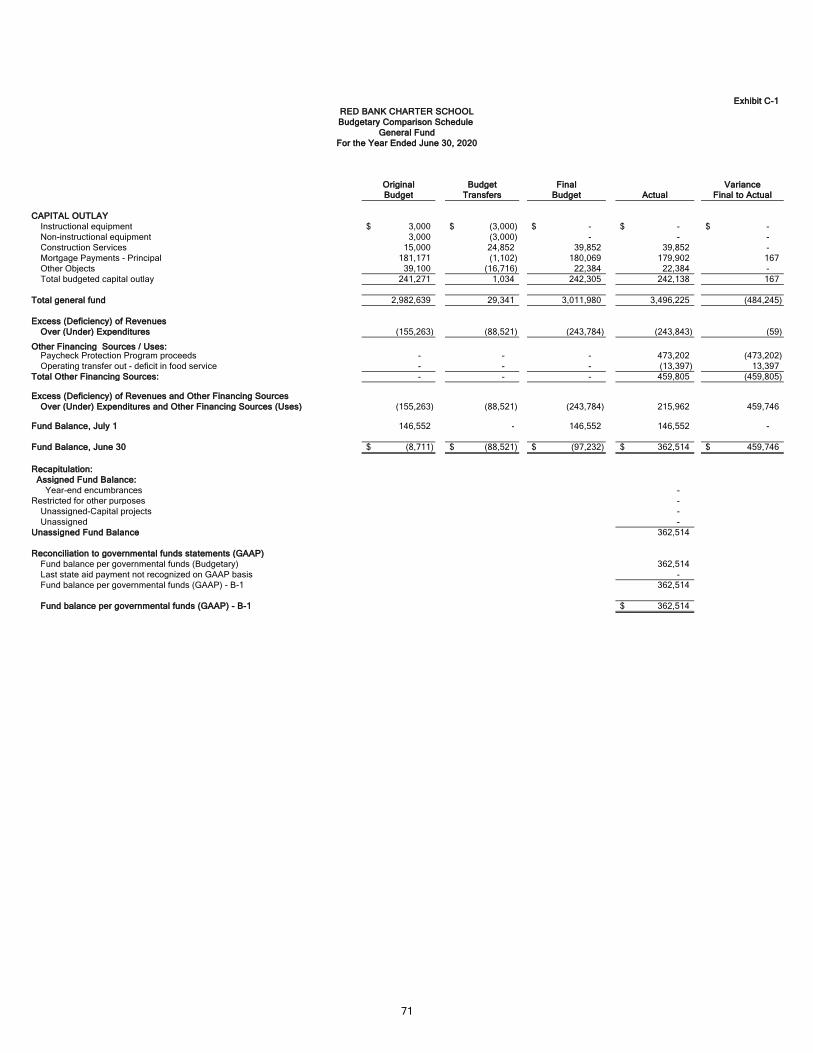

C. Budgetary Comparison Schedules

C-1 Budgetary Comparison Schedule - General Fund 69-71C-1a Combining Schedule of Revenues, Expenditures, and N/A

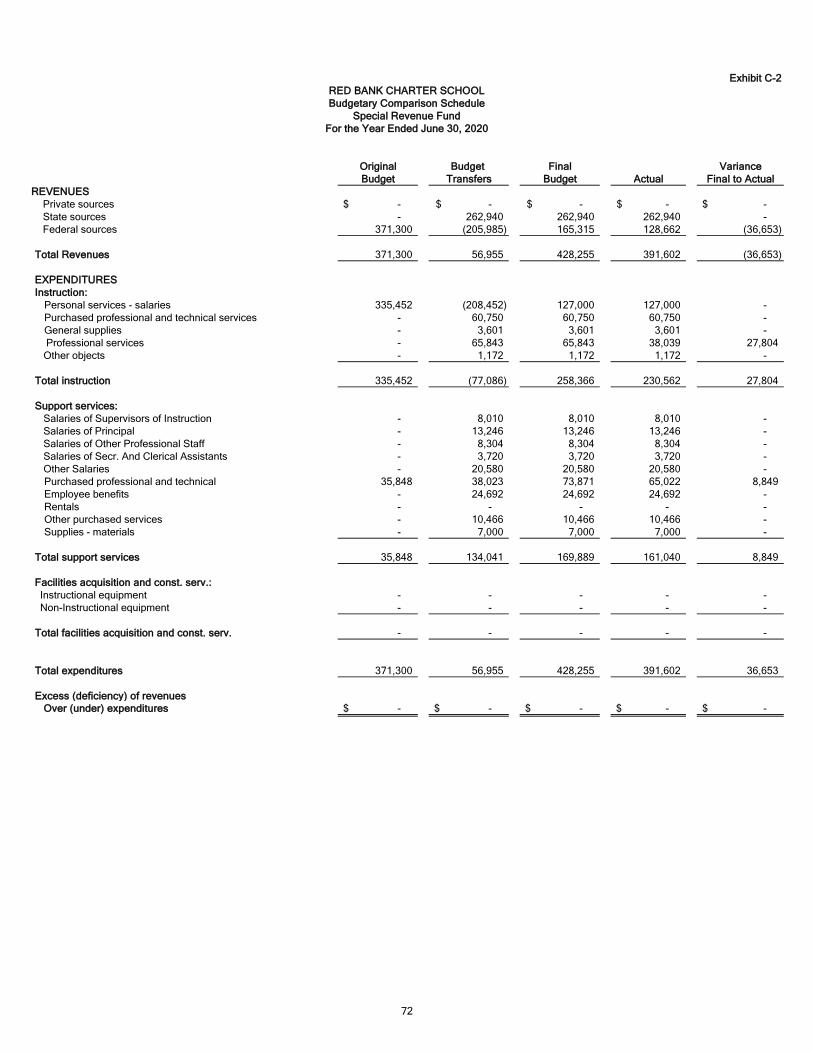

Changes In Fund Balance - Budget and ActualC-1b Community Development Block Grant - Budget and Actual N/AC-2 Budgetary Comparison Schedule - Special Revenue Fund 72

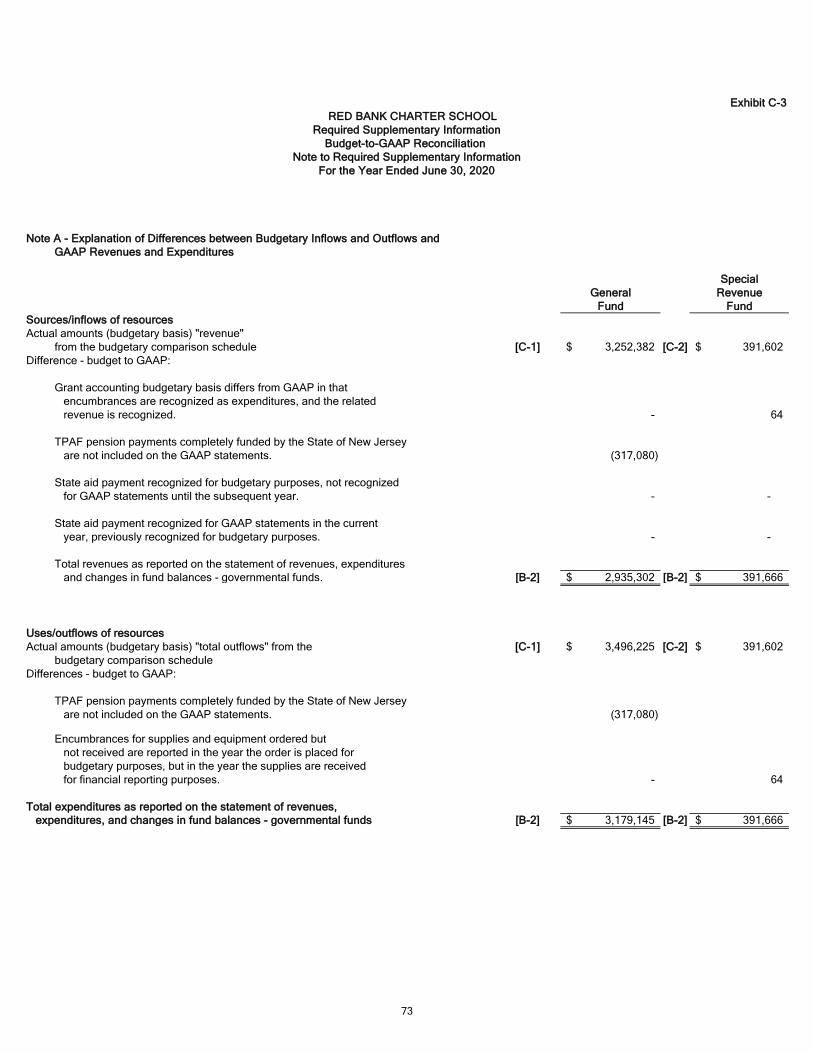

Notes to the Required Supplementary Information

C-3 Budget-to-GAAP Reconciliation 73

Required Supplementary Information - Part III

L. Schedules Related to Accounting and Reporting for Pensions (GASB 68)

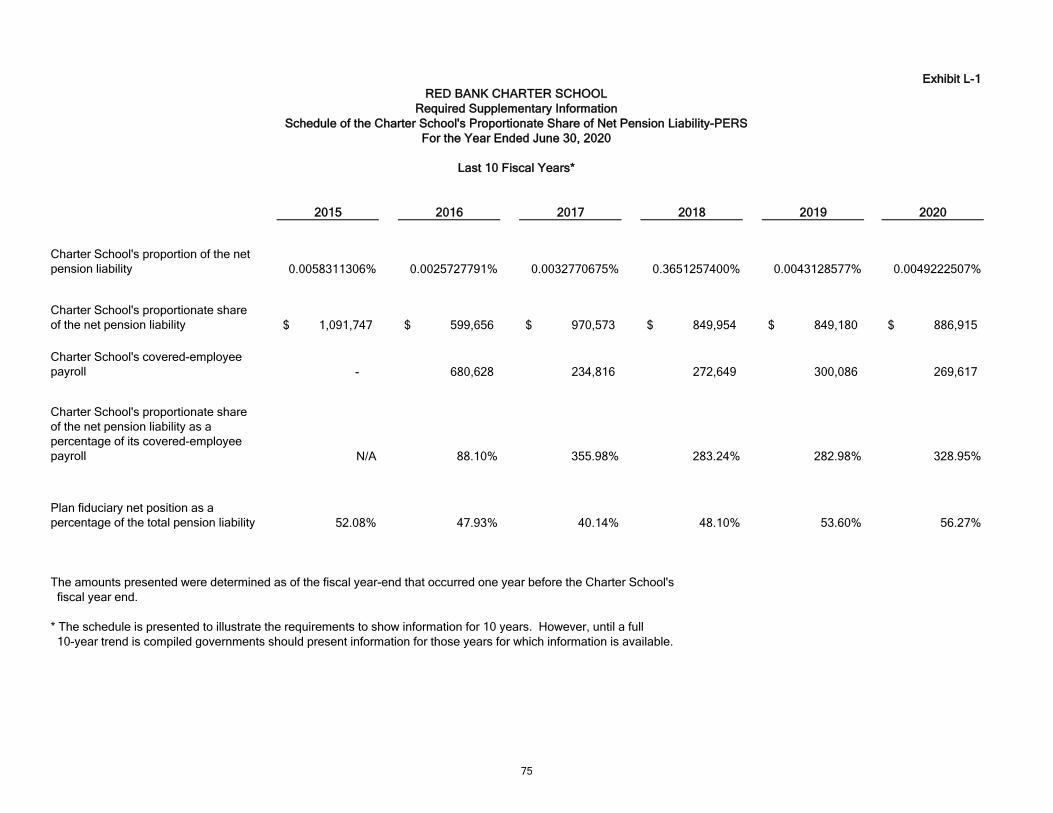

L-1 Schedule of the Charter School's Proportionate Share of the Net 75Pension Liability - PERS

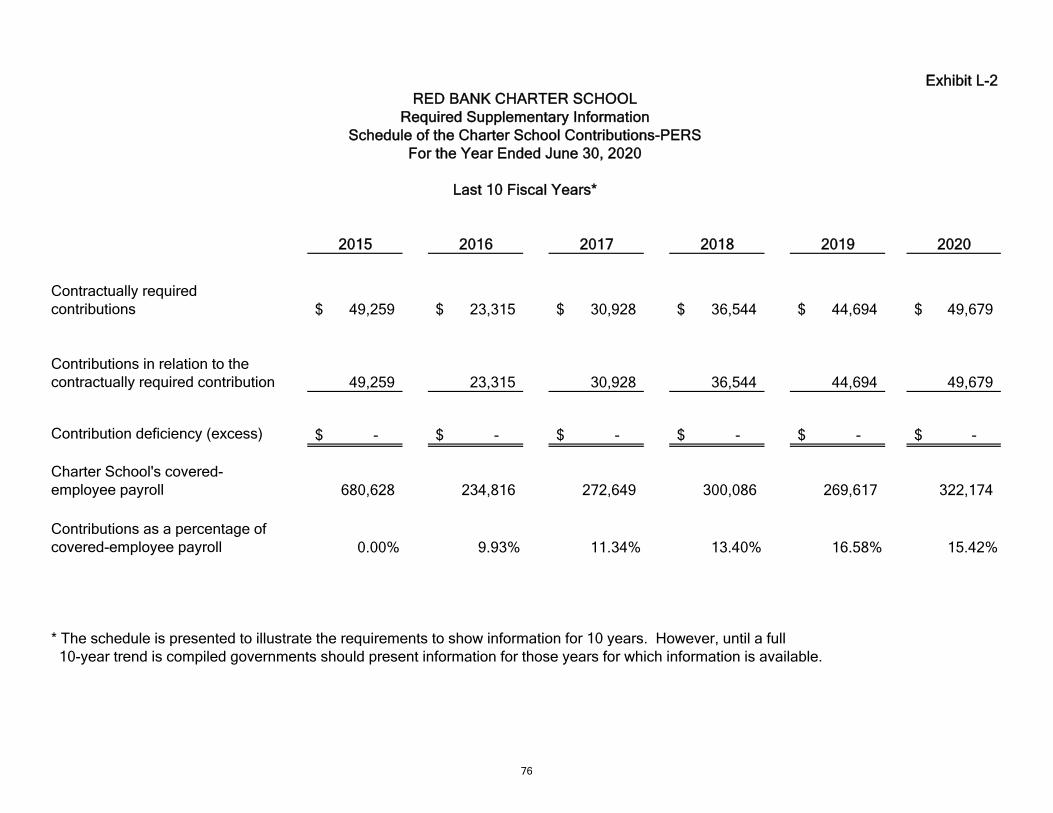

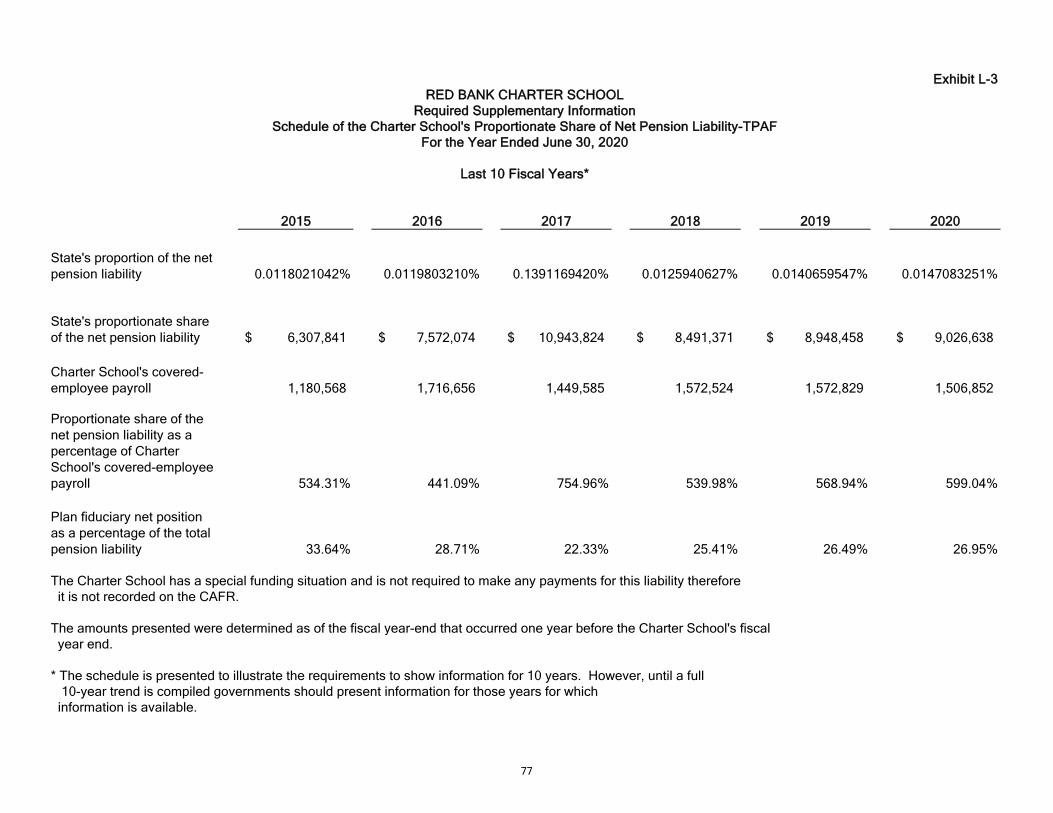

L-2 Schedule of Charter School Contributions - PERS 76L-3 Schedule of the Charter School's Proportionate Share of the Net

Pension Liability - TPAF 77

M. Schedules Related to Accounting and Reporting for Postemployment Benefits Other Than Pensions

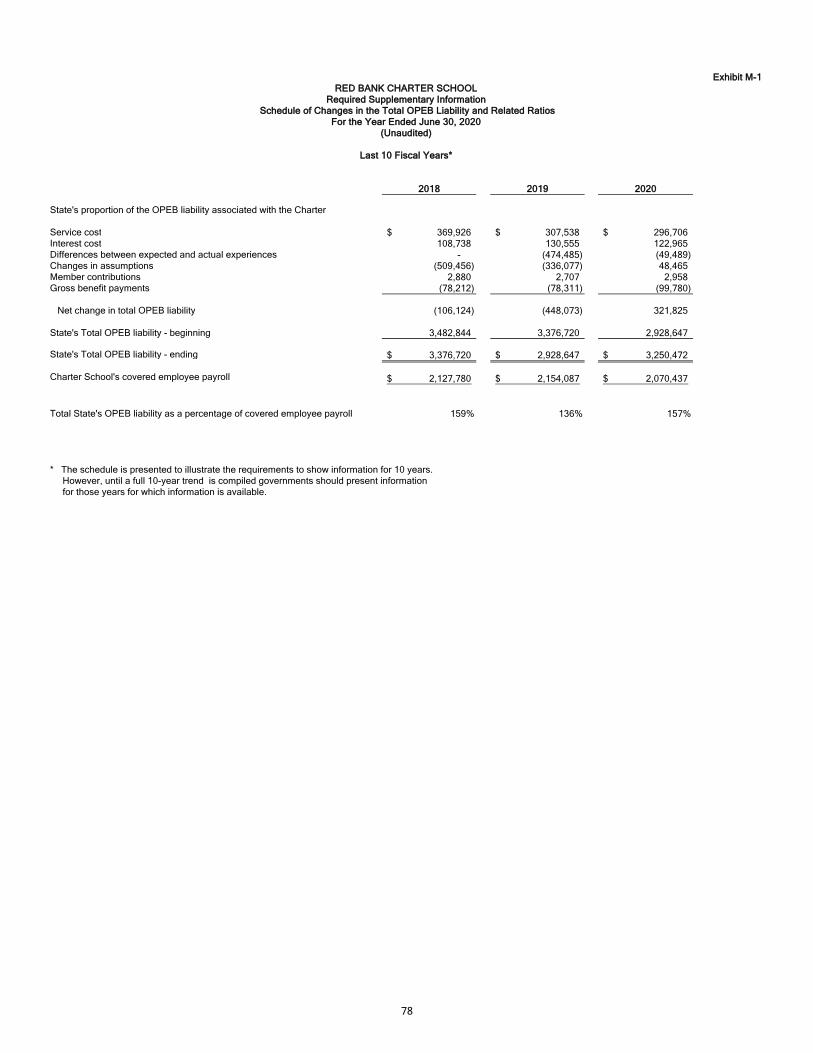

M-1 Schedule of Changes in the Total OPEB Liability and Related Ratios 78

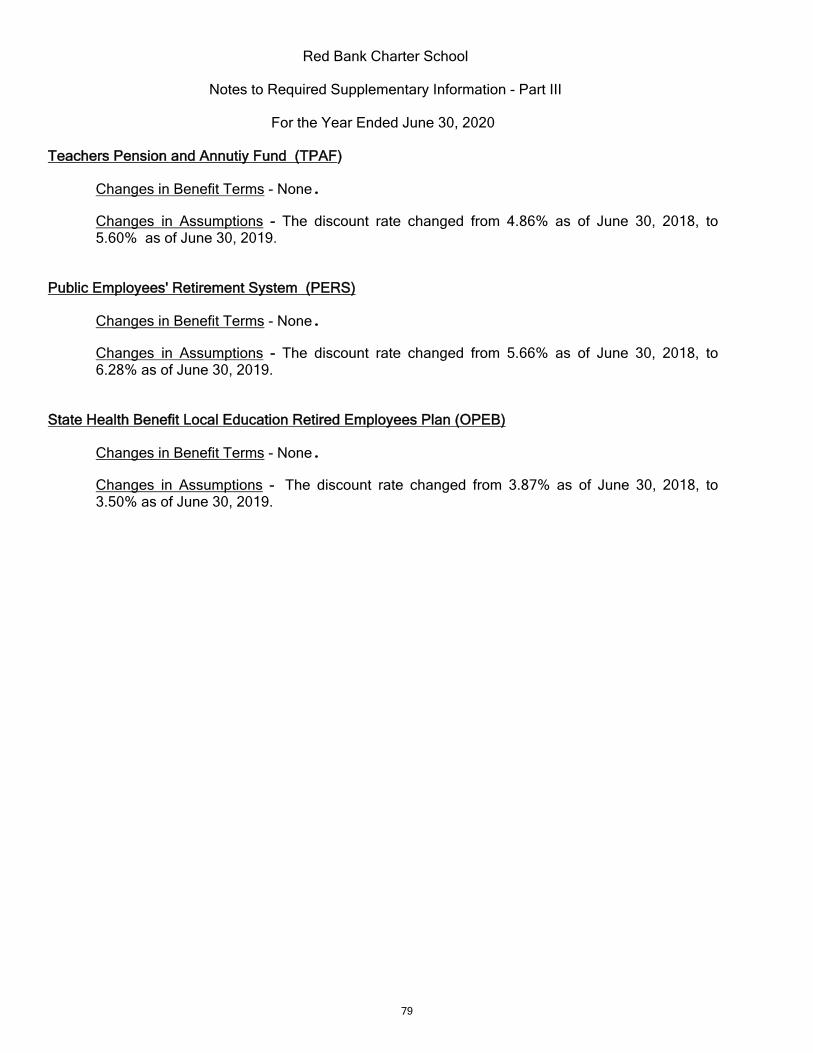

Notes to the Required Supplementary Information - Part III 79

Other Supplementary Information

D. School Based Budget Schedules

D-1 Combining Balance Sheet N/AD-2 Blended Resource Fund - Schedule of Expenditures

Allocated by Resource Type - Actual N/AD-3 Blended Resource Fund - Schedule of Blended Expenditures

Budget and Actual N/A

E. Special Revenue Fund

E-1 Combining Schedules of Program Revenues and Expenditures - Budgetary Basis 83

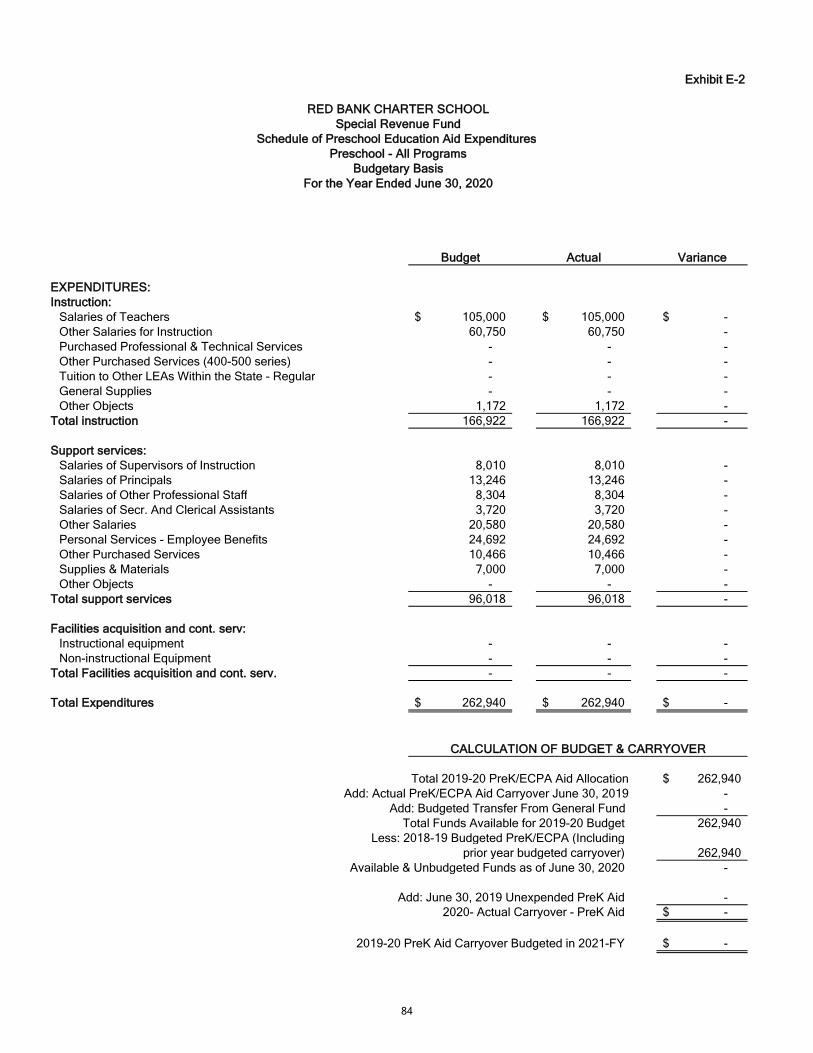

E-2 Preschool Education Aid Schedule of Expenditures -Budgetary Basis 84

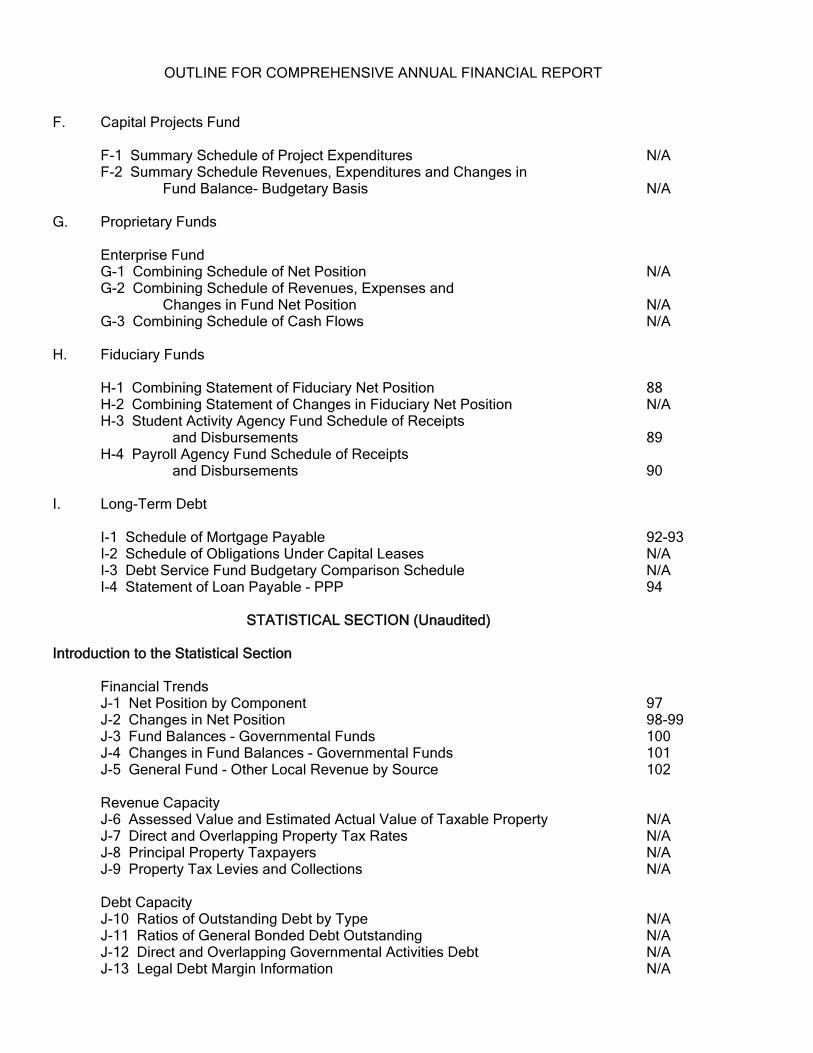

OUTLINE FOR COMPREHENSIVE ANNUAL FINANCIAL REPORT

F. Capital Projects Fund

F-1 Summary Schedule of Project Expenditures N/AF-2 Summary Schedule Revenues, Expenditures and Changes in

Fund Balance- Budgetary Basis N/A

G. Proprietary Funds

Enterprise FundG-1 Combining Schedule of Net Position N/AG-2 Combining Schedule of Revenues, Expenses and

Changes in Fund Net Position N/AG-3 Combining Schedule of Cash Flows N/A

H. Fiduciary Funds

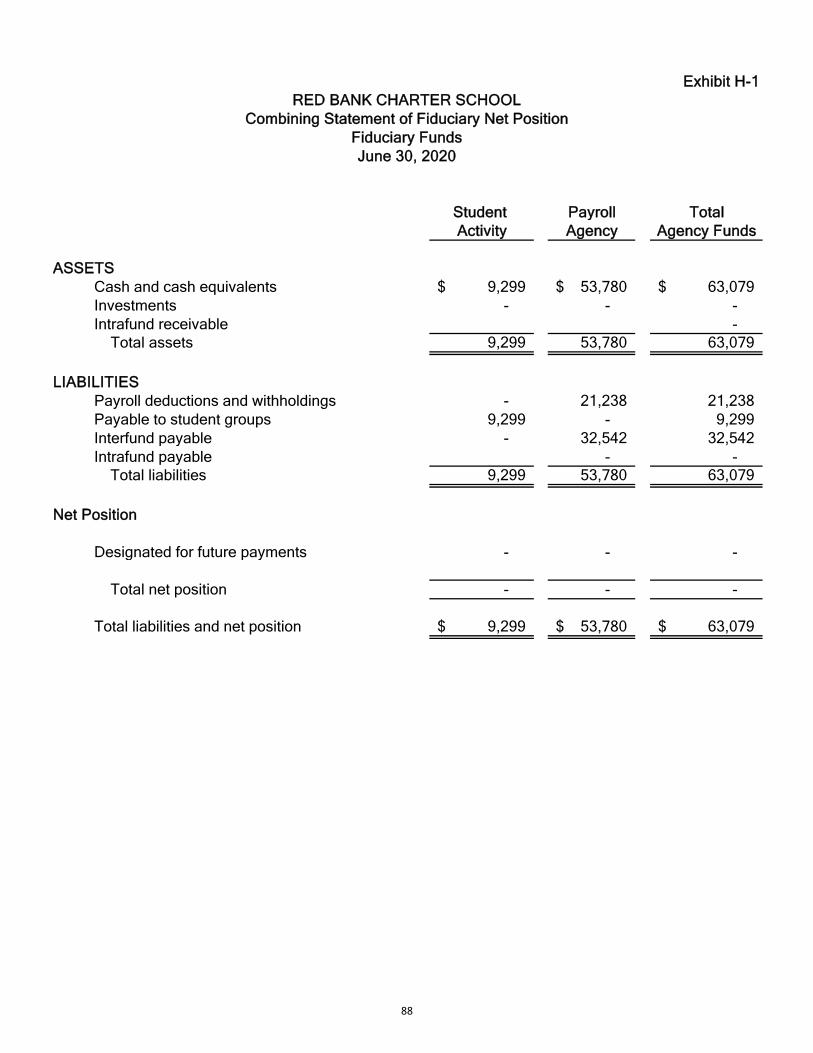

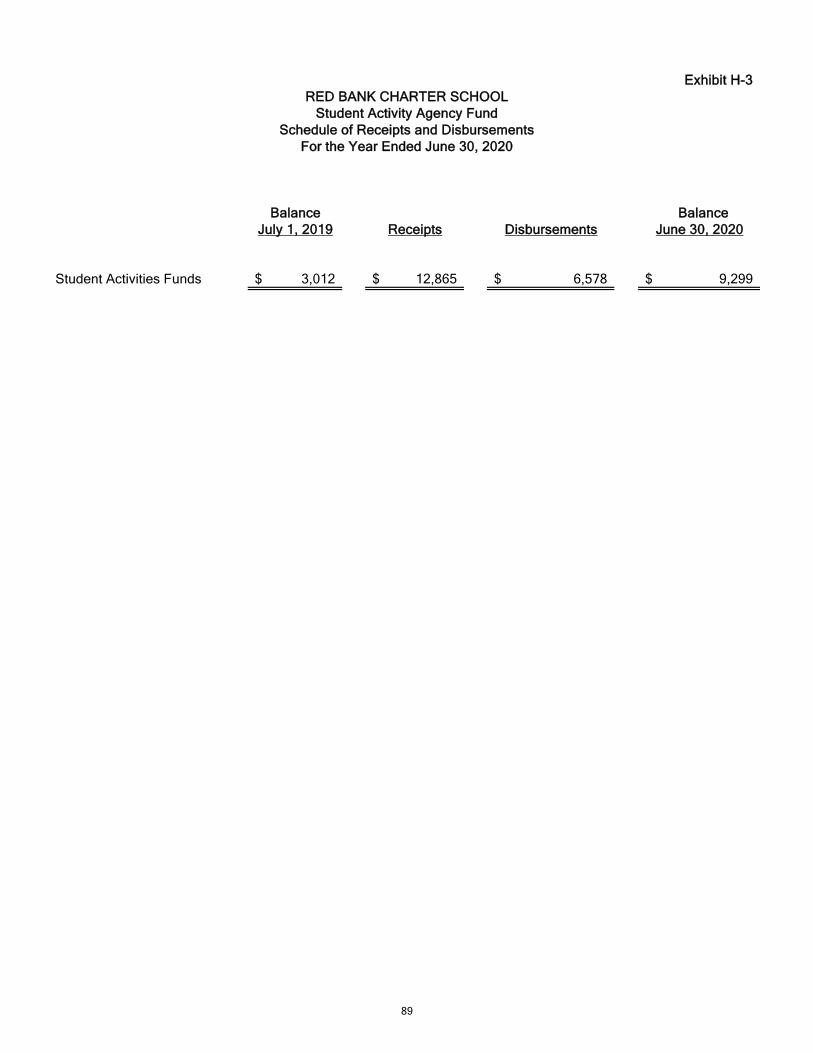

H-1 Combining Statement of Fiduciary Net Position 88H-2 Combining Statement of Changes in Fiduciary Net Position N/AH-3 Student Activity Agency Fund Schedule of Receipts

and Disbursements 89H-4 Payroll Agency Fund Schedule of Receipts

and Disbursements 90

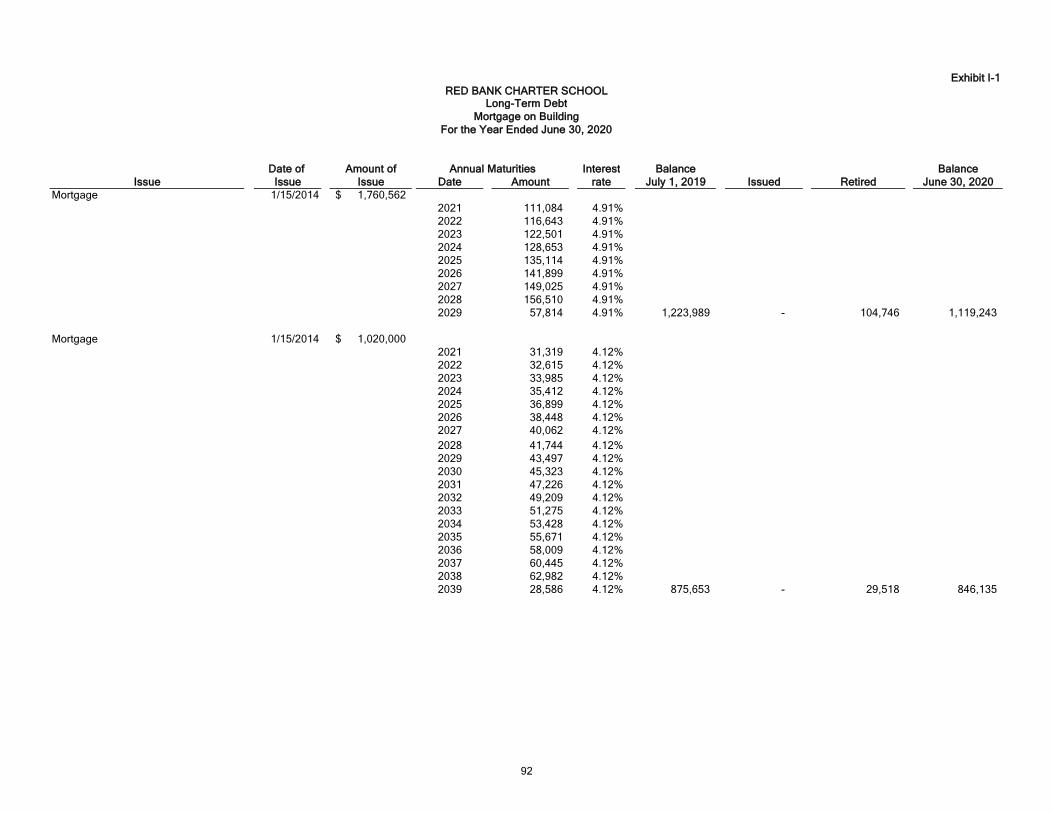

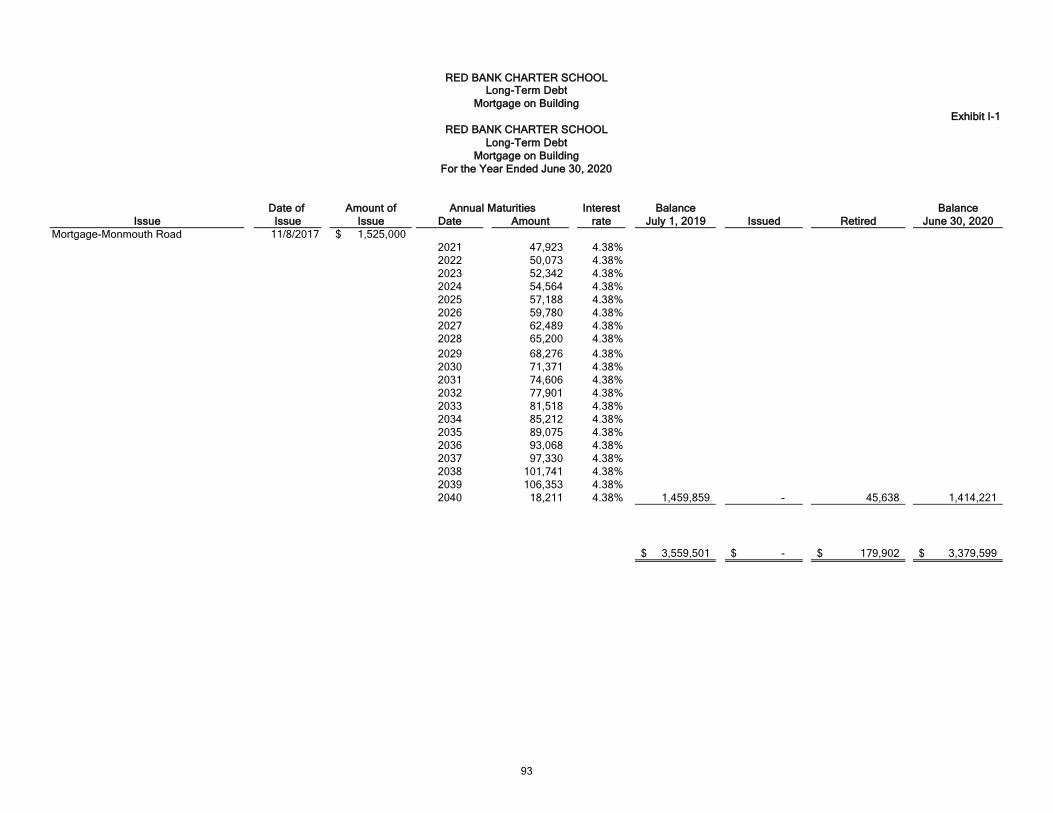

I. Long-Term Debt

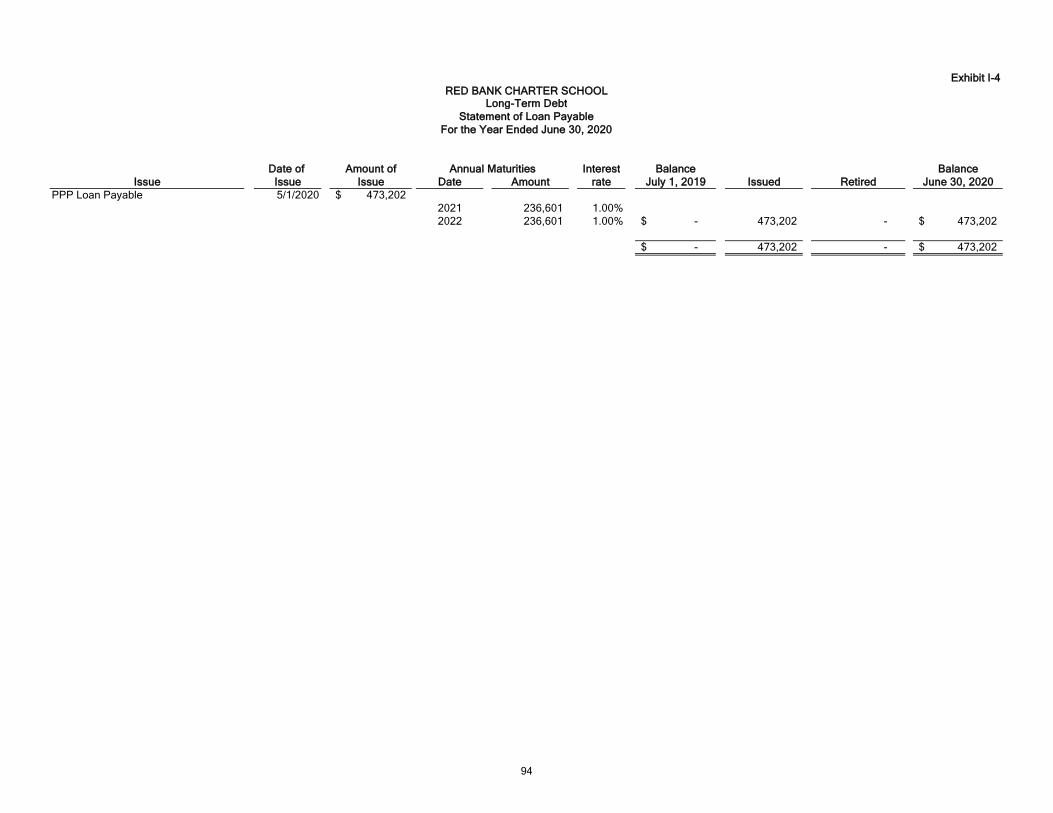

I-1 Schedule of Mortgage Payable 92-93I-2 Schedule of Obligations Under Capital Leases N/AI-3 Debt Service Fund Budgetary Comparison Schedule N/AI-4 Statement of Loan Payable - PPP 94

STATISTICAL SECTION (Unaudited)

Introduction to the Statistical Section

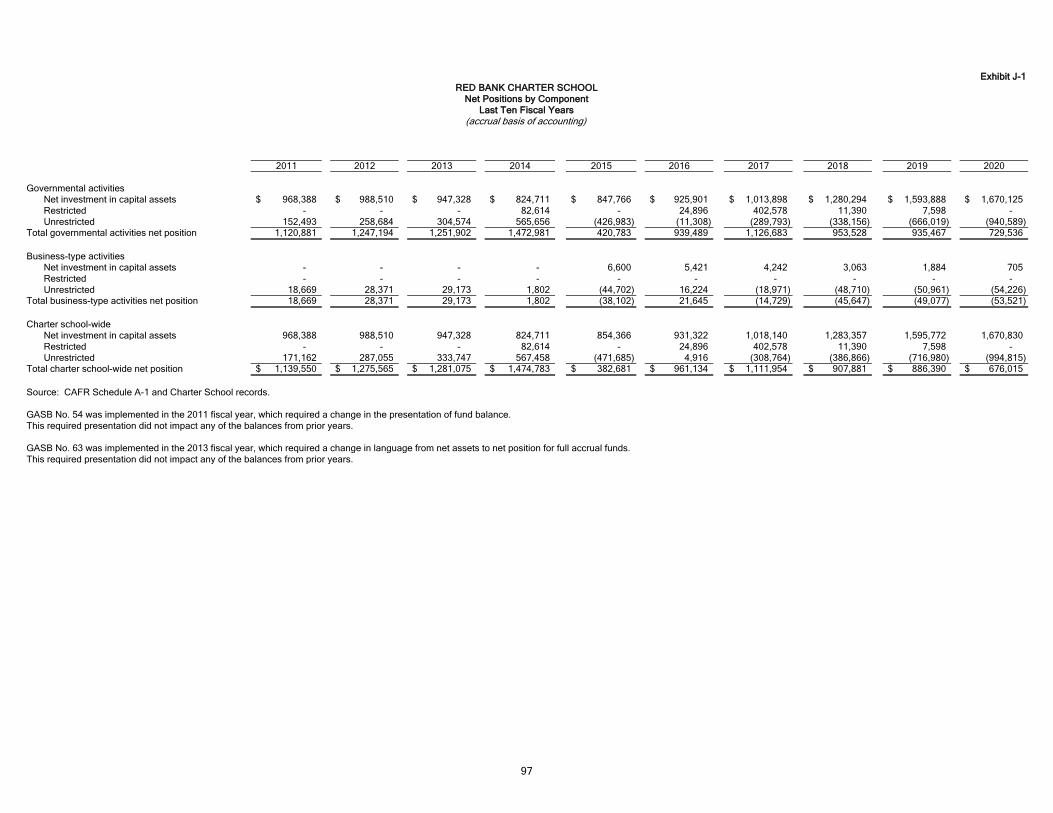

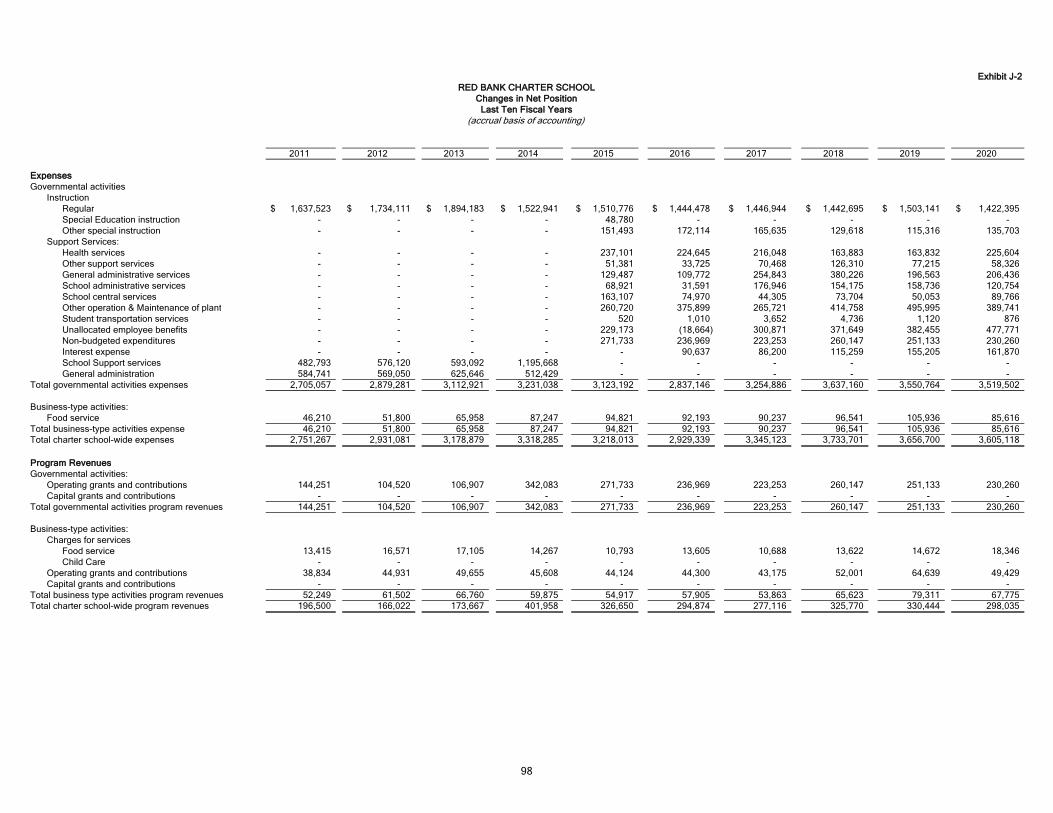

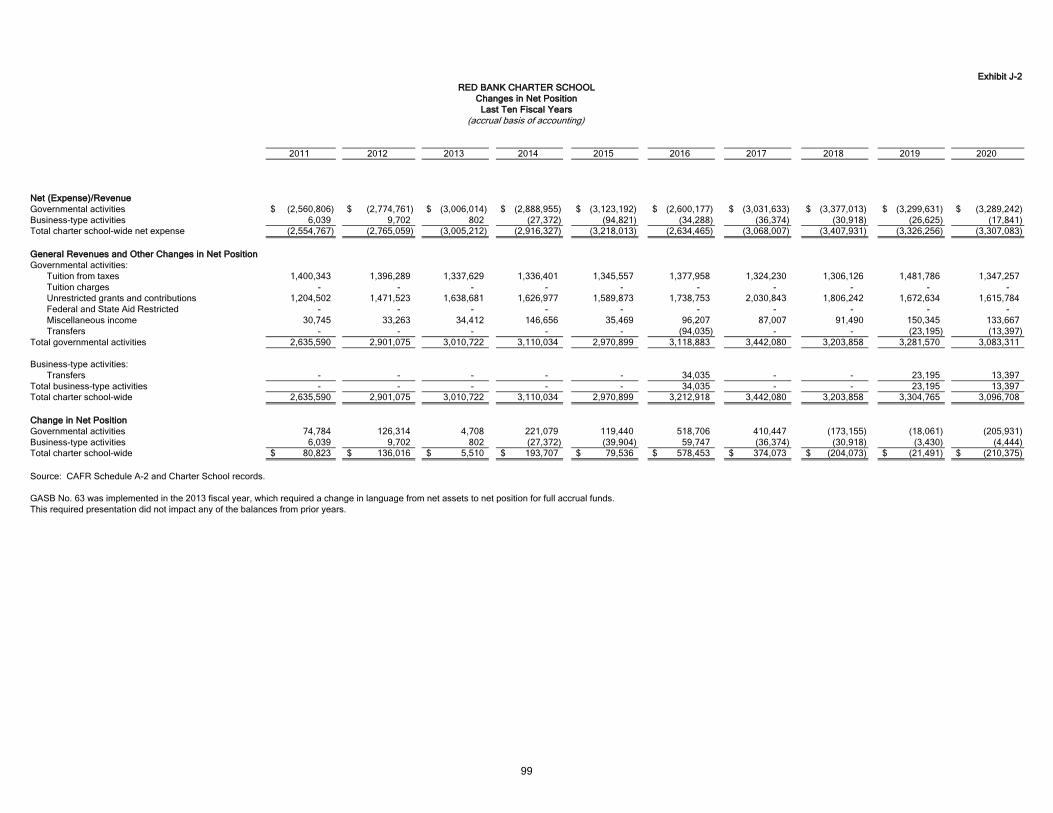

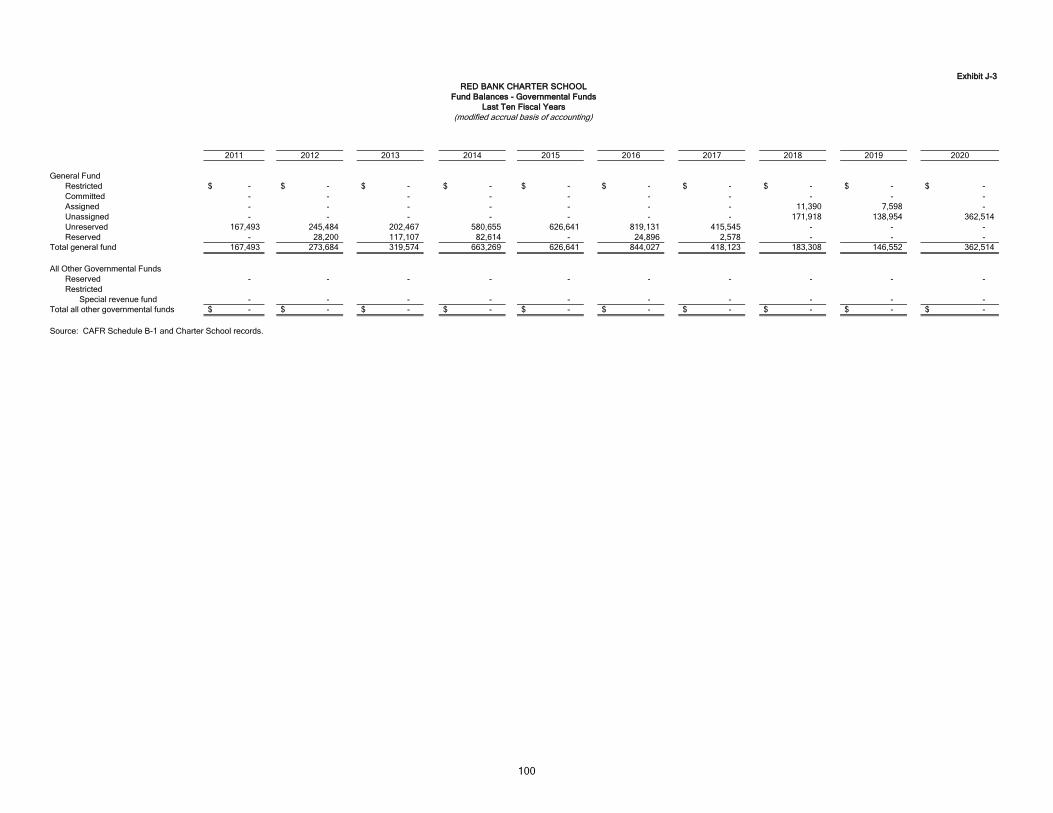

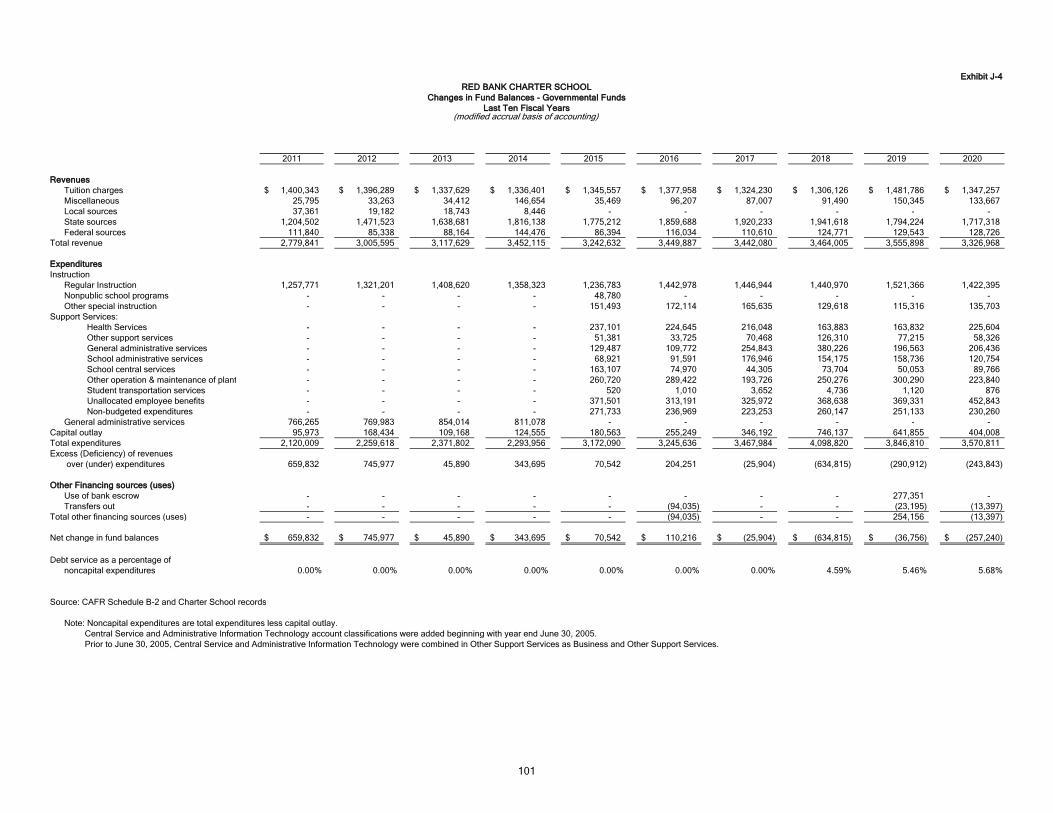

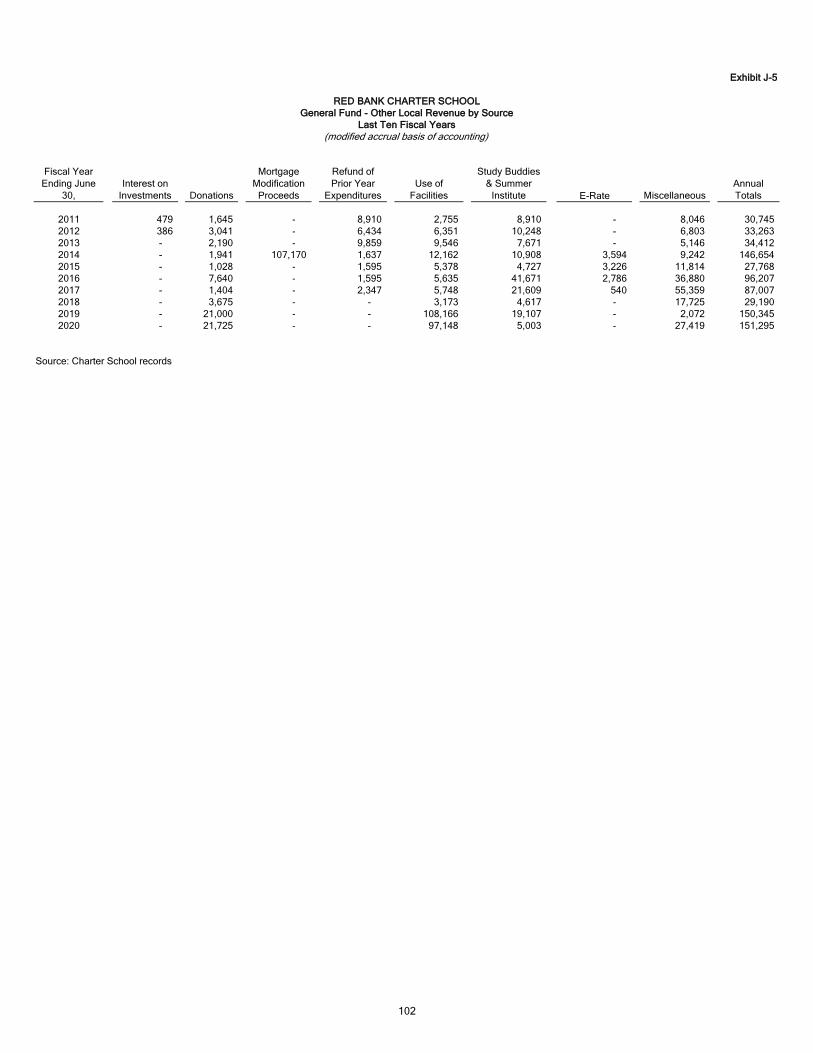

Financial TrendsJ-1 Net Position by Component 97J-2 Changes in Net Position 98-99J-3 Fund Balances - Governmental Funds 100J-4 Changes in Fund Balances - Governmental Funds 101J-5 General Fund - Other Local Revenue by Source 102

Revenue CapacityJ-6 Assessed Value and Estimated Actual Value of Taxable Property N/AJ-7 Direct and Overlapping Property Tax Rates N/AJ-8 Principal Property Taxpayers N/AJ-9 Property Tax Levies and Collections N/A

Debt CapacityJ-10 Ratios of Outstanding Debt by Type N/AJ-11 Ratios of General Bonded Debt Outstanding N/AJ-12 Direct and Overlapping Governmental Activities Debt N/AJ-13 Legal Debt Margin Information N/A

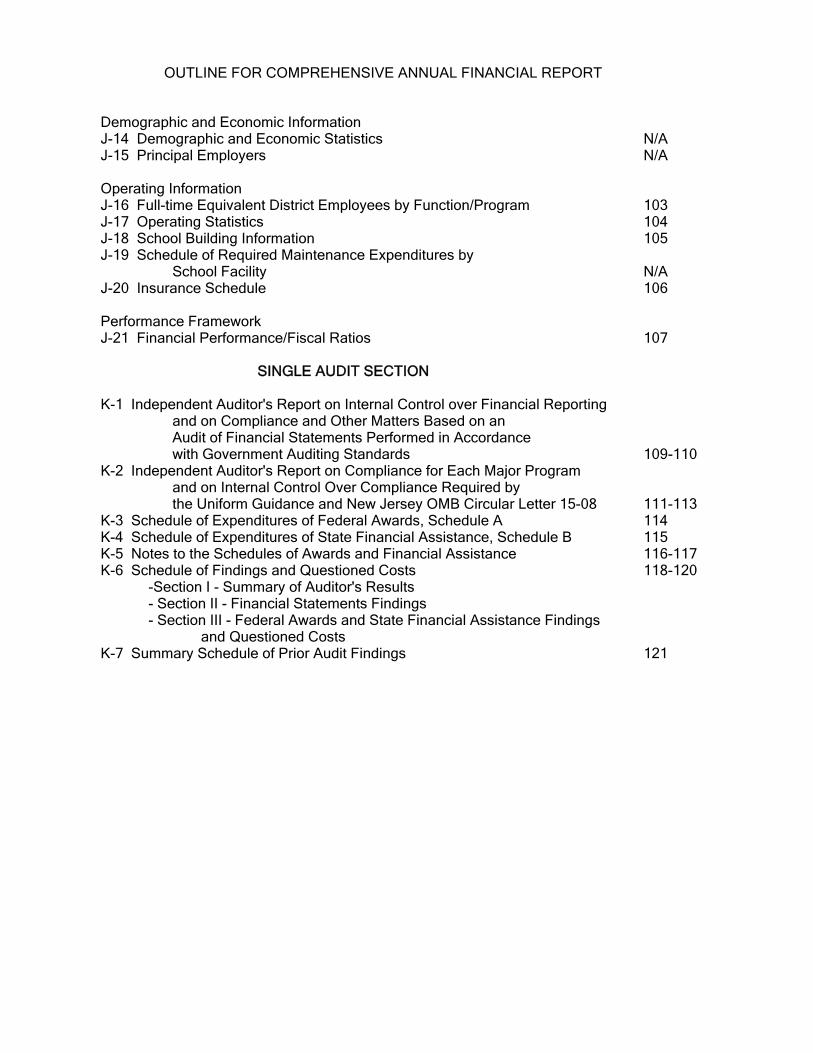

OUTLINE FOR COMPREHENSIVE ANNUAL FINANCIAL REPORT

Demographic and Economic InformationJ-14 Demographic and Economic Statistics N/AJ-15 Principal Employers N/A

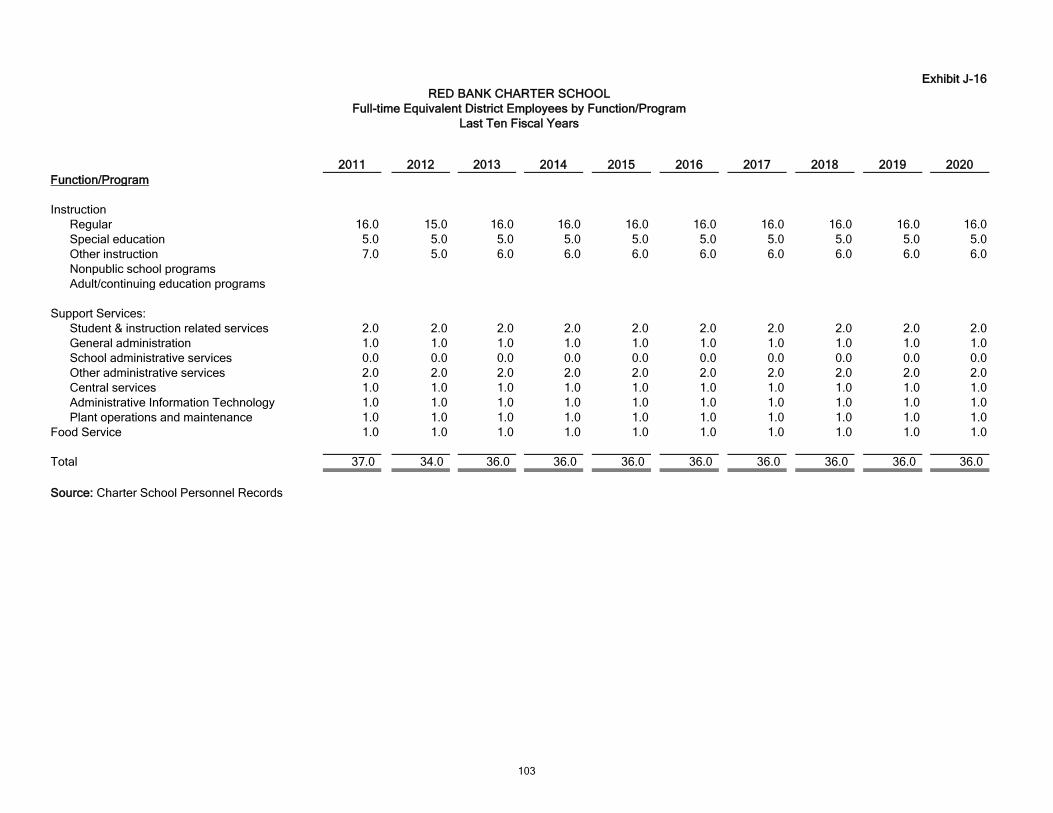

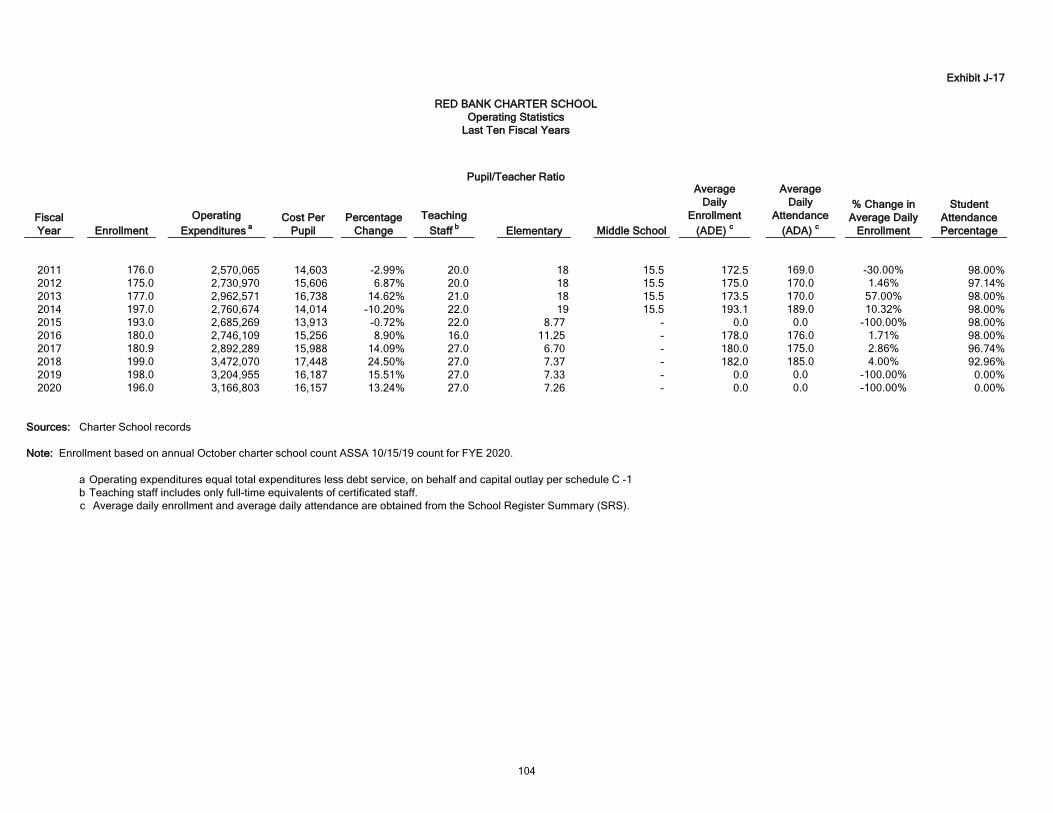

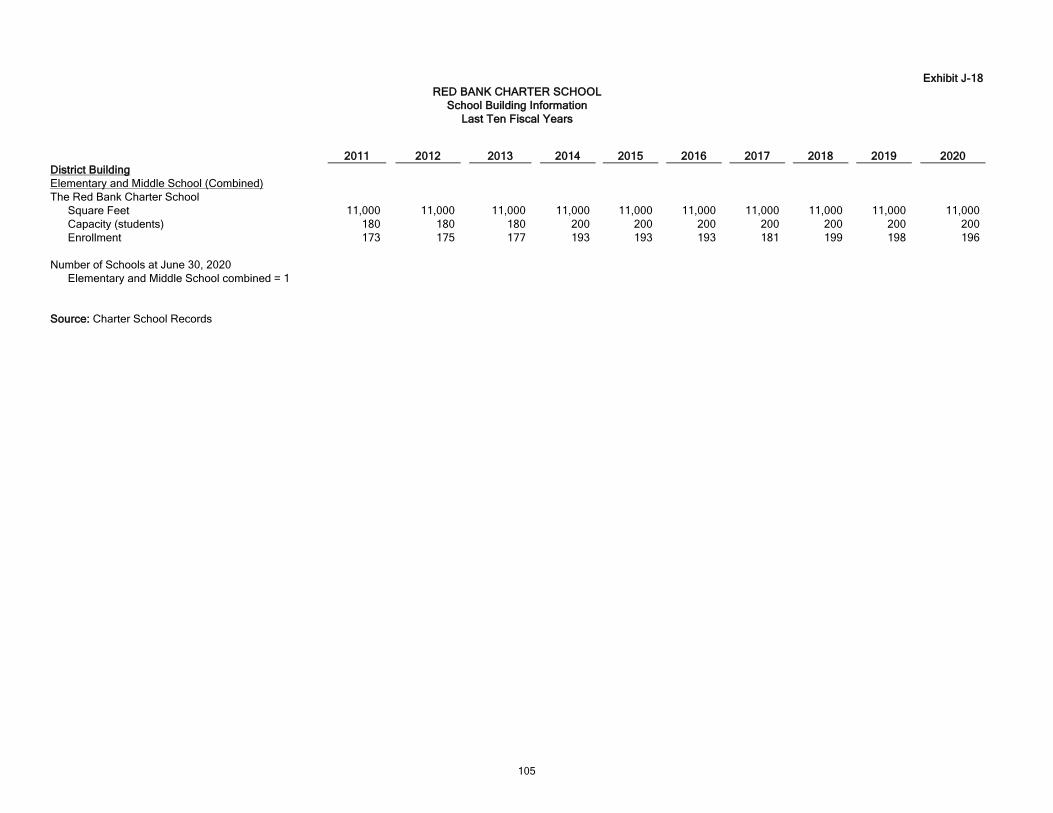

Operating InformationJ-16 Full-time Equivalent District Employees by Function/Program 103J-17 Operating Statistics 104J-18 School Building Information 105J-19 Schedule of Required Maintenance Expenditures by

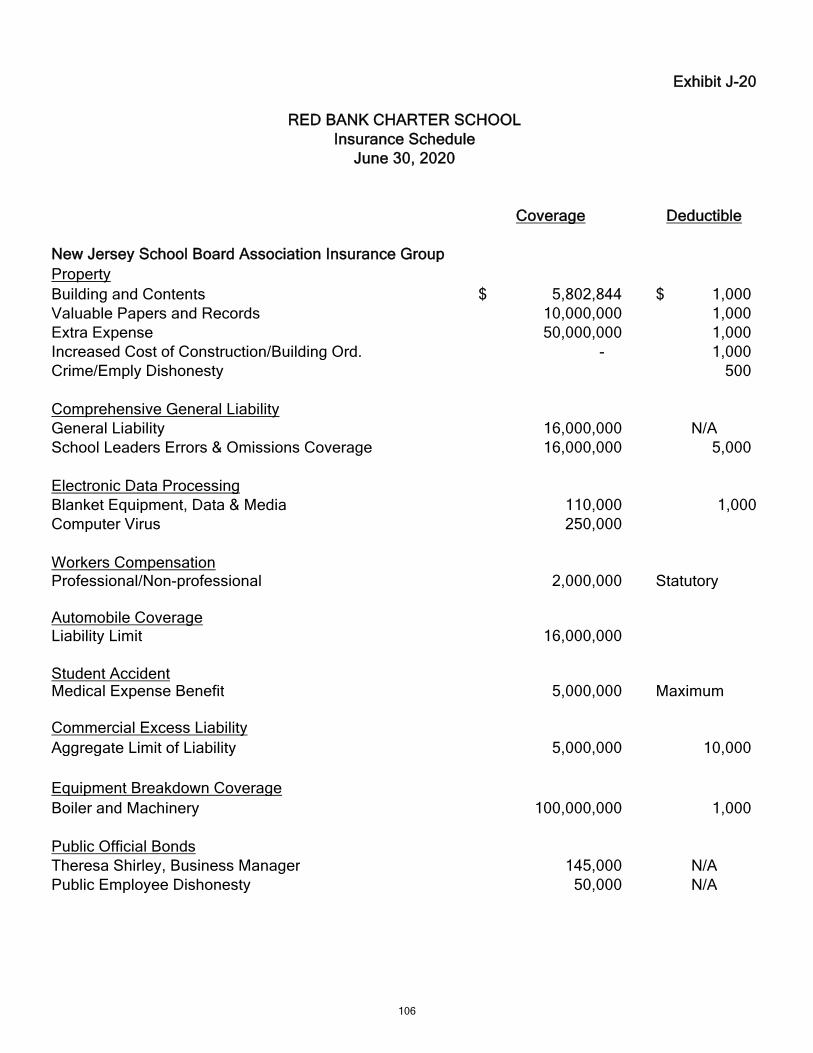

School Facility N/AJ-20 Insurance Schedule 106

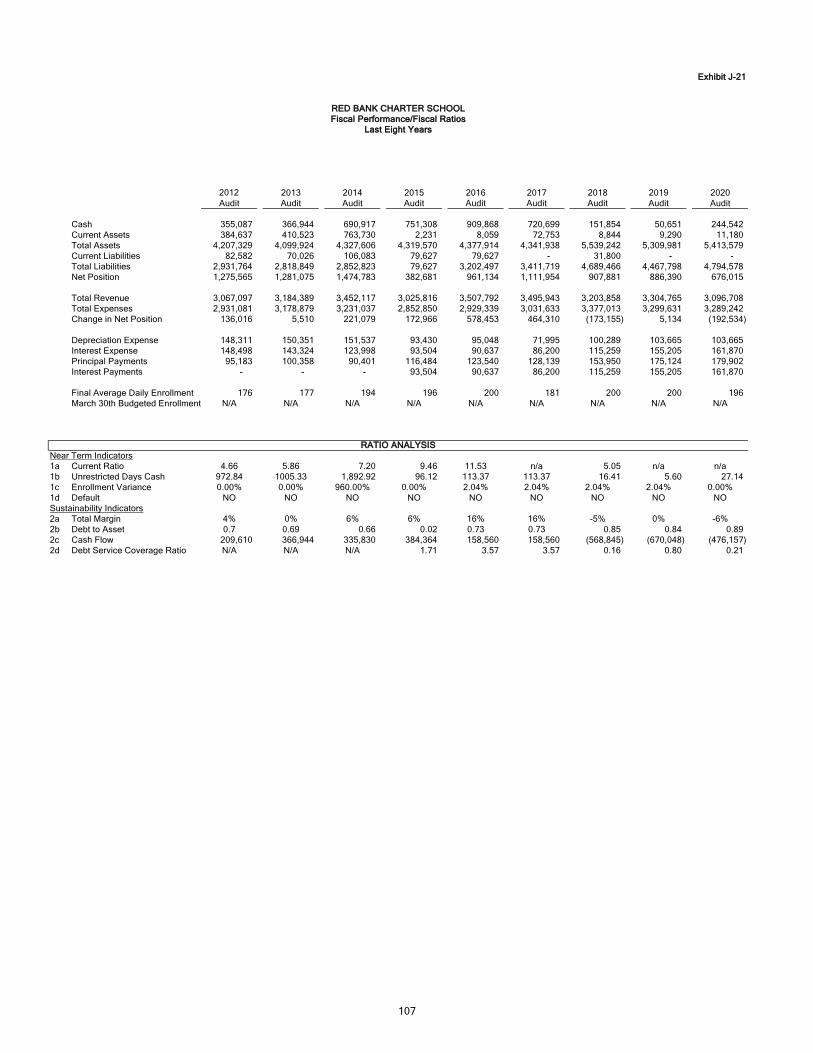

Performance FrameworkJ-21 Financial Performance/Fiscal Ratios 107

SINGLE AUDIT SECTION

K-1 Independent Auditor's Report on Internal Control over Financial Reportingand on Compliance and Other Matters Based on anAudit of Financial Statements Performed in Accordancewith Government Auditing Standards 109-110

K-2 Independent Auditor's Report on Compliance for Each Major Programand on Internal Control Over Compliance Required bythe Uniform Guidance and New Jersey OMB Circular Letter 15-08 111-113

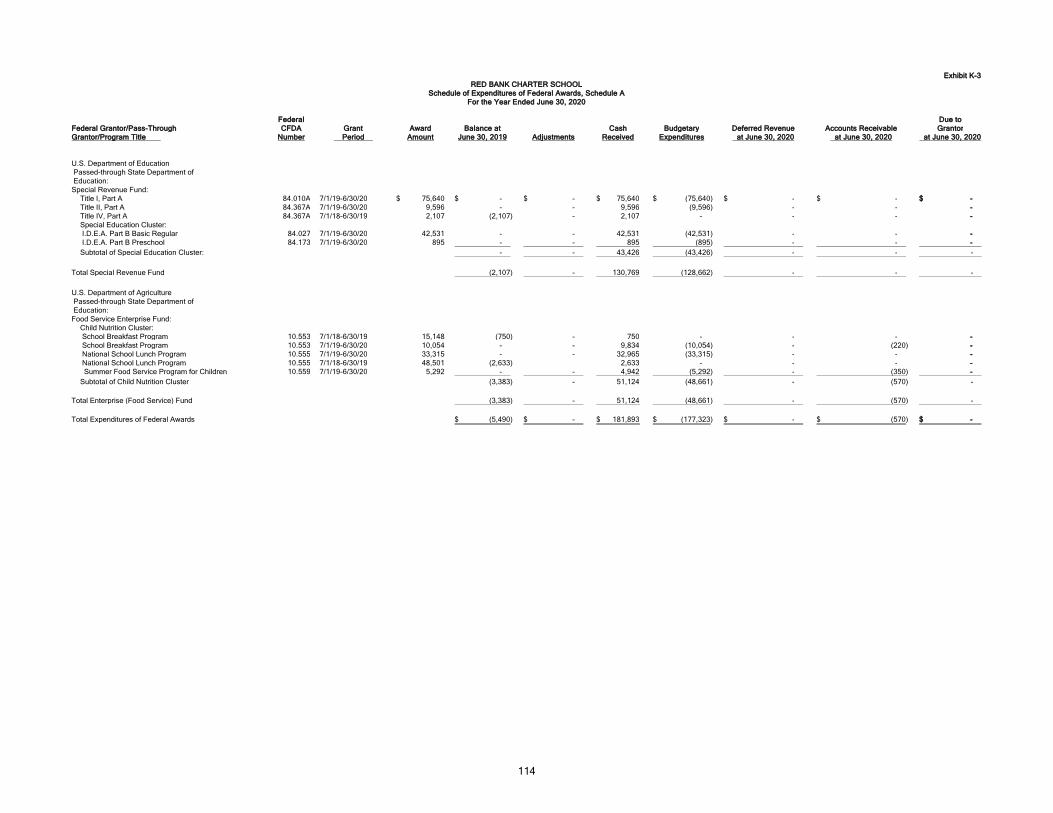

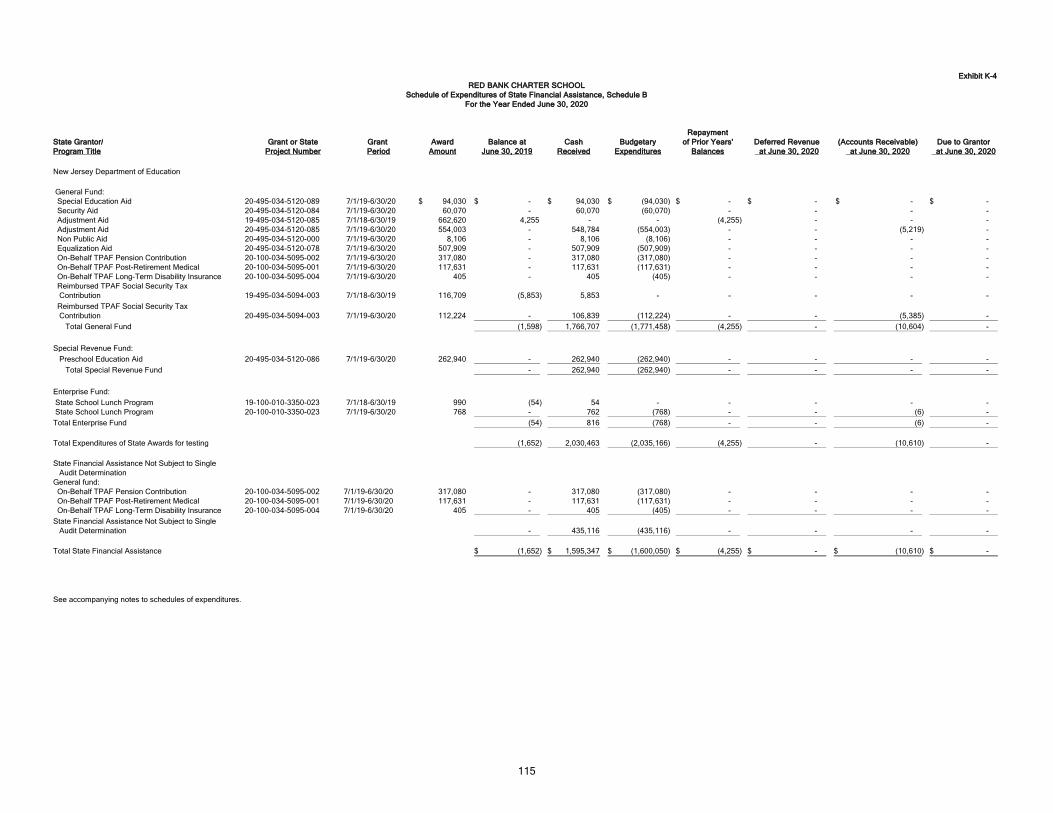

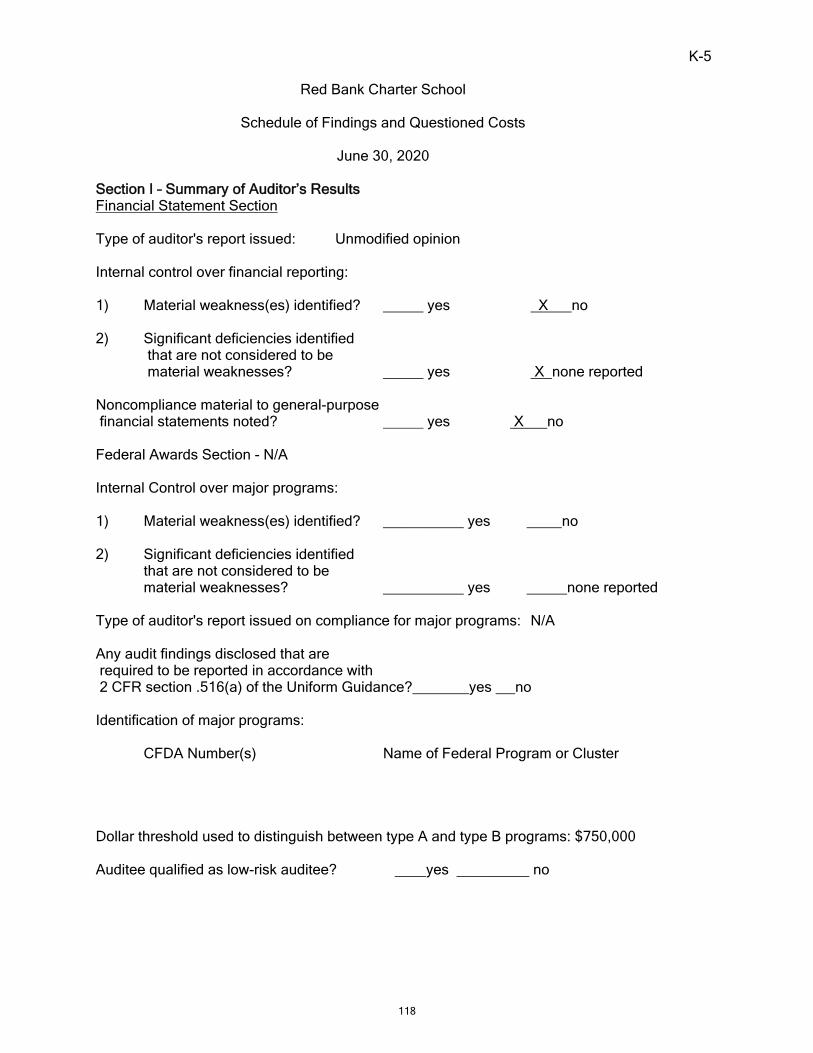

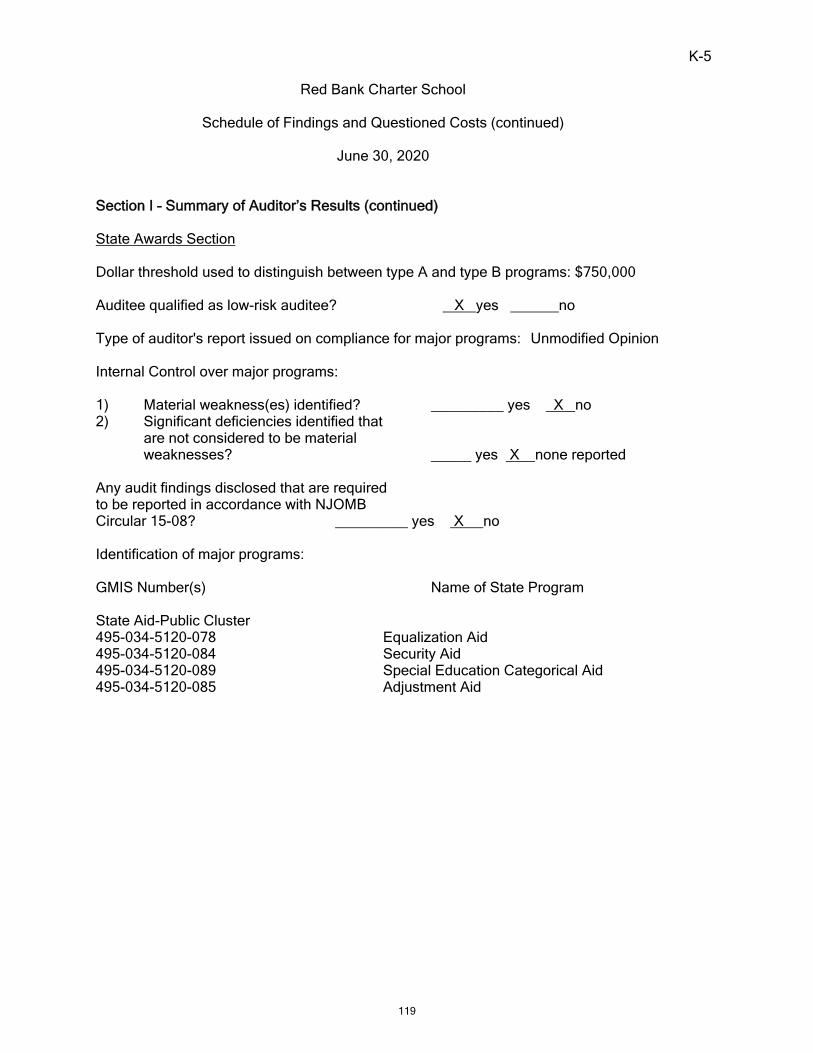

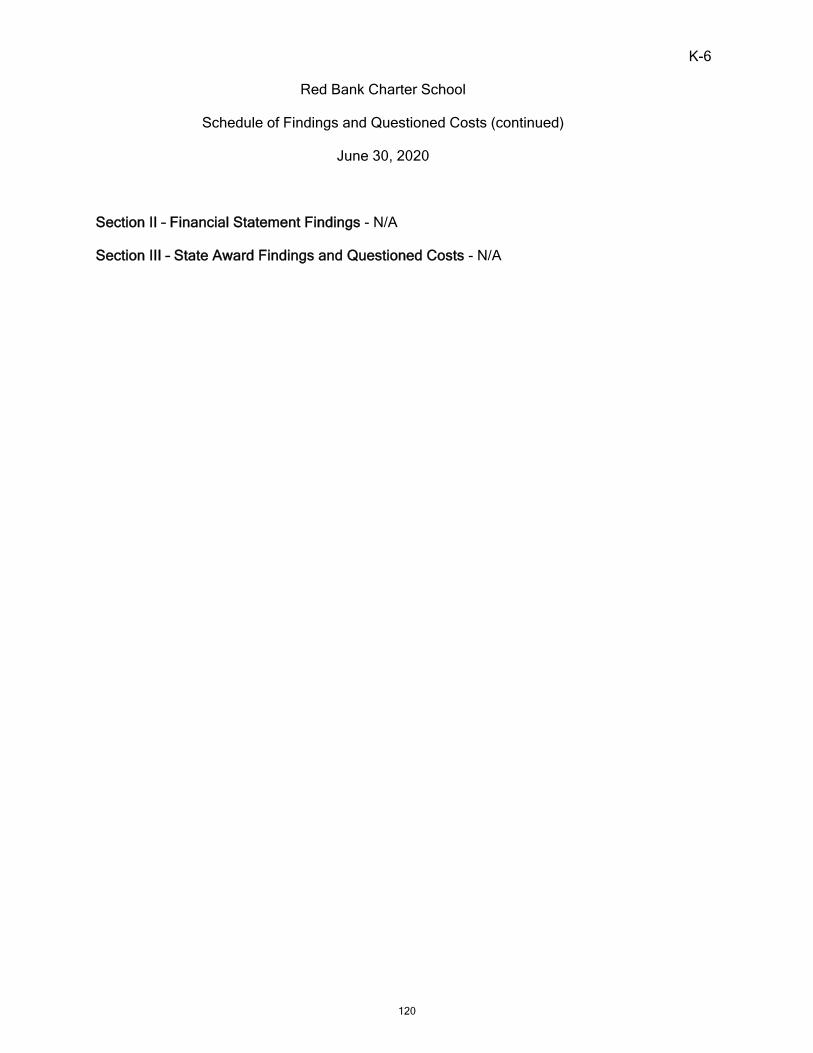

K-3 Schedule of Expenditures of Federal Awards, Schedule A 114K-4 Schedule of Expenditures of State Financial Assistance, Schedule B 115K-5 Notes to the Schedules of Awards and Financial Assistance 116-117K-6 Schedule of Findings and Questioned Costs 118-120

-Section I - Summary of Auditor's Results- Section II - Financial Statements Findings- Section III - Federal Awards and State Financial Assistance Findings

and Questioned CostsK-7 Summary Schedule of Prior Audit Findings 121

INTRODUCTORY SECTION

1

2

3

4

5

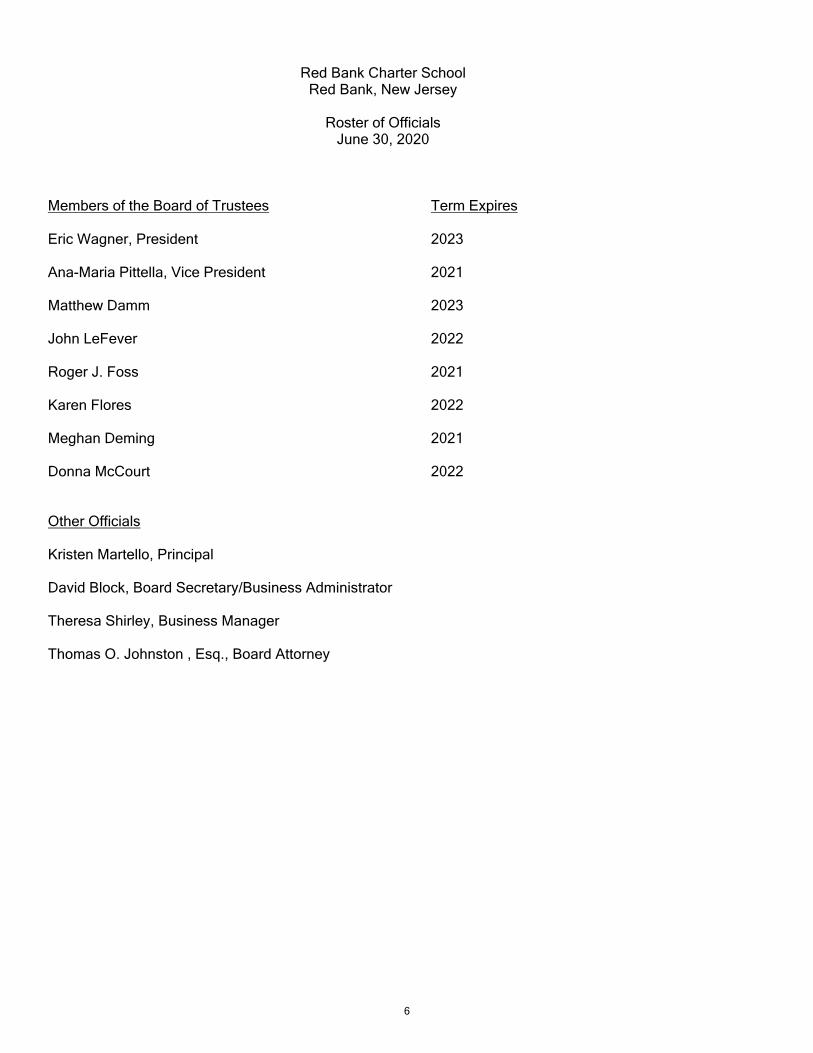

Red Bank Charter SchoolRed Bank, New Jersey

Roster of OfficialsJune 30, 2020

Members of the Board of Trustees Term Expires

Eric Wagner, President 2023

Ana-Maria Pittella, Vice President 2021

Matthew Damm 2023

John LeFever 2022

Roger J. Foss 2021

Karen Flores 2022

Meghan Deming 2021

Donna McCourt 2022

Other Officials

Kristen Martello, Principal

David Block, Board Secretary/Business Administrator

Theresa Shirley, Business Manager

Thomas O. Johnston , Esq., Board Attorney

6

Red Bank Charter SchoolConsultants and Advisors

Audit Firm

Kathryn Perry, CPAJump, Perry and Company, L.L.P.

12 Lexington AvenueToms River, New Jersey 08753

Attorney

Johnston Law Firm, LLC151 Forest Street, Suite A

Montclair, New Jersey 07042

Official Depositories

TD BankFront Street

Red Bank, New Jersey 07701

Bank of AmericaBroad Street

Red Bank, New Jersey 07701

7

FINANCIAL SECTION

8

INDEPENDENT AUDITOR'S REPORT

Honorable President and Members of the Board of TrusteesRed Bank Charter School:County of Monmouth Red Bank, New Jersey

Report of the Financial Statements

We have audited the accompanying financial statements of the governmental activities, thebusiness-type activities, each major fund, and the aggregate remaining fund information of RedBank Charter School ("Charter School") in the County of Monmouth, State of New Jersey, as ofand for the year ended June 30, 2020, and the related notes to the financial statements, whichcollectively comprise the Charter School’s basic financial statements as listed in the table ofcontents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financialstatements in accordance with accounting principles generally accepted in the United States ofAmerica; this includes the design, implementation, and maintenance of internal control relevantto the preparation and fair presentation of financial statements that are free from materialmisstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. Weconducted our audit in accordance with auditing standards generally accepted in the UnitedStates of America; the standards applicable to financial audits contained in Government AuditingStandards, issued by the Comptroller General of the United States; and in compliance with theaudit requirements as prescribed by the Office of School Finance, Department of Education,State of New Jersey. Those standards require that we plan and perform the audit to obtainreasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditor’sjudgment, including the assessment of the risks of material misstatement of the financialstatements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the Charter School’s preparation and fair presentation ofthe financial statements in order to design audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of theCharter School’s internal control. Accordingly, we express no such opinion. An audit alsoincludes evaluating the appropriateness of accounting policies used and the reasonableness ofsignificant accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinions.

9

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects,the respective financial position of the governmental activities, the business-type activities, eachmajor fund, and the aggregate remaining fund information of Red Bank Charter School in theCounty of Monmouth, State of New Jersey as of June 30, 2020 and the respective changes infinancial position and, where applicable, cash flows thereof for the year then ended inaccordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that themanagement’s discussion and analysis and budgetary comparison information, and theschedules related to accounting and reporting for pensions and post-retirement benefits, aslisted in the table of contents be presented to supplement the basic financial statements. Suchinformation, although not a part of the basic financial statements, is required by theGovernmental Accounting Standards Board, who considers it to be an essential part of financialreporting for placing the basic financial statements in an appropriate operational, economic, orhistorical context. We have applied certain limited procedures to the required supplementaryinformation in accordance with auditing standards generally accepted in the United States ofAmerica, which consisted of inquiries of management about the methods of preparing theinformation and comparing the information for consistency with management’s responses to ourinquiries, the basic financial statements, and other knowledge we obtained during our audit ofthe basic financial statements. We do not express an opinion or provide any assurance on theinformation because the limited procedures do not provide us with sufficient evidence to expressan opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise the Red Bank Charter School's basic financial statements. Theintroductory section, combining fund financial statements and schedules and statistical section,are presented for purposes of additional analysis and are not a required part of the basicfinancial statements. The schedule of expenditures of federal and state awards is presented forpurposes of additional analysis as required by Title 2 U.S. Code of Federal Regulations (CFR)Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements forFederal Awards, and New Jersey OMB’s Circular 15-08, Single Audit Policy for Recipients ofFederal Grants, State Grants and State Aid, and is also not a required part of the basic financialstatements.

10

The combining fund financial statements and schedules and the schedule of expenditures offederal and state awards are the responsibility of management and were derived from and relatedirectly to the underlying accounting and other records used to prepare the basic financialstatements. Such information has been subjected to the auditing procedures applied in the auditof the basic financial statements and certain additional procedures, including comparing andreconciling such information directly to the underlying accounting and other records used toprepare the basic financial statements or to the basic financial statements themselves, and otheradditional procedures in accordance with auditing standards generally accepted in the UnitedStates of America. In our opinion, the combining fund financial statements and schedules andthe schedule of expenditures of federal and state awards are fairly stated, in all materialrespects in relation to the basic financial statements as a whole.

The introductory and statistical sections have not been subjected to the auditing proceduresapplied in the audit of the basic financial statements and, accordingly, we do not express anopinion or provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report datedDecember 28, 2020 on our consideration of the Red Bank Charter School in the County ofMonmouth, State of New Jersey internal control over financial reporting and on our tests of itscompliance with certain provisions of laws, regulations, contracts, and grant agreements andother matters. The purpose of that report is to describe the scope of our testing of internalcontrol over financial reporting and compliance and the results of that testing, and not to providean opinion on internal control over financial reporting or on compliance. That report is anintegral part of an audit performed in accordance with Government Auditing Standards inconsidering Red Bank Charter School in the County of Monmouth, State of New Jersey internalcontrol over financial reporting and compliance.

Respectfully Submitted,

Jump, Perry and Company L.L.P.Toms River, New Jersey

Kathryn Perry, PartnerLicensed Public School AccountantNo. CS 20CS00226400

December 28, 2020

11

REQUIRED SUPPLEMENTARY INFORMATION - PART I

12

Red Bank Charter School

Management's Discussion and Analysis

For the Fiscal Year Ended June 30, 2020

Unaudited

The discussion and analysis of Red Bank Charter School's financial performance provides an overallreview of the Charter School's financial activities for the fiscal year ended June 30, 2020. The intent ofthis discussion and analysis is to look at the Charter School's financial performance as a whole; readersshould also review the notes to the basic financial statements and financial statements to enhance theirunderstanding of the Charter School's financial performance.

Financial Highlights

Key financial highlights for June 30, 2020 are as follows:

Net position totaled $676,015, which represents a 23.73 percent decrease from June 30, 2019.

General revenues accounted for $3,096,708 in revenue or 91.22 percent of all revenues. Programspecific revenues in the form of charges for services, operating grants and contributions, and capitalgrants and contributions accounted for $298,035 or 8.78 percent of total revenues of $3,394,743.

Total assets increased by $103,598 as current assets increased by $208,442 and capital assets, netdecreased by $(104,844).

The Charter School had $3,605,118 in expenses; only $298,035 of these expenses were offset byprogram specific charges for services, grants or contributions. General revenues (tuition charges andrelated state aid) of $3,096,708 were adequate to provide for these programs.

Among major funds, the General Fund had $2,935,302 in revenues and $2,719,340 in expenditures andtransfers. The General Fund's balance decreased $(215,962) over June 30, 2019. The General Fund'sbalance is $362,514.

Using this Comprehensive Annual Financial Report (CAFR)

The annual report consists of a series of financial statements and notes to those statements. Thesestatements are organized so the reader can understand Red Bank Charter School as a financial whole,an entire operating entity. The statements then proceed to provide an increasingly detailed look atspecific financial activities.

The Statement of Net Position and Statement of Activities provide information about the activities of theSchool Board, presenting both an aggregate view of the Charter School's finances and longer-term viewof those finances. Fund financial statements provide the next level of detail. For government funds,these statements tell how services were financed in the short term as well as what remains for futurespending. The fund financial statements also look at the Charter School's most significant funds with allother non-major funds presented in total in one column. In the case of Red Bank Charter School, theGeneral Fund is by far the most significant.

13

Reporting the School Board as a Whole

Statement of Net Position and the Statement of Activities

The Statement of Net Position and Statement of Activities provide information about the activities of theCharter School and are designed to provide readers with a broad overview of the Charter School'sfinances, in a manner similar to private-sector business.

These statements include all assets, deferred outflows of resources, liabilities, and deferred inflows ofresources using the accrual basis of accounting similar to the accounting used by most private-sectorbusinesses. This basis of accounting takes into consideration all of the current year's revenues andexpenses regardless of when cash is received or paid.

These two statements report the Charter School's net position and changes in net position. The changein net position is important because it informs the reader that the financial position of the Charter Schoolhas improved or worsened. The causes of the change may be the result of many factors, some financialand some not. Non-financial factors include, but are not limited to, the Charter School's property taxbase, current laws in New Jersey restricting revenue growth, facility conditions, and required educationalprograms. In the Statement of Net Position and the Statement of Activities, the Charter School is dividedinto two kinds of activities:

Governmental Activities - All of the Charter School's programs and services are reported here including,instruction, support services, operation and maintenance of plant facilities, pupil transportation andextracurricular activities.

Business-Type Activities - This service is provided on a charge for goods or services basis to recover allthe expense of the goods or services provided. The Food Service Funds are reported as a businessactivity.

Reporting the Charter School's Most Significant Funds

Fund Financial Statement

The analysis of the Charter School's major funds begins with Exhibit B-1. Fund financial reports providedetailed information about the Charter School's major funds. The Charter School's major governmentalfunds are the General Fund and Special Revenue Fund.

Governmental Funds

The Charter School's activities are reported in governmental funds, which focus on how money flows intoand out of the funds and balances left at year-end available for spending in the future years. These fundsare reported using a modified accrual accounting method which measures cash and all other financialassets that can readily be converted to cash. The governmental fund statements provide a detailed short-term view of the Charter School's general government operations and the basic services it provides.Governmental fund information helps determine whether there are more or fewer financial resources thatcan be spent in the near future to finance educational programs. The relationship between governmentalactivities (reported in the Statement of Net Position and the Statement of Activities) and governmentalfunds is reconciled in the financial statements.

Enterprise Fund

The Enterprise Fund uses the same basis of accounting as business-type activities.

14

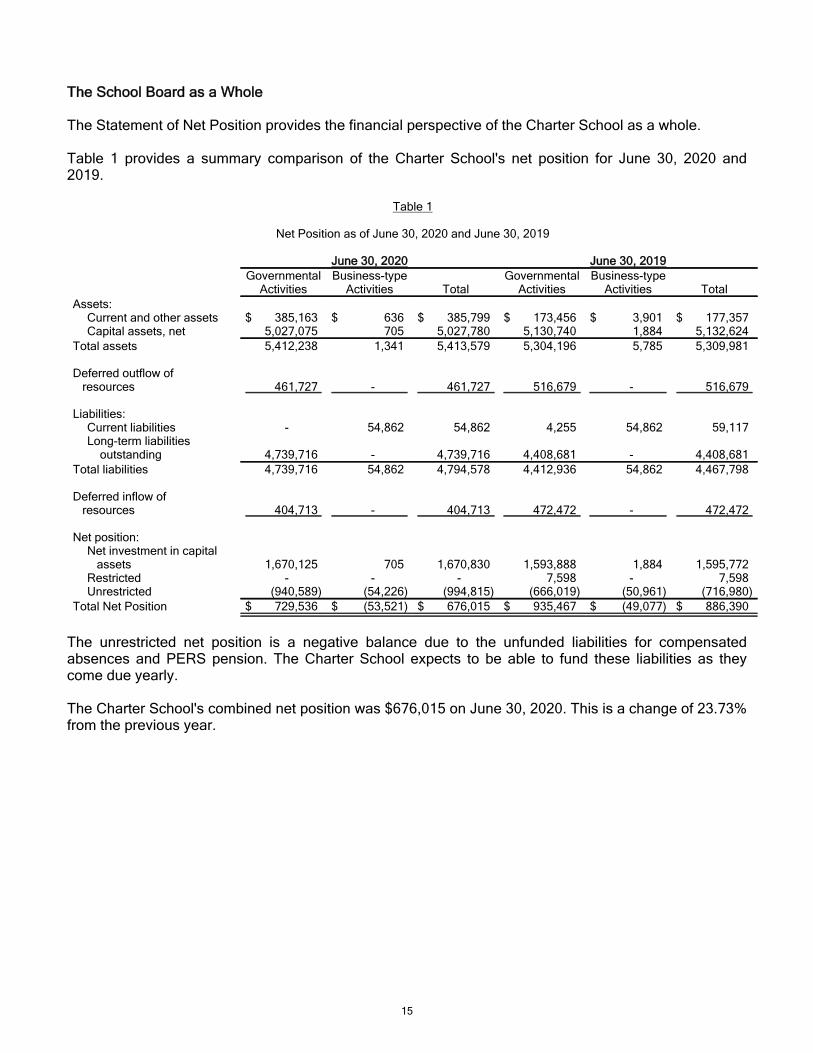

The School Board as a Whole

The Statement of Net Position provides the financial perspective of the Charter School as a whole.

Table 1 provides a summary comparison of the Charter School's net position for June 30, 2020 and2019.

Table 1

Net Position as of June 30, 2020 and June 30, 2019

June 30, 2020 June 30, 2019Governmental

ActivitiesBusiness-type

Activities TotalGovernmental

ActivitiesBusiness-type

Activities TotalAssets:

Current and other assets $ 385,163 $ 636 $ 385,799 $ 173,456 $ 3,901 $ 177,357Capital assets, net 5,027,075 705 5,027,780 5,130,740 1,884 5,132,624

Total assets 5,412,238 1,341 5,413,579 5,304,196 5,785 5,309,981

Deferred outflow of resources 461,727 - 461,727 516,679 - 516,679

Liabilities:Current liabilities - 54,862 54,862 4,255 54,862 59,117Long-term liabilities outstanding 4,739,716 - 4,739,716 4,408,681 - 4,408,681

Total liabilities 4,739,716 54,862 4,794,578 4,412,936 54,862 4,467,798

Deferred inflow of resources 404,713 - 404,713 472,472 - 472,472

Net position:Net investment in capital assets 1,670,125 705 1,670,830 1,593,888 1,884 1,595,772Restricted - - - 7,598 - 7,598Unrestricted (940,589) (54,226) (994,815) (666,019) (50,961) (716,980)

Total Net Position $ 729,536 $ (53,521) $ 676,015 $ 935,467 $ (49,077) $ 886,390

The unrestricted net position is a negative balance due to the unfunded liabilities for compensatedabsences and PERS pension. The Charter School expects to be able to fund these liabilities as theycome due yearly.

The Charter School's combined net position was $676,015 on June 30, 2020. This is a change of 23.73%from the previous year.

15

Table 2 provides a comparison analysis of Charter School's changes in net position from fiscal yearsJune 30, 2020 and 2019.

Table 2

Changes in Net Position

June 30, 2020 June 30, 2019Governmental

ActivitiesBusiness-type

Activities TotalGovernmental

ActivitiesBusiness-type

Activities TotalRevenuesProgram revenues:

Charges for services $ - $ 18,346 $ 18,346 $ - $ 14,672 $ 14,672Operating and capital grants and contributions 230,260 49,429 279,689 251,133 64,639 315,772

General revenues:Tuition 1,347,257 - 1,347,257 1,481,786 - 1,481,786Federal and state aid 1,615,784 - 1,615,784 1,672,726 - 1,672,726Investment earnings - - - - - -Miscellaneous 133,667 - 133,667 150,345 - 150,345

Total revenues 3,326,968 67,775 3,394,743 3,555,990 79,311 3,635,301

ExpensesInstructional services 1,558,098 - 1,558,098 1,618,457 - 1,618,457Support services 1,799,534 85,616 1,885,150 1,777,194 105,936 1,883,130Interest on long-term liabilities 161,870 - 161,870 155,205 - 155,205

Total expenses 3,519,502 85,616 3,605,118 3,550,856 105,936 3,656,792

Change in net position (192,534) (17,841) (210,375) 5,134 (26,625) (21,491)

Transfer (13,397) 13,397 - (23,195) 23,195 -

Net position - beginning 935,467 (49,077) 886,390 953,528 (45,647) 907,881Net position (deficit) - ending $ 729,536 $ (53,521) $ 676,015 $ 935,467 $ (49,077) $ 886,390

Government Activities

The tuition portion paid by the sending district is made up 40.50% of revenues for governmental activitiesfor the fiscal year 2020. The Charter School's total revenues were $3,326,968 for the year endedJune 30, 2020. Federal, state and local grants accounted for another 59.50%.

The total cost of all programs and services was $3,519,502. Instruction and instruction direct supportcomprises 58.88% of the Charter School's expenses.

16

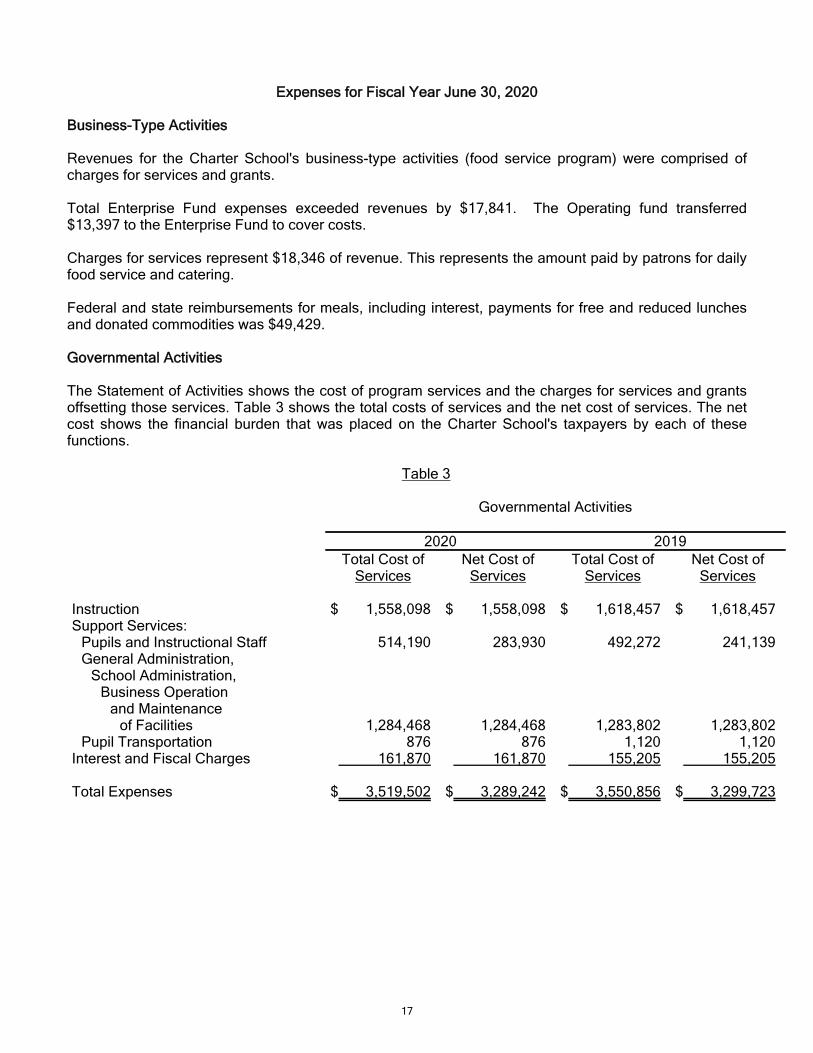

Expenses for Fiscal Year June 30, 2020

Business-Type Activities

Revenues for the Charter School's business-type activities (food service program) were comprised ofcharges for services and grants.

Total Enterprise Fund expenses exceeded revenues by $17,841. The Operating fund transferred$13,397 to the Enterprise Fund to cover costs.

Charges for services represent $18,346 of revenue. This represents the amount paid by patrons for dailyfood service and catering.

Federal and state reimbursements for meals, including interest, payments for free and reduced lunchesand donated commodities was $49,429.

Governmental Activities

The Statement of Activities shows the cost of program services and the charges for services and grantsoffsetting those services. Table 3 shows the total costs of services and the net cost of services. The netcost shows the financial burden that was placed on the Charter School's taxpayers by each of thesefunctions.

Table 3

Governmental Activities

2020 2019Total Cost of

ServicesNet Cost of

ServicesTotal Cost of

ServicesNet Cost of

Services

Instruction $ 1,558,098 $ 1,558,098 $ 1,618,457 $ 1,618,457Support Services:

Pupils and Instructional Staff 514,190 283,930 492,272 241,139General Administration,

School Administration,Business Operation

and Maintenanceof Facilities 1,284,468 1,284,468 1,283,802 1,283,802

Pupil Transportation 876 876 1,120 1,120Interest and Fiscal Charges 161,870 161,870 155,205 155,205

Total Expenses $ 3,519,502 $ 3,289,242 $ 3,550,856 $ 3,299,723

17

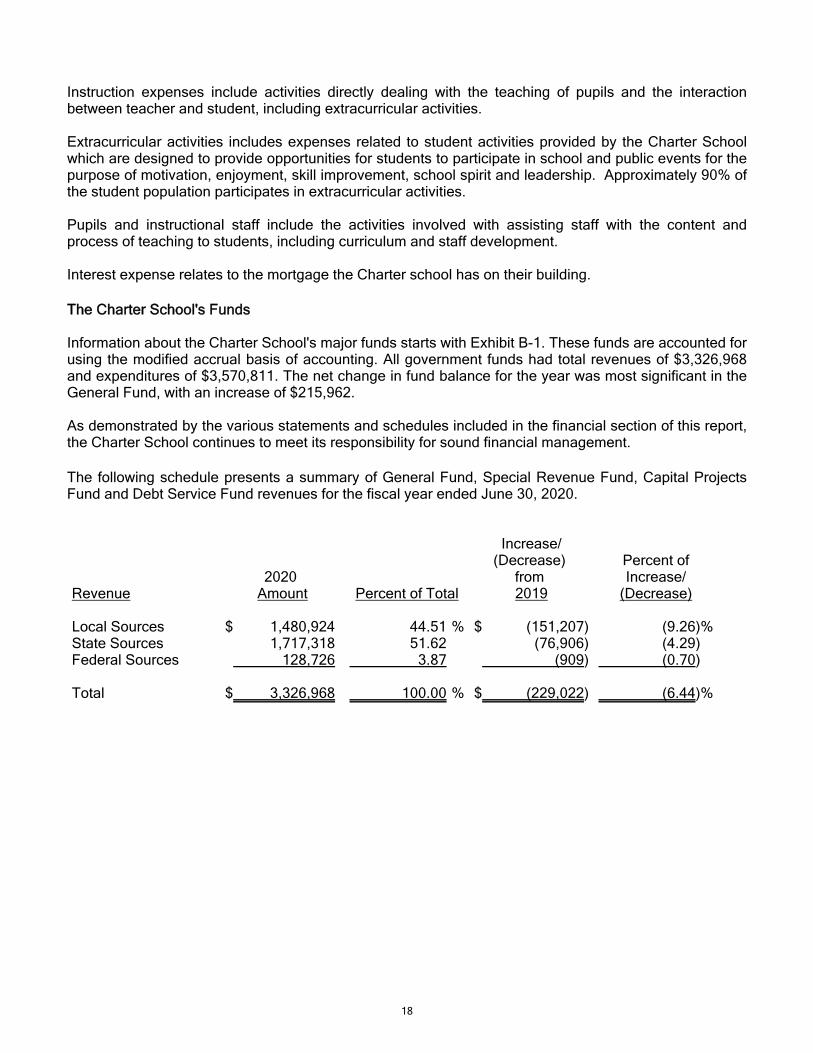

Instruction expenses include activities directly dealing with the teaching of pupils and the interactionbetween teacher and student, including extracurricular activities.

Extracurricular activities includes expenses related to student activities provided by the Charter Schoolwhich are designed to provide opportunities for students to participate in school and public events for thepurpose of motivation, enjoyment, skill improvement, school spirit and leadership. Approximately 90% ofthe student population participates in extracurricular activities.

Pupils and instructional staff include the activities involved with assisting staff with the content andprocess of teaching to students, including curriculum and staff development.

Interest expense relates to the mortgage the Charter school has on their building.

The Charter School's Funds

Information about the Charter School's major funds starts with Exhibit B-1. These funds are accounted forusing the modified accrual basis of accounting. All government funds had total revenues of $3,326,968and expenditures of $3,570,811. The net change in fund balance for the year was most significant in theGeneral Fund, with an increase of $215,962.

As demonstrated by the various statements and schedules included in the financial section of this report,the Charter School continues to meet its responsibility for sound financial management.

The following schedule presents a summary of General Fund, Special Revenue Fund, Capital ProjectsFund and Debt Service Fund revenues for the fiscal year ended June 30, 2020.

Revenue2020

Amount Percent of Total

Increase/(Decrease)

from 2019

Percent ofIncrease/

(Decrease)

Local Sources $ 1,480,924 %44.51 $ (151,207) %(9.26)State Sources 1,717,318 51.62 (76,906) (4.29)Federal Sources 128,726 3.87 (909) (0.70)

Total $ 3,326,968 %100.00 $ (229,022) %(6.44)

18

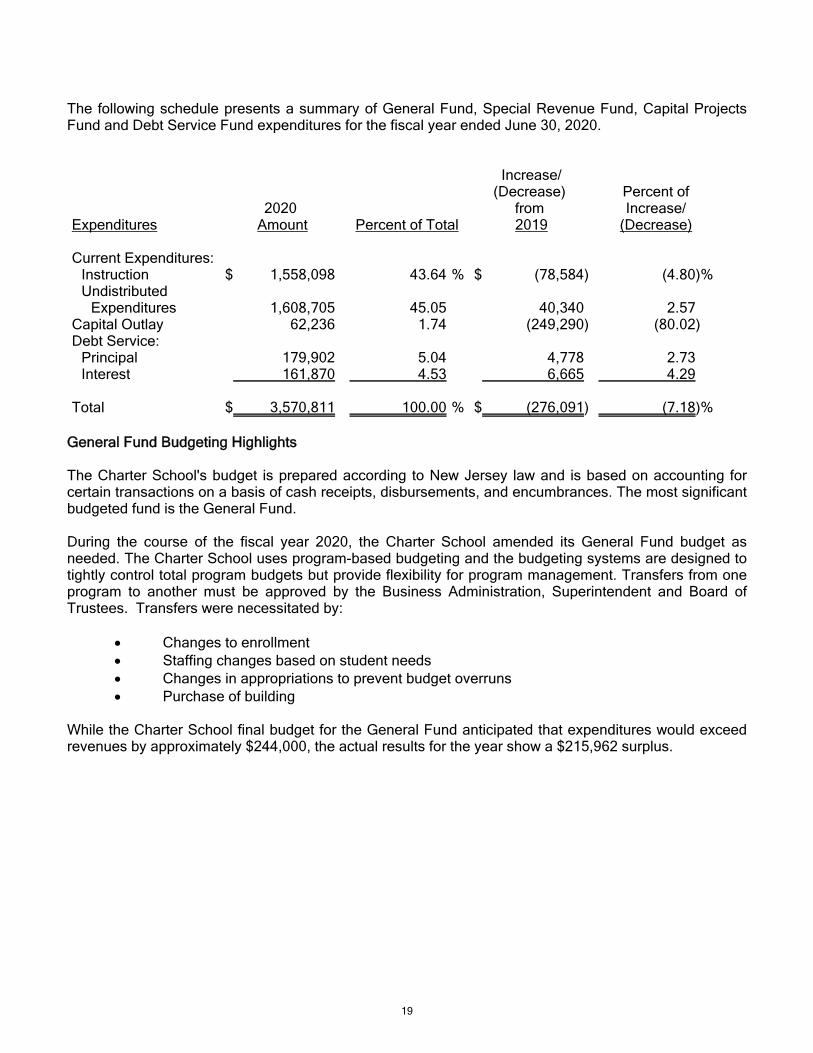

The following schedule presents a summary of General Fund, Special Revenue Fund, Capital ProjectsFund and Debt Service Fund expenditures for the fiscal year ended June 30, 2020.

Expenditures2020

Amount Percent of Total

Increase/(Decrease)

from 2019

Percent ofIncrease/

(Decrease)

Current Expenditures:Instruction $ 1,558,098 %43.64 $ (78,584) %(4.80)Undistributed

Expenditures 1,608,705 45.05 40,340 2.57Capital Outlay 62,236 1.74 (249,290) (80.02)Debt Service:

Principal 179,902 5.04 4,778 2.73Interest 161,870 4.53 6,665 4.29

Total $ 3,570,811 %100.00 $ (276,091) %(7.18)

General Fund Budgeting Highlights

The Charter School's budget is prepared according to New Jersey law and is based on accounting forcertain transactions on a basis of cash receipts, disbursements, and encumbrances. The most significantbudgeted fund is the General Fund.

During the course of the fiscal year 2020, the Charter School amended its General Fund budget asneeded. The Charter School uses program-based budgeting and the budgeting systems are designed totightly control total program budgets but provide flexibility for program management. Transfers from oneprogram to another must be approved by the Business Administration, Superintendent and Board ofTrustees. Transfers were necessitated by:

Changes to enrollment Staffing changes based on student needs Changes in appropriations to prevent budget overruns Purchase of building

While the Charter School final budget for the General Fund anticipated that expenditures would exceedrevenues by approximately $244,000, the actual results for the year show a $215,962 surplus.

19

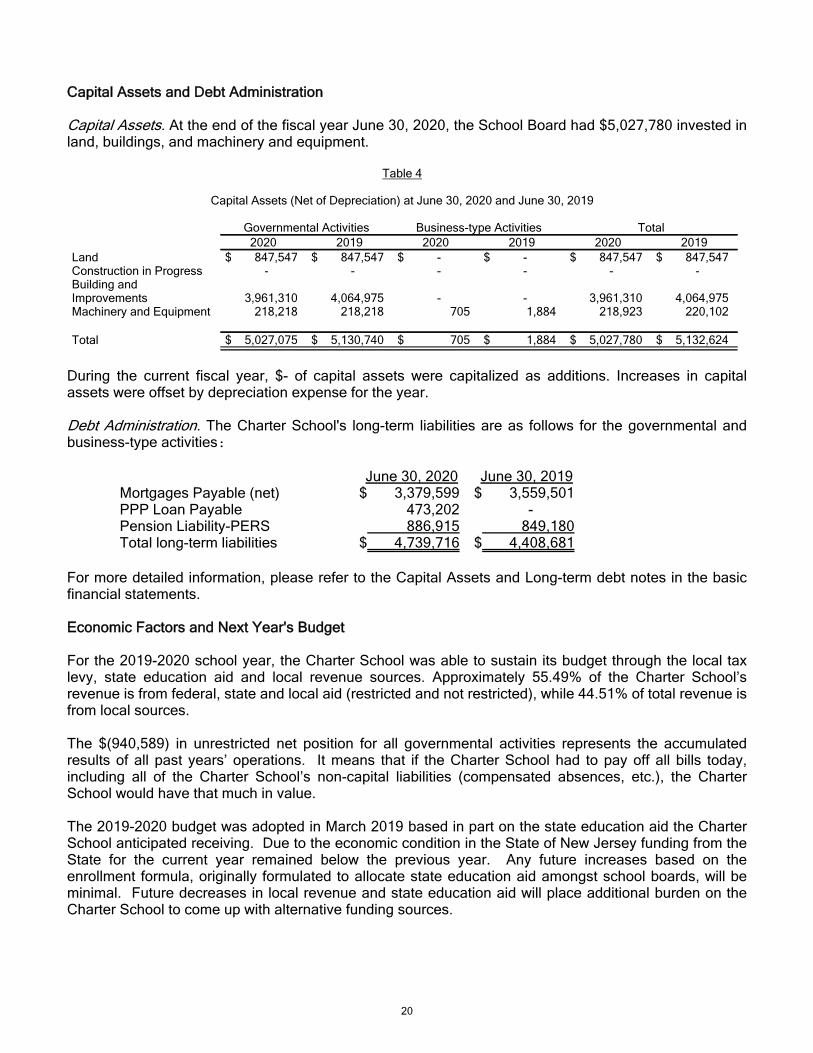

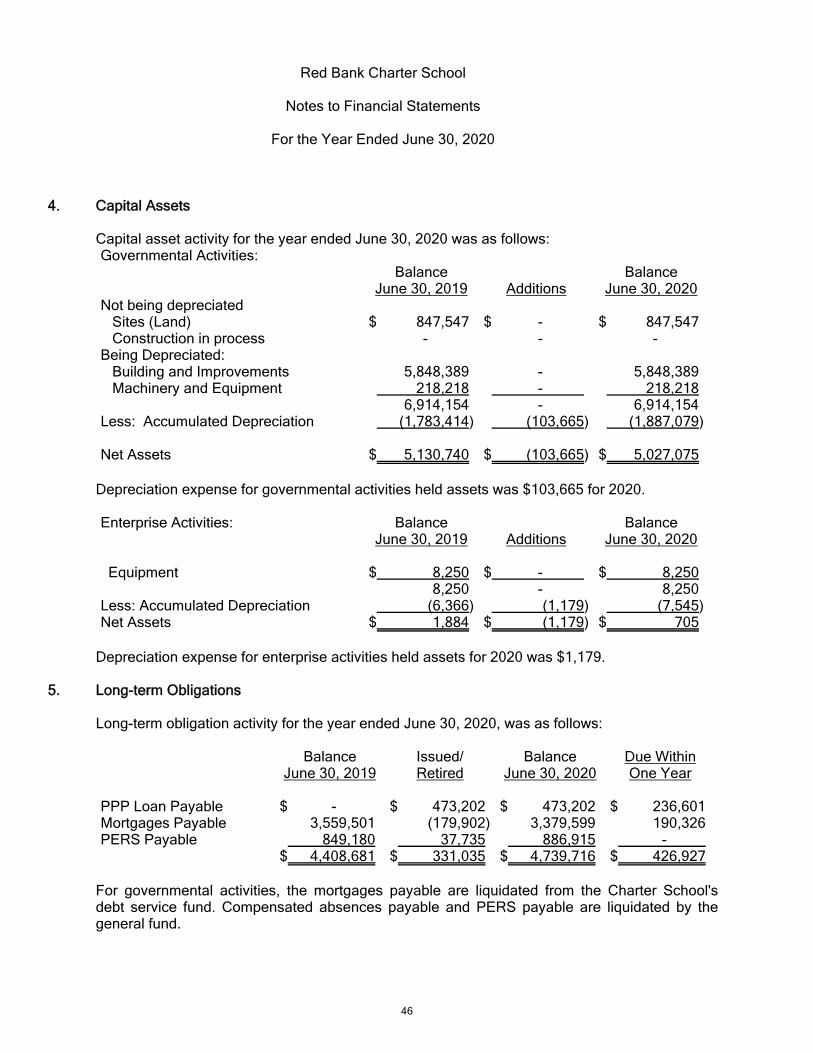

Capital Assets and Debt Administration

Capital Assets. At the end of the fiscal year June 30, 2020, the School Board had $5,027,780 invested inland, buildings, and machinery and equipment.

Table 4

Capital Assets (Net of Depreciation) at June 30, 2020 and June 30, 2019

Governmental Activities Business-type Activities Total2020 2019 2020 2019 2020 2019

Land $ 847,547 $ 847,547 $ - $ - $ 847,547 $ 847,547Construction in Progress - - - - - -Building andImprovements 3,961,310 4,064,975 - - 3,961,310 4,064,975Machinery and Equipment 218,218 218,218 705 1,884 218,923 220,102

Total $ 5,027,075 $ 5,130,740 $ 705 $ 1,884 $ 5,027,780 $ 5,132,624

During the current fiscal year, $- of capital assets were capitalized as additions. Increases in capitalassets were offset by depreciation expense for the year.

Debt Administration. The Charter School's long-term liabilities are as follows for the governmental andbusiness-type activities:

June 30, 2020 June 30, 2019Mortgages Payable (net) $ 3,379,599 $ 3,559,501PPP Loan Payable 473,202 -Pension Liability-PERS 886,915 849,180Total long-term liabilities $ 4,739,716 $ 4,408,681

For more detailed information, please refer to the Capital Assets and Long-term debt notes in the basicfinancial statements.

Economic Factors and Next Year's Budget

For the 2019-2020 school year, the Charter School was able to sustain its budget through the local taxlevy, state education aid and local revenue sources. Approximately 55.49% of the Charter School’srevenue is from federal, state and local aid (restricted and not restricted), while 44.51% of total revenue isfrom local sources.

The $(940,589) in unrestricted net position for all governmental activities represents the accumulatedresults of all past years’ operations. It means that if the Charter School had to pay off all bills today,including all of the Charter School’s non-capital liabilities (compensated absences, etc.), the CharterSchool would have that much in value.

The 2019-2020 budget was adopted in March 2019 based in part on the state education aid the CharterSchool anticipated receiving. Due to the economic condition in the State of New Jersey funding from theState for the current year remained below the previous year. Any future increases based on theenrollment formula, originally formulated to allocate state education aid amongst school boards, will beminimal. Future decreases in local revenue and state education aid will place additional burden on theCharter School to come up with alternative funding sources.

20

The Charter School anticipates a slight increase in enrollment for the 2020-2021 fiscal year. If theCharter School were to experience a significant increase in enrollment with no appreciable increase instate aid for future budgets, the Charter School will be faced with the following alternatives: (a) reduceprograms and services, (b) increase local tax levy or (c) seek alternative sources of funding.

Contacting the School Board's Financial Management

This financial report is designed to provide our citizens, taxpayers, investors and creditors with a generaloverview of the Charter School's finances and to show the School Board's accountability for the money itreceives. If you have questions about this report or need additional information, you may contact theSchool Business Administrator/Board Secretary at Red Bank Charter School, 58 Oakland Street, RedBank, NJ, 07701.

21

BASIC FINANCIAL STATEMENTS

22

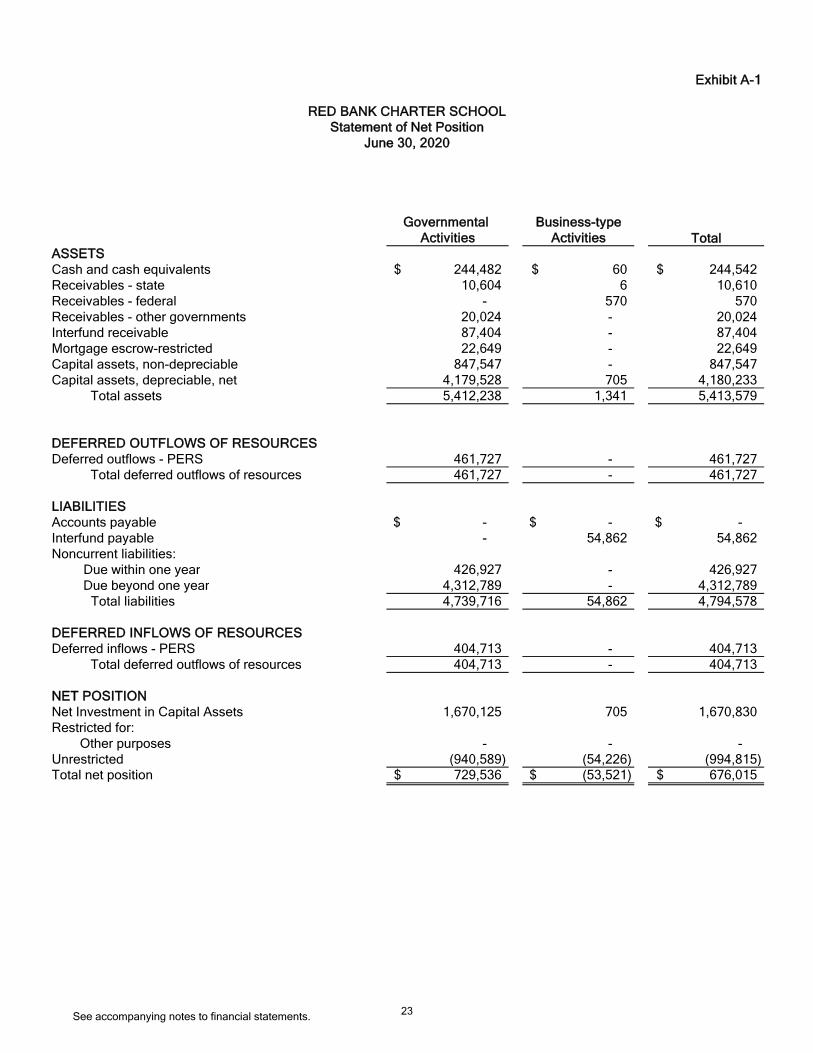

Exhibit A-1

Governmental Business-typeActivities Activities Total

ASSETSCash and cash equivalents 244,482$ 60$ 244,542$ Receivables - state 10,604 6 10,610 Receivables - federal - 570 570 Receivables - other governments 20,024 - 20,024 Interfund receivable 87,404 - 87,404 Mortgage escrow-restricted 22,649 - 22,649 Capital assets, non-depreciable 847,547 - 847,547 Capital assets, depreciable, net 4,179,528 705 4,180,233 Total assets 5,412,238 1,341 5,413,579

DEFERRED OUTFLOWS OF RESOURCESDeferred outflows - PERS 461,727 - 461,727 Total deferred outflows of resources 461,727 - 461,727

LIABILITIESAccounts payable -$ -$ -$ Interfund payable - 54,862 54,862 Noncurrent liabilities: Due within one year 426,927 - 426,927 Due beyond one year 4,312,789 - 4,312,789 Total liabilities 4,739,716 54,862 4,794,578

DEFERRED INFLOWS OF RESOURCESDeferred inflows - PERS 404,713 - 404,713 Total deferred outflows of resources 404,713 - 404,713

NET POSITIONNet Investment in Capital Assets 1,670,125 705 1,670,830 Restricted for: Other purposes - - - Unrestricted (940,589) (54,226) (994,815) Total net position 729,536$ (53,521)$ 676,015$

RED BANK CHARTER SCHOOLStatement of Net Position

June 30, 2020

See accompanying notes to financial statements.23

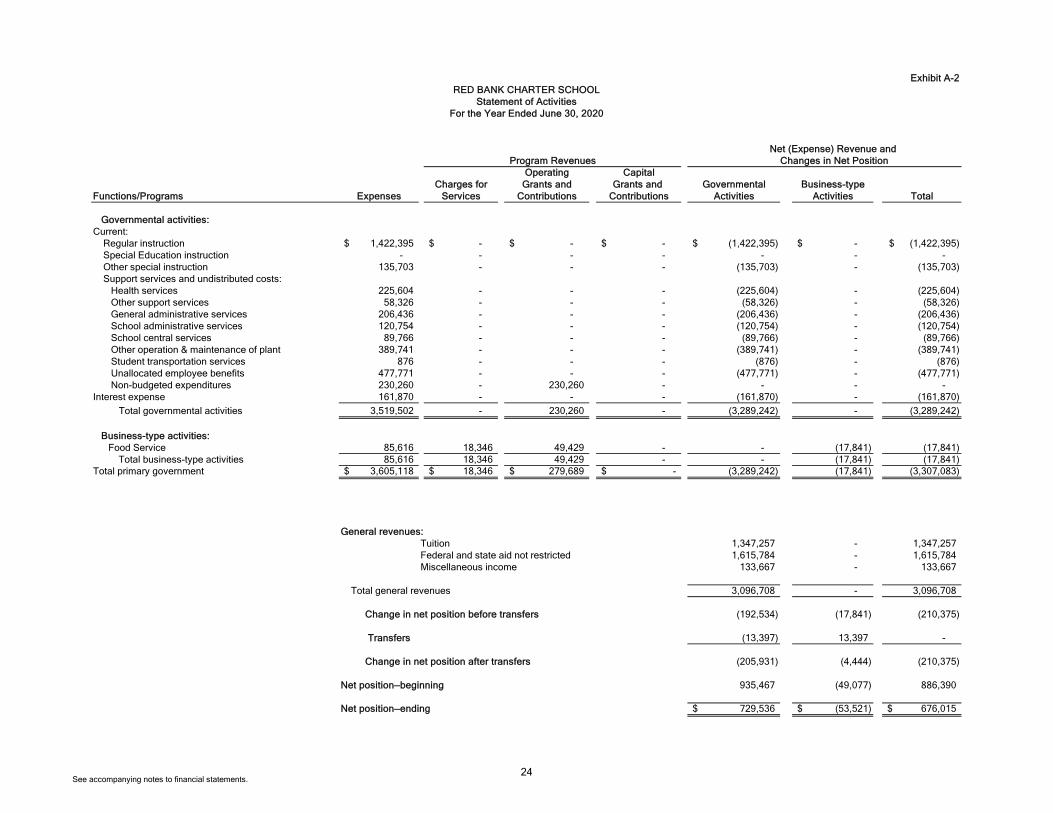

Exhibit A-2

Net (Expense) Revenue andProgram Revenues Changes in Net Position

Operating CapitalCharges for Grants and Grants and Governmental Business-type

Functions/Programs Expenses Services Contributions Contributions Activities Activities Total

Governmental activities:Current: Regular instruction 1,422,395$ -$ -$ -$ (1,422,395)$ -$ (1,422,395)$ Special Education instruction - - - - - - - Other special instruction 135,703 - - - (135,703) - (135,703) Support services and undistributed costs: Health services 225,604 - - - (225,604) - (225,604) Other support services 58,326 - - - (58,326) - (58,326) General administrative services 206,436 - - - (206,436) - (206,436) School administrative services 120,754 - - - (120,754) - (120,754) School central services 89,766 - - - (89,766) - (89,766) Other operation & maintenance of plant 389,741 - - - (389,741) - (389,741) Student transportation services 876 - - - (876) - (876) Unallocated employee benefits 477,771 - - - (477,771) - (477,771) Non-budgeted expenditures 230,260 - 230,260 - - - - Interest expense 161,870 - - - (161,870) - (161,870) Total governmental activities 3,519,502 - 230,260 - (3,289,242) - (3,289,242)

Business-type activities: Food Service 85,616 18,346 49,429 - - (17,841) (17,841) Total business-type activities 85,616 18,346 49,429 - - (17,841) (17,841) Total primary government 3,605,118$ 18,346$ 279,689$ -$ (3,289,242) (17,841) (3,307,083)

General revenues:Tuition 1,347,257 - 1,347,257Federal and state aid not restricted 1,615,784 - 1,615,784 Miscellaneous income 133,667 - 133,667

Total general revenues 3,096,708 - 3,096,708

Change in net position before transfers (192,534) (17,841) (210,375)

Transfers (13,397) 13,397 -

Change in net position after transfers (205,931) (4,444) (210,375)

Net position—beginning 935,467 (49,077) 886,390

Net position—ending 729,536$ (53,521)$ 676,015$

RED BANK CHARTER SCHOOL

For the Year Ended June 30, 2020Statement of Activities

See accompanying notes to financial statements.24

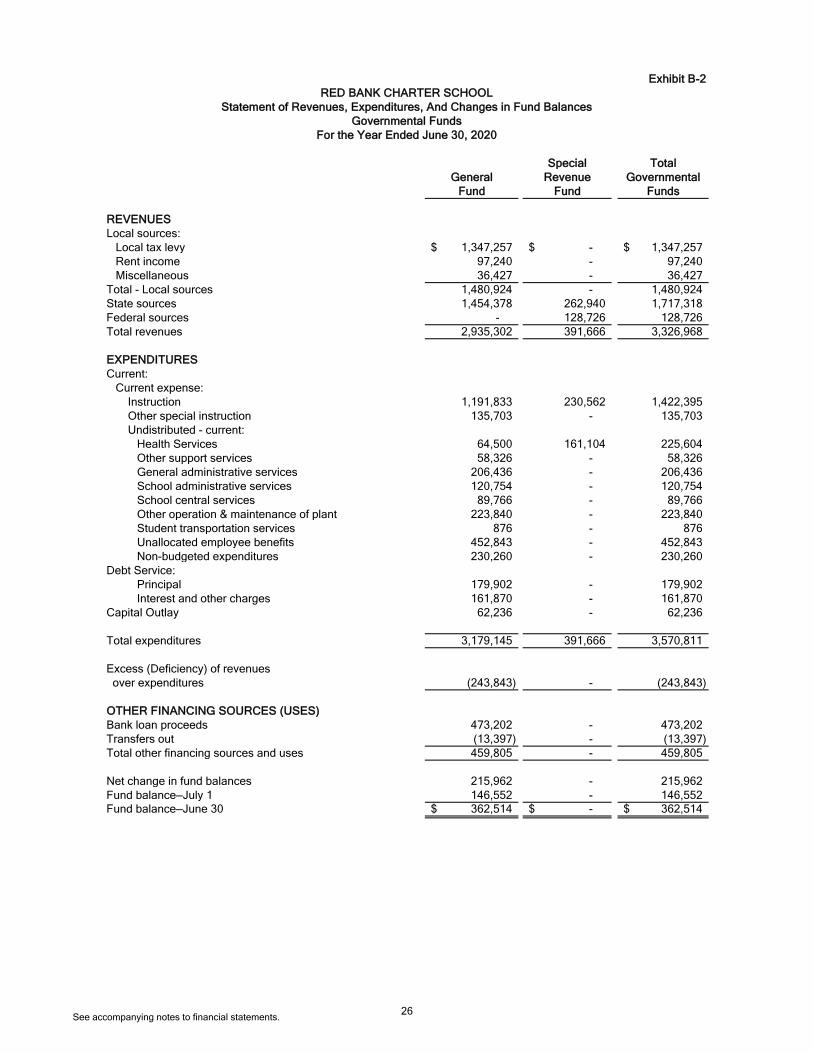

Exhibit B-1

Special TotalGeneral Revenue Governmental

Fund Fund Funds

ASSETS Cash and cash equivalents 249,599$ (5,117)$ 244,482$ Receivables from other governments 14,907 5,117 20,024 Receivables from other funds 87,404 - 87,404 Receivables from state 10,604 - 10,604 Total assets 362,514 - 362,514

LIABILITIES AND FUND BALANCES Liabilities: Payable to other governments - - - Total liabilities - - -

Fund Balances: Assigned to: Other purposes - - - Unassigned to: General fund 362,514 - 362,514 Total fund balances 362,514 - 362,514 Total liabilities and fund balances 362,514$ -$

Amounts reported for governmental activities in the statement of net position (A-1) are different because:

Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds. The cost of the assets is $6,914,154 and the accumulated depreciation is $1,887,079. 5,027,075

Funds held in escrow for the purchase of the building that is not reported inthis fund financial statement, but is presented in the statement of net position. 22,649

Deferred outflows related to the PERS pension plan 461,727

Deferred inflows related to the PERS pension plan (404,713)

Long-term liabilities, including mortgage payable, are not due and payable in the current period and therefore are not reported as liabilities in the funds:

Pension liability - PERS (886,915) Paycheck Protection Program Loan (473,202) Mortgages Payable (3,379,599) (4,739,716)

Net position of governmental activities 729,536$

RED BANK CHARTER SCHOOLBalance Sheet

Governmental FundsJune 30, 2020

See accompanying notes to financial statements.25

Exhibit B-2

Special TotalGeneral Revenue Governmental

Fund Fund Funds

REVENUESLocal sources: Local tax levy 1,347,257$ -$ 1,347,257$ Rent income 97,240 - 97,240 Miscellaneous 36,427 - 36,427 Total - Local sources 1,480,924 - 1,480,924 State sources 1,454,378 262,940 1,717,318 Federal sources - 128,726 128,726 Total revenues 2,935,302 391,666 3,326,968

EXPENDITURESCurrent: Current expense: Instruction 1,191,833 230,562 1,422,395 Other special instruction 135,703 - 135,703 Undistributed - current: Health Services 64,500 161,104 225,604 Other support services 58,326 - 58,326 General administrative services 206,436 - 206,436 School administrative services 120,754 - 120,754 School central services 89,766 - 89,766 Other operation & maintenance of plant 223,840 - 223,840 Student transportation services 876 - 876 Unallocated employee benefits 452,843 - 452,843 Non-budgeted expenditures 230,260 - 230,260 Debt Service: Principal 179,902 - 179,902 Interest and other charges 161,870 - 161,870 Capital Outlay 62,236 - 62,236

Total expenditures 3,179,145 391,666 3,570,811

Excess (Deficiency) of revenues over expenditures (243,843) - (243,843)

OTHER FINANCING SOURCES (USES)Bank loan proceeds 473,202 - 473,202 Transfers out (13,397) - (13,397) Total other financing sources and uses 459,805 - 459,805

Net change in fund balances 215,962 - 215,962 Fund balance—July 1 146,552 - 146,552 Fund balance—June 30 362,514$ -$ 362,514$

RED BANK CHARTER SCHOOLStatement of Revenues, Expenditures, And Changes in Fund Balances

Governmental FundsFor the Year Ended June 30, 2020

See accompanying notes to financial statements.26

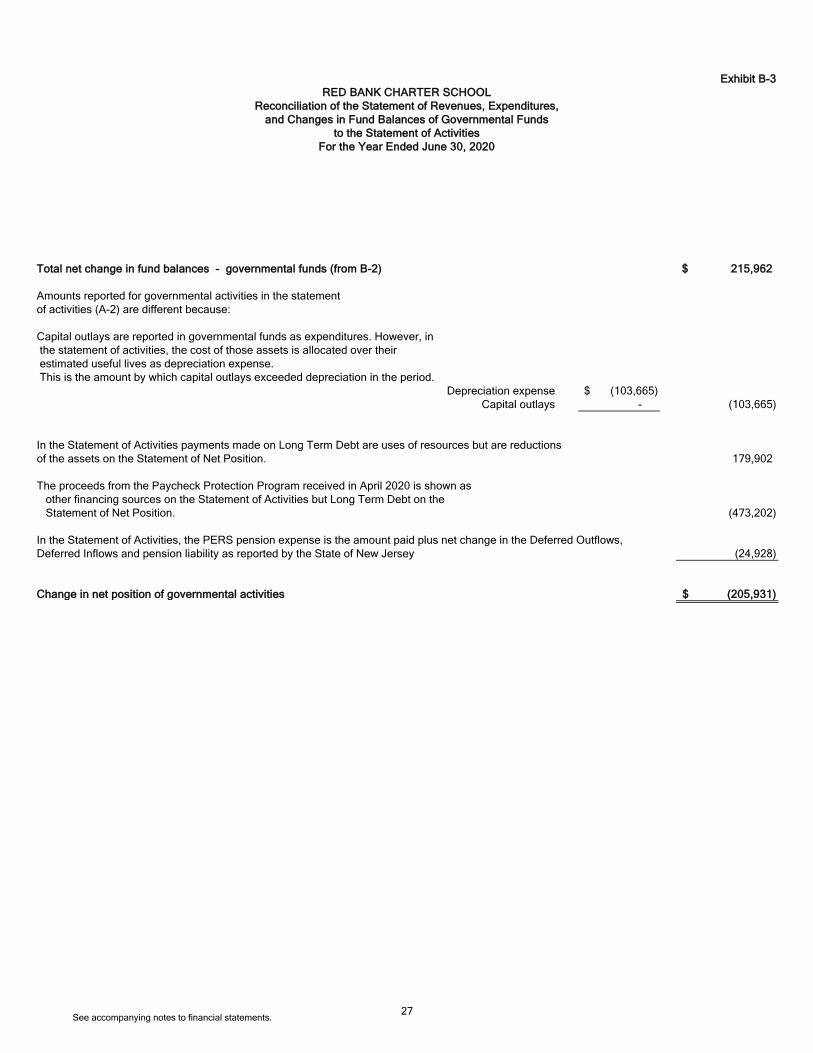

Exhibit B-3

Total net change in fund balances - governmental funds (from B-2) 215,962$

Amounts reported for governmental activities in the statementof activities (A-2) are different because:

Capital outlays are reported in governmental funds as expenditures. However, in the statement of activities, the cost of those assets is allocated over their estimated useful lives as depreciation expense. This is the amount by which capital outlays exceeded depreciation in the period.

Depreciation expense (103,665)$ Capital outlays - (103,665)

In the Statement of Activities payments made on Long Term Debt are uses of resources but are reductions of the assets on the Statement of Net Position. 179,902

The proceeds from the Paycheck Protection Program received in April 2020 is shown as other financing sources on the Statement of Activities but Long Term Debt on the Statement of Net Position. (473,202)

In the Statement of Activities, the PERS pension expense is the amount paid plus net change in the Deferred Outflows, Deferred Inflows and pension liability as reported by the State of New Jersey (24,928)

Change in net position of governmental activities (205,931)$

RED BANK CHARTER SCHOOLReconciliation of the Statement of Revenues, Expenditures,

and Changes in Fund Balances of Governmental Fundsto the Statement of Activities

For the Year Ended June 30, 2020

See accompanying notes to financial statements.27

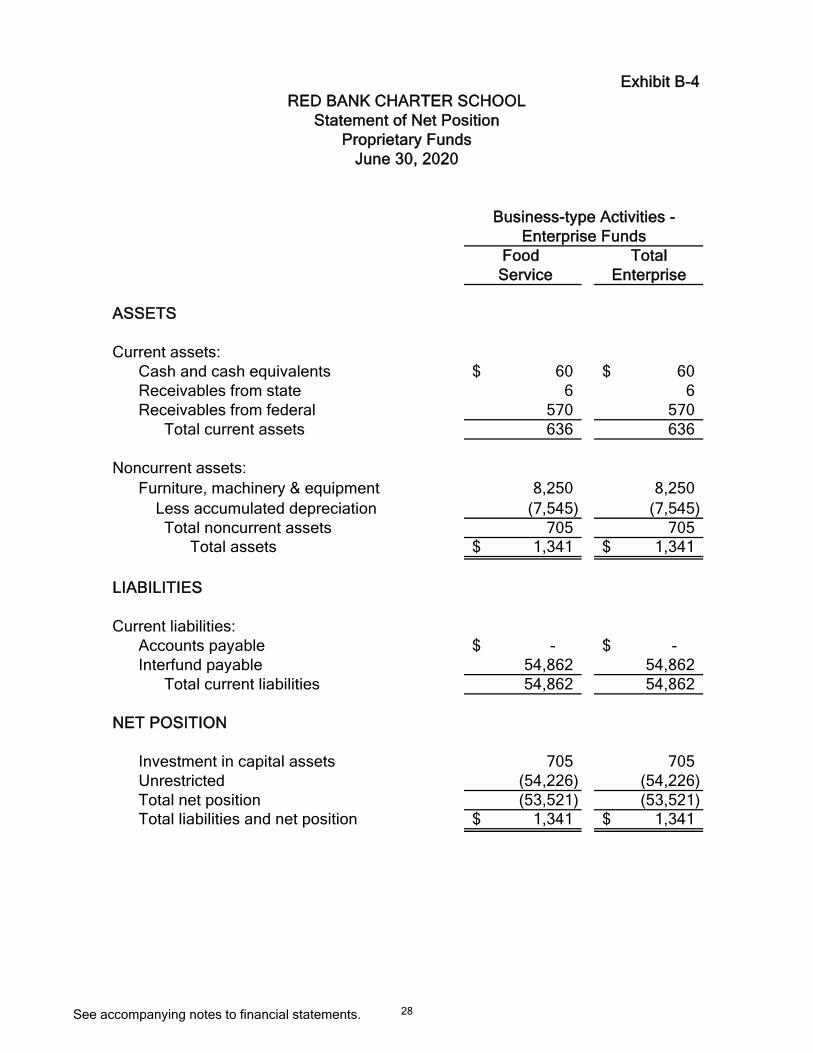

Exhibit B-4

Food Total Service Enterprise

ASSETS

Current assets:Cash and cash equivalents 60$ 60$ Receivables from state 6 6 Receivables from federal 570 570 Total current assets 636 636

Noncurrent assets:

Furniture, machinery & equipment 8,250 8,250

Less accumulated depreciation (7,545) (7,545) Total noncurrent assets 705 705 Total assets 1,341$ 1,341$

LIABILITIES

Current liabilities:Accounts payable -$ -$ Interfund payable 54,862 54,862 Total current liabilities 54,862 54,862

NET POSITION

Investment in capital assets 705 705 Unrestricted (54,226) (54,226) Total net position (53,521) (53,521) Total liabilities and net position 1,341$ 1,341$

Business-type Activities -Enterprise Funds

RED BANK CHARTER SCHOOLStatement of Net Position

Proprietary FundsJune 30, 2020

See accompanying notes to financial statements. 28

Exhibit B-5

Business-type Activities - Enterprise Fund

Food Total Service Enterprise

Operating revenues:Local sources:Daily sales reimbursable programs School breakfast -$ -$ School lunch 18,346 18,346 Total daily sales reimbursable programs 18,346 18,346

Total operating revenues 18,346 18,346

Operating expenses:Salaries 33,784 33,784 Supplies and materials - - Depreciation 1,179 1,179 Cost of sales - reimbursable programs 50,653 50,653 Cost of sales - non-reimbursable programs - -

Total operating expenses 85,616 85,616 Operating income (loss) (67,270) (67,270)

Nonoperating revenues (expenses):State sources: State school lunch program 768 768 Federal sources: School breakfast program 10,054 10,054 National school lunch program 33,315 33,315 Summer Food Service Program for Children 5,292 5,292 Total nonoperating revenues (expenses) 49,429 49,429 Income (loss) before contributions & transfers (17,841) (17,841)

Transfers in (out) 13,397 13,397 Change in net position (4,444) (4,444)

Total net position—beginning (49,077) (49,077) Total net position—ending (53,521)$ (53,521)$

RED BANK CHARTER SCHOOLStatement of Revenues, Expenses, and Changes in Fund Net Position

Proprietary FundsFor the Year Ended June 30, 2020

See accompanying notes to financial statements. 29

Exhibit B-6

Food Total Service Enterprise

CASH FLOWS FROM OPERATING ACTIVITIESReceipts from customers and other funds 18,346$ 18,346$ Payments to employees & benefits (33,784) (33,784) Payments to suppliers (50,653) (50,653) Net cash provided by (used in) operating activities (66,091) (66,091)

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIES - State sources 816 816 Federal sources 51,474 51,474 Board interfund transfer 13,397 13,397 Net cash provided by (used in) non-capital financing activities 65,687 65,687

Net increase (decrease) in cash and cash equivalents (404) (404) Balances—beginning of year 464 464 Balances—end of year 60$ 60$

Reconciliation of operating income (loss) to net cash provided by (used in) operating activities: Operating income (loss) (67,270)$ (67,270)$ Adjustments to reconcile operating income (loss) to net cash provided by (used in) operating activities: Depreciation and net amortization 1,179 1,179 Total adjustments (66,091) (66,091)

Net cash used in operating activities (66,091)$ (66,091)$

RED BANK CHARTER SCHOOL

Business-type Activities -Enterprise Funds

For the Year Ended June 30, 2020Proprietary Funds

Statement of Cash Flows

See accompanying notes to financial statements.30

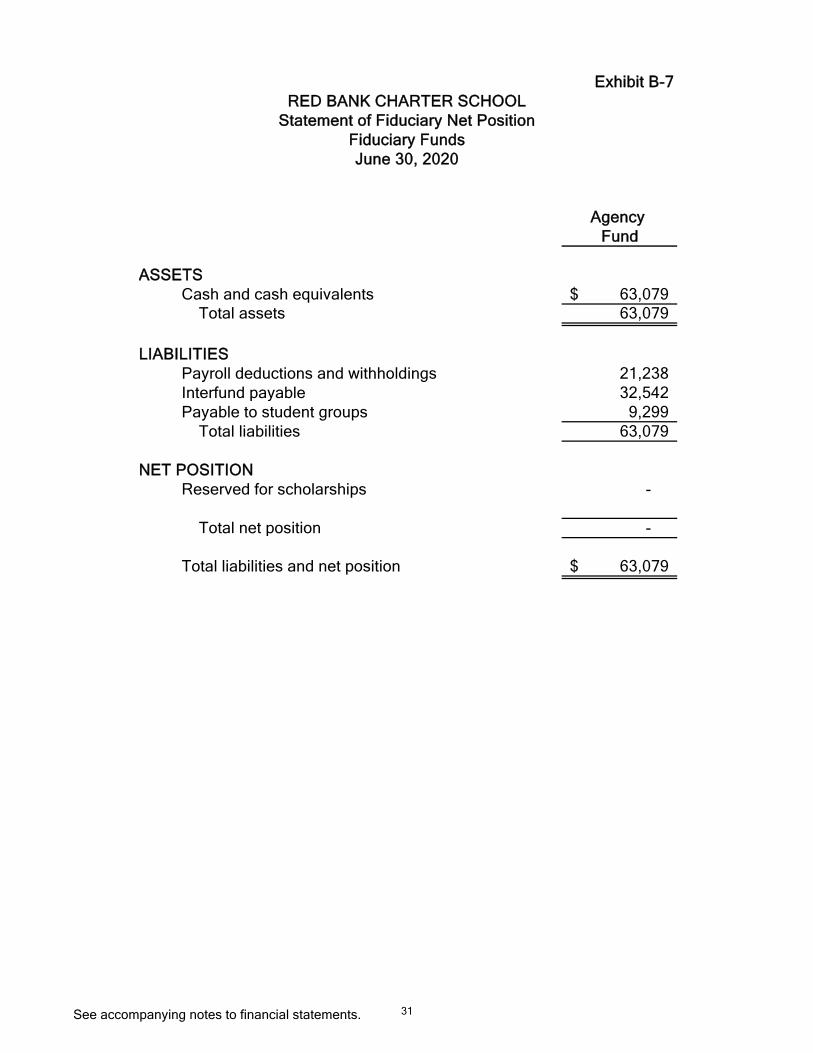

Exhibit B-7

Agency Fund

ASSETSCash and cash equivalents 63,079$ Total assets 63,079

LIABILITIES Payroll deductions and withholdings 21,238 Interfund payable 32,542 Payable to student groups 9,299 Total liabilities 63,079

NET POSITIONReserved for scholarships -

Total net position -

Total liabilities and net position 63,079$

RED BANK CHARTER SCHOOLStatement of Fiduciary Net Position

June 30, 2020Fiduciary Funds

See accompanying notes to financial statements. 31

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

1. Description of the Charter School and Reporting Entity

Red Bank Charter School ("Charter School") is an instrumentality of the State of New Jersey,established to function as an education institution in Red Bank, New Jersey. The Board ofTrustees (the "Board") consists of appointed officials and are responsible for the fiscal control ofthe Charter School. An Educational Director is appointed by the Board and is responsible for theadministrative control of the Charter School.

A reporting entity is comprised of the primary government, component units and otherorganizations that are included to insure that the financial statements of the Charter School arenot misleading. The primary government consists of all funds, departments, boards andagencies that are not legally separate from the Charter School. For the Charter School, thisincludes general operations, food service and student related activities.

The primary criterion for including activities within the Charter School's reporting entity, as setforth in Section 2100 of the GASB Codification of Governmental Accounting and FinancialReporting Standards, is the degree of oversight responsibility maintained by the Charter School.Oversight responsibility includes financial interdependency, section of governing authority,designation of management, ability to significantly influence operations and accountability forfiscal matters. The combined financial statements include all funds of the Charter School overwhich the Board exercises operating control. The Charter School serves students in grades Pre-K through eight. There were no additional entities required to be included in the reporting entityunder the criteria as described above, in the current fiscal year. Furthermore, the Charter Schoolis not includable in any other reporting entity on the basis of such criteria.

2. Summary of Significant Accounting Policies

The financial statements of the Charter School have been prepared in conformity with generallyaccepted accounting principles (GAAP) as applied to governmental units. The GovernmentalAccounting Standards Board (GASB) is the accepted standard-setting body for establishinggovernmental accounting and financial reporting principles. The Charter School also appliesFinancial Accounting Standards Board (FASB) Statements and Interpretations issued on orbefore November 30, 1989, to its governmental activities provided they do no conflict with orcontradict GASB pronouncements. The most significant of the Charter School's accountingpolicies are described below.

A. Basis of Presentation

The Charter School's basic financial statements consists of charter school-widestatements, including a statement of net position and a statement of activities, and fundfinancial statements that provide a more detailed level of financial information.

1. Charter School-Wide Statements

The statement of net position and the statement of activities display information aboutthe Charter School as a whole. These statements include the financial activities of theprimary government, except for fiduciary funds.

32

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

A. Basis of Presentation (Cont'd)

1. Charter School-Wide Statements (Cont'd)

The statement of net position presents the financial condition of the governmentalactivities of the Charter School at fiscal year-end. The statement of activities presentsa comparison between direct expenses and program revenues for each program orfunction of the Charter School's governmental activities. Direct expenses are thosethat are specifically associated with a service, program or department and thereforeclearly identifiable to a particular function. Program revenues include charges paid bythe recipient of the goods or services offered by the program, grants and contributionsthat are restricted to meeting the operational or capital requirements of a particularprogram. Revenues that are not classified as program revenues are presented asgeneral revenues of the Charter School, with certain limited expectations. Thecomparison of direct expenses with program revenues identifies the extent to whicheach governmental function is self-financing or draws from the general revenues of theCharter School.

2. Fund Financial Statements

During the fiscal year, the Charter School segregates transactions related to certainCharter School functions or activities in separate funds in order to aid financialmanagement and to demonstrate legal compliance.

Fund financial statements are designed to present financial information of the CharterSchool at this more detailed level. The focus of governmental and enterprise fundfinancial statements is on major funds. Each major fund is presented in a separatecolumn.

B. Fund Accounting

The Charter School uses funds to maintain its financial records during the fiscal year. Afund is defined as a fiscal and accounting entity with a self-balancing set of accounts.

1. Governmental Funds

Government funds are those through which most governmental functions typically arefinanced. Governmental fund reporting focuses on the sources, uses and balances ofcurrent financial resources. Expendable assets are assigned to the variousgovernmental funds according to the purposes for which they may or must be used.Current liabilities are assigned to the fund from which they will be paid. The differencebetween governmental fund assets and liabilities is reported as fund balance. Thefollowing are the Charter School's major governmental funds:

33

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

B. Fund Accounting (Cont'd)

1. Governmental Funds (Cont'd)

General Fund - The General Fund is the general operating fund of the CharterSchool. It is used to account for all financial resources except those required to beaccounted for in another fund. Included are certain expenditures for vehicles andmovable instructional or noninstructional equipment that are classified in the CapitalOutlay subfund.

As required by the New Jersey State Department of Education, the Charter Schoolincluded budgeted capital outlay in this fund. Generally accepted accountingprinciples as they pertain to governmental entities state that General Fund resourcesmay be used to directly finance capital outlays for long-lived improvements as long asthe resources in such cases are derived exclusively from unrestricted revenues.

Resources for budgeted capital outlay purposes are normally derived from State ofNew Jersey Aid, district taxes and appropriated fund balance. Expenditures are thosethat result in the acquisition of or additions to capital assets for land, existingbuildings, improvements of grounds, construction of buildings, additions to orremodeling of buildings and the purchase of built-in equipment. These resources canbe transferred from and to Current Expense by board resolution.

Special Revenue Fund - The Special Revenue Fund is used to account for theproceeds of specific revenue from State and Federal Government, (other than majorcapital projects, Debt Service or the Enterprise Funds) and local appropriations thatare legally restricted to expenditures for specified purposes.

2. Proprietary Funds

The focus of Proprietary Fund measurement is upon determination of net income,financial position and cash flows. The generally accepted accounting principlesapplicable are those similar to businesses in the private sector. The following is adescription of the proprietary fund of the Charter School:

34

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

B. Fund Accounting (Cont'd)

2. Proprietary Funds (Cont'd)

Enterprise Fund - The Enterprise Fund is utilized to account for operations that werefinanced and operated in a manner similar to private business enterprises - where theintent of the Charter School is that the costs (i.e. expenses including depreciation andindirect costs) of providing goods or services to the students on a continuing educationbasis be financed or recovered primarily through user charges; or, where the CharterSchool has decided that periodic determination of revenues earned, expensesincurred, and/or net income is appropriate for capital maintenance, public policy,management control, accountability or other purposes.

The Charter School's Enterprise Fund is comprised of the Food Service Fund.

All proprietary funds are accounted for on a cost of services or "capital maintenance"measurement focus. This means that all assets and all liabilities, whether current ornoncurrent, associated with their activity are included on their balance sheets. Theirreported fund equity (net position) is segregated into invested in capital assets net ofrelated debt and unrestricted net position, if applicable. Proprietary fund type operatingstatements present increases (revenues) and decreases (expenses) in net totalposition.

Depreciation of all exhaustive capital assets used by proprietary funds is charged asan expense against their operations.

3. Fiduciary Funds

Trust and Agency Funds - The Trust and Agency Funds are used to account forassets held by the Charter School in a trustee capacity or as an agent for individuals,private organizations, other governments and/or other funds.

Agency Funds - Agency Funds are used to account for the assets that the CharterSchool holds on behalf of others as their agent. Agency Funds are custodial in natureand do not involve measurement of results of operations. Agency Funds includepayroll and student activities funds.

35

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

C. Measurement Focus

1. Charter School-Wide Financial Statements

The charter school-wide financial statements are prepared using the economicresources measurement focus. All assets and liabilities associated with the operationof the Charter School are included on the Statement of Net Position.

2. Fund Financial Statements

All governmental funds are accounted for using a flow of current financial resourcesmeasurement focus. With this measurement focus, only current assets and currentliabilities generally are included on the balance sheet. The statement of revenues,expenditures and changes in fund balances reports on the sources (i.e., revenues andother financing sources) and uses (i.e., expenditures and other financing uses) ofcurrent financial resources. This approach differs from the manner in which thegovernmental activities of the charter school-wide financial statements are prepared.Governmental fund financial statements therefore include a reconciliation with briefexplanations to better identify the relationship between the charter school-widestatements and the statements for governmental funds.

All proprietary funds are accounted for on a flow of economic resources measurementfocus. With this measurement, all assets and all liabilities associated with theoperation of these funds are included on the balance sheet. Proprietary fund-typeoperating statements present increases (i.e., revenues) and decreases (i.e.,expenses) in net total position.

Fiduciary funds are reported using the economic resources measurement focus.

D. Basis of Accounting

The modified accrual basis of accounting is used for measuring financial position andoperating results of all governmental funds types, expendable trust funds and agencyfunds. Under the modified accrual basis of accounting, revenues are recognized whenthey become both measurable and available. "Measurable" means the amount of thetransaction can be determined and "available" means collectible within the current periodor soon enough thereafter to be used to pay liabilities of the current period. Stateequalization monies are recognized as revenue during the period in which they areappropriated. A one-year availability period is used for revenue recognition for all othergovernmental fund revenues. Expenditures are recognized in the accounting period inwhich the fund liability is incurred, except for principal and interest on general long-termdebt which are recorded when due.

36

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

D. Basis of Accounting (Cont'd)

The Charter School receives a portion of the local tax levy and state aid from the severalschool districts based upon the number of enrolled students. The State Department ofEducation in conjunction with the local school district revises the amounts to be receivedby the Charter School three times a year based upon the enrollment counts on June 1,October 15, and the last day of the school year. The local tax levy and state aid aresusceptible to accrual. The Charter School records the entire anticipated local tax levy tobe received at the start of the fiscal year based upon the June 1 enrollment count andcertification from the New Jersey State Department of Education, since the revenue isboth measurable and available. The Charter School is entitled to receive monies underthe established payment schedule, which is revised after each enrollment count date,and the unpaid amount is considered to be an "accounts receivable". At June 30, 2020,the Charter School had accounts receivable of $5,219 that represented amounts thathad not been repaid based upon the current year final enrollment count.

In its accounting and final reporting, the Charter School follows the pronouncements ofthe Governmental Accounting Standards Board (GASB) and the pronouncements of theFinancial Accounting Standards Board (FASB) and its predecessor organizations issuedon or before November 30, 1989, unless they conflict with or contradict GASBpronouncements. The Charter School's proprietary funds have elected not to apply thestandards issued by FASB after November 30, 1989.

The accrual basis of accounting is used for measuring financial position and operatingresults of proprietary fund types and nonexpendable trust funds. Under this method,revenues are recognized in the accounting period in which they are earned andexpenses are recognized when they are incurred.

E. Budgets/Budgetary Control

Annual appropriated budgets are prepared in the spring of each year for the general andspecial revenue funds. The budgets are submitted to the county office for approval.Budgets are prepared using the modified accrual basis of accounting, except for thespecial revenue fund as described later. The legal level of budgetary control isestablished at line item accounts within each fund. Line item accounts are defined asthe lowest (most specific) level of detail as established pursuant to the minimum chart ofaccounts referenced in N.J.A.C. 6:20-2A.2(m)1. Transfers of appropriations may bemade by School Board resolution at any time during the fiscal year subject to thelimitation of P.L. 2004 c73 (S1701). The Board of Trustees did not make any materialsupplemental budgetary appropriations during the fiscal year.

37

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

E. Budgets/Budgetary Control (Cont'd)

Formal budgetary integration into the accounting system is employed as a managementcontrol device during the year. For governmental funds, there are no substantialdifferences between the budgetary basis of accounting and accounting principlesgenerally accepted in the United States of America (GAAP) with the exception of thelegally mandated revenue recognition of the last state aid payment for budgetarypurposes only and the special revenue fund as noted below. Encumbrance accounting isalso employed as an extension of formal budgetary integration in the governmental fundtypes. Unencumbered appropriations lapse at fiscal year end.

The accounting records of the special revenue fund are maintained on the grantaccounting budgetary basis. The grant accounting budgetary basis differs from GAAP inthat the grant accounting budgetary basis recognizes encumbrances as expendituresand also recognizes the related revenues, whereas the GAAP basis does not. Sufficientsupplemental records are maintained to allow for the presentation of GAAP basisfinancial reports.

Exhibit C-3 represents a reconciliation of the General Fund revenues and SpecialRevenue Fund revenues and expenditures from the budgetary basis of accounting aspresented in the Budgetary Comparison Schedule - General Fund and Special RevenueFund to the GAAP basis of accounting as presented in Exhibit B-2.

F. Encumbrances

Under encumbrance accounting purchase orders, contracts and other commitments forthe expenditure of resources are recorded to reserve a portion of the applicableappropriation. Open encumbrances in governmental funds, other than the specialrevenue fund, are reported as reservations of fund balances at fiscal year end as they donot constitute expenditures or liabilities but rather commitments related to unperformedcontracts for goods and services.

Open encumbrances in the special revenue fund, for which the Charter School hasreceived advances, are reflected in the balance sheet as deferred revenues at fiscal yearend. There were no encumbrances at June 30, 2020.

The encumbered appropriation authority carries over into the next fiscal year. An entrywill be made at the beginning of the next fiscal year to increase the appropriationreflected in the certified budget by the outstanding encumbrance amount as of thecurrent fiscal year end.

38

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

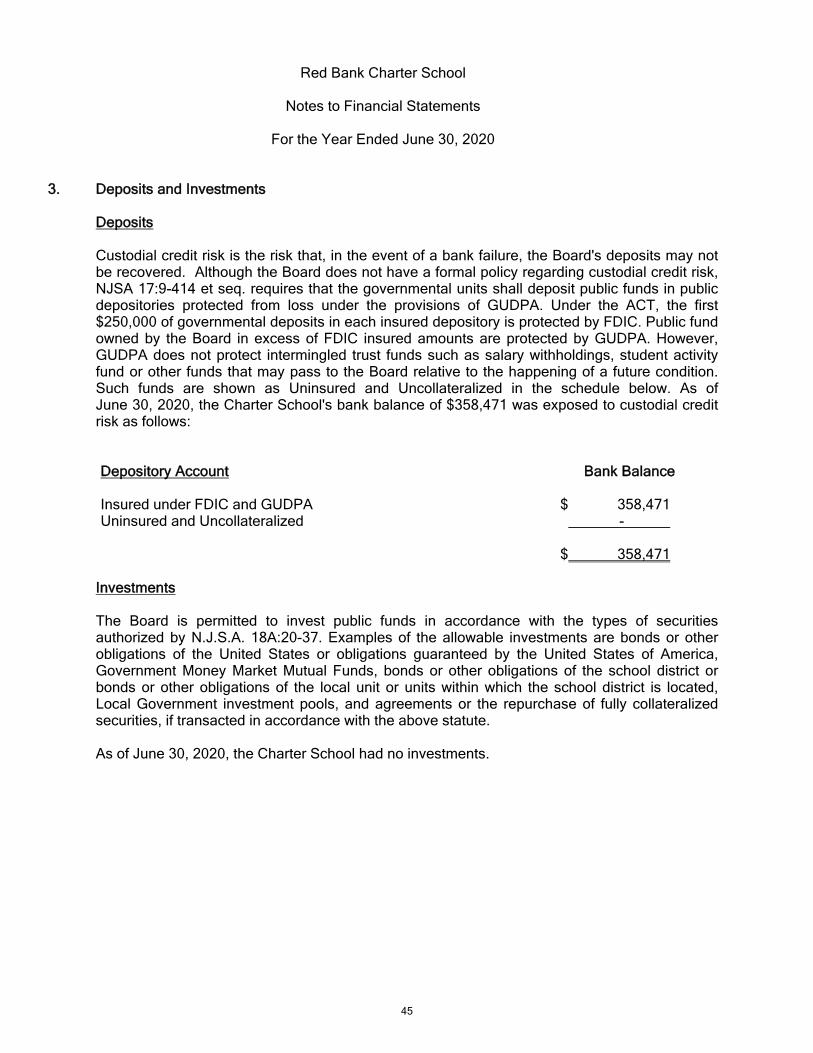

G. Cash, Cash Equivalents and Investments

Cash and cash equivalents include petty cash, change funds, cash in banks and allhighly liquid investments with a maturity of three months or less at the time of purchaseand are stated at cost plus accrued interest. U.S. Treasury and agency obligations andcertificates of deposit with maturities of one year or less when purchased are stated atcost. All other investments are stated at fair value.

New Jersey school districts are limited as to the types of investments and types offinancial institutions they may invest in. New Jersey statute 18A:20-37 provides a list ofpermissible investments that may be purchased by New Jersey school districts.

Additionally, the Charter School has adopted a cash management plan that requires it todeposit public funds in public depositories protected from loss under the provisions of theGovernmental Unit Deposit Protection Act ("GUDPA"). GUDPA was enacted in 1970 toprotect Governmental Units from a loss of funds on deposit with a failed bankinginstitution in New Jersey.

N.J.S.A. 17:9-41 et. seq. establishes the requirements for the security of deposits ofgovernmental units. The statute requires that no governmental unit shall deposit publicfunds in a public depository unless such funds are secured in accordance with the Act.Public depositories include Savings and Loan institutions, banks (both state and nationalbanks) and savings banks, the deposits of which are federally insured. All publicdepositories must pledge collateral, having a market value at least equal to five percentof the average daily balance of collected public funds, to secure the deposits ofGovernmental Units. If a public depository fails, the collateral it has pledged, plus thecollateral of all other public depositories, is available to pay the full amount of theirdeposits to the Governmental Units.

H. Inventories and Prepaid Expenses

Inventories and prepaid expenses, which benefit future periods are recorded as anexpenditure during the year of purchase.

Inventories are valued at cost, using the first-in/first-out (FIFO) method. The costs ofinventories are recorded as expenditures when consumed rather when purchased.

39

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

I. Short-Term Interfund Receivables/Payables

Short-term interfund receivables/payables represent amounts that are owed, other thancharges for goods or services rendered to/from a particular fund in the Charter Schooland that are due within one year.

J. Capital Assets

General capital assets result from expenditures in the governmental funds. These assetsare reported in the governmental activities column of the charter school-wide statementof net position but are not reported in the fund financial statements.

All capital assets are capitalized at cost (or estimated historical cost) and updated foradditions and retirements during the year. Donated capital assets are recorded at theiracquisition value as of the date received. The Charter School maintains a capitalizationthreshold of $2,000. Improvements are capitalized; the costs of normal maintenance andrepairs that do not add to the value of the asset or materially extend an asset's life arenot.

All reported capital assets except for land are depreciated. Improvements aredepreciated over the remaining useful lives of the related capital assets. Depreciation iscomputed using the straight-line method over the following useful lives:

Description Estimated Lives

Building Improvements 20-50 yearsFurniture and Equipment 5-10 yearsVehicles 3-5 years

K. Compensated Absences

Compensated absences are those absences for which employees will be paid, such asvacation and sick leave. A liability for compensated absences that are attributable toservices already rendered, and that are not contingent on a specific event that is outsidethe control of the Charter School and its employees, is accrued as the employees earnthe rights to the benefits. Compensated absences that relate to future services, or thatare contingent on a specific event that is outside the control of the Charter School and itsemployees, are accounted for in the period in which such services are rendered or inwhich such events take place.

40

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

K. Compensated Absence (Cont'd)

The entire sick leave and vacation liabilities are reported on the charter school-widefinancial statements.

For governmental fund financial statements, the current portion of unpaid compensatedabsences is in the amount expected to be paid using expendable available resources.These amounts are recorded in the account "compensated absences payable" in thefund from which the employees who have accumulated unpaid leave are paid. Thenoncurrent portion of the liability is not reported. The Charter School had a compensatedabsence liability of $- at year end.

L. Accrued Liabilities and Long-Term Obligations

All payables, accrued liabilities and long-term obligations are reported in the charterschool-wide financial statements.

In general, payables and accrued liabilities those, once incurred, are paid in a timelymanner and in full from current financial resources are reported as obligations of thegovernmental funds. However, the noncurrent portion of compensated absences andmortgage payable that will be paid from governmental funds are reported as a liability inthe fund financial statements only to the extent that they are normally expected to bepaid with expendable, available financial resources.

M. Net Position

Net position represents the difference between assets and liabilities. Net investment incapital assets consists of capital assets, net of accumulated depreciation, reduced by theoutstanding balances of any borrowings used for the acquisition, construction orimprovement of those assets. Net position is reported as restricted when there arelimitations imposed on their use either through the enabling legislation adopted by theCharter School or through external restrictions imposed by creditors, grantors, or laws orregulations of other governments.

N. Unearned Revenue

Unearned revenue in the special revenue fund represents cash that has been receivedbut not yet earned.

O. Fund Balance Reserves

Reserves represent those portions of fund equity not available for appropriation forexpenditure or legally segregated for a specific future use. Designated fund balancesrepresent plans for future use of financial resources.

41

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

P. Management Estimates

The preparation of financial statements in conformity with generally accepted accountingprinciples require management to make estimates and assumptions that affect reportedamounts and disclosures. Actual results could differ from those estimates.

R. Deferred Outflows/Inflows of Resources

In addition to assets, the statement of net position will sometimes report a separatesection for deferred outflows of resources. This separate financial statement element,deferred outflows of resources, represent a consumption of net position that applies to afuture period(s) and so will not be recognized as an outflow of resources(expense/expenditure) until then.

In addition to liabilities, the statement of net position will sometimes report a separatesection for deferred inflows of resources. This separate financial statement element,deferred inflows of resources, represents an acquisition of net position that applies tofuture periods and so will not be recognized as an inflow of resources (revenue) until thattime.

S. GASB Pronouncements

Recently Issued Accounting Pronouncements to be implemented in future years

Statement No. 84, Fiduciary Activities in January 2017. This Statement establishesstandards of accounting and financial reporting for fiduciary activities. The requirementsof this Statement are effective for periods beginning after December 15,2019. Management has not yet determined the impact of this Statement on the financialstatements.

Statement No. 87, Leases in June 2017. This Statement establishes standards ofaccounting and financial reporting for leases by lessees and lessors. The requirementsof this Statement are effective for periods beginning after June 15, 2021, and all reportingperiods thereafter. Management has not yet determined the impact of this Statement onthe financial statements.

Statement No. 89, Accounting for Interest Cost Incurred before the End of a ConstructionPeriod. The objectives of this Statement are (1) to enhance the relevance andcomparability of information about capital assets and the cost of borrowing for a reportingperiod and (2) to simplify accounting for interest cost incurred before the end of aconstruction period. The requirements of this Statement are effective for reporting periodsbeginning after December 15, 2020. Management does not expect this Statement to havea material impact on the Charter School’s financial statements.

42

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

S. GASB Pronouncements (Cont'd)

Statement No. 90, Majority Equity Interests - an amendment of GASB Statements No. 14and No. 61. The primary objectives of this Statement are to improve the consistency andcomparability of reporting a government’s majority equity interest in a legally separateorganization and to improve the relevance of financial statement information for certaincomponent units. It defines a majority equity interest and specifies that a majority equityinterest in a legally separate organization should be reported as an investment if agovernment’s holding of the equity interest meets the definition of an investment. Amajority equity interest that meets the definition of an investment should be measuredusing the equity method, unless it is held by a special-purpose government engaged onlyin fiduciary activities, a fiduciary fund, or an endowment (including permanent and termendowments) or permanent fund. Those governments and funds should measure themajority equity interest at fair value. Statement No. 90 is effective for reporting periodsbeginning after December 15, 2019. Management has not yet determined the potentialimpact on the Charter School’s financial statements.

Statement No. 91, Conduit Debt Obligations, The primary objectives of this Statement areto provide a single method of reporting conduit debt obligations by issuers and eliminatediversity in practice associated with (1) commitments extended by issuers, (2)arrangements associated with conduit debt obligations, and (3) related note disclosures.This Statement achieves those objectives by clarifying the existing definition of a conduitdebt obligation; establishing that a conduit debt obligation is not a liability of the issuer;establishing standards for accounting and financial reporting of additional commitmentsand voluntary commitments extended by issuers and arrangements associated withconduit debt obligations; and improving required note disclosures. Statement No. 91 iseffective for reporting periods beginning after December 15, 2021. Management has notyet determined the potential impact on the Charter School’s financial statements.

Statement No. 92, Omnibus 2020, The objectives of this Statement are to enhancecomparability in accounting and financial reporting and to improve the consistency ofauthoritative literature by addressing practice issues that have been identified duringimplementation and application of certain GASB Statements. Statement No. 92 iseffective for reporting periods beginning after June 15, 2021. Management has not yetdetermined the potential impact on the Charter School’s financial statements.

43

Red Bank Charter School

Notes to Financial Statements

For the Year Ended June 30, 2020

2. Summary of Significant Accounting Policies (Cont'd)

S. GASB Pronouncements (Cont'd)

Statement No. 93, Replacement of Interbank Offered Rates, Some governments haveentered into agreements in which variable payments made or received depend on aninterbank offered rate (IBOR)—most notably, the London Interbank Offered Rate (LIBOR).As a result of global reference rate reform, LIBOR is expected to cease to exist in itscurrent form at the end of 2021, prompting governments to amend or replace financialinstruments for the purpose of replacing LIBOR with other reference rates, by eitherchanging the reference rate or adding or changing fallback provisions related to thereference rate. The objective of this Statement is to address accounting and financialreporting implications that result from the replacement of an IBOR. The removal of LIBORas an appropriate benchmark interest rate is effective for reporting periods ending afterDecember 31, 2021. All other requirements of Statement No. 93 are effective for reportingperiods beginning after June 15, 2020. Management has not yet determined the potentialimpact on the Charter School’s financial statements.

Statement No. 94, Public-Private and Public-Public Partnerships and Availability PaymentArrangements, The primary objective of this Statement is to improve financial reporting byaddressing issues related to public-private and public-public partnership arrangements(PPPs). Statement No. 94 is effective for reporting periods beginning after June 15, 2022,and all reporting periods thereafter. Management has not yet determined the potentialimpact on the Charter School’s financial statements.

Statement No. 95, Postponement of the Effective Dates of Certain AuthoritativeGuidance, The primary objective of this Statement is to provide temporary relief togovernments and other stakeholders in light of the COVID-19 pandemic. Therequirements of Statement No. 95 are effective immediately.