rating oil & gas companies

TRANSCRIPT

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 1/15

june 2009

Methodology

Rating Oil and Gas Companies

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 2/15

CONTACT INFORMATIONEsther Mui, MBA, CMA

Senior Vice President

Tel. +1 416 597 [email protected]

Michael Rao, CFA

Senior Vice President

Tel. +1 416 597 7541

Brian Ko

Assistant Vice President

Tel. +1 416 597 7597

Howard Nishi

Assistant Vice President

Tel. +1 416 597 7370

Michael J. Caranci

Managing Director - EnergyTel. +1 416 597 7304

DBRS is a full-service credit rating agencyestablished in 1976. Privately owned and operatedwithout af filiation to any financial institution,DBRS is respected for its independent, third-party

evaluations of corporate and government issues,spanning North America, Europe and Asia.DBRS’s extensive coverage of securitizationsand structured finance transactions solidifies our

standing as a leading provider of comprehensive,in-depth credit analysis.

All DBRS ratings and research are available in

hard-copy format and electronically on Bloombergand at DBRS.com, our lead delivery tool fororganized, Web-based, up-to-the-minute infor-mation. We remain committed to continuouslyrefining our expertise in the analysis of creditquality and are dedicated to maintainingobjective and credible opinions within the globalfinancial marketplace.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 3/15

Rating Oil and Gas Companies

June 2009

Rating Oil and Gas Companies

TABLE OF CONTENTS

I. Overview 4

II. General Business Risk Profile 5

Key Considerations in Evaluating a Company’s Business Risk Profile 5

Economic Environment 5

Legislative and Regulatory Environment 5

Competitive Environment 5

Country Risk 5

Industry Cyclicality 6

Management 6

Corporate Governance 6

III. General Financial Risk Profile 7

Key Considerations in Evaluating a Company’s Financial Risk Profile 7

A. Earnings 7

B. Cash Flow/Coverage 7

C. Balance Sheet and Financial Flexibility Considerations 8

IV. Industry-Specific Factors 9

Key Considerations in Evaluating Companies in the Oil and Gas Sector 9

Primary Factors 9

Price and Cost Relationship 9

Market Volatility 10

Business Mix and Diversification 10

Cash Flow 11

Liquidity 11

Capital Spending 11

Capital Structure 12

Secondary Factors 12

Political Risks 12

Regulatory/Environmental Factors 12

Qualitative and Quantitative Factors 12

Qualitative Factors 12

Quantitative Factors 13

Note: DBRS provides third-party, independent evaluations in four major areas: the corporate sector, financial institutions,public finance and structured finance. The corporate sector consists of a wide variety of industries.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 4/15

Rating Oil and Gas Companies

June 2009

4

I. Overview

DBRS ratings are opinions that reflect the creditworthiness of an issuer, a security, or an obligation. Theyare opinions based on forward-looking measurements that assess a company’s ability and willingness tomake timely payments on outstanding obligations (whether principal, interest, or dividend) with respectto the terms of an obligation. Ratings are not buy, hold or sell recommendations and they do not addressthe market price of a security.

DBRS rating methodologies include consideration of general business and financial risk factors applicableto most industries in the corporate sector as well as industry specific issues and more subjective factors,nuances and intangible considerations. Our approach is not based solely on statistical analysis but includesa combination of both quantitative and qualitative considerations. The considerations outlined in DBRSmethodologies are not intended to be exhaustive. In certain cases, a major strength can compensate for aweakness that would be more critical for a peer company. Conversely, there are cases where one weaknessis so critical that it overrides the fact that the company may be strong in most other areas.

DBRS rating methodology is underpinned by a stable rating philosophy, which means that in order to

minimize the rating changes due primarily to global economic changes DBRS generally factors the impactof a cyclical economic environment into its rating. Consequently, DBRS takes a longer-term “through thecycle” view of a company and, as such, rating changes are not based solely on normal economic cycles.Rating revisions do occur, however, when it is clear that a structural change, either positive or negative,has transpired or appears likely to transpire in the near future. An equally important aspect of DBRSanalysis is its broad industry coverage, which it undertakes in order to understand the major differencesand subtle nuances within a particular industry and to form an appropriate rating of a company relativeto its competitors.

As a framework, DBRS rating methodologies consist of three components that together form the basis

of the rating: an assessment of the company’s general business risk profile based on cross-industry andmacro business considerations; an assessment of the company’s financial risk profile primarily basedon quantitative ratio analysis; and consideration of industry-specific factors and measures particularlyunique to the company. To some extent, the business risk and financial risk profiles are inter-related. Thedegree of financial risk considered acceptable for a company depends to a large measure on the businessrisks it faces.

Critical in the determination of a rating is the application of the analyst’s experience and expertise informing an initial rating opinion and recommendation for the rating committee and the role of the DBRSrating committee as the final decision maker. DBRS rating committees, which are comprised of experi-enced and knowledgeable DBRS personnel, strive to provide objective and independent rating decisionswhich are based upon all relevant information and factors, incorporate both global and local consider-

ations, apply DBRS approved methodologies and reflect the opinion of DBRS.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 5/15

Rating Oil and Gas Companies

June 2009

II. General Business Risk Profile

A fundamental component of DBRS analysis is the consideration of macro business factors that applyto most, if not all, industries within the Corporate sector. The general business risk profile is largely aqualitative assessment of the environment a company is affected by and operates in. An assessment of the

general business risk profile serves as a backdrop for the analysis of the company’s financial risk profileas well as other qualitative and quantitative factors that are particularly unique to the company. Differingbusiness risk profiles impact the assessment of a company’s financial risk profile, and thus, it is importantto understand the extraneous influences and business factors a company is or could be affected by despiteits financial strength.

KEY CONSIDERATIONS IN EVALUATING A COMPANY’SBUSINESS RISK PROFILEThe following considerations, while not intended to be an exhaustive list, indicate the key areas DBRS

considers in evaluating a company’s business risk profile:

Economic Environment The importance of the industry within the overall economy, in terms of either how it impacts or is impactedby the economy, shapes a company’s viability. How the industry is influenced by current economic factorssuch as inflation or deflation, supply and demand, interest rates, currency swings and demographics.

Legislative and Regulatory Environment Whether an industry is regulated The degree of regulation and legislative oversight can severely restrict orassist a company depending on its stage of growth, industry influence and regulatory relations. A regu-lated industry imposes a certain rigor and governance. It is also important to understand the frequencyof change or stability in industry rules and whether regulations may require companies to make costlymodifications to their infrastructure.

Competitive Environment The nature of the market structure (e.g. monopoly versus oligopoly) determines the extent of competitive-ness and the barriers to entry a company may face. Many industries are undergoing significant structural

changes such as consolidation or deconsolidation, excess capacity, or competitive threats from newcapacity in “low-cost” countries such as China, Brazil, and Russia in both domestic and internationalmarkets. Even small changes in the competitive environment can have a profound impact on a company.

Country RiskGovernments often intervene in their economies and occasionally make substantial changes in policyregarding competition, ownership, wage and price controls, restrictions on foreign currency, capitaland imports/exports, among other things. Such policy changes can significantly affect a company, and

therefore, considerations include the company’s main location or country of operation, the extent of government intervention and support, and the degree of economic and political stability. The assess-ment of country risk is not limited to direct government actions to interfere with the private sector, butalso encompasses the full range of financial and economic events that can spill across a country, causingwidespread defaults in otherwise healthy corporate credits. As such, country risk can have considerableimplications for corporate ratings. A country ceiling is assigned to corporate foreign currency ratingsbased on the country’s susceptibility to systemic shocks and the private sector’s ability to maintain itsforeign currency debt payments when shocks occur.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 6/15

Rating Oil and Gas Companies

June 2009

6

Industry CyclicalityCyclicality is influenced by factors such as levels of consumer spending, consumer confidence, and thestrength of the economy. The degree of cyclicality is influenced by the market segment in which a companyspecializes. Non-cyclical industries are better able to withstand dramatic economic changes as are com-

panies with more predictable cycles than those with significant peaks and troughs. It is important toexamine a company’s strategies and performance over the longer term and understand them in cyclicalhighs and lows.

Management The capability and strength of management is a pivotal factor to company success. An objective profile of management can be obtained by assessing the following: the appropriateness of core strategies; rigor of key policies, processes and practices; management’s reaction to problem situations; its appetite for growth,either organically by adding new segments or through acquisition; its ability to smoothly integrate acqui-

sitions without business disruption; and its track record in achieving financial results. Retention strategiesand succession planning for senior roles are also critical considerations.

Corporate GovernanceEffective corporate governance requires a healthy tension between management, the board of directors,and the public. There is no one “right” approach for all companies. A good board can have a profoundimpact on growing companies, those in fragile financial states, or those undergoing significant change.Beyond a review of management, assessment should focus on the appropriateness of board compositionand structure (including the independence and expertise of the audit committee) to approve executive

compensation and corporate strategy, and to oversee execution and opportunities for management self-interest. Other important areas include the extent of disclosure of financial and non-financial information(including aggressiveness of accounting practices and control weaknesses), share ownership (includingdirector’s) and shareholder rights.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 7/15

Rating Oil and Gas Companies

June 2009

III. General Financial Risk Profile

The financial risk profile is largely a quantitative assessment of the company’s financial strength and anestimation of its future performance and financial profile. DBRS reviews three key areas: earnings, cashflow, and additional measures for balance sheet and financial flexibility. Within each area, DBRS focuseson key metrics and considerations which are assessed over time noting that the trend in the ratios is alsoimportant to the rating. However, ratios alone cannot be used as an absolute test of financial strength.With a focus on future expectations, the primary goal of financial risk assessment is to understand the

inter-relationship between the numbers, interpret what they mean, and determine what they indicateabout the company’s ability to service and repay debt on a timely basis given the industry background.

KEY CONSIDERATIONS IN EVALUATING A COMPANY’SFINANCIAL RISK PROFILEThe following financial considerations and ratios tend to be analyzed for the majority of industries inthe Corporate sector. There may be additional quantitative factors and ratios that are considered on an

industry-specific basis which are noted under Section IV - Industry Specific-Factors.

Also refer to the Corporate Sector – Glossary of Ratio Definitions.

A. EarningsDBRS earnings analysis focuses on core or normalized earnings and in doing so considers issues such as:the sources, mix and quality of revenue; the volatility or stability of revenue; the underlying cost base(e.g. company is a low-cost producer); optimal product pricing; and potential growth opportunities.Accordingly, earnings as presented in the financial statements are often adjusted for non-recurring itemsor items not considered part of ongoing operations. DBRS generally reviews company budgets and fore-

casts for future periods. Segmented breakdowns by division are also typically part of DBRS’s analysis.

Typical earnings ratios include:• Gross margin• Return on common equity• Return on capital• EBIT margin and EBITDA margin

B. Cash Flow/CoverageDBRS cash flow analysis focuses on the core cash flow generating ability of the company to servicecurrent debt obligations and other cash requirements as well as the future direction of cash flow. From acredit analysis perspective, insuf ficient cash sources can create financial flexibility problems even thoughnet income metrics may be favourable. DBRS evaluates the sustainability and quality of a company’s corecash flow by focusing on cash flow from operations and free cash flow before and after working capital

changes. Using core or normalized earnings as a base, DBRS adjusts cashflow from operations for asmuch non-recurring items as possible. In terms of outlook, DBRS focuses on the projected direction of free

cash flow, the liquidity and coverage ratios, and the company’s ability to internally versus externally funddebt reduction and future capital expenditure and dividend/stock repurchase programs, as applicable.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 8/15

Rating Oil and Gas Companies

June 2009

8

Typical cash flow ratios include:• EBIT interest coverage and EBITDA interest coverage• EBIT fixed charges coverage• Cash flow/total debt and Cash flow/adjusted total debt• Cash flow/capital expenditures

• Capital expenditures/depreciation• Debt/EBITDA• Dividend payout ratio

C. Balance Sheet and Financial Flexibility ConsiderationsAs part of determining the overall financial risk profile, DBRS evaluates various other factors to measurethe strength and quality of the company’s assets and its financial flexibility.

From a balance sheet perspective, DBRS focuses on the quality and composition of assets includinggoodwill and other intangibles, off-balance-sheet risk, and capital strength including the quality of capital,appropriateness of leverage to asset quality, and the ability to raise new capital. DBRS also reviews the

company’s strategies for growth including capital expenditures, plans for maintenance or expansion, and

the expected source for funding these requirements. Where the numbers are considered significant and theadjustments would meaningfully impact the credit analysis, DBRS adjusts certain ratios for items such asoperating leases, derivatives, securitizations, hybrid issues, off-balance-sheet liabilities and various otheraccounting issues.

Typical balance-sheet ratios include:• Current ratio• Turnover – Receivables and inventory

• Asset coverage (times)• Per cent total debt to capital and per cent adjusted total debt to capital• Per cent adjusted net debt to capitalThe following factors focus on the company’s liquidity:

• Maintaining suf ficient bank-lines or cash balances;• Prudent use of cash balances for dividends or stock repurchases;• Terms and conditions of credit facilities including unique terms and/or financial covenants;• Debt management approach including dependence on short-term versus long-term debt, fixed versus

variable rate debt, and debt maturity schedule;• Interest rate and/or foreign exchange exposure;• Relationship and strength or weakness of a parent holding company or associated companies, if

applicable.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 9/15

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 10/15

Rating Oil and Gas Companies

June 2009

10

Price SensitivityThe price realization of the commodity is highly dependent on the quality of the product (e.g., sweetversus sour crude, wet versus dry gas, heavy oil versus light oil), given that most upstream productionmust be processed to varying degrees before consumption. The location of the reserves is another keyfactor (e.g., natural gas from the Rocky Mountains versus Equatorial Guinea). As such, upstream compa-

nies often operate in countries where significant geopolitical challenges exist.

ReservesA company’s production and growth profile is largely dependent on the quality of its reserve base andwhether the proved and probable reserves are in suf ficient quantities and commercially accessible forfuture developments. Upgrading of a company’s portfolio of reserves can be achieved through selectivepurchases and disposals as well as technological enhancement.

Supply/DemandReserves, production and consumption are significant factors that affect price realizations on a globalbasis in the case of crude oil, and generally on a regional basis for natural gas, which is also affected by

storage levels. Refining capacity is an important determinant in the pricing of refined products. Given

the substantial number and size of industry participants, individual companies are typically price-takersin a very competitive market. It is noteworthy that the Organization of Petroleum Exporting Countries(OPEC), through the cooperative effort of its member states, could affect crude oil prices by setting pro-duction quotas and offering fairly substantial spare capacity through Saudi Arabia.

Pipeline Availability/ConstraintsDBRS examines the transportation system required to meet the logistical requirements of the industry.Since energy production tends to be remote from the product’s ultimate end-users, pipeline availability

is a significant determinant of producer netbacks. This is especially true for natural gas, for which thetransportation cost relative to its realized selling price is much higher than for crude oil. Other Issues

Other factors include prices for condensate (which is required to transport heavy oil through a pipeline),drilling rig availability/pricing, and weather conditions (e.g., some regions are accessible only in winter,while demand for natural gas is tied to the summer air conditioning and winter heating seasons). Arbitrageopportunities ensure that pricing ef ficiencies are closely maintained between competing markets.

Market VolatilityDBRS rates oil and gas companies through a cycle, taking into consideration the inherent volatility of com-modity prices, high capital reinvestment risk, cost structure and operating ef ficiency. Cash flow is the mostimportant measure of performance, and DBRS focuses on the sustainability and adequacy of cash flowsupport for debt protection, funding of capital spending and dividends, and generation of free cash flow.Oil and gas ratings focus on assessing the downside risks to cash flow and incorporate forward-lookingDBRS expectations of operating performance and credit quality. Operating performance for individual oil

and gas companies is consistently monitored in the context of peer group comparative analysis.

Business Mix and DiversificationThere are three broad categories of petroleum companies, as outlined below, each with its own specificrisk characteristics and credit profiles. Generally, companies with more integrated and diverse opera-tions, with the benefit of economy of scale, are viewed more favourably, and could receive higher creditratings

Independent Exploration and Production (E&P) CompaniesThese companies can experience significant volatility in earnings and cash flow due to their exposure to

commodity price swings and large investments to replace reserves.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 11/15

Rating Oil and Gas Companies

June 2009

Independent Refiners/MarketersThese companies are subject to general economic conditions that determine demand for refined products.

Refiners in particular benefit from larger differentials between crude oil feedstock prices and price realiza-tions of refined products. In this respect, refiners in North America are generally focusing on expandingand upgrading their refining capacities to handle heavier crude oil, especially from the Canadian oil

sands.

IntegratedsDBRS views the integrated oil and gas companies (Integrateds) as the most stable and highly rated of thepetroleum companies, with more diversified cash flow and often countercyclical upstream and downstreamoperations. Integrateds are typically engaged in all phases of the business, from oil & gas exploration and

production through marketing and refining and even petrochemical and/or oil sands operations. Thesecompanies typically have greater capacity to internally fund capital spending than pure E&P companies.

Cash FlowThe oil and gas industry reports high levels of depreciation, depletion and amortization and relativelyhigh levels of deferred taxes, which are all non-cash items. For this reason, DBRS believes that cash flow,

which is primarily used to fund capital spending, is a more appropriate measure for assessing an oil andgas company’s financial performance than is net income. Crude oil and natural gas prices can fluctuate

widely, depending on factors such as supply and demand fundamentals, inventory levels, weather condi-tions and seasonal factors. This makes the cash flow of oil and gas companies inherently volatile. Amongthe mitigants to this volatility are hedging arrangements, which, applied on a consistent basis, couldprovide a certain measure of cash flow stability for the near term. In addition, a production profile thatis balanced between crude oil and natural gas can provide an element of stability relatively to companiesthat have a significant weighting to one commodity.

LiquidityLiquidity analysis assesses a company’s corporate philosophy as well as its ability to meet its capital

programs, debt and other obligations. Consideration is given to the adequacy of bank credit lines, cash

balances and other readily accessible sources of liquidity. Other factors include counterparty credit, cashcollateral requirements, debt financings and other general liquidity demands. Any sharp drop in commod-ity prices coupled with continuing turmoil in the credit and capital markets could heighten the challengesfaced by industry participants in maintaining adequate liquidity to fund existing and future obligations.

Capital Spending Capital spending analysis provides an understanding of a company’s operating strategies, growth plansand areas under investment and divestment. Analysis of capital spending begins with an examination

of a company’s capital needs. Cash flow adequacy is viewed from the standpoint of a company’s abilityto finance capital maintenance requirements internally, as well as its ability to finance capital additions.An important dimension of capital spending is the extent of a company’s flexibility to alter the timing of projects without permanent impairment of its operations. In the case of oil sands projects, special atten-

tion is focused on the substantial front-end capital and the relatively infl

exible timeline for developments,particularly for mining projects with upgrading operations.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 12/15

Rating Oil and Gas Companies

June 2009

12

Capital StructureWhen assessing an oil and gas company’s balance sheet and capital structure, DBRS considers a varietyof factors, including the use of leverage, interest coverage and fixed-charge coverage ratios, debt maturityand refinancing risk, fixed-rate versus floating-rate debt, average coupon interest costs and cash balances,

as well as other potential sources of liquidity. Although DBRS recognizes the importance of traditional

debt-to-capital ratios as an indicator of financial leverage, the capitalized value of property, plant andequipment and book equity values may not be reflective of the true underlying value of oil and gasreserves in the ground. As a result, DBRS tends to place greater emphasis on debt-to-cash flow, interestand fixed-charge coverage ratios as measures of balance sheet strength. Off-balance sheet liabilities suchas operating leases, which are most commonly found among oil and gas companies, are also factored intothe leverage analysis. DBRS typically treats these leases as a use of debt capacity.

SECONDARY FACTORS Political RisksCompanies in the oil and gas industry are often confronted with significant political challenges. Whilethese risks can be quantified to some degree using various metrics or tools (e.g., percentage of productionfrom OECD countries, credit ratings of host countries, concentration of production and reserves), fore-

casting the actual impact on a company’s cash flows over time can be considerably less precise. Included inthese risks are unilateral changes in royalties, production sharing contracts as well as indignant matters.

Regulatory/Environmental FactorsDBRS assesses the extent to which oil and gas companies face government laws and regulations, whichcan have an impact on a company’s business and prospects. Among the more stringent laws are allow-able limits of emissions. Industry participants, whether conventional or unconventional, including oilsands operators, are among the major contributors to greenhouse emissions (GHG), principally as aresult of carbon dioxide generated through hydrocarbon production. In light of the global push towardslower GHG through regulatory requirements, including the Kyoto Protocol, DBRS views this risk and itsassociated cost as growing over time. Integrateds also face environmental risks from their downstreamoperations, especially in refining. DBRS also examines the impact of site reclamation and asset retirement

obligations.

QUALITATIVE AND QUANTITATIVE FACTORSQualitative FactorsThere are many qualitative factors that DBRS considers in evaluating quantitative findings and in assess-ing the company’s current and future production and cash flow prospects. These include: (1) scale of operations, (2) production profile and product mix, (3) company expertise, (4) reserves profile, qualityand booking practices, (5) geographic location, infrastructure and market access, and (6) integration.

To reflect more accurately the ongoing earnings power and comparability of peer group companies, DBRSalso takes into consideration the potential impact of accounting variations, and non-recurring events,which include: (1) full cost vs. successful efforts accounting, (2) inventory accounting (FIFO versus LIFO),

(3) tax issues, (4) non-recurring charges/gains, and (5) ceiling test and asset impairment writedowns.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 13/15

Rating Oil and Gas Companies

June 2009

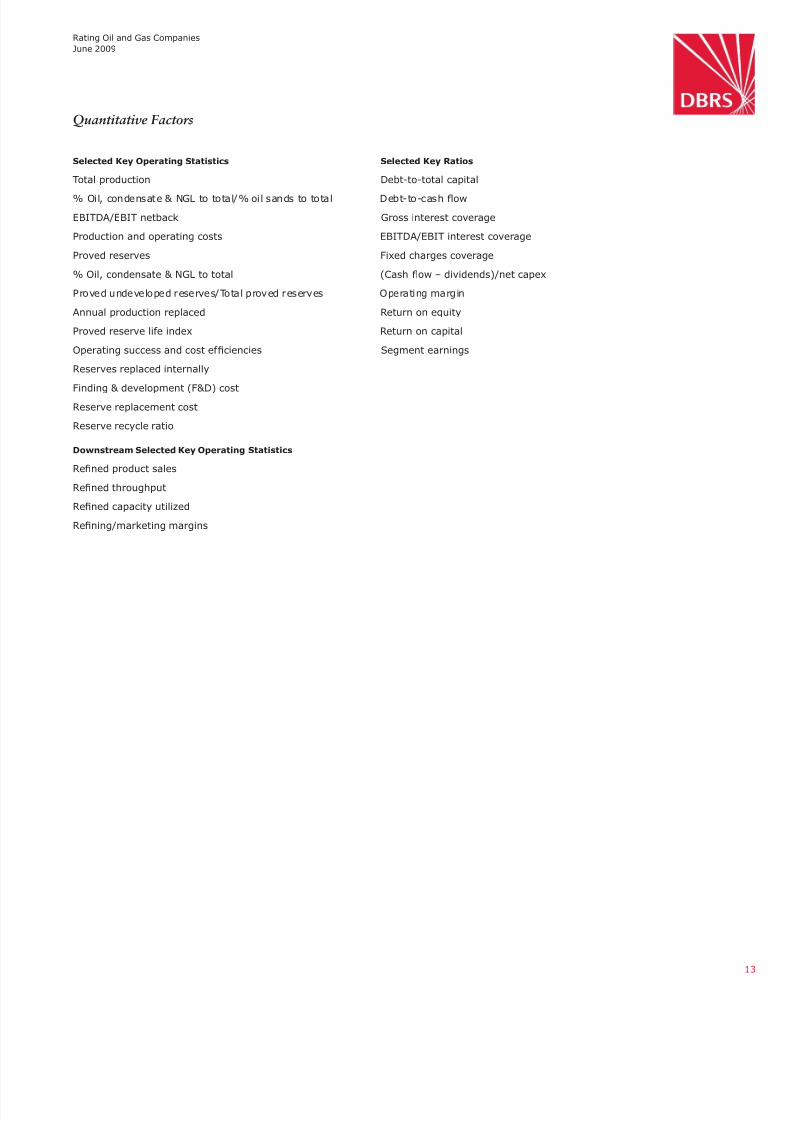

Quantitative Factors

Selected Key Operating Statistics Selected Key Ratios

Total production Debt-to-total capital

% Oil, condensate & NGL to total/% oil sands to total Debt-to-cash flow

EBITDA/EBIT netback Gross interest coverage

Production and operating costs EBITDA/EBIT interest coverage

Proved reserves Fixed charges coverage

% Oil, condensate & NGL to total (Cash flow – dividends)/net capex

Proved undeveloped reserves/Total proved reserves Operating margin

Annual production replaced Return on equity

Proved reserve life index Return on capital

Operating success and cost ef ficiencies Segment earnings

Reserves replaced internally

Finding & development (F&D) costReserve replacement cost

Reserve recycle ratio

Downstream Selected Key Operating Statistics

Refined product sales

Refined throughput

Refined capacity utilized

Refining/marketing margins

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 14/15

Copyright © 2009, DBRS Limited and DB RS, Inc. (collectively, DBRS). All rights reserved. The information upon which DBRS ratings and reports are based is obtained by DBRS from

sources believed by DBRS to be accurate and reliable. DBRS does not perform any audit and does not independently verify the accuracy of the information provided to it. DBRS ratings,

reports and any other information provided by DBRS are provided “as is” and without representation or warranty of any kind. DBRS hereby disclaims any representation or warranty,

express or implied, as to the a ccuracy, timeliness, completeness, merchantability, fitness for any particular purpose or non-infringement of any of such information. In no event shall

DBRS or its directors, officers, employees, independent contractors, agents and representatives (collectively, DBRS Representatives) be liable (1) for any inaccuracy, delay, loss of data,

interruption in service, error or omission or for any damages resulting therefrom, or (2) for any direct, indirect, incidental, special, compensatory or consequential damages arising

from any use of ratings and rating reports or arising from any error (negligent or otherwise) or other circumstance or contingency within or outside the control of DBRS or any DBRS

Representative, in connection with or related to obtaining, collecting, compiling, analyzing, interpreting, communicating, publishing or delivering any such information. Ratings and

other opinions issued by DBRS are, and must be construed solely as, statements of opinion and not statements of fact as to credit worthiness or recommendations to purchase, sell

or hold any securities. A report providing a DBRS rating is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and

its agents in connection with the sale of the securities. DBRS receives compensation for its rating activities from is suers, insurers, guarantors and/or underwriters of debt securities

for assigning ratings and from subscribers to its website. DBRS is not responsible for the content or operation of third party websites accessed through hypertext or other computer

links and DBRS shall have no liability to any person or entity for the use of such third party websites. This publication may not be reproduced, retransmitted or distributed in any form

without the prior written consent of DBR S.

8/14/2019 Rating Oil & Gas Companies

http://slidepdf.com/reader/full/rating-oil-gas-companies 15/15

www.dbrs.com

Corporate Headquarters

DBRS Tower

181 University Avenue

Suite 700

Toronto, ON M5H 3M7

TEL +1 416 593 5577