r muralidharan senior director in the tax practice of deloitte of gs… · 25/05/2015 · topic:...

TRANSCRIPT

Topic: Impact of GST on Services

Proposed Rules and its Impact

R Muralidharan

Senior Director in the Tax Practice of Deloitte

Soumya R

Product Expert, SAP Labs India

GST India Forum

Impact on service sector

R Muralidharan

May 18, 2015

2

Agenda

• Service Sector – Current State of Play

• Paving way for GST – Improvements in Tax Structure

• GST – Tax structure for Services

• GST – Broad impact on Service Sector

• Potential Implications – Place of Supply Rules

• Proactive Approach for GST

© 2015 Deloitte Touche Tohmatsu India Private Limited 3

Service Sector – Current State of Play

© 2015 Deloitte Touche Tohmatsu India Private Limited 4

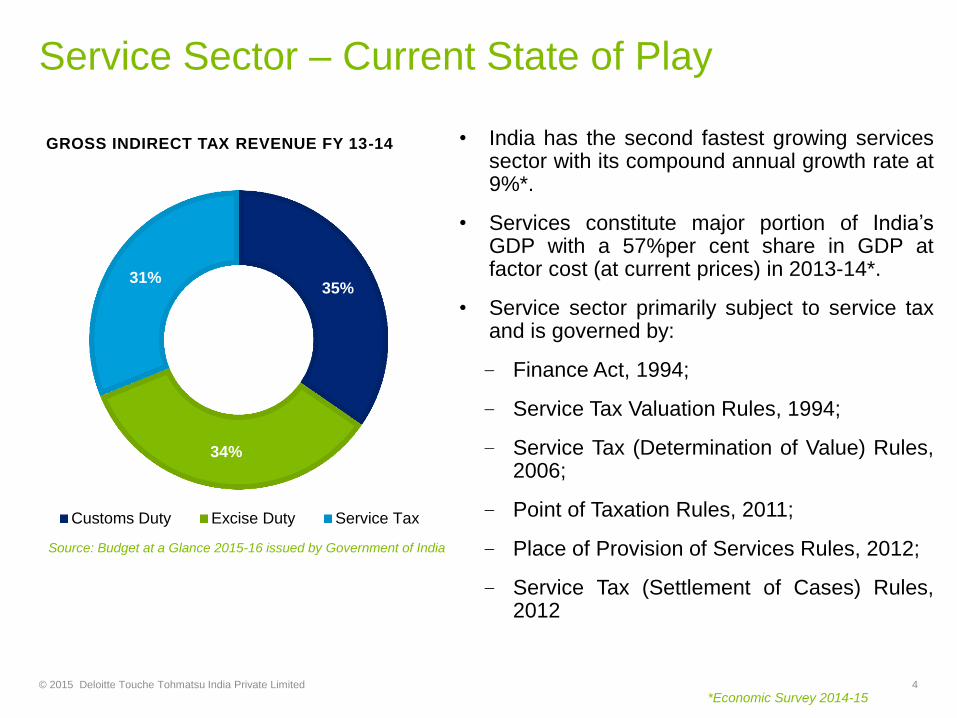

• India has the second fastest growing services sector with its compound annual growth rate at 9%*.

• Services constitute major portion of India’s GDP with a 57%per cent share in GDP at factor cost (at current prices) in 2013-14*.

• Service sector primarily subject to service tax and is governed by:

– Finance Act, 1994;

– Service Tax Valuation Rules, 1994;

– Service Tax (Determination of Value) Rules, 2006;

– Point of Taxation Rules, 2011;

– Place of Provision of Services Rules, 2012;

– Service Tax (Settlement of Cases) Rules, 2012

Source: Budget at a Glance 2015-16 issued by Government of India

35%

34%

31%

GROSS INDIRECT TAX REVENUE FY 13-14

Customs Duty Excise Duty Service Tax

*Economic Survey 2014-15

Paving way for GST – Improvements in Tax

Structure

Over the past several years, significant progress has been made to improve the

service tax structure, broaden the base and rationalize the rates to pave way for

GST

© 2015 Deloitte Touché Tohmatsu India Private Limited 5

Substantial expansion of service tax base by introduction of negative list regime of service tax

Introduction of Place of Provision of Services, Rules 2012

Pruning of exemptions available under service tax

Increase in rate of service tax vide Budget 2015

GST – Tax structure for Services

© 2015 Deloitte Touché Tohmatsu India Private Limited 6

GS

T

Intra-State CGST

SGST

Inter-State IGST*

(CGST+SGST)

Imports IGST

Exports Proposed to be

zero rated

*Integrated GST (IGST) on imports and inter-state supplies of services in India

• In the current regime, taxable event is rendition of taxable service but in GST

regime, the taxable event will be supply of taxable services

• The current Place of Provision of Services will be replaced with the proposed

Draft Place of Supply of Goods and Services Rules

• Dual GST comprising Central GST and State GST to operate concurrently on

supply of services for consideration

• GST Tax Structure:

GST – Broad impact on Service Sector

7

Issues Impact

©2015 Deloitte Touche Tohmatsu India Private Limited

Availability of Input Tax Credits (VAT)

Double taxation on certain services – Rates are same

Abatement on value of services with a restriction on

taking of input tax credit in GST regime

Self assessment provisions to be replaced with regular

assessment

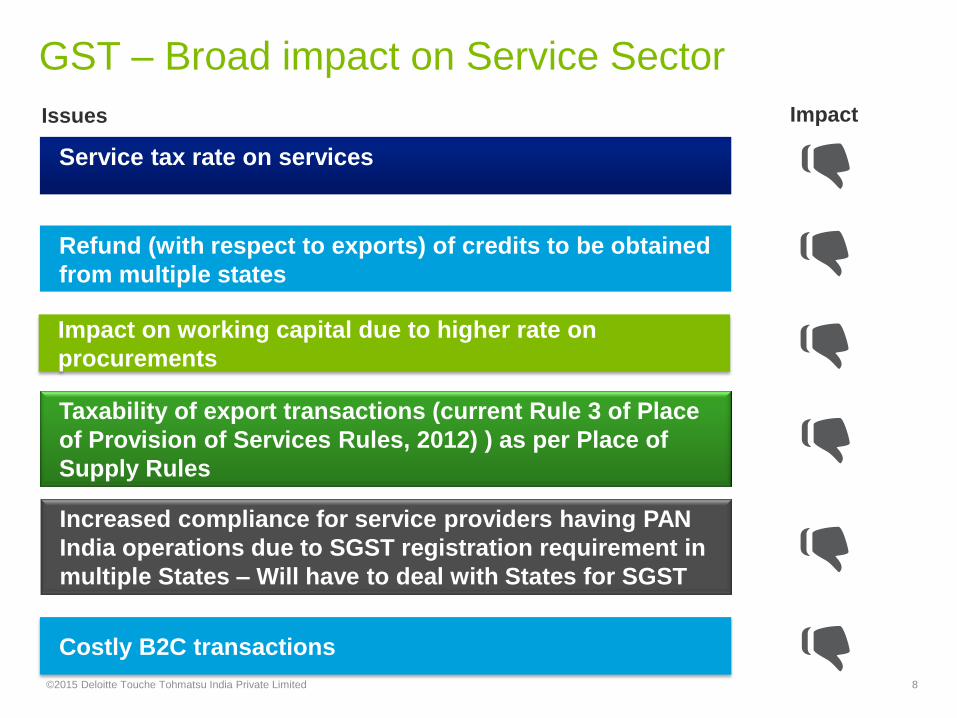

GST – Broad impact on Service Sector

8

Issues Impact

©2015 Deloitte Touche Tohmatsu India Private Limited

Increased compliance for service providers having PAN

India operations due to SGST registration requirement in

multiple States – Will have to deal with States for SGST

Impact on working capital due to higher rate on

procurements

Service tax rate on services

Refund (with respect to exports) of credits to be obtained

from multiple states

Taxability of export transactions (current Rule 3 of Place

of Provision of Services Rules, 2012) ) as per Place of

Supply Rules

Costly B2C transactions

Potential Implications

Place of Supply Rules

© 2015 Deloitte Touché Tohmatsu India Private Limited 9

Highlights of the proposed Place of Supply Rules

Export of services under Rule 4 of Place of Supply Rules???

Rule Nature of Service Description Place of Supply

3

Services (other than

specified services)

provided to a

registered person

Service receiver registered in one

State

Location of the

registered service

receiver

Service receiver registered in more

than one States

State where supply

is sought to be

billed

4

Services (other than

specified services)

provided to other

than a registered

person

NIL Location of service

provider

Deloitte Management

service ABC Inc, USA

Delhi USA ABC Inc is

not registered

and has no

BE in India

Proposed POS is Delhi Current POPS is USA

Potential Implications

Place of Supply Rules

© 2015 Deloitte Touché Tohmatsu India Private Limited 9

Proactive Approach for GST

Phases in transitioning to GST regime

© 2015 Deloitte Touché Tohmatsu India Private Limited 11

Overview Assessment:

• Overview assessment of different business functions and operations in order to be better prepared for transition

Impact Analysis:

• Identifying potential impact including quantification of impact, identifying affected business functions

Fine tuning of operations

• Validation & fine-tuning the business process and functions (i.e. finance, commercial, IT, accounting etc.)

Implementation:

• Assistance in transition to new regime to the impacted functions (i.e. finance, commercial, IT, accounting etc.)

R. Muralidharan

Senior Director

Delhi Office

Phone: +91 124 679 3608

Email: [email protected]

Senior Director

Contact Information

12 © 2015 Deloitte Touche Tohmatsu India Private Limited

Deloitte refers to on or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of

which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche

Tohmatsu Limited and its member firms

This material and the information contained herein prepared by Deloitte Touche Tohmatsu India Private Limited (DTTIPL) is intended to provide general

information on a particular subject or subjects and is not an exhaustive treatment of such subject(s). None of DTTIPL, Deloitte Touche Tohmatsu Limited,

its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this material, rendering professional advice or services. The

information is not intended to be relied upon as the sole basis for any decision which may affect you or your business. Before making any decision or

taking any action that might affect your personal finances or business, you should consult a qualified professional adviser.

No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this material.

©2015 Deloitte Touche Tohmatsu India Private Limited

Member of Deloitte Touche Tohmatsu Limited

13

Soumya R / Globalization Services / SAP Labs India

May 18, 2015

GST India Forum, New Delhi

SAP Solution for Services Current Scenario Vs. GST Scenario

Public

© 2015 SAP SE or an SAP affiliate company. All rights reserved. 15 Public

SAP Solution for Services Current Scenario Vs. GST Scenario

Topic Current Scenario GST Scenario

Registration Central Service tax

Registration number

• Central Registration +

• State registration for every

state that the service

provider operates in

• +IGST??

Service

Invoices

Fields as required by

the central

government

• Fields as required by

Center

• Fields specific to Recipient

state and Provider state,

• Rates and exemptions

Interstate &

Import

scenarios

Central tax IGST (Central + State tax)

© 2015 SAP SE or an SAP affiliate company. All rights reserved. 16 Public

SAP Solution for Services Current Scenario Vs. GST Scenario

Topic Current Set-up GST Set-up

Tax incidence • Provision of

service rules

• Point of taxation

rules

• Place of Supply rules

• Point of taxation

rules???

Credit Availment &

refunds

Service Tax <->

Service tax, BED,

SED, AED, NCCD,

CVD, ADC, Ecess,

S&HEcess

• CGST <-> CGST

• SGST<-> SGST

• IGST <-> IGST, CGST,

SGST

Returns Central (ST3) • Central for CGST

• State for SGST

• IGST??

© 2015 SAP SE or an SAP affiliate company. All rights reserved.

Thank you

Contact information:

Soumya R

Product Expert, Globalization Services, SAP Labs