q4 global talent market quarterly

TRANSCRIPT

FOURTH QUARTER | 2015

CONTENTS

3 Global Economic Situation

6 Global Labor Market Update• Americas• EMEA• APAC• Global Labor Market Spotlight• Legislative Update

12 U.S. Labor Market Overview• Current Employment Conditions• Supply and Demand• U.S. Labor Market Spotlight

16 Workforce Solutions Industry Insight• Managing SOW Talent• Land of the Free (Agent)• KGWI 2015: Work-Life Design• The Talent Project

FOURTH QUARTER | 2015

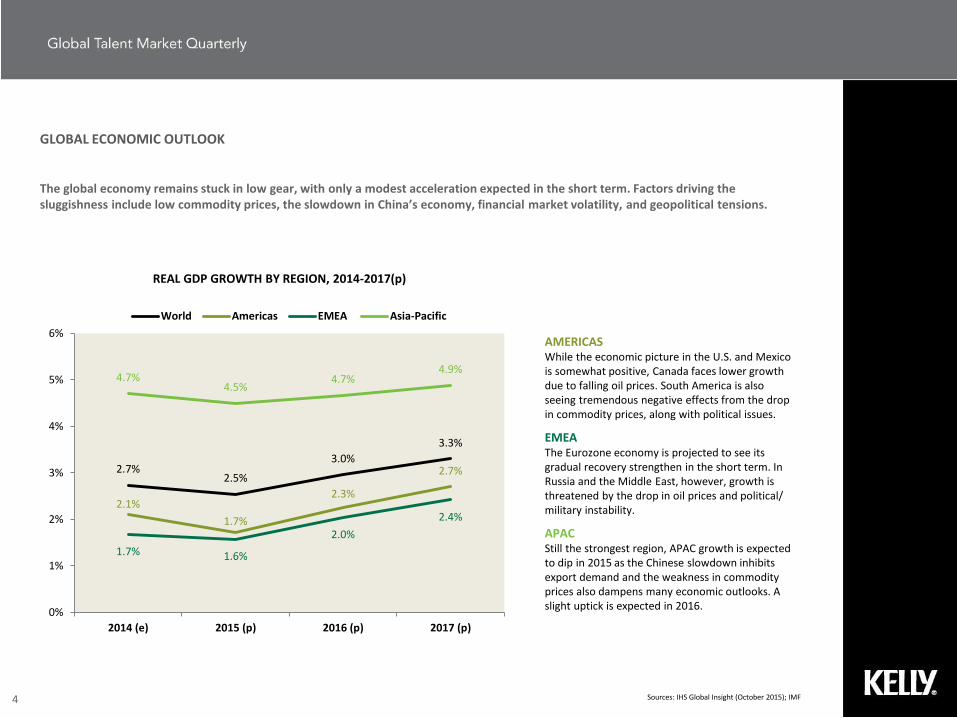

GLOBAL ECONOMIC OUTLOOK

The global economy remains stuck in low gear, with only a modest acceleration expected in the short term. Factors driving thesluggishness include low commodity prices, the slowdown in China’s economy, financial market volatility, and geopolitical tensions.

Sources: IHS Global Insight (October 2015); IMF4

AMERICASWhile the economic picture in the U.S. and Mexico is somewhat positive, Canada faces lower growth due to falling oil prices. South America is also seeing tremendous negative effects from the drop in commodity prices, along with political issues.

EMEAThe Eurozone economy is projected to see its gradual recovery strengthen in the short term. In Russia and the Middle East, however, growth is threatened by the drop in oil prices and political/ military instability.

APACStill the strongest region, APAC growth is expected to dip in 2015 as the Chinese slowdown inhibits export demand and the weakness in commodity prices also dampens many economic outlooks. A slight uptick is expected in 2016.

2.7%2.5%

3.0%

3.3%

2.1%

1.7%

2.3%

2.7%

1.7% 1.6%

2.0%

2.4%

4.7%4.5%

4.7%4.9%

0%

1%

2%

3%

4%

5%

6%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

REAL GDP GROWTH BY REGION, 2014-2017(p)

World Americas EMEA Asia-Pacific

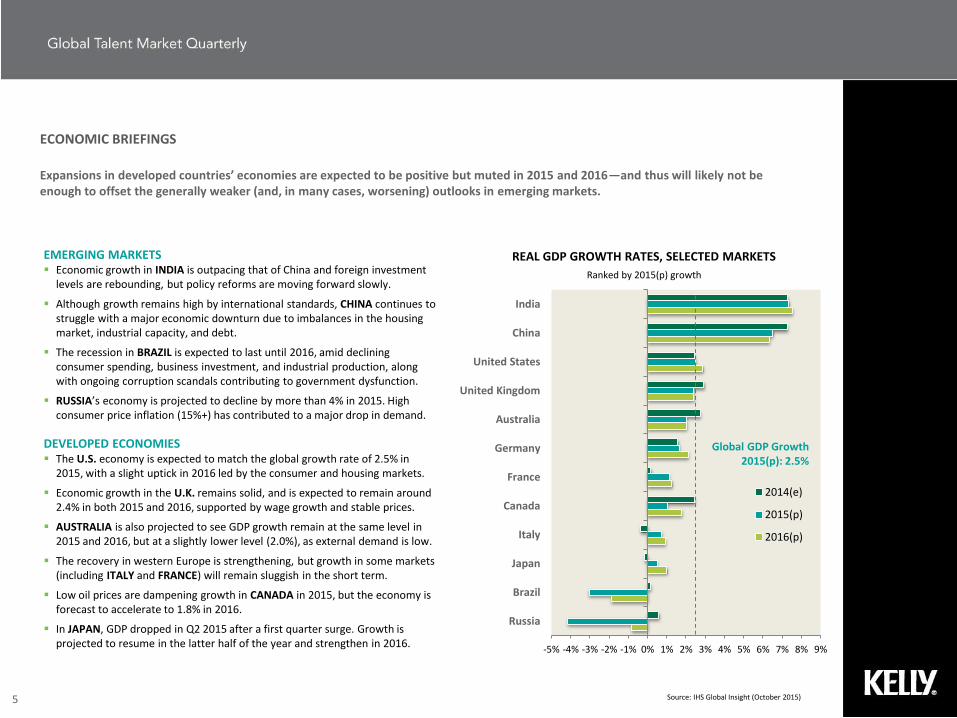

ECONOMIC BRIEFINGS

Expansions in developed countries’ economies are expected to be positive but muted in 2015 and 2016—and thus will likely not be enough to offset the generally weaker (and, in many cases, worsening) outlooks in emerging markets.

-5% -4% -3% -2% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Russia

Brazil

Japan

Italy

Canada

France

Germany

Australia

United Kingdom

United States

China

India

REAL GDP GROWTH RATES, SELECTED MARKETS

Ranked by 2015(p) growth

2014(e)

2015(p)

2016(p)

5

Global GDP Growth2015(p): 2.5%

Source: IHS Global Insight (October 2015)

EMERGING MARKETS Economic growth in INDIA is outpacing that of China and foreign investment

levels are rebounding, but policy reforms are moving forward slowly.

Although growth remains high by international standards, CHINA continues to struggle with a major economic downturn due to imbalances in the housing market, industrial capacity, and debt.

The recession in BRAZIL is expected to last until 2016, amid declining consumer spending, business investment, and industrial production, along with ongoing corruption scandals contributing to government dysfunction.

RUSSIA’s economy is projected to decline by more than 4% in 2015. High consumer price inflation (15%+) has contributed to a major drop in demand.

DEVELOPED ECONOMIES The U.S. economy is expected to match the global growth rate of 2.5% in

2015, with a slight uptick in 2016 led by the consumer and housing markets.

Economic growth in the U.K. remains solid, and is expected to remain around 2.4% in both 2015 and 2016, supported by wage growth and stable prices.

AUSTRALIA is also projected to see GDP growth remain at the same level in 2015 and 2016, but at a slightly lower level (2.0%), as external demand is low.

The recovery in western Europe is strengthening, but growth in some markets (including ITALY and FRANCE) will remain sluggish in the short term.

Low oil prices are dampening growth in CANADA in 2015, but the economy is forecast to accelerate to 1.8% in 2016.

In JAPAN, GDP dropped in Q2 2015 after a first quarter surge. Growth is projected to resume in the latter half of the year and strengthen in 2016.

FOURTH QUARTER | 2015

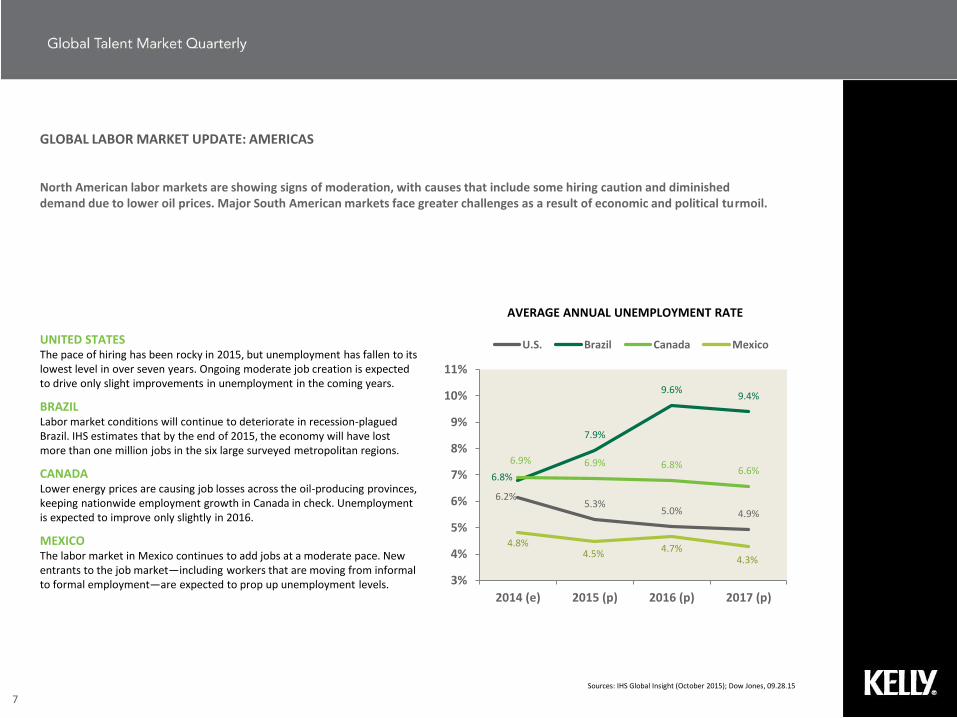

GLOBAL LABOR MARKET UPDATE: AMERICAS

North American labor markets are showing signs of moderation, with causes that include some hiring caution and diminished demand due to lower oil prices. Major South American markets face greater challenges as a result of economic and political turmoil.

Sources: IHS Global Insight (October 2015); Dow Jones, 09.28.15

7

UNITED STATESThe pace of hiring has been rocky in 2015, but unemployment has fallen to its lowest level in over seven years. Ongoing moderate job creation is expected to drive only slight improvements in unemployment in the coming years.

BRAZILLabor market conditions will continue to deteriorate in recession-plagued Brazil. IHS estimates that by the end of 2015, the economy will have lost more than one million jobs in the six large surveyed metropolitan regions.

CANADALower energy prices are causing job losses across the oil-producing provinces, keeping nationwide employment growth in Canada in check. Unemployment is expected to improve only slightly in 2016.

MEXICOThe labor market in Mexico continues to add jobs at a moderate pace. New entrants to the job market—including workers that are moving from informal to formal employment—are expected to prop up unemployment levels.

6.2%5.3%

5.0% 4.9%

6.8%

7.9%

9.6%9.4%

6.9% 6.9% 6.8%6.6%

4.8%4.5%

4.7%4.3%

3%

4%

5%

6%

7%

8%

9%

10%

11%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

AVERAGE ANNUAL UNEMPLOYMENT RATE

U.S. Brazil Canada Mexico

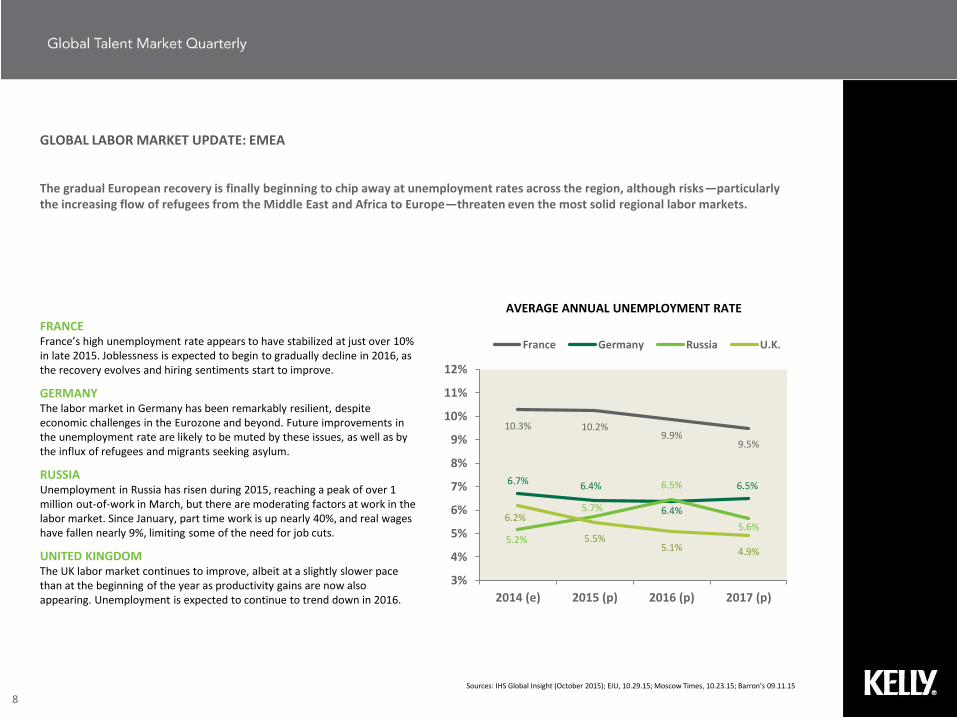

GLOBAL LABOR MARKET UPDATE: EMEA

The gradual European recovery is finally beginning to chip away at unemployment rates across the region, although risks—particularly the increasing flow of refugees from the Middle East and Africa to Europe—threaten even the most solid regional labor markets.

Sources: IHS Global Insight (October 2015); EIU, 10.29.15; Moscow Times, 10.23.15; Barron’s 09.11.15

8

FRANCEFrance’s high unemployment rate appears to have stabilized at just over 10% in late 2015. Joblessness is expected to begin to gradually decline in 2016, as the recovery evolves and hiring sentiments start to improve.

GERMANYThe labor market in Germany has been remarkably resilient, despite economic challenges in the Eurozone and beyond. Future improvements in the unemployment rate are likely to be muted by these issues, as well as by the influx of refugees and migrants seeking asylum.

RUSSIAUnemployment in Russia has risen during 2015, reaching a peak of over 1 million out-of-work in March, but there are moderating factors at work in the labor market. Since January, part time work is up nearly 40%, and real wages have fallen nearly 9%, limiting some of the need for job cuts.

UNITED KINGDOMThe UK labor market continues to improve, albeit at a slightly slower pace than at the beginning of the year as productivity gains are now also appearing. Unemployment is expected to continue to trend down in 2016.

10.3% 10.2%9.9%

9.5%

6.7% 6.4%

6.4%

6.5%

5.2%

5.7%

6.5%

5.6%6.2%

5.5%5.1% 4.9%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

AVERAGE ANNUAL UNEMPLOYMENT RATE

France Germany Russia U.K.

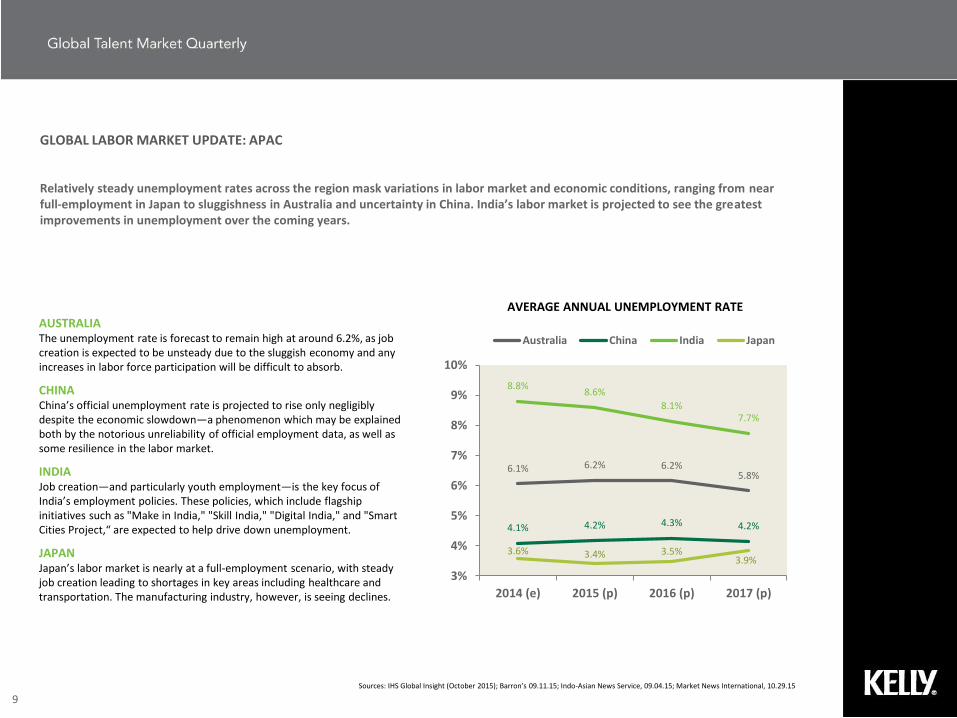

GLOBAL LABOR MARKET UPDATE: APAC

Relatively steady unemployment rates across the region mask variations in labor market and economic conditions, ranging from near full-employment in Japan to sluggishness in Australia and uncertainty in China. India’s labor market is projected to see the greatest improvements in unemployment over the coming years.

Sources: IHS Global Insight (October 2015); Barron’s 09.11.15; Indo-Asian News Service, 09.04.15; Market News International, 10.29.15

9

AUSTRALIAThe unemployment rate is forecast to remain high at around 6.2%, as job creation is expected to be unsteady due to the sluggish economy and any increases in labor force participation will be difficult to absorb.

CHINAChina’s official unemployment rate is projected to rise only negligibly despite the economic slowdown—a phenomenon which may be explained both by the notorious unreliability of official employment data, as well as some resilience in the labor market.

INDIAJob creation—and particularly youth employment—is the key focus of India’s employment policies. These policies, which include flagship initiatives such as "Make in India," "Skill India," "Digital India," and "Smart Cities Project,“ are expected to help drive down unemployment.

JAPANJapan’s labor market is nearly at a full-employment scenario, with steady job creation leading to shortages in key areas including healthcare and transportation. The manufacturing industry, however, is seeing declines.

6.1% 6.2% 6.2%5.8%

4.1% 4.2% 4.3% 4.2%

8.8%8.6%

8.1%7.7%

3.6% 3.4% 3.5%3.9%

3%

4%

5%

6%

7%

8%

9%

10%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

AVERAGE ANNUAL UNEMPLOYMENT RATE

Australia China India Japan

LABOR MARKET SPOTLIGHT: LABOR MISMATCHES

Source: The causes and consequences of field-of-study mismatch, OECD Working Papers, 2015

10

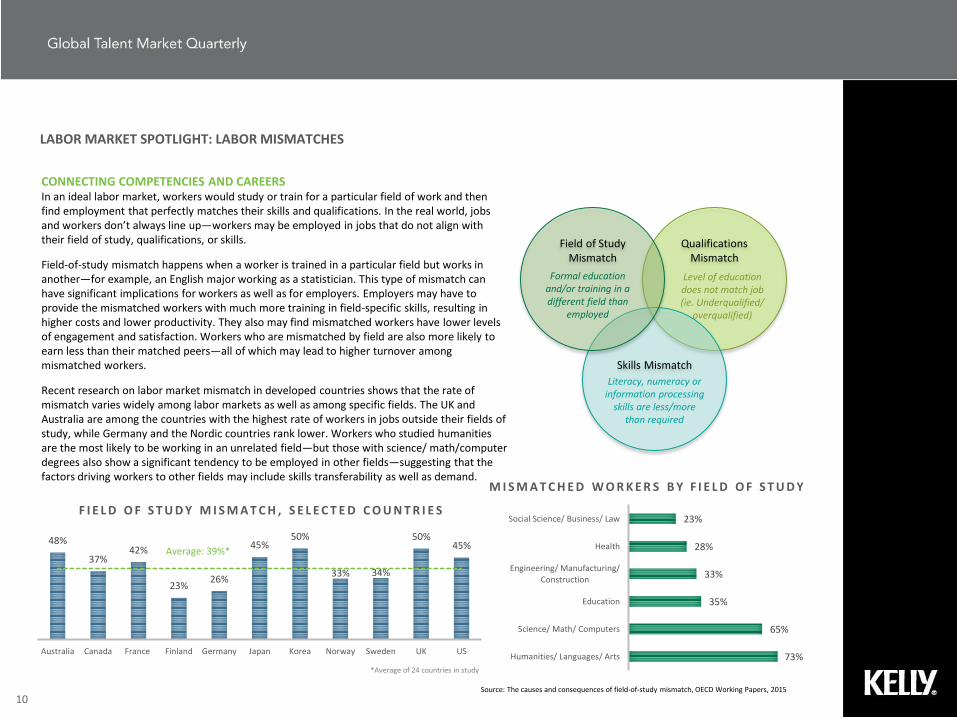

CONNECTING COMPETENCIES AND CAREERSIn an ideal labor market, workers would study or train for a particular field of work and then find employment that perfectly matches their skills and qualifications. In the real world, jobs and workers don’t always line up—workers may be employed in jobs that do not align with their field of study, qualifications, or skills.

Field-of-study mismatch happens when a worker is trained in a particular field but works in another—for example, an English major working as a statistician. This type of mismatch can have significant implications for workers as well as for employers. Employers may have to provide the mismatched workers with much more training in field-specific skills, resulting in higher costs and lower productivity. They also may find mismatched workers have lower levels of engagement and satisfaction. Workers who are mismatched by field are also more likely to earn less than their matched peers—all of which may lead to higher turnover among mismatched workers.

Recent research on labor market mismatch in developed countries shows that the rate of mismatch varies widely among labor markets as well as among specific fields. The UK and Australia are among the countries with the highest rate of workers in jobs outside their fields of study, while Germany and the Nordic countries rank lower. Workers who studied humanities are the most likely to be working in an unrelated field—but those with science/ math/computer degrees also show a significant tendency to be employed in other fields—suggesting that the factors driving workers to other fields may include skills transferability as well as demand.

Qualifications Mismatch

Skills Mismatch

Field of Study Mismatch

Level of education does not match job (ie. Underqualified/

overqualified)

Literacy, numeracy or information processing

skills are less/more than required

Formal education and/or training in a different field than

employed

48%

37%42%

23%26%

45%50%

33% 34%

50%45%

Australia Canada France Finland Germany Japan Korea Norway Sweden UK US

F I E L D O F S T U D Y M I S M A T C H , S E L E C T E D C O U N T R I E S

Average: 39%*

*Average of 24 countries in study

73%

65%

35%

33%

28%

23%

Humanities/ Languages/ Arts

Science/ Math/ Computers

Education

Engineering/ Manufacturing/Construction

Health

Social Science/ Business/ Law

M I S M A T C H E D W O R K E R S B Y F I E L D O F S T U D Y

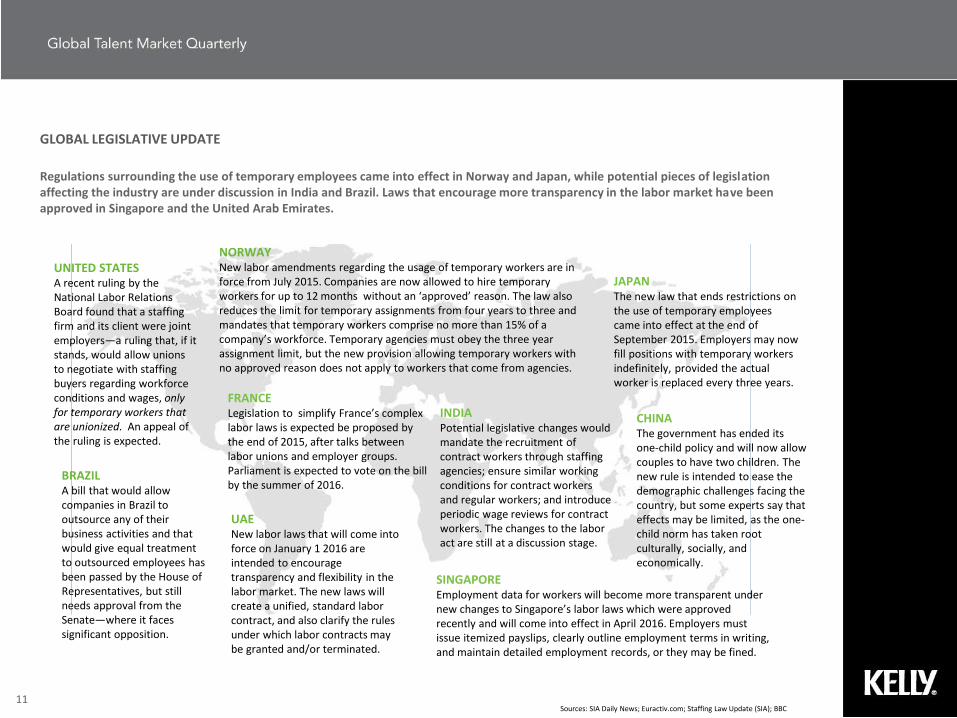

GLOBAL LEGISLATIVE UPDATE

Regulations surrounding the use of temporary employees came into effect in Norway and Japan, while potential pieces of legislation affecting the industry are under discussion in India and Brazil. Laws that encourage more transparency in the labor market have been approved in Singapore and the United Arab Emirates.

Sources: SIA Daily News; Euractiv.com; Staffing Law Update (SIA); BBC 11

UNITED STATESA recent ruling by the National Labor Relations Board found that a staffing firm and its client were joint employers—a ruling that, if it stands, would allow unions to negotiate with staffing buyers regarding workforce conditions and wages, only for temporary workers that are unionized. An appeal of the ruling is expected.

UAENew labor laws that will come into force on January 1 2016 are intended to encourage transparency and flexibility in the labor market. The new laws will create a unified, standard labor contract, and also clarify the rules under which labor contracts may be granted and/or terminated.

FRANCELegislation to simplify France’s complex labor laws is expected be proposed by the end of 2015, after talks between labor unions and employer groups. Parliament is expected to vote on the bill by the summer of 2016.

JAPANThe new law that ends restrictions on the use of temporary employees came into effect at the end of September 2015. Employers may now fill positions with temporary workers indefinitely, provided the actual worker is replaced every three years.

INDIAPotential legislative changes would mandate the recruitment of contract workers through staffing agencies; ensure similar working conditions for contract workers and regular workers; and introduce periodic wage reviews for contract workers. The changes to the labor act are still at a discussion stage.

SINGAPOREEmployment data for workers will become more transparent under new changes to Singapore’s labor laws which were approved recently and will come into effect in April 2016. Employers must issue itemized payslips, clearly outline employment terms in writing, and maintain detailed employment records, or they may be fined.

BRAZILA bill that would allow companies in Brazil to outsource any of their business activities and that would give equal treatment to outsourced employees has been passed by the House of Representatives, but still needs approval from the Senate—where it faces significant opposition.

NORWAYNew labor amendments regarding the usage of temporary workers are in force from July 2015. Companies are now allowed to hire temporary workers for up to 12 months without an ‘approved’ reason. The law also reduces the limit for temporary assignments from four years to three and mandates that temporary workers comprise no more than 15% of a company’s workforce. Temporary agencies must obey the three year assignment limit, but the new provision allowing temporary workers with no approved reason does not apply to workers that come from agencies.

CHINAThe government has ended its one-child policy and will now allow couples to have two children. The new rule is intended to ease the demographic challenges facing the country, but some experts say that effects may be limited, as the one-child norm has taken root culturally, socially, and economically.

FOURTH QUARTER | 2015

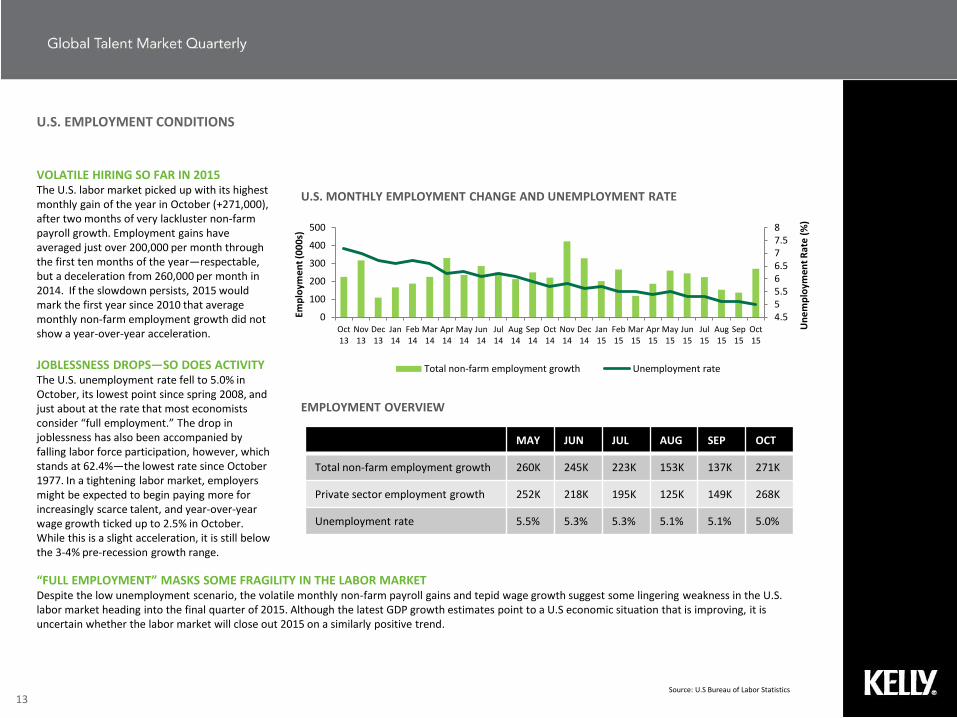

VOLATILE HIRING SO FAR IN 2015 The U.S. labor market picked up with its highest monthly gain of the year in October (+271,000), after two months of very lackluster non-farm payroll growth. Employment gains have averaged just over 200,000 per month through the first ten months of the year—respectable, but a deceleration from 260,000 per month in 2014. If the slowdown persists, 2015 would mark the first year since 2010 that average monthly non-farm employment growth did not show a year-over-year acceleration.

JOBLESSNESS DROPS—SO DOES ACTIVITYThe U.S. unemployment rate fell to 5.0% in October, its lowest point since spring 2008, and just about at the rate that most economists consider “full employment.” The drop in joblessness has also been accompanied by falling labor force participation, however, which stands at 62.4%—the lowest rate since October 1977. In a tightening labor market, employers might be expected to begin paying more for increasingly scarce talent, and year-over-year wage growth ticked up to 2.5% in October. While this is a slight acceleration, it is still below the 3-4% pre-recession growth range.

U.S. EMPLOYMENT CONDITIONS

EMPLOYMENT OVERVIEW

13Source: U.S Bureau of Labor Statistics

U.S. MONTHLY EMPLOYMENT CHANGE AND UNEMPLOYMENT RATE

“FULL EMPLOYMENT” MASKS SOME FRAGILITY IN THE LABOR MARKET Despite the low unemployment scenario, the volatile monthly non-farm payroll gains and tepid wage growth suggest some lingering weakness in the U.S. labor market heading into the final quarter of 2015. Although the latest GDP growth estimates point to a U.S economic situation that is improving, it is uncertain whether the labor market will close out 2015 on a similarly positive trend.

4.555.566.577.58

0

100

200

300

400

500

Oct13

Nov13

Dec13

Jan14

Feb14

Mar14

Apr14

May14

Jun14

Jul14

Aug14

Sep14

Oct14

Nov14

Dec14

Jan15

Feb15

Mar15

Apr15

May15

Jun15

Jul15

Aug15

Sep15

Oct15

Un

em

plo

ymen

t R

ate

(%

)

Emp

loym

en

t (0

00

s)

Total non-farm employment growth Unemployment rate

MAY JUN JUL AUG SEP OCT

Total non-farm employment growth 260K 245K 223K 153K 137K 271K

Private sector employment growth 252K 218K 195K 125K 149K 268K

Unemployment rate 5.5% 5.3% 5.3% 5.1% 5.1% 5.0%

U.S. LABOR MARKET: SUPPLY AND DEMAND

14

U.S. MONTHLY LABOR DEMAND VS. LABOR SUPPLY

Sources: Conference Board Help Wanted OnLine, Bureau of Labor Statistics

Un

em

plo

yed

Wo

rke

rs(i

n t

ho

usa

nd

s)

On

line

Jo

b A

ds

(in

th

ou

san

ds)

GAP BETWEEN HELP WANTED ADS AND AVAILABLE WORKERS NARROWINGAlthough the demand for workers in the U.S., as measured by the number of online job advertisements, dipped slightly in September 2015, the labor market continues to tighten. The supply/ demand ratio, or the number of unemployed workers to online advertised vacancies, has fallen below 1.5. There are around 2.6 million more unemployed workers than job ads currently, down from a gap of 4.2 million in September 2014.

HIGHER COMPETITION FOR JOBS IN THE WEST, PROFESSIONAL OCCUPATIONSNine metropolitan areas—only two of which are on the east coast—have supply/demand ratios below 1 (that is, there are more job ads than unemployed workers). Among the ten largest occupational areas, six fields—primarily those needing higher skills/education—have supply/demand ratios below 1.

0

2000

4000

6000

8000

10000

12000

14000

0

2000

4000

6000

8000

10000

12000

14000

Jan

12

Ap

r 1

2

Jul 1

2

Oct

12

Jan

13

Ap

r 1

3

Jul 1

3

Oct

13

Jan

14

Ap

r 1

4

Jul 1

4

Oct

14

Jan

15

Ap

r 1

5

Jul 1

5

# of Unemployed Workers # of Online Job Ads

“Labor demand in 2015 started with a very strong first quarter, followed by losses in the second quarter and an essentially flat third quarter, leaving the average monthly increases in 2015 at a modest 18,000 per month. While the number of ads flattened in recent months, it remains at a very high level, suggesting a strong labor demand.”

— Gad Levanon, Director of Macroeconomics and Labor Markets, The Conference Board

Lowest Supply/Demand Ratios: Metro Area/ Occupation

Salt Lake CityAustinSan JoseDenverMinneapolis-St PaulSan FranciscoBostonWashington DCSeattle-Tacoma

0.610.750.760.780.790.850.880.920.93

Computer & mathematicalHealthcare practitioners & technical Architecture & engineeringManagementBusiness & financial operationsInstallation, maintenance, and repair

0.220.23

0.400.690.700.70

U.S. LABOR MARKET SPOTLIGHT: LABOR SUPPLY OUTLOOK

15Sources: The U.S. Labor Supply Problem: Which States are Most at Risk? The Conference Board, 2015; U.S. Census; http://www.amcharts.com/

Decline Low growth High growth

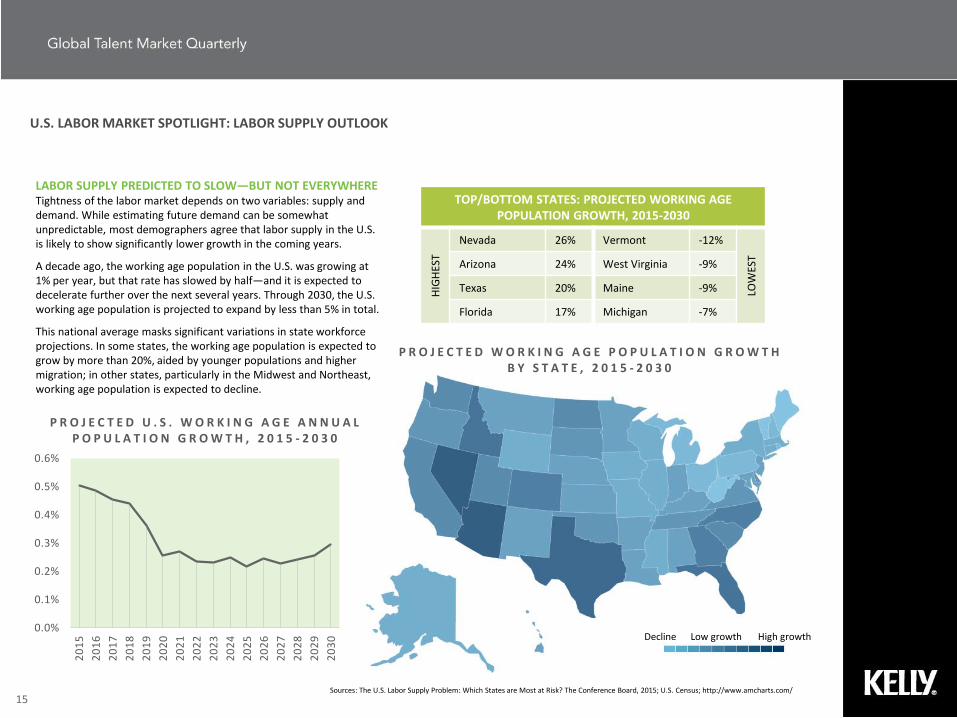

LABOR SUPPLY PREDICTED TO SLOW—BUT NOT EVERYWHERETightness of the labor market depends on two variables: supply and demand. While estimating future demand can be somewhat unpredictable, most demographers agree that labor supply in the U.S. is likely to show significantly lower growth in the coming years.

A decade ago, the working age population in the U.S. was growing at 1% per year, but that rate has slowed by half—and it is expected to decelerate further over the next several years. Through 2030, the U.S. working age population is projected to expand by less than 5% in total.

This national average masks significant variations in state workforce projections. In some states, the working age population is expected to grow by more than 20%, aided by younger populations and higher migration; in other states, particularly in the Midwest and Northeast, working age population is expected to decline.

P R O J E C T E D W O R K I N G A G E P O P U L A T I O N G R O W T H B Y S T A T E , 2 0 1 5 - 2 0 3 0

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

P R O J E C T E D U . S . W O R K I N G A G E A N N U A L P O P U L A T I O N G R O W T H , 2 0 1 5 - 2 0 3 0

TOP/BOTTOM STATES: PROJECTED WORKING AGE POPULATION GROWTH, 2015-2030

HIG

HES

T

Nevada 26% Vermont -12%

LOW

EST

Arizona 24% West Virginia -9%

Texas 20% Maine -9%

Florida 17% Michigan -7%

FOURTH QUARTER | 2015

MANAGING SOW TALENT

Taking a more holistic approach to managing the workforce means examining all categories of full-time and contingent talent. More and more companies are including statement of work (SOW) or project-based consultants as part of their talent supply chain strategies.

17Source: 2015 Contingent Buyers’ Survey, SIA

MAKING A STATEMENT (OF WORK)Unlike temporary staffing employees, who are usually engaged under an hourly billing arrangement, statement of work (SOW) consultants are project-based workers that are generally billed based on a fixed-price deliverable or when certain milestones are met. Forward-thinking companies are not only using more statement of work consultants, but they are also increasingly choosing to include these types of workers in their contingent workforce (CW) management strategies.

Research from Staffing Industry Analysts shows that the APAC region appears to be leading the way in both use of SOW consultants and in incorporating them into their CW programs: SOW workers make up a median 30% of the total contingent worker spend among APAC staffing buyers, and around two-thirds of APAC buyers say they currently manage SOW consultants in their CW programs. As for future plans, European staffing buyers show the brightest outlook for using more SOW consultants, with around two-thirds saying that they plan to increase usage over the coming decade.

EuropeNorth America APAC

25% 30%20%

PROJECT-BASED/ ST ATEMENT -O F-WO RK (SOW): MEDIAN % OF CONTINGENT SPEND

SOW CONSULTANTS INCORPORATED INTO CONTINGENT WORKFORCE PROGRAM

51% 59% 66%

39% 28%25%

North America Europe APAC

Likely to Explore within 2 Years

In Use Today

59%

66%

57%

26%

25%

27%

16%

9%

16%

APAC

Europe

North America

Increase Stay the Same Decrease

PROJECTED USAGE OF SOW CONSULTANTS OVER THE NEXT 10 YEARS

LAND OF THE FREE (AGENT)

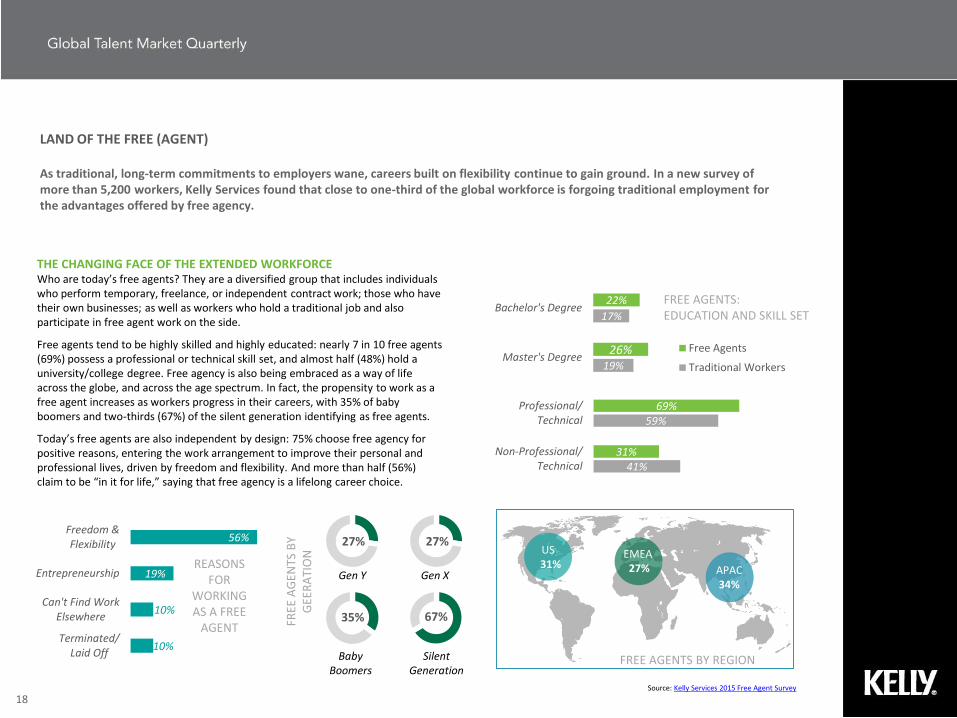

As traditional, long-term commitments to employers wane, careers built on flexibility continue to gain ground. In a new survey of more than 5,200 workers, Kelly Services found that close to one-third of the global workforce is forgoing traditional employment for the advantages offered by free agency.

18Source: Kelly Services 2015 Free Agent Survey

THE CHANGING FACE OF THE EXTENDED WORKFORCEWho are today’s free agents? They are a diversified group that includes individuals who perform temporary, freelance, or independent contract work; those who have their own businesses; as well as workers who hold a traditional job and also participate in free agent work on the side.

Free agents tend to be highly skilled and highly educated: nearly 7 in 10 free agents (69%) possess a professional or technical skill set, and almost half (48%) hold a university/college degree. Free agency is also being embraced as a way of life across the globe, and across the age spectrum. In fact, the propensity to work as a free agent increases as workers progress in their careers, with 35% of baby boomers and two-thirds (67%) of the silent generation identifying as free agents.

Today’s free agents are also independent by design: 75% choose free agency for positive reasons, entering the work arrangement to improve their personal and professional lives, driven by freedom and flexibility. And more than half (56%) claim to be “in it for life,” saying that free agency is a lifelong career choice.

22%

26%

17%

19%

Bachelor's Degree

Master's DegreeFree Agents

Traditional Workers

69%

31%

59%

41%

Professional/Technical

Non-Professional/Technical

US 31% APAC

34%

EMEA27%

FREE AGENTS BY REGION

27% 27%

Gen Y Gen X

Baby Boomers

Silent Generation

35% 67%FREE

AG

ENTS

BY

GEE

RA

TIO

NFREE AGENTS: EDUCATION AND SKILL SET

56%

19%

10%

10%

Freedom &Flexibility

Entrepreneurship

Can't Find WorkElsewhere

Terminated/Laid Off

REASONS FOR

WORKING AS A FREE

AGENT

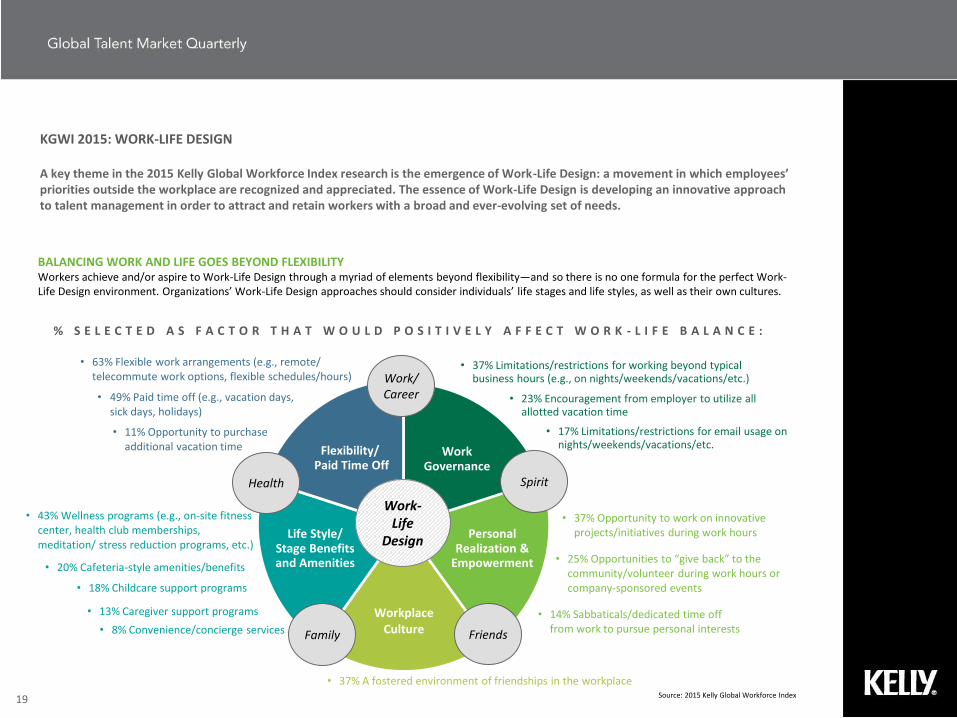

• 37% A fostered environment of friendships in the workplace

KGWI 2015: WORK-LIFE DESIGN

A key theme in the 2015 Kelly Global Workforce Index research is the emergence of Work-Life Design: a movement in which employees’ priorities outside the workplace are recognized and appreciated. The essence of Work-Life Design is developing an innovative approach to talent management in order to attract and retain workers with a broad and ever-evolving set of needs.

19 Source: 2015 Kelly Global Workforce Index

BALANCING WORK AND LIFE GOES BEYOND FLEXIBILITYWorkers achieve and/or aspire to Work-Life Design through a myriad of elements beyond flexibility―and so there is no one formula for the perfect Work-Life Design environment. Organizations’ Work-Life Design approaches should consider individuals’ life stages and life styles, as well as their own cultures.

Work Governance

Personal Realization &

Empowerment

Workplace Culture

Life Style/ Stage Benefits and Amenities

Flexibility/Paid Time Off

Work-Life

Design

Work/ Career

Spirit

Family Friends

Health

• 14% Sabbaticals/dedicated time off from work to pursue personal interests

• 63% Flexible work arrangements (e.g., remote/ telecommute work options, flexible schedules/hours)

• 37% Limitations/restrictions for working beyond typical business hours (e.g., on nights/weekends/vacations/etc.)

• 37% Opportunity to work on innovative projects/initiatives during work hours

• 43% Wellness programs (e.g., on-site fitness center, health club memberships, meditation/ stress reduction programs, etc.)

• 23% Encouragement from employer to utilize all allotted vacation time

• 17% Limitations/restrictions for email usage on nights/weekends/vacations/etc.

• 25% Opportunities to “give back” to the community/volunteer during work hours or company-sponsored events

% S E L E C T E D A S F A C T O R T H A T W O U L D P O S I T I V E L Y A F F E C T W O R K - L I F E B A L A N C E :

• 18% Childcare support programs

• 49% Paid time off (e.g., vacation days, sick days, holidays)

• 13% Caregiver support programs

• 8% Convenience/concierge services

• 20% Cafeteria-style amenities/benefits

• 11% Opportunity to purchase additional vacation time

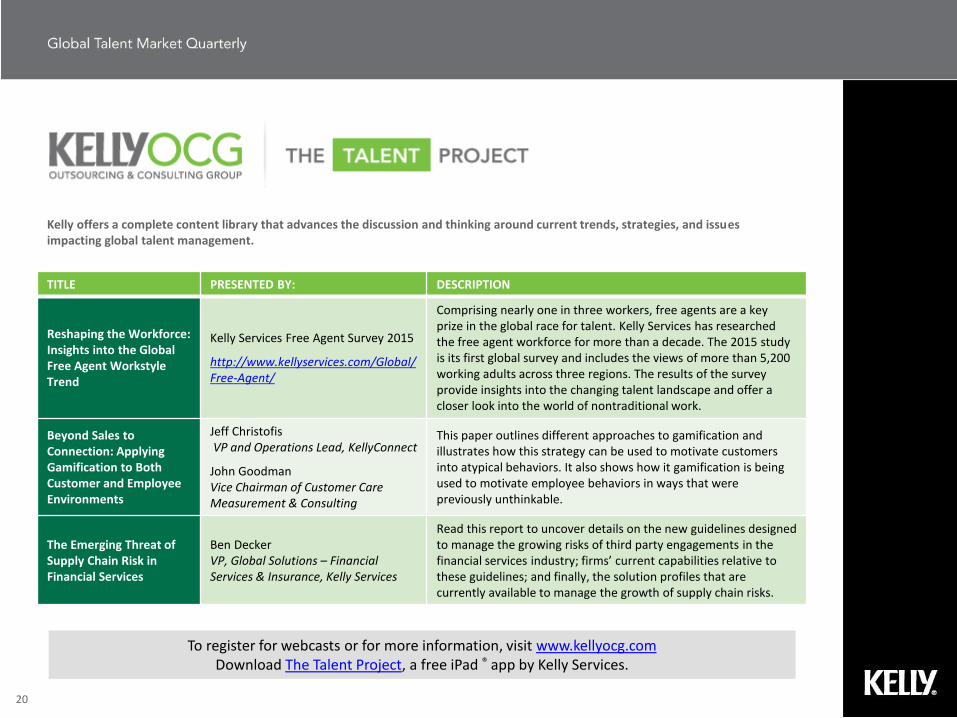

Kelly offers a complete content library that advances the discussion and thinking around current trends, strategies, and issues impacting global talent management.

To register for webcasts or for more information, visit www.kellyocg.comDownload The Talent Project, a free iPad ® app by Kelly Services.

TITLE PRESENTED BY: DESCRIPTION

Reshaping the Workforce:Insights into the Global Free Agent WorkstyleTrend

Kelly Services Free Agent Survey 2015

http://www.kellyservices.com/Global/Free-Agent/

Comprising nearly one in three workers, free agents are a key prize in the global race for talent. Kelly Services has researched the free agent workforce for more than a decade. The 2015 study is its first global survey and includes the views of more than 5,200 working adults across three regions. The results of the survey provide insights into the changing talent landscape and offer a closer look into the world of nontraditional work.

Beyond Sales to Connection: Applying Gamification to Both Customer and Employee Environments

Jeff ChristofisVP and Operations Lead, KellyConnect

John GoodmanVice Chairman of Customer Care Measurement & Consulting

This paper outlines different approaches to gamification and illustrates how this strategy can be used to motivate customers into atypical behaviors. It also shows how it gamification is being used to motivate employee behaviors in ways that were previously unthinkable.

The Emerging Threat of Supply Chain Risk in Financial Services

Ben DeckerVP, Global Solutions – Financial Services & Insurance, Kelly Services

Read this report to uncover details on the new guidelines designed to manage the growing risks of third party engagements in the financial services industry; firms’ current capabilities relative to these guidelines; and finally, the solution profiles that are currently available to manage the growth of supply chain risks.

20

Kelly Services Inc. makes no representation or warranty with respect to the material contained within this report.