program income: the what, when, why, how, and where of dealing with program income

TRANSCRIPT

Program Income:

The What, When, Why, How, and Where of dealing with

Program Income

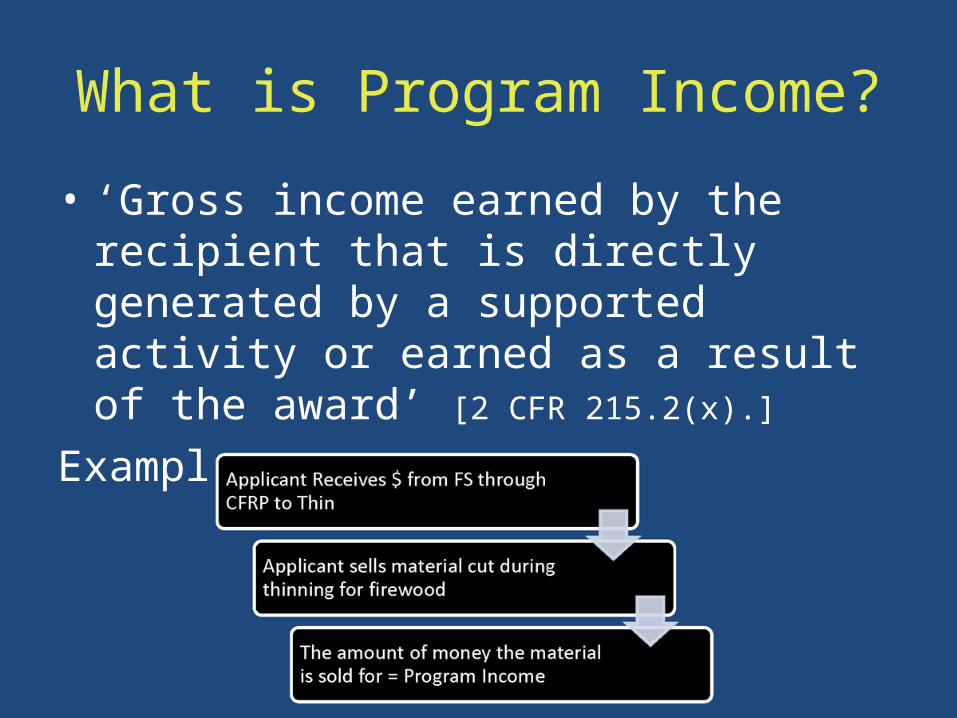

What is Program Income?

• ‘Gross income earned by the recipient that is directly generated by a supported activity or earned as a result of the award’ [2 CFR 215.2(x).]

Example:

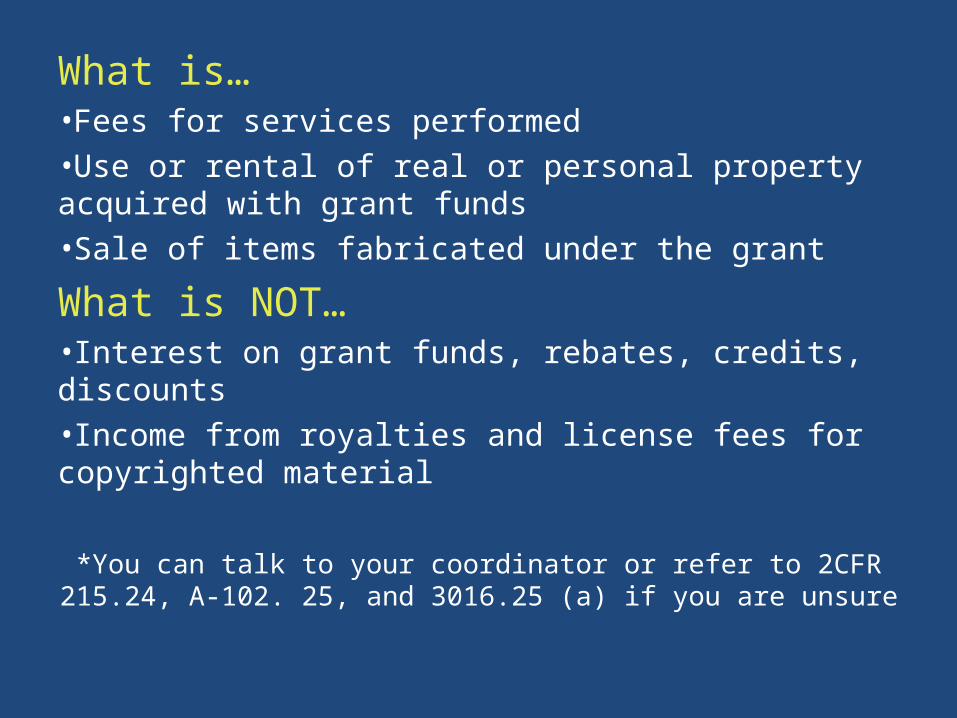

What is…•Fees for services performed•Use or rental of real or personal property acquired with grant funds•Sale of items fabricated under the grant

What is NOT…•Interest on grant funds, rebates, credits, discounts•Income from royalties and license fees for copyrighted material

*You can talk to your coordinator or refer to 2CFR 215.24, A-102. 25, and 3016.25 (a) if you are unsure

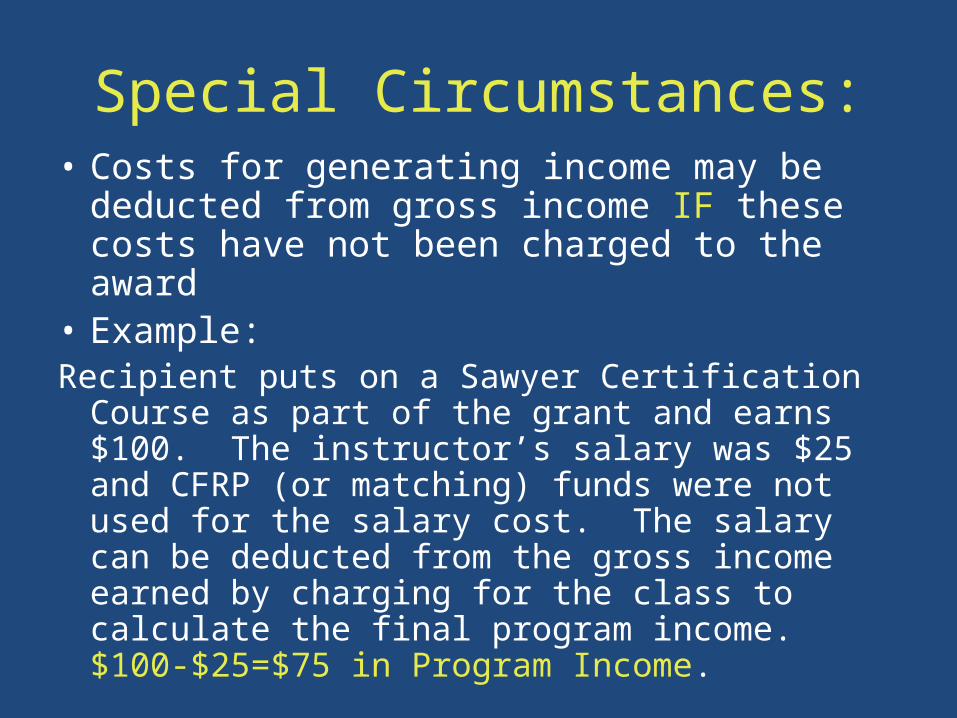

Special Circumstances:• Costs for generating income may be

deducted from gross income IF these costs have not been charged to the award

• Example:Recipient puts on a Sawyer Certification

Course as part of the grant and earns $100. The instructor’s salary was $25 and CFRP (or matching) funds were not used for the salary cost. The salary can be deducted from the gross income earned by charging for the class to calculate the final program income. $100-$25=$75 in Program Income.

When does income qualify as Program Income?

• earned during the grant period (the effective date of the award through the ending date reflected in the final financial report)

• no obligation after the grant ends [Uniform Administrative Requirements 3016.25 (a, h) & 3019.24 (e) ]

Why do you have to document Program Income?

• Under the legislation that allows agencies to award grants guidelines were created for the administration of grant funds.

• ALL agencies (not just the F.S.) must have applicants account for Program Income

• There is some discretion given to the agency to determine how Program Income will be accounted for

How does CFRP deal with Program Income?

• 3 options for dealing with Program Income under Forest Service regulations

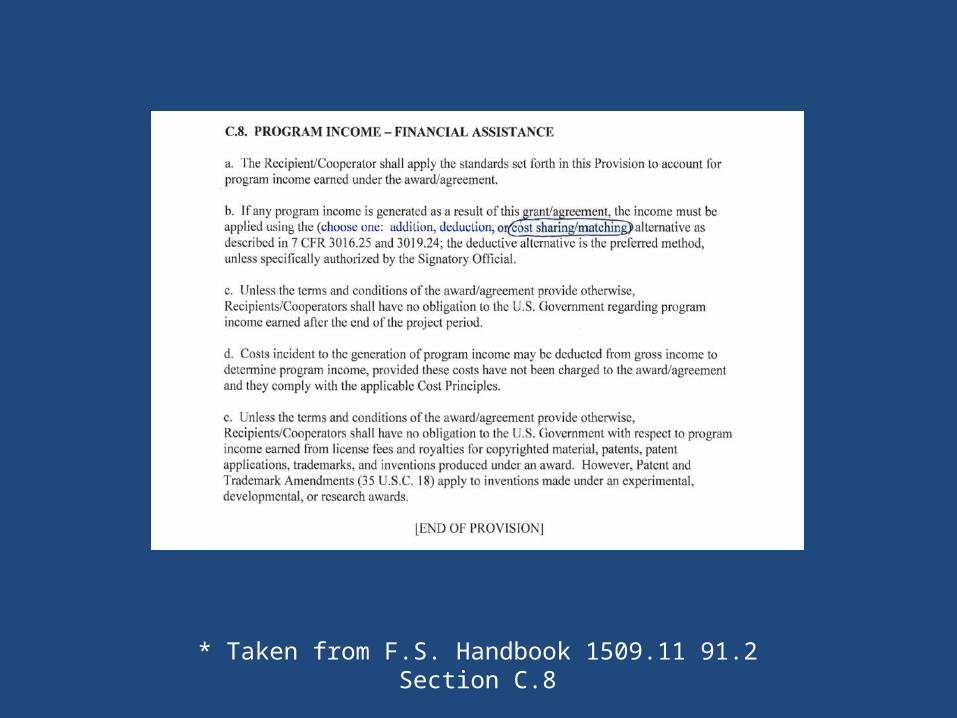

• CFRP uses the ‘Cost Sharing or Matching Alternative’

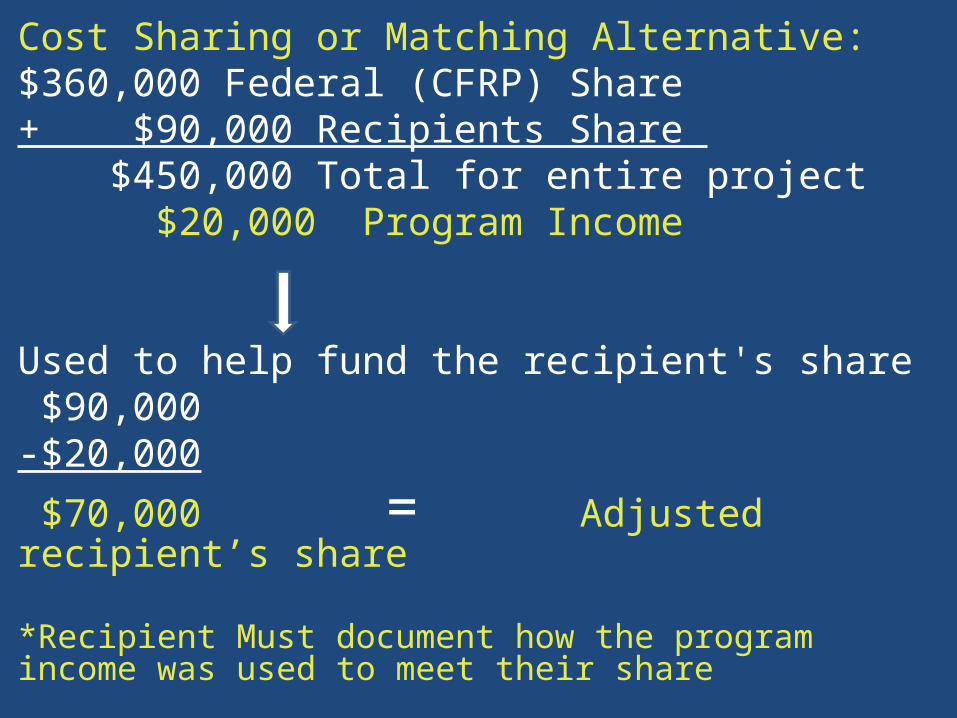

Cost Sharing or Matching Alternative:$360,000 Federal (CFRP) Share+ $90,000 Recipients Share $450,000 Total for entire project $20,000 Program Income

Used to help fund the recipient's share $90,000-$20,000

$70,000 = Adjusted recipient’s share

*Recipient Must document how the program income was used to meet their share

* Taken from F.S. Handbook 1509.11 91.2 Section C.8

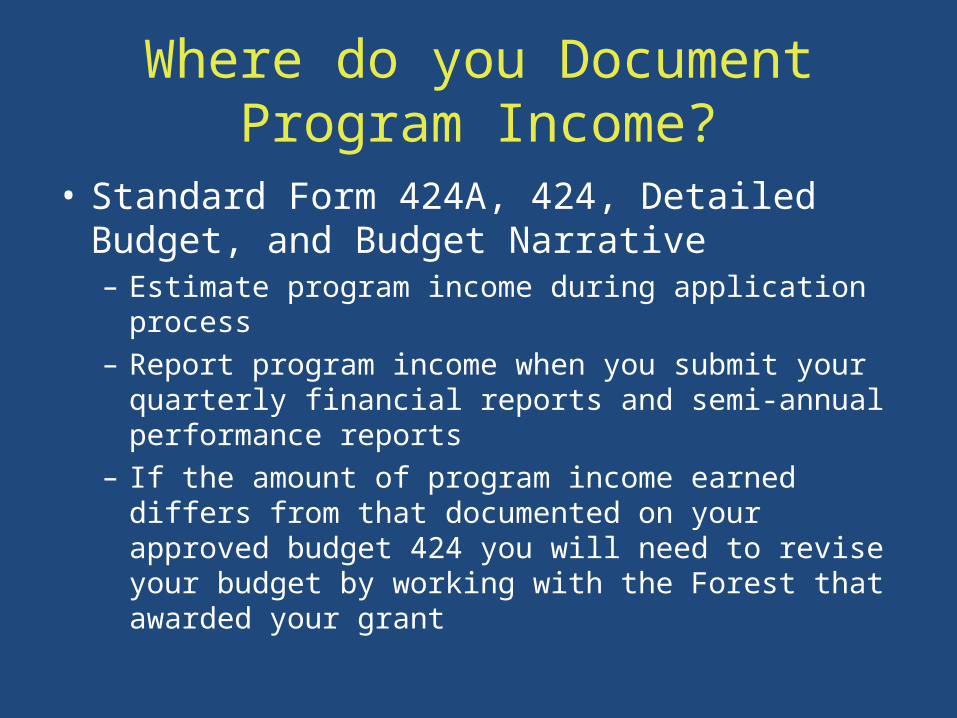

Where do you Document Program Income?

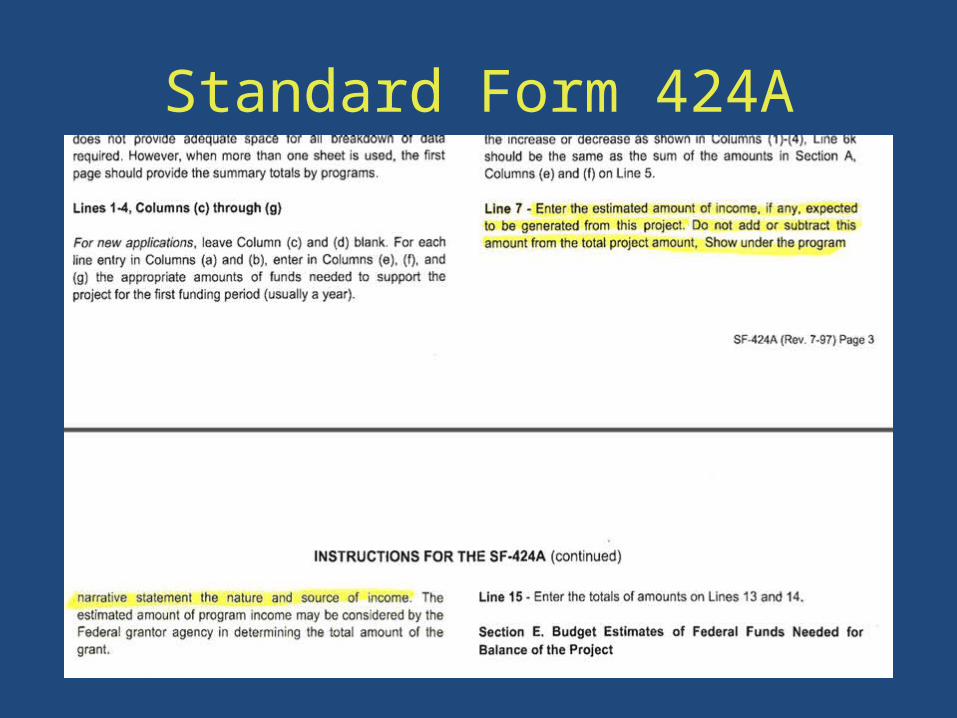

• Standard Form 424A, 424, Detailed Budget, and Budget Narrative– Estimate program income during application

process– Report program income when you submit your

quarterly financial reports and semi-annual performance reports

– If the amount of program income earned differs from that documented on your approved budget 424 you will need to revise your budget by working with the Forest that awarded your grant

Standard Form 424A

Standard Form 424 A continued

Standard Form 424

Detailed Budget and Budget Narrative

Conclusion

• Talk to the coordinator on your Forest if you have questions as you are completing the budget for your application!

• Work closely with the your coordinator if funded – keep them updated if you expect changes to your program income!

• REMEMBER: you are still responsible for the 20% match even if your program income is less than expected!