rapcer 01-18 - stefancollignon.de · stefan collignon, gianluca cubadda, giuseppe de arcangelis,...

TRANSCRIPT

Rapporto CER

Re-inventing Europe

n.1 2018

CENTRO EUROPA RICERCHE

ER produces short and medium-term forecast of the Italian economy, evalua-

tions on economic policy, reports on public finance, fiscal, monetary and industrial policy.

CER is regularly invited to auditions by the Italian Parliament on the economic outlook and

public finance trends. CER prepares a «consensus forecast» for the Italian Ministry of the

Economy jointly with other research institutes.

CER's forecasting and simulation expertise is embodied in its econometric models, which

are continuously updated to take into account structural changes in the national and in-

ternational economy. The econometric models are used to test the impact of policy

measures as well as provide forecasts of economic and financial variables.

The micro-simulation model, using data on wages and consumer expenditure, is used to

evaluate the distribution impact of tax and tariff measures on Italian households.

CER's reports are available to subscribers as are presentations and workshops on the reports

organised and sponsored by CER and attended to by experts and leading personalities

and policy makers.

Centro Europa Ricerche S.r.l.

Via G. Carissimi, 41 - 00198 Roma

Tel. (0039) 06 8081304

E-mail: [email protected]

www.centroeuroparicerche.it

Presidente Onorario: Giorgio Ruffolo

Presidente: Vladimiro Giacché

Vicepresidenti: Claudio Levorato, Gennaro Mariconda

Direttore della ricerca: Stefano Fantacone

Comitato scientifico: Paolo Guerrieri Paleotti (presidente), Barbara Annicchiarico, Pierluigi Ciocca,

Stefan Collignon, Gianluca Cubadda, Giuseppe De Arcangelis, Flavio Delbono, Francesco Ferrante,

Giovanni Ferri, Luca Fiorito, Sergio Ginebri, Paolo Giordani, Anna Giunta, Pasquale Lelio Iapadre, Mas-

similiano Marzo, Valentina Meliciani, Salvatore Nisticò, Antonio Pedone, Andrea Cesare Resti, Gio-

vanna Vallanti

Rapporto CER: pubblicazione periodica a carattere economico. Anno XXXV

Direttore responsabile: Jacopo Tondelli

Iscrizione n. 59/2016 del 5 aprile 2016 del Registro della Stampa del Tribunale di Roma

Proprietario della testata: Centro Europa Ricerche S.r.l.

C.C.I.A.A. Roma: R.E.A. 480286

Edizione: Centro Europa Ricerche S.r.l.

Printed out at CER – May, 2018

Re- invent ing Europe

The fol lowing authors have contributed to this report: Stefan Col l ignon,

Stefano Fantacone, Antonio Forte, Chiara Guerel lo.

R A P P O R T O C E R

5 5

Executive summary 7

The return of economic growth in Europe

11

UNEMPLOYMENT 13

PRODUCTIVITY GAPS 15

WAGE COST COMPETITIVENESS 17

Box 1. Non-TFP growth and output-gap 20

Policy mix

21

THE INTERACTION OF MONETARY AND FISCAL POLICY 21

MONETARY POLICY 25

FISCAL POLICY 28

EMPIRICAL EVIDENCE ON THE INTERACTION OF MONETARY AND FISCAL POLICY 32

Box 2. Fiscal-monetary policy mix in theory 36

Box 3. The ECB unconventional monetary stance 38

Box 4. Glossary for fiscal policy terms 39

European Fiscal Union

41

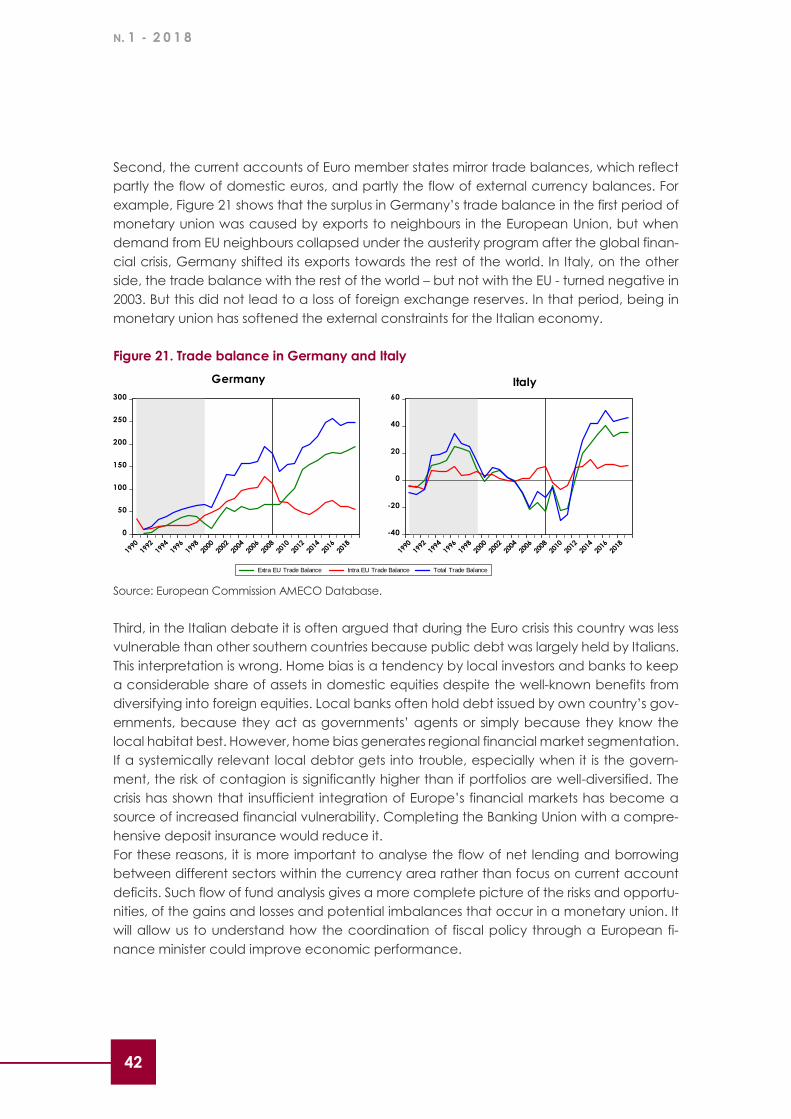

FISCAL POLICY COORDINATION IN THE EURO AREA 41

THE FLOW OF FUNDS ANALYSIS 43

Box 5. The current debate on fiscal spill-overs in the Euro Area 50

Towards a European Fiscal Union

51

THE EUROPEAN UNION BUDGET 52

A EUROPEAN FISCAL UNION FOR MACROECONOMIC STABILITY 55

References

57

R A P P O R T O C E R

7 7

Executive summary

President Macron has called for the re-invention of Europe. “Faced with the great chal-

lenges of our times, such as defence and security, great migrations, development, climate

change, the digital revolution and regulation of a globalized economy”, he asked, “have

European countries found means to defend their interests and values, and to guarantee

and adapt their democratic and social model that is unique worldwide? Can they address

each of these challenges alone? We cannot afford to keep the same policies, the same

habits, the same procedures and the same budget. No more can we choose to turn in-

wards within national borders. The only way to ensure our future, is the rebuilding of a sov-

ereign, united and democratic Europe” (1).

This year’s Rapporto Europa will focus on the economic context for re-inventing European

model. We give particular attention to the details of a European Fiscal Union. The Maas-

tricht Treaty did not incorporate any form of Fiscal Union, except in the very narrow sense

of fiscal discipline: each member state committed to maintain sound finances and the

Stability and Growth Pact (SGP) detailed the operationalisation of fiscal discipline. A com-

mon European budget exists, but it is small and has no specific functions for the Euro Area.

The Euro crisis has revealed that this institutional set-up is not optimal.

In June 2015, the so-called Five Presidents’ Report noted that “all mature Monetary Unions

have put in place a common macroeconomic stabilisation function to better deal with

shocks that cannot be managed at the national level alone” (p. 14). It proposed a “fiscal

union” that would “improve the cushioning of large macroeconomic shocks and thereby

make EMU over all more resilient” (p.14) (2).

Since then, many improvements have happened:

1. By the European Semester of economic policy coordination has been given clearer

guidance for the Euro Area as a whole and a stronger focus on social aspects.

2. European Fiscal Boards and National Productivity Boards have been set up.

3. Technical assistance to Member States was boosted with the creation of the Structural

Reform Support Service.

4. Important steps towards completing the Banking Union and Capital Markets Union

have been taken, notably by advancing in parallel on risk-reduction and risk-sharing

measures in the banking sector.

(1) http://www.elysee.fr/assets/Initiative-for-Europe-a-sovereign-united-democratic-Europe-Emmanuel-

Macron.pdf

(2) Juncker J‐C., D. Tusk, J. Dijsselbloem, M. Draghi and M. Schulz (2015): Completing Europe’s Economic

and Monetary Union, Five Presidents’ Report, 22 June. https://ec.europa.eu/commission/publica-

tions/five-presidents-report-completing-europes-economic-and-monetary-union_en

N. 1 - 2 0 1 8

8

In December 2017, the European Commission has presented new proposals and initiatives

that echoed President Macron’s discourse and Commission President Junker’s State of the

Union speech:

1. A European Monetary Fund (EMF) is to safeguard the financial stability of the Euro

Area, as well as the financial stability of the 'participating member states'

2. The so-called Fiscal compact (Treaty on Stability, Coordination and Governance) is to

be integrated into the Union legal framework, taking into account the appropriate

flexibility.

3. New budgetary instruments for the Euro Area are to be developed within the Union

framework.

4. For the period 2018-2020, EU funds will be mobilised in support of national reforms and

the Structural Reform Support Programme is to be strengthened.

5. Finally, reflection has started whether the Euro Area needs a European Minister of

Economy and Finance.

The interaction between sovereign member states’ fiscal policy and the unified monetary

policy is not optimal in the European Monetary Union (EMU). Therefore, the European Cen-

tral Bank is overcharged and the policy mix in the Euro Area has been suboptimal for a

long time. We believe that a European Fiscal Union will help to improve the policy mix and,

therefore, the long run development of the member states in the Euro Area. We develop

the analysis in this year’s Rapporto Europa starting from an overview of the main develop-

ments of the Euro Area economies. We then look at the economic governance of the Euro

Area, especially the coordination of fiscal policy between member states and the interac-

tion with monetary policy.

Economic activity is now well above the previous peak attained in 2008: it is 7.5% higher in

the Euro Area as a whole. Not only actual, but also potential output growth has improved

since the ECB has started its unconventional monetary policy in 2012. While this was a nec-

essary policy response to the crisis, the situation now calls for a cautious normalization of

monetary policy and a careful evaluation of fiscal policy.

The closing of the output gaps may explain why potential output is improving again across

Europe. Although the impact of closing the output gap on non-TFP growth differentials is

small, the indirect effect that output gaps exert on potential output growth through the

growth of factors of production is large. However, as the gaps disappear, one must con-

sider that in the long-run economic growth is determined by total factor productivity (TFP).

For stagnating countries like Italy, the challenge does not so much consist in stimulating the

economy, which could of course contribute to an increase in the use of capital and labour,

but more importantly structural reforms are urgently needed to improve the efficiency of

resource use and raise TFP. This is also necessary in order to improve competitiveness and

raise the purchasing power of wages.

R A P P O R T O C E R

9 9

Between 2011 and 2014, fiscal consolidation made the policy mix excessively tight; after

2014, monetary policy has contributed to a significant softening (real long-term interest

rates fell), but fiscal policy remained stuck at an aggregated cyclically adjusted deficit of

-1%. This aggregate development is not fully reflected in the levels of individual member

states’ real long-term interest rates: while in Italy nominal interest rates strongly declined,

the deflationary pressures shrank the gap between nominal and real interest rates, but in

Germany this gap widened, driving real interest rates into negative territory for several

years. The divergence in the real long-term interest rates’ dynamic observed in the last

years might be attributable to country-specific policy, and in particular to heterogeneous

fiscal stance. Before the crisis the relationship between long-term interest rate and the fiscal

stance was linear and negative across the countries, but during the crises and even more

recently this relationship has become highly non-linear.

We show that the government budget position does not explain the output gap, nor is the

volatility in government budgets affected by output gap volatility over the medium run. By

contrast, monetary policy is highly significant, confirming the excessive burden for

monetary policy in the European policy mix. However, monetary policy affects real long

run interest rates in the short-run, although in the medium run their dynamics depends also

on government budget positions. This highlights that the effectiveness of monetary policy

is highly dependent on the fiscal policy stance in shaping the dynamic of the long-run rate.

Since fiscal policies are heterogenous among the countries, the effectiveness of monetary

policy in stimulating the economy is highly uneven across countries.

Fiscal policies by member states are not neutral in the European monetary union, because

the changes of fiscal stances will generate spillover effects in neighbouring member states.

Our estimations suggest that signs and dimensions of spillovers are strongly hetoregeneous

among member countries so that a different form of fiscal policies coordination within the

Euro Area, defined by a strategic interaction between member countries on the timing of

consolidation, would be preferable to just a common set of rules, which might induce all

countries to consolidate at the same moment, making austerity unsustainable. However,

since the cross-country heterogeneity of attitude towards a joint consolidation across

country is a matter of fact, supranational coordination by means of a European Minister of

Finance might mediate this position, increasing the sustainability of fiscal consolidation in

Europe.

The budget of the European Union pays for policies carried out at the European level. The

total budget amounted to € 136 bln in 2016, which is less than 1% of gross national income

(GNI) of the European Union. Of this amount, € 117.9 bln are spend inside the EU but only €

77.2 bln in the Euro Area. There are therefore good reasons for increasing the budget for

the monetary union, as President Macron has demanded.

The experience has proven that the voluntary cooperation among the EU member states

is no longer sufficient to generate and allocate European public goods efficiently. Instead

N. 1 - 2 0 1 8

10

of intergovernmental cooperation, it may be a better solution to provide certain public

goods by a federal agency, which is acting on the basis of competing legislation. With

these elements, a re-invented European Union would be able to keep its founding promise:

namely to preserve peace, increase welfare and bring people together.

R A P P O R T O C E R

11 11

The return of economic growth in Europe

After a decade of economic recession, stagnation and crisis, Europe has finally returned

to solid economic growth. The recovery is part of a worldwide trend (IMF, 2018). Global

output has grown by 3.7% in 2017, and global growth forecasts for 2018 and 2019 have

been revised upward to 3.9%. The pickup in growth is broad-based, reflecting also upside

surprises in Europe and Asia and the expected impact of the recently approved U.S. tax

policy changes.

Economic activity, measured by GDP at constant prices, is now well above the previous

peak attained in 2008: it is 7.5% higher in the Euro Area as a whole. Contrary to the short-

lived export led economic revival in 2011, the present European recovery is fed by domes-

tic demand and has spread across countries and sectors. Figure 1 shows in the left panel

that in the Euro Area output is getting close to its potential and in the right panel that the

output gap has closed. This means that the recessionary tendencies and deflationary risks

are subsiding, while there are still no excessive demand pressures which could ignite a

wage-price inflation. The right-hand panel in Figure 1 also shows that not only actual, but

also potential output growth has improved since the European Central Bank has started its

unconventional monetary policy in 2012. While this was a necessary policy response to the

crisis, the situation now calls for a cautious normalization of monetary policy and a careful

evaluation of fiscal policy. However, the recent economic progress is not equally distrib-

uted. In Germany, GDP is 13.4% above its 2008 level, in France 8.6%, in Spain 4.3%, but it is

still -3.2% below that level in Italy and even -23.0% in Greece.

Figure 1. Economic activity and growth in the Euro Area

Source: European Commission AMECO database.

5000

5500

6000

6500

7000

7500

8000

8500

9000

9500

10000

10500

2000 2002 2004 2006 2008 2010 2012 2014 2016

-4

-2

0

2

4

6

8

Euro Area

Output Gap Real GDP Potential GDP

2000 2002 2004 2006 2008 2010 2012 2014 2016

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Euro Area

Real GDP Growth Rate Potential GDP Growth Rate

N. 1 - 2 0 1 8

12

Figure 2 shows that Germany quickly closed the output gap after 2009, but potential

growth only improved after 2012, the year of aggressive monetary loosening. In France,

the output gap is still negative and potential output growth has nearly halved from 2% in

2000 to 1.2% in 2018, although the tendency is rising again. In Italy, the situation is far worse.

The output gap has been nearly double of France, and potential growth has been nega-

tive in every year from 2009 to 2016. In 2017 it turned positive with 0.3%. Thus, Italian living

conditions have deteriorated in absolute and relative terms. Nevertheless, Spain is an ex-

ample that not all of the South is doom and gloom: the output gap was larger than in Italy,

but potential output is now growing again and with 2.3% this is faster than in 2008. The worst

case is Greece, where the output gap is still large and potential output still falling.

Figure 2. Economic activity and growth in selected Member States

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

2000 2002 2004 2006 2008 2010 2012 2014 2016

-6

-4

-2

0

2

4

6

Germany

Output Gap Real GDP Potential GDP

2000 2002 2004 2006 2008 2010 2012 2014 2016

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Germany

Real GDP Growth Rate Potential GDP Growth Rate

1000

1200

1400

1600

1800

2000

2200

2000 2002 2004 2006 2008 2010 2012 2014 2016

-4

-2

0

2

4

6

8

France

Output Gap Real GDP Potential GDP

2000 2002 2004 2006 2008 2010 2012 2014 2016

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

France

Real GDP Growth Rate Potential GDP Growth Rate

1000

1100

1200

1300

1400

1500

1600

1700

2000 2002 2004 2006 2008 2010 2012 2014 2016

-6

-4

-2

0

2

4

6

Italy

Output Gap Real GDP Potential GDP

2000 2002 2004 2006 2008 2010 2012 2014 2016

-6%

-4%

-2%

0%

2%

4%

6%

Italy

Real GDP Growth Rate Potential GDP Growth Rate

R A P P O R T O C E R

13 13

cont. Figure 2. Economic activity and growth in selected Member States

Source: European Commission AMECO database.

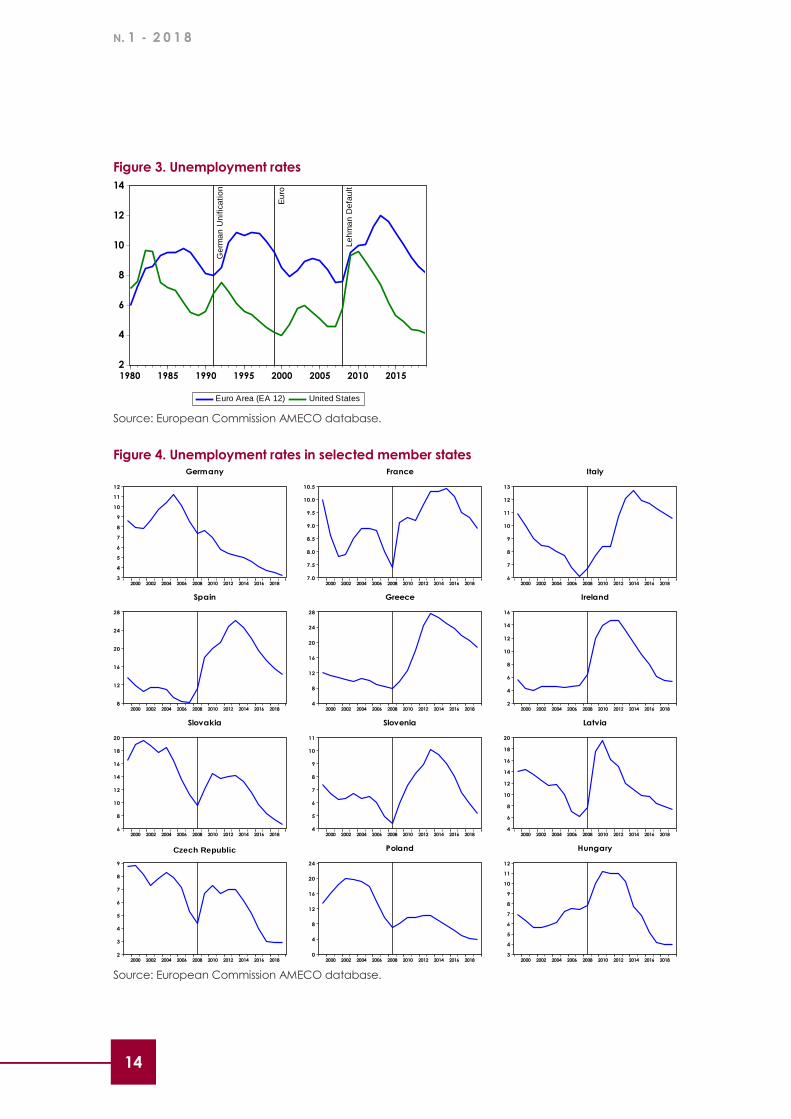

UNEMPLOYMENT

Unemployment is also coming down in Europe, although more slowly than in the US where

it is now at 4.3% - the lowest level since 2000 and the second lowest since 1970. As shown

in Figure 3, in the Euro Area, unemployment stood at 8.6% in 2018, still higher than at the

beginning of the Global Financial Crisis (7.5%), but below the level (9.7%) when monetary

union started in 1999. Thus, despite the severe crisis, it would be hard to argue that Europe

was better off without the euro.

Labour markets are improving in all member states (in the core as well as in the southern

periphery), although the levels are still diverging widely (see Figure 4). In Germany unem-

ployment stands at 3.5% of the labour force, in Ireland it has fallen from a peak of 14.5 to

5.5% and in Spain from 25.1 to 15.6%. Even in Greece, unemployment rates have come

down from 27.5 to 20.6%. Progress is slowest in Italy (10.9% down from 12.7%– still far above

the 6.8% before the crisis) and France (9.3% down from 10.4%). In the new member states,

unemployment rates stand between 7.7% (Latvia, Slovakia) and 2.9% (Czech Republic),

but in all Eastern member states they have come down by more than one half.

400

600

800

1000

1200

2000 2002 2004 2006 2008 2010 2012 2014 2016

-10

-5

0

5

10

15

Spain

Output Gap Real GDP Potential GDP

2000 2002 2004 2006 2008 2010 2012 2014 2016

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Spain

Real GDP Growth Rate Potential GDP Growth Rate

0

50

100

150

200

250

2000 2002 2004 2006 2008 2010 2012 2014 2016

-18

-9

0

9

18

27

Greece

Output Gap Real GDP Potential GDP

2000 2002 2004 2006 2008 2010 2012 2014 2016

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Greece

Real GDP Growth Rate Potential GDP Growth Rate

N. 1 - 2 0 1 8

14

Figure 3. Unemployment rates

Source: European Commission AMECO database.

Figure 4. Unemployment rates in selected member states

Source: European Commission AMECO database.

2

4

6

8

10

12

14

1980 1985 1990 1995 2000 2005 2010 2015

Euro Area (EA 12) United States

Ge

rma

n U

nif

ica

tio

n

Eu

ro

Le

hm

an

De

fau

lt

3

4

5

6

7

8

9

10

11

12

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Germany

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

France

6

7

8

9

10

11

12

13

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Italy

8

12

16

20

24

28

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Spain

4

8

12

16

20

24

28

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Greece

2

4

6

8

10

12

14

16

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Ireland

6

8

10

12

14

16

18

20

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Slovakia

4

5

6

7

8

9

10

11

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Slovenia

4

6

8

10

12

14

16

18

20

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Latvia

2

3

4

5

6

7

8

9

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Czech Republic

0

4

8

12

16

20

24

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Poland

3

4

5

6

7

8

9

10

11

12

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Hungary

R A P P O R T O C E R

15 15

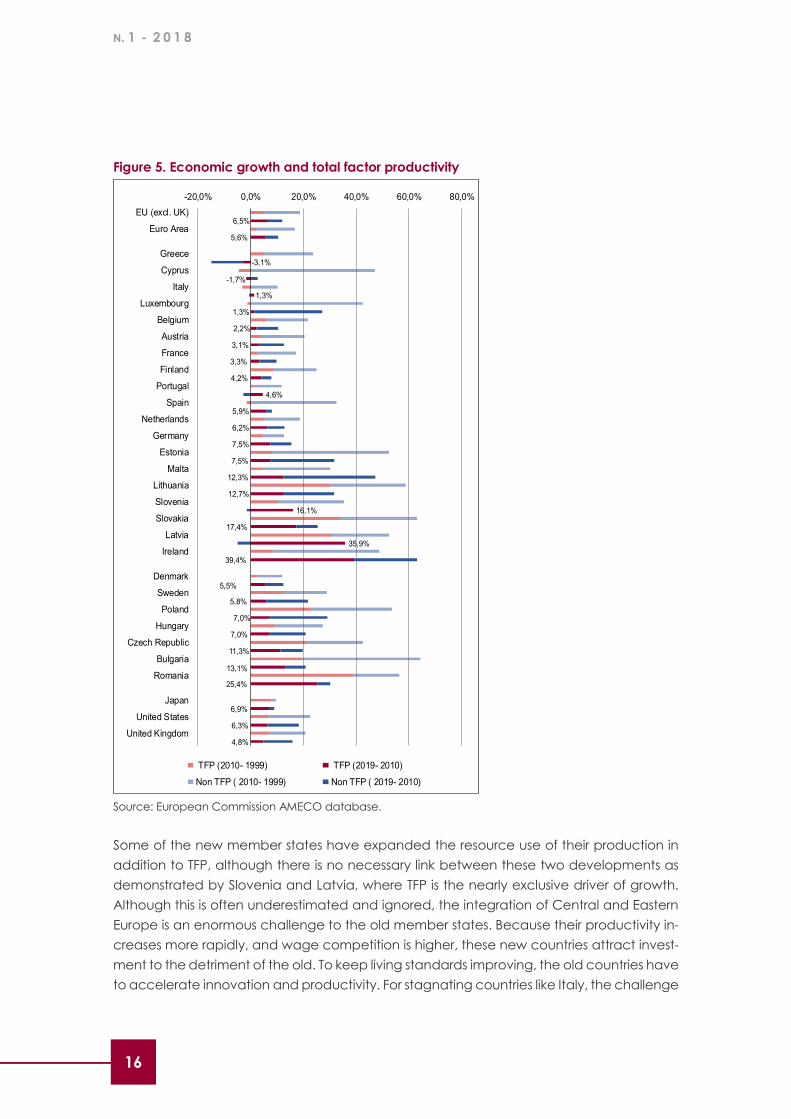

PRODUCTIVITY GAPS

In previous Rapporti, we have emphasized the lack of demand which has aggravated the

crisis. We presented evidence (notably in Rapporto Europa 2016) that the length and

depth of output gaps have an impact on investment and potential output. The closing of

the output gaps may explain why potential output is improving again across Europe (see

Box 1). However, as the gaps disappear, one must consider that output gap is only a short-

run measure of the effective demand, while in the long-run economic growth is deter-

mined by total factor productivity (TFP). A country’s standards of living depend upon

productivity (i.e. on the efficiency by which capital and labour are used in the production

process). Productivity determines income, wages, the capacity of fiscal space and, wel-

fare and social expenditure. The relative stagnation of TFP, hence, appears as a deteriora-

tion of living standards relative to other countries. This is a major source for Euroscepticism.

Figure 5 presents the cumulative effect of TFP in total economic growth. We distinguish the

first decade of monetary union (1999-2010) from the post-crisis period (2010-2018) and ob-

serve an extreme variety of performances between countries and over time. Not surpris-

ingly, overall growth was higher in the first decade in all countries, except in Ireland. For the

Euro Area in aggregate, the contribution of TFP and additional resource employment is

equally balanced. However, the contribution of TFP varies substantially between member

states.

On the one side, we find stagnating countries like Italy, where GDP grew by 7% between

2000 and 2010 (equivalent to 0.7% per year), and only by 0.8% between 2010 and 2018

(equivalent to 0.1% per year). In the early period, TFP fell by -3.3%, so that extensive growth

through expanding uses of factors of production was 10.3%. In other words, while the Italian

demand boom of the first decade put more people to work, their efficiency declined. Dur-

ing the crisis years, this has changed. Italian TFP has now improved by a meagre 1.3%

(equivalent to 0.16% per year), but the contribution of extensive use of labour and capital

has fallen by 0.5%, so that observed growth is only 0.8%. In comparison, French TFP has

increased by 3.3% since 2010, and German TFP by 7.5%. Extensive growth is more con-

strained in Germany, which may be a consequence of operating at full employment, and

this may have led to increased productivity.

On the other side, Ireland has dramatically improved its productivity since 2010 with TFP

improvements of 39.4%, equivalent to 4.2% per year. This performance is heavily influenced

by the Manufacturing and ICT sectors and in particular by FDI enterprises in these sectors.

However, the narrow base of enterprises in high value-added sectors (particularly in foreign

owned Pharma and ICT) disguises underperforming sectors and skews Ireland’s productiv-

ity level and growth rate (3). Similar discrepancies occur in the new member states in Cen-

tral and Eastern Europe. Finally, the new member states in Eastern Europe have also signif-

icantly improved total factor productivity (on average 17% since 2010, i.e. 2% per year),

which is the result of profound transformations in the formerly planned economies under So-

viet domination, but also of the sustained wage competitiveness (which we discuss below).

(3) See (Irish National Competitiveness Council, 2017.

N. 1 - 2 0 1 8

16

Figure 5. Economic growth and total factor productivity

Source: European Commission AMECO database.

Some of the new member states have expanded the resource use of their production in

addition to TFP, although there is no necessary link between these two developments as

demonstrated by Slovenia and Latvia, where TFP is the nearly exclusive driver of growth.

Although this is often underestimated and ignored, the integration of Central and Eastern

Europe is an enormous challenge to the old member states. Because their productivity in-

creases more rapidly, and wage competition is higher, these new countries attract invest-

ment to the detriment of the old. To keep living standards improving, the old countries have

to accelerate innovation and productivity. For stagnating countries like Italy, the challenge

6,5%

5,6%

-3,1%

-1,7%

1,3%

1,3%

2,2%

3,1%

3,3%

4,2%

4,6%

5,9%

6,2%

7,5%

7,5%

12,3%

12,7%

16,1%

17,4%

35,9%

39,4%

5,5%

5,8%

7,0%

7,0%

11,3%

13,1%

25,4%

6,9%

6,3%

4,8%

-20,0% 0,0% 20,0% 40,0% 60,0% 80,0%

EU (excl. UK)

Euro Area

Greece

Cyprus

Italy

Luxembourg

Belgium

Austria

France

Finland

Portugal

Spain

Netherlands

Germany

Estonia

Malta

Lithuania

Slovenia

Slovakia

Latvia

Ireland

Denmark

Sweden

Poland

Hungary

Czech Republic

Bulgaria

Romania

Japan

United States

United Kingdom

TFP (2010- 1999) TFP (2019- 2010)

Non TFP ( 2010- 1999) Non TFP ( 2019- 2010)

R A P P O R T O C E R

17 17

does not so much consist in stimulating the economy, which could of course contribute to

an increase in the use of capital and labour, but more importantly in improving the effi-

ciency of resource use and raise total factor productivity.

In the UK, productivity has slowed down. A major reason for this development is the uncer-

tainty for investors created by Brexit. A detailed study by the National Institute of Economic

and Social Research (Young, 2017) has shown that the UK’s standard of living are deterio-

rating because of higher cost of living due to the currency depreciation that weighs heavily

on the unemployed, single parents and pension holders. In addition, weak investment and

the delocalisation of businesses will have long run effects, which are already showing up

as a 20% reduction in the productivity trend.

WAGE COST COMPETITIVENESS

The unequal developments in productivity affect the competitiveness in the different re-

gions and member states of the Euro Area. In previous RAPPORTI, we have elaborated a

methodology for assessing the competitiveness of wage levels.

We have derived a benchmark wage level from the classic textbook assumption that equi-

librium in a single market would reflect equal returns on capital. Given the relative levels of

capital and labour productivity, we can derive from this assumption the equilibrium level

of wages at which this equal return would be realised. When the actual wage levels are

below the equilibrium, an economy is considered to be competitive, and inversely if actual

wages are higher, it lacks competitiveness. This means that the evolution of the equilibrium

wage is highly significant for the improvement of standards of living and this improvement

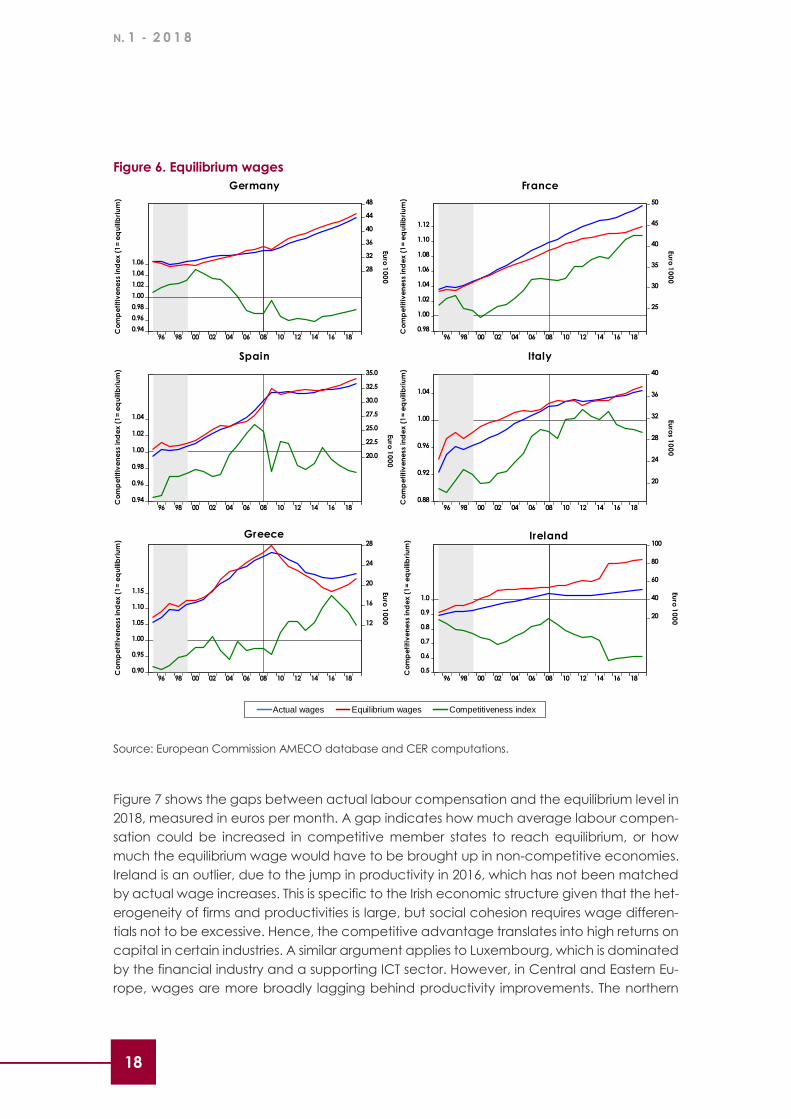

depends on the developments of productivity. Figure 6 shows the developments of actual

and equilibrium wages for selected Euro Area member states and Figure 7 shows the 2018

wage gaps for all member states in the European Union.

We find in Figure 6 that Germany has regained competitiveness since it undertook labour

market reforms in the mid-2000s, while France has persistently lost competitiveness with

wages today 10% above equilibrium. The loss was accelerated in 2015 when actual labour

compensation increased despite a stagnation in the equilibrium level. Since 2016 compet-

itiveness has improved in Italy and Spain. In Italy this seems to be the effect of the Job Act

of 2014-15. In Greece, the equilibrium wage has now started to rise after a sustained re-

duction before 2016, which was not compensated by the cuts in actual wage costs. In

Ireland, by contrast, we observe a significant leap in equilibrium wages, which is explained

by increases in productivity: “Across the OECD, labour productivity growth in manufactur-

ing has tended to outpace services sector growth. Between 2009 and 2015, Irish growth in

manufacturing was 16% compared with 3% in services and -2% in construction. Irish manu-

facturing productivity data has been significantly influenced by corporate restructuring

[…], including the relocation of firms with significant IP assets and aircraft leasing, [leading]

to noteworthy increases in labour productivity, particularly in 2015 (22.5%)” (Irish National

Competitiveness Council, 2017, pp. 58-62).

N. 1 - 2 0 1 8

18

Figure 6. Equilibrium wages

Source: European Commission AMECO database and CER computations.

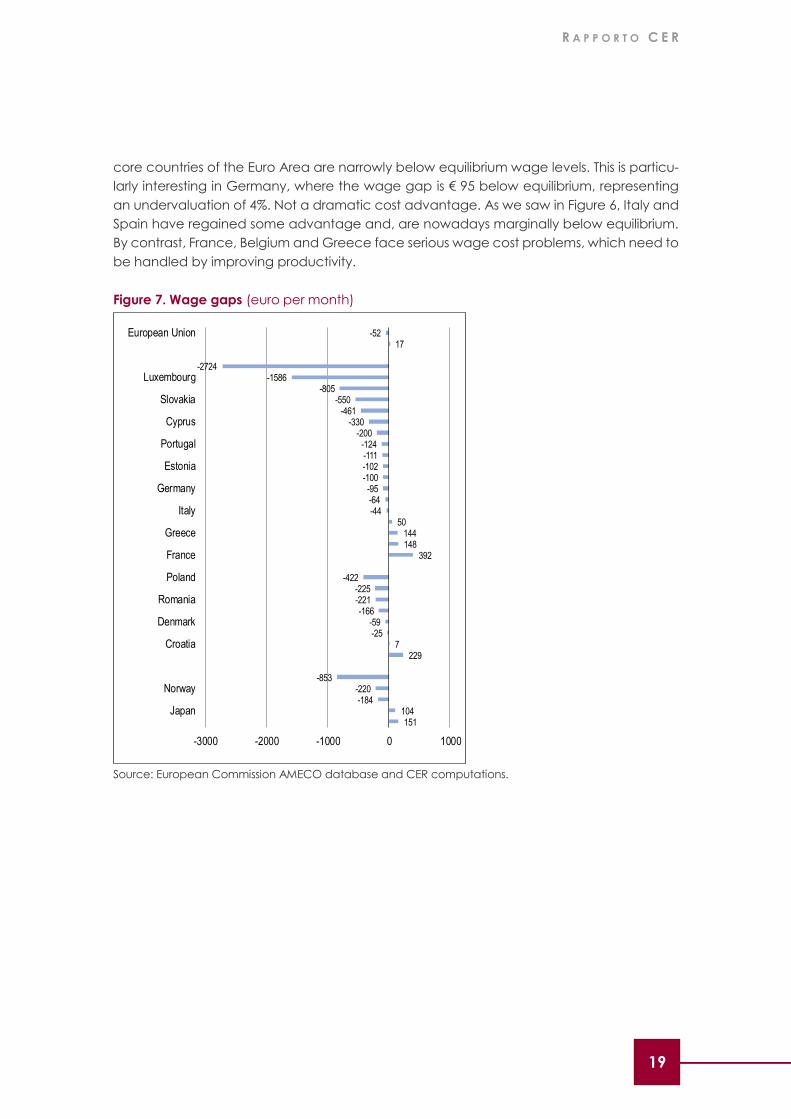

Figure 7 shows the gaps between actual labour compensation and the equilibrium level in

2018, measured in euros per month. A gap indicates how much average labour compen-

sation could be increased in competitive member states to reach equilibrium, or how

much the equilibrium wage would have to be brought up in non-competitive economies.

Ireland is an outlier, due to the jump in productivity in 2016, which has not been matched

by actual wage increases. This is specific to the Irish economic structure given that the het-

erogeneity of firms and productivities is large, but social cohesion requires wage differen-

tials not to be excessive. Hence, the competitive advantage translates into high returns on

capital in certain industries. A similar argument applies to Luxembourg, which is dominated

by the financial industry and a supporting ICT sector. However, in Central and Eastern Eu-

rope, wages are more broadly lagging behind productivity improvements. The northern

0.94

0.96

0.98

1.00

1.02

1.04

1.0628

32

36

40

44

48

96 98 00 02 04 06 08 10 12 14 16 18

Germany

Eu

ro 1

00

0

Co

mp

eti

tiv

en

ess in

de

x (

1=

eq

uili

bri

um

)

0.98

1.00

1.02

1.04

1.06

1.08

1.10

1.12

25

30

35

40

45

50

96 98 00 02 04 06 08 10 12 14 16 18

France

Co

mp

eti

tiv

en

ess in

de

x (

1=

eq

uili

bri

um

)

Eu

ro 1

00

0

0.94

0.96

0.98

1.00

1.02

1.04

20.0

22.5

25.0

27.5

30.0

32.5

35.0

96 98 00 02 04 06 08 10 12 14 16 18

Co

mp

eti

tiv

en

ess

ind

ex

(1

= e

qu

ilib

riu

m)

Spain

0.88

0.92

0.96

1.00

1.04

20

24

28

32

36

40

96 98 00 02 04 06 08 10 12 14 16 18

Italy

Co

mp

eti

tiv

en

ess

ind

ex

(1

= e

qu

ilib

riu

m)

Euro

s 10

00

0.90

0.95

1.00

1.05

1.10

1.15

12

16

20

24

28

96 98 00 02 04 06 08 10 12 14 16 18

Co

mp

eti

tiv

en

ess

ind

ex

(1

= e

qu

ilib

riu

m)

Euro

10

00

Greece

0.5

0.6

0.7

0.8

0.9

1.0

20

40

60

80

100

96 98 00 02 04 06 08 10 12 14 16 18

Act ual w ages Equilibrium wages Comet it iveness index

Ireland

Co

mp

eti

tiv

en

ess

ind

ex

(1

= e

qu

ilib

riu

m)

Euro

10

00

Euro

10

00

0

50

100

150

200

250

300

Titolo del grafico

Actual wages Equilibrium wages Competitiveness index

R A P P O R T O C E R

19 19

core countries of the Euro Area are narrowly below equilibrium wage levels. This is particu-

larly interesting in Germany, where the wage gap is € 95 below equilibrium, representing

an undervaluation of 4%. Not a dramatic cost advantage. As we saw in Figure 6, Italy and

Spain have regained some advantage and, are nowadays marginally below equilibrium.

By contrast, France, Belgium and Greece face serious wage cost problems, which need to

be handled by improving productivity.

Figure 7. Wage gaps (euro per month)

Source: European Commission AMECO database and CER computations.

-5217

-2724-1586

-805-550

-461-330

-200-124-111-102-100-95-64-44

50144148

392

-422-225-221-166

-59-25

7229

-853-220-184

104151

-3000 -2000 -1000 0 1000

European Union

Luxembourg

Slovakia

Cyprus

Portugal

Estonia

Germany

Italy

Greece

France

Poland

Romania

Denmark

Croatia

Norway

Japan

N. 1 - 2 0 1 8

20

BOX 1. NON-TFP GROWTH AND OUTPUT GAP

Total factor productivity is measured by mean of a modelized production function, where output

(GDP in constant prices) is produced by capital and labour. Hence, output increases when more

capital and more workers are employed. However, with technological progress, the same amount

of labour and capital will be able to produce more. TFP is the residual growth that is not explained by

larger amounts of production factors.

We have first performed a panel analysis to assess whether increasing output gaps boosts non-TFP

growth, namely the economic growth due to change in factors of production and not in productivity.

We employ the common correlated effects estimator of Chudik e Pesaran (2015) a panel of 30 coun-

tries (Europe and US) for the period 1996-2019. We estimate so the correlation of the distance be-

tween country-specific non-TFP growth and the cross-countries average (csa), and output gaps. The

pooled estimates of the model are:

Eq. 1 𝑛𝑜𝑛𝑇𝐹𝑃𝑖,𝑡 = 0.09 𝑛𝑜𝑛𝑇𝐹𝑃𝑖,𝑡−1 + 0.09 𝑜𝑢𝑡𝑝𝑢𝑡𝑔𝑎𝑝𝑖,𝑡−1 + 0.95 𝑛𝑜𝑛𝑇𝐹𝑃_𝑐𝑠𝑎𝑡 + 𝜀𝑖,𝑡

We find a very strong cross-country dependence as shown by the high correlation with the aggre-

gate European non-TFP growth (cross-country average): the elasticity is 95%. This means that country-

specific factors play only a marginal role in determining the divergence of non-TFP from the European

trend. On average a 1% reduction of negative output gaps drives an increase of 9 basis points in the

non-TFP growth rates, over and above the European stance. However, although the dynamics of

non-TFP growth is highly interconnected, only in few countries does the distance of a single country’s

non-TFP growth to the European trend significantly respond to the output gaps of that country. Typi-

cally, large open economies, like US, Germany, France, Italy and Spain, show a positive correlation

between non-TFP growth and national output gap. For few other smaller economies, the same sig-

nificant association holds: Bulgaria, Denmark and Portugal inside the EU and, also, Switzerland.

Although the impact of closing the output gap on non-TFP growth differentials is small, the indirect

effect that output gaps exert on potential output growth through the growth of factors of production

is large. To show this stylized fact, we regressed the growth of real potential output on its determinants

(TFP and non-TFP growth rates), disentangling the non-TFP growth differentials due to increasing out-

put gap (𝑛𝑜𝑛𝑇𝐹𝑃̂𝑖,𝑡, the predicted values from Eq. 1) from the residual components 𝜀𝑖,𝑡 (inclusive of

the European average). The estimates are as follows:

Eq. 2 𝑃𝑜𝑡𝑒𝑛𝑡𝑖𝑎𝑙 𝑂𝑢𝑡𝑝𝑢𝑡 𝐺𝑟𝑜𝑤𝑡ℎ𝑖,𝑡 = 0.21 𝑇𝐹𝑃𝑖,𝑡−1 + 0.28 𝑛𝑜𝑛𝑇𝐹𝑃̂𝑖,𝑡−1 +

+0.38( 𝑛𝑜𝑛𝑇𝐹𝑃_𝑐𝑠𝑎𝑡−1 + 𝜀𝑖,𝑡−1) + 0.83 𝑃𝑜𝑡𝑒𝑛𝑡𝑖𝑎𝑙 𝑂𝑢𝑡𝑝𝑢𝑡 𝐺𝑟𝑜𝑤𝑡ℎ_𝑐𝑠𝑎𝑡 + 𝜐𝑖,𝑡

We observe that country-specific non-TFP growth due to changes in output gaps explains the diver-

gence of potential output growth from European trend as much as TFP growth does.

R A P P O R T O C E R

21 21

Policy mix

While long-run standards of living depend on productivity and supply side conditions, the

management of aggregate demand generates incentives for private investment and

growth. If these incentives are sustained over time, productivity and potential output will

rise. This is why a stability oriented macroeconomic policy framework is crucial for the per-

formance of the Euro Area economy. However, if different regions and sectors of produc-

tion respond with different elasticities to demand impulses, economic growth will diverge,

generating inequalities which might cause political backlashes. This is an important argu-

ment in favour of more coordinated economic policies in Europe.

The Euro Area has a unique set of policy rules and institutions, which makes policy coordi-

nation difficult. Monetary policy is centralized by the independent European Central Bank,

while fiscal and economic policy is decentralized in the hands of sovereign member states,

which are, however, constrained by a set of rules such as the Stability and Growth Pact

and the new Fiscal Compact. These rules do not apply to the same extend to member

states outside the Euro Area. However, experience of the Euro crisis has shown that the

interaction between monetary policy and fiscal policy, i.e. the policy mix, has not been

satisfactory. Fiscal policy was excessively rigid, while the European Central Bank has done

its utmost to save the euro and stimulate the euro economy. This sub-optimal performance,

which risks undermining the credibility of the ECB, has been widely recognized. It has given

rise to calls for a European Fiscal Union. Before analysing the effects of fiscal policy in detail,

we will first discuss the experience of the policy mix during the crisis.

THE INTERACTION OF MONETARY AND FISCAL POLICY

About the interaction of monetary and fiscal policies there is an abundance of literature

(4). Monetary policy refers to the central bank’s control of the availability of credit in the

economy to achieve the broad objectives of economic policy. Fiscal policy refers to the

government’s choice regarding the use of taxation and public spending to regulate the

aggregate level of economic activity. This is also called the stabilisation function of public

finance. Its purpose is to avoid excess demand pressures, which would cause inflation, and

lack of aggregate demand which would cause recessions and unemployment. Thus, the

output gap is a good proxy for measuring whether the stability objective is attained.

Because total public expenditure in the Euro Area is around 45% of GDP, the role of public

spending is of prime importance for the performance of aggregate demand. Yet, given

the independence of sovereign member states, each government can decide its own

budget, so that the aggregate budget position for the Euro Area is the random outcome

of national decisions. This means fiscal policy cannot be used as a policy instrument, and

as a consequence the full burden of managing the macroeconomic conditions in the Euro

Area falls on the European Central Bank. However, while the ECB can respond to an ag-

(4) For a review see (Hilbers, 2005) and (Fores, 2018).

N. 1 - 2 0 1 8

22

gregate shock to the Euro Area as a whole, it does not have instruments to manage asym-

metric shocks which translate into unequal output gaps between member states.

This is true for all integrated monetary economies, but in traditional nation states govern-

ments can use public finances to avoid or correct excessive deviations. Of course, eco-

nomic liberals are opposed to the interference by governments in the market, because

they believe the “invisible hand of the market” mechanism will restore equilibrium. How-

ever, our analysis of wage competitiveness shows that this adjustment process may take

longer than is politically acceptable. The populist alternative is to exit monetary union and

the single market. However, even if it were possible to do so without serious welfare losses

(which is not true) (5), this does not solve the fundamental economic problem in any inte-

grated currency union. Because substantial economic heterogeneities prevail, logically

northern Italy should also break away from monetary union with the Mezzogiorno, West

Germany from East Germany, Catalonia from Spain, and Flanders from Wallonia. Robert

Mundell, who was awarded the Nobel Prize for his work on optimum currency areas, has

therefore always argued that monetary union is a political project and not an economic

optimum. But this implies that a well-working monetary union requires a fiscal union with

additional policy tools and ultimately also a political union.

Thus, although monetary and fiscal policy are implemented by different bodies, these pol-

icies are far from independent. As explained in Box 2, a change in one will influence the

effectiveness of the other and thereby the overall impact of any policy change. Finding

the right policy mix is not always easy, but in the European Monetary Union the difficulty is

compounded by the fact that there is no federal authority to determine the aggregate

fiscal policy stance for the Euro Area.

Figure 9 gives an idea of the policy trade-off in the Euro Area. We have proxied monetary

policy by the long run real interest rates and fiscal policy by the cyclically adjusted struc-

tural deficits. The regression line, which stands for our efficiency line in Figure B2.1 of Box 2,

indicates that the long run real interest at balanced budgets would be 1.9%, which - in

“normal times” and given the inflation target of the ECB - is equivalent to a nominal long-

term rate of 3.9%. Given the historic record, this seems reasonable (see Figure 11).

Defining an optimal policy mix in the Euro Area poses a problem, because the aggregate

budget position which corresponds to the unified monetary policy stance is the sum of

different national government positions. Each national government has its own welfare

function and chooses its budget position in response to its national constituency. But if each

country is allowed to set its fiscal policy stance independently of the others, the conse-

quence will be that high deficits in some countries would push interest rates up for member

states with low deficits. Hence, national fiscal policies create externalities for all citizens in the

Euro Area. The resultant policy mix cannot be optimal. On the other hand, imposing a unique

policy stance for every government would create welfare losses because the policy prefer-

ences resulting from different welfare functions would be overwritten by the unique policy

rule. The Stability and Growth Pact effectively imposes a balanced budget at point E of Fig-

ure B2.1, where the indifference curve does not correspond with the policy preference of R.

(5) The National Institute (Young, 2017) has estimated that the first 18 months since the Brexit vote have

created costs “worth over £600 per annum to the average household” in the UK.

R A P P O R T O C E R

23 23

Figure 9. Policy mix in the Euro Area

Source: European Commission AMECO database.

The problem is partly economic, partly political. It is economic if the response of the eco-

nomic system to a fiscal deficit is significantly different from the Euro Area average. There

is evidence, discussed below, that the single currency has endogenously generated con-

vergence to a more unified economic response. However, as shown in Box 2, the political

problem remains unsolved, for example, at the balanced budget point E (Figure B2.1),

countries with a preference for point R remain on a lower level of utility. In a federal de-

mocracy the policy mix is chosen by all citizens through the democratic procedures of

electing a government. This means, there is only one collectively chosen welfare function,

which represents a democratic consensus. The point where such indifference curve

touches the efficiency line would therefore correspond to a welfare optimum. For exam-

ple, in the American context of the 1980s, the point R (for Republican) reflected the Volker-

Reagan policy mix, while the point E was closer to the Clinton Greenspan policy mix of the

1990s. In the European Union, where sovereign nation states are in command, such collec-

tive choice is not possible, and this undermines the perception of welfare gains in monetary

union. To overcome this problem, it would be desirable to find a form of policy coordina-

tion, which allows, on the one hand, the designation of a collective fiscal position that cor-

responds to the integrated monetary policy, and, on the other hand, that enables citizens’

representation in the conduct of fiscal policy. This would be the European equivalent of

the American slogan: “no taxation without representation”.

The most remarkable feature in Figure 9 is the complete absence of fiscal policy during the

Euro crisis. Fiscal consolidation between 2011 and 2014 made the policy mix excessively

tight: the points for those years are well above the equilibrium line. Finally, after 2014, mon-

etary policy contributed to a significant softening (real long-term interest rates fell verti-

cally), but fiscal policy remained stuck at an aggregated cyclically adjusted deficit of -1%.

No doubt, this was due to the fact that fiscal policy in the Euro Area is constrained by the

Stability and Growth Pact and the Fiscal Compact, which impose the identical rule of bal-

ancing cyclically adjusted deficits. We shall discuss this further below. Furthermore, in recent

years, budget positions have been quite heterogeneous across member states, while the

long-term interest rates had a tendency to decline. Figure 10 indicates the spread of na-

tional long- term interest rates in relation to the national deviation from the Euro Area fiscal

2010

2011

2012

2013

2014

2015

2016

y = -0,8631x - 0,1872R² = 0,7444

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

-4,5 -4,0 -3,5 -3,0 -2,5 -2,0 -1,5 -1,0 -0,5 0,0

Rea

l Lon

g-Te

rm In

tere

ts R

ate

Structural Government Balance (% of potential GDP)

N. 1 - 2 0 1 8

24

stance. The scatterplot shows country-specific cyclically adjusted government budgets net

of interest (i.e. the distance from EA average) and the associated 10-year government

bond yield (distance from EA average) as the mean through the period 1999-2008 or 2009-

2017.

Figure 10. Correlation between fiscal stance and long-term interest rates

Source: European Commission AMECO database and ECB statistical data warehouse (SDW).

Before the financial crisis and the European sovereign crisis the relationship between long-

term interest rate and the fiscal stance was linear and negative. That means that if a

country under-consolidates (primary fiscal deficit higher than the Euro Area average), then

it would have paid a positive spread between the country’s long-term interest rate and the

Euro average one. This mechanism was called the market discipline, and it worked even if

it did not prevent the Euro crisis. By contrast, during the crises and even more recently this

relationship has become highly non-linear. This seems to be the result of the emergence of

four clusters. The spread of long-term interest rates over the average Euro rate was

negative for countries with fiscal consolidation, with the exception of Italy and Greece

(Greece being a large outlier, the data are not shown). These two countries have the

highest debt-GDP ratios in Europe and this explains why long-term bond yields contain

significant risk permia, so that even the strong fiscal consolidation does not bring the spread

down. However, another explanation would be that excessive austerity is

counterproductive because it increases market worries and uncertainty. This interpretation

is supported by the two other clusters in Figure 10. In Portugal, Cyprus, Latvia, and Lithuania

interest spreads remain high against a moderate fiscal losening. But in Spain, Slovakia,

Slovenia and France, the fiscal expansion goes together with a fall of long-term rates below

the Euro average, which makes sense if markets expect that the looser fiscal stance will

generate growth. Nevertheless, from the point of view of the Euro Area one could also

argue that this last cluster is free riding on the consolidation efforts by Germany, Luxemburg

and Italy.

BE

DE

FR

LV

LT

LU

MT

NLAT

SI

SK

FI

ES IT

CY

PT

BEDE IEES

FR

ITCYLV

LT

LU

MTNLAT

PT

SI

SK

y = 0,3135x3 - 0,4454x2 - 1,2962xR² = 0,4249

y = 0,0296x2 - 0,2722xR² = 0,4914

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

-4,0 -3,0 -2,0 -1,0 0,0 1,0 2,0 3,0 4,0 5,0 6,0

Lo

ng

-te

rm In

tere

st R

ate

(M

S-E

A)

Fiscal Stance (MS-EA)

2009-2017 1999-2008 Trend (09-17) Trend (99-08)

R A P P O R T O C E R

25 25

MONETARY POLICY

Monetary policy has saved the euro. During the crisis the European Central Bank has re-

mained “the only game in town” for stabilizing the Euro economy. The rigid rules of the

Stability and Growth Pact and governments’ concern with consolidating deficits (which

was very different from the policy mix in the United States) has put an unprecedented onus

on monetary policy to support aggregate demand. The ECB has responded to this chal-

lenge by acting decisively to secure price stability in the face of an unparalleled economic

and financial crisis. However, experience after nearly one decade of monetary policy has

revealed that unconventional monetary policy loses efficiency over time. Thus, it is clear

the central bank cannot remain the only game in town indefinitely. This requires further

structural and institutional reforms in order to improve the policy mix for the Euro Area as a

whole and to ensure balanced growth for member states. With the closing of output-gaps

the time has now come to exit the unconventionally loose monetary policies.

Monetary policy during the crisis has gradually softened as economic conditions deterio-

rated. This development is not fully reflected in the levels of real long-term interest rates

shown in Figure 11. In fact, when the room for negative short-run rates is constrained, other

unconventional measures had to supplement nominal long-term rate cuts. In a liquidity

trap, when the nominal short-run interest rate approaches the zero-lower-bound (in Figure

11 this is summarized by the grey areas indicating when the rate are below 1%), the effec-

tiveness of monetary policy sharply declines. In this case, the central bank can control nei-

ther the dynamic of the long-term interest rate nor inflation and runs the risk of de-anchor-

ing inflation expectations from the 2% target.

In most of the advanced economies, central banks continue to exert some control over

inflation, mostly by relying on forward guidance, namely the promise to keep the short-term

nominal rate to very low values for longer than necessary. They are thereby generating

inflation expectations at longer-term horizons. However, they have also attempted to cut

long-term interest rates by means of unconventional monetary policy (see Box 3). However,

while these policies were initially very effective in deeply troubled financial markets, they

have lost their power over the real long-term rate during the last few years. In 2015, real

long-term interest rates increased and eventually turned positive even though nominal

rates fell, because the inflation rate became negative in most countries. Nowadays, only

Germany and Sweden are facing negative real interest rates. In Germany, this phenome-

non is mostly attributable to very low (zero) long-term nominal interest rates coupled with

rising prices, while in Sweden it is a consequence of the ultra-loose monetary policy driving

the nominal short-term rates into negative territories as well. In Eastern European countries

with local currency, all interest rates were generally higher than in the Euro Area.

Outside the Euro Area most of the difference in the long-term interest rates is reflected in

the exchange rates dynamic, reported in Figure 12. For instance, after the Brexit vote (2016-

2017), sterling strongly depreciated against the Euro, and real interest rates in the UK en-

tered negative territories, although short-term interest rates were kept constant, or even

increased in the later quarters of 2017. However, within the European Monetary Union, the

divergence in the real long-term interest rates’ dynamic observed in the last years might

be attributable to country-specific policy, and in particular to heterogeneous fiscal stance.

N. 1 - 2 0 1 8

26

Figure 11. Long-term and short-term interest rates

Source: ECB Statistical Data Warehouse (SDW) and European Commission AMECO database.

Figure 12. Exchange rates against the Euro (% deviation from long run trend)

Source: ECB Statistical Data Warehouse (SDW).

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Polish zloty Swedish krona UK pound sterling US dollar

R A P P O R T O C E R

27 27

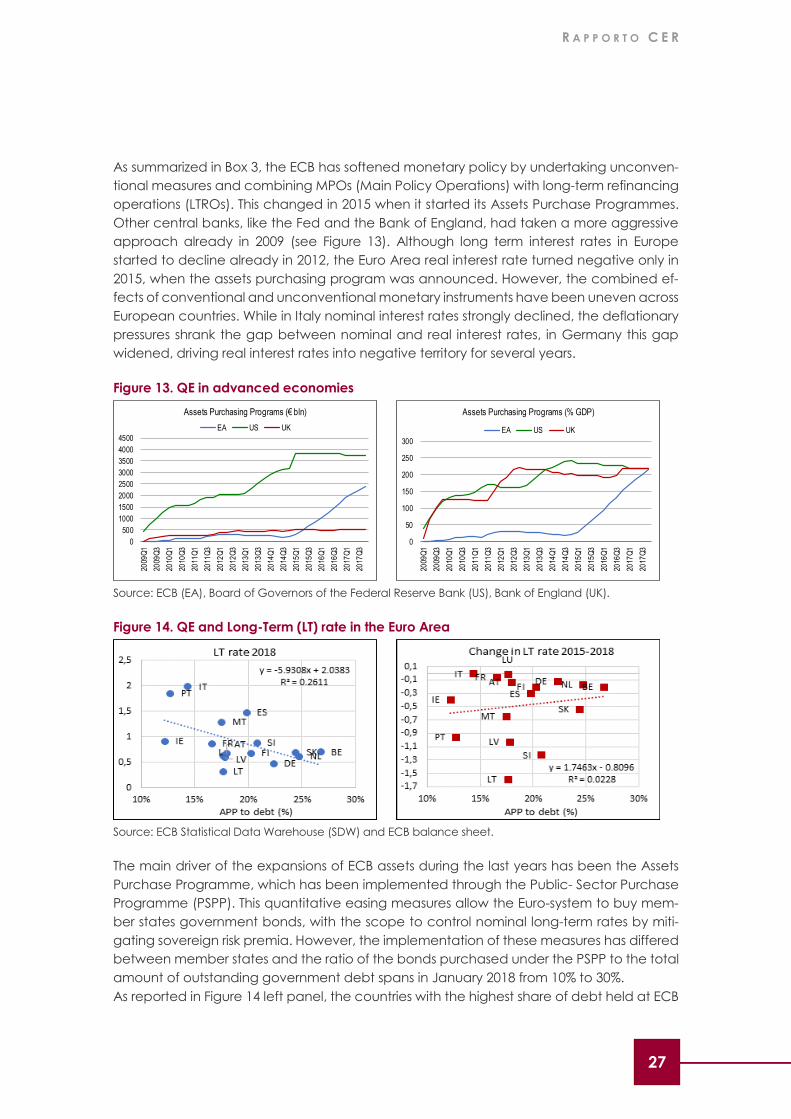

As summarized in Box 3, the ECB has softened monetary policy by undertaking unconven-

tional measures and combining MPOs (Main Policy Operations) with long-term refinancing

operations (LTROs). This changed in 2015 when it started its Assets Purchase Programmes.

Other central banks, like the Fed and the Bank of England, had taken a more aggressive

approach already in 2009 (see Figure 13). Although long term interest rates in Europe

started to decline already in 2012, the Euro Area real interest rate turned negative only in

2015, when the assets purchasing program was announced. However, the combined ef-

fects of conventional and unconventional monetary instruments have been uneven across

European countries. While in Italy nominal interest rates strongly declined, the deflationary

pressures shrank the gap between nominal and real interest rates, in Germany this gap

widened, driving real interest rates into negative territory for several years.

Figure 13. QE in advanced economies

Source: ECB (EA), Board of Governors of the Federal Reserve Bank (US), Bank of England (UK).

Figure 14. QE and Long-Term (LT) rate in the Euro Area

Source: ECB Statistical Data Warehouse (SDW) and ECB balance sheet.

The main driver of the expansions of ECB assets during the last years has been the Assets

Purchase Programme, which has been implemented through the Public- Sector Purchase

Programme (PSPP). This quantitative easing measures allow the Euro-system to buy mem-

ber states government bonds, with the scope to control nominal long-term rates by miti-

gating sovereign risk premia. However, the implementation of these measures has differed

between member states and the ratio of the bonds purchased under the PSPP to the total

amount of outstanding government debt spans in January 2018 from 10% to 30%.

As reported in Figure 14 left panel, the countries with the highest share of debt held at ECB

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2009

Q1

2009

Q3

2010

Q1

2010

Q3

2011

Q1

2011

Q3

2012

Q1

2012

Q3

2013

Q1

2013

Q3

2014

Q1

2014

Q3

2015

Q1

2015

Q3

2016

Q1

2016

Q3

2017

Q1

2017

Q3

Assets Purchasing Programs (€ bln)

EA US UK

0

50

100

150

200

250

300

2009

Q1

2009

Q3

2010

Q1

2010

Q3

2011

Q1

2011

Q3

2012

Q1

2012

Q3

2013

Q1

2013

Q3

2014

Q1

2014

Q3

2015

Q1

2015

Q3

2016

Q1

2016

Q3

2017

Q1

2017

Q3

Assets Purchasing Programs (% GDP)

EA US UK

N. 1 - 2 0 1 8

28

(cumulated net acquisition of bonds) at beginning of 2018, are typically the countries with

the lowest nominal long term-interest rate today. However, if we contrast the acquisition of

assets under the PSPP and the change in the long-term rate between 2015 and today, the

effect of the QE has been quite uneven. In several countries with relative large scale PSPP,

like Netherlands and Belgium, the change in the long-term rate before and after the im-

plementation of the policy measure has been almost null. For some others, like Italy, the

relatively smaller PSPP is reflected in even smaller changes in the long-term interest rate.

Actually, interest rates started declining in 2012 and most of the drop in the long-run rate

was motivated to the signalling effects of the “whatever it takes” speech of ECB president

Mario Draghi in 2012.

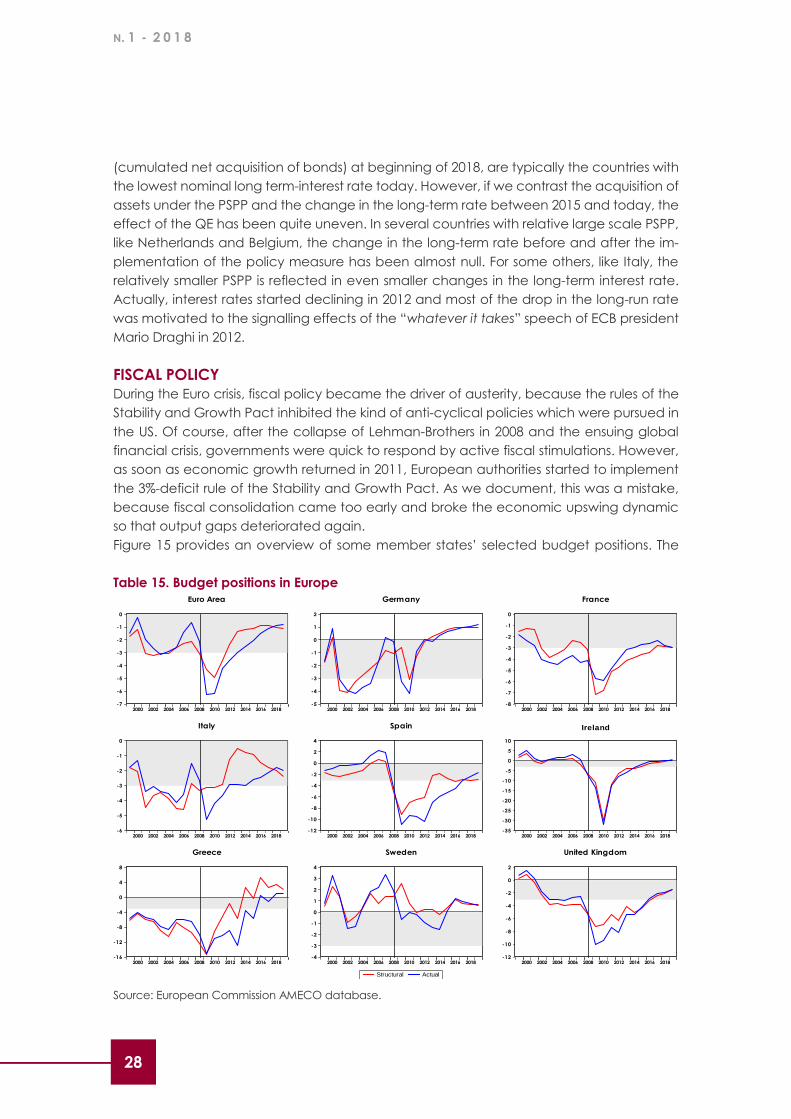

FISCAL POLICY

During the Euro crisis, fiscal policy became the driver of austerity, because the rules of the

Stability and Growth Pact inhibited the kind of anti-cyclical policies which were pursued in

the US. Of course, after the collapse of Lehman-Brothers in 2008 and the ensuing global

financial crisis, governments were quick to respond by active fiscal stimulations. However,

as soon as economic growth returned in 2011, European authorities started to implement

the 3%-deficit rule of the Stability and Growth Pact. As we document, this was a mistake,

because fiscal consolidation came too early and broke the economic upswing dynamic

so that output gaps deteriorated again.

Figure 15 provides an overview of some member states’ selected budget positions. The

Table 15. Budget positions in Europe

Source: European Commission AMECO database.

-7

-6

-5

-4

-3

-2

-1

0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Euro Area

-5

-4

-3

-2

-1

0

1

2

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Germany

-8

-7

-6

-5

-4

-3

-2

-1

0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

France

-6

-5

-4

-3

-2

-1

0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Italy

-12

-10

-8

-6

-4

-2

0

2

4

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Spain

-35

-30

-25

-20

-15

-10

-5

0

5

10

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Ireland

-16

-12

-8

-4

0

4

8

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Greece

-4

-3

-2

-1

0

1

2

3

4

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Structural Actual

Sweden

-12

-10

-8

-6

-4

-2

0

2

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

United Kingdom

R A P P O R T O C E R

29 29

Euro Area operated in a rage of budget deficits between zero and -3% of GDP before the

crisis; immediately after the Lehman Brothers bankruptcy the actual deficit fell below 6%,

but consolidation after 2010 was steady and sharp. The rising gap between the structural

and actual deficit after 2012 is an indicator of the excessively tight fiscal consolidation in

the Euro Area. See Box 4 for an explanation of the terms used in this report. The policies

pursued by individual member states vary significantly. Germany only marginally overshot

the 3% deficit criterion in 2010 and moved into a structural and actual budget surplus after

2014. But most Euro Area members remained significantly below the 3% deficit ratio.

France, Spain and Greece only got there in 2017. In Italy fiscal consolidation was radical

in 2011-13, because financial markets where close to a melt-down, given the high debt-

GDP ratio. Outside the Euro Area some countries like Sweden also consolidated their budg-

ets and generated surpluses, while others like the UK used fiscal policy to stimulate demand

during the crisis.

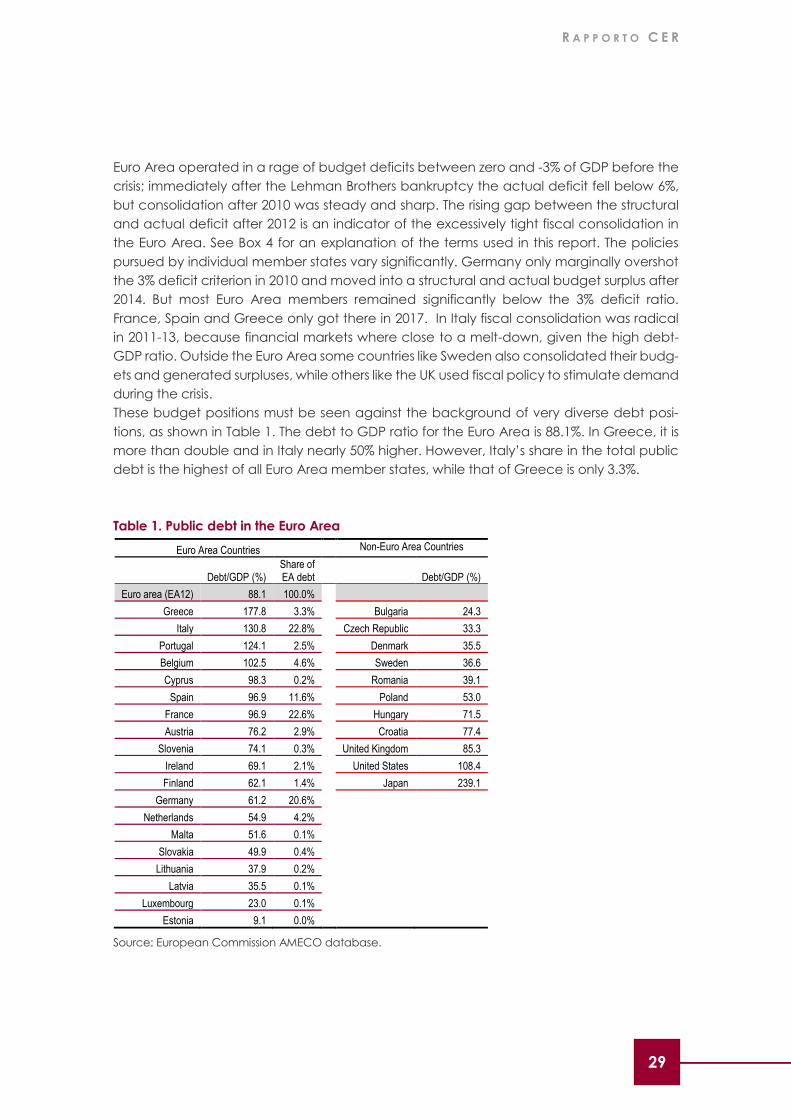

These budget positions must be seen against the background of very diverse debt posi-

tions, as shown in Table 1. The debt to GDP ratio for the Euro Area is 88.1%. In Greece, it is

more than double and in Italy nearly 50% higher. However, Italy’s share in the total public

debt is the highest of all Euro Area member states, while that of Greece is only 3.3%.

Table 1. Public debt in the Euro Area

Source: European Commission AMECO database.

Euro Area Countries Non-Euro Area Countries

Debt/GDP (%) Share of EA debt

Debt/GDP (%)

Euro area (EA12) 88.1 100.0%

Greece 177.8 3.3% Bulgaria 24.3

Italy 130.8 22.8% Czech Republic 33.3

Portugal 124.1 2.5% Denmark 35.5

Belgium 102.5 4.6% Sweden 36.6

Cyprus 98.3 0.2% Romania 39.1

Spain 96.9 11.6% Poland 53.0

France 96.9 22.6% Hungary 71.5

Austria 76.2 2.9% Croatia 77.4

Slovenia 74.1 0.3% United Kingdom 85.3

Ireland 69.1 2.1% United States 108.4

Finland 62.1 1.4% Japan 239.1

Germany 61.2 20.6%

Netherlands 54.9 4.2%

Malta 51.6 0.1%

Slovakia 49.9 0.4%

Lithuania 37.9 0.2%

Latvia 35.5 0.1%

Luxembourg 23.0 0.1%

Estonia 9.1 0.0%

N. 1 - 2 0 1 8

30

Figure 16. Annual Standard Deviation of budget positions

Source: European Commission AMECO database and CER computations.

Despite the constraining fiscal rules, budget positions have been more volatile in the Euro

Area during the crisis then outside. Figure 16 shows that the cross-country standard devia-

tion of actual budget deficits within the EMU has been significantly higher between 2008

and 2014 than in the Non-Euro Area countries. However, the standard deviation of the

structural deficits has been in excess of the Non-Euro Area only immediately after the Leh-

man-Brothers bankruptcy and in the depth of the Euro-crisis.

The excessively tight fiscal stance, especially between 2011 and 2014, is also documented

by Figure 17. The premature tightening is clear from the movements of the fiscal stance

Figure 17. Euro Area fiscal stance

1

2

3

4

5

6

7

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Le

hm

an

De

fau

lt

Structural Budget Position

1

2

3

4

5

6

7

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Euro Area St. Dev . Non-Euro Area St. Dev .

Le

hm

an

De

fau

lt

Actual Budget Position

R A P P O R T O C E R

31 31

cont. Figure 17. Euro Area fiscal stance

Source: European Commission AMECO database and CER computations.

between 2009 and 2011. Only in 2015-16 did the Euro Area take a weak anti-cyclical and

stimulating position that is now turning into pro-cyclical loosening. This was different in Non-

Euro Area member states, which generally followed anti-cyclical policies.

The fiscal policy stance is measured by the variation of the cyclically adjusted structural

deficit net of interest rates. The Euro Area’s restrictive policy stance reflected the require-

ments in Germany, where – take in isolation - the relatively expansive boom would have

justified anti-cyclical tightening in 2011 and in 2012 (see Figure 12 and Figure 17), but it did

not take into consideration the more adverse conditions in some of the other Euro Area

economies. The alternating policy mix in Greece between tightening and loosening re-

flects the confused approach to the sovereign debt crisis in Greece. It is, however, interest-

ing that the policy mix in the Non-Euro Area countries was generally more anti-cyclical and

the fiscal policy stance was more stable: changes in the cyclically adjusted primary budget

20072008

20092010

2011

2012

2013

2014

2015

2016

2017

2018

2019

y = -0.1622x - 0.3699R² = 0.0778

-6

-4

-2

0

2

4

6

8

10

-20 -15 -10 -5 0 5 10

Tit

le

Title

Greece

anticyclical tightening

anticyclical losening

procyclical tightening

procyclical losening

N. 1 - 2 0 1 8

32

position varied between +1.6 and -1.4 percentage points, but in the out-countries only be-

tween +1.03 and -0.96 points. Thus, fiscal policy was actually more active in the Euro Area

than outside, but the crisis was also deeper here.

EMPIRICAL EVIDENCE ON THE INTERACTION OF MONETARY AND FISCAL POLICY

We will now investigate the relationship between fiscal policy and monetary policy. We

quantify the direct impact of monetary policy by a change in the short-run interest rate or

in the stock of assets held by the ECB (two proxies for conventional and unconventional

monetary stance) and fiscal policy by a change in the fiscal stance. We also look at the

indirect impact transmitted by the business cycle (measured by the output gap) on these

monetary variables. We also consider the loopback response of monetary policy to the

effects of the fiscal reaction. For this purpose, we have constructed a Panel VAR model,

estimating contemporaneously the correlation between the fiscal stance, the output gap,

short-term money market rates, 10-year government bond yields and the change in ECB

assets. The model has the form:

Eq. 3 𝒚𝒊,𝒕 = 𝜌𝒚𝒊,𝒕−𝟏 + 𝛽𝒙𝒕 + 𝛼𝑖 + 𝜀𝑖,𝑡

Where 𝒚𝒊,𝒕 is a vector composed (in order) of the output gaps (AMECO), the cyclically ad-

justed government surplus/deficits net of interests as a percentage of GDP (AMECO), the

Euro Area 3-months money market rate (Eurostat) and the long-run interest rates as the 10-

year government bond yields (Eurostat). Furthermore, the eventuality of common factors

affecting both the European business-cycle is collected by including in 𝒙𝒕 the first three lags

of the cross-sectional average of the output gaps (6). In order to capture the heterogeneity

between member states (MS), we look at MS output gaps and fiscal position as the differ-

ence from the aggregate Euro Area (EA) values by including the cross-sectional average

fiscal stance in 𝒙𝒕.

We ran the estimates for the full monetary union period 1998-2017 and the coefficients

represent the average elasticities across the 18 Euro Area countries (Estonia excl.)

considered. The variables named MS are the deviation of each member state from the

integrated Euro Area performance. We catch the average cross-country heterogeneity in

the business cycle and in the fiscal policy stance, which are due to structural differences,

by estimating the fixed effects of the VAR model. However, the model does not tell us much

about the heterogeneity in the elasticities between countries. Despite this limitation, we are

able to distinguish between country-specific and aggregate Euro Area shocks. Hence, the

coefficient for the (lagged) member state (MS) budget reflects the average elasticity of

individual countries and the Euro Area (EA) government budget indicates the change in

the dependent variables due to the aggregate fiscal policy stance of the Euro Area. For

instance, an increase in a member state’s government deficit may be due to a national

policy of increasing public expenditure or it may be induced by more flexible fiscal rules at

the European level (say because the Stability Pact is less strictly applied).

Figure 18 reports the contribution of fiscal and monetary policy to the forecasted volatility

(6) This method, proposed by (Chudik & Pesaran, 2015) allows to consider implicitly the cross-states depend-

ence of output gaps due to business cycle synchronization.

R A P P O R T O C E R

33 33

of selected variables; Figure 19 shows the Impulse Response Functions (IRF) after a negative

shock to the short term interest rate or after an improvement in the fiscal stance. Those

results jointly show how the output gap, fiscal policy and monetary policy (i.e. short and

long term interst rates) respond to the various shocks.

Figure 18. Fiscal and monetary policy contribution to the volatility of selected variables

Source: ECB Statistical Data Warehouse (SDW), EC AMECO database and CER computations.

Figure 19. Panel VAR on the monetary and fiscal policy mix in the Euro Area

IRFs to a shock to either the short-term rate (-1 p.p.) or to the government surplus-to-GDP (+1 p.p.)

Source: European Commission AMECO database and CER computations.

0%

5%

10%

15%

20%

25%

30%

35%

40%

Output

Gap

ECB

assets

Long-term

rate

Short-term

rate

Gov.

Budget

Output

Gap

ECB

assets

Long-term

rate

Short-term

rate

Gov.

Budget

2-year 5-year

FE

VD

Response Varibale and time horizon

Output Gap ECB assets Long-term rate Short-term rate Gov. Budget

0,00

0,10

0,20

0,30

0,40

0,50

0,60

0,70

0,80

0,90

1,00

0 1 2 3 4 5

Output Gap

Short-Term Interest Rate Government Surplus/Deficit

-1,20

-1,00

-0,80

-0,60

-0,40

-0,20

0,00

0,20

0,40

0 1 2 3 4 5

Short-Term Interest Rate

Short-Term Interest Rate Government Surplus/Deficit

-0,35

-0,30

-0,25

-0,20

-0,15

-0,10

-0,05

0,00

0 1 2 3 4 5

Long-Term Interest Rate

Short-Term Interest Rate Government Surplus/Deficit

-0,20

0,00

0,20

0,40

0,60

0,80

1,00

1,20

0 1 2 3 4 5

Government Surplus/Deficit

Short-Term Interest Rate Government Surplus/Deficit

N. 1 - 2 0 1 8

34

We start with the determinants of the forecasted volatility of selected variables in Figure 18.

The output gap is not explained by the government budget position, nor is the government

budget volatility affected by output gap volatility in the medium run. We interpret this as a

sign for the inconsistent fiscal policy stances shown in Figure 17. Hence, better policy

coordination would improve the economic performance of the Euro Area. Furthermore,

monetary policy is highly significant. The contribution to output gap volatility by short-term

interest rate changes, which are controlled by the ECB, is larger than for long-term rates;

the impact by unconventional monetary policy measures, which have expanded the ECB

balance sheet, is even stronger. This confirms the excessive burden for monetary policy in

the European policy mix.

Furthermore, we turn to the analysis of the dynamic response to either a monetary or a

fiscal policy shock. We start by looking at the impact on the output gap in the top-left panel

of Figure 19. First of all, we observe that output gaps respond quickly to monetary policy,

but are rather persistent in the long run. The response to a fiscal policy shock is slow and

weak. Another striking result, although not reported here, is that it is positively correlated

with the aggregate output gap of the Euro Area. This clearly means that by improving the

policy mix for the Euro Area as a whole, the economic conditions in each member state

will improve. This is an important argument in favour of better macroeconomic policy

coordination at the European level.

Second, this latter result is confirmed by the dynamics of the member states fiscal stance

after a monetary shock, because fiscal policy does not respond to monetary policy,

supporting the view that fiscal stance is an independent and autonomous decision.

Third, monetary policy (proxied by short-term interest rate) responds weakly to country-

specific conditions, as shown in Figure 19, but strongly to the Euro Area aggregate fiscal

stance. Hence, monetary policy does not respond to fiscal policy in member states, but in

fact, the ECB lowers short-term rates exclusively in response to fiscal consolidation in the

aggregate Euro Area stance while increases them when the output gap turns positive and