ptak prizeindia2014 sc_next_varden_xlri_jamshedpur

TRANSCRIPT

E-Commerce Supply Chain Challenges

Team Varden

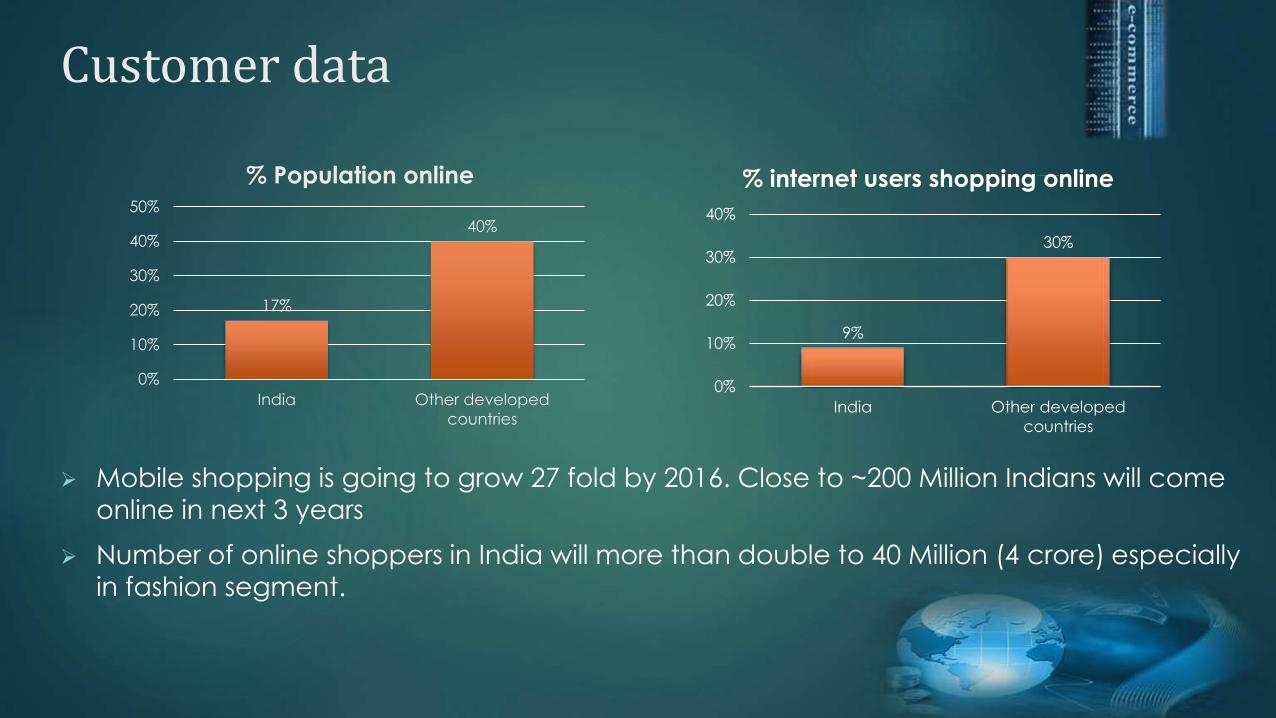

Customer data

Mobile shopping is going to grow 27 fold by 2016. Close to ~200 Million Indians will come

online in next 3 years

Number of online shoppers in India will more than double to 40 Million (4 crore) especially in fashion segment.

17%

40%

0%

10%

20%

30%

40%

50%

India Other developed

countries

% Population online

9%

30%

0%

10%

20%

30%

40%

India Other developed

countries

% internet users shopping online

243Mn (

98%)

4Mn(2%)

Offline Sales Online Sales

Mobile Shipments

555Mn(92%)

45Mn(8%)

Offline Sales Online Sales

Books

44.92Bn,

99.8%

0.08Bn( 0.02%)

Offline Sales Online Sales

Jewellery

Enough opportunity for growth

42Mn(99%)

0.5Mn(1%)

Offline Sales Online Sales

Fashion & Footwear

0

20

40

60

80

No. of websites

All figures in USD

Bottleneck in E-commerce : Logistics

Large volumes of non-uniform, irregularly shaped products in e-commerce

E-commerce logistics requires greater agility to be more responsive to customer demands

Cannot use document courier service – hassles in clearing check post, taxation issues

Express cargo logistics used for bulk loads to distributors etc – cannot provide door-to-door delivery

Fewer warehouses as compared to carrying & forwarding agents for other retail stores

Separate logistics infrastructure for various categories of goods such as foods & beverages,

departmental stores, healthcare and office equipment

Customer order point needs to be pushed forward to reduce inventory

Strategic location choices for fulfilment centres - proximal to delivery nodes

Last mile network planning & scheduling

Challenges:

Customer not present at delivery location while delivery/Customer not answering call -

leading to revisits especially for Cash-on-Delivery (COD)

Installations for few products (electronics, home appliances etc) require skilled

manpower while delivery

The non-standardisation of postal addresses - few heavily populated parts in large

cities where even having door numbers is not good enough

More complex services such as scheduled returns, exchanges or COD

While COD is essential in nascent markets, it impacts business margins negatively

COD exposes companies to a significant amount of risk, especially when many of the

logistics and express players are franchised or heavily subcontracted

53%

37%

6%4%

0%

20%

40%

60%

80%

100%

1

Cost structure per

parcel

Collection Sorting

Line Haul Last-mile delivery

Bargaining power of

Customers Lucrative discounts offered by

e-commerce firms

Free delivery preferred by

customers on any order size

Price sensitivity is high

Less loyalty towards any site

Ability to substitute high

Difference in competitors only in

terms of delivery time and low

prices offered

Bargaining power of

suppliers Suppliers have the power to provide

must of the discounts

Have option of forward integration

Amazon uses FBA (Fulfillment by

Amazon) to get discounts from

sellers

Huge number of suppliers – need

platform to showcase their price

compatibility, discounts,

advertisements and ratings

Threat of substitutes Brick and mortar stores

Branded online stores for

customers who have less

trust in online stores

Substitute products are

cheaper and product

quality is equal or higher

Low switching cost makes

the industry price sensitive

Porter’s Five

ForcesPower of

buyers

Power of

suppliers

Threat of

substitutes

Threat of

new entrants

Internal

Rivalry

Competitive Rivalry

Many players offering similar products

Competing on price – leading to low brand loyalty

Market share is fairly constant, difficult to increase

Entry of Amazon – has already acquired half of

what Flipkart built in 6 yrs

Rate of industry growth determines rivalry

Diversity of competitors – different segments

Economies of scale difficult to achieve if a wider

customer base not present.

Porter’s Five

ForcesPower of

buyers

Power of

suppliers

Threat of

substitutes

Threat of

new entrants

Internal

Rivalry

Threat of new entrants

High price elasticity of demand - new entrants offer very low

prices to capture market share

Established and trusted Brands opening online stores

Players can enter into various segments of e commerce -

baby care, automobile service, jewellery, custom designed,

groceries, cab rentals, furniture etc

Availability of numerous investors, funding opportunities

available from advertising companies as well as sellers who

wish to gain visibility

Low initial capital investment required

Distribution channels are easy to access

Low consumer switching cost

Strategy for the next five yearsFront End

Integrated OMNI channel approach – Brick n Mortar and online shopping

Feasibility of ware house in every state – preferably nearer to shoppers destination – reduces shipping time

Discount for card users to move COD customer base to online payments - decreases last mile delivery costs

& associated risks

Peak traffic preparedness including load testing and performance benchmarking

Increase average order size by providing combo discounts

Anticipatory Shipping

Tie up for exclusive product releases

Improvement in interface – personalize websites based on previous searches

Option of Nearest alternate address (or Name of neighbour etc), where it can be delivered if customer is

not present.

Provide Realistic date of delivery on site based on availability in nearest warehouse

Delivery and fulfillment

Optimise inventory (product and location wise)

Standardising package sizes (beneficial to all in delivery chain)

Automate movements in the warehouse & packaging (eg. KIVA systems)

Strengthen own delivery network

Explore long term contracts with railways which are cheaper for interstate transport & have lower

clearing and taxation issues

Maintain strictly monitored service level agreements with 3rd party logistics who take care of last

mile delivery.

Call COD customers beforehand to ensure they will be available for delivery at respective times

Environment

Reduce use of plastic and bubble wrap in packaging.

Optimise Package sizes

Provide option on site for customers for whom paper bill is not required and reduce size of sticker

on package. (only name, address and bar code)

Strategy for the next five years

Ecommerce to BnM BnM to Ecommerce

Real estate costs Huge investment to be made.

Number of stores is difficult to match

No Additional cost

IT Infrastructure Minimal modifications to include BnM

Stores also

Investment in setting up IT system, inventory

management, customer management etc

Range of products Requirement of massive display areas

in offline stores

Wide range of products required to match the e

commerce companies

Logistics and delivery

system

Existing logistics network can be used

for catering to the offline stores

Initial investment in creating a distribution

network or partnering with 3PL. Diligence in

establishing & maintaining last mile network &

reverse logistics

Manpower training Skilled labour required for operating

the stores

Manpower to be trained in warehouse

operations and reverse logistics management

Customer service Salesmen/store operator can address

the customer grievances

Separate customer service cell has to be

created

OMNI Channel - Click to Brick Vs Brick to Click

Ecommerce to

BnM

BnM to

Ecommerce

Real estate costs

IT Infrastructure

Range of products

Logistics and

delivery system

Manpower training

Customer service

Brand equity

Brick n Mortar to Ecommerce is very

likely to succeed

IT infrastructure and skilled

manpower a one time fixed cost for

new entrants into e commerce

Will give high returns in the long run.

Logistics can be outsourced for the

initial period.

Humungous investment for e

commerce companies for going

offline

Gains in brand enhancement would

not be proportional to the

investment made

OMNI Channel - Click to Brick Vs Brick to Click

Thank you